Singapore Joint Property Ownership Guide 2026: Joint Tenancy vs Tenancy in Common Explained

Key Takeaways: Singapore Joint Property Ownership 2026

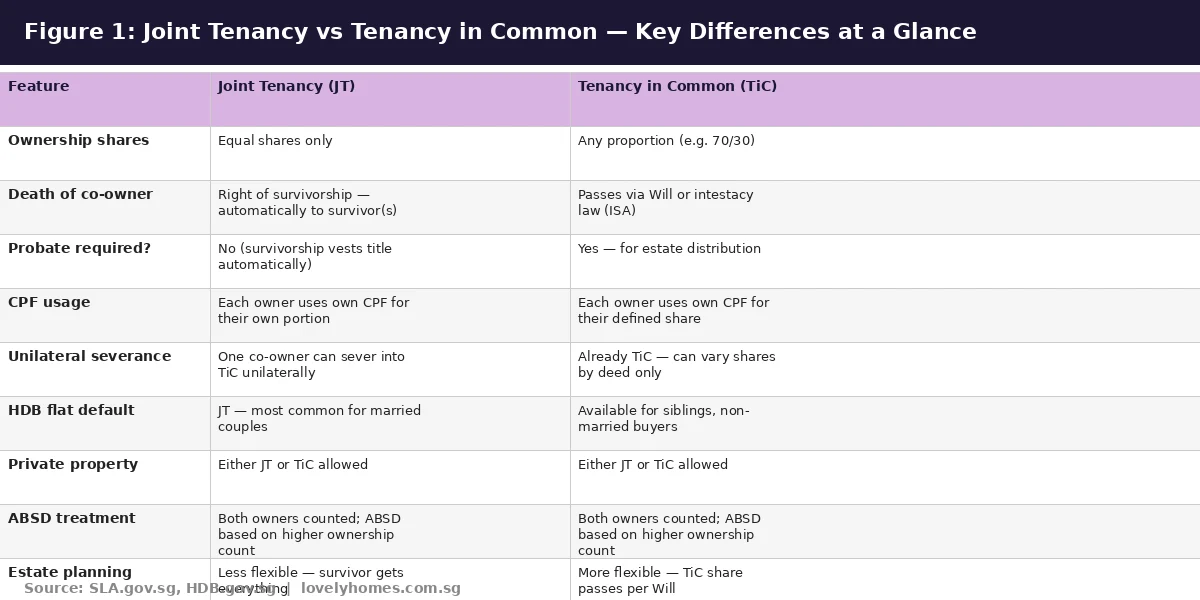

- Two modes of co-ownership: Joint Tenancy (JT) — equal shares, right of survivorship; Tenancy in Common (TiC) — flexible proportions, passes via Will or intestacy.

- ABSD on joint purchases: For mixed-profile co-purchases (e.g. one owner already owns property), ABSD is calculated based on the higher ownership count across all co-owners. A Singapore Citizen who already owns an HDB buying a private condo jointly with a first-timer SPR pays the SC second-property ABSD rate of 20% on the full purchase price.

- CPF usage: Each co-owner draws on their own CPF Ordinary Account for their respective mortgage contributions. There is no cross-pooling of CPF funds between co-owners.

- ABSD and decoupling: Married couples who hold property under JT may consider “decoupling” — severing the JT into TiC and transferring one spouse’s share to the other — as a strategy to free up the departing spouse’s ABSD first-property entitlement. BSD applies on the transfer but ABSD is nil if the transferring spouse is disposing of their only property.

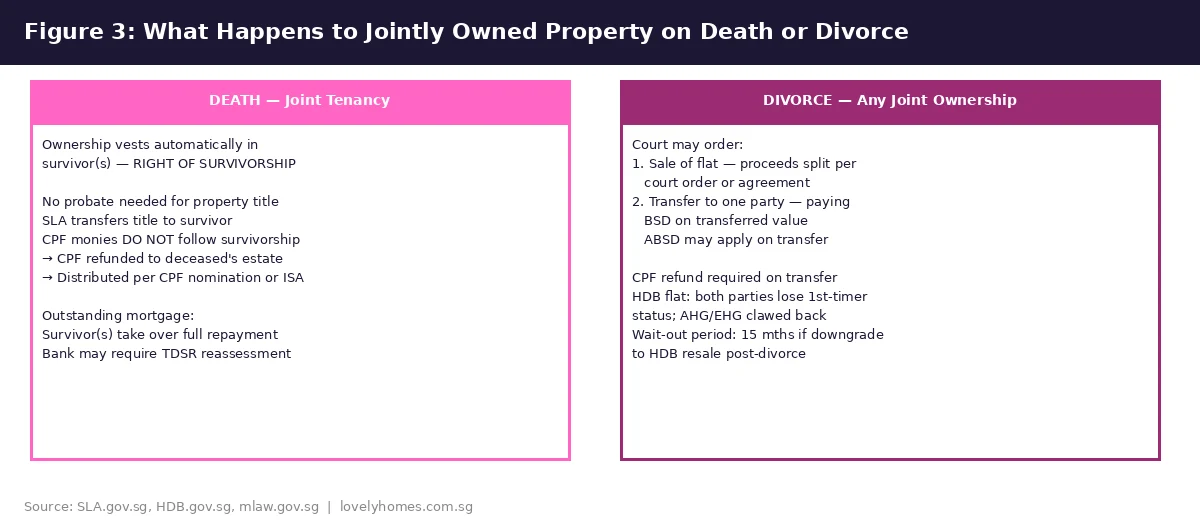

- Death under JT: Title vests automatically in the surviving co-owner(s) — no probate required. CPF monies do not follow survivorship and are returned to the deceased’s estate.

- Divorce: Courts may order sale or transfer of jointly owned property. Both parties lose first-timer HDB status; CPF grants are clawed back.

- Foreigners and joint ownership: A Singapore Citizen or PR may co-purchase a private condo with a foreigner under JT or TiC, but the foreigner’s ABSD rate (60% as at June 2026) applies to the entire purchase price — not just the foreigner’s share.

Introduction: Why Joint Property Ownership Matters in Singapore

Jointly owned property is the norm in Singapore. The vast majority of HDB flats are purchased by couples or families as joint owners, and many private condominiums and landed homes are also held under co-ownership arrangements. Yet the legal and financial mechanics of joint property ownership are surprisingly misunderstood — even by experienced property owners.

The two recognised forms of co-ownership under Singapore law are Joint Tenancy and Tenancy in Common. The choice between them has far-reaching implications for estate planning, ABSD strategy, CPF withdrawal, and what happens to the property on the death of a co-owner or the breakdown of a marriage. Understanding these mechanics is not just a legal formality — it can mean the difference between a clean, probate-free property transfer and years of legal disputes, or the difference between a well-timed decoupling saving S$300,000 in ABSD and an unnecessary stamp duty bill.

This guide covers both forms of co-ownership in depth, explains how the ABSD framework applies to joint purchases across different buyer-profile combinations, and provides a worked example for couples navigating the HDB-to-private upgrade path.

Joint Tenancy (JT): What It Means and How It Works

A Joint Tenancy is the default co-ownership structure for HDB flats purchased by married couples in Singapore, and it is also commonly used by couples purchasing private residential property together. Under JT, co-owners hold the property in equal, undivided shares. There is no “60/40 split” or any other fractional allocation — each joint tenant holds an identical and indivisible interest in the whole property.

The defining legal feature of JT is the right of survivorship (jus accrescendi). When one joint tenant dies, their interest in the property does not form part of their estate — it passes automatically and immediately to the surviving joint tenant(s) by operation of law. This means:

- No probate or letters of administration are required for the property title.

- The property cannot be bequeathed by Will — any attempt to do so is ineffective against JT property.

- The Singapore Land Authority (SLA) will transfer the title to the survivor(s) upon production of the death certificate and relevant forms.

One consequence property owners sometimes overlook is that CPF monies do not follow the right of survivorship. Even if the property is held under JT, the CPF contributions the deceased co-owner made towards the property are refunded to their CPF account and then distributed according to their CPF nomination — or, if no nomination exists, under the Intestate Succession Act. This means the surviving spouse does not automatically receive the CPF monies used to pay the mortgage, and may need to refinance or use their own CPF to discharge the remaining loan.

Tenancy in Common (TiC): Flexible Shares and Estate Planning

Under a Tenancy in Common, co-owners hold distinct and quantified proportions of the property — for example, 50/50, 70/30, or any other split agreed upon at the time of purchase. Each co-owner’s share is their individual asset and may be dealt with separately: they may sell their share, mortgage it (subject to bank consent), or leave it by Will.

The key distinction from JT is that there is no right of survivorship in TiC. When a co-owner under TiC dies, their share forms part of their estate and is distributed according to their Will or, if there is no valid Will, under the Intestate Succession Act (Cap. 146). This means probate proceedings (or letters of administration if there is no Will) are required before the deceased’s share can be transferred to beneficiaries.

TiC is often the preferred structure when:

- Co-owners are not married to each other (e.g. siblings, friends, or business partners co-purchasing an investment property) and wish to hold proportionate shares reflecting their respective financial contributions.

- Couples wish to hold proportions that reflect their CPF contributions or cash payments accurately, for clean accounting on eventual sale.

- One co-owner wants the flexibility to bequeath their share to a specific beneficiary (e.g. children from a prior marriage) rather than have it vest automatically in the surviving spouse.

- A decoupling strategy is being implemented (see below).

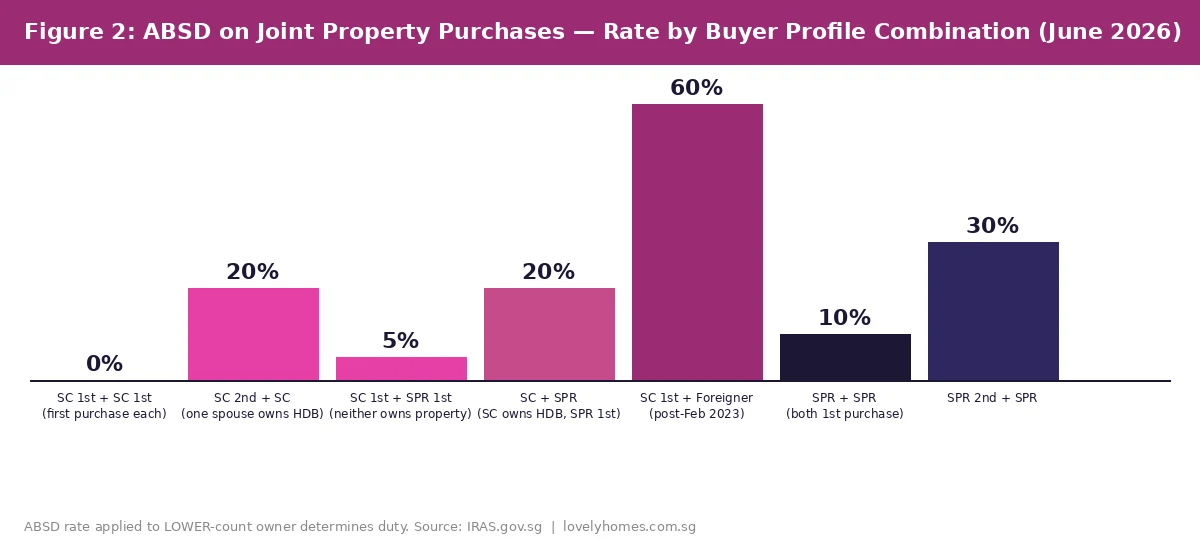

ABSD on Joint Purchases: The Higher-Count Rule

The Additional Buyer’s Stamp Duty (ABSD) framework applies to the full purchase price of a jointly acquired property, at the rate applicable to the co-owner with the highest ownership count. This is often misunderstood: buyers do not pay ABSD on “their share” of the purchase price — the duty is assessed on the whole transaction.

Practical examples as at June 2026:

- Two Singapore Citizens, both first-time buyers (neither owns any property): ABSD = 0%. The most favourable outcome — no duty above the standard Buyer’s Stamp Duty (BSD).

- SC couple where one spouse already owns an HDB flat: ABSD = 20% on the full purchase price. The spouse who owns the HDB has a higher ownership count, so the 20% SC second-property rate applies to the entire purchase.

- SC + Singapore Permanent Resident, both first-time buyers: ABSD = 5% on the full purchase price (SPR first-property rate). The SPR’s ownership profile drives the rate.

- SC (owns HDB) + SPR (first-time buyer): The SC is the higher-count owner — ABSD = 20%.

- SC + foreigner (any ownership profile), post-February 2023: ABSD = 60% on the full purchase price. The foreigner’s rate applies regardless of the SC co-owner’s profile. This rule was tightened in April 2023 and remains in force as at June 2026.

- Two SPRs, both first-time buyers: ABSD = 10% on the full purchase price.

CPF Usage in Joint Property Purchases

Each co-owner draws on their own CPF Ordinary Account (OA) to fund their respective mortgage instalments and/or part of the downpayment. There is no pooling of CPF funds across co-owners, and no co-owner may use another’s CPF without that person’s explicit authorisation through a CPF nomination or legal assignment — neither of which is available for mortgage purposes.

For HDB flats under JT, each owner’s CPF contribution is tracked separately by the Central Provident Fund Board (CPF). On sale of the flat, each owner must refund their own CPF principal withdrawn plus the accrued interest (calculated at 2.5% per annum) back to their own CPF OA. These refunds are entirely separate — even under JT, CPF repayments do not cross between co-owners.

This has important implications for couples planning an ABSD remission strategy. If Wife uses significantly more CPF than Husband towards the property, her CPF refund obligation on sale will be larger — reducing the net cash she receives. This must be factored into the financial model for any property upgrade or decoupling exercise.

Changing Between JT and TiC: Deed of Severance and Decoupling

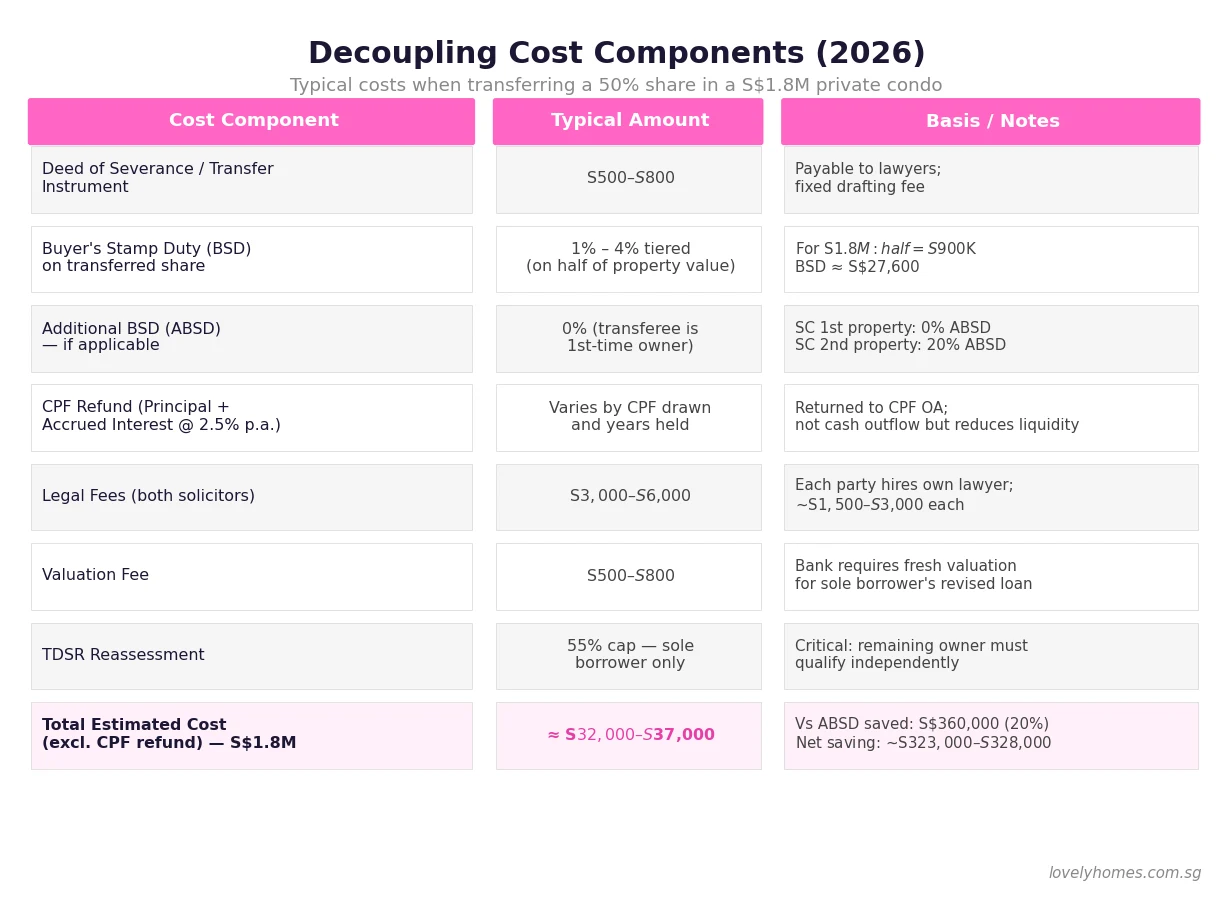

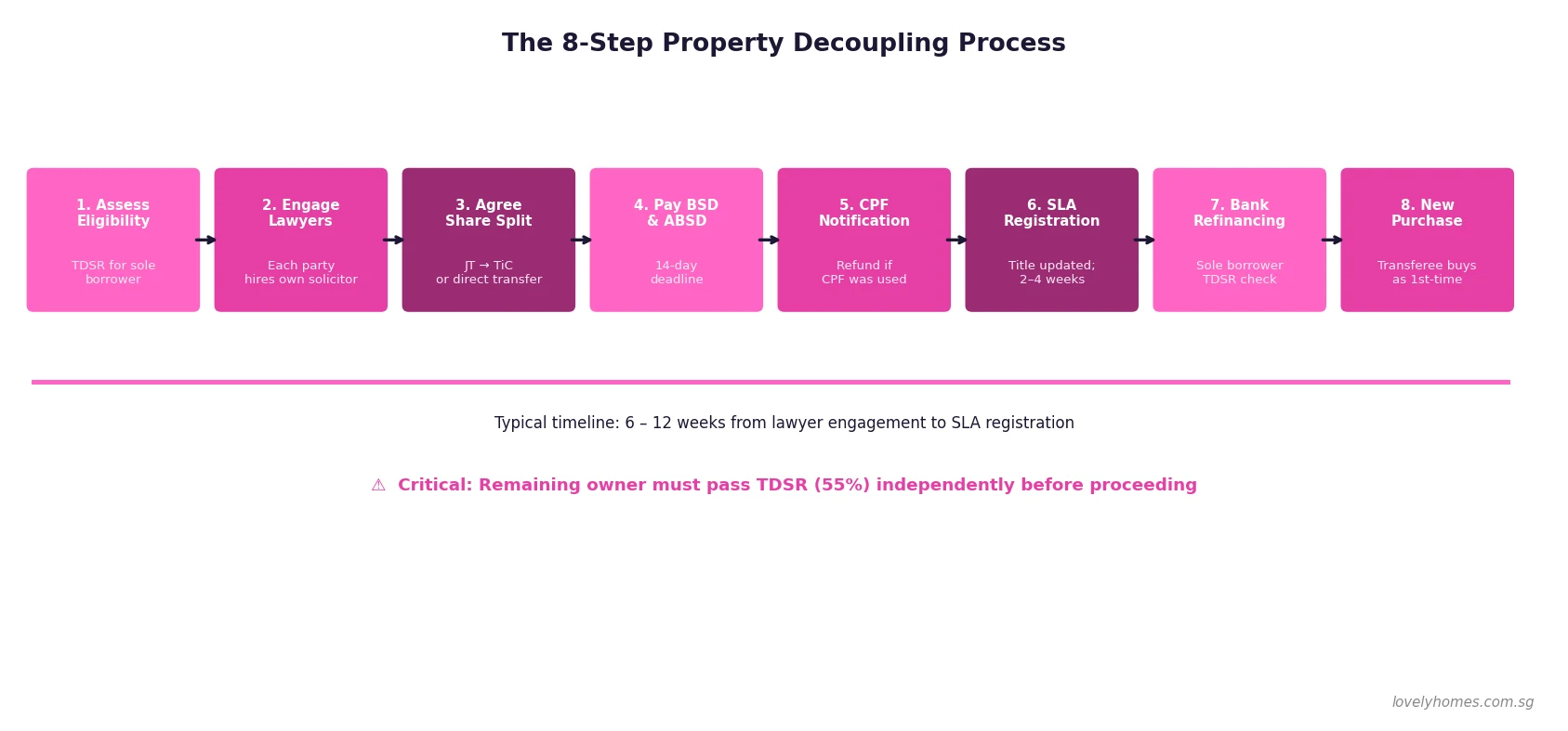

It is possible to convert a JT into a TiC — and vice versa — through a legal process. Converting from JT to TiC is called severance and can be done unilaterally by one joint tenant (i.e. without the other’s consent) by serving a notice of severance, though in practice solicitors will draft a Deed of Severance to document the transaction formally. Converting from TiC to JT requires the agreement of all co-owners and is done by deed.

Decoupling is a related but distinct strategy that has gained popularity among HDB upgrader couples. It involves one co-owner transferring their share in a jointly owned property to the other co-owner, so that the transferring co-owner ends up with no property in their name. The “clean” spouse can then purchase a new property as a first-time buyer, paying 0% ABSD (for SC first-property buyers).

The decoupling process involves:

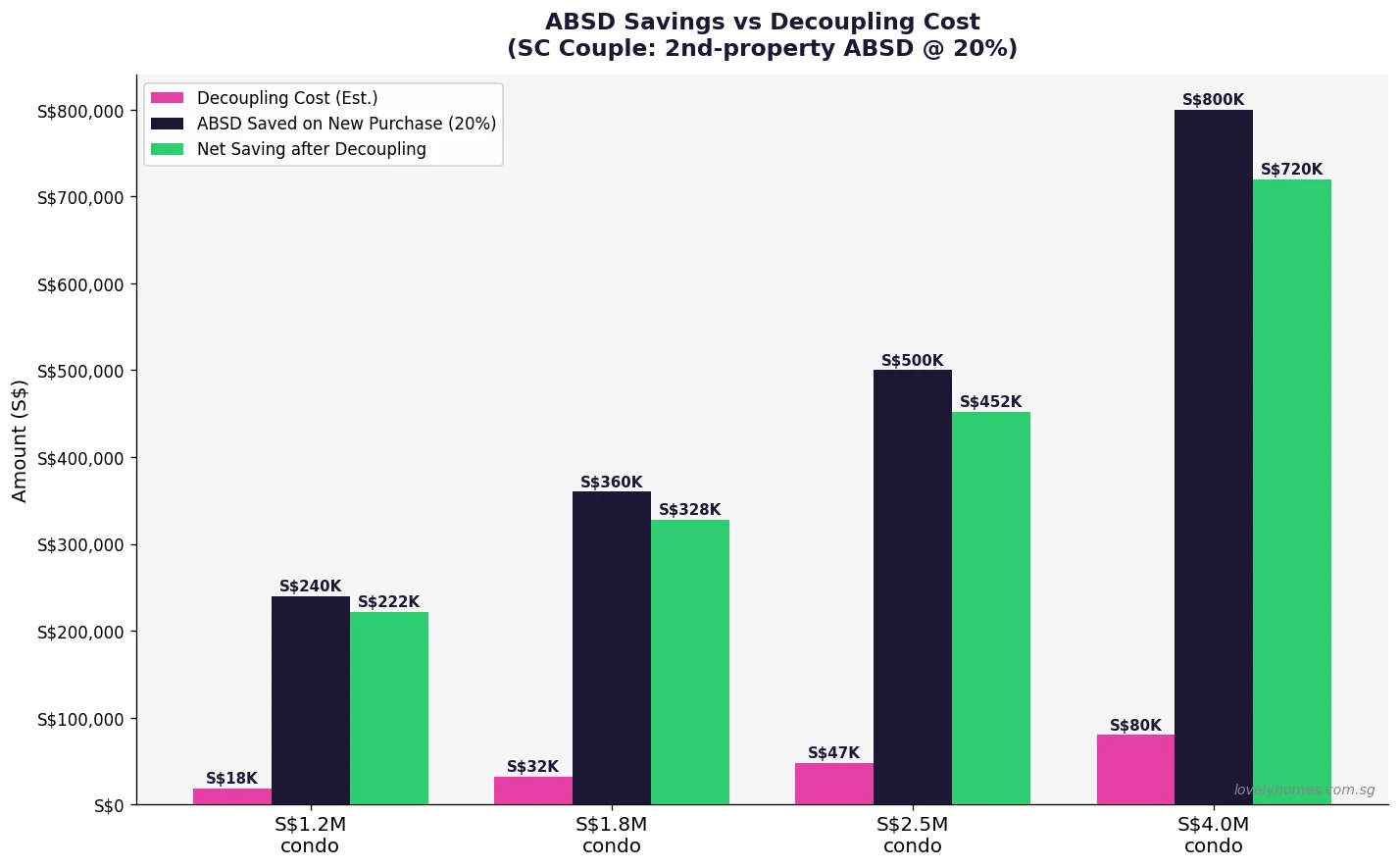

- A Deed of Severance (if converting from JT to TiC first) or direct transfer deed.

- Buyer’s Stamp Duty (BSD) on the value of the share transferred. For a S$1.8 million condo, a 50% share transfer attracts BSD on S$900,000 — approximately S$24,600.

- ABSD on the share transferred — this is generally nil if the transferring co-owner is disposing of their only property interest, but care must be taken around whether they hold any other property interests.

- CPF refund: The transferring owner must refund their CPF principal and accrued interest to their OA at the time of transfer.

- Bank refinancing: The remaining owner must demonstrate sufficient TDSR headroom to service the loan as sole borrower. This is the most common practical barrier to decoupling.

- Legal fees: Typically S$3,000–S$6,000 for the full decoupling exercise.

For a detailed analysis of decoupling costs and worked examples, see our dedicated guide: Singapore Property Decoupling Guide 2026.

Joint Ownership, Death and Divorce

On death under JT: Title vests in the surviving joint tenant(s) automatically by the right of survivorship. The surviving owner must notify SLA, HDB (for HDB flats), and the bank, and submit the required documentation (death certificate, SD/5 or equivalent form for SLA). There is no need to engage the courts for a Grant of Probate in respect of the property itself. However, as noted, CPF monies are returned to the deceased’s estate and must be distributed via their CPF nomination or Will.

On death under TiC: The deceased’s share forms part of their estate. If they have a valid Will, the share will be distributed according to its terms after Grant of Probate. If there is no Will, the share is distributed under the Intestate Succession Act — which specifies default distribution rules based on family relationships (e.g. spouse, children, parents). Probate proceedings typically take two to six months. During this period, the property cannot be sold or transferred without a court order.

On divorce: Jointly owned property — whether HDB or private — becomes a matrimonial asset subject to division by the Family Justice Courts (FJC) under the Women’s Charter. The court has broad discretion to order sale of the property and division of proceeds, or transfer of one spouse’s share to the other. Considerations include the length of the marriage, each party’s financial contributions, and the welfare of any children.

For HDB flats on divorce, both parties lose their first-timer status. Any CPF Housing Grants (EHG, AHG, Family Grant) received are subject to clawback. The departing spouse must refund their CPF principal and accrued interest. If the receiving spouse wishes to purchase another HDB flat subsequently, they will be treated as a second-timer buyer with the associated restrictions.

Worked Example: SC Couple — JT vs TiC and the ABSD Upgrade Decision

The Lim Family — Choosing Between JT and TiC for a Private Condo Purchase

Profile: Mr Lim (SC, owns HDB Sengkang 4-room, MOP cleared 2024) and Mrs Lim (SC, no other property). Joint gross income S$16,000/month.

Target: 3-bedroom private condo in District 19, S$2,000,000.

Option A — Joint purchase of condo (both on title):

- Mr Lim is a second-time property owner (owns HDB) → ABSD rate = 20% SC second property

- ABSD on full purchase price: 20% × S$2,000,000 = S$400,000 upfront

- BSD: S$74,600

- ABSD remission: sell HDB within 6 months of SPA → recover S$400,000

- Risk: if HDB cannot be sold within 6 months, ABSD is forfeited

- Bank loan: 75% LTV = S$1,500,000 @ 3.0% over 30 years → S$6,321/mth; TDSR 39.5% — PASS

Option B — Decouple HDB first, Mrs Lim buys condo as sole purchaser:

- Step 1: Decouple HDB. Mr Lim transfers his 50% share to Mrs Lim. BSD on S$550K (50% of S$1.1M HDB value) ≈ S$11,400. ABSD nil (Mr Lim disposing of only property). CPF refund by Mr Lim: principal + accrued interest ≈ S$130,000 to his OA. Mrs Lim’s TDSR must support full HDB loan as sole borrower.

- Step 2: Mr Lim (now owning nothing) buys the S$2M condo as a first-time buyer: ABSD = 0%. BSD = S$74,600.

- Total stamp duty: S$11,400 (HDB transfer BSD) + S$74,600 (condo BSD) = S$86,000

- Saving vs Option A (net of remission): decoupling saves S$0 upfront ABSD vs A’s remission — but eliminates the remission timing risk entirely and allows Mr Lim to retain the HDB as a rental property (MOP cleared). Net rental yield on S$1.1M HDB estimated at 4.2% per annum.

- Practical constraint: Mrs Lim must qualify under TDSR for HDB loan solo. At S$8,000 income, HDB loan maximum at 30% MSR for 25 years ≈ S$696K. HDB outstanding balance ~S$260,000 — well within limit. ✅

Recommended approach: For couples where keeping the HDB as a rental property is financially viable and the TDSR supports solo HDB ownership, decoupling and a clean first-purchase of the private property is generally more tax-efficient and risk-free than the simultaneous purchase + ABSD remission route. The key question is always whether the remaining co-owner’s TDSR supports solo mortgage servicing.

Summary: Joint Ownership Rules at a Glance

| Feature | Joint Tenancy | Tenancy in Common |

|---|---|---|

| Ownership shares | Equal and undivided | Any proportion agreed |

| On death | Right of survivorship — auto-transfer | Passes via Will / ISA — probate needed |

| CPF on death | Refunded to estate (not survivorship) | Refunded to estate |

| Estate planning | Cannot bequeath by Will | Can bequeath TiC share by Will |

| HDB flat default | JT (married couples) | Available by request |

| ABSD basis | Higher ownership count of any co-owner | Higher ownership count of any co-owner |

| Decoupling / Severance | Convert to TiC → transfer share | Transfer share directly by deed |

| Suitable for | Married couples, simple estate | Investors, co-buyers, complex estates |

What Might Change: Policy Outlook for Joint Ownership 2026

Singapore’s legal framework for co-ownership — rooted in English common law and codified in the Conveyancing and Law of Property Act (Cap. 61) and the Land Titles Act (Cap. 157) — has remained stable for decades. There are no announced reforms to the JT/TiC framework as at June 2026.

However, the ABSD framework governing joint purchases has evolved significantly since 2021. The April 2023 increase in foreigner ABSD to 60% was a major shift that effectively eliminated most mixed SC-foreigner joint property purchases in Singapore. The rule that the higher-ownership-count co-owner’s ABSD rate applies to the full purchase price has remained unchanged, and the government has shown no signs of softening this position given the property market’s continued strength.

Decoupling as an ABSD-reduction strategy has attracted increased scrutiny from IRAS since 2021. While decoupling remains a legitimate tax planning technique as at June 2026, IRAS has the power to disregard transactions that appear to be purely tax-motivated under its general anti-avoidance provisions. Property owners considering decoupling should ensure there is a genuine, non-tax rationale (such as portfolio management, retirement planning, or change in financial circumstances) and should take legal advice before proceeding.

Frequently Asked Questions

If I hold a property under Joint Tenancy and my co-owner dies, do I pay ABSD?

No — the transfer of title from a deceased joint tenant to the surviving joint tenant(s) by the right of survivorship is not a “purchase” and does not trigger ABSD. However, it is a dutiable transaction for stamp duty purposes under the Stamp Duties Act. The surviving owner must attend to the transmission of title at the Singapore Land Authority (SLA) and will need to pay a nominal transmission fee; this is not the same as stamp duty on a purchase. The surviving owner should also notify the bank and CPF Board of the change in ownership circumstances.

Can a foreigner co-own an HDB flat with a Singapore Citizen?

No. HDB flats — both BTO and resale — may only be purchased by Singapore Citizens and, in certain circumstances, Singapore Permanent Residents. Foreigners (i.e. non-Citizens, non-PRs) are not eligible to purchase or co-own HDB flats under any scheme. The restriction applies regardless of whether the other co-purchaser is a SC or SPR. Foreigners who wish to own residential property in Singapore may do so through private condominiums, apartments or (with Singaporeland Authority approval) restricted residential property, but not HDB flats or Executive Condominiums during their MOP period.

What happens to ABSD if I add or remove a co-owner from an existing property title?

Adding a co-owner to an existing property title is treated as a partial purchase by the incoming co-owner. BSD and potentially ABSD will apply on the value of the share being acquired, based on the incoming co-owner’s buyer profile and existing property ownership count. For example, if a SC who already owns two properties is added as a co-owner, they will pay the third-property ABSD rate (30% for SC as at June 2026) on the value of the share they are acquiring. Removing a co-owner (transferring their share to the remaining owner) triggers BSD — and potentially ABSD — on the transferring share in the hands of the receiving owner, based on their profile and ownership count at the time of transfer.

If my spouse and I hold our HDB flat under Joint Tenancy, can we sever it to Tenancy in Common for a decoupling exercise?

Yes — HDB permits the conversion of a joint tenancy to a tenancy in common (and vice versa) for HDB flats, subject to HDB’s approval. The process requires both owners to apply to HDB and to engage solicitors to prepare the relevant deed. Once converted to TiC, one co-owner can transfer their share to the other, triggering BSD on the transferred portion. ABSD on the transfer will depend on the profiles of both parties at the time of the transfer — if the transferring owner is disposing of their only property interest, ABSD is generally nil on that transfer. The receiving owner’s ABSD position on any subsequent purchase depends on their resultant ownership count after the transfer is completed.

Can my partner and I — unmarried — purchase an HDB flat jointly?

Unmarried couples below the age of 35 may purchase an HDB BTO flat jointly only if both are Singapore Citizens and they qualify under the Fiancé/Fiancée Scheme (they must marry within three months of key collection). Otherwise, unmarried couples generally do not qualify for joint HDB BTO purchases. Unmarried Singapore Citizens aged 35 and above may purchase a 2-room Flexi flat in a non-mature estate under the Single Singapore Citizen (SSC) scheme, but only as a single buyer — not jointly with an unmarried partner. For resale HDB flats, unmarried couples may apply under the Non-Citizen Spouse Scheme or the Joint Singles Scheme if both are Singapore Citizens and both are aged 35 or above.

What is the ABSD implication of inheriting a property share under Tenancy in Common?

Inheriting a property share under a deceased’s Will or intestacy does not trigger ABSD — inheritance is not a purchase. However, the inherited share is counted as a property interest for future ABSD purposes. If you inherit a 50% TiC share in a condominium, you are now treated as owning that property for ABSD purposes. Any subsequent property purchase you make will be assessed as a second (or later) property purchase, with the corresponding ABSD rate. You may choose to disclaim the inheritance to avoid this ABSD impact, but you should take legal and financial advice before doing so, as disclaimer is irrevocable.

How does a Lasting Power of Attorney (LPA) interact with jointly owned property?

A Lasting Power of Attorney (LPA) registered under the Mental Capacity Act (Cap. 177A) allows a person (the “donor”) to appoint a trusted individual (the “donee”) to make decisions about their personal welfare and/or property and financial affairs if the donor loses mental capacity. An LPA donee with authority over property and financial affairs can deal with the donor’s share of a jointly owned property — including signing sale and purchase agreements — on the donor’s behalf. For JT property, the donee can act in respect of the donor’s JT interest. For TiC property, the donee can deal with the donor’s defined share. HDB requires the Office of the Public Guardian’s endorsed LPA before it will process transactions involving a co-owner who lacks mental capacity.

Tags: joint tenancy Singapore, tenancy in common Singapore, joint ownership property Singapore 2026, ABSD joint purchase, decoupling ABSD, Singapore property co-ownership, JT vs TiC, CPF joint property, Singapore property inheritance, joint ownership divorce Singapore, joint property ownership rules 2026