HDB June 2026 BTO Launch: 6,900 Flats Across 5 Towns — Complete Buyer’s Guide

Quick Answer

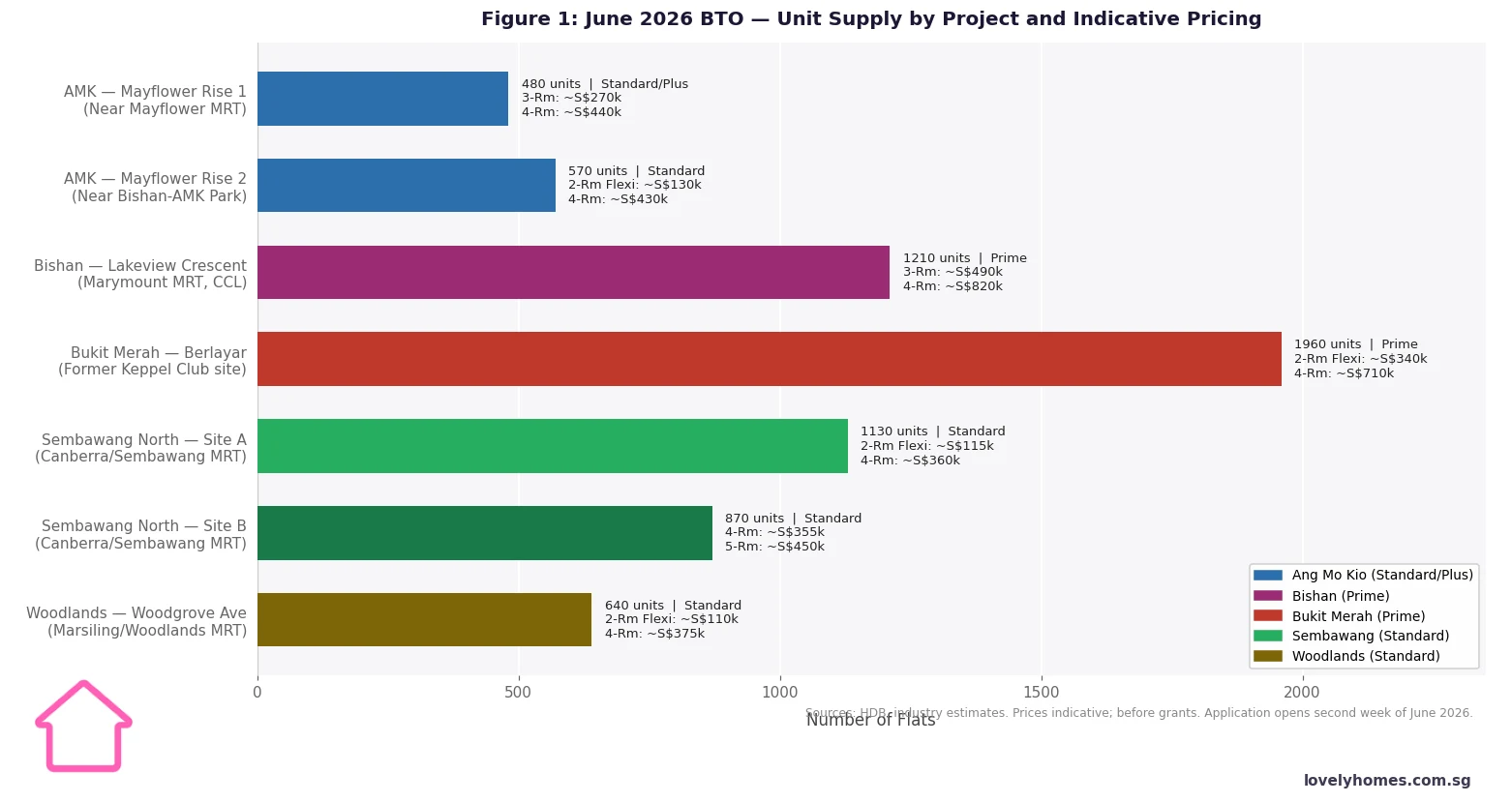

- The June 2026 BTO exercise will offer approximately 6,900 flats across 7 projects in 5 towns: Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands. The application window opens in the second week of June 2026.

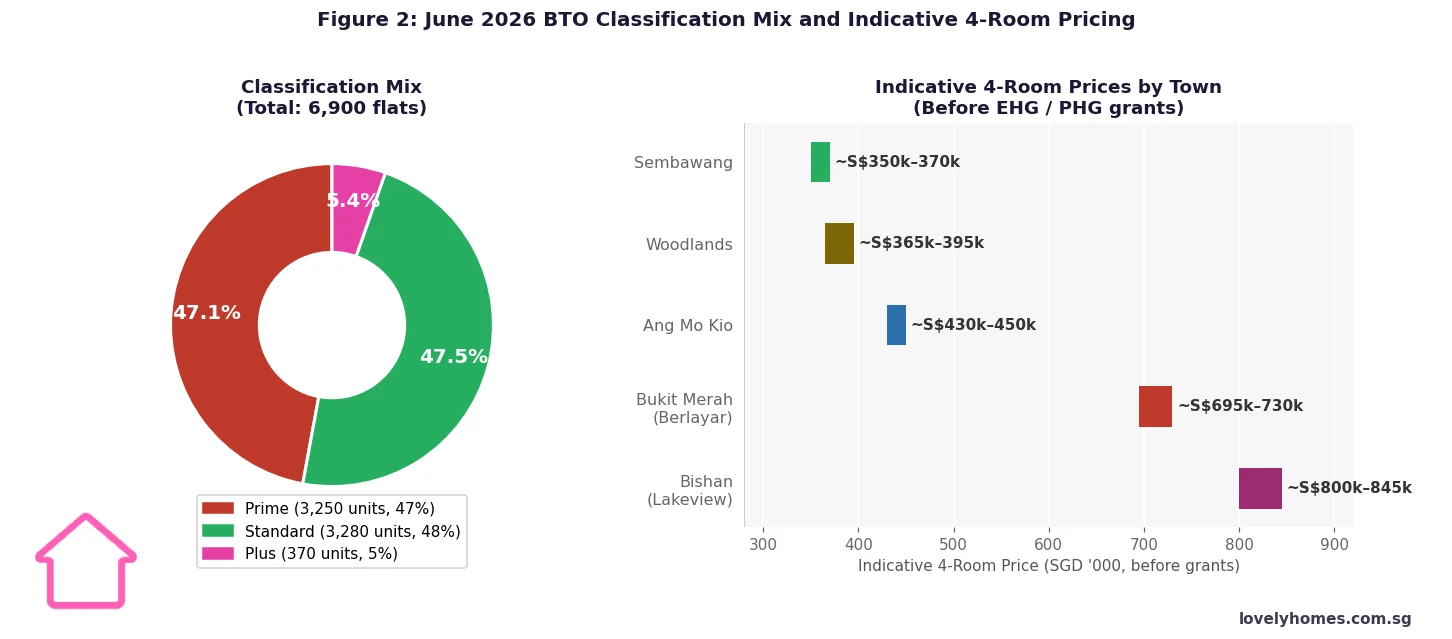

- Nearly half the supply (approximately 3,250 units, or 47%) is classified as Prime — concentrated in Bishan (Lakeview Crescent) and Bukit Merah (Berlayar). Prime flats carry a 10-year MOP, SC-only resale, and a subsidy clawback on first resale.

- Bishan — Lakeview Crescent is the headline project: the first new HDB development in Bishan in over 40 years, near Marymount MRT. Indicative 4-room prices are approximately S$820k before grants. Classified as Prime.

- Berlayar (Bukit Merah) offers 1,960 units on the former Keppel Club site. Indicative 4-room: approximately S$710k. Classified as Prime.

- Sembawang North offers the largest Standard supply (~2,000 units) at the most affordable prices — indicative 4-room from approximately S$350k before grants, with full EHG eligibility.

- First-timer SC households earning up to S$9,000/month qualify for the Enhanced Housing Grant (EHG) of up to S$120,000 on Standard and Plus flats.

- Ballot results are expected approximately 3 weeks after the application window closes, with flat selection appointments typically following 1–2 months later.

Overview: What Is on Offer in June 2026

The June 2026 BTO exercise is the second of three sales exercises HDB has planned for 2026, following the February 2026 exercise (4,692 flats) and ahead of the October 2026 exercise. At approximately 6,900 flats, it is the largest of the three 2026 tranches and includes some of the most sought-after locations in years — particularly the Bishan and Bukit Merah (Berlayar) projects.

HDB will launch the exercise on its HDB Flat Portal in the second week of June 2026. Potential buyers should prepare eligibility documents — including income declaration and citizenship verification — in advance, as these must be on file before a successful application can proceed to booking.

Project-by-Project Analysis

Bishan — Lakeview Crescent (~1,210 units, Prime): This is the standout project of the exercise and arguably the most significant HDB launch in years. Bishan last received new BTO flats in 1984 — a gap of over 40 years. Lakeview Crescent sits near Marymount MRT (Circle Line) adjacent to the vast Bishan-Ang Mo Kio Park. CCL connectivity is excellent: Marymount to Dhoby Ghaut interchange in three stops, to Marina Bay in approximately seven. Blue-chip schools in the catchment include Catholic High School and St Gabriel’s Primary. Being classified Prime, it carries a 10-year MOP, income ceiling on resale, SC-only resale pool, and a subsidy clawback. Indicative 4-room: approximately S$820k before grants (EHG not available for Prime).

Bukit Merah — Berlayar (~1,960 units, Prime): Located on the former Keppel Club site off Telok Blangah Road, adjacent to the Southern Ridges nature corridor. Nearest MRT: Labrador Park or Telok Blangah (CCL). Unit mix is heavy on 4-room (~980) and 2-room Flexi (~810). Classified Prime: 10-year MOP, SC-only resale. Indicative 4-room: S$695k–S$730k. Strong lifestyle appeal for those who value the Southern Ridges and Harbourfront precinct.

Ang Mo Kio — Mayflower Rise (~1,050 units, Standard/Plus): Two projects near Mayflower MRT (Thomson-East Coast Line). Project 1 (480 units, Plus) near CHIJ St Nicholas Girls’: 3-room and 4-room at ~S$440k. Project 2 (570 units, Standard) near Bishan-AMK Park: 2-room Flexi and 4-room at ~S$430k. TEL provides direct access to Orchard Road and Marina Bay without interchange. EHG eligible for Standard project.

Sembawang North (~2,000 units, Standard): Largest town supply, most affordable pricing. Two projects near Canberra and Sembawang MRT (NSL). Indicative 4-room: S$350k–S$370k before EHG. Full EHG eligibility for qualifying households. Site A includes eating house, minimart, preschool, Residents’ Network Centre.

Woodlands — Woodgrove Avenue (~640 units, Standard): Moderate supply near Marsiling/Woodlands MRT (NSL). Indicative 4-room: ~S$375k before grants. Woodlands Regional Centre is undergoing long-term transformation as a northern business hub.

Classification Mix and Ballot Strategy

The June 2026 exercise is polarised: 47% Prime (Bishan + Berlayar), 48% Standard (Sembawang + Woodlands + AMK Project 2), and just 5% Plus (AMK Project 1). Buyers who need to sell or upgrade within five to eight years should avoid Prime flats — the 10-year MOP is a genuine life commitment and the subsidy clawback at resale partially offsets the apparent price advantage.

For Standard and Plus flats, first-timer SC applicants receive 95% of ballot queue allocations. Demand for Standard flats in Sembawang and Woodlands is historically more moderate than for central locations, improving odds for applicants who are flexible on location.

Summary Table: June 2026 BTO at a Glance

| Town / Project | Units | Class | MOP | Indicative 4-Rm | Nearest MRT |

|---|---|---|---|---|---|

| AMK Mayflower Rise 1 | 480 | Plus | 10 yr | ~S$440k | Mayflower (TEL) |

| AMK Mayflower Rise 2 | 570 | Standard | 5 yr | ~S$430k | Mayflower (TEL) |

| Bishan Lakeview Crescent | 1,210 | Prime | 10 yr | ~S$820k | Marymount (CCL) |

| Bukit Merah Berlayar | 1,960 | Prime | 10 yr | ~S$710k | Labrador Pk (CCL) |

| Sembawang North A | 1,130 | Standard | 5 yr | ~S$360k | Canberra (NSL) |

| Sembawang North B | 870 | Standard | 5 yr | ~S$360k | Canberra (NSL) |

| Woodlands Woodgrove Ave | 640 | Standard | 5 yr | ~S$375k | Marsiling (NSL) |

| Total | ~6,860 | 47% Prime · 48% Standard · 5% Plus | |||

Worked Example: The Lim Couple Comparing Sembawang vs Bishan

Mr and Mrs Lim are both Singapore Citizens aged 30, applying as first-timers for the June 2026 BTO. Combined household income: S$7,000/month. They are comparing a Sembawang North Standard 4-room at S$360,000 versus a Bishan Lakeview Prime 4-room at S$820,000.

| Item | Sembawang Standard | Bishan Prime |

|---|---|---|

| Selling price (indicative) | S$360,000 | S$820,000 |

| EHG (income S$7,000/mth) | – S$20,000 | Not eligible (Prime) |

| Net price after EHG | S$340,000 | S$820,000 |

| CPF OA downpayment (20%) | S$68,000 | S$164,000 |

| HDB loan (80%, 25-yr, 2.60%) | S$272,000 | S$656,000 |

| Monthly instalment (HDB loan) | ~S$1,230 | ~S$2,966 |

| MSR check (30% of S$7,000) | PASS (S$2,100 limit) | FAIL (exceeds S$2,100) |

| MOP duration | 5 years | 10 years |

| Earliest eligible to sell | ~2031 | ~2036 |

| Resale eligibility after MOP | SC/SPR buyers | SC only (income ceiling) |

The MSR check reveals an important constraint: the Lim couple on S$7,000/month can borrow at most 30% × S$7,000 = S$2,100/month via an HDB loan. On the Bishan Prime flat, the required monthly instalment of ~S$2,966 exceeds this limit — meaning an HDB loan is insufficient and a bank loan would be required (subject to TDSR and prevailing rates). On the Sembawang Standard flat, the monthly instalment of ~S$1,230 easily clears the MSR, leaving S$870/month in MSR headroom for other debts. For a first-timer couple with moderate income, the Sembawang Standard flat is clearly the financially sound choice.

What Happens After You Apply

The BTO application process follows HDB’s standard sequence: applicants submit via the HDB Flat Portal within the application window (second week of June 2026, approximately one week long) and pay a S$10 application fee. Ballot results are typically released 3 weeks after the window closes. First-timers receive 95% of ballot queue allocation. Applicants with a queue number are called for flat selection in order — upon selecting a unit, a booking fee of approximately S$2,000 is payable. Key collection for June 2026 flats is estimated in the 2029–2030 range, depending on project and contractor progress.

Related Articles

- June 2026 BTO Launch Preview: 6,900 Flats Across 7 Projects in 5 Towns

- HDB Minimum Occupation Period (MOP) Singapore 2026: Standard, Plus and Prime Explained

- HDB Plus and Prime Flats Singapore 2026: What the BTO Classification Means for Buyers

- Enhanced Housing Grant (EHG) Singapore 2026: Who Qualifies and How to Apply

- HDB BTO Application and Ballot System Singapore 2026: Priority Schemes and Ballot Odds

- Upgrading from HDB to Private Property Singapore 2026: Cost, ABSD and Timing

Frequently Asked Questions

When does the June 2026 BTO application window open?

The application window is expected to open in the second week of June 2026 for approximately one week. HDB will announce the exact dates on the HDB Flat Portal (homes.hdb.gov.sg). There is no advantage to applying on the first day — all applications within the window are treated equally in the computer ballot. Prepare eligibility documents (income declaration, citizenship, prior HDB ownership history) before the window opens to avoid delays.

Is the Bishan Lakeview Prime flat worth the premium?

For a SC couple in their late 20s to early 30s with stable employment and no plans to move for at least 10 years, Bishan Lakeview at approximately S$820k is excellent value relative to nearby private condo prices of S$1.8M–S$2.5M. The Circle Line connectivity and park access are genuine quality-of-life advantages. The 10-year MOP is the key constraint — if there is any chance of needing to upgrade, downsize, or relocate internationally within a decade, a Standard flat is the more prudent choice. Buyers should also confirm they can satisfy the Mortgage Servicing Ratio (30% of income cap) at the Bishan price point before applying.

Can SC-SPR couples apply for the June 2026 BTO?

Yes. An SC-SPR household is eligible to apply for HDB BTO flats as a family nucleus. For Plus and Prime flats, the SC member’s status governs the resale conditions — the SPR spouse co-owns but the SC-only resale restriction (Prime) or income ceiling (Plus/Prime) applies when the flat is later sold. Both spouses’ incomes are counted for grant eligibility and MSR purposes.

Can I apply for two June 2026 BTO projects?

No. Each household may submit only one BTO application per exercise. If unsuccessful or if no suitable unit remains in the ballot, you receive enhanced priority (deferred applicant status) in the next exercise.

Are Prime flats eligible for the EHG grant?

No. Enhanced Housing Grant (EHG) is not available for Prime BTO flats. The EHG is designed to make Standard and Plus housing affordable for middle-income first-timers; Prime flats already carry a significant built-in subsidy through their pricing. The Proximity Housing Grant (PHG) — which gives S$20k–S$30k for buying near parents — is available for Prime flats. Verify the latest grant conditions directly with HDB at the time of application.

Disclaimer: This article is for general information only. All pricing is indicative and based on publicly available industry estimates as at 16 May 2026; actual selling prices will be released by HDB at the time of launch. Grant eligibility and amounts are subject to HDB review and may change. Always verify the latest requirements at hdb.gov.sg before making housing decisions. Monthly instalment figures are illustrative only.