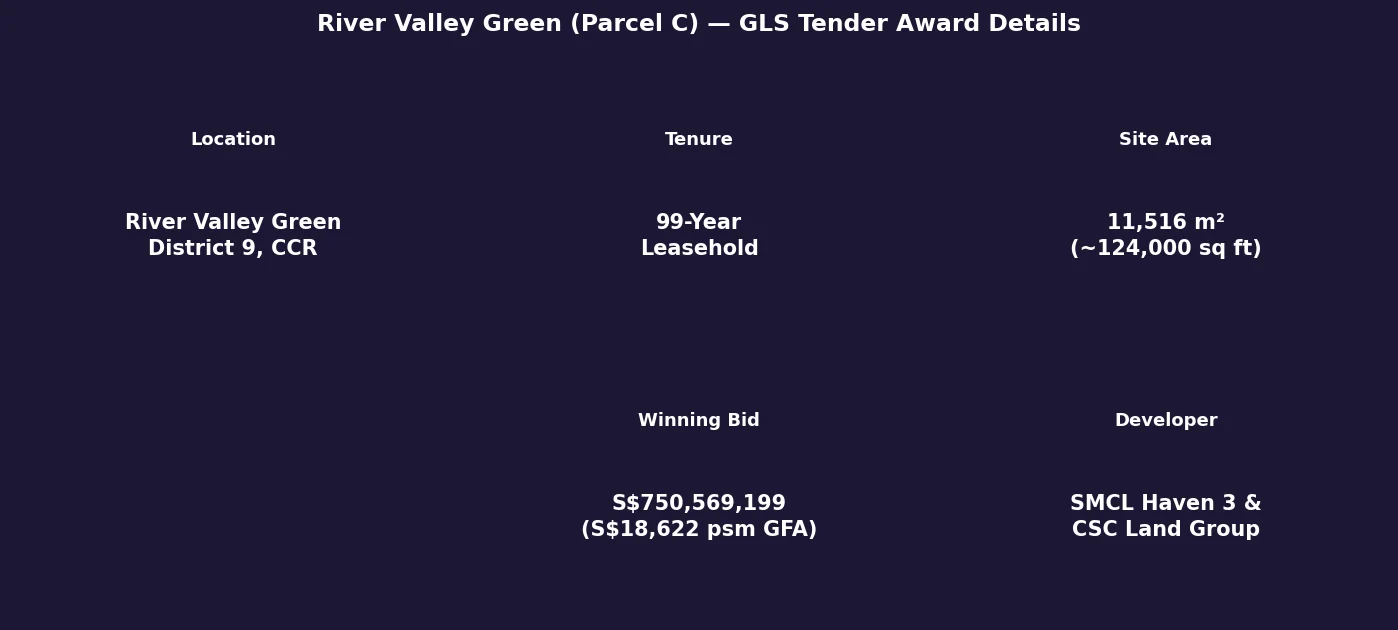

River Valley Green Parcel C: S$750.6M GLS Award — What It Means for CCR Property

⚡ Quick Answer — River Valley Green Parcel C Award

- The URA has awarded the River Valley Green (Parcel C) GLS tender to SMCL Haven 3 Pte. Ltd. and CSC Land Group (Singapore) Pte. Ltd. (URA pr26-48, 23 June 2026).

- The winning bid was S$750,569,199 — equivalent to S$18,621.77 per square metre of GFA.

- The site occupies 11,516 m² of land with a maximum permissible GFA of 40,306 m², on a 99-year leasehold tenure.

- The land rate of S$18,622 psm GFA translates to approximately S$1,730 per square foot of GFA — a benchmark that will inform CCR launch pricing from this developer.

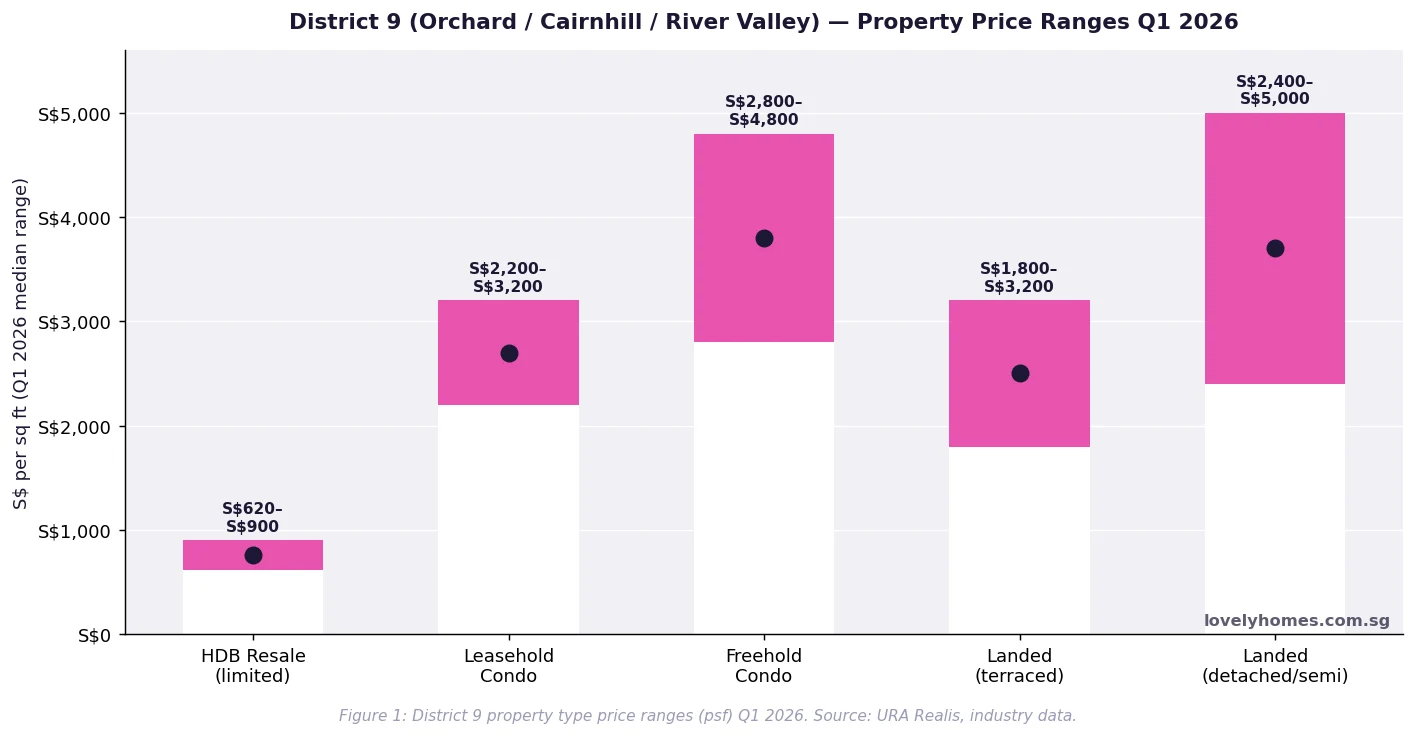

- Estimated breakeven for the developer (land + construction + carrying costs) points to launch prices in the range of S$3,200–S$3,800 psf, depending on unit mix and construction timeline.

- The River Valley Green precinct (D09 CCR) continues to attract firm developer conviction despite the elevated ABSD environment for foreign buyers.

URA Awards River Valley Green Parcel C for S$750.6 Million

The Urban Redevelopment Authority (URA) confirmed on 23 June 2026 that the Government Land Sales (GLS) tender for River Valley Green (Parcel C) has been awarded to SMCL Haven 3 Pte. Ltd. and CSC Land Group (Singapore) Pte. Ltd. — a joint-venture consortium — at a bid price of S$750,569,199, or S$18,621.77 per square metre of permissible gross floor area (GFA).

The site was launched for tender on 9 April 2026 as part of URA’s first-half 2026 Government Land Sales programme and closed for bids on 18 June 2026. The 99-year leasehold residential parcel is the third of three River Valley Green sites to be tendered by URA, completing the planned residential component of the River Valley Green development corridor adjacent to Alexandra Canal.

Site Specifications and Award Details

What the Land Rate Signals About the CCR Market

The S$18,621.77 psm GFA land rate is a significant data point for the Core Central Region (CCR) residential market. To contextualise: this rate implies a total land cost of approximately S$1,730 per square foot on GFA — before construction, financing, professional fees, and developer profit are factored in.

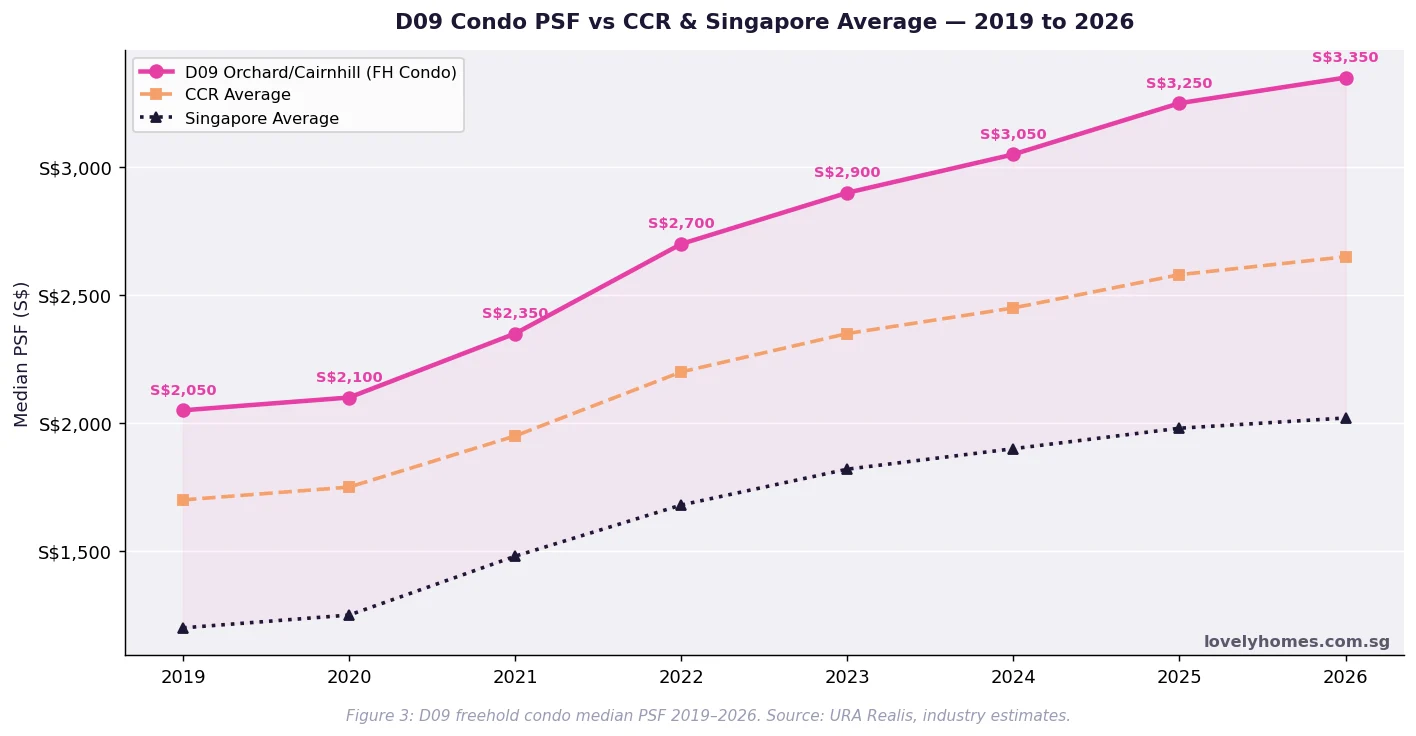

Industry estimates suggest a typical CCR high-end residential project carries total development costs (land + construction + fees + financing) of S$3,000–S$3,500 psf on GFA before profit. Applying a 15–20% developer margin, the anticipated launch price range for the future project is approximately S$3,200–S$3,800 psf. This range is consistent with the broader CCR pricing environment in 2026 (median S$2,500–S$3,800 psf depending on project age and location) and suggests developers continue to price in buyer demand from Singapore-based ultra-high-net-worth individuals and PRs, notwithstanding the 60% ABSD deterrent for foreign buyers.

The award contrasts with the broader narrative of cooling CCR volumes: while the number of new sale transactions in D09 has declined since the 2023 ABSD hike, absolute pricing has held firm. The S$750.6M bid is a vote of confidence that there is an addressable buyer base — primarily Singapore Citizens and PRs — willing to transact at S$3,200+ psf in the River Valley sub-district.

Context: The River Valley Green GLS Programme

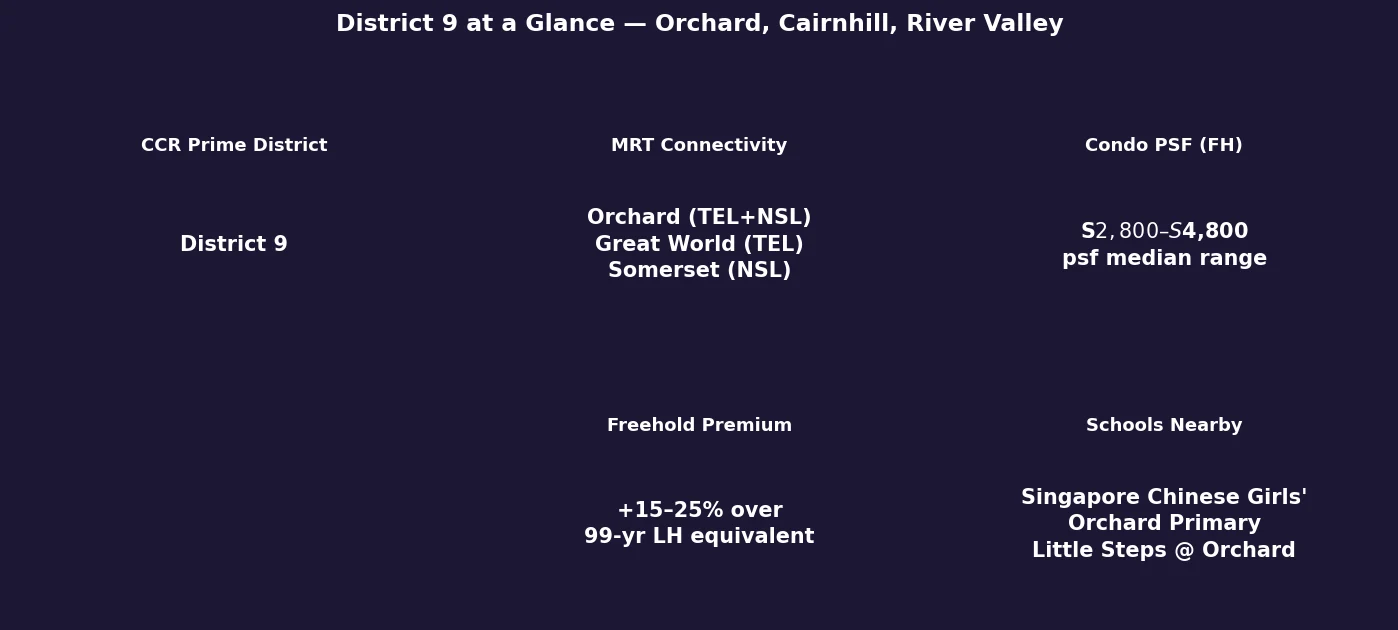

River Valley Green (Parcel C) is the final piece in a three-parcel residential GLS programme that URA has been releasing along the River Valley Green corridor. Earlier parcels in the same corridor attracted competitive bids, establishing a price trajectory for the sub-district. The proximity to the Great World MRT station (Thomson–East Coast Line), opened in 2022, has been a consistent factor cited by market participants in supporting GLS valuations along the Alexandra Canal fringe.

CSC Land Group is a Singapore-based developer with a portfolio spanning residential and mixed-use developments across the island. SMCL Haven 3 Pte. Ltd. is the project-specific SPV established for this joint venture. The choice of a joint-venture structure for a S$750M+ land parcel is consistent with Singapore market practice for managing capital concentration risk on large CCR sites.

Summary: River Valley Green Parcel C at a Glance

| Detail | Data |

|---|---|

| URA Press Release | pr26-48, 23 June 2026 |

| Site Location | River Valley Green (Parcel C), District 9 |

| Tenure | 99-Year Leasehold |

| Land Area | 11,516 m² (~124,000 sq ft) |

| Max Permissible GFA | 40,306 m² (~434,000 sq ft) |

| Winning Bidder | SMCL Haven 3 Pte. Ltd. & CSC Land Group (Singapore) Pte. Ltd. |

| Winning Bid (total) | S$750,569,199 |

| Bid Per PSM of GFA | S$18,621.77 |

| Bid Per PSF of GFA (approx.) | S$1,730 |

| Estimated Launch PSF (industry est.) | S$3,200–S$3,800 psf (subject to project planning) |

Frequently Asked Questions

What is a GLS tender and how does URA award it?

A Government Land Sales (GLS) tender is Singapore’s primary mechanism for releasing state land to private developers for residential or mixed-use development. Sites are offered on a Confirmed List (mandatory release within a programme period) or a Reserve List (released only when a developer triggers the tender by committing to a minimum bid). Bidders submit sealed tenders by a closing date; URA evaluates bids and awards to the highest qualifying tenderer, subject to a technical reserve price. The award is binding — developers must pay the full bid price and complete development within the stipulated period. The GLS programme is coordinated jointly by URA and the Singapore Land Authority (SLA).

What does this award mean for current River Valley property owners?

For owners of existing freehold and leasehold properties in the River Valley and Orchard fringe (D09), the S$18,622 psm GFA land rate provides a valuation signal. Developers will need to launch the future project at S$3,200–S$3,800+ psf to cover costs — which anchors new-launch comparable pricing in the precinct. Existing resale units in the River Valley sub-district typically trade at a 10–20% discount to new launches of equivalent specification, suggesting a price floor around S$2,800–S$3,400 psf for resale transactions near this site. However, each property is valued on its own merits, and owners should commission a formal valuation from a licensed appraiser before drawing conclusions about their specific unit.

When can buyers expect a new project launch from this site?

Based on typical Singapore residential development timelines — site planning approval (6–12 months), construction (3–4 years for a high-rise residential project) — a project launch from the River Valley Green Parcel C site could be expected in 2027–2028, with TOP (Temporary Occupation Permit) around 2030–2032. This is an estimate based on industry norms and is subject to the developer’s planning decisions, the Economic Development Board’s (EDB) permit process, and building construction pace. The developer has not yet made public announcements about the project name, unit mix, or launch timeline.

Is the 60% ABSD deterring foreign buyers from CCR new launches?

The 60% Additional Buyer’s Stamp Duty (ABSD) for foreign individuals, introduced in April 2023 (raised from 30%), has significantly reduced the proportion of foreign buyers in the CCR new launch market. URA data for 2023–2025 shows foreign purchases as a share of private residential transactions fell from roughly 7–8% (pre-2023) to under 3% post-ABSD hike. In dollar value terms, the deterrent is stark: a foreigner buying a S$4M CCR unit pays S$2.4M in ABSD alone. However, developers targeting the S$3,200–S$3,800 psf range for River Valley Green Parcel C are primarily underwriting to Singapore Citizen and PR demand — the ABSD regime makes foreign buyer demand a bonus rather than a base case for CCR projects launched post-2023.

How does this site compare to the Peck Hay Road GLS award?

The Peck Hay Road site (URA pr26-45, 16 June 2026) was awarded at a different psm GFA rate reflecting its distinct location, plot ratio, and site characteristics. Both sites are in the CCR (D09) and on 99-year leasehold tenure, but their proximity to MRT stations, site geometry, and view potential differ. River Valley Green Parcel C’s proximity to Great World MRT (TEL) is a key differentiator from the Peck Hay Road site, which is closer to the Orchard sub-precinct. Comparing land rates across sites of different specifications is useful for market context but should not be treated as a direct apples-to-apples benchmark.

Related Articles

- Orchard Road Singapore 2026: D09 Prices, Luxury Living & Investment Analysis

- Jurong Lake District White Site 2026: S$186k sqm GFA Development Opportunity

- URA Releases Lorong Puntong/Sin Ming Avenue and Kitchener Link GLS Sites

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Government Land Sales Guide 2026

Disclaimer

All figures in this article are sourced directly from URA press release pr26-48 (23 June 2026). Developer cost estimates, launch price projections, and valuation commentary are based on industry consensus estimates as at July 2026 and are speculative — they do not constitute a valuation or investment advice. Actual launch prices, project timelines, and market outcomes will depend on factors including developer decisions, construction costs, interest rates, and government policy. Readers should consult a licensed appraiser and property professional for advice specific to their circumstances. Official GLS data: ura.gov.sg/land-sales.

Click anywhere or press Esc to close