Bukit Batok Neighbourhood Guide Singapore 2026: HDB Prices, JRL and Investment Outlook

⚡ Bukit Batok at a Glance — Quick Answer

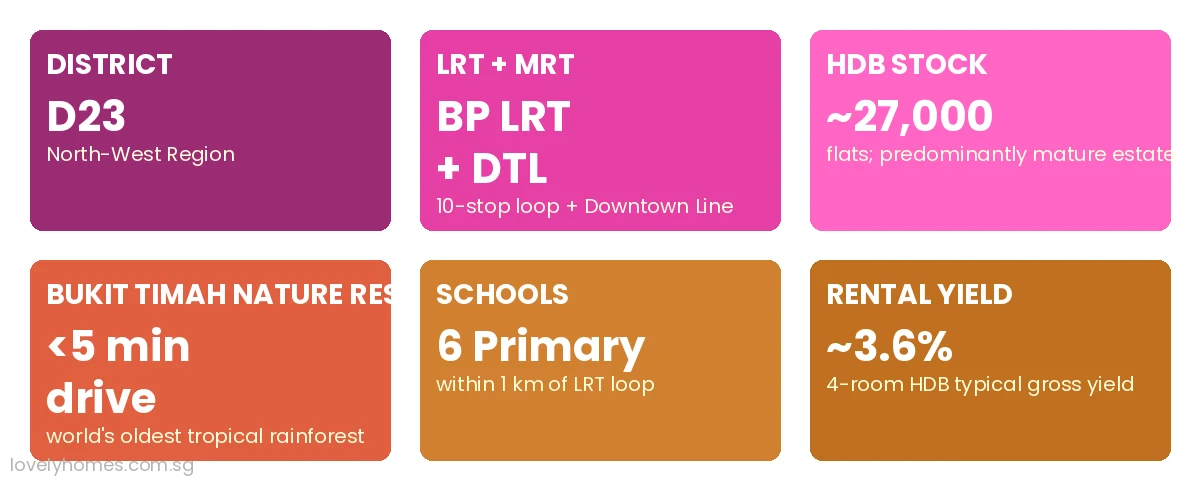

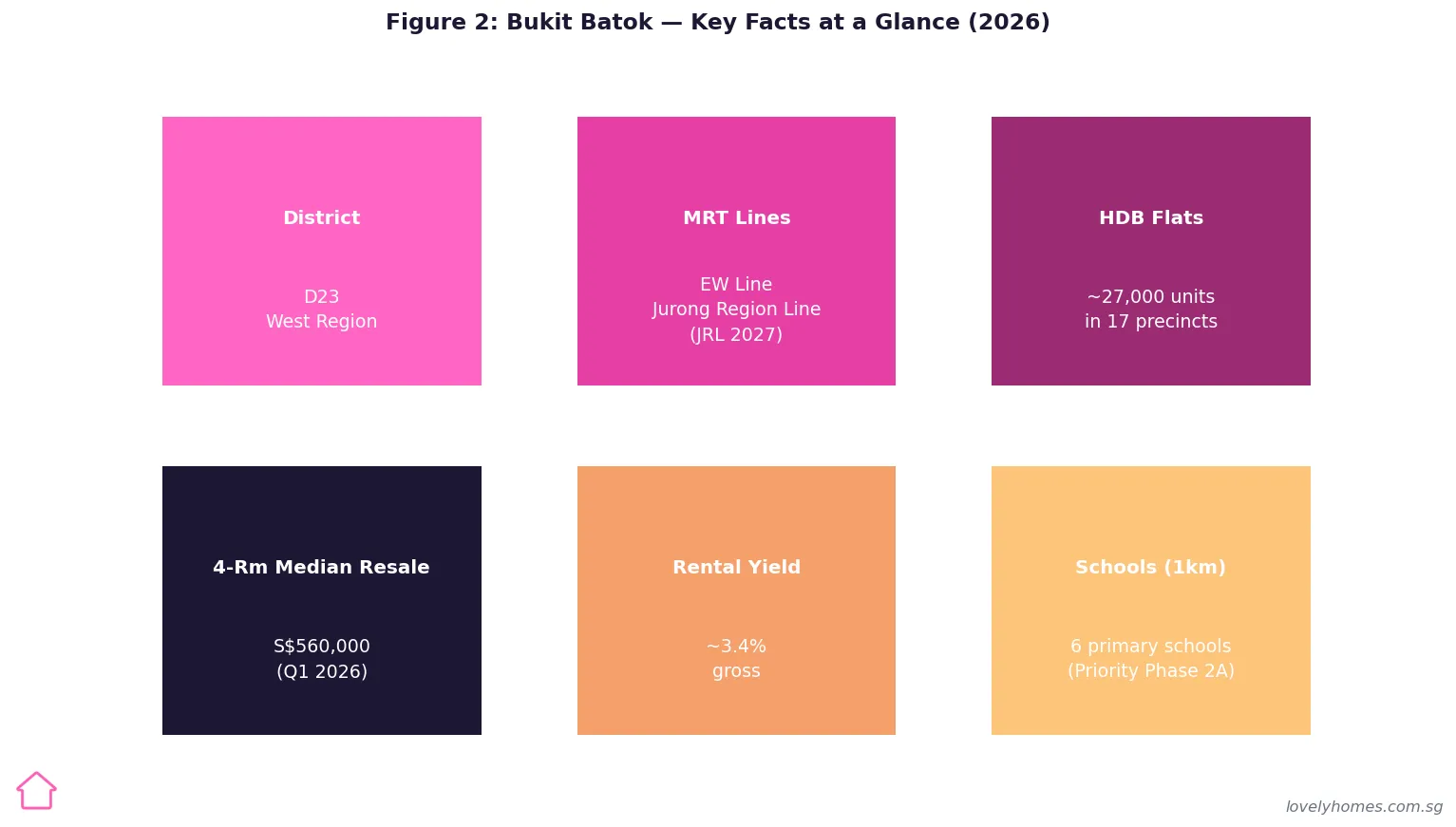

- District & Region: D23, West Region — predominantly HDB town with mature estate status and ~27,000 flats.

- Transport: EW Line (Bukit Batok MRT, Bukit Gombak MRT); Jurong Region Line opening 2027 adds two new stations at Tengah Park and Bahar Junction.

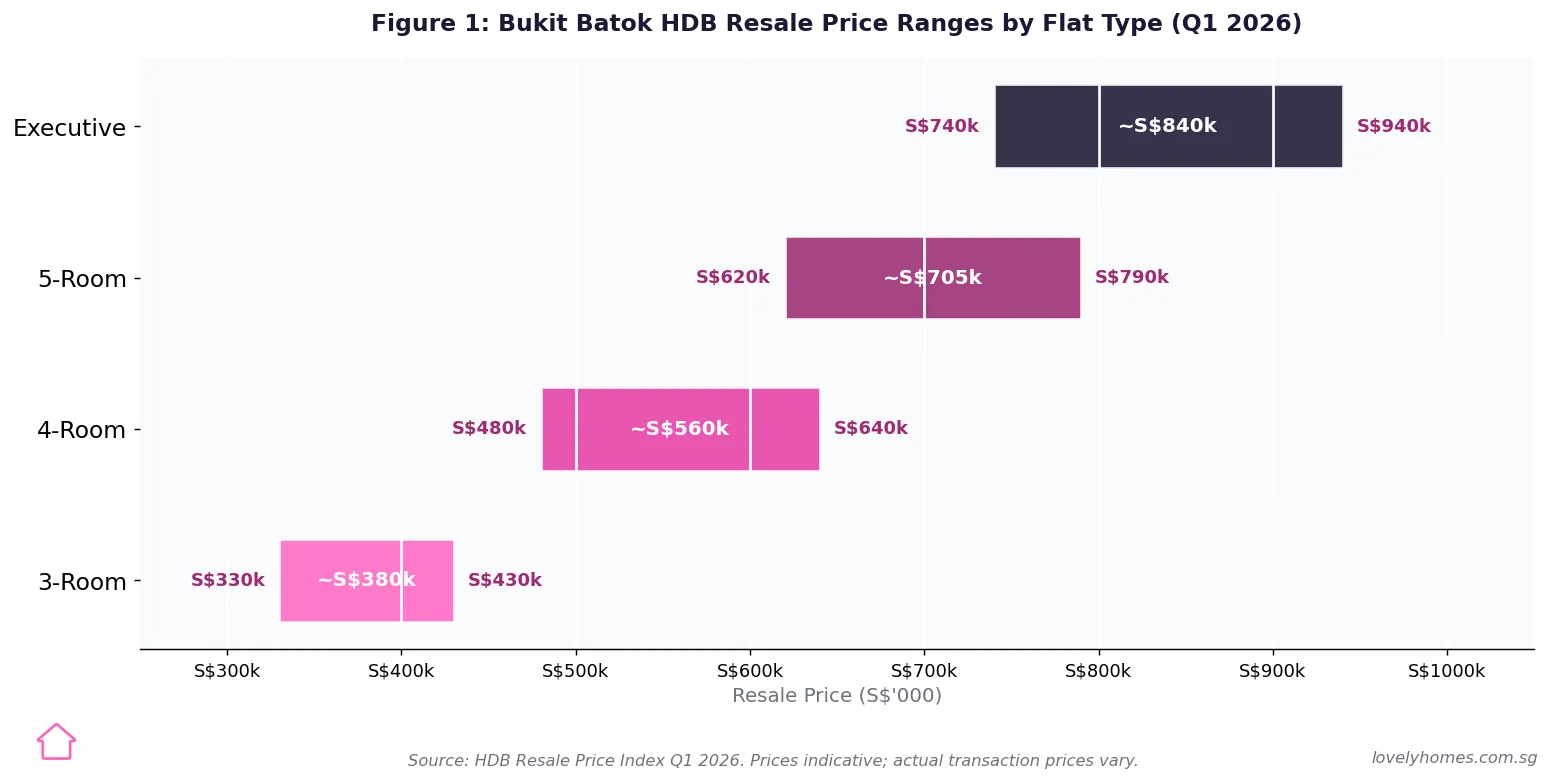

- HDB Resale Prices (Q1 2026): 4-room flats S$480k–S$640k; 5-room S$620k–S$790k.

- Private Condos: OCR pricing ~S$1,300–S$1,550 psf; notable projects include Le Quest, Altura EC, and West Scape.

- Rental Yields: ~3.2%–3.6% gross for HDB and condo units.

- Schools: Six primary schools within 1 km of most precincts, including Bukit Batok Primary, St. Anthony’s Primary, and Bukit View Primary.

- Key Catalysts: JRL Phase 1 (2027), Tengah new town development, and potential Bukit Timah–Dairy Farm masterplan uplift.

- Best For: HDB upgraders, first-time buyers seeking OCR value, and investors targeting yield over capital appreciation.

Tucked between Bukit Timah Nature Reserve and the emerging Tengah new town, Bukit Batok is one of Singapore’s most established yet persistently underrated residential precincts. Administered under the West Region of Singapore’s planning framework, it occupies District 23 (D23) alongside Choa Chu Kang — a zone that has historically traded at a meaningful discount to the Rest of Central Region (RCR) while offering mature estate infrastructure, abundant greenery, and very strong rental fundamentals.

For buyers in 2026, Bukit Batok presents a compelling proposition: the Jurong Region Line (JRL), delayed but now confirmed for Phase 1 opening in 2027, will add two stations directly serving the estate and cut travel times to Jurong Lake District (JLD) significantly. Combined with the Tengah “Forest Town” development next door — which will eventually add 42,000 new public and private housing units — Bukit Batok is positioned as a quiet beneficiary of Singapore’s largest urban transformation project since Punggol.

This guide covers everything buyers, renters, and investors need to know about Bukit Batok in 2026: HDB resale prices, private condo options, school landscapes, transport connectivity, and the investment thesis for the decade ahead.

Location and Transport Connectivity

Bukit Batok sits in the West Region of Singapore, bounded by Bukit Timah to the east, Jurong East to the south, Choa Chu Kang to the north, and the emerging Tengah planning area to the west. The estate is roughly 20–25 km from the Central Business District (CBD), placing it firmly in Outside Central Region (OCR) pricing territory.

MRT Access

Today, Bukit Batok is served by two East-West Line (EW) stations: Bukit Batok (EW27) and Bukit Gombak (EW28). Journey time to Jurong East (the regional hub) is two stops (~5 minutes); to City Hall, it is 25–30 minutes with no transfers. The Jurong Region Line (JRL), confirmed for Phase 1 opening in 2027, will introduce stations at Tengah Park and Bahar Junction within or adjacent to Bukit Batok’s boundary, connecting directly to the JLD White Site and the future Jurong-Tuas Corridor.

Road and Bus

Bukit Batok sits along the Bukit Timah Expressway (BKE) and is well-served by trunk bus routes to Jurong East, Clementi, and the CBD. Cycling infrastructure under the Bukit Batok Active Mobility Network connects residential precincts to Bukit Batok Nature Park and West Mall.

Housing Stock: HDB, Executive Condominiums and Private Condos

Bukit Batok is overwhelmingly a public housing town, with approximately 27,000 HDB flats distributed across 17 precincts — from Bukit Batok West Avenue 5 to Bukit Batok Crescent. The flat stock skews toward the 1990s and early 2000s, meaning most flats carry 67–75 years of remaining lease — generally comfortable for CPF usage and bank lending under current HDB and MAS rules.

Private residential supply is limited but growing:

- Le Quest (completed 2022): 516-unit mixed-development with a retail podium; one of the first integrated private-residential-commercial projects in Bukit Batok.

- Altura EC (2023 launch, under construction): 360-unit executive condominium on Bukit Batok West Avenue 8; the first EC in Bukit Batok in over a decade. Fully sold.

- West Scape: Smaller boutique private condo serving the Bukit Gombak catchment.

The limited private supply and proximity to Tengah — which will generate a substantial volume of new BTO launches — mean Bukit Batok’s HDB resale market is likely to face moderate upward price pressure over the next five to seven years as Tengah buyers seek established amenities nearby.

Property Prices and Rental Market in 2026

HDB Resale

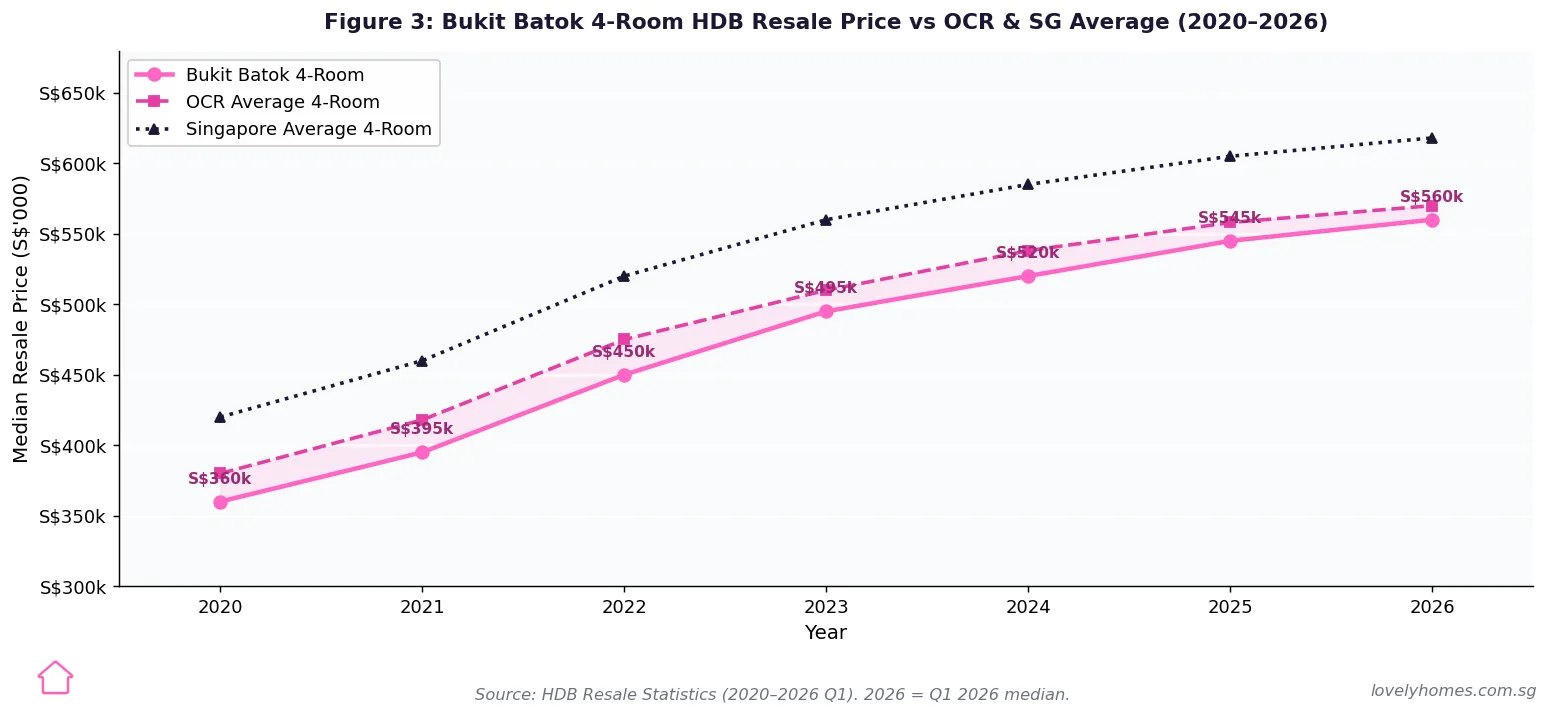

Bukit Batok HDB resale prices have appreciated steadily since 2020, driven by broad OCR resale market strength and limited new private supply. In Q1 2026, the median 4-room resale transaction in Bukit Batok stood at approximately S$560,000 — below the OCR average of S$570,000 and the Singapore-wide average of S$618,000, presenting a modest value opportunity for buyers comparing like-for-like. Five-room flats command S$620k–S$790k depending on location, floor, and remaining lease.

Private Condominiums

For private property, Bukit Batok / D23 transacts at S$1,300–S$1,550 psf for non-landed units — well below the RCR average (~S$2,100 psf) and meaningfully below Districts 21 and 22 despite comparable green surrounds. Le Quest’s resale units have traded in the S$1,380–S$1,520 psf range in 2025–2026, anchoring buyer expectations.

Rental Market

HDB rental demand in Bukit Batok benefits from proximity to the International Business Park and Jurong Lake District, which house a growing expat and professional workforce. Gross rental yields for 4-room HDB flats average ~3.2%–3.6%; private condos (Le Quest) yield ~3.0%–3.4% gross, broadly in line with OCR benchmarks.

Schools and Amenities

Primary Schools (within 1–2 km)

Bukit Batok has six primary schools within a 1 km radius of most residential precincts, giving families access to the HDB Priority Admission (Phase 2A) advantage:

- Bukit Batok Primary School

- Bukit View Primary School

- St. Anthony’s Primary School (Catholic; popular, competitive ballot)

- Dazhong Primary School

- Lianhua Primary School

- Hillgrove Secondary School (secondary)

Shopping and Lifestyle

Bukit Batok’s main retail node is West Mall (Bukit Batok MRT), a mid-sized mall anchored by Giant Hypermarket, Cathay Cineplexes, and a public library. The nearby Le Quest Mall adds a boutique lifestyle component. Residents are also within driving distance of Jurong Point (15 min), one of the largest suburban malls in Singapore. Nature assets include Bukit Batok Nature Park, Little Guilin (a scenic granite quarry pool), and foot access to the Central Catchment Nature Reserve via Bukit Timah.

Bukit Batok Property Summary (2026)

| Property Type | Price Range | Gross Yield | Typical Size | Notes |

|---|---|---|---|---|

| 3-Room HDB Resale | S$330k–S$430k | 3.4%–3.9% | 65–75 sqm | Lease typically 55–70 yrs remaining |

| 4-Room HDB Resale | S$480k–S$640k | 3.2%–3.6% | 90–105 sqm | Median ~S$560k Q1 2026 |

| 5-Room HDB Resale | S$620k–S$790k | 3.0%–3.4% | 120–130 sqm | Best lease: 2000s blocks |

| Executive HDB (EA/EM) | S$740k–S$940k | 2.8%–3.2% | 140–155 sqm | Rare; check lease carefully |

| Private Condo (Le Quest) | S$1,380–S$1,520 psf | 3.0%–3.4% | 430–1,400 sqft | Integrated mall; 99-yr lease |

| Altura EC | ~S$1,300 psf (launch) | N/A (TOP 2027) | 614–1,711 sqft | Fully sold; watch resale from 2028 (MOP 5yr) |

Worked Example: SC Couple Buying a 4-Room HDB Resale in Bukit Batok

👥 The Wong Family — Joint SC Buyers, S$9,200/mth Household Income

Property: 4-room HDB resale flat, Bukit Batok West Avenue 6, 12th floor, 1999 block (64 years lease remaining), transacted at S$568,000 (no COV in this example; buyers paid valuation).

Financing: HDB Loan (2.60% p.a., 25-year tenure). Loan eligibility: up to 80% LTV = S$454,400. Downpayment 20% = S$113,600 (can be partly from CPF OA).

CPF check (lease sufficiency): Wong couple aged 32 + 29. Youngest buyer is 29. Lease of 64 years + 29 = 93 years — falls below the 95-year threshold, so CPF usage is pro-rated. Maximum CPF withdrawal = (64/65) × Valuation = 98.5% of S$568,000 = S$559,480. Full CPF usage effectively available; no material restriction here.

Monthly repayment: HDB loan S$454,400 @ 2.60%, 25 years = S$2,058/mth.

MSR check: S$2,058 ÷ S$9,200 = 22.4% — well below the 30% MSR cap. ✓

Stamp duty (BSD): First S$180k @ 1% = S$1,800; next S$180k @ 2% = S$3,600; next S$640k @ 3% = S$6,240; total BSD = S$11,640. (No ABSD — first property for both; both SC.)

Total upfront cost: Downpayment S$113,600 + BSD S$11,640 + HDB admin fee ~S$2,000 + legal S$3,500 ≈ S$130,740 (a portion covered by CPF OA balance).

CPF Housing Grant: Wong couple, first-timer HDB resale buyers. Family Grant: S$50,000 (income S$9,200 ≤ S$14,000 ceiling). Applied to reduce loan — effective outlay S$404,400. Monthly repayment drops to ~S$1,831/mth (MSR 19.9% ✓).

Why Bukit Batok Matters for Property Buyers in 2026

Bukit Batok punches above its weight for several structural reasons that differentiate it from comparable OCR towns such as Choa Chu Kang or Jurong West:

1. Bukit Timah nature premium at OCR prices. Few mature HDB towns can offer direct trail access to the Central Catchment Nature Reserve — a premium that adds lifestyle value without adding Central Region pricing. Bukit Batok’s proximity to Bukit Timah and Little Guilin is a genuine differentiator that does not show up in psf numbers yet.

2. JRL connectivity uplift arriving in 2027. The Jurong Region Line’s Phase 1 will connect Bukit Batok’s western fringe to Jurong Lake District — Singapore’s second CBD and the planned site of the Tuas Mega Port, the Singapore Terminus (HSR), and a major white-site commercial cluster. JRL accessibility is already being priced into Tengah BTO launches; Bukit Batok’s established resale stock has not moved as sharply, suggesting residual value.

3. Tengah demand spillover. Tengah new town will eventually house ~42,000 units, many of which are Standard and Plus classification with 5-year MOPs. Residents completing MOP from 2031 onwards will look for nearby resale options — and Bukit Batok, with its larger flat sizes, nature access, and established amenities, is a natural landing zone.

What Might Come Next for Bukit Batok (Speculative)

The following are forward-looking possibilities, not confirmed plans, and should not be relied upon for financial decisions:

- JRL Phase 1 (2027): The Land Transport Authority has confirmed Tengah Park and Bahar Junction stations in Phase 1 of the JRL. Once operational, Bukit Batok will be within two stops of both the EW Line (existing) and the JRL, enhancing its multi-modal connectivity.

- Bukit Timah–Dairy Farm Long Valley: URA’s masterplan indicates a potential linear park and cycling-friendly corridor through this corridor. If realised, Bukit Batok would be a key access point, adding recreational value.

- New BTO Supply: HDB has indicated potential BTO sites in the Bukit Batok West Extension area in 2026–2027. New BTO launches would set fresh pricing benchmarks and could generate resale demand 5 years post-occupation.

- Commercial cluster at Le Quest: CapitaLand’s ongoing placemaking of the Le Quest podium retail could catalyse further F&B and lifestyle tenants, deepening the town’s amenity profile.

Frequently Asked Questions

Is Bukit Batok a good place to buy property in 2026?

Bukit Batok offers a solid value proposition for buyers prioritising lifestyle, nature access, and OCR pricing. HDB resale values have appreciated steadily since 2020, and the upcoming JRL Phase 1 (2027) adds a structural connectivity catalyst. For investors, gross rental yields of 3.2%–3.6% are competitive for an OCR town. The main risks are the estate’s age (much of the HDB stock dates to the 1990s), which means lease-decay considerations for CPF and bank financing become relevant for older blocks.

When will the Jurong Region Line (JRL) serve Bukit Batok?

JRL Phase 1 is confirmed for opening in 2027, according to the Land Transport Authority (LTA). Bukit Batok will benefit from the Tengah Park and Bahar Junction stations in the adjacent Tengah planning area, which are within cycling and bus-feeder distance of Bukit Batok West. The full JRL network, stretching from Jurong Lake District to Choa Chu Kang, is expected to be completed by 2028–2029. Property values in JRL-adjacent areas have historically seen 5–8% appreciation in the 12–24 months surrounding a line opening.

What is the minimum income needed to buy a 4-room HDB resale in Bukit Batok?

Using a median 4-room transacted price of S$568,000 and an HDB loan at 2.60% over 25 years, the monthly repayment is approximately S$2,058. The MSR cap is 30% of gross income, which implies a minimum household income of ~S$6,860/mth to service the loan without grants. With the Family Grant (up to S$50,000 for first-timer couples), the effective loan reduces and the income requirement drops to ~S$6,100/mth. Note: the actual income ceiling for HDB loans is S$14,000/mth for couples, so most buyers will be within the eligible range.

How does Bukit Batok compare to Choa Chu Kang or Jurong West for property investment?

All three are D23–D22 OCR towns with broadly similar HDB resale price ranges. Bukit Batok distinguishes itself through: (1) nature access (Bukit Timah, Little Guilin), which commands a lifestyle premium; (2) better MRT connectivity today via two EW Line stations; (3) slightly lower median prices than Choa Chu Kang’s most popular blocks. Jurong West offers lower psf pricing and is closer to the JLD employment cluster, making it a stronger pure-yield play. Choa Chu Kang (served by CCK MRT on both the EW and NS Lines) has the edge on MRT coverage for now. Bukit Batok’s JRL upgrade in 2027 may tip the balance for medium-term capital appreciation.

Are there any en-bloc opportunities in Bukit Batok?

Bukit Batok has limited private residential stock, meaning true private en-bloc activity is rare. Le Quest (2022 completion) is too new to be a realistic en-bloc candidate for at least a decade. For HDB owners, the SERS (Selective En Bloc Redevelopment Scheme) administered by HDB is the analogous process — HDB selects older, strategically located estates for redevelopment and offers residents replacement flats. Blocks in older precincts near Bukit Batok Town Centre have been SERS candidates historically, though HDB has not announced any new SERS exercises in Bukit Batok as at mid-2026. Any SERS announcement would be a strong positive catalyst for nearby resale values.

What CPF housing grants are available for Bukit Batok HDB resale buyers?

The main grants for first-timer couples buying HDB resale flats in Bukit Batok are: (1) Family Grant — S$50,000 (income ≤ S$9,000) or S$40,000 (income S$9,001–S$12,000) or S$20,000 (income S$12,001–S$14,000); (2) Half-Housing Grant — S$25,000 for couples where one partner is a first-timer; (3) Proximity Housing Grant (PHG) — S$30,000 (living with parents) or S$20,000 (within 4 km), provided the resale flat is within the stipulated proximity. Grants are administered by HDB and are credited to the CPF OA to reduce the outstanding loan. Eligibility rules are set by HDB and updated periodically; buyers should verify on the HDB website before OTP exercise.

Is Bukit Batok suitable for foreigners or permanent residents?

HDB resale flats are generally not available to foreigners (non-Singapore Citizens or Permanent Residents). Singapore Permanent Residents (SPRs) may purchase resale HDB flats subject to the Ethnic Integration Policy (EIP) and SPR quota, and must form an eligible SPR family nucleus. Foreigners are restricted to private residential properties in Singapore. In Bukit Batok, the only private options are Le Quest (99-year leasehold) and boutique private condos such as West Scape — both accessible to foreigners, though ABSD of 60% applies to all foreigners purchasing residential property in Singapore. SPRs pay ABSD of 5% on their first purchase and 30% on subsequent properties.

Disclaimer: This article is for general informational purposes only and does not constitute financial, legal, or property investment advice. Property prices, grant amounts, loan rates, and government policies are subject to change. HDB resale price data is indicative and sourced from the HDB Resale Price Index and publicly available transaction records. Readers should verify all figures and eligibility criteria directly with HDB (www.hdb.gov.sg), the Urban Redevelopment Authority (www.ura.gov.sg), and CPF Board (www.cpf.gov.sg) before making any property decision. LovelyHomes recommends consulting a licensed property agent (CEA-registered) and a licensed financial adviser before proceeding with any transaction.

Click anywhere to close