HDB BTO Application Process Singapore 2026: Step-by-Step Guide from Eligibility to Keys

- BTO stands for Build-to-Order — HDB launches new flats for sale before construction begins, then builds only the units that were successfully balloted and purchased.

- BTO exercises are held quarterly (typically February, May, August and November) with application windows of about two weeks per exercise.

- Eligibility requirements include Singapore Citizenship (at least one SC in a family nucleus), minimum age 21 for families (35 for singles), and a monthly household income cap of S$7,000 (2-room/3-room) or S$14,000 (4-room and above).

- Successful applicants receive a queue number via ballot — first-timers receive priority balloting chances.

- Construction typically takes 3 to 4 years from booking to keys collection.

- CPF Housing Grants — the Additional CPF Housing Grant (AHG), Proximity Housing Grant (PHG), and Enhanced CPF Housing Grant (EHG) — can reduce your purchase price by up to S$80,000 or more, depending on income and family situation.

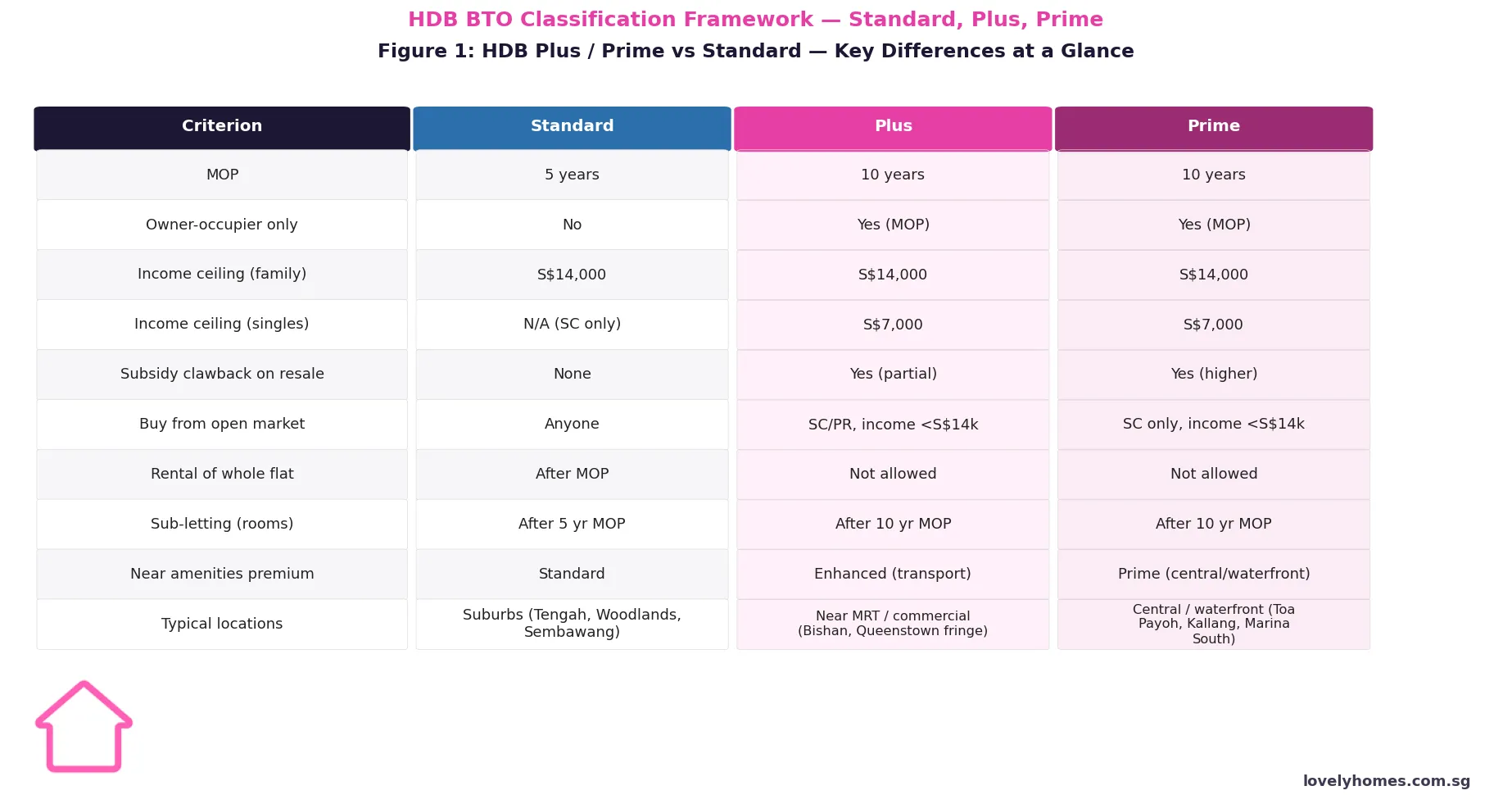

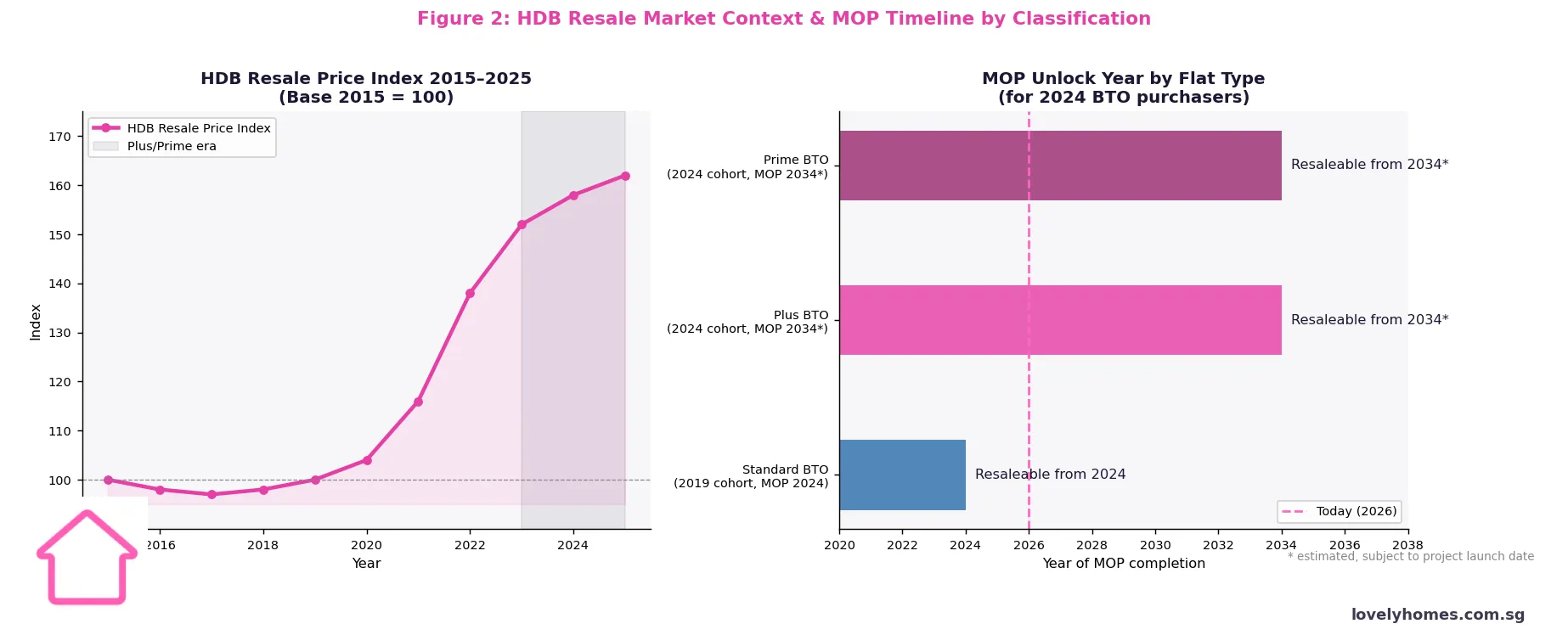

- Under the 2023 reclassification, BTO flats are now categorised as Standard, Plus or Prime, each carrying different subsidy levels, Minimum Occupation Periods (MOP) and resale restrictions.

- You can only own one HDB flat at a time; buying a BTO requires you to dispose of any existing private property within six months of key collection.

What is the HDB BTO Scheme?

The Housing and Development Board’s Build-to-Order (BTO) scheme is the primary pathway for Singapore Citizens to purchase a subsidised new public housing flat. Unlike a developer pre-sale, where a developer speculates on demand, the BTO model means HDB constructs only those units that have been successfully applied for and paid a deposit on — dramatically reducing the risk of oversupply and keeping public housing prices aligned with demand.

In any given BTO exercise, HDB offers flats across several estates, ranging from mature towns such as Bishan and Queenstown to non-mature estates such as Tengah, Sembawang and Punggol. As of 2023, flats are further classified as Standard, Plus or Prime under the HDB Flat Classification Framework (RFC), with Plus and Prime flats attracting tighter resale restrictions and longer Minimum Occupation Periods (MOP) in exchange for larger subsidies in higher-demand locations.

Step 1: Check Your Eligibility

Before you apply for a BTO flat, you must satisfy HDB’s eligibility criteria. Failing to check these upfront can mean losing your application fee or, worse, having to return a flat after booking.

Citizenship: At least one person in the family nucleus must be a Singapore Citizen. A Singapore Permanent Resident (SPR) spouse may co-apply, but both buyers cannot be SPR if applying as a family — the SC must be the primary applicant.

Age: For family applications, the minimum age is 21 years old. For Joint Singles Scheme (JSS) applicants (two or more unrelated singles buying together), the minimum age is 35. Single applicants buying a 2-room Flexi flat must also be at least 35.

Income ceiling: There is a gross monthly household income ceiling, assessed over the preceding 12 months. For 2-room and 3-room flats, the ceiling is S$7,000. For 4-room flats and larger, the ceiling is S$14,000. For 2-room Flexi flats under the Single scheme, the ceiling is S$7,000 per single applicant.

Property ownership: You must not own any private residential property locally or overseas. If you or your co-applicant currently owns or has recently sold a private property, an MOP or 15-month wait-out period may apply before you are eligible to apply for a BTO. HDB also requires that you must not have previously sold an HDB flat within the past 30 months under certain grant conditions.

Relationship status: BTO flats under the Public Scheme require a valid family nucleus — married couples, engaged couples (intent to marry), parent(s) with children, siblings, or parent(s) with unmarried children. Single applicants are restricted to 2-room Flexi flats in non-mature estates.

Step 2: Research Estates and Flat Types

Once you confirm eligibility, the next step is to decide where and what type of flat to target. HDB publishes details about upcoming BTO exercises on the HDB website and the HDB Flat Portal several weeks before the application window opens.

Key considerations include estate maturity (mature vs non-mature affects grant eligibility and historical resale values), flat classification (Standard/Plus/Prime determines MOP and resale restrictions), proximity to your parents’ home (important for the Proximity Housing Grant), school catchment areas, and transport connectivity.

It is worth shortlisting two or three options across different exercises — if your first-choice ballot is unsuccessful, having a backup plan reduces the wait time significantly.

Step 3: Apply Online During the Exercise Window

BTO applications are submitted online through the HDB Flat Portal (flatportal.hdb.gov.sg) during the application window, which is typically open for approximately two weeks. You cannot walk into an HDB branch to apply — the entire process is digital.

Each application requires a non-refundable application fee of S$10 per application. You may only submit one application per exercise. You can, however, apply for different flat types within the same exercise (e.g., a 4-room in Estate A and a 5-room in Estate B), though you will need to choose one if both succeed.

During the application, you will need your NRIC, co-applicant details, income documents (for grant assessment), and declarations of property ownership. HDB’s MyHDBPage and SingPass integration allow most fields to be pre-filled.

Step 4: Receive Your Ballot Queue Number

Approximately two months after the application window closes, HDB releases ballot results. You will receive an email and SMS notification if you have been successful in the ballot. Your queue number determines your booking appointment date — a lower queue number means you get to choose from a larger pool of available units.

First-timer priority: HDB reserves 85–95% of units in most exercises for first-timers (those who have never previously bought a subsidised flat). Second-timers and seniors compete for the remaining quota. First-timers who are unsuccessful in five or more exercises are granted Deferred Income Assessment (DIA) status, making their next application more competitive.

If you receive a queue number but it is too high for the number of available units, you are treated as a non-selection — your first-timer count is preserved, and you can try again in the next exercise without losing any priority status.

Step 5: Attend the Flat Selection Appointment

When your queue number is called, you will be invited to a flat selection appointment at the HDB Hub or via the HDB Flat Portal (for later exercises, HDB has digitised this step). You must bring your NRIC, the original signed declarations, and supporting income documents.

At this appointment, you will see the remaining available units on a real-time availability display, select your preferred unit, and pay a non-refundable booking fee: S$500 for 2-room Flexi, S$1,000 for 3-room, and S$2,000 for 4-room and larger. Choosing wisely matters — floor level, facing, proximity to lift lobbies, and stack orientation all affect both your living experience and eventual resale value.

Step 6: Sign the Agreement for Lease (AFL)

Approximately four to six months after your flat selection, HDB will invite you to sign the Agreement for Lease (AFL). This is the binding contract that commits you to purchasing the flat. At the signing, you will also pay the down-payment:

- If using an HDB concessionary loan (up to 80% LTV): down-payment = 20% of purchase price (can be fully paid from CPF Ordinary Account).

- If using a bank loan (up to 75% LTV): minimum 25% down-payment, of which at least 5% must be cash, and the remaining 20% can be CPF OA.

CPF Housing Grants (AHG, PHG, EHG) are disbursed at this stage, reducing your outstanding loan amount. Your HDB loan eligibility letter (HLE) or bank’s Letter of Offer must be in hand by the AFL signing date.

Step 7: Await Construction

Once the AFL is signed, construction begins (or continues — some exercises have already broken ground). The typical BTO construction timeline is 3 to 4 years, though projects in mature estates can sometimes run slightly longer due to more complex site conditions. HDB publishes progress updates via the My HDBPage portal, and you can track construction milestones — superstructure completion, temporary occupation permit (TOP) application, and handover dates — online.

During this period, most buyers continue living in their existing home. If you are renting, factor the construction period into your rental budget. If you sold an HDB flat to apply, you would typically have arranged for a Temporary Extension of Stay or moved into alternative accommodation.

Step 8: Keys Collection and Final Payment

When the development receives its TOP, HDB will contact you to book a keys collection appointment. You will need to pay the balance of your purchase price (minus down-payment and grants already applied), and your bank loan will be disbursed to HDB at this stage. Your CPF Ordinary Account will also be debited for the approved CPF usage amount.

At the appointment, you will inspect the flat, receive your keys, and sign the Lease in Escrow document. The Minimum Occupation Period (MOP) clock begins from the date of key collection — 5 years for Standard flats, and 10 years for Plus and Prime flats under the 2023 framework.

Summary Table: BTO Application Process at a Glance

| Stage | Timing | Key Action | Cost / Payment |

|---|---|---|---|

| Check eligibility | Before exercise | Confirm citizenship, age, income, property status | Free |

| Research & decide | Before exercise | Shortlist estates, flat types, classification | Free |

| Apply online | Exercise window (~2 wks) | Submit via HDB Flat Portal | S$10 (non-refundable) |

| Ballot result | ~2 months post-exercise | Receive queue number (if successful) | Nil |

| Flat selection | When queue called | Choose unit; pay booking fee | S$500–S$2,000 |

| AFL signing | ~4–6 mths after booking | Sign Agreement for Lease; pay down-payment | 20% (HDB loan) or 25% (bank loan) |

| Construction | ~3–4 years | Monitor progress on MyHDBPage | Progress payments if applicable |

| Keys collection | Upon TOP | Inspect flat; sign Lease in Escrow; pay balance | Balance purchase price (via CPF/cash/loan) |

Worked Example: The Lims Apply for a 4-Room BTO

Mr and Mrs Lim are a Singapore Citizen couple, both aged 29, with a combined gross monthly income of S$8,500. They are first-time applicants with no prior HDB flat ownership and no private property. They are interested in a 4-room Standard BTO flat in Tengah, priced at S$380,000.

Eligibility check: Both SC ✓. Age 29 (≥ 21) ✓. Combined income S$8,500 < S$14,000 ceiling ✓. No property ownership ✓. Married ✓. They qualify.

Grants:

- Enhanced CPF Housing Grant (EHG): Based on S$8,500/mth income, they qualify for an EHG of approximately S$35,000 (EHG tapers from S$80,000 at S$4,500 income to S$5,000 at S$9,000 income — the exact amount for S$8,500 is S$35,000 per the CPF Board’s schedule).

- Proximity Housing Grant (PHG): If Mrs Lim’s parents live within 4km of Tengah (non-mature estate threshold), they receive an additional S$20,000 PHG.

- Total grants: S$55,000

Net purchase price: S$380,000 – S$55,000 = S$325,000.

Financing via HDB loan: HDB loan maximum at 80% LTV = S$260,000. Down-payment 20% = S$65,000, fully payable from CPF OA. Monthly repayment at HDB concessionary rate (currently 2.60% p.a.) over 25 years: approximately S$1,175/month. MSR check: S$1,175 / S$8,500 = 13.8% — well below the 30% MSR cap. ✓

Timeline: They apply in the August 2026 BTO exercise. Ballot result in October 2026. Flat selection appointment in December 2026 (assuming low queue number). AFL signing mid-2027. Keys collection estimated Q4 2030. MOP ends Q4 2035 (Standard flat, 5-year MOP), after which they may sell on the open market or upgrade to a private property.

CPF Housing Grants in Detail

Singapore’s CPF Housing Grant framework for BTO buyers in 2026 encompasses three main components. The Enhanced CPF Housing Grant (EHG) is the most significant, providing up to S$80,000 for families earning S$4,500/month or less, tapering to S$5,000 for those just below the income ceiling. The EHG is available for both new BTO and resale flat purchases.

The Additional CPF Housing Grant (AHG) applies to buyers earning S$5,000/month or less and provides an additional S$5,000 to S$40,000 depending on income and flat type. The Proximity Housing Grant (PHG) rewards buyers who choose to live near their parents — S$30,000 if within 4km of parents, S$20,000 if living with parents. All grants are disbursed by the CPF Board directly to HDB at the AFL stage and reduce your outstanding loan principal.

What Might Change

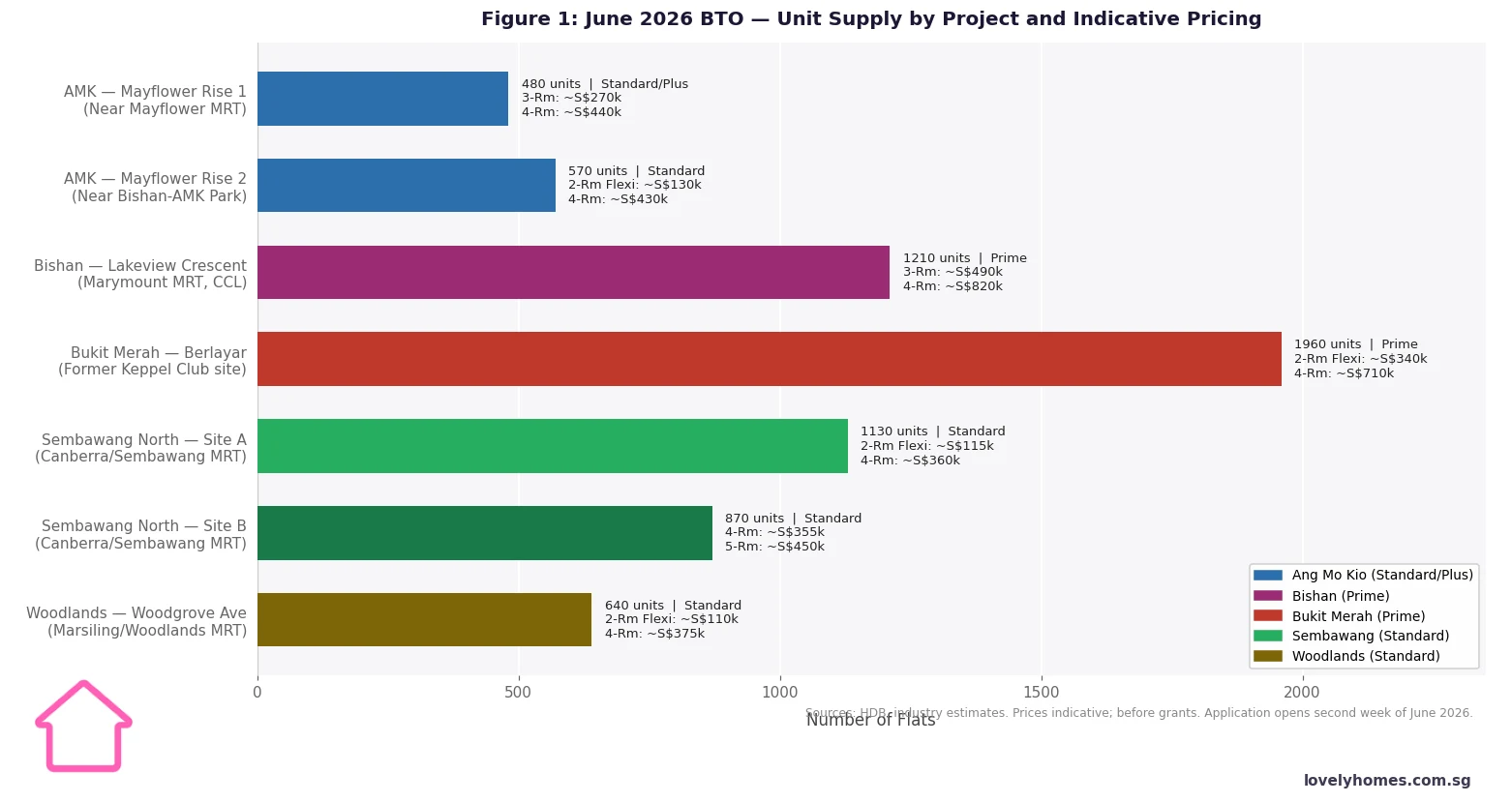

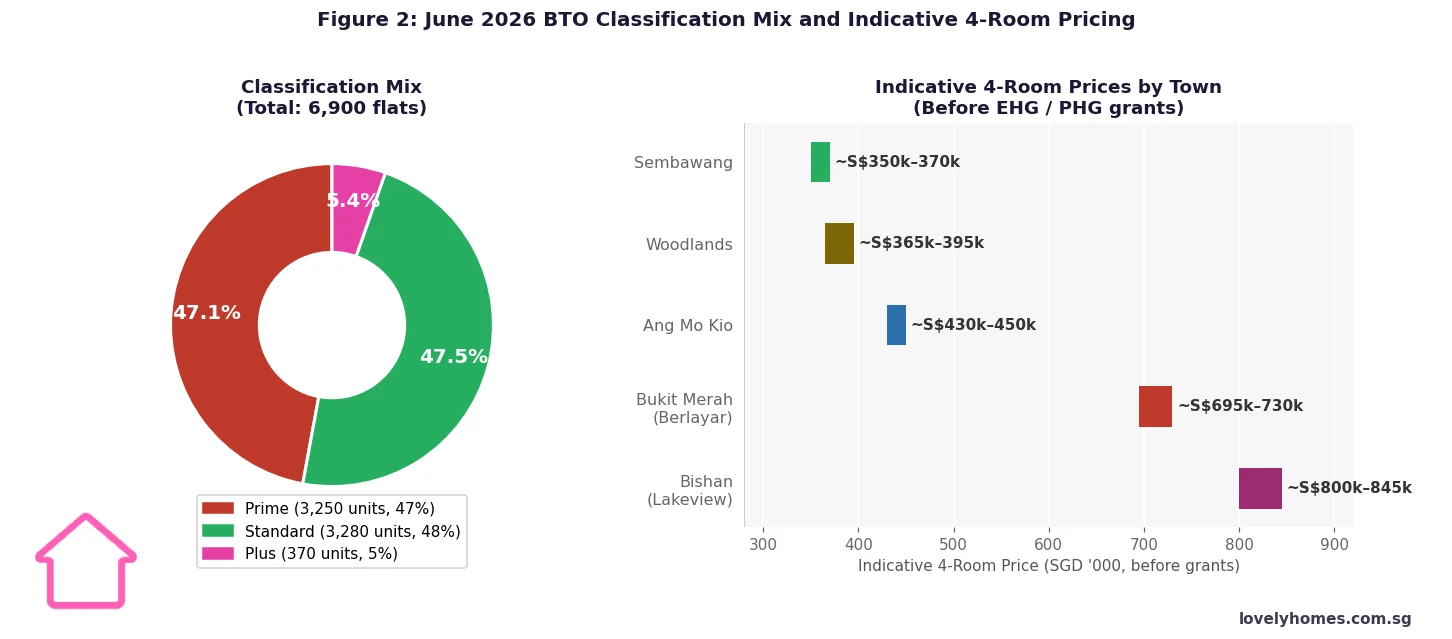

HDB has signalled that BTO supply will remain elevated through 2026 and 2027, with approximately 19,000 to 23,000 flats planned annually, partly to address pent-up demand from pandemic delays. The June 2026 exercise (6,900 flats) is already confirmed. Looking ahead, BTO exercises from 2027 may gradually incorporate more Plus and Prime developments as Tengah and Jurong Lake District mature. Any adjustment to the MSR or income ceiling thresholds — last revised in 2019 for the S$14,000 cap — would be flagged by HDB well in advance of any exercise.

Frequently Asked Questions

How many times can I apply for a BTO before losing first-timer priority?

There is no hard limit on the number of applications a first-timer can submit. However, if you are unsuccessful in five or more BTO exercises as a first-timer, you receive Deferred Income Assessment (DIA) status, which improves your priority in subsequent applications. Additionally, HDB periodically grants enhanced priority to first-timers who have been waiting for an extended period. Your first-timer status is maintained until you successfully purchase a subsidised flat.

Can I apply for BTO if I currently own a private property?

You are not eligible to apply for a BTO flat if you currently own any private residential property in Singapore or overseas. You must dispose of the private property — and complete the sale — before you can apply. Additionally, if you or your co-applicant has disposed of a private property within the last 15 months (the wait-out period introduced in September 2022), you are also ineligible until the 15-month cooling period expires.

What is the difference between HDB concessionary loan and a bank loan for BTO?

An HDB concessionary loan is offered by HDB directly at a rate of 0.10% above the CPF Ordinary Account interest rate, currently 2.60% per annum (fixed quarterly). It allows up to 80% LTV, and the entire down-payment (20%) can be funded from CPF OA with no cash component required. A bank loan offers potentially lower rates (SORA-linked, often 2.8–3.5% in 2026) but is capped at 75% LTV, requires at least 5% cash as down-payment, and rates are variable. For most first-time BTO buyers, the HDB loan’s stability and zero-cash-down-payment requirement make it the simpler initial choice.

What is the MOP and does it differ by flat classification?

The Minimum Occupation Period (MOP) is the period you must live in the flat as your principal residence before you are allowed to sell it on the open market or rent out the entire flat. For BTO flats launched from 2024 onwards under the new classification framework: Standard flats carry a 5-year MOP (unchanged); Plus and Prime flats carry a 10-year MOP. During the MOP, you may rent out individual bedrooms (but not the entire flat). Violations of MOP rules — such as not residing in the flat for extended periods without HDB approval — can result in HDB repossessing the flat.

Can singles buy a BTO flat?

Yes, but with restrictions. Single Singapore Citizens aged 35 and above may apply for a 2-room Flexi flat in non-mature estates under the Single Singapore Citizen (SSC) Scheme. They are also eligible for the Enhanced CPF Housing Grant (EHG) at a capped income of S$7,000/month. Singles cannot apply for 3-room or larger BTO flats under the single scheme. Two or more unrelated singles aged 35+ may apply together under the Joint Singles Scheme (JSS) for 2-room Flexi or 3-room flats (the latter in non-mature estates only).

What happens if I cannot collect my keys when called?

If you are unable to attend the keys collection appointment, you must inform HDB in advance. HDB will generally allow one deferment for medical or work-related reasons, but cannot defer indefinitely. If you fail to collect your keys and pay the balance without an acceptable reason, HDB may cancel the Agreement for Lease and forfeit your booking fee. In practice, HDB is willing to accommodate reasonable requests — contact them early if your circumstances change.

How is the BTO purchase price determined?

HDB prices BTO flats at a subsidised rate below market value, with the subsidy embedded in the initial selling price. The price is set by HDB based on the comparable resale values in the surrounding estate, adjusted downward for the subsidy. This is why BTO prices can vary significantly between a Standard flat in Tengah and a Prime flat in Queenstown with similar floor areas — the Prime flat’s price reflects the higher land value and deeper subsidy given. When you eventually sell the flat, you sell at open market value (minus applicable CPF accrued interest repayment), so the subsidy is effectively recouped by the nation through the resale market over time.

Related Articles

- HDB June 2026 BTO Launch Guide: 6,900 Flats in Sembawang, Bishan, Punggol, Queenstown and Tengah

- HDB Plus and Prime Flats Singapore 2026: What the BTO Classification Means for Buyers

- HDB MOP Singapore 2026: Minimum Occupation Period Rules for Standard, Plus and Prime Flats

- CPF Housing Grant for Resale Flats Singapore 2026: EHG, PHG and Family Grant Explained

- TDSR and MSR Singapore 2026: How Much Can You Borrow for Your Home?

- CPF for Property Purchase Singapore 2026: Ordinary Account, Withdrawal Limit and Housing Rules

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer

This article is for general informational and educational purposes only. It does not constitute financial, legal, or property advice. HDB BTO eligibility criteria, grant amounts, income ceilings, MOP rules, and application procedures cited reflect publicly available information from the Housing and Development Board (HDB) and CPF Board as at May 2026. Rules and thresholds are subject to change. Readers should verify current information at hdb.gov.sg and consult a licensed financial adviser, HDB-approved mortgage specialist, or conveyancing solicitor before making any property decisions.

Click anywhere outside to close