Renting Out Your HDB Flat 2026: Rules, Quotas, Rental Rates and Step-by-Step Landlord Guide

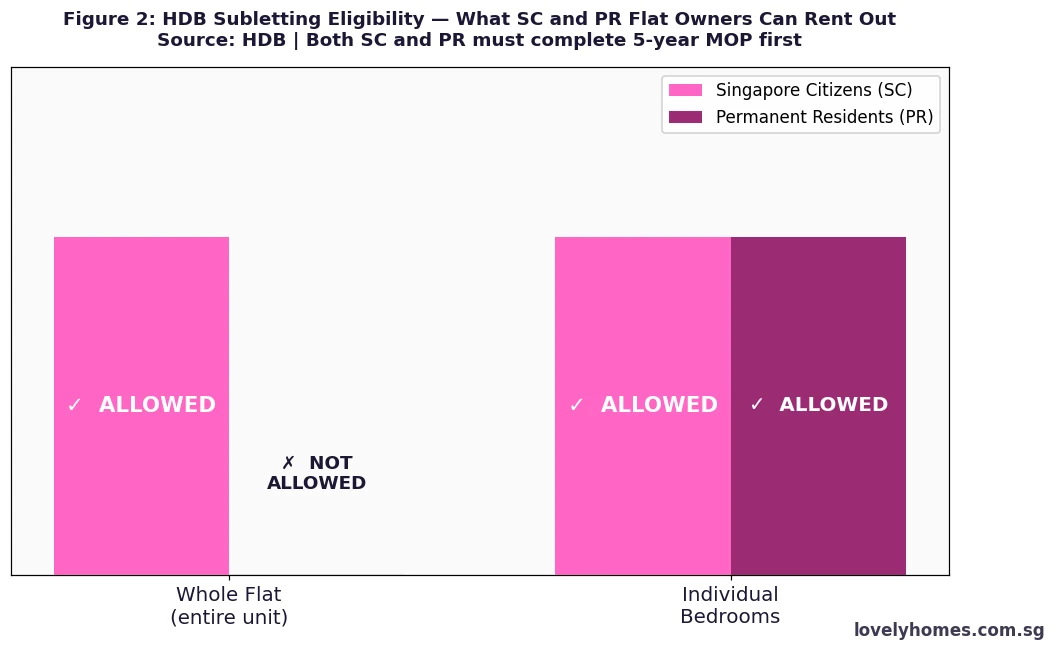

- Who can sublet the whole flat? Singapore Citizens (SC) only. Permanent Residents (PR) may only rent out individual bedrooms — not the entire flat.

- Minimum Occupation Period (MOP): 5 years from the date of key collection before subletting is permitted. Older flats purchased before 30 August 2010 without a grant have a 3-year MOP.

- Minimum lease term: 6 months per tenancy agreement for whole-flat rental. No minimum for bedroom rental.

- Non-Citizen Quota: 8% at neighbourhood level and 11% at block level. Applies when any tenant renting the whole flat is a non-Malaysian non-citizen.

- Occupancy cap (temporarily relaxed): Up to 8 unrelated persons in a 4-room or larger HDB flat (relaxed from 6 until 31 December 2026).

- HDB approval required: Flat owners must register the subletting with HDB online before tenants move in. Failure is a serious offence.

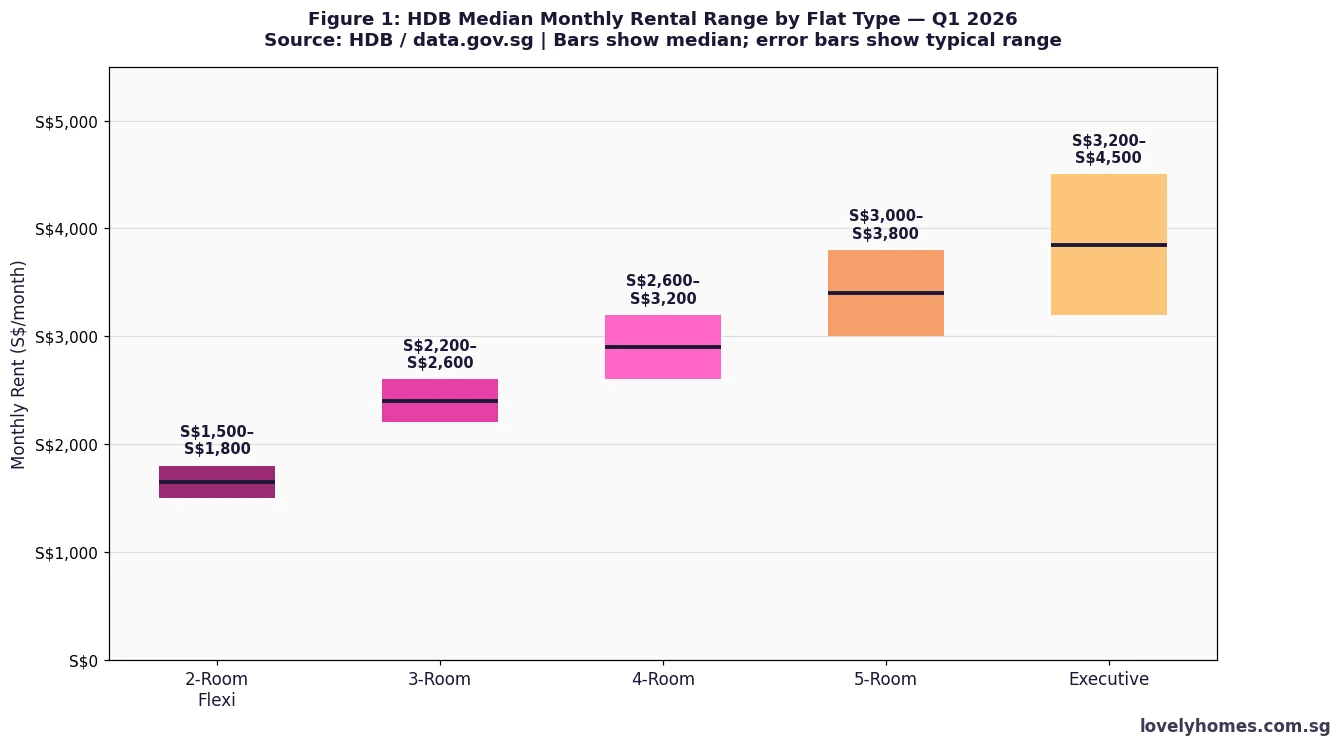

- Typical rental rates (Q1 2026): 3-room S$2,200–2,600/mth; 4-room S$2,600–3,200/mth; 5-room S$3,000–3,800/mth.

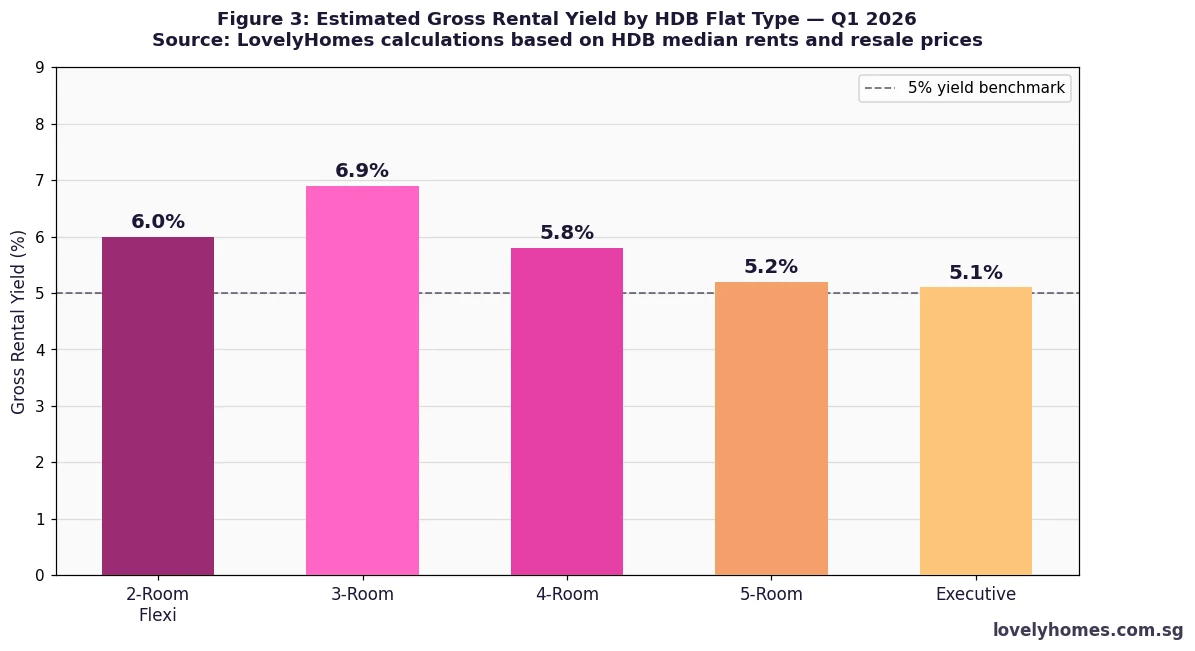

- Rental yields: Approximately 5–7% gross depending on flat type and estate.

Can You Rent Out Your HDB Flat?

HDB flats in Singapore can be rented out, but the rules are considerably more prescriptive than for private residential property. The framework is administered by HDB under the Housing and Development Act (Cap 129), and non-compliance can result in severe penalties including compulsory acquisition of the flat. The rules distinguish sharply between who can rent (citizenship status), what can be rented (whole flat versus individual bedrooms), who the tenants can be (nationality quotas), and for how long (minimum tenancy periods).

Before considering subletting, flat owners should also understand how rental income interacts with their CPF, ABSD obligations, and income tax position — particularly if they have moved out to live elsewhere. This guide covers the complete picture for Singapore Citizens and Permanent Residents who own an HDB flat and wish to generate rental income from it.

Who is Eligible to Sublet?

The eligibility rules operate at two levels: (1) who can sublet the entire flat, and (2) who can rent out individual bedrooms.

Singapore Citizens (SC) may sublet their entire flat or individual bedrooms, subject to completing the MOP and receiving HDB’s approval for each subletting period. The flat owner does not need to live in the flat during the subletting period — they may reside elsewhere, including in private property, for the duration.

Permanent Residents (PR) may rent out individual bedrooms in their HDB flat, but may NOT sublet the entire flat. If a PR owns an HDB flat, the PR (or at least one listed owner) must continue to reside in the flat at all times while bedrooms are being rented out. PRs who wish to vacate entirely and rent out the whole flat must either sell the flat or apply for an SC-sponsored transfer — there is no exception.

Both SC and PR flat owners must have completed the applicable MOP before any subletting (whole flat or bedroom) is permitted.

Minimum Occupation Period (MOP) Before Subletting

The MOP is the most fundamental gating requirement for HDB subletting. It runs from the date of key collection (not purchase date) and applies to all flats regardless of whether they were purchased directly from HDB (BTO/DBSS) or on the open resale market with a grant:

- Standard MOP (most flats): 5 years from key collection. Applies to all BTO flats, DBSS, and resale flats purchased with a CPF housing grant.

- Shortened MOP: 3 years for resale flats purchased before 30 August 2010 without any housing grant. Very few flats remain in this category.

- Plus and Prime flats: 10-year MOP. These are flats in highly sought-after locations announced under the 2023 HDB classification framework. Subletting the whole flat is not permitted even after the 10-year MOP — only bedroom rental is allowed for Plus and Prime flat owners.

Note that any period during which the flat was unoccupied (e.g., the owner lived overseas for work) may be deducted from the MOP clock by HDB in certain circumstances — check with HDB directly if this situation applies to you.

HDB Rental Rates in 2026

HDB rental rates have risen meaningfully since the pandemic-era demand surge, with median rents across all flat types up approximately 3.2% year-on-year as of Q1 2026. The chart below shows the typical monthly rental range by flat type across Singapore:

These are Singapore-wide medians — estate location significantly affects achievable rents. Central estates (Toa Payoh, Bishan, Queenstown) typically command 15–25% premiums over the national median for the same flat type. Outer estates (Woodlands, Sembawang, Choa Chu Kang) trade at 5–15% discounts. The temporary relaxation of the occupancy cap to 8 unrelated persons (until 31 December 2026) has supported demand from shared accommodation arrangements, particularly in the co-living segment.

Non-Citizen Subletting Quota

To maintain the ethnic and community character of HDB estates, HDB imposes a Non-Citizen Quota (NCQ) on whole-flat subletting:

| Level | Quota | What It Means |

|---|---|---|

| Neighbourhood | 8% | No more than 8% of flats in the neighbourhood may be sublet to non-Malaysian non-citizen tenants |

| Block | 11% | No more than 11% of flats in the block may be sublet to non-Malaysian non-citizen tenants |

Source: HDB | Quota does not apply to bedroom rental — only whole-flat subletting.

Malaysian nationals are excluded from the NCQ calculation — a legacy of the historical close ties between Singapore and Malaysia. If the NCQ for your block or neighbourhood has been reached, you may only sublet your flat to Singaporean or Malaysian tenants. You can check the current NCQ status for any block through the HDB e-Services portal before entering into a tenancy agreement.

The NCQ is particularly relevant in popular expat neighbourhoods (Queenstown, Tiong Bahru, Toa Payoh) and around MRT hubs, where demand from foreign professionals is high. Landlords in these estates should monitor the NCQ status regularly — it changes as tenancy agreements expire and new ones begin.

Occupancy Cap — Temporarily Relaxed Until 31 December 2026

In January 2024, the Government temporarily relaxed the maximum number of unrelated occupants in larger HDB flats and private residential properties to address tight rental market conditions for foreign workers and students. As at 7 June 2026, this relaxation remains in effect:

| Property Type | Normal Cap | Relaxed Cap (until 31 Dec 2026) |

|---|---|---|

| HDB 4-room or larger (or private property 90sqm+) | 6 unrelated persons | 8 unrelated persons |

| HDB 1-room, 2-room, 3-room (or private property below 90sqm) | 6 unrelated persons | 6 unrelated persons (no change) |

Source: HDB / URA joint press release, January 2024 | Relaxation valid until 31 December 2026.

Landlords of larger flats who wish to maximise occupancy for room-rental models should note that the occupancy cap reverts to 6 persons on 1 January 2027 unless HDB announces a further extension. Co-living operators using HDB flats as their supply base are particularly exposed to this change.

How to Apply — The Subletting Process

The subletting process involves HDB approval before tenants can move in. Here is the step-by-step workflow for a whole-flat subletting:

- Confirm MOP has been satisfied: Check your key collection date and ensure 5 years have passed. Do not sign any tenancy agreement until the MOP is complete.

- Confirm eligibility: Ensure you are an SC flat owner. Confirm all registered owners consent to the subletting.

- Check NCQ status: Log in to HDB e-Services to confirm the NCQ for your block and neighbourhood is not fully utilised if you plan to rent to non-Malaysian non-citizens.

- Negotiate and sign a tenancy agreement: The minimum tenancy period for a whole flat is 6 months. You may sublet for up to 3 years at a time, subject to renewal approval from HDB.

- Register the subletting with HDB: Submit the subletting application online via HDB e-Services before the tenants move in. Provide tenants’ details (NRIC/FIN, nationality, employment pass type if applicable). This is a statutory requirement — failure to register before tenants move in is a breach of the Housing and Development Act.

- Receive HDB approval: HDB will issue a confirmation letter (typically within a few working days for compliant applications). Retain this letter for your records.

- Collect rent and manage the tenancy: Issue a proper tenancy agreement. Collect a security deposit (typically 1–2 months rent). Stamp the tenancy agreement via IRAS e-Stamping (stamp duty on rental: 0.4% of total rent for leases exceeding one year).

- Renewal: Notify HDB and apply for renewal before each renewal period. HDB re-checks eligibility and NCQ at each renewal.

Rental Yield Analysis — Is Renting Out Worth It?

Gross rental yields on HDB flats are among the highest of any property class in Singapore, ranging from approximately 5.1% to 6.9% depending on flat type. Smaller flats (2-room, 3-room) generate higher yields relative to their resale values because rents have not declined proportionately with the relatively lower price points. Larger flats (5-room, Executive) generate lower percentage yields but higher absolute monthly income.

Net yields — after property tax, maintenance fees, and occasional void periods — are typically 0.5–1.0 percentage points lower than gross. At 5–6% net yield, HDB flats compare favourably to private condo yields (typically 3–4% net) and offer a meaningful income return for SC flat owners who have upgraded to private property and retained their HDB flat — a common wealth-building strategy for Singapore families, subject to ABSD on the second property.

Summary Table: HDB Whole-Flat vs Bedroom Rental — Key Differences

| Rule | Whole-Flat Rental | Bedroom Rental |

|---|---|---|

| Who can sublet | Singapore Citizens only | SC and PR flat owners |

| Owner must reside in flat | No — owner may live elsewhere | Yes — PR owner must remain in flat |

| Minimum lease | 6 months | No statutory minimum |

| Maximum subletting period | 3 years (renewable) | No statutory maximum per term |

| Non-Citizen Quota | Yes — 8%/11% (neighbourhood/block) | Not applicable |

| HDB approval required | Yes — before tenants move in | Yes — must register bedroom tenants |

| Tenancy stamp duty | 0.4% of total rent (IRAS) | 0.4% of total rent (IRAS) |

| Income tax on rental income | Yes — reportable to IRAS | Yes — reportable to IRAS |

Source: HDB / IRAS | As at 7 June 2026.

Worked Example: Mr and Mrs Tan Rent Out Their Toa Payoh HDB Flat

Mr and Mrs Tan, both Singapore Citizens, purchased a 4-room HDB flat in Toa Payoh in June 2018 and collected keys in September 2021. They completed their 5-year MOP in September 2026. Having upgraded to a private condominium in Bishan in April 2026 (paying ABSD as a second property purchase), they wish to sublet their HDB flat for rental income to help service the new mortgage.

Rental market check: A 4-room HDB in Toa Payoh commands S$2,800–S$3,200/mth. They aim for S$3,000/mth.

NCQ check: Their block in Toa Payoh Lorong 2 has NCQ utilisation at 6% (neighbourhood) and 9% (block) — both below the 8%/11% thresholds. They can rent to non-Malaysian non-citizens.

Process: They sign a 12-month tenancy agreement at S$3,000/mth with an expatriate family. Security deposit: S$6,000 (2 months). Tenancy stamp duty: 0.4% x S$3,000 x 12 months = S$144, payable to IRAS. They register the subletting with HDB before the tenants move in.

Financials:

- Annual rental income: S$36,000

- Property tax on rented-out flat (annual value ~S$20,400 x 12% owner-occupier rate — no, since it is now non-owner-occupied, higher rates apply: 10–20% on AV): approximately S$2,040–S$4,080/year

- Maintenance fee: approximately S$70–S$80/mth = S$840–S$960/year

- Gross yield: S$36,000 / S$780,000 (estimated flat value) = 4.6% gross

- Net yield (after property tax and maintenance): approximately 3.7–4.0%

- Annual net rental income (approx.): S$29,000–S$31,000

Mr and Mrs Tan must also declare the rental income in their annual personal income tax returns filed with IRAS. They may deduct allowable expenses (property tax, maintenance fees, mortgage interest if the loan relates to the rented property, insurance, agent fees) from the rental income before tax. There is no Capital Gains Tax in Singapore, so future sale proceeds are not taxed.

Why HDB Rental Income Matters — and What It Means for Flat Owners

For Singapore Citizens who have upgraded to private housing and retained their HDB flat, rental income from the HDB flat is one of Singapore’s most tax-efficient income streams. At yields of 5–7% gross and no CGT, a S$600,000 HDB flat generating S$30,000 per year in net rental income represents a meaningful supplement to household income. The key constraint is that such a strategy requires paying ABSD on the private property (currently 20% for SC second property — see our ABSD guide for full rates), which takes years of rental income to recover. The maths works best for SC couples who are certain they want to hold both properties long term.

For SC flat owners who do not own other property — for example, those who travel frequently for work — the ability to rent out the whole flat while living elsewhere provides genuine flexibility. The 6-month minimum tenancy ensures landlords are not trapped in indefinitely short arrangements, while the 3-year maximum subletting period (renewable) provides medium-term income stability.

What Might Change for HDB Rental Rules

This section reflects editorial analysis and is speculative in nature.

The temporary occupancy cap relaxation (from 6 to 8 unrelated persons in larger flats) is set to expire on 31 December 2026. HDB will assess whether rental market conditions continue to justify the relaxation. If the rental market tightens further — driven by continued foreign workforce growth and an undersupply of completed units — the relaxation may be extended. If the private rental market stabilises, it is more likely to revert to 6 persons. Landlords operating shared-accommodation models should not assume the relaxation will continue beyond year-end without official confirmation.

More broadly, the HDB Plus and Prime classification framework (announced in 2023) will progressively bring more units with 10-year MOPs and whole-flat subletting restrictions into the resale pool as these projects complete. Over the next decade, the supply of freely-sublettable HDB flats (i.e., non-Plus, non-Prime flats with completed MOPs) will remain substantial but may not grow as rapidly as the overall HDB stock.

Frequently Asked Questions

I am a PR and want to rent out my whole HDB flat — is this allowed?

No. Permanent Residents are not permitted to sublet the entire HDB flat. PRs may only rent out individual bedrooms in the flat, and must continue to reside in the flat at all times while bedroom tenants are present. If you are a PR and wish to vacate the flat entirely, you must sell the flat on the open market. There is no exception for this rule. If you become a Singapore Citizen after purchasing your flat, you immediately become eligible to sublet the whole flat (subject to MOP completion) — another advantage of SC status for property owners.

Can a foreigner rent an HDB flat in Singapore?

Yes, foreigners may rent HDB flats as tenants. However, the Non-Citizen Quota (8% neighbourhood / 11% block) limits how many HDB flats in any given area can be rented to non-Malaysian non-citizens. If the quota for a block is reached, only Singaporean or Malaysian tenants are permitted. Foreigners should check with potential landlords whether the quota has been reached before committing to a lease. The quota does not apply to bedroom rental — foreigners may always rent individual bedrooms in HDB flats regardless of quota status.

What happens if I rent out my flat without HDB approval?

Subletting without HDB approval is a serious breach of the Housing and Development Act. Penalties include a fine of up to S$5,000 for first offences, and compulsory acquisition of the flat (forced sale at market value with no premium) for repeat or serious offences. HDB conducts periodic estate checks and receives tip-offs from neighbours, so non-compliant landlords are regularly caught. The financial cost of compulsory acquisition — losing the flat at market value with no recourse to negotiate — far outweighs any short-term rental income gained from operating without approval.

Do I need to pay tax on rental income from my HDB flat?

Yes. Rental income from an HDB flat is taxable income in Singapore and must be declared in your annual Income Tax Return filed with IRAS. The income is taxed at your marginal personal income tax rate (ranging from 0% to 24% for residents). You may deduct allowable expenses from the rental income: mortgage interest (if the loan relates to the rented property), property tax, fire insurance, maintenance fees, and agent commission. Wear and tear (depreciation) is not a deductible expense under Singapore tax rules. You are also entitled to a deemed deduction of 15% of the gross rent in lieu of actual expenses if that is simpler. Speak to a tax adviser if your rental income is material. See the IRAS website for the specific guidelines.

Can I rent out my HDB flat on Airbnb or other short-term platforms?

No. Short-term rentals of HDB flats — defined as any rental period of less than 6 months — are strictly prohibited under HDB rules and the Hotels Licensing Act. Platforms like Airbnb, Booking.com, and similar services facilitate short-term stays that would violate the minimum 6-month tenancy requirement for whole-flat subletting. HDB has prosecuted flat owners for Airbnb violations and the consequences are the same as for any unlicensed subletting: fines and potential compulsory acquisition. This prohibition applies to HDB flats; private residential property is governed by separate URA rules (which also generally prohibit short-term lets of under 3 months for most private properties).

What is the stamp duty on a rental agreement for an HDB flat?

Rental agreements for HDB flats (and private residential property) must be stamped via the IRAS e-Stamping Portal within 14 days of signing. The stamp duty rate is 0.4% of the total rent for leases exceeding one year, and 0.2% of the total rent for leases of one year or less. For a typical 12-month lease at S$2,800/mth, the stamp duty is 0.4% x S$33,600 = S$134.40. The duty is conventionally paid by the tenant (as the party receiving the tenancy document), though landlord and tenant may agree otherwise in the tenancy agreement.

My HDB MOP will be completed in 3 months. Can I start looking for tenants now?

You may market the flat and negotiate tenancy terms before the MOP is completed, but you cannot sign a tenancy agreement or submit the HDB subletting application until the MOP date has passed. In practice, the market is aware of this constraint and tenants are generally willing to allow for a short lead time between signing and move-in. A common approach is to agree on the lease terms and execute the tenancy agreement on the day of (or shortly after) MOP completion, with tenants moving in a week or two later — giving time for HDB approval to be received (typically 3–5 working days for compliant applications).

Related Articles

- Singapore HDB Resale Guide 2026: Complete Guide to Buying and Selling HDB Resale Flats

- Singapore HDB Upgrading Guide 2026: Costs, ABSD, CPF and Step-by-Step Process

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Seller’s Stamp Duty (SSD) 2026: New 4-Year Holding Period, Rates and Exemptions

- Singapore Home Loan Complete Guide 2026: HDB Loans, Bank Loans, TDSR and MSR Explained

- HDB Grants Singapore 2026: EHG, CPF Housing Grant, Proximity Grant and Step-Up Grant Explained

- Singapore Property Investment Guide 2026: How to Build Wealth Through Property

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. HDB policies, occupancy cap rules, and rental regulations can change. Always verify current eligibility conditions, quotas, and approval requirements directly with HDB and consult a qualified Singapore property lawyer or tax adviser before making rental decisions. Rental rates, yields, and government policy cited are based on information available as at 7 June 2026.