Singapore HDB SERS Guide 2026: Selective En Bloc Redevelopment Scheme, Compensation and What It Means for Flat Owners

Quick Answer: HDB SERS — What You Need to Know in 2026

- SERS stands for Selective En Bloc Redevelopment Scheme, administered by HDB to redevelop ageing public housing estates with good redevelopment potential.

- Under SERS, HDB compulsorily acquires selected old flats at fair market compensation and offers residents a replacement flat at a discounted price in a new development nearby.

- SERS is rare and selective — only around 79 precincts involving approximately 33,000 flats have been selected since 1995. Most old HDB flats will NOT receive SERS.

- Affected residents receive a compensation package including market value, a rehousing allowance, an inconvenience allowance, and a stamp duty waiver on the replacement flat.

- The Voluntary Early Redevelopment Scheme (VERS) was announced in 2018 as a potential future alternative; as at June 2026 it has not been implemented for any estate.

- SERS announcements are made by HDB with no prior notice to affected residents. You cannot apply for SERS or nominate your estate.

- The average SERS programme takes approximately 4–6 years from announcement to key collection for the replacement flat.

What is the HDB Selective En Bloc Redevelopment Scheme (SERS)?

The Selective En Bloc Redevelopment Scheme (SERS) is Singapore’s public housing equivalent of a compulsory en-bloc sale — but in reverse. Instead of private owners voting to sell to a developer, HDB selects specific precincts of ageing public housing for compulsory acquisition and offers residents a comprehensively packaged relocation deal that typically puts them in a newer, better-located flat.

Introduced in 1995 by the Housing & Development Board, SERS applies when HDB identifies a precinct of older flats — typically from the 1960s, 1970s, or 1980s — that has what HDB terms “good redevelopment potential.” This is generally understood to mean the land can be used more intensively: taller blocks, higher density, or repurposed for a different use entirely. The scheme is funded by the Singapore government and is not subject to market forces in the same way that a private en-bloc sale would be.

For residents, SERS is often viewed favourably — HDB’s compensation is generally regarded as fair, the replacement flats are new, and residents receive a bundle of financial support including a rehousing allowance, inconvenience allowance, and a full waiver of Buyer’s Stamp Duty (BSD) on the replacement flat. From a pure financial standpoint, SERS residents almost invariably end up owning a newer flat with a fresh 99-year lease — reversing the lease decay that afflicts all HDB flats over time.

How Rare is SERS? The Numbers in Context

This is perhaps the most important thing to understand about SERS: it is exceptional, not a standard entitlement. As at June 2026, HDB has announced SERS for approximately 79 precincts since 1995, covering around 33,000 flats — representing less than 4% of Singapore’s entire public housing stock. Singapore has more than 1.1 million HDB flats; the vast majority will not receive SERS.

In a parliamentary speech in March 2018, then-National Development Minister Lawrence Wong confirmed that only a “small fraction” of flats would qualify, and introduced the concept of a Voluntary Early Redevelopment Scheme (VERS) as a future alternative for estates that do not meet SERS criteria. VERS would allow residents to collectively vote for early redevelopment at an older age (in the flat’s 70th to 80th year), but the scheme remains in conceptual form as at 2026 — no VERS exercise has commenced for any estate.

| Metric | Figure | Context |

|---|---|---|

| Year SERS introduced | 1995 | First precinct: Stirling Road, Queenstown |

| Total precincts selected (1995–2026) | ~79 precincts | Approx. 33,000 flats across all selections |

| Share of HDB stock covered | Less than 4% | Over 1.1 million HDB flats island-wide |

| Typical programme duration | 4–6 years | From announcement to key collection |

| Last major SERS announcements | 2023 (Bukit Merah) | No new SERS announcements in 2024–2026 as at June 2026 |

| VERS status (2026) | Announced 2018, not yet implemented | Applicable in flat’s 70th–80th year; no timeline announced |

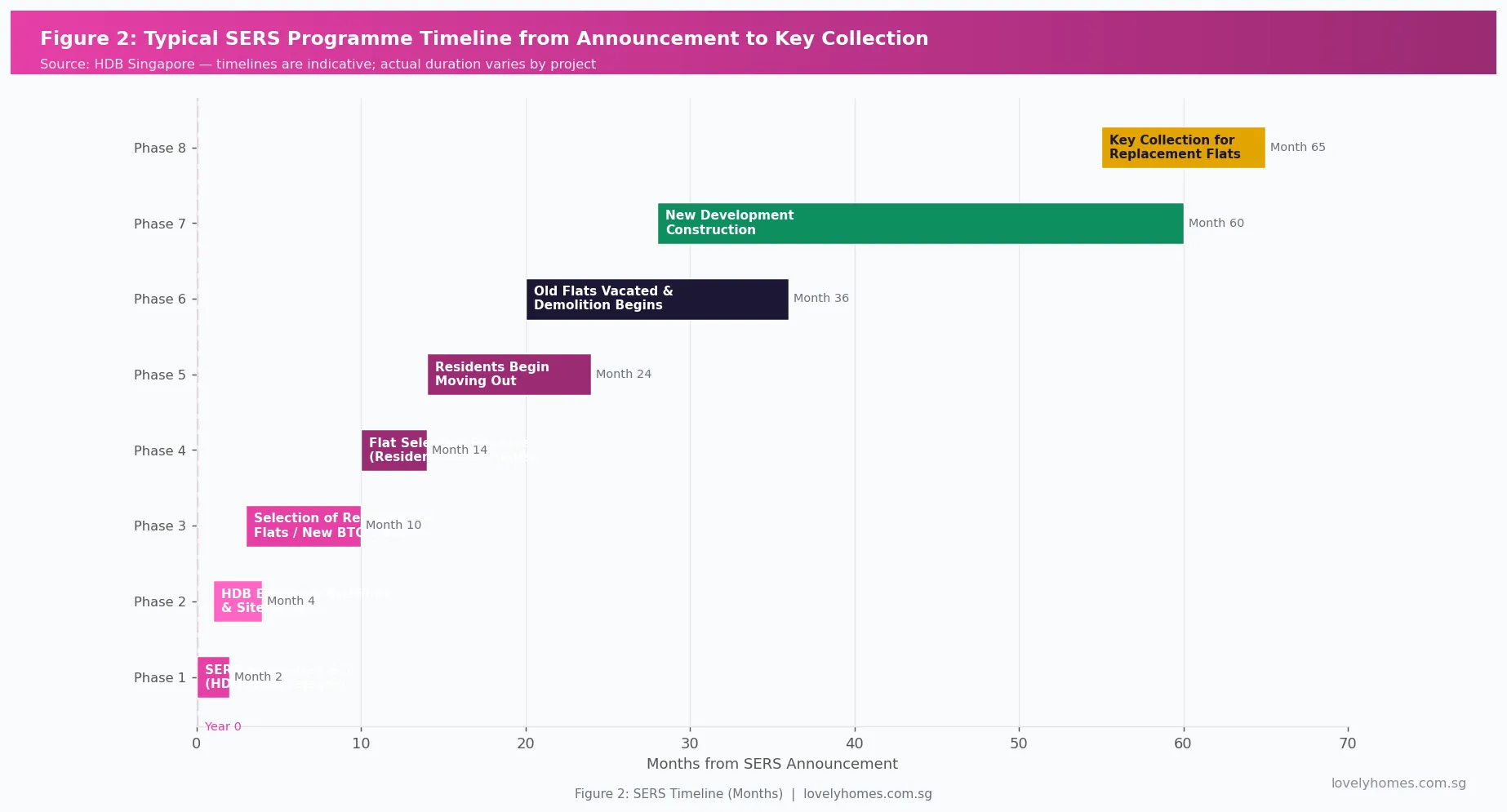

How Does SERS Work? The Process Step by Step

When HDB decides to proceed with a SERS exercise, the process follows a structured sequence that takes several years. The outline below reflects the typical SERS process based on past exercises. Individual SERS exercises may vary in sequencing and timing:

Phase 1 — SERS Announcement: HDB issues a press release identifying the affected precincts. This is the first notification residents receive — there is no prior consultation or warning. HDB simultaneously announces the location of the SERS replacement site, which is generally within 1 km of the original location. An HDB SERS team is set up to manage communications and assist residents.

Phase 2 — Flat Selection: Residents select their replacement flat from the new SERS development, following a selection priority order based primarily on the type and size of the existing flat. Residents can generally choose a like-for-like replacement (same flat type) or upgrade at an additional cost. Some SERS exercises also allow residents to take a cash compensation package instead of a replacement flat — particularly relevant for those who no longer wish to remain in public housing.

Phase 3 — Moving Out & Demolition: Residents vacate the old flat by a HDB-specified date and receive their inconvenience and rehousing allowances. HDB then proceeds with demolition and site clearance.

Phase 4 — Construction and Key Collection: The new SERS replacement development is constructed, typically taking 3–5 years from demolition. Key collection follows, completing the SERS cycle. Throughout this period, residents typically live in transitional housing — often renting a flat privately or staying in HDB-managed interim accommodations, with the rehousing allowance helping to offset rental costs.

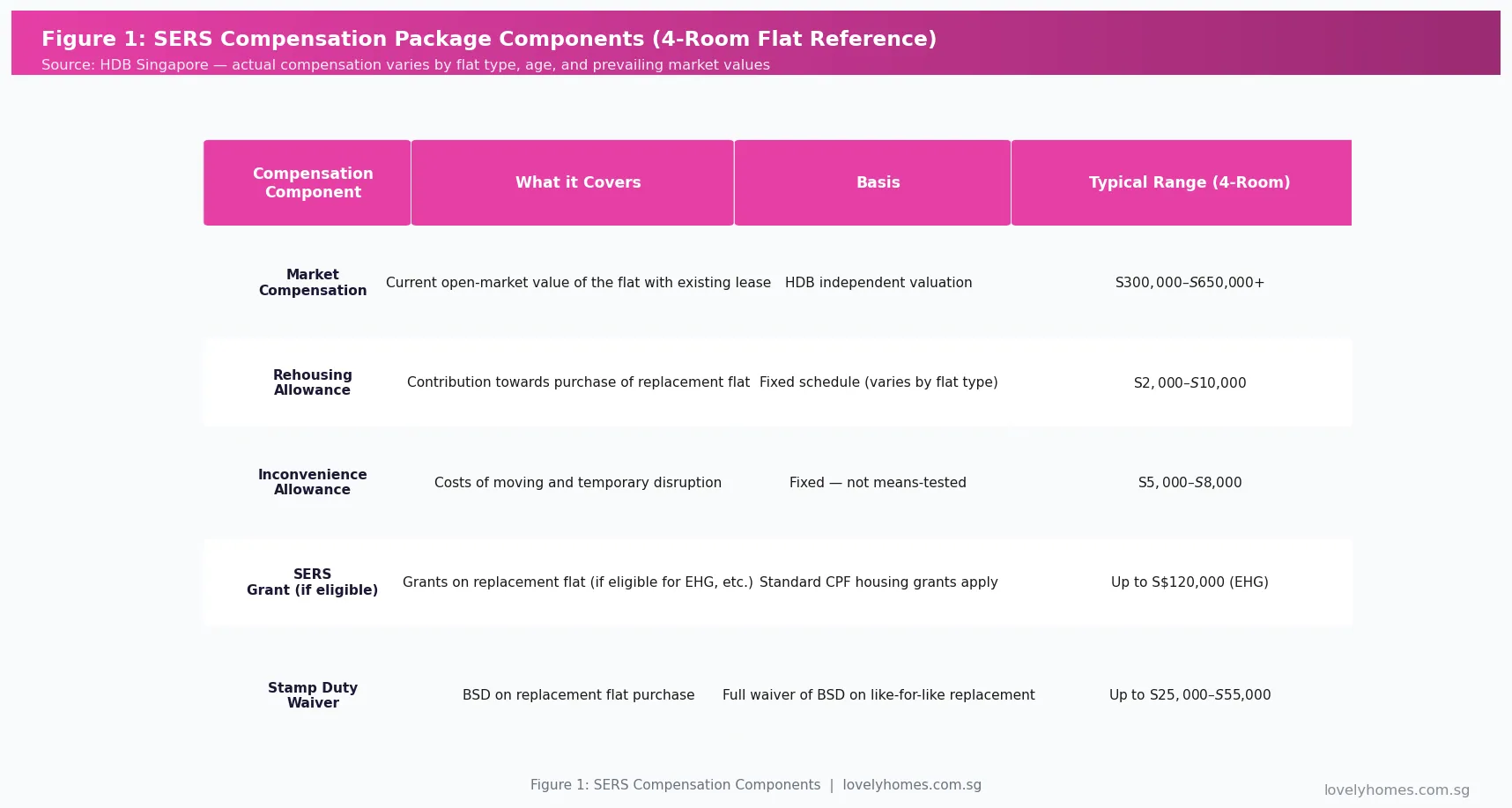

The SERS Compensation Package

The compensation package under SERS is designed to leave affected residents in a broadly equivalent or better position than before. Its main components are as follows, with representative figures for a 4-room flat as a reference point:

- Market Compensation: Based on an independent valuation of the flat’s current open-market value — typically reflecting the value of a comparable flat in the resale market at that time, including a valuation uplift for the lease remaining. For a 4-room flat in a mature estate as at 2026, this might range from S$350,000 to S$650,000+.

- Rehousing Allowance: A fixed contribution towards the cost of purchasing the replacement flat. The quantum varies by flat type and is updated periodically.

- Inconvenience Allowance: A one-time payment to compensate for the disruption of moving, typically S$5,000–S$8,000 as at recent exercises.

- Stamp Duty Waiver: Residents receive a full waiver of Buyer’s Stamp Duty (BSD) on the like-for-like replacement flat purchase. This is a significant concession — BSD on a S$500,000 flat is approximately S$9,600; on a S$800,000 flat, it is S$21,600.

- Applicable Housing Grants: SERS residents purchasing the replacement flat remain eligible for standard CPF housing grants (EHG, Family Grant, etc.) if they meet grant eligibility criteria. As at June 2026, the Enhanced Housing Grant (EHG) provides up to S$120,000 for eligible buyers.

SERS vs Lease Expiry: Why Most Old Flats Will Not Be “Rescued”

A persistent misconception in the Singapore property market is the belief that old HDB flats will inevitably receive SERS before their leases expire. This is a flawed assumption that the government has repeatedly and explicitly corrected.

In a landmark National Day Rally speech in 2018, Prime Minister Lee Hsien Loong directly addressed this misconception, stating that the government could not commit to SERS for all ageing flats because not all estates have good redevelopment potential, and because the financial cost of doing so would be unsustainable. The PM confirmed that some HDB flats would indeed “run their full lease to zero” — meaning, at the end of the 99-year lease, the flat and its leasehold interest revert to the state with no residual value.

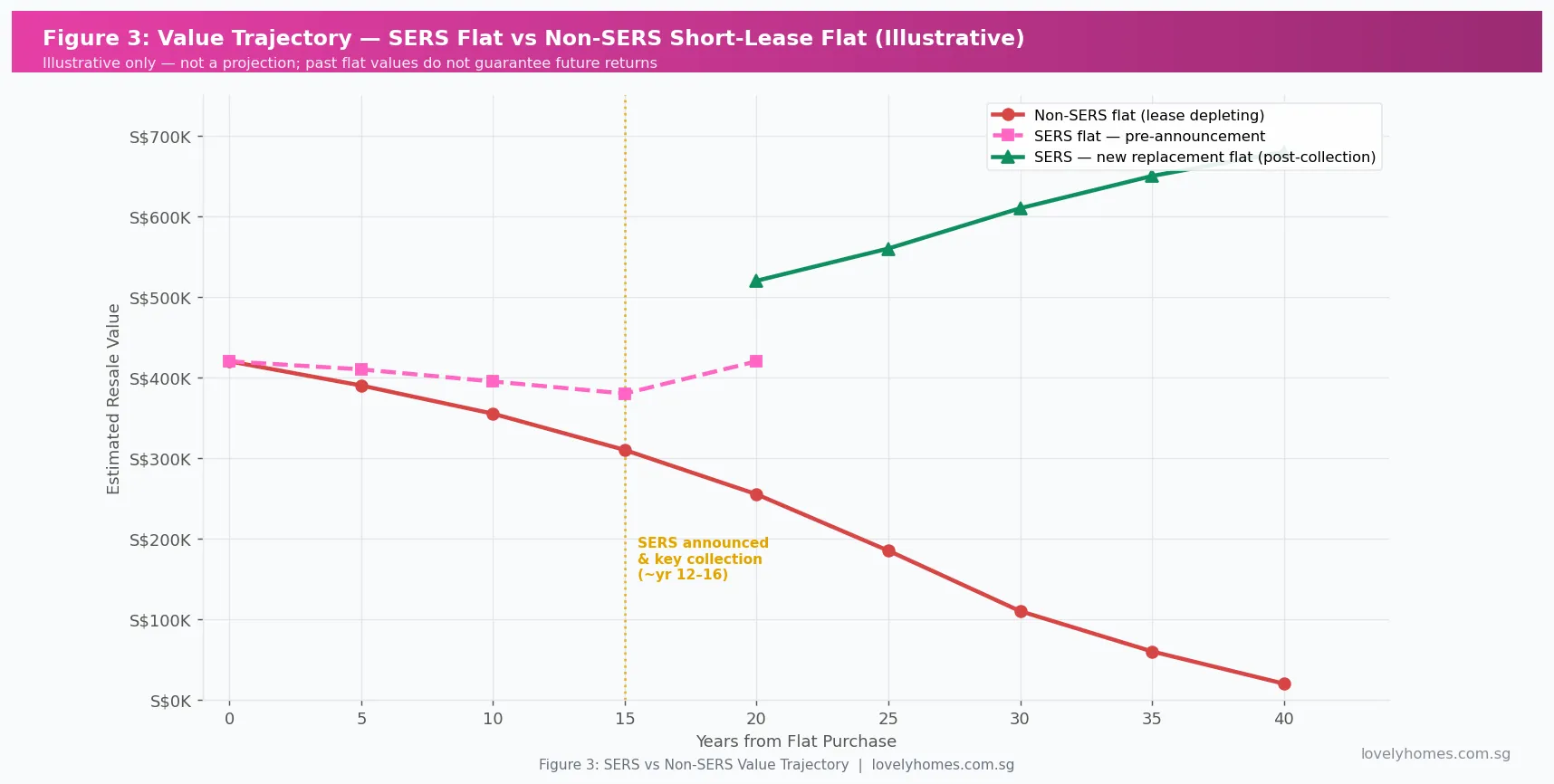

The value trajectory of an HDB flat selected for SERS diverges sharply from one that is left to age. A SERS flat effectively receives a “reset” — its owner walks away with market-rate compensation and a new flat on a fresh lease. A non-SERS flat on a depleting lease will, in theory, trend towards zero as the lease count decreases and CPF eligibility narrows. In practice, HDB flats with short leases continue to transact — often to older, cash-rich buyers for owner-occupation rather than investment — but at significant discounts relative to 99-year lease comparables.

Worked Example: The Krishnamurthys, Queenstown 4-Room Flat

Mr and Mrs Krishnamurthy, both Singapore Citizens, purchased a 4-room HDB flat in Queenstown in 1985 for S$65,000. As at June 2026, the flat is approximately 41 years old and has around 58 years remaining on its lease. They have been living in the flat ever since.

In an imagined SERS scenario: HDB announces SERS for their precinct in January 2027. HDB’s independent valuer assesses the flat’s market value at S$550,000 (reflecting Queenstown’s mature estate premium and the 57-year remaining lease at that point). HDB’s full offer is:

- Market compensation: S$550,000

- Rehousing allowance: S$7,000

- Inconvenience allowance: S$5,000

- BSD waiver on new flat: S$13,400 (equivalent of BSD on S$650,000 flat)

- Total effective package value: ~S$575,400

The Krishnamurthys select a new 4-room SERS replacement flat nearby at S$650,000 (applying S$550,000 compensation + S$7,000 rehousing + S$93,000 top-up from CPF OA savings). They pay no BSD. They take the keys in 2032 to a brand-new flat in Queenstown with a fresh 99-year lease expiring 2131. Net financial position: they spent S$65,000 in 1985 and approximately S$93,000 in 2032 in additional top-up, receiving a new flat worth an estimated S$700,000–S$800,000 in the resale market of that time.

What Might Come Next: VERS and the Future of Ageing Estates

This section contains forward-looking commentary and speculation. It does not constitute financial advice or a prediction of government policy.

By the mid-2030s, Singapore’s earliest HDB estates — particularly Queenstown, Toa Payoh, and parts of the Ang Mo Kio and Bedok new towns — will have leases at or below 60 years. The CPF and financing constraints on these flats will become acutely relevant for the next generation of buyers. The government will face growing political pressure to clarify the future of these estates beyond the binary of SERS (expensive, selective) and lease expiry (politically unpalatable).

The VERS mechanism — if implemented — could offer a middle path: a government-sponsored opt-in collective sale at a modest premium, returning the land for redevelopment without the full costs of a SERS package. Industry commentators have also speculated about hybrid arrangements where some precincts receive partial state acquisition with residents retaining the option to remain in the redeveloped estate as rental tenants. These outcomes remain speculative as at June 2026.

FAQ: HDB SERS Singapore 2026

Can I find out if my flat is likely to receive SERS?

HDB does not publish advance lists of estates or precincts being considered for SERS. You cannot apply to be included, and HDB will not confirm or deny SERS plans in advance. Speculation about SERS eligibility should be treated with caution — it is frequently used as a marketing narrative to justify premium pricing for older flats, and is not supported by any official confirmation process. The general criteria (good redevelopment potential, older estates, land-use efficiency) are publicly stated, but do not translate into predictable selection. As at June 2026, HDB has not announced any new SERS exercises since the 2023 Bukit Merah selections.

What if I do not want the SERS replacement flat?

You can opt for cash compensation instead of a replacement flat. HDB will pay you the market compensation, rehousing allowance, and inconvenience allowance in cash, and you may then apply for a different flat or private housing using those proceeds. The BSD waiver, however, applies only to the SERS replacement flat — it cannot be transferred to another property purchase. If you take the cash option, you will pay standard BSD on any subsequent property purchase.

Does SERS affect my CPF savings?

Yes — when you receive SERS compensation and sell your flat, your CPF OA savings that were used to fund the original purchase (principal drawn down plus the standard 2.5% p.a. accrued interest) must be refunded to your CPF account. This is the same rule that applies to any HDB flat sale. The refunded CPF can then be used towards the SERS replacement flat. Flat owners who used significant CPF for their original purchase should model this carefully — if the market compensation does not cover the CPF refund plus the upgrade cost, additional cash may be required at the point of SERS replacement flat selection.

Will I receive ABSD relief on the SERS replacement flat if I own other properties?

ABSD rules generally apply to the SERS replacement flat purchase based on your total property count at that time. If the SERS flat is your only property and you are a Singapore Citizen purchasing a like-for-like HDB replacement, no ABSD is payable. If you own another property simultaneously — for example, you purchased a private condo while living in the SERS flat — ABSD at 20% (SC second property) would normally apply. SERS compensation is not an ABSD exemption mechanism. IRAS’s ABSD remission for upgrading SC couples does not apply to SERS directly; however, if the sequence of your SERS sale and replacement flat purchase falls within the remission window (replacement flat purchased before SERS flat is compulsorily acquired), you may be eligible. Consult a solicitor for specific advice.

Can SPR flat owners also participate in SERS?

Yes — Singapore Permanent Residents who own HDB flats and are included in a SERS precinct will also receive the SERS compensation package. They are eligible to participate in the replacement flat selection on the same terms as Singapore Citizens. However, SPRs must meet the standard eligibility criteria for the SERS replacement flat (typically, the replacement must be at the same or smaller flat type). If they wish to upgrade beyond the standard replacement tier, they will need to qualify for the additional borrowing required, and standard ABSD rules (SPR 5% first property) apply to any top-up purchase.

How does SERS differ from a private en-bloc sale?

In a private en-bloc (collective sale), private property owners vote to sell the entire development to a developer. The process requires a 80% supermajority vote (for developments over 10 years old) under the Land Titles (Strata) Act, and compensation is the development’s collective sale proceeds divided by share value. SERS is entirely different: it is government-initiated and compulsory — there is no vote, and flat owners cannot block or veto the acquisition. The compensation methodology is also different — SERS uses independent market valuation plus allowances rather than a negotiated collective price. SERS is also not taxable (no capital gains tax in Singapore), and no SSD is triggered by the compulsory acquisition.

What happens to my flat if neither SERS nor VERS applies and the lease runs out?

At the end of the 99-year lease, the leasehold interest expires and the flat reverts to the state (HDB/SLA) with no residual value or compensation. The flat owner and any occupants are required to vacate. This is the theoretical outcome for HDB flats that do not receive SERS or VERS and that are not otherwise redeveloped by HDB through other means. As at 2026, no HDB flat has yet reached its lease expiry (the earliest HDB flats from the 1960s have leases expiring around 2060+), so this remains a future scenario rather than an observed one. However, the declining value trajectory for short-lease flats — well documented in URA and HDB resale transaction data — is consistent with the market pricing in this eventual zero-residual-value outcome.

Related Articles

- Singapore HDB Lease Top-Up Guide 2026: Eligibility, Premium Costs and How to Apply

- HDB Minimum Occupation Period (MOP) Singapore 2026: Complete Guide

- HDB Loan vs Bank Loan Singapore 2026: Which Saves You More?

- Singapore Strata-Titled Landed Property Guide 2026: Cluster Houses, MCST and Stamp Duties

- Singapore Annual Property Tax Guide 2026: Annual Value, IRAS Rates and 2026 Rebate

- Singapore Seller’s Stamp Duty (SSD) 2026: New 4-Year Holding Period and Rates Explained

- Singapore CPF Housing Grant Guide 2026: EHG, PHG and Family Grant Explained

- Singapore HDB BTO Application Guide 2026: Eligibility, Balloting and Key Collection

Disclaimer

This article is intended as a general educational resource only and does not constitute financial, legal, or property investment advice. SERS eligibility, compensation packages, timelines, and policies are subject to change by HDB at any time. All figures and descriptions reflect LovelyHomes’ understanding as at June 2026 based on publicly available information. Readers should consult HDB directly at www.hdb.gov.sg, IRAS at www.iras.gov.sg, and the CPF Board at www.cpf.gov.sg for current and authoritative information. Engage a licensed property agent or solicitor for advice tailored to your circumstances. Past SERS outcomes do not guarantee future selection or compensation levels.