CPF Housing Grant for Resale Singapore 2026: Complete Guide to EHG, PHG and Step-Up Grant

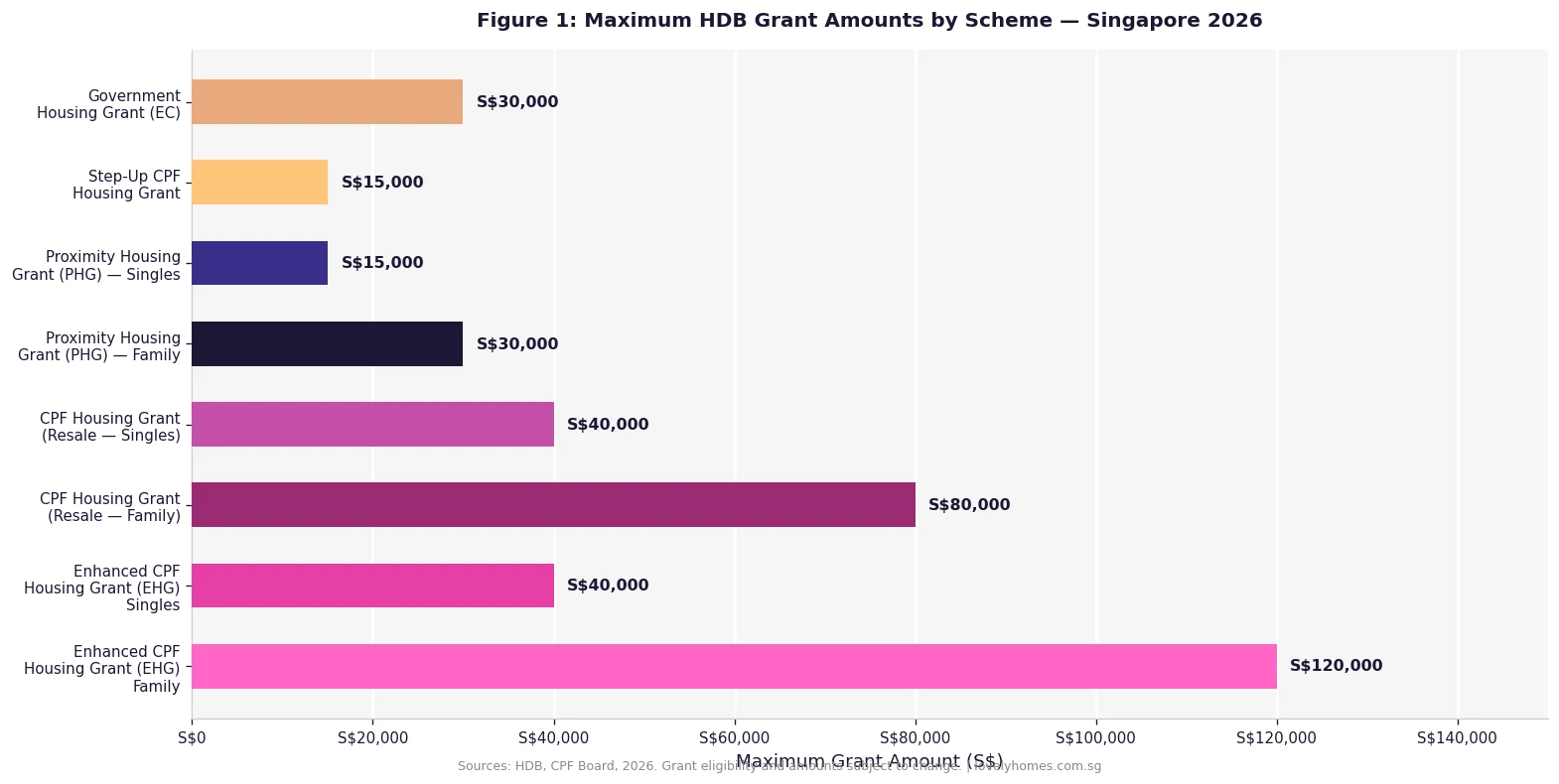

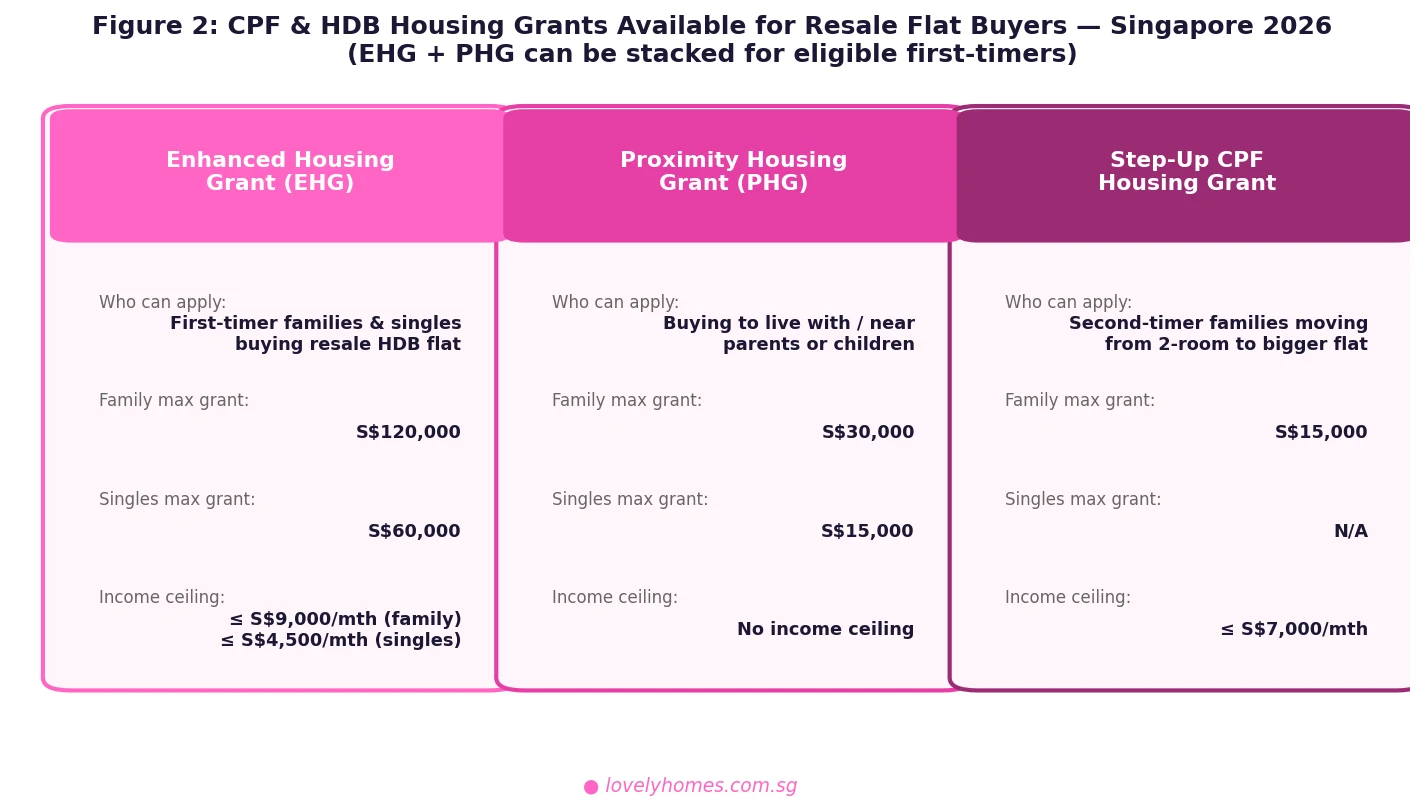

- First-timer families can receive up to S$120,000 via the Enhanced Housing Grant (EHG), based on monthly household income.

- First-timer singles receive up to S$60,000 EHG (income ceiling S$4,500/mth).

- The Proximity Housing Grant (PHG) adds S$20,000–S$30,000 for families buying near or with parents — no income ceiling applies.

- The Step-Up CPF Housing Grant offers S$15,000 to qualifying second-timers moving from a 2-room flat.

- EHG and PHG can be stacked, giving eligible first-timer families up to S$150,000 in combined grants.

- Grants are credited to your CPF Ordinary Account and used to offset the flat purchase; PHG cash may be disbursed after purchase.

- Apply via the HDB Resale Portal when submitting your resale application; grants are assessed at the HFE (HDB Flat Eligibility) letter stage.

- EHG carries a 5-year occupation requirement before the flat can be sold; early sale forfeits the EHG.

What Are CPF Housing Grants for Resale Flats?

When Singaporeans buy a resale HDB flat on the open market, the Government makes housing affordable through a suite of cash and CPF-based grants administered jointly by the Housing & Development Board (HDB) and the CPF Board. Unlike grants for Build-To-Order (BTO) flats — which are newer, typically cheaper, and come with their own set of schemes — resale flat grants are designed to bridge the gap between the higher open-market price and a buyer’s financing capacity.

There are three primary grants available to resale flat buyers in 2026: the Enhanced Housing Grant (EHG), the Proximity Housing Grant (PHG), and the Step-Up CPF Housing Grant. Each targets a different buyer profile. Understanding which grants apply to you, how they interact with your CPF usage and HDB loan amount, and what obligations you take on is essential before you submit an offer on any resale flat.

This guide covers every grant in detail, including income tiers, eligibility conditions, the application workflow, and a worked dollar-figure example for a first-timer couple buying a four-room resale flat in 2026.

Enhanced Housing Grant (EHG) — The Primary Resale Grant

The Enhanced Housing Grant, administered by HDB and funded through the Ministry of National Development, is the backbone of the resale grant framework. Introduced in September 2019 to replace the Additional CPF Housing Grant (AHG) and the Special CPF Housing Grant (SHG), the EHG removed the old BTO-only restrictions and extended generous support to resale buyers for the first time.

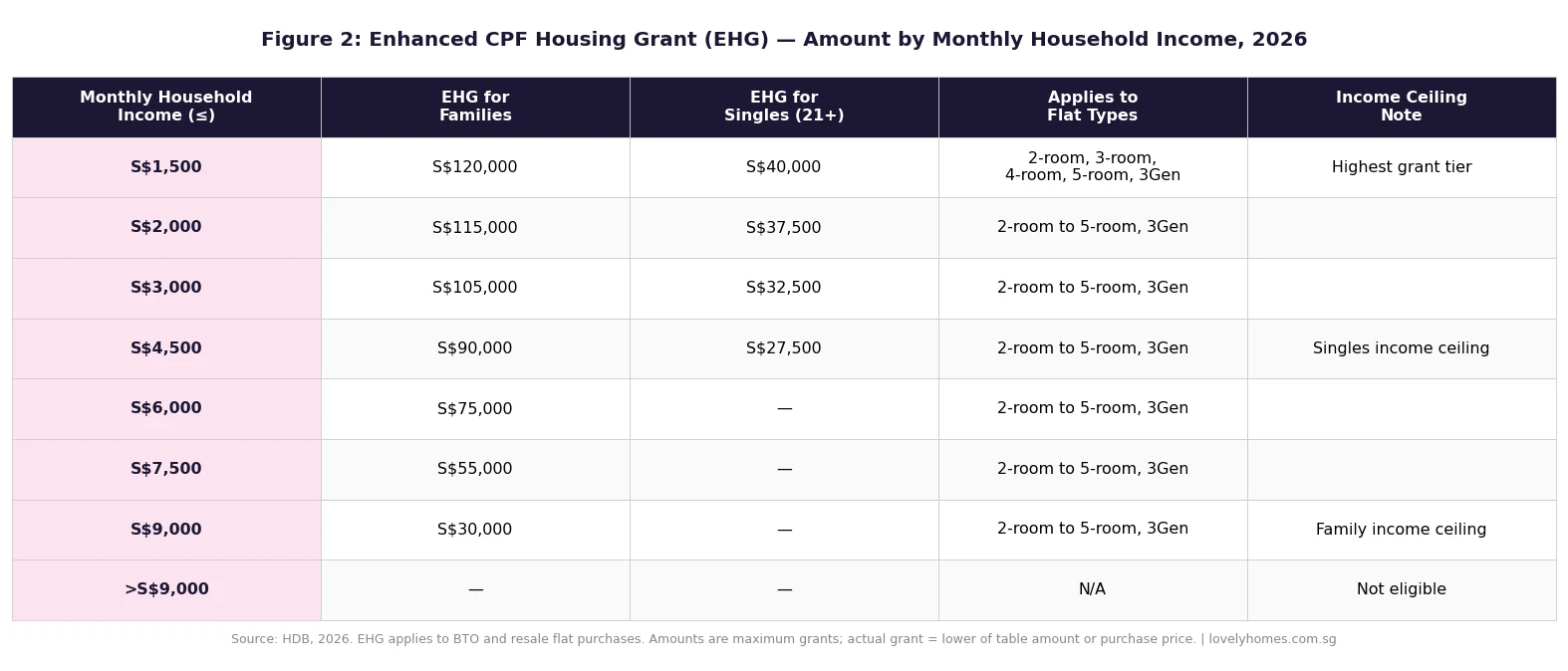

In 2026, the EHG provides between S$5,000 and S$120,000 depending on the applicant’s average monthly household income over the 12 months preceding the HFE application. The grant is means-tested across 14 income tiers: households earning S$1,500 per month or less receive the maximum S$120,000, tapering in steps to S$5,000 for households earning up to S$9,000 per month. Households above the S$9,000 ceiling do not qualify.

First-timer singles aged 35 and above qualify at half the family rate — up to S$60,000 at the same income tiers, with an income ceiling of S$4,500 per month. Singles purchasing under the Single Singapore Citizen (SSC) scheme or the Joint Singles Scheme must meet the same 5-year occupation requirement that applies to families.

To qualify for the EHG, all applicants must:

- Be a Singapore Citizen (at least one applicant must be an SC for joint purchases; co-applicant may be an SC or Singapore Permanent Resident).

- Be a first-timer — defined as never having received a housing subsidy before (whether via HDB flat ownership, an Executive Condominium, or a previous housing grant).

- Not own or have an interest in any private residential property in Singapore or overseas, and not have disposed of any private property within the 30 months before the HFE application.

- Have been continuously employed (or self-employed with CPF contributions) for the 12 consecutive months before the HFE application.

- Purchase a resale flat that has a remaining lease of at least 20 years and covers the youngest applicant to at least age 95 (lease coverage requirement).

The EHG is credited directly to the applicants’ CPF Ordinary Accounts and used to offset the purchase price. It is not paid in cash. Once granted, the EHG creates a 5-year minimum occupation period (MOP) obligation — the flat cannot be sold, rented out in full, or transferred within five years of the key collection date without forfeiting the grant and triggering HDB’s recovery action.

Proximity Housing Grant (PHG) — Buying Near or With Family

The Proximity Housing Grant, administered by HDB, supports Singapore’s strong multigenerational family values by financially incentivising buyers to live near or with their parents or children. Unlike the EHG, the PHG has no income ceiling — any eligible buyer can access it regardless of household income, making it one of the most underutilised grants in the resale market.

The PHG is structured in two tiers in 2026:

| Proximity Condition | Families (SC+SC or SC+SPR) | Singles (SC only) |

|---|---|---|

| Living WITH parents / children (same address) | S$30,000 | S$15,000 |

| Living NEAR parents / children (within 4 km) | S$20,000 | S$10,000 |

To access the higher S$30,000 tier, buyers must purchase a flat in the same block or development as their parents or children, or purchase a flat where the parent or child will be listed as an occupant at the same address. The S$20,000 tier applies when the parent or child continues to reside within a four-kilometre straight-line radius of the buyer’s flat for at least five years after the flat purchase is completed.

The PHG imposes a key ongoing obligation: the proximity condition must be maintained for a minimum of five years. If the parent or child moves beyond four kilometres within that period without a valid reason recognised by HDB (such as medical necessity), HDB may require the grant to be refunded in full. Buyers should factor this into long-term planning, particularly if parents are in the consideration age where they may eventually require elderly care facilities in different locations.

The PHG is generally credited to the buyer’s CPF OA as a housing grant offset, though HDB’s process may disburse part of it after the resale completion is registered with the Singapore Land Authority. Always confirm the exact disbursement timeline with your HDB case officer during the resale application process.

Step-Up CPF Housing Grant — For Second-Timers Moving Up

The Step-Up CPF Housing Grant is the most narrowly targeted of the three grants. It provides S$15,000 to second-timer families — those who previously received a housing subsidy, typically in the form of a 2-Room Flexi flat — who are now purchasing a larger resale flat (3-room or bigger) in a non-mature estate.

Eligibility conditions for the Step-Up Grant in 2026:

- The applicant family must include at least one SC and one SC or SPR.

- At least one applicant must have previously received a housing subsidy (i.e., is a second-timer).

- The previous flat must have been a 2-Room Flexi flat, a Studio Apartment, or a subsidised 1- or 2-room flat in a non-mature estate.

- The resale flat being purchased must be a 3-room or larger flat in a non-mature estate.

- Monthly household income must not exceed S$7,000.

The Step-Up Grant is credit to CPF OA and cannot be combined with the EHG (which is only for first-timers). However, a second-timer family purchasing near their parents may still access the PHG alongside the Step-Up Grant.

Grant Stacking — Maximum Combined Support

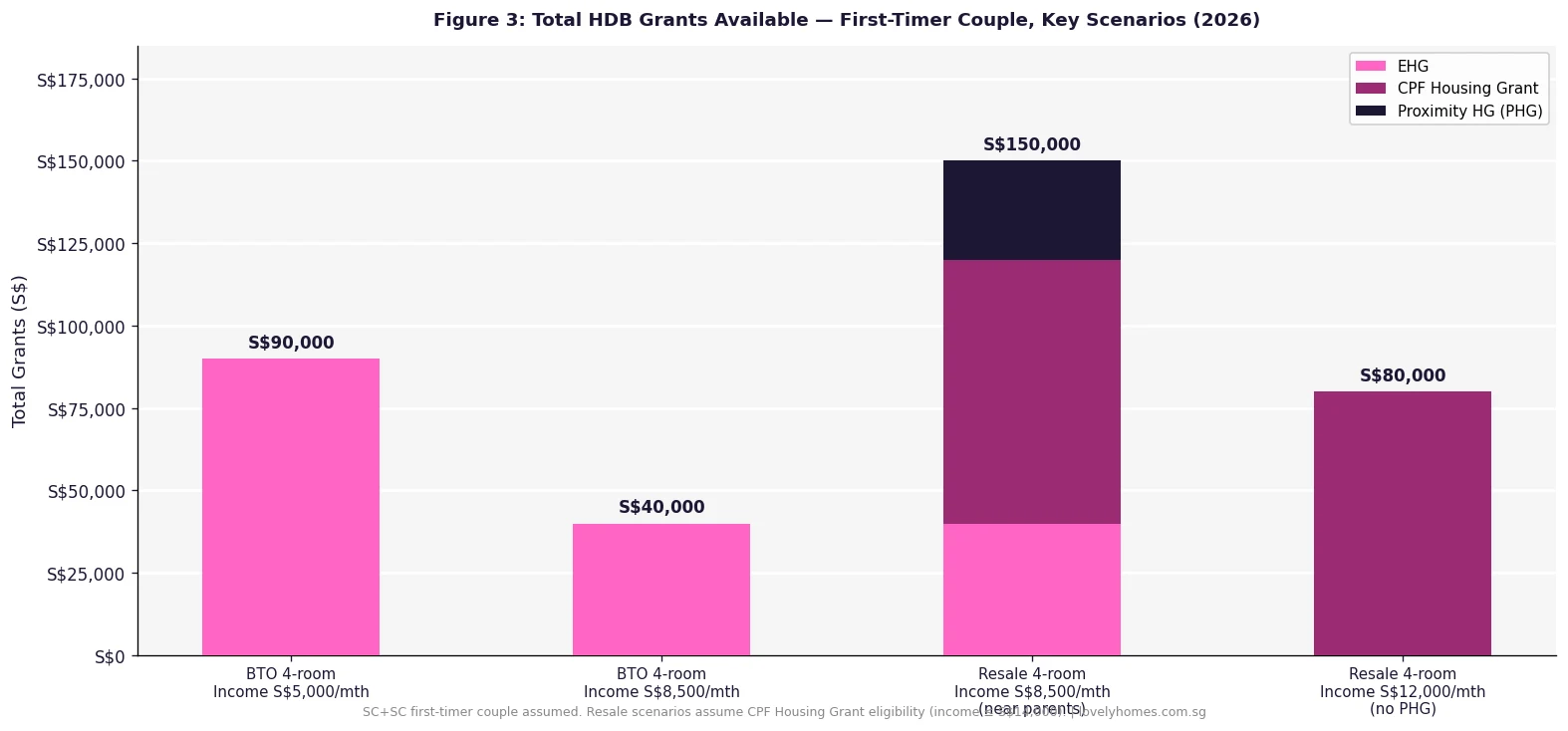

The most powerful outcome occurs when EHG and PHG are stacked by an eligible first-timer family:

| Buyer Profile | EHG | PHG | Combined Max |

|---|---|---|---|

| First-timer family, income ≤ S$1,500/mth, living with parents | S$120,000 | S$30,000 | S$150,000 |

| First-timer family, income S$7,000/mth, within 4 km of parents | S$25,000 | S$20,000 | S$45,000 |

| First-timer single, income ≤ S$4,500/mth, within 4 km of parents | Up to S$60,000 | S$10,000 | Up to S$70,000 |

| Second-timer family, income ≤ S$7,000/mth, within 4 km of parents | N/A | S$20,000 | S$35,000* |

*Includes S$15,000 Step-Up Grant + S$20,000 PHG for qualifying second-timers purchasing near parents in non-mature estates.

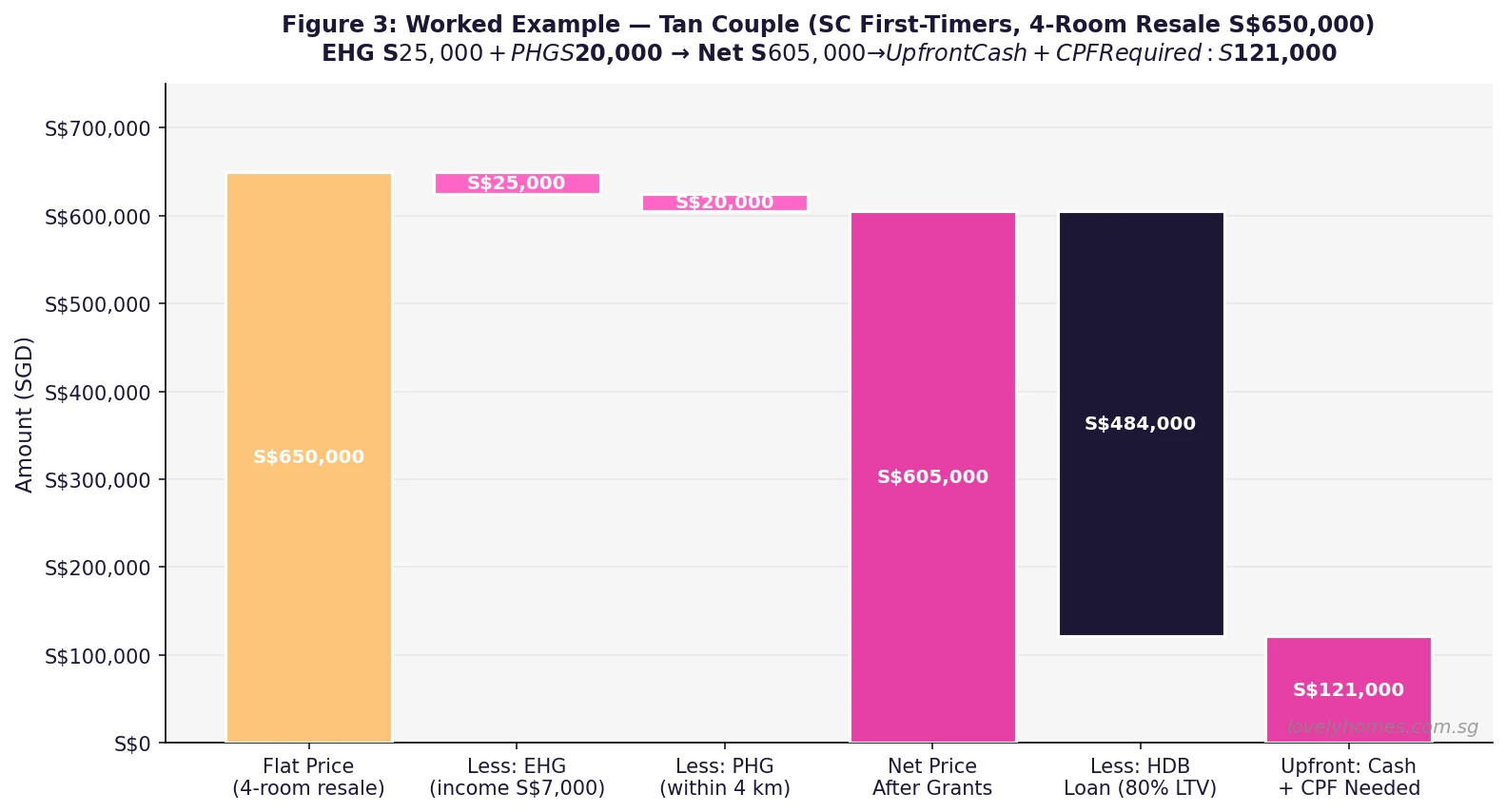

Worked Example: Mr & Mrs Tan — 4-Room Resale, Tampines

Mr & Mrs Tan are a Singapore Citizen couple in their early 30s. Their combined gross monthly income is S$7,000. They wish to purchase a four-room resale flat in Tampines at the asking price of S$650,000. Mrs Tan’s parents live in a Housing Board flat in Pasir Ris — approximately 3.2 kilometres away — and will remain there after the purchase.

Step 1 — Grant entitlement. Mr & Mrs Tan are first-timers (neither has owned an HDB flat or received a housing subsidy before). At a joint income of S$7,000 per month, their EHG entitlement is S$25,000. As they are buying within 4 km of Mrs Tan’s parents and the parents will remain there for at least five years, they qualify for the PHG at S$20,000. Total grants: S$45,000, credited to their combined CPF Ordinary Accounts.

Step 2 — BSD calculation. Buyer’s Stamp Duty on S$650,000: 1% × S$180,000 = S$1,800; 2% × S$180,000 = S$3,600; 3% × S$290,000 = S$8,700. Total BSD = S$14,100. No ABSD applies as Mr & Mrs Tan are SC first-timers.

Step 3 — HDB loan and monthly instalment. The couple qualifies for an HDB Concessionary Loan at 2.6% per annum (0.1% above the prevailing CPF OA rate). Maximum loan quantum is 80% of the purchase price = S$520,000. Monthly instalment over 30 years: approximately S$2,079. MSR check: S$2,079 ÷ S$7,000 = 29.7% — within the 30% Mortgage Servicing Ratio cap. ✓

Step 4 — Upfront CPF and cash. 20% down payment = S$130,000, payable from CPF OA. Less EHG + PHG credited to CPF OA (S$45,000): net CPF drawdown from own savings = S$85,000. The couple must also have at least S$85,000 in their combined CPF OA at the point of the HFE letter. Cash outlays: BSD S$14,100 + legal conveyancing fees ~S$2,800 = approximately S$17,000 cash minimum.

Summary for Mr & Mrs Tan: Purchase price S$650,000 → grants reduce effective CPF burden by S$45,000 → HDB loan S$520,000 @ 2.6% for 30 years → monthly S$2,079 (MSR 29.7%) → cash upfront ~S$17,000 → own CPF OA needed ~S$85,000.

How CPF Grants Affect Accrued Interest on Sale

A point that many buyers overlook: when you eventually sell a grant-assisted resale flat, the CPF Board requires you to refund to your CPF account not only the principal amount of CPF withdrawn (including the EHG and PHG credited) but also the accrued interest that amount would have earned had it remained in your CPF OA at 2.5% per annum compounded annually.

For the Tan couple, if S$45,000 in grants remains in their CPF account for 10 years, the accrued interest would add approximately S$12,600 to the CPF refund on sale. This is refunded to their own CPF — it does not go back to HDB — so it is not a loss, but it reduces the cash proceeds from the sale. Buyers planning to monetise their flat in the medium term should model the CPF accrued interest carefully. See our detailed CPF accrued interest guide for the full calculation methodology.

How to Apply for CPF Housing Grants (Resale)

All CPF housing grants for resale flats are applied for through the HDB Resale Portal (resale.hdb.gov.sg). The process runs in parallel with your resale flat application:

- Obtain your HFE Letter. Before registering your Intent to Buy, both buyers must obtain a valid HDB Flat Eligibility (HFE) letter via the My HDBPage portal. The HFE letter assesses your eligibility for grants, loan quantum, and flat types. It is valid for nine months.

- Grant eligibility is confirmed in the HFE. The EHG amount, PHG eligibility, and Step-Up Grant are all stated in your HFE letter. No separate grant application is required for EHG.

- Submit your resale application. After agreeing on the Option to Purchase (OTP) with the seller, both parties submit their portions of the resale application within 21 calendar days. Grants are confirmed at this stage.

- PHG confirmation after completion. For the PHG, HDB conducts a verification that the parent or child is living within the stipulated proximity before the final disbursement. Ensure the parent has updated their official registered address with ICA before your resale completion date.

What This Means for Resale Buyers in 2026

The continued availability of EHG for resale purchases — without a BTO-style income ceiling that excluded higher-earning households from BTO priority — has been a stabilising force in the HDB resale market. The EHG effectively lowers the barrier for lower-income first-timer families who might otherwise face a wide gap between their budget and resale prices in mature estates.

However, with HDB resale prices rising 2.9% in 2025 and the Resale Price Index at 203.6 as at Q4 2025, the real purchasing power of grants has not kept pace with price appreciation in mature estates. A S$30,000 PHG represents a smaller percentage of the purchase price for a S$1 million flat in Bishan or Queenstown than it did five years ago. Buyers should treat grants as a CPF OA top-up that smooths the financing, rather than a game-changer that expands their budget ceiling significantly.

The PHG’s “no income ceiling” feature makes it particularly valuable for mid-to-high income couples who do not qualify for EHG but are buying near their parents. A couple earning S$12,000 per month gets zero EHG — but can still collect S$20,000 or S$30,000 in PHG. Many such buyers are unaware of this and miss out simply because they assume their income disqualifies them from all grants.

What Might Come Next — Grant Outlook

Speculation only — but directionally relevant. Following the May 2026 EC cooling measures (10-year MOP for new ECs, abolition of Deferred Payment Scheme), the Government has signalled a continued preference for demand-side measures that target speculative activity rather than reducing support for genuine first-timer buyers. This suggests the EHG framework is unlikely to be tightened in the near term. Income ceilings may be gradually adjusted upward if median household incomes continue rising and if resale prices in mature estates persistently exceed the reach of lower-income buyers. The PHG proximity condition may also be reviewed if data shows a mismatch between declared proximity and actual living arrangements.

FAQ: CPF Housing Grants for Resale Flats 2026

Can I use my CPF housing grant to pay for stamp duty?

No. Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) must be paid in cash within 14 days of exercising the Option to Purchase. Housing grants are credited to your CPF Ordinary Account and can only be used for the flat purchase itself (down payment and/or monthly loan instalments), not for stamp duty, legal fees, or any other transaction costs. This is a common misconception that catches buyers off-guard when planning their cash flow.

Can a Singapore Permanent Resident (SPR) receive the EHG or PHG?

An SPR cannot receive the EHG as a sole applicant. However, an SPR co-applying with a Singapore Citizen spouse can benefit from the EHG — the SC spouse must be the main applicant. The PHG is also accessible to SC+SPR couple combinations, provided at least one applicant is an SC. SPR singles are not eligible for any of the CPF housing grants described in this guide.

Does the EHG affect how much HDB loan I can borrow?

The EHG does not directly change your loan quantum, which is determined by the HDB financial assessment based on income, outstanding loans, and age. However, because the EHG is credited to your CPF OA and reduces the CPF shortfall in the down payment, it can effectively free up CPF OA funds for future mortgage repayments or reduce the cash you need on hand. Your maximum HDB loan quantum remains at 80% of the purchase price subject to the Mortgage Servicing Ratio (MSR) cap of 30% of gross monthly income.

What happens to my EHG if I sell the flat before the 5-year MOP?

The EHG imposes a mandatory 5-year Minimum Occupation Period (MOP) from the date the keys are collected. If you sell, sublet the entire flat, or transfer ownership before this period is up, HDB will require you to refund the full EHG amount received. In practice, HDB also charges interest on the refund. The 5-year MOP for grant purposes runs concurrently with the standard 5-year HDB MOP, so in most cases you cannot sell early anyway — but it is worth knowing that the grant creates an additional contractual obligation on top of the statutory MOP.

Can I get both the EHG and the PHG at the same time?

Yes — EHG and PHG can be stacked. A first-timer family purchasing near or with their parents can receive both grants simultaneously. The maximum combined grant under this stacking arrangement is S$150,000 (S$120,000 EHG for income ≤ S$1,500/mth plus S$30,000 PHG for living with parents). Both grants are assessed at the HFE letter stage and disbursed upon resale completion. There is no restriction preventing simultaneous access, but each grant has its own eligibility conditions which must be met independently.

I am a first-timer single aged 35. How do the grants work for me?

Singles aged 35 and above buying under the Single Singapore Citizen (SSC) scheme or with another single under the Joint Singles Scheme can access the EHG at half the family rate — up to S$60,000 for those earning S$4,500 or less per month. You can also receive the PHG at the singles rate: S$15,000 if your parents live at the same address, or S$10,000 if they live within 4 km. Like families, you must maintain the proximity condition for five years after purchase. You are not eligible for the Step-Up Grant as a single applicant. Note that singles can only purchase resale HDB flats of any flat type if aged 35 or above; there is no age restriction for 2-Room Flexi BTO flats in non-mature estates.

Do I need to physically live near my parents immediately, or can I move in later?

For the PHG proximity condition, the parent must reside within 4 km of your resale flat from the date of your flat purchase completion onwards. HDB will verify the parent’s registered address at CPF disbursement and at intervals during the 5-year obligation period. You cannot count on moving your parents closer after you have already purchased the flat to retroactively qualify — the proximity condition must be met at the point of purchase and maintained continuously for five years.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Enhanced Housing Grant (EHG) Singapore 2026 — Full Deep-Dive

- HDB Resale Flat Eligibility Singapore 2026: Who Can Buy

- CPF Accrued Interest and Property Sales Singapore 2026

- Home Loan Comparison Singapore 2026: HDB Loan vs Bank Loan

- Stamp Duty Calculator Singapore 2026: BSD and ABSD Guide

- First-Time Property Buyer Checklist Singapore 2026

Disclaimer: This article is intended as general information only and does not constitute financial or legal advice. Grant amounts, income ceilings, and eligibility conditions are based on HDB and CPF Board guidelines current as at 22 May 2026 and may change without notice. Readers are encouraged to verify all information directly with HDB (hdb.gov.sg) and the CPF Board (cpf.gov.sg) before making any financial decisions. Consult a licensed financial adviser or HDB-accredited conveyancer for advice specific to your circumstances.

Click anywhere to close