HDB Upgrader’s Complete Guide 2026: From HDB Flat to Private Property

- MOP first: You must fulfil the Minimum Occupation Period (5 years for most flats; 10 years for Prime and Plus flats launched from August 2024) before selling your HDB flat on the open market or buying a private residential property while retaining the flat.

- Two upgrade strategies: “Sell first, buy later” avoids ABSD on your private purchase (you are a first-time private buyer). “Buy first, sell later” triggers 20% ABSD on the private property for SCs — S$270,000 on a S$1.35M condo — though an ABSD remission is available if you sell within 6 months.

- CPF refund: When you sell your HDB flat, all CPF OA monies used for the purchase — plus accrued interest — must be refunded to your CPF account. The net cash you receive is the sale price minus the outstanding HDB loan (if any) and the CPF refund.

- Grant repayment: CPF Housing Grants (EHG, Family Grant, etc.) used for the HDB flat do not need to be repaid upon sale — they are subsumed into the CPF OA refund.

- HDB loan discharged on sale: The HDB loan is discharged at the point of the flat sale. Any outstanding balance is deducted from the sale proceeds before cash is released.

- Private property financing: After selling your HDB flat, you are eligible for a bank loan of up to 75% LTV for a private property purchase. You cannot use an HDB concessionary loan for private property.

- ABSD remission (SC married couples): If you buy a private property before selling your HDB flat, you can claim an ABSD refund if the HDB flat is sold within 6 months of completing the private purchase.

Who is an HDB Upgrader?

In Singapore’s property lexicon, an HDB upgrader is a flat owner — typically a Singapore Citizen couple who purchased a Housing & Development Board flat as their first home — who subsequently wishes to sell the flat and purchase a private residential property. The upgrade journey is one of the most significant financial decisions many Singaporeans make: it unlocks accumulated HDB equity, introduces bank mortgage financing (with its stricter credit requirements), and subjects the buyer to ABSD unless the timing is managed carefully.

The upgrader market is a structural pillar of Singapore’s private residential demand. According to the Urban Redevelopment Authority (URA), HDB upgraders historically account for 30–40% of new private condominium sales in Outside Central Region (OCR) developments. Policy levers — chiefly ABSD and MOP duration — are calibrated in part to pace the rate at which HDB flat owners enter the private market.

Understanding the mechanics of the upgrade journey — from MOP completion to key collection — is essential to avoid costly timing errors, particularly the S$270,000+ ABSD cash outlay that catches many upgraders off guard.

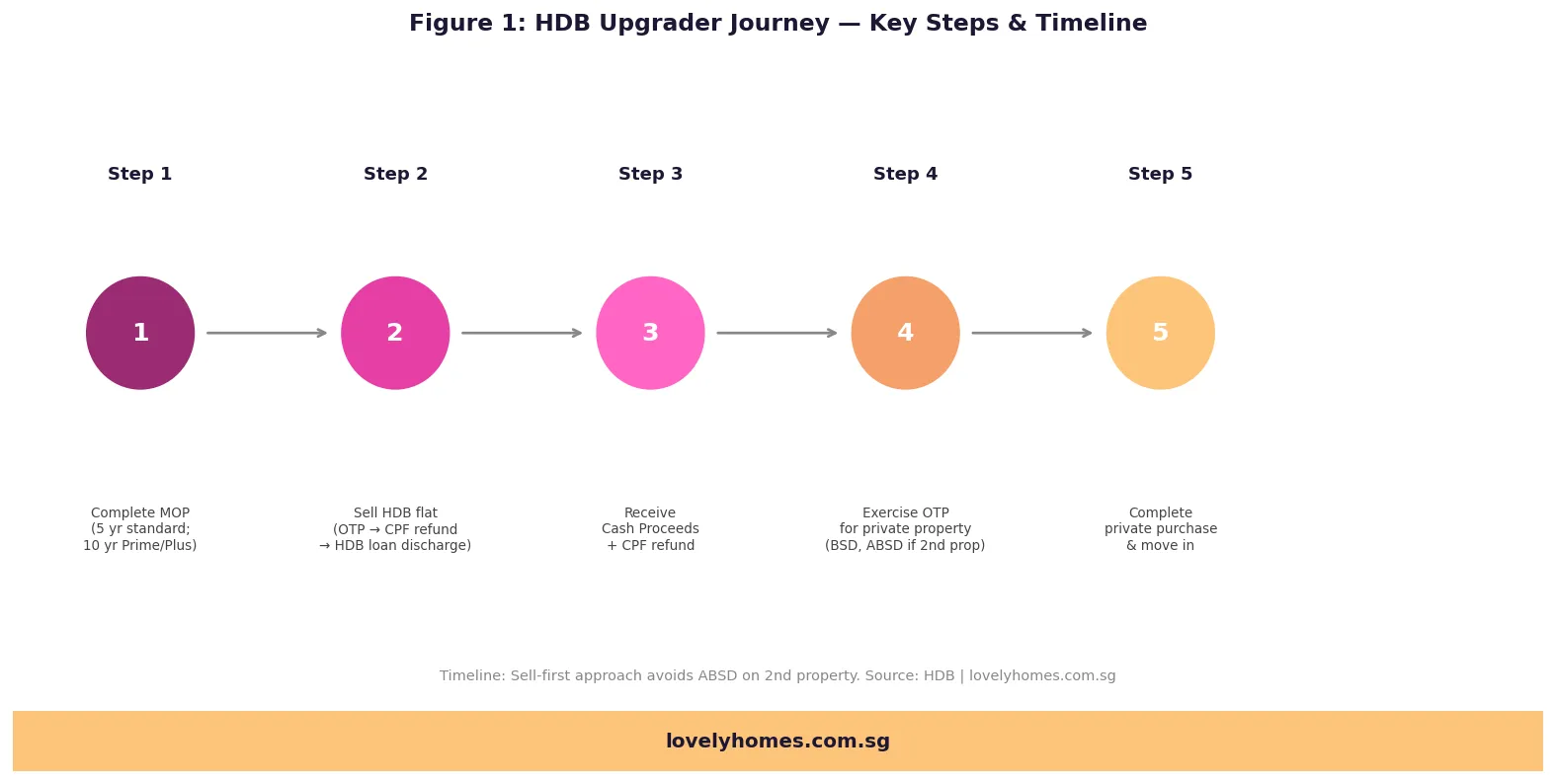

Step 1: Confirm Your MOP Status

The Minimum Occupation Period (MOP) is the period during which an HDB flat owner must occupy the flat as their principal residence before they are permitted to sell it on the open market or to purchase a private residential property.

The standard MOP is 5 years from the date the keys are collected (the date of possession), not from the date the sale was exercised or the mortgage was drawn. The MOP clock stops if the flat is rented out in full, if the flat owner stays overseas for extended periods, or in other prescribed circumstances — so owners who sublet their flat prematurely may find their effective MOP extended.

For Prime and Plus classification flats launched from August 2024 onwards under the new HDB classification framework, the MOP is 10 years, and additional ownership restrictions apply (including an income ceiling on resale buyers and a clawback provision on subsidy). Owners of these flats face a longer upgrader journey.

Figure 1: The HDB upgrader’s journey — five key steps from MOP completion to private property key collection. Source: HDB | lovelyhomes.com.sg

Step 2: Understand What You Will Receive from the HDB Sale

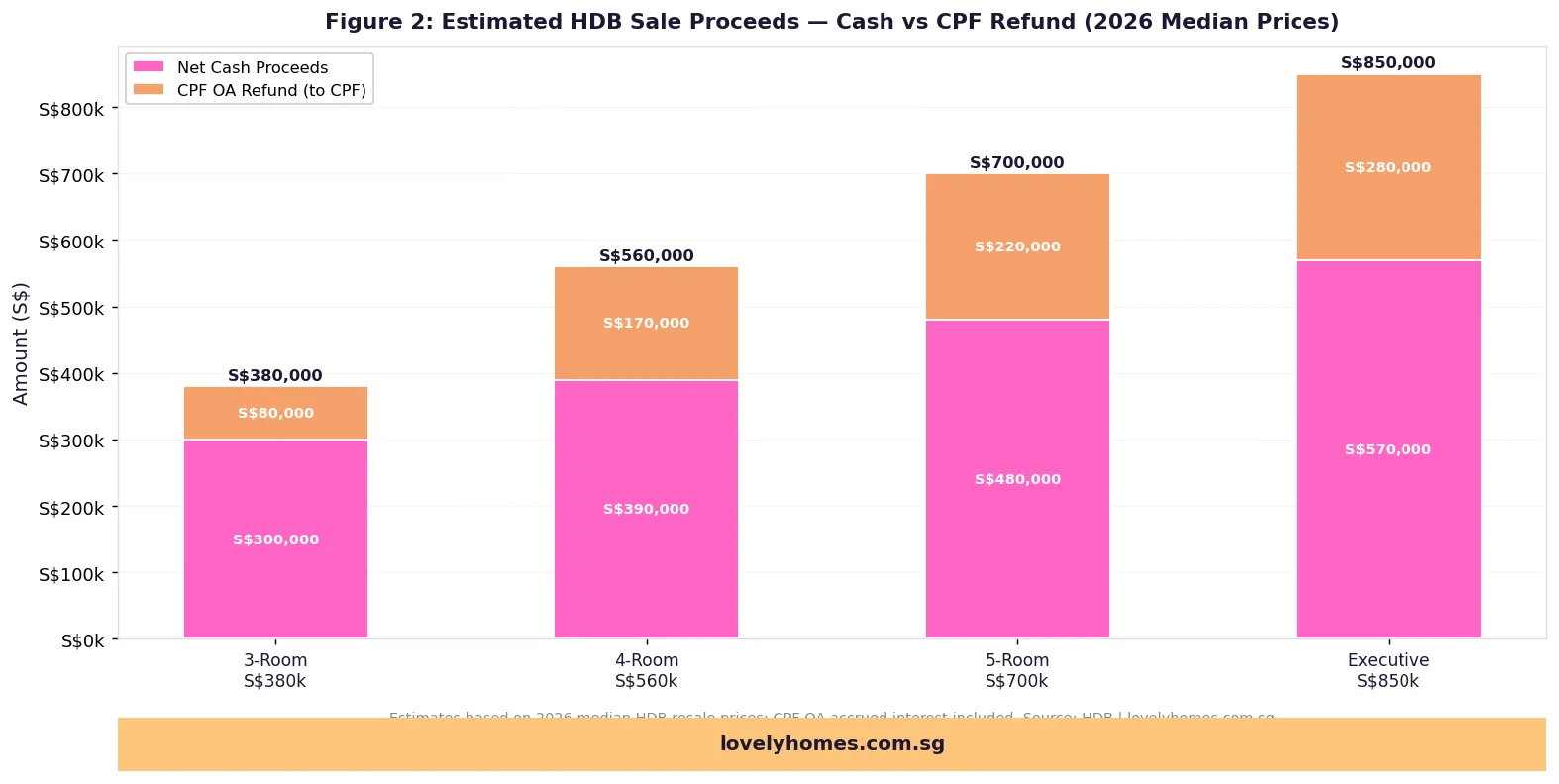

The sale of your HDB flat generates two streams of value: a cash component and a CPF refund. The distinction matters enormously for financial planning, because the CPF refund goes back into your CPF Ordinary Account — it cannot be used freely as cash, though it can be used for the down payment and stamp duty on your subsequent private property purchase.

The CPF OA refund comprises: (a) the principal CPF OA amount withdrawn for the flat, and (b) accrued interest — the notional interest CPF Board charges on those withdrawn funds at the CPF OA rate (currently 2.5% p.a. on the first S$20,000 of OA, 3.5% p.a. thereafter, effective 1 January 2024). Accrued interest compounds over the full holding period and can be significant: on S$150,000 CPF withdrawn over 8 years, accrued interest at 2.5% compounding amounts to approximately S$34,000.

Figure 2: Estimated HDB sale proceeds by flat type — cash component vs CPF OA refund, based on 2026 median resale prices. Source: HDB | lovelyhomes.com.sg

If there is an outstanding HDB concessionary loan, the remaining balance is deducted from sale proceeds before cash is released to the seller. HDB loan interest rate is currently set at the CPF OA rate + 0.1% (i.e. approximately 2.6% p.a.), making it among the most competitive mortgage rates in Singapore — but flat owners who have used HDB loans extensively may find less net cash available after discharge.

Step 3: Decide on Your Upgrade Strategy — Sell First or Buy First?

The single most consequential decision in the upgrade journey is the sequencing of transactions: do you sell your HDB flat before purchasing the private property, or do you purchase first and sell after?

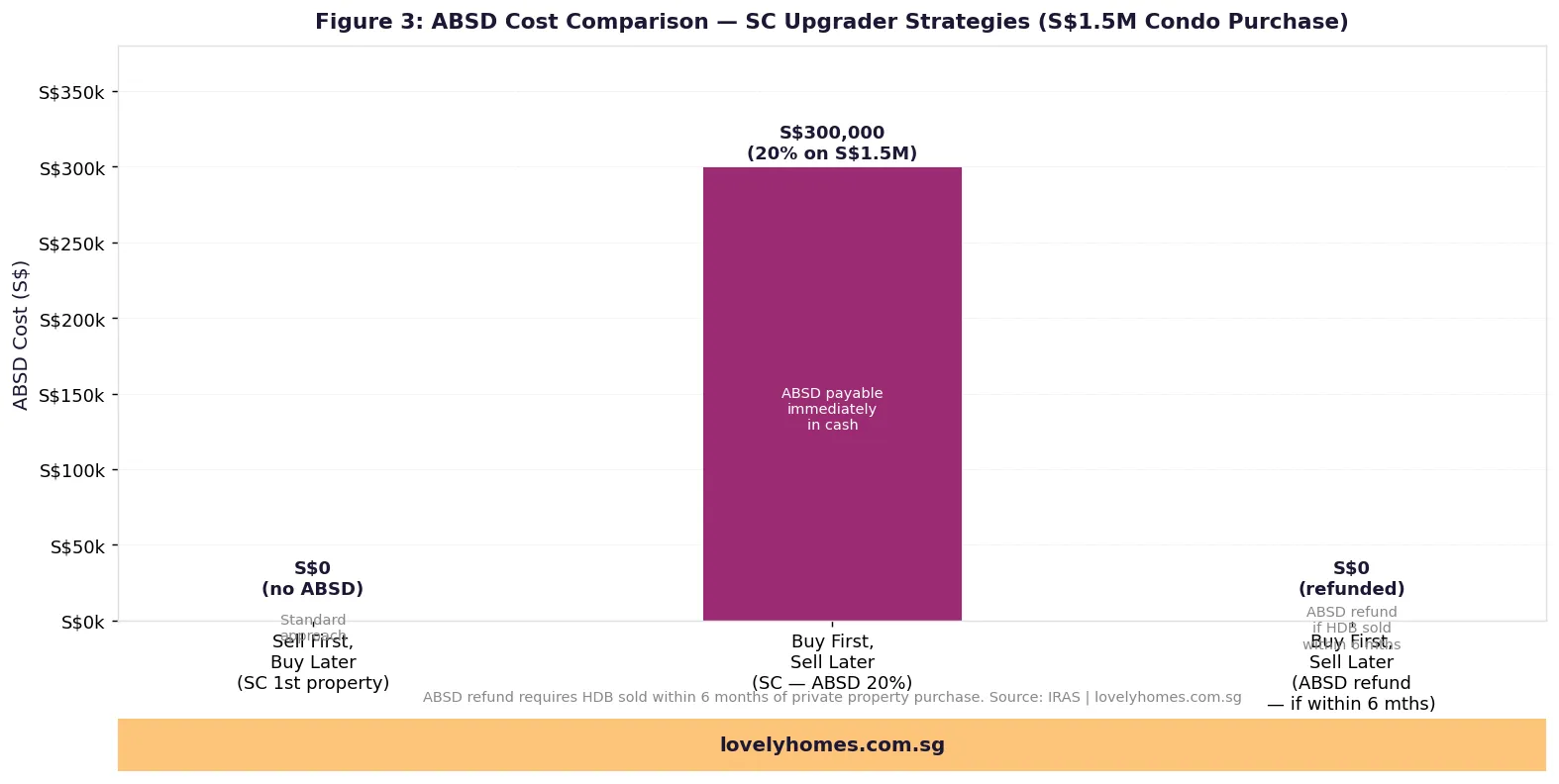

The sell-first strategy means you complete the sale of your HDB flat, receive the sale proceeds (cash + CPF refund), arrange interim accommodation (typically renting), and then purchase the private property as a first-time private-property buyer. The key advantage: you pay 0% ABSD on the private purchase (for SC buyers with no other property). The key risk: you may miss your preferred private property while searching for one during the rental period, and the private property market may move against you in the interim.

The buy-first strategy means you exercise an OTP on a private property while still owning the HDB flat, paying 20% ABSD on the private purchase price in cash. You then have 6 months from the date of completing the private property purchase (Legal Completion) to sell the HDB flat and apply for an ABSD remission refund from IRAS. If the HDB flat is sold within 6 months, IRAS refunds the ABSD paid (less a processing deduction of 0.1% p.p. on the refunded amount, effective from certain periods). If you miss the 6-month window, the ABSD is forfeited — a potentially catastrophic financial loss.

Figure 3: ABSD cost comparison — “sell first” avoids ABSD entirely; “buy first” triggers 20% ABSD but may be remitted if HDB flat sold within 6 months. Source: IRAS | lovelyhomes.com.sg

Summary Table: Key Upgrader Decision Points

| Decision Point | Sell First, Buy Later | Buy First, Sell Later (+ ABSD remission) |

|---|---|---|

| ABSD upfront | S$0 (first-time private buyer) | 20% on purchase price (e.g. S$270,000 on S$1.35M) — cash only |

| ABSD recovery | N/A — not paid | Refundable if HDB sold within 6 months of private completion |

| CPF available | Full CPF refund from HDB sale usable for private downpayment | CPF still tied up in HDB until flat sold |

| Accommodation | Must rent during search period | Can stay in HDB until private is ready |

| Market risk | Private prices may rise during rental period | Locks in private price; HDB sale price uncertainty |

| Bridge financing | Not required | May need bridging loan if cash-flow is tight |

| MOP Standard flat | 5 years from possession | 5 years from possession |

| MOP Prime/Plus flat | 10 years from possession | 10 years from possession |

Worked Example: The Tan Family Upgrade

Profile: Mr Tan (SC, 42) and Mrs Tan (SC, 40) own a 4-room HDB flat in Bishan, purchased in 2016 for S$470,000 using an HDB concessionary loan of S$376,000. MOP completed May 2021. Current market value: S$620,000. Outstanding HDB loan: S$92,000 (after 10 years of repayments). Total CPF OA withdrawn (both): S$185,000. Accrued CPF interest: S$42,000. Combined gross income: S$13,000/month.

HDB Sale proceeds:

- Sale price: S$620,000

- Less HDB loan discharge: S$92,000

- Less CPF refund (principal + accrued interest): S$227,000

- Net cash proceeds: S$301,000

- CPF OA balance after refund: S$227,000 (reusable for private purchase)

Target private property: 3-bedroom resale condominium in Bishan (D20), S$1,380,000.

Sell-first strategy (0% ABSD):

- BSD = 1% × S$180,000 + 2% × S$180,000 + 3% × S$640,000 + 4% × S$380,000 = S$1,800 + S$3,600 + S$19,200 + S$15,200 = S$39,800 (can use CPF OA)

- 25% down payment = S$345,000 (5% cash min = S$69,000; remaining S$276,000 from CPF OA)

- Available CPF OA after BSD: S$227,000 − S$39,800 = S$187,200 → cash shortfall of S$276,000 − S$187,200 = S$88,800 (to be covered by net cash proceeds S$301,000)

- Bank loan: 75% × S$1,380,000 = S$1,035,000 at 3.5% over 25 years → monthly S$5,183

- TDSR: S$5,183 / S$13,000 = 39.9% — PASS (well within 55% cap)

- Total cash outlay: S$69,000 (down) + S$88,800 (CPF shortfall) + S$0 ABSD + S$8,000 legal fees = ~S$165,800 in cash

Buy-first strategy (20% ABSD, remission expected):

- ABSD = 20% × S$1,380,000 = S$276,000 cash upfront (before HDB sale)

- The Tans must fund S$276,000 ABSD + S$345,000 down payment + S$39,800 BSD simultaneously — total cash need: S$660,800 at exercise. If their HDB sale is completed within 6 months of private legal completion, IRAS refunds S$276,000 ABSD (less 0.1% = S$275,724 net refund).

- Risk: HDB not sold within 6 months → S$276,000 lost.

Verdict: For the Tan family, sell-first is clearly superior — the net cash from HDB sale is sufficient to fund the private purchase without triggering ABSD, and TDSR is comfortably met. Buy-first requires bridge financing of ~S$660,000 simultaneously, which is feasible but expensive and risky if HDB sale stalls.

Why This Matters: Common Upgrader Mistakes

The three most expensive upgrader mistakes in Singapore each carry a six-figure price tag. First, miscounting the MOP: flat owners who sublet their entire flat for periods during the MOP — even with HDB approval — pause the MOP clock, sometimes discovering that their expected MOP date is later than they assumed. A single year’s delay translates into a year’s additional rent if the family has already moved out.

Second, assuming ABSD remission is automatic: the IRAS remission must be actively applied for, with evidence of the HDB sale completion. Families who miss the 6-month window — even by days — forfeit the remission entirely. Delays in HDB sale registration at the HDB Hub can erode the 6-month window; upgraders should build in a buffer and not list the HDB flat for sale at the last possible moment.

Third, ignoring CPF accrued interest: many upgraders are surprised to find that their CPF OA balance after the flat sale is materially lower than expected, because accrued interest — compounding for 5–10 years — has grown the CPF refund obligation substantially. This reduces the CPF available for the private property down payment and may require a larger cash component.

What Might Come Next: Policy Outlook for Upgraders

The Singapore government has shown a willingness to adjust ABSD policy in response to market conditions. The August 2024 introduction of the Prime and Plus HDB flat classification — with its 10-year MOP — signals an intent to slow the entry of Prime/Plus flat owners into the private market, preserving HDB estates as long-term communities rather than transient stepping-stones.

The ABSD remission for SC married couples remains in place as at July 2026. There is periodic market commentary that the 6-month window may be reduced if private prices accelerate — buyers should not rely on the remission window remaining unchanged. IRAS reviews the scheme in conjunction with broader cooling measure calibration.

On financing, MAS guidelines on TDSR and LTV have been stable since 2023. Any future tightening — such as a reduction in the 75% LTV cap for bank loans on private residential property — would increase the cash required for the down payment and could reduce upgrader demand at higher price points.

Frequently Asked Questions

1. Can I buy a private property while still in my HDB flat’s MOP?

No. HDB rules prohibit flat owners from owning or purchasing a private residential property in Singapore during the MOP. You must wait until the MOP is fully served before exercising an OTP on a private property. If you purchase a private property during the MOP, HDB may compulsorily acquire your flat. The prohibition covers direct ownership — owning shares in a company that owns private property is a separate issue and subject to its own rules.

2. Do I have to sell my HDB flat when I buy a private property?

No — you are not legally required to sell your HDB flat when you purchase a private property after MOP completion, provided you pay the applicable ABSD (20% for SC buying a 2nd residential property). Many upgraders choose to retain the HDB flat as a rental asset. However, renting out an HDB flat requires HDB approval, and both flat owners must be at least 35 years old (for non-family schemes). Also note: retaining both properties means the HDB flat rental income may affect TDSR calculations for the private property mortgage.

3. How long does an HDB resale typically take to complete?

An HDB resale transaction typically takes 8–12 weeks from the date an Option to Purchase (OTP) is granted to the HDB Hub’s completion and key handover. The process involves the HDB resale portal submission within 7 days of exercising the OTP, a First Appointment (HDB confirms eligibility), and a Second Appointment (key handover). Delays can occur if there are CPF accrued interest calculations to resolve, outstanding town council arrears, or if HDB flat type or scheme eligibility checks surface issues.

4. What is a bridging loan and when do upgraders need one?

A bridging loan is a short-term loan from a bank that covers the period between purchasing the new private property and receiving the proceeds from the HDB flat sale. Upgraders who adopt the buy-first strategy often need a bridging loan to fund the initial private property down payment (or ABSD, if applicable) before their HDB sale proceeds are available. Bridging loans in Singapore typically carry interest rates of 5–7% per annum and are repaid in full when the HDB sale is completed. They are a useful tool but add cost — every month the bridge is outstanding costs approximately S$400–S$500 per S$100,000 borrowed.

5. Can I use CPF OA from my HDB sale refund to pay the ABSD on my new private property?

No. ABSD must be paid entirely in cash — it cannot be funded from CPF OA. This is one of the most important cash-flow constraints in the upgrade journey. At S$270,000 ABSD on a S$1.35M private property, an upgrader using the buy-first strategy must have S$270,000 in cash available at the point of OTP exercise, in addition to the cash portion of the 25% down payment. CPF OA (including the refund from the HDB sale) can be used for the BSD and the down payment for the private property, but not for ABSD.

6. What happens if I cannot sell my HDB flat within 6 months for the ABSD remission?

If the HDB flat is not sold (legal completion of resale) within 6 months of the private property’s legal completion, the 20% ABSD paid upfront is forfeited — it is not refundable under any extension of time. IRAS does not grant extensions. If you have not yet found a buyer for the HDB flat and the 6-month deadline is approaching, you may need to price the flat more aggressively to accelerate the sale. This is why upgraders using the buy-first strategy typically list their HDB flat for sale as soon as they have exercised the OTP on the private property.

7. Are there any grants available to HDB upgraders buying private property?

No — CPF Housing Grants (EHG, Family Grant, Step-Up Grant, Singles Grant, Proximity Housing Grant) are only available for HDB flat purchases, not for private residential property. When you upgrade to a private property, you do not receive any government grant. The only financial assistance is the ability to use your CPF OA savings for the private property down payment and BSD, subject to the CPF Withdrawal Limit and Valuation Limit rules.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- HDB Minimum Occupation Period (MOP) Guide 2026

- Singapore Condo Resale Guide 2026: Step-by-Step Buyer’s Complete Guide

- HDB Resale Guide 2026

- HDB CPF Housing Grant Guide 2026: EHG, Family Grant, Step-Up & PHG Explained

- Buyer’s Stamp Duty Singapore 2026: BSD Rates & Calculator Guide

- HDB vs Condo Singapore 2026: Complete Comparison Guide

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or tax advice. ABSD rates, MOP requirements, CPF rules, HDB regulations, and financing policies are subject to change. Readers should verify current information with the relevant authorities — the Housing & Development Board (HDB) at hdb.gov.sg, the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg, the Central Provident Fund Board (CPF) at cpf.gov.sg, and the Monetary Authority of Singapore (MAS) at mas.gov.sg — and consult a licensed conveyancing solicitor and/or a registered estate agent before making any property transaction decisions.