HDB MOP Supply Bumper 2026: How 13,484 Newly-Eligible Flats Are Reshaping Resale and Rentals

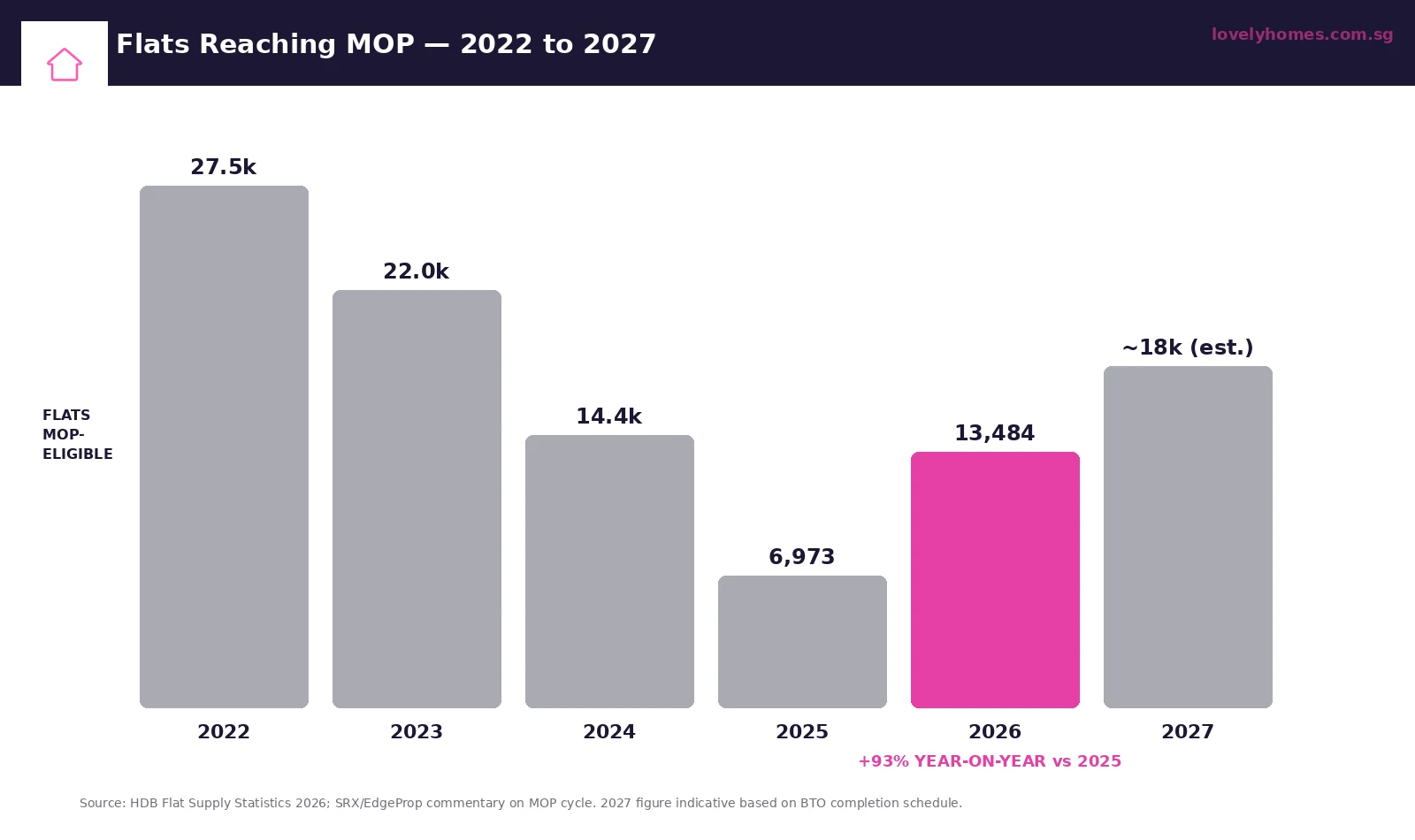

The Housing & Development Board’s flat-supply pipeline has just delivered the largest year-on-year jump in Minimum Occupation Period (MOP) eligibility since 2022. 13,484 HDB flats reach the end of their five-year MOP in 2026 — almost double the 6,973 flats that crossed the same threshold in 2025. The wave is concentrated in young estates that were under construction in 2018–19, and it is large enough to reshape the rental and resale dynamics that have defined Singapore’s HDB market since the post-Covid run-up.

For the household holding a flat that just reached MOP this quarter, the question is when to act. For the household renting one, the question is whether the higher supply finally delivers the rental softening that has been forecast since late 2024. For the prospective upgrader, the question is whether the wave triggers a window of opportunity to dispose of an existing flat into a deeper buyer pool. This piece walks through what the numbers show, where the supply is concentrated, and how the secondary effects are likely to play out across the rest of 2026.

Quick Answer — the 2026 MOP wave at a glance

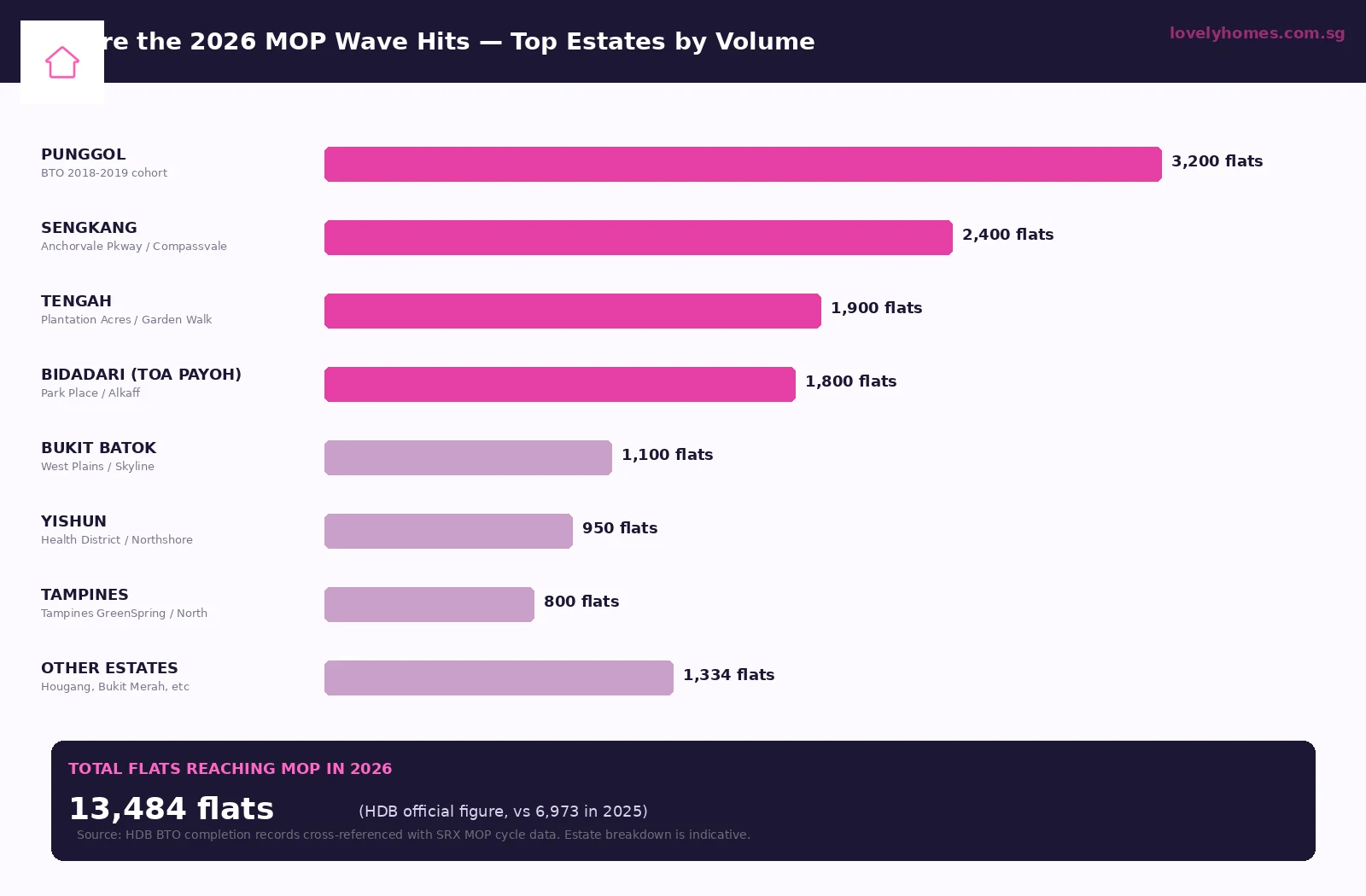

- Volume: 13,484 flats reach MOP in 2026 vs 6,973 in 2025 — a 93% increase year-on-year.

- Why now: the BTO cohort that was launched and built between 2018 and 2019 is hitting its 5-year MOP this year.

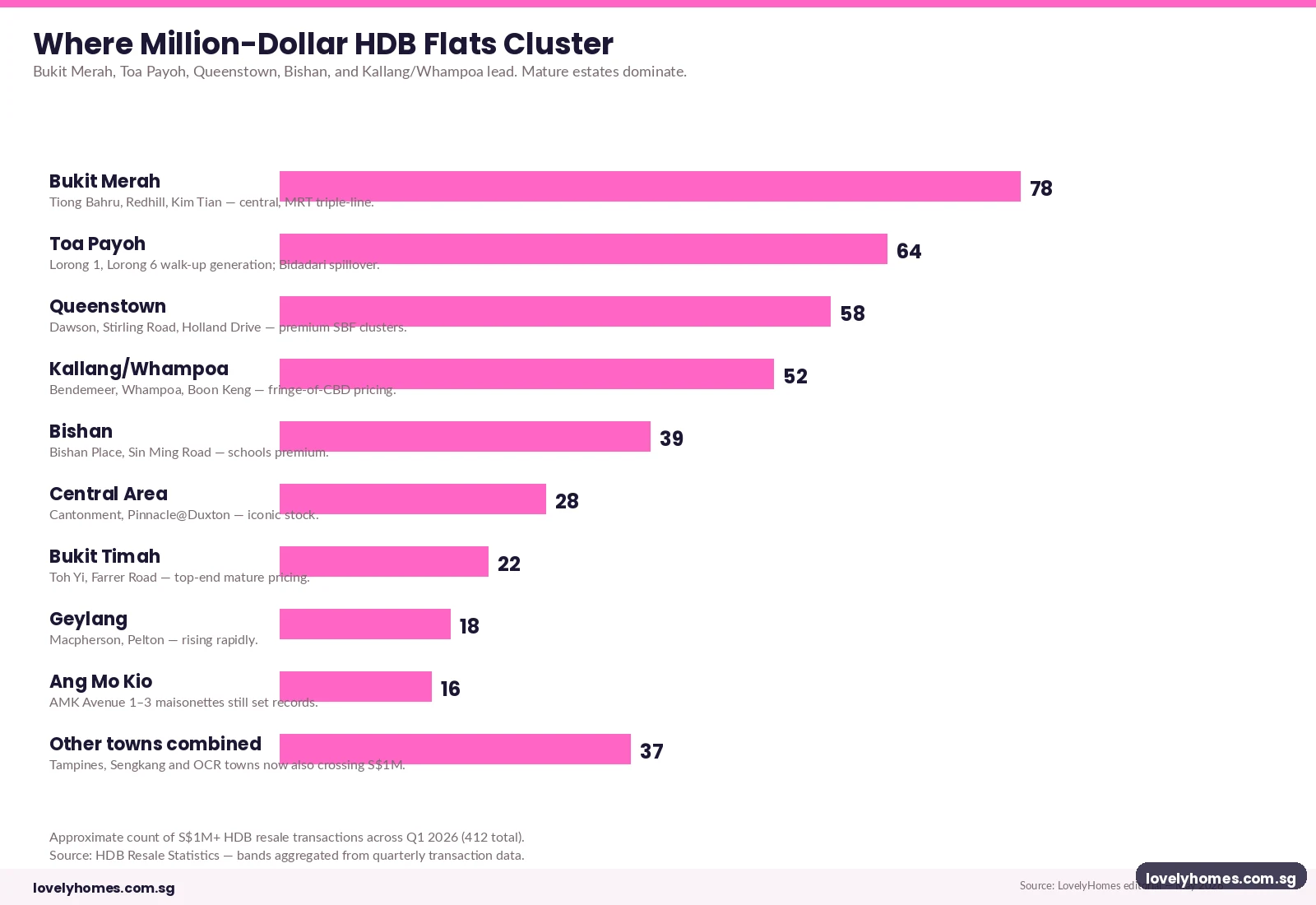

- Top estates: Punggol leads with about 3,200 flats, followed by Sengkang (~2,400), Tengah (~1,900) and Bidadari/Toa Payoh (~1,800).

- Resale impact: deeper supply moderates the price index — HDB resale fell 0.1% QoQ in Q1 2026, the first decline since Q2 2019, and Q2 is expected to remain flat to mildly negative.

- Rental impact: the bumper supply is the largest single factor capping HDB rental growth at 1–2% for 2026, after two years of mid-to-high single-digit growth.

- Window for upgraders: sellers have a deeper buyer pool but face thinner pricing power; upgraders should plan the buy-side leg first to avoid being squeezed.

- Trajectory: 2027 supply estimates push the figure higher again on the back of the 2019–20 BTO cohort, before normalising in 2028.

How the 2026 Cohort Came to Be

HDB requires owners of a Build-To-Order (BTO) flat to live in the unit as their primary residence for a Minimum Occupation Period of five years before they can sell on the open market or rent the entire flat out. The MOP clock starts ticking from key collection. The 2026 MOP wave is therefore the cohort that received keys in 2020–21, which in turn corresponds to BTO launches in 2018–19. That two-year BTO programme was a particularly high-volume one — HDB launched roughly 17,500 flats in 2018 and 16,000 in 2019, and most of those have now arrived at the moment of release.

Counted purely against the 2025 baseline of just under 7,000 MOP-eligible flats, this is the largest single-year supply uplift since the post-2018 launch surge. The Government has signalled in its 2026 BTO programme announcement that 2027 is likely to remain elevated as the 2019–20 launch cohort completes its MOP, before normalising in 2028 toward a steady-state of around 12,000 flats per year.

Where the Wave Hits

The 2026 MOP cohort is concentrated geographically in the estates that absorbed the bulk of the 2018–19 BTO launches. Punggol is the single largest contributor, with roughly 3,200 flats reaching MOP across the Punggol Town Centre, Punggol Coast and Punggol Northshore precincts. Sengkang follows with about 2,400 flats, primarily in the Anchorvale Parkway and Compassvale Highway projects. Tengah, the youngest mature estate-in-the-making, contributes around 1,900 flats from the Plantation Acres and Garden Walk launches. Bidadari (administered under Toa Payoh) adds another 1,800 from Park Place and Alkaff.

The estate composition matters because resale and rental absorption is local. A flood of newly-MOP flats in Punggol does not directly weigh on resale prices in Bishan or Ang Mo Kio; it weighs on Punggol prices and to a smaller degree on the surrounding Sengkang corridor. The implication is that the calmer trajectory in the headline HDB Resale Price Index masks meaningful divergence between estates: young suburban estates with thick MOP supply are likely to see the most price moderation, while mature estates with thin MOP volumes (Bishan, Queenstown, Toa Payoh outside Bidadari) are likely to remain firm.

Resale: From Mid-Single-Digit Growth to a Flat Quarter

The Q1 2026 final HDB resale data, released by the Housing & Development Board on 24 April 2026, showed the Resale Price Index fell 0.1 per cent quarter-on-quarter — the first decline since Q2 2019. Transaction volume came in at 6,285 flats for the quarter, slowing on a year-on-year basis but slightly higher quarter-on-quarter. The combination of softer prices and resilient volumes is consistent with a market entering a digestion phase: more sellers (driven by the MOP wave) meeting steady but not accelerating buyer demand.

The MOP supply is one of three factors moderating the index. The other two are the larger BTO programme (19,600 flats across 2026 versus 6,000 in the depths of the post-Covid pause), which provides a credible primary-market alternative for first-timer demand, and the cumulative effect of the cooling measures introduced between 2021 and 2024 — the 55 per cent TDSR, the 15-month wait-out for ex-private downsizers, and the wider tenure restrictions on HDB Loans. Each contributes; the MOP supply is the new element in 2026 that pushes the index from “moderating” to “flat”.

For owners considering a sale this year, the practical implication is that pricing power is tighter than it was in 2024. The cash-over-valuation (COV) figures that buoyed the 2024 market are normalising back toward listed valuation. Sellers who set realistic asking prices and refresh their listings against current comparables clear the market; sellers who anchor on 2024 valuations are increasingly seeing extended days-on-market.

Rental: The Largest Single-Year Supply Shock Since 2022

Owners who reach MOP in 2026 have two primary monetisation paths — sell, or rent out. Historically the split has run roughly 60:40 in favour of selling, with the rental fraction skewing higher in young estates where the MOP holders are typically dual-income households who are upgrading to a private property and prefer to retain the HDB as a rental asset. Applied to a 13,484-flat cohort, that translates to perhaps 5,000–6,000 newly-MOP flats joining the rental pool over the course of 2026.

That is the single largest quasi-instant supply addition the rental market has absorbed since the 2022 expat reshoring wave drove rents to record highs. URA data shows private residential rents rose just 0.3 per cent quarter-on-quarter in Q1 2026, and HDB rentals have softened by about 0.3 per cent month-on-month entering the year. Industry forecasts now centre on HDB rental growth of 1–2 per cent for 2026, down sharply from the 8–10 per cent annualised pace of 2022–23.

The rental moderation is unevenly distributed. Mature estates like Tiong Bahru, Tampines Central and Queenstown — where MOP supply is thin and expat demand remains anchored — continue to clear rents at firm or even slightly rising levels. Young estates with thick MOP supply, especially Punggol and Sengkang, are seeing rental softness as the new supply meets a tenant pool that is increasingly price-sensitive. The price-sensitivity is itself a shift: companies have tightened relocation budgets, and tenants on longer-term assignments are negotiating harder against the deeper inventory.

Worked Example — The Lim Family in Punggol

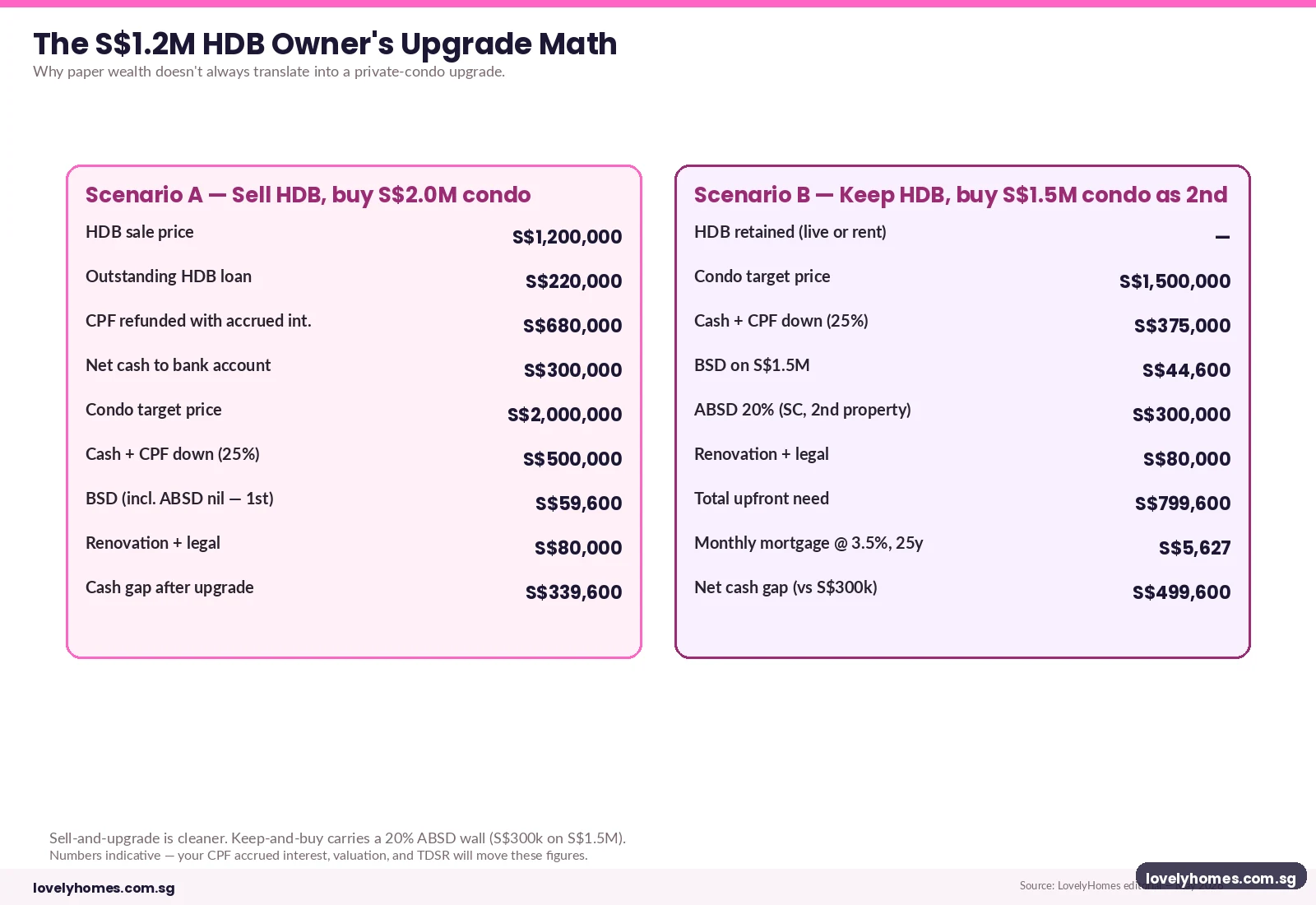

Worked Example. Mr and Mrs Lim, both Singapore Citizens in their late 30s, took keys to a 4-room BTO at Punggol Northshore in March 2021. Combined gross income S$13,000/month; outstanding HDB Loan balance approximately S$340,000 at 2.6 per cent over the remaining 21 years; current valuation around S$680,000 based on Q1 2026 transactions in the precinct. Their flat reaches MOP in March 2026.

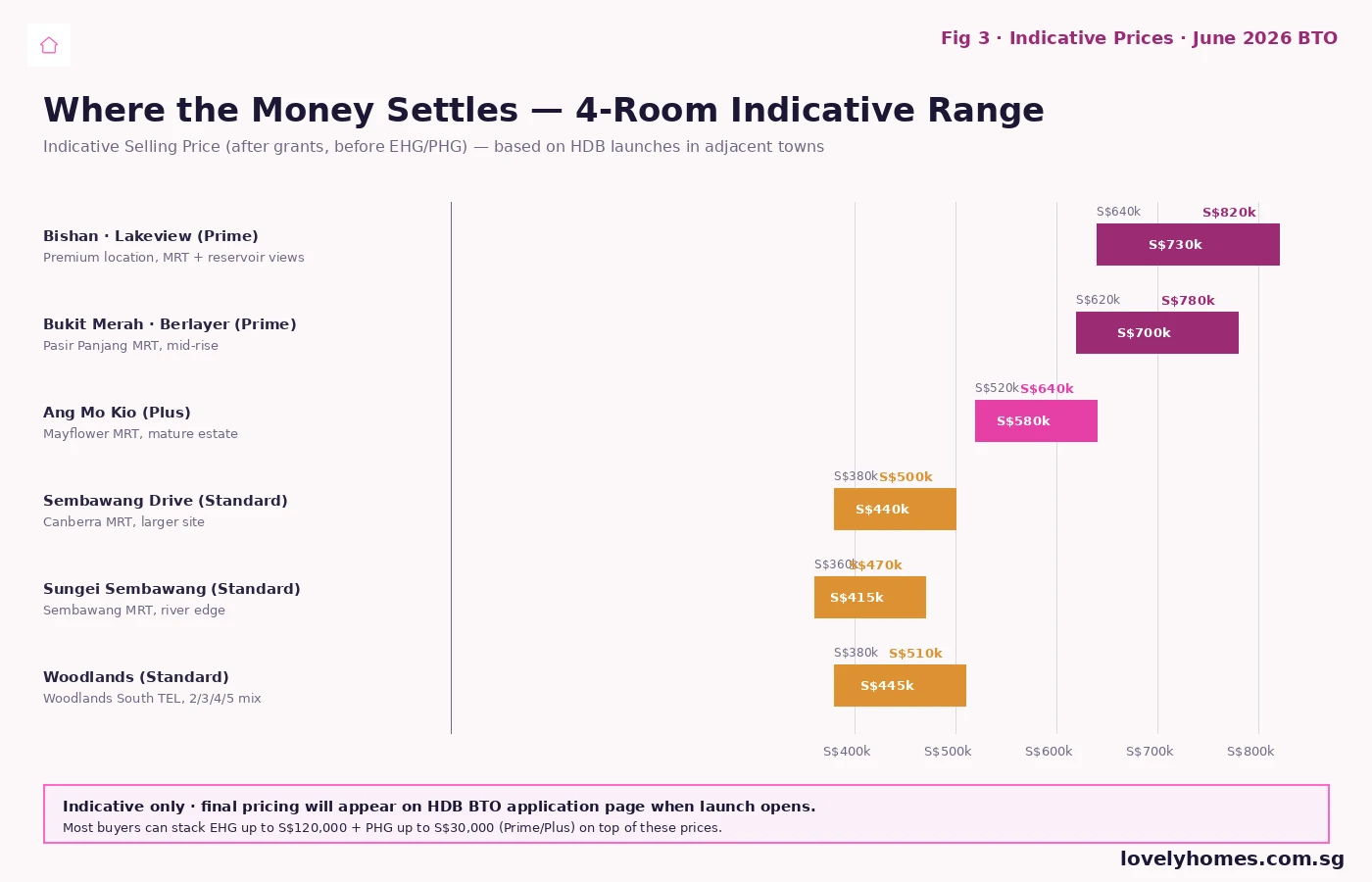

Path A — Sell now and upgrade. List at S$680,000, expect to clear at S$650,000–S$670,000 given the deeper Punggol supply (~3,200 flats reaching MOP across the year). Net cash and CPF on completion roughly S$310,000–S$330,000 after redeeming the HDB Loan and refunding accrued interest. Transition into a 2-bedroom OCR private condo in the S$1.5–1.7M range using the proceeds plus a fresh bank loan.

Path B — Rent out and retain. Rent out at S$3,400/month — softer than the S$3,600 a similar 4-room would have achieved in early 2025 because of the supply influx. Net of agency fees, HDB Loan instalment and property tax under the non-owner-occupier ladder, monthly cash flow is roughly S$300–S$400. The Lims continue to live in their HDB for the time being, retain optionality for a private upgrade later, and benefit if Punggol prices firm again into 2027–28 once the MOP supply normalises.

Path C — Sell into the resale market and rent in mature estate. Sell as in Path A, but rent a Bishan or Toa Payoh 4-room at roughly S$3,200/month while waiting for a private launch in a preferred location (Bidadari, Tengah extension, or a CCR launch in late 2026). This path frees up CPF and cash, locks in current valuation, and keeps the household nimble while the market digests the MOP wave.

The decision between the three paths is heavily personal — financial, lifestyle and timing — and the right answer for the Lims is not necessarily the right answer for a similar couple in Sengkang or Bidadari. What the analysis does highlight is that the MOP wave creates an asymmetry in 2026 that is worth modelling carefully before acting.

Summary Table — 2026 MOP Wave Quick Reference

| Metric | 2025 | 2026 (this year) | Implication |

|---|---|---|---|

| Flats reaching MOP | 6,973 | 13,484 | +93% supply uplift |

| HDB RPI (QoQ) | +1.0% to +1.7% range | −0.1% Q1 (first decline since Q2 2019) | Calmer trajectory |

| HDB rental growth (annual) | ~5–6% | 1–2% (forecast) | Tenant-friendly |

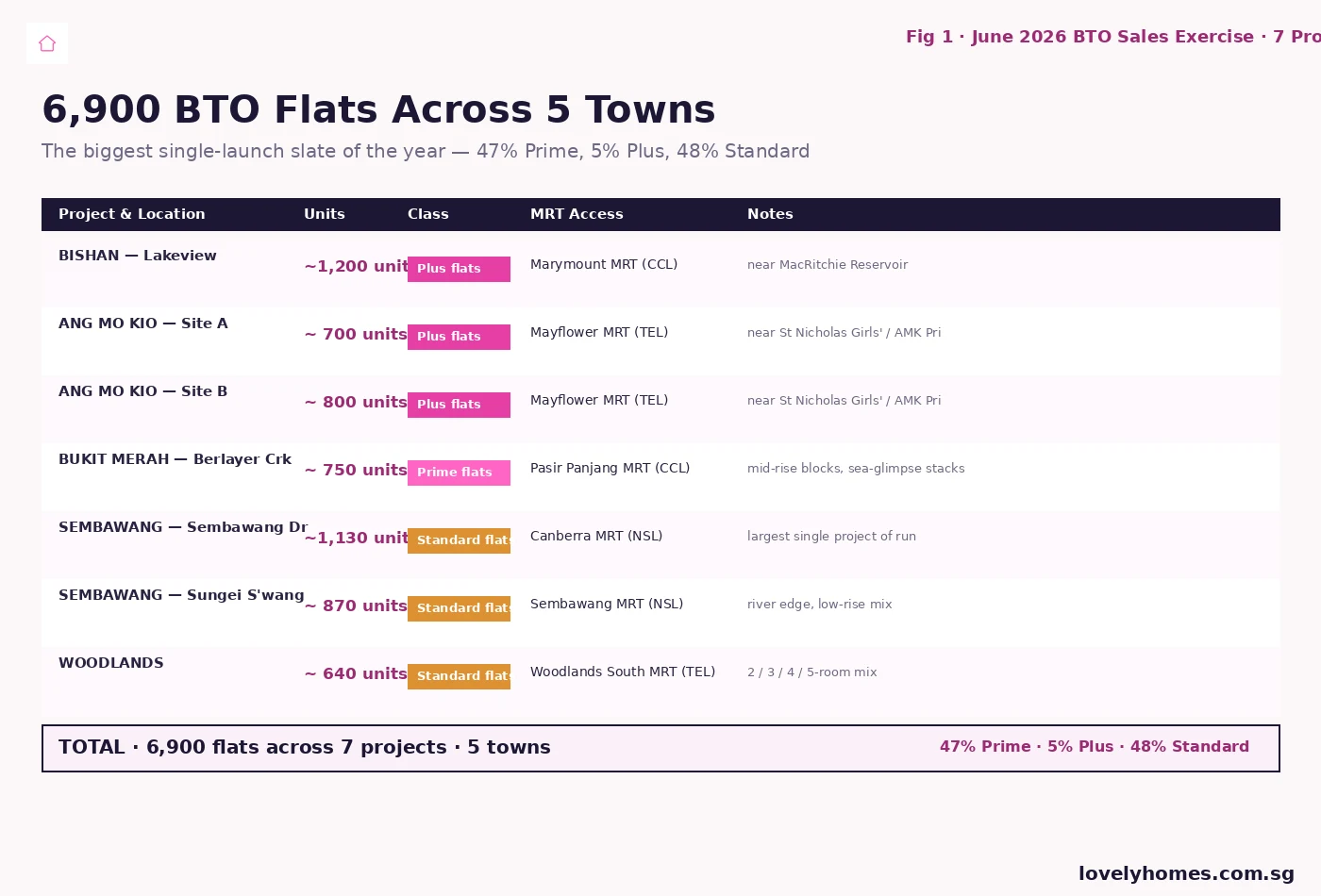

| BTO programme | ~6,000 flats | 19,600 flats (3 exercises) | Primary-market alternative |

| Top MOP estate | Tampines (~1,400) | Punggol (~3,200) | Suburban supply skew |

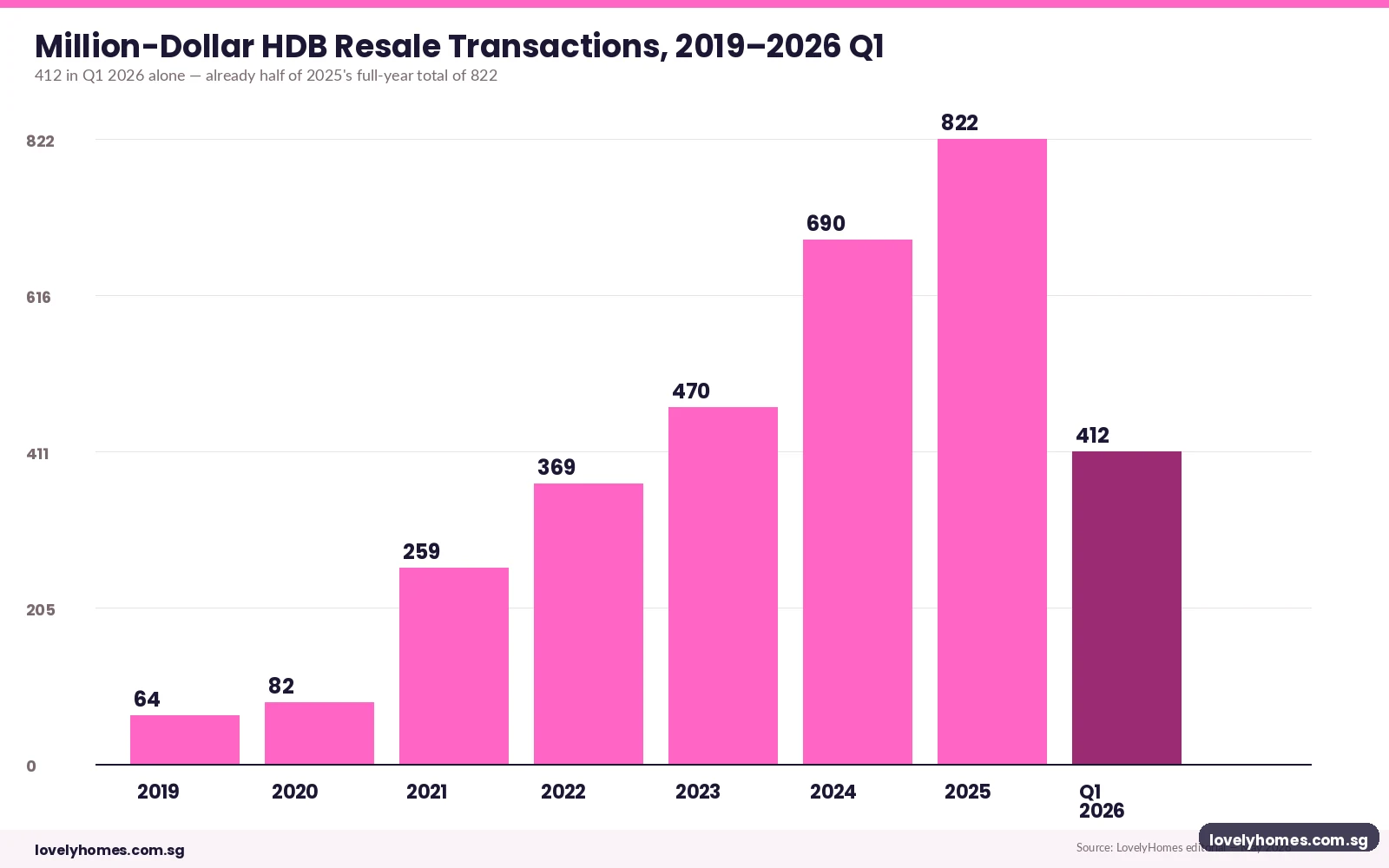

| Million-dollar HDB flats | ~1,030 transactions | 412 transactions in Q1 | Pace remains elevated |

| Days-on-market (resale) | ~28 days median | ~38 days median (estimate) | Less seller pricing power |

What This Means for You

The 2026 MOP wave is not a price collapse — the HDB Resale Price Index is essentially flat, not down materially — but it is a meaningful repricing of the seller’s position. Five rules of thumb follow from how the wave is reshaping the market.

For sellers in young estates (Punggol, Sengkang, Tengah, Bidadari): price against current Q1 2026 comparables, not against 2024 highs. Refresh listings every 4–6 weeks. Expect a longer time-on-market and weaker COV. The deeper buyer pool is good news for finding a buyer; the asymmetry is in pricing power.

For sellers in mature estates (Bishan, Queenstown, Toa Payoh outside Bidadari): the MOP wave barely touches your supply. Pricing remains firm, days-on-market remain short, and selective premium pricing is still achievable for renovated units. The market segmentation that has defined HDB resale since 2022 — where mature-estate scarcity attracts a premium — continues to hold.

For tenants: 2026 is the first genuinely tenant-friendly year since 2021. Use the leverage. Negotiate harder on renewal rents and on the new-lease-shopping pool. The supply uplift is most visible in young estates and OCR condos; mature-estate rents remain firmer.

For upgraders: sequence the buy-side first. The resale market is no longer a guaranteed quick clearance, especially in young estates with thick MOP supply. Lock in the upgrade purchase before listing the existing flat, or budget for a longer disposal window. Bridging loans are an option if cash-flow allows.

For investors holding HDB-near-MOP: retaining for rental no longer offers the rent-up surprise of 2022–23. The rental yield maths now sits in a 2.5 per cent–3.5 per cent net range for most 4-room flats in young suburban estates, which compares unfavourably to comparable yields on smaller OCR condos for households in higher tax brackets. The case for selling and reallocating capital strengthens at this point in the cycle.

What Might Come Next

Two trajectories are worth watching across the rest of 2026 and into 2027. First, the second half of 2026 brings additional MOP supply from the 2019–20 BTO cohort, particularly the Q3 and Q4 keys collected in 2021. SRX and EdgeProp commentary points toward a 2027 supply that may remain at or above the 2026 figure before normalising in 2028. If true, the price moderation that defined Q1 2026 is likely to extend through the full year and into the early part of 2027.

Second, the rental market is approaching the inflection point where tenant price-sensitivity meets real wage growth. Singapore’s median household income continues to rise at roughly 3 per cent a year nominal; if rental growth caps at 1–2 per cent across 2026 and 2027, rent-to-income ratios moderate for the first time since 2021. That is a meaningful structural improvement for the household sector and may reduce the political pressure that drove some of the cooling-measure calibration of 2023–24.

The structural variable that could disturb both trajectories is the BTO completion pace. If construction delays push the 2027 MOP cohort into 2028, the 2027 supply moderates and the rental softening may reverse earlier than expected. Conversely, if the 2026 BTO programme of 19,600 flats accelerates rather than smooths the pipeline, the 2031 MOP wave (five years out from 2026) could be even larger than 2026’s. The Government’s stated intent is a smooth, predictable supply cadence; markets should plan for that base case while keeping an eye on the construction-completion data that will feed the 2027 picture.

Frequently Asked Questions

What does MOP mean and why is the 5-year clock important?

MOP — the Minimum Occupation Period — is the 5-year minimum during which a household must occupy its HDB flat as primary residence before it can be sold on the open market or rented out as a whole unit. The 5-year clock starts on key collection. Until MOP is served, the flat cannot be sold to anyone other than HDB itself, and rental is restricted to room-by-room arrangements (and only with HDB approval). The MOP is a cornerstone of HDB’s policy that public housing is shelter first and asset second.

Why is the 2026 cohort so much larger than 2025?

The 2025 cohort was unusually small because the 2020 BTO programme was sharply curtailed during the post-Covid construction pause. The 2018–19 cohort that hits MOP in 2026 was a much larger BTO vintage, by design — the Government had ramped up supply ahead of the 2017–18 demand surge. The 2027 figure is also expected to be elevated as the 2019–20 cohort completes its MOP, before the pipeline normalises in 2028.

Will HDB resale prices fall further in 2026?

The Q1 2026 print of −0.1 per cent QoQ is the first decline in seven years, but the consensus across SRX, EdgeProp and HDB’s own commentary is that the full-year trajectory is flat to mildly positive (0–2 per cent), not a meaningful drop. The market is digesting the supply influx, not collapsing under it. Mature estates are likely to remain firm; young suburban estates with thick MOP supply are the segments most exposed to flat or mildly negative prints in Q2 and Q3.

Should I rent out my MOP-eligible flat or sell?

The arithmetic depends on three variables: net rental yield (typically 2.5–3.5 per cent for young suburban 4-rooms in 2026), expected price trajectory of the estate (firmer in mature estates, softer in MOP-heavy ones), and the household’s need for capital from the sale. For households planning to upgrade to private property within the next 12 to 24 months, selling now and crystallising the equity tends to be cleaner. For households happy to retain the HDB and add a private property on top, the rental retention path remains viable but the rent-up surprise of 2022–23 has fully passed.

How do I check when my own flat reaches MOP?

The MOP completion date is 5 years from the date of key collection. Owners can verify the exact MOP date through the HDB Resale Portal (My HDBPage) under “My Flat Details”, which shows the date of key collection and the calculated MOP completion. The portal also shows whether any partial occupation gaps (e.g. for prolonged overseas postings) need to be made up before the MOP is officially served.

Does the new Plus and Prime classification change MOP rules for 2026 flats?

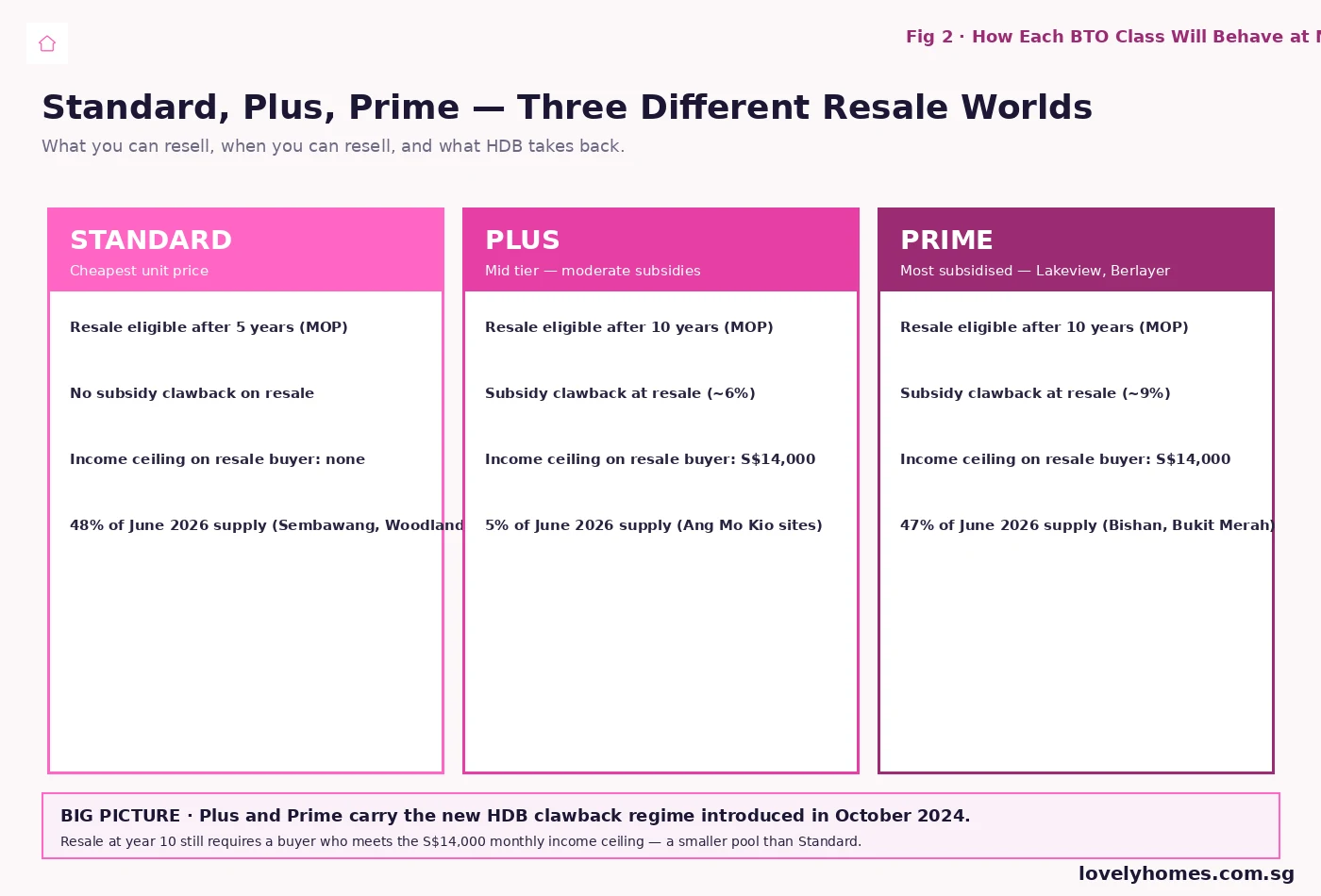

For most flats reaching MOP in 2026 — which were launched in 2018–19 under the old Mature/Non-Mature classification — the standard 5-year MOP applies. The Plus and Prime classifications introduced from October 2024 carry longer 10-year MOPs, with subsidy clawbacks of 6 per cent (Plus) or 9 per cent (Prime) on resale, and a S$14,000 monthly income cap for resale buyers. Those classifications affect the 2034-and-later MOP cohorts; they do not change the 2026 supply picture.

Will the BTO programme of 19,600 flats in 2026 cannibalise resale demand?

Partially, yes. The 19,600 BTO programme is the largest in over a decade and provides a credible primary-market alternative for first-timer households, particularly those with EHG entitlements that work better against a BTO than a resale. The cannibalisation is most visible in non-mature young estates where the BTO and resale segments overlap. In mature estates with no BTO supply (Bishan, Queenstown, Toa Payoh outside Bidadari), the resale market continues to clear at firm prices because the BTO is not a substitute.

Disclaimer

This piece is general analysis of the 2026 HDB MOP supply pipeline and its implications for the resale and rental markets, drawing on data from HDB, the Urban Redevelopment Authority, SRX, EdgeProp and Stacked Homes published as at the date of writing. Estimates of estate-level MOP volumes and the rental/sale split are indicative; the actual mix will depend on individual household decisions and may vary materially across the year. This is not financial, tax or legal advice. For decisions on your own flat, consult HDB Mortgage Servicing, a licensed Singapore property adviser and (where relevant) a tax practitioner. Always rely on official sources — HDB, URA, data.gov.sg — for the latest position before transacting.