Quick Answer — the 2026 supply squeeze in 30 seconds

Singapore’s 2026 private condo launch pipeline is estimated at 17 projects / ~8,100 units — a 30% year-on-year drop.

This is the tightest launch pipeline since 2014 and drives pricing power back to sellers in resale and to developers in new launches.

Q1 2026 URA private PPI rose 0.3% quarter-on-quarter — the softest quarterly print in six quarters but still positive in a thin market.

The OCR led the quarter (+1.3% QoQ); the RCR and CCR posted smaller gains.

Absorption of the 2026 tranche is expected to be above 65% within launch quarter for projects priced within 3% of resale comps.

The pipeline is materially thinner — here is the number

Industry-collated data for the 2026 private condominium launch calendar shows roughly 17 confirmed new projects bringing about 8,100 units to market. That is a 30% year-on-year decline from the roughly 23 projects and 11,000+ units launched in 2025, and well below the 25,000+ units delivered annually during the 2013–2015 supply bulge. Confirmed-list Government Land Sales tenders have also leaned selective, meaning the thinner supply is unlikely to be back-filled by late 2026 GLS awards landing before 2028.

For context, the Monetary Authority of Singapore’s last Financial Stability Review (November 2025) flagged a re-normalising pipeline as supportive of price discipline. URA’s Q1 2026 flash estimate — a 0.3% quarter-on-quarter increase in the Private Property Price Index, the softest in six quarters — is being read by market analysts as the product of a thin but transacting market: fewer launches, steady take-up, no fire-sale.

Why supply collapsed

Three factors explain the 2026 crunch:

GLS confirmed-list discipline in 2023–2024. The confirmed-list parcels tendered during that period were smaller and more location-specific (River Valley Green, Clementi Avenue 1, Zion Road, Faber Walk). Fewer mega-plots means fewer mega-launches, which compresses the headline unit count.

Interest-rate overhang on developer breakevens. Higher cost of construction finance from 2022 through early 2025 kept developers cautious on site accumulation. Only the strongest balance sheets — CDL, Frasers, UOL, City Developments, Wing Tai, Allgreen, Frasers Property, SingHaiyi and a handful of JV partners — acquired in the window. The rest sat out.

En-bloc market remaining selective. Large collective sales drove much of the 2017–2019 pipeline; that channel has materially thinned in the current cycle. Owners’ reserve prices have risen faster than developer bid discipline, so en-bloc deal count has stayed low.

What the supply crunch means for prices

Historical precedent is instructive. The last sustained supply tightening (2014–2016, when unsold inventory fell from ~32,000 to under 20,000 units) preceded the sharp 2017–2018 price run-up. The current setting is not identical — credit conditions are tighter, ABSD is higher, TDSR is binding — but the directional implication is the same: thin supply supports pricing power in the following 12–24 months.

Worked example — what a 30% supply drop does to take-up maths

Assume annual new-launch absorption of 7,500–9,000 units based on the 2021–2024 average. With 8,100 units launching in 2026, theoretical absorption coverage is close to 100% of launch inventory within 12 months. Any launch priced within 3% of resale comps has a first-weekend take-up expectation of 40%–65%.

Regional read — OCR leads, CCR warms up

URA’s Q1 2026 flash estimate showed the Outside Central Region up 1.3% quarter-on-quarter — the strongest of the three sub-markets. The Rest of Central Region rose 0.9%. The Core Central Region, which had previously lagged, gained 0.4% from a low base, rebounding off its earlier decline. For a thin launch year, the flash estimates confirm two patterns: the OCR retains the mass-market depth that absorbs any supply, and the CCR is now price-competitive enough to re-attract both local upgraders and renewed foreign interest at the margin (within ABSD constraints).

Region

Q1 2026 QoQ

Q4 2025 QoQ

OCR

+1.3%

+1.2%

RCR

+0.9%

+0.6%

CCR

+0.4%

−0.2%

Q1 2026 numbers are flash estimates. URA will publish final statistics on 24 April 2026. Q4 2025 numbers are URA final.

What this means for buyers

First-time buyers should not wait for a supply glut that is unlikely to arrive. The combination of thin launches, still-positive PPI, and elevated interest rates means “wait-and-see” becomes expensive. Lock in on fair-valued new launches with a 12–18-month horizon; prioritise project quality and transit connectivity over chasing the lowest psf.

Upgraders face a cleaner market. Resale stock for HDB owners remains active (the HDB RPI slipped 0.1% in Q1 but the million-dollar category continued to set records, signalling a bifurcating resale market). Sequence the sale of the HDB before the new-launch OTP; the ABSD Remission window for second-property purchases only works when you document divestment within 6 months.

Investors should revisit the rental-yield arithmetic. OCR launches near MRT continue to show 4.0%–4.5% gross yields. With supply tight and demand resilient, net-yield maths at 2026 financing rates is at its tightest — but improving from 2024 troughs as rental growth has restarted.

What this means for sellers

Thin supply plus steady price discovery is the most favourable sellers’ market in three years. Two practical implications: (a) price your resale 1%–3% above the last-six-months median rather than at median; (b) stock ready by mid-year if you want to transact before the final-quarter launch cluster. Buyers who are priced out of new launches at psf premiums over resale will migrate to equivalent-aged resale.

Key takeaway

A 30% launch-supply drop does not translate into a 30% price rise — TDSR, ABSD and the wider macro will contain that. It does translate into narrower negotiation room for buyers, faster take-up for well-priced launches, and cleaner sell-through for well-prepared resale stock. Plan your transaction around these dynamics rather than waiting for a correction that the supply data does not support.

Disclaimer: Market statistics cited are from publicly available URA, HDB and MAS publications as at publication date. Pipeline counts for 2026 are industry estimates subject to revision as developers confirm launch timelines. This article is commentary only and not a recommendation to transact. LovelyHomes is an independent editorial publication.

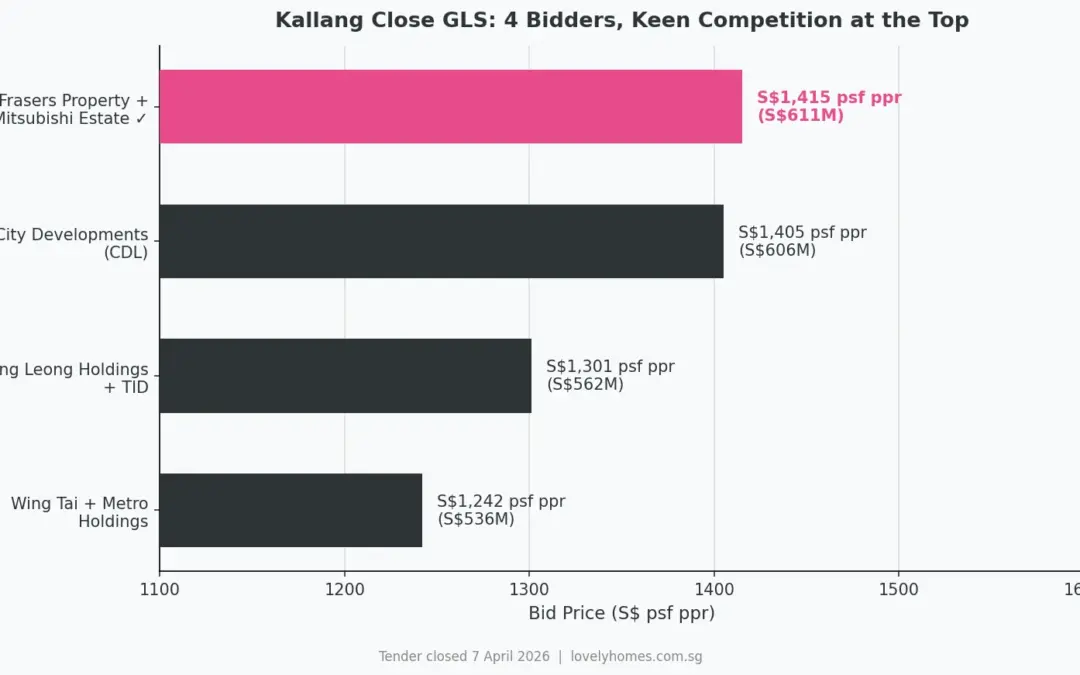

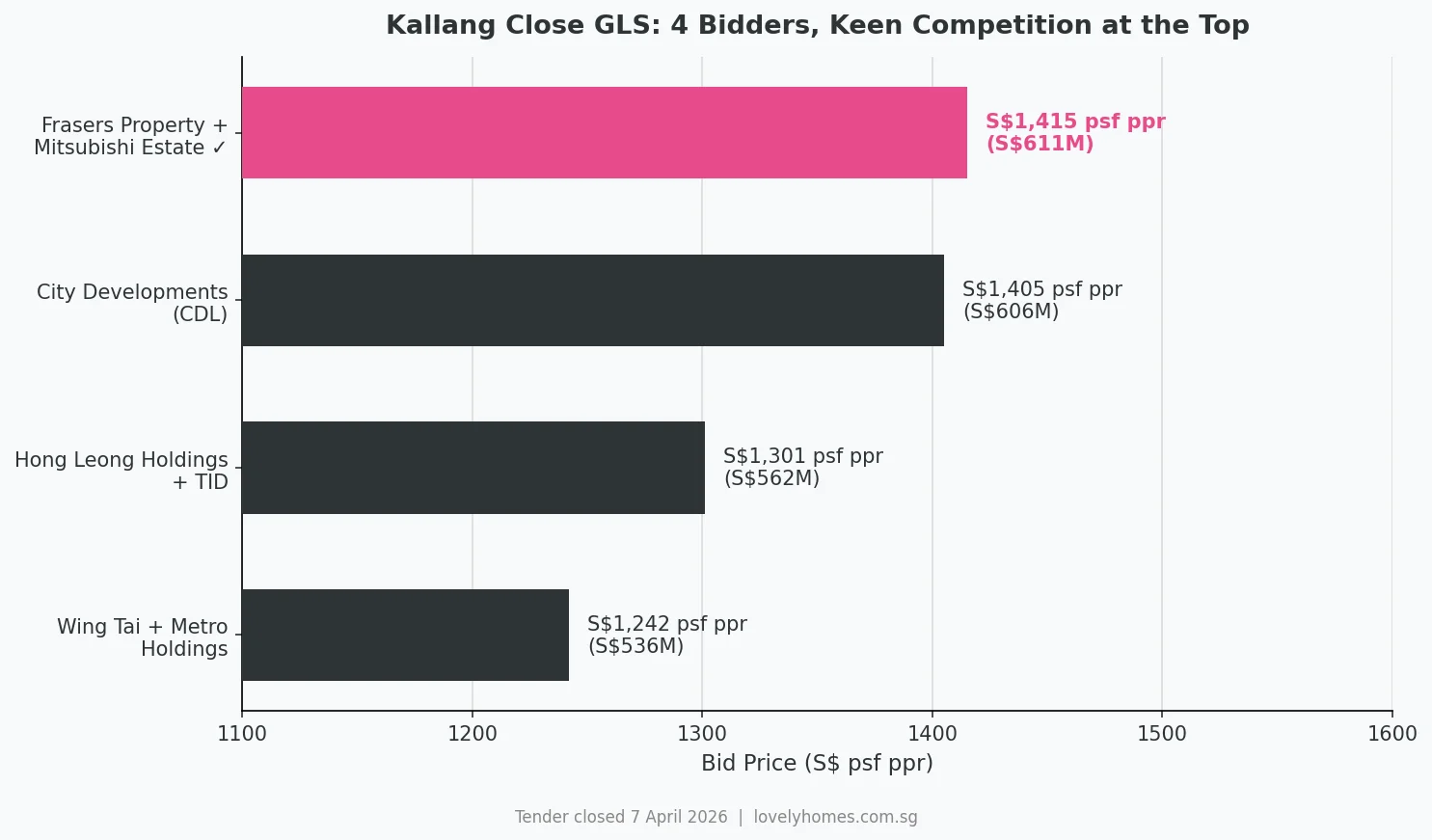

Quick Answer: The GLS tender for Kallang Close closed on 7 April 2026. A joint venture between Frasers Property and Mitsubishi Estate submitted the winning bid of S$610.75 million (S$1,415 psf ppr), the highest psf ppr for a city-fringe residential GLS site in recent years. The site can yield approximately 470 homes and will be the first private residential development in the Kallang Close industrial enclave in 12 years.

Horizontal bar chart comparing the four bids for the Kallang Close GLS site, with Frasers Property and Mitsubishi Estate’s winning bid of S$1,415 psf ppr.

The government land sale (GLS) tender for the Kallang Close residential site closed on 7 April 2026 with four bids — and a result that underscores sustained developer confidence in city-fringe locations, even amid a broader market that posted its lowest transaction volume since Q2 2020.

The winning consortium, a joint venture between Frasers Property Singapore and Mitsubishi Estate, submitted a bid of S$610.75 million (S$1,415 per square foot per plot ratio) — just S$4.35 million, or 0.7%, above second-placed City Developments Ltd. The paper-thin margin between first and second illustrates how keenly both bidders valued the site, and gives a clear signal of where institutional capital believes city-fringe launch prices can go.

Site Factsheet

Detail

Information

Address

Kallang Close, Singapore

District

D08 — Kallang / Whampoa

Site Area

Approximately 11,456 sq m (123,320 sq ft)

Plot Ratio

3.5

Maximum GFA

Approximately 40,107 sq m (431,611 sq ft)

Estimated Units

~470 private residential homes

Tenure

99-year leasehold (from date of award, Apr 2026)

Retail Component

Capped at 115 sq m GFA

Childcare Centre

Minimum 500 sq m GFA (mandatory)

Winning Bid

S$610.75 million (S$1,415 psf ppr)

Joint Venture

Frasers Property Singapore × Mitsubishi Estate

Tender Closed

7 April 2026

The Four Bids: Near-Record Competition

Rank

Bidder

Total Bid

S$ psf ppr

1st (Winner)

Frasers Property + Mitsubishi Estate

S$610.75M

S$1,415

2nd

City Developments Ltd (CDL)

S$606.40M

S$1,405

3rd

Hong Leong Holdings + TID JV

~S$561.5M

S$1,301

4th

Wing Tai Holdings + Metro Holdings

~S$536.4M

S$1,242

The 0.7% gap between the top two bids is one of the narrowest in recent Singapore GLS tender history. CDL — which co-developed Norwood Grand in Woodlands with Frasers Property — was effectively beaten by its own partner on a different site. The spread between first and fourth bidders was 13.9%, indicating that all four consortia saw real value in the Kallang Close waterfront location, but had genuinely different views on achievable launch pricing and margins.

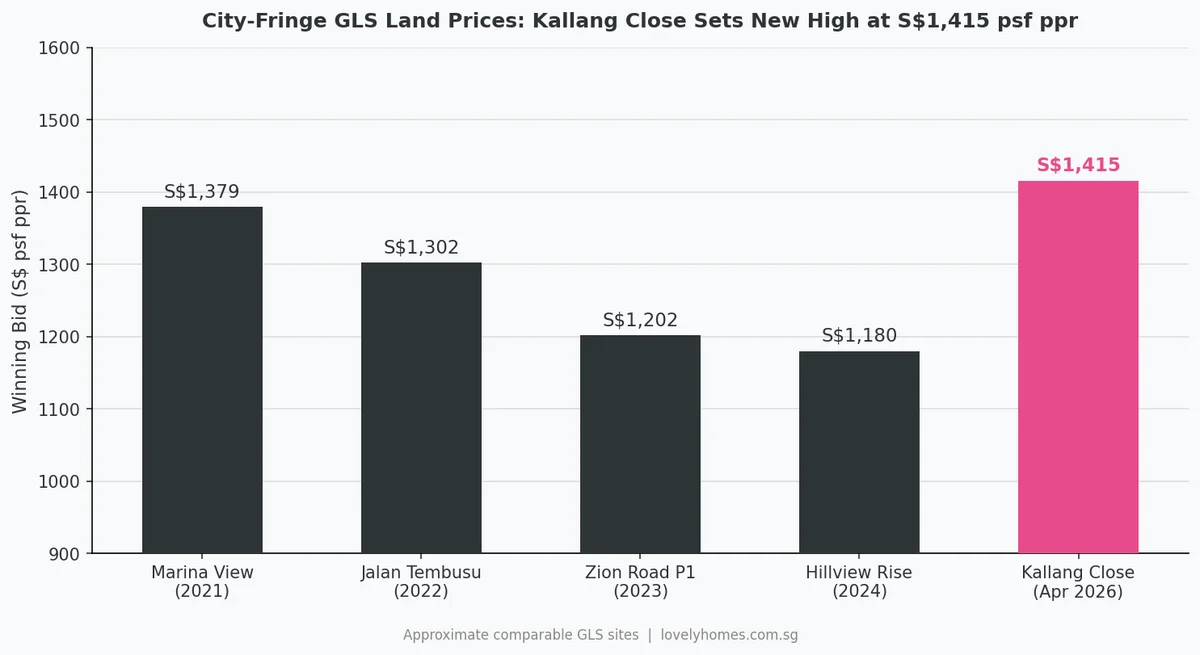

Why Kallang Close Commands a Premium

Bar chart comparing winning GLS bids for comparable city-fringe residential sites from 2021 to April 2026.

The site’s premium psf ppr reflects several structural advantages that are difficult to replicate in the GLS pipeline:

Kallang River waterfront frontage. The site sits adjacent to the Kallang River, and the consortium has committed to delivering a publicly accessible riverfront promenade. Waterfront residential sites are rare in Singapore’s land-scarce market; comparable waterfront addresses — Robertson Quay, Marina Bay, Harbourfront — consistently command significant price premiums.

First private homes in the precinct in 12 years. Kallang Close has been predominantly industrial. The last private residential development in the immediate vicinity launched over a decade ago. Buyers arriving at this project will be entering a precinct undergoing transformation, which historically has been a strong driver of early-adopter price appreciation.

Dual MRT accessibility. Kallang MRT (East-West Line) and Bendemeer MRT (Downtown Line) are both within walking distance, giving future residents cross-island connectivity without transfers.

Proximity to the city and Kallang planning transformation. The Kallang Area Master Plan envisions a sports and lifestyle precinct around the Singapore Sports Hub, Kallang Alive, and the future redevelopment of the National Stadium precinct. The broader area is also benefiting from the Geylang-to-Kallang urban renewal corridor.

Retail and childcare anchors. The mandatory childcare centre (minimum 500 sq m) and capped retail (115 sq m) will add day-to-day amenity value for residents without creating oversupply of commercial space.

What Will Launch Pricing Look Like?

At a land cost of S$1,415 psf ppr, industry analysts have modelled potential launch prices in the S$2,800–3,100 psf range, depending on:

Construction cost trajectory. Building costs in Singapore rose significantly in 2022–2024 and have moderated but remain elevated. A 99-year leasehold development on a 3.5 plot-ratio site with waterfront features and a childcare component will carry above-average construction costs.

Positioning relative to comparable launches. Recent city-fringe new launches — Robertson Opus (D09, ~S$3,150–3,360 psf), UPPERHOUSE (D10, ~S$3,350 psf) — provide a ceiling benchmark. Kallang Close, while waterfront, is in D08 which has historically priced at a modest discount to D09/D10.

Launch timing. The project is unlikely to launch before late 2027 or 2028, given the need for site clearing, design, and construction commencement. The market trajectory over the next 12–18 months will influence the eventual strategy.

A rough breakeven analysis, assuming a 20–22% developer margin over total project cost (land + construction + marketing), suggests a launch price of approximately S$2,900–3,100 psf is required for the project to pencil. Some analysts have modelled upside to S$3,300 psf if the waterfront premium commands a strong early take-up rate.

The Frasers × Mitsubishi Partnership

This is the first JV between Frasers Property Singapore and Mitsubishi Estate, Japan’s largest real estate company by market capitalisation. Frasers Property brings deep Singapore-market execution capability — it has developed One Canberra, Riverfront Residences, and North Park Residences, among others. Mitsubishi Estate brings global real estate expertise and balance sheet scale.

The partnership follows a trend of Japanese developers deepening their Singapore exposure: Sekisui House co-developed THE ORIE in Toa Payoh, MCL Land (a Jardine Matheson subsidiary with deep ties to the Japanese market) developed ELTA in Clementi alongside CSC Land. Japanese investors view Singapore freehold and 99-year leasehold assets as strategic long-term holdings with stable SGD returns.

What This Means for the Broader Market

The Kallang Close result has several read-throughs for Singapore property market observers:

Developer confidence in RCR/city-fringe pricing remains high. Despite Q1 2026 transaction volumes falling 39.7% QoQ, four major consortia competed vigorously for a single site. Developers are bidding for land they believe they can sell at S$2,900+ psf — a vote of confidence in demand fundamentals.

CDL’s near-miss is notable. CDL bid aggressively at S$1,405 psf ppr — its second near-miss in recent GLS tenders. The developer appears determined to rebuild its Singapore residential pipeline following a period of relative inactivity.

The GLS programme is working as a supply valve. The 1H 2026 GLS programme placed 9 sites on the Confirmed List. Kallang Close is the first to be awarded. The forthcoming sites at River Valley Green, Holland Plain, and Peck Hay Road will further test developer appetite in the CCR and RCR.

Waterfront as a permanent premium. Both the Frasers–Mitsubishi bid and CDL’s second-place bid exceeded S$1,400 psf ppr for a site with river frontage. This reinforces that waterfront views in Singapore command a structural premium that survives cooling measures and interest-rate cycles.

Timeline and What to Watch

Date / Period

Milestone

7 April 2026

GLS tender closed; Frasers × Mitsubishi named provisional winner

Q2/Q3 2026

URA formally awards site; conveyance and commencement of site works

Late 2026 – 2027

Architectural design, planning approval, showflat construction

2027 – 2028 (est.)

Showflat preview; public launch (subject to market conditions)

2030 – 2031 (est.)

Expected temporary occupation permit (TOP) based on 99-yr leasehold timeline

Frequently Asked Questions

Who won the Kallang Close GLS tender?

A joint venture between Frasers Property Singapore and Mitsubishi Estate, with a bid of S$610.75 million (S$1,415 psf ppr). The tender closed on 7 April 2026.

How many units will the Kallang Close development have?

Approximately 470 private residential homes, based on the site’s GFA of approximately 431,611 sq ft at a plot ratio of 3.5.

What is the expected launch price for the Kallang Close condo?

Industry analysts estimate a launch price in the range of S$2,900–3,100 psf, reflecting the land cost, construction expenses, waterfront premium, and comparable city-fringe launches. The project is unlikely to launch before late 2027 or 2028.

Is the Kallang Close site freehold or leasehold?

99-year leasehold, from the date of site award in April 2026.

Which MRT stations are near Kallang Close?

Kallang MRT Station (East-West Line) and Bendemeer MRT Station (Downtown Line) are both within walking distance of the Kallang Close site.

Why is this site significant?

It will be the first private residential development in the predominantly industrial Kallang Close precinct in approximately 12 years. The site has Kallang River waterfront frontage and sits within the broader Kallang Area Master Plan transformation zone, including the Kallang Alive sports and leisure precinct.

When will the Kallang Close condo be completed?

Based on typical construction timelines for a 99-year leasehold project of this scale, the estimated target for a Temporary Occupation Permit (TOP) is approximately 2030–2031. The official construction schedule will be confirmed after the site is formally awarded and planning approval obtained.

Interested in the Kallang Close launch? Register for early updates.

This article is for general informational purposes only and does not constitute financial or investment advice. Property prices are projections based on analyst estimates at the time of writing; actual launch prices will depend on market conditions at the time of launch. All figures cited are based on publicly available GLS tender results and URA data as at 20 April 2026. No marketing agency is named in connection with this development.

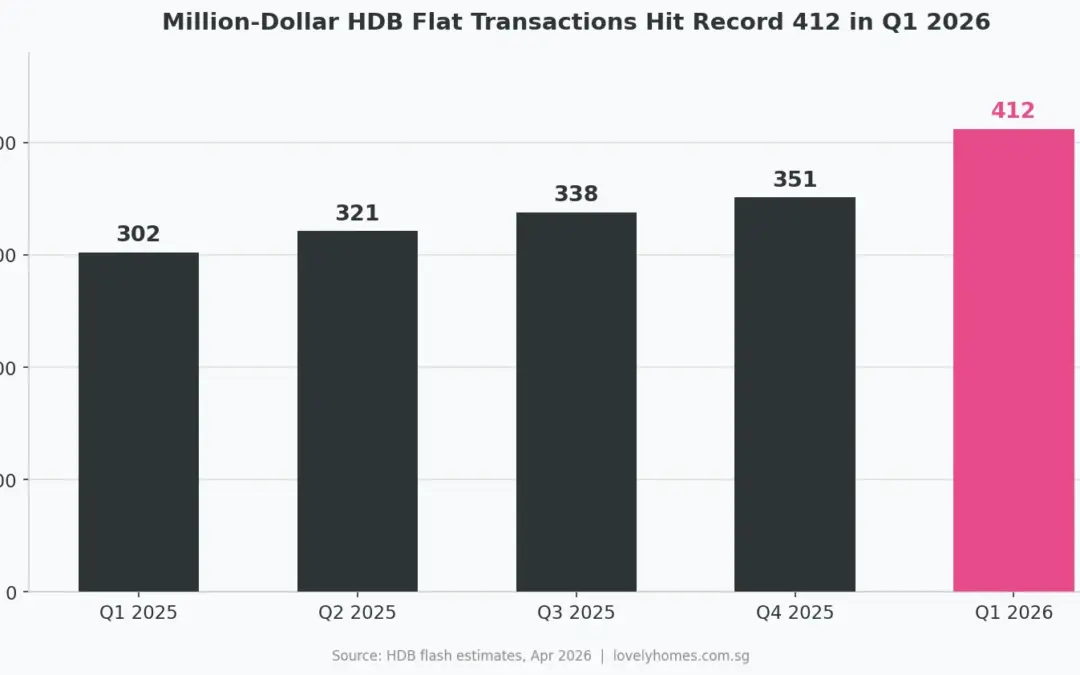

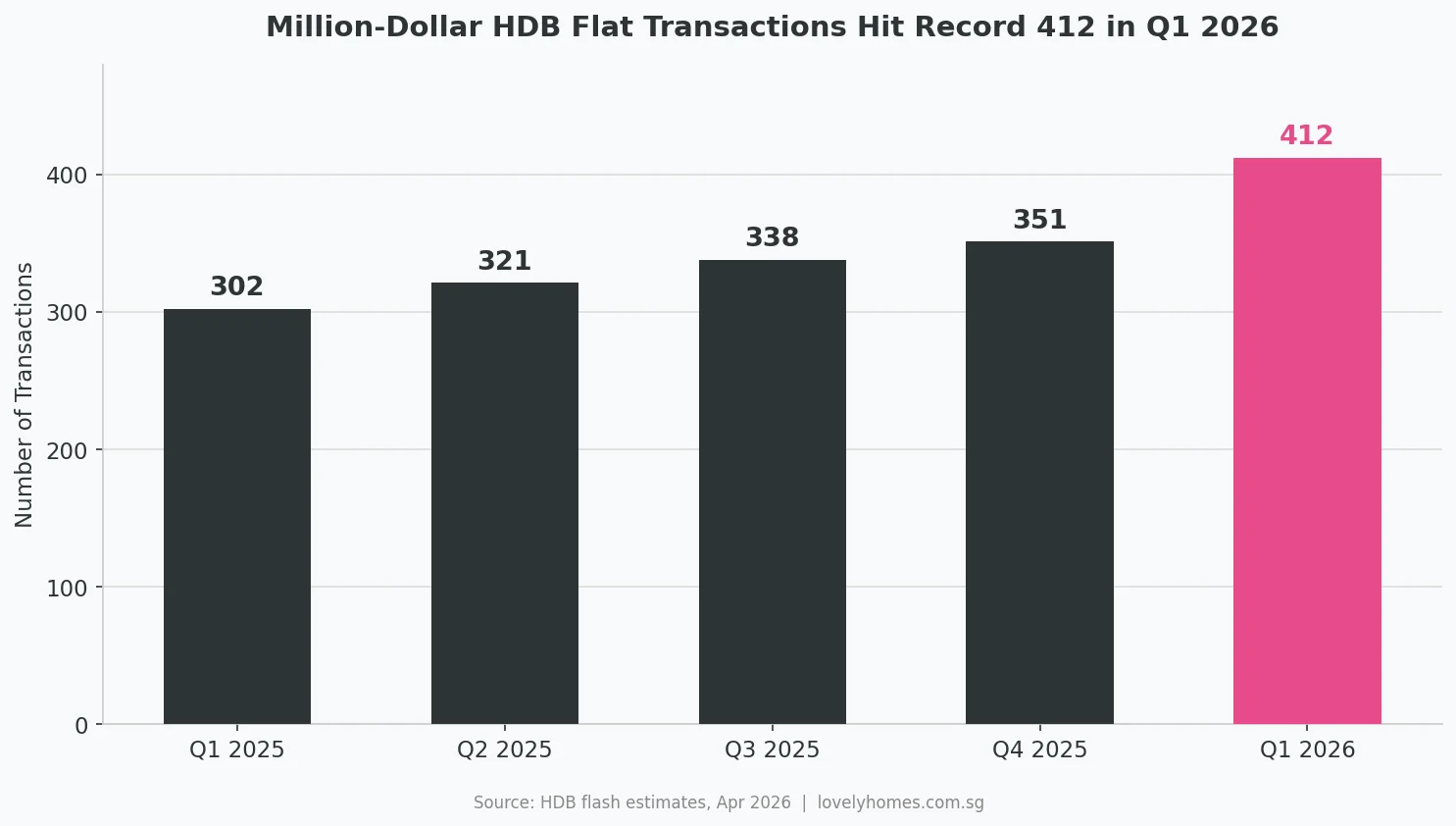

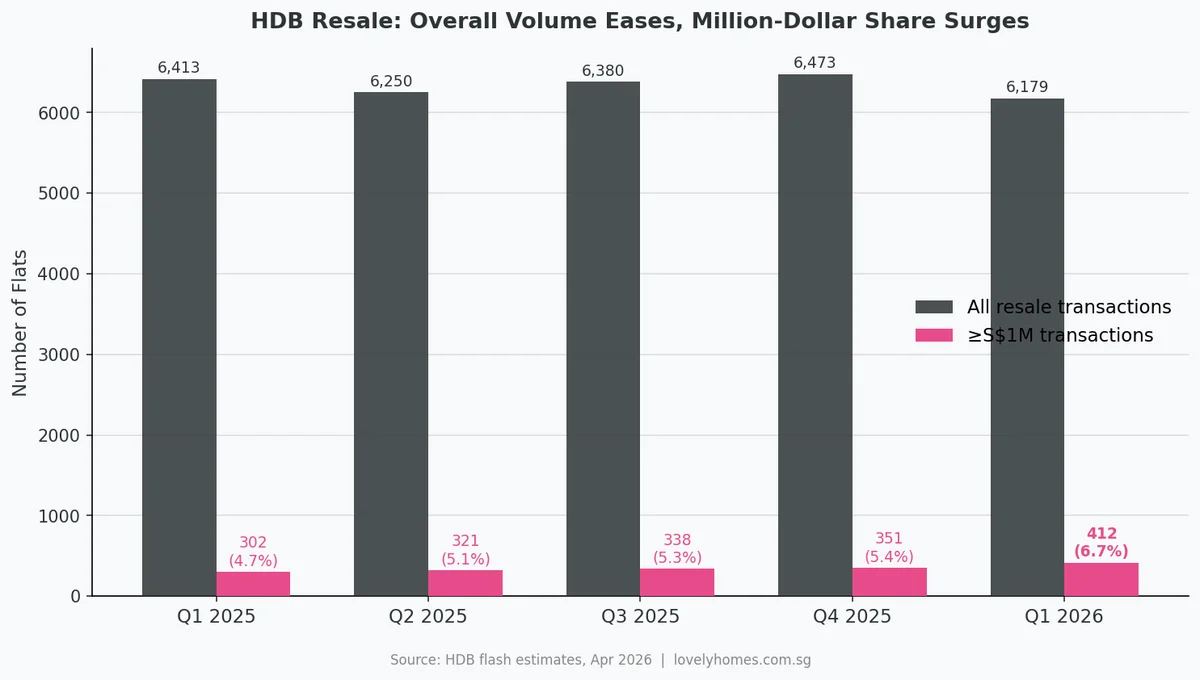

Quick Answer: In Q1 2026, HDB resale prices fell 0.1% — the first quarterly decline in seven years. Yet 412 flats changed hands at S$1 million or more, a new all-time quarterly record. The headline dip and the record premium sales are both real; they just reflect different segments of the same market.

Singapore’s HDB resale market delivered a headline that surprised many commentators on 1 April 2026: the Resale Price Index fell 0.1% quarter-on-quarter — the first decline since Q2 2019. In the same breath, the Housing and Development Board confirmed that 412 flats had sold for S$1 million or above in the same three months, eclipsing the prior record of 351 set in Q4 2025.

The juxtaposition is not a contradiction. It is a portrait of a two-speed resale market: broad price moderation driven by cooling-measure discipline, overlaid by an accelerating premium segment concentrated in a handful of mature estates.

The Numbers at a Glance

Metric

Q1 2026

Q4 2025

Change

HDB Resale Price Index (RPI)

203.4

203.6

−0.1% QoQ

Total resale transactions

6,179

6,473

−4.5% QoQ

Million-dollar transactions

412

351

+17.4% QoQ

Million-dollar share of total

6.7%

5.4%

+1.3 pp

S$1.7M all-time record

Dawson Rd 5-room (Feb 2026)

—

New benchmark

The overall RPI decline is technically modest — 0.1 percentage point — and should be understood in the context of seven consecutive quarters of price growth. Analysts at Knight Frank and JLL have characterised the dip as a “soft landing” rather than a structural correction, pointing to policy-driven affordability guardrails: the Mortgage Servicing Ratio (MSR) cap of 30%, Enhanced CPF Housing Grant (EHG) eligibility reviews, and the 15-month wait-out period for private downgraders.

Why Are Million-Dollar Transactions Still Rising?

Overall resale volume has eased while the share of million-dollar transactions has climbed steadily.

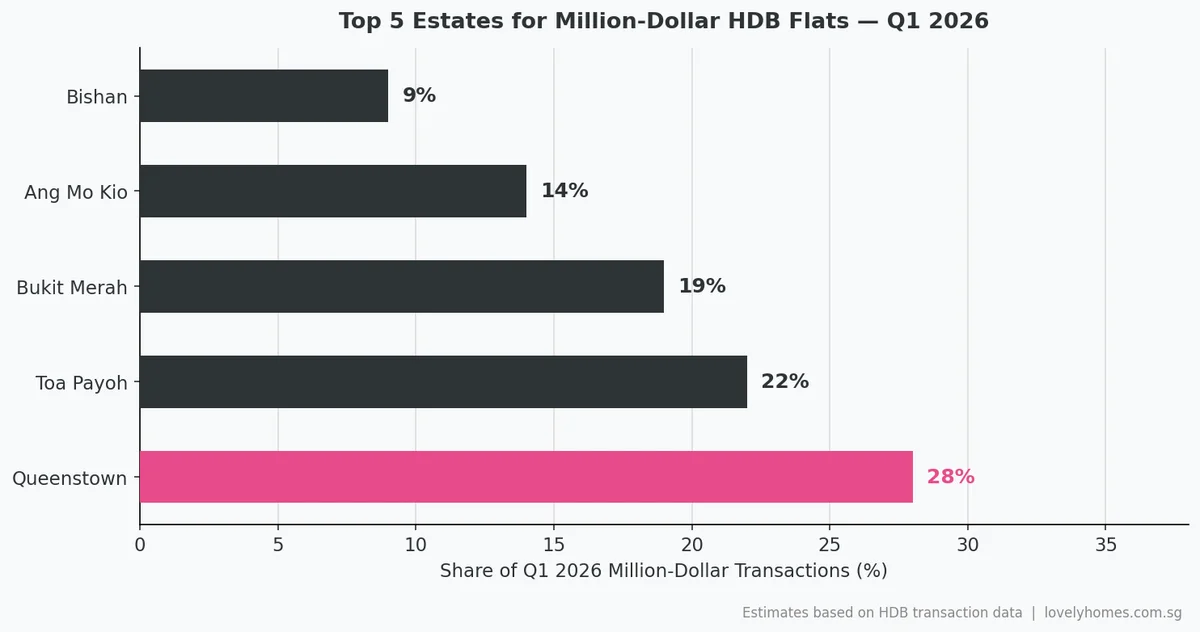

The premium segment operates on different fundamentals. Million-dollar HDB flats are almost entirely concentrated in a narrow band of mature estates — Queenstown, Toa Payoh, Bukit Merah, Ang Mo Kio and Bishan — where flat supply is structurally constrained, location premiums are well-established, and buyer profiles skew towards upgraders and cash-rich upsizers.

Several structural factors underpin the record:

Supply scarcity in mature estates. Large flats (5-room and executive) in central locations such as Queenstown and Toa Payoh are finite. As older owners pass on or move to assisted-living arrangements, each resale becomes a competition between multiple qualified buyers.

Private-market spillover. Buyers priced out of District 9–10 condos at S$2,500–3,500 psf are finding that a large, well-located HDB flat at S$1.0–1.4 million still represents value on a per-square-foot basis (often below S$900 psf).

The Dawson effect. The award-winning SkyParc @ Dawson and the broader Dawson precinct continue to set benchmarks. The S$1.7 million February 2026 transaction for a 5-room flat in Dawson Road is now the all-time national record for any HDB resale flat.

Diminished Alternative Housing Supply (DAHS) effect. New private condo launches fell ~60% QoQ in Q1 2026; with fewer new options, HDB upgraders are staying put or competing harder for premium resale flats.

The S$1.7 Million Record: Unpacking the Dawson Road Transaction

The record-setting flat is a 5-room unit along Dawson Road in Queenstown. At S$1.7 million, it surpasses the previous record of S$1.588 million set in 2023 and represents a premium of roughly 65–70% over the average 5-room flat price island-wide (approximately S$610,000–640,000). The buyer paid predominantly in cash above valuation, reflecting both the location’s scarcity value and the unit’s large floor area (approximately 113 square metres).

Queenstown holds a unique position: it was Singapore’s first public-housing satellite town, developed from the 1950s onwards, and retains some of the densest concentrations of MRT-accessible, well-maintained mature flats in the city. Its proximity to Alexandra, Buona Vista, and the upcoming Greater Southern Waterfront corridor ensures continued demand from professionals and dual-income households.

Top Estates Driving Million-Dollar Transactions

Queenstown, Toa Payoh, and Bukit Merah account for the majority of S$1M+ HDB resale flats in Q1 2026.

The concentration of premium transactions in five mature estates is a structural feature of the market, not a temporary anomaly. About 90% of million-dollar HDB transactions since 2021 have occurred in the core central and near-city estates, according to HDB transaction data. This geographic concentration has two implications:

Policy relevance: The data does not indicate broad HDB price inflation. The 90% of the market transacting below S$1 million is where the cooling measures are working as intended.

Buyer planning: Aspiring premium HDB buyers need to consider that million-dollar transactions in these estates are now the norm rather than the exception. Budget planning, CPF usage limits, and stamp duty calibration (BSD applies to HDB resale transactions too) are essential.

What the HDB Resale Price Dip Actually Means

The 0.1% dip in the RPI is historically significant — it is the first in 28 quarters — but it is marginal in absolute terms. It does not imply that HDB flat prices are about to fall sharply. Key counterpoints:

Volume decline, not distress: The 4.5% QoQ drop in transactions (6,179 vs 6,473) reflects seasonality and reduced new-flat completions, not seller distress or forced selling.

Full Q1 2026 data on 24 April 2026: URA and HDB will release complete Q1 2026 real estate statistics on 24 April 2026. The flash estimate (released 1 April) covers caveats lodged up to 30 March — the final data will capture some additional March transactions.

Policy signals are neutral: MAS and MND have not signalled any relaxation of cooling measures, nor any tightening. The market is operating within the intended guardrails.

June 2026 BTO exercise: HDB’s June 2026 sales exercise will offer approximately 6,900 flats across Ang Mo Kio, Bishan, Bukit Merah, Sembawang and Woodlands. Increased BTO supply provides an alternative for first-timers, which may further moderate resale volumes in the lower price bands.

Practical Implications for HDB Resale Buyers and Sellers

If you are buying a resale flat

The flat price dip provides a marginal negotiating advantage in the broad market, but this advantage does not extend to million-dollar premium flats in mature estates, where demand continues to outstrip supply. Buyers targeting Queenstown, Toa Payoh or Bukit Merah 5-room units should budget above S$1 million and ensure their CPF Ordinary Account balance and cash savings can cover cash-over-valuation (COV), which remains common in these sub-markets.

If you are selling a resale flat

Sellers in non-mature estates may find price expectations need modest recalibration, particularly for 3-room and smaller flats where supply from BTO completions is increasing. Sellers of large flats in prime mature estates remain in a strong position — Q1 2026 data confirms undiminished buyer appetite for well-located units.

If you are a private-property buyer watching the HDB market

The correlation between HDB premium prices and private OCR/RCR condo prices is real but lagged. The current HDB resale dip has not yet translated into private price weakness — private non-landed prices rose 0.4% QoQ in Q1 2026. Monitoring both indices over Q2 2026 will be instructive.

Frequently Asked Questions

How many HDB flats sold for S$1 million or more in Q1 2026?

412 flats, the highest quarterly total on record. This is up 17.4% from the previous quarter’s 351 transactions.

What is the most expensive HDB flat ever sold?

As of Q1 2026, a 5-room flat along Dawson Road in Queenstown that sold for S$1.7 million in February 2026. This surpassed the prior record and set a new national benchmark across all flat types.

Did HDB resale prices fall in Q1 2026?

Yes. The Resale Price Index (RPI) declined 0.1% quarter-on-quarter in Q1 2026, the first quarterly fall since Q2 2019 (seven years). The full Q1 2026 HDB data is scheduled for release by HDB on 24 April 2026.

Why are million-dollar HDB transactions rising even as prices dip?

The overall price dip reflects broad market moderation in non-mature estates and smaller flat types, while the million-dollar segment is driven by structurally scarce supply in mature estates such as Queenstown and Toa Payoh. The two trends coexist because they serve different buyer segments.

Which HDB estates have the most million-dollar transactions?

Queenstown, Toa Payoh, Bukit Merah, Ang Mo Kio, and Bishan account for the vast majority of million-dollar HDB resale transactions. Approximately 90% of all such transactions are in mature, centrally-located estates.

Are HDB cooling measures being relaxed?

No. As of April 2026, there has been no policy signal from MAS, MND or HDB indicating any relaxation of the Mortgage Servicing Ratio (MSR) cap, Additional Buyer’s Stamp Duty (ABSD) rates, or loan-to-value (LTV) limits applicable to HDB resale purchases.

How does the HDB price dip affect private property?

Private non-landed residential prices rose 0.3% QoQ in Q1 2026 despite the HDB dip, representing a divergence between the two markets for the first time since Q2 2019. Analysts regard this as a soft-landing scenario rather than a leading indicator of private price weakness.

Have questions about HDB resale prices or upgrading strategy?

This article is for general informational purposes only and does not constitute financial, legal or property advice. Property prices and market conditions change; readers should conduct their own due diligence or consult a licensed property professional before making any investment decision. All figures cited are based on HDB and URA flash estimates for Q1 2026 released 1 April 2026; full statistics will be published 24 April 2026.

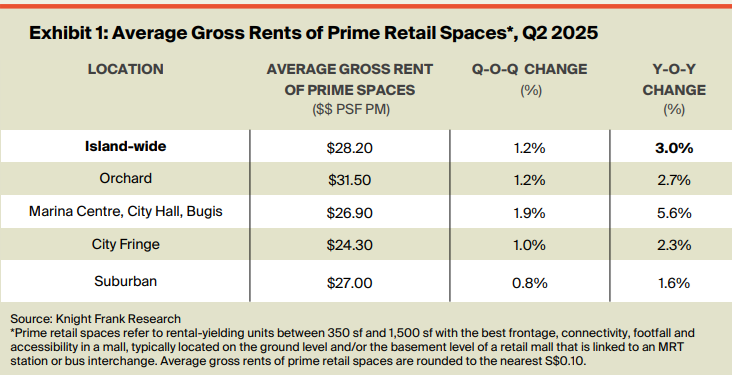

Singapore’s prime retail property sector continues to demonstrate remarkable strength, with average gross rents climbing 3% year-on-year. A new report from real estate consultancy Knight Frank reveals that the market is thriving despite broader economic pressures. The “Singapore Retail Market Update – Q2 2025” shows a consistent upward trend, giving investors and landlords reason for optimism.

According to the research, the average gross rent for prime retail spaces across the island now stands at S$28.20 per square foot per month. This figure also represents a healthy 1.2% increase compared to the previous quarter. For clarity, the report defines these prime units as spaces between 350 and 1,500 square feet that boast the best frontage, connectivity, and footfall within a mall. Typically, these are located on the ground or basement levels with direct links to MRT stations or bus interchanges, ensuring maximum consumer traffic. This sustained growth underscores the enduring appeal of premium physical retail locations.

City Centre Hotspots Lead the Charge in Rental Growth

While the island-wide average shows solid growth, a detailed look reveals that specific central locations are significantly outperforming the rest of the market. The area encompassing Marina Centre, City Hall, and Bugis reported the most substantial increase. Rents in this popular precinct surged by an impressive 5.6% since the same time last year, jumping 1.9% in the last quarter alone. The average gross rent here has now reached S$26.90 per square foot per month. This highlights strong demand for centrally located malls with a vibrant mix of office crowds, tourists, and local shoppers.

In contrast, suburban malls saw the most modest annual rental increase at just 0.8%, although their average rent remains competitive at S$27 per square foot.

Unsurprisingly, the Orchard Road area continues to command the highest rents in the nation.Prime spaces along the iconic shopping belt fetch an average of S$31.50 per square foot per month, cementing its status as Singapore’s premier retail destination. This data provides clear insights for investors looking to target areas with the highest growth potential and rental yields.

A Look Ahead: Can a Supply Boom Stabilise Rising Rents?

The steady increase in gross rent, however, presents a significant challenge for tenants. Retail businesses, particularly in the food and beverage (F&B) sector, are already grappling with high operating expenses. The Knight Frank report notes that operating expenditures for F&B businesses have reached a record high of S$12.3 billion, and rising rents could further erode their margins. The resilience of these businesses will be a key factor to watch in the coming months. This dynamic underscores the delicate balance between landlord profitability and tenant sustainability.

Fortunately, a silver lining appears on the horizon. The report projects that rental prices are likely to stabilize and potentially even decrease in the medium term. Between 2025 and 2029, a substantial 4.3 million square feet of new gross retail floor area is scheduled to enter the market. This significant increase in supply is expected to ease the upward pressure on rents, helping to normalize lease values and provide tenants with more options. For investors and developers, this signals a more competitive landscape ahead, while for businesses, it may offer much-needed relief. Despite the rise of e-commerce, this report reaffirms that physical retail remains a powerful force, contributing to over 85% of all retail sales in Singapore.

The Singapore government has announced its slate for the second half of 2025 under the closely watched Singapore GLS programme. This latest release makes eleven new sites available for private residential development. Moreover, this strategic move is pivotal in shaping the nation’s property landscape. It aims to ensure a stable and sustainable supply of private housing. Specifically, ten of these plots are on the confirmed list, signalling a definite sale within the period. In addition, a site in the Central Business District (CBD) for serviced apartments is on the reserve list. This means it can be triggered for sale based on developer demand. This curated list arrives amid cautious market sentiment, balancing new housing needs with economic uncertainties.

Consequently, market analysts are forecasting strong, and even fierce, competition. This is particularly true for prized sites in the Newton and Tanjong Rhu planning areas. Remarkably, these areas have not seen new state land offered for sale in nearly three decades. This long hiatus, therefore, makes them exceptionally rare opportunities for developers. They can establish a flagship presence in established, high-value residential enclaves.

Highly Anticipated Prime Locations: A Closer Look

The Newton site, a 0.59-hectare plot on Bukit Timah Road, is widely seen as the crown jewel. Slated for an August launch, it is poised to attract top-tier developers. The plot can be developed into approximately 340 exclusive homes. Furthermore, its history is notable; the land was previously used for transitional offices. The plot’s allure is now magnified by its prime location and excellent connectivity. For instance, it is near the Newton MRT interchange and the Orchard Road shopping belt. As a result, experts predict it will be highly sought after, potentially setting new price benchmarks.

Similarly, the Tanjong Rhu site is generating significant industry buzz. This substantial plot can accommodate around 525 residential units and is scheduled for a November tender. As the first GLS site in this waterfront precinct since 1997, it presents a unique chance. Developers can cater to the sustained upgrader demand for city-fringe living. The location’s appeal is also enhanced by its proximity to the Singapore Swimming Club. It is also near the future Katong Park MRT station, promising excellent connectivity.

Other Key Sites on the Confirmed List

In addition, developers can bid on a Dunearn Road site in the new Turf City housing estate. This 1.91-hectare plot will support 335 private homes and retail space. Its location near Sixth Avenue MRT and popular schools should ensure robust interest when it launches in December.

Furthermore, a large 1.35-hectare site along Dover Road is set to launch in November. It is expected to yield 625 units, making it the largest project on this list. Located near Singapore’s One-North R&D hub, this development provides much-needed housing. It brings residents closer to key employment centres for the area’s 50,000-strong workforce.

Meanwhile, a Bedok Rise plot for 380 units will likely see intense competition in September. This is a direct result of the limited supply of new homes in this mature estate. It also represents the last major development parcel near the Tanah Merah MRT interchange.

Increased Supply to Meet Strong EC Demand

In a clear response to robust demand, the government has included two executive condominium (EC) sites. The first, in Woodlands Drive 17, can be developed into 560 units. Consequently, a second site in Miltonia Close will yield around 430 EC units. This injection of supply brings the total of new EC units to its highest level since 2014. Therefore, experts believe increasing EC supply is crucial for providing more housing choices. It also helps mitigate the “fear of missing out” effect that can drive prices higher.

Reserve List and Overall Market Caution

Beyond the confirmed plots, a Cross Street site is available on the reserve list. It can yield 305 long-stay serviced apartments, which may appeal to certain investors. However, analysts remain uncertain if it will be triggered soon. This is because the asset class is a relatively untested concept in the Singapore market.

Overall, the government’s decision to place more supply on the reserve list reflects a measured approach. It acknowledges the recent slowdown in home sales and a cautious developer outlook. This caution stems from rising costs and an uncertain macroeconomic climate.

Singapore’s vibrant retail landscape is currently navigating a period of significant adjustment as vacancy rates show a noticeable increase. Recent government data highlights that the islandwide retail vacancy rate climbed to 6.8 per cent in the first quarter of 2025. This figure represents a clear uptick from the 6.2 per cent recorded in the previous quarter. This consequently signals a shift in market dynamics. This trend is primarily driven by a slowdown in the net take-up of spaces. This has been compounded by the introduction of a fresh supply into the market. Therefore, both landlords and tenants must understand the underlying causes and future outlook to make informed decisions.

The Driving Forces Behind Rising Vacancies and Tenant Exits

Several converging factors are contributing to the challenging environment that is prompting more retailers to reconsider their physical footprint. Firstly, a prolonged slowdown across the retail and dining sectors has put sustained pressure on businesses. This economic reality is exacerbated by relentless cost pressures, including a persistent labour crunch, which retailers are struggling to absorb. Consequently, their inability to fully pass on these rising costs to consumers is resulting in painfully squeezed profit margins.

Furthermore, consumer behaviour has shifted, with shoppers becoming more cautious and cutting back on discretionary spending. This is evidenced by a drop in retail sales during February and March 2025, following a promising start to the year. In addition, the marketplace has become fiercely competitive, particularly within the Food and Beverage (F&B) sector. Some industry reports suggest the F&B scene is at risk of oversupply, leading to a cycle of rapid expansion followed by equally swift closures, which ultimately results in wasted capital and resources.

The Retail Tenant’s Dilemma: High Rents and Lease Negotiations

Unsustainable rental rates remain a critical pain point for many businesses, affecting even those in traditionally high-traffic locations. Tenants in less populated areas or developments with low footfall are understandably the most pronounced casualties of this pressure. As a result, many tenants are actively seeking to pre-terminate their leases, a clear indicator of market distress. This option, however, comes with stringent conditions that require careful consideration before any action is taken.

Typically, early lease termination requires at least six months’ notice or a significant payment equivalent to six months’ gross rent. Landlords also often require additional compensation equal to the security deposit, making it a costly exit strategy for struggling businesses. For tenants whose lease contracts do not permit early termination, the focus shifts towards negotiation. These discussions may involve requesting a rent reduction, proposing a restructured payment plan, or finding a suitable replacement tenant. These alternatives require the landlord’s explicit approval.

A Tale of Two Markets: Prime Resilience Amidst General Weakness

Despite the overall increase in vacancy, the market is not uniform, revealing a fascinating and complex picture. In the first quarter, net demand for retail spaces was a negative 129,000 square feet, starkly reversing five consecutive quarters of positive take-up. Simultaneously, about 323,000 square feet of new retail space came on stream, which new entrants absorbed, preventing an even sharper spike in vacancy.

However, a key paradox has emerged where average rents have largely held steady, particularly in prime locations. Rents in the coveted Orchard Road and suburban areas remained flat at S$23.20 per square foot (psf) and S$14.70 psf, respectively. Malls in prime districts continue to demonstrate remarkable resilience, supported by a limited supply of available space. This scarcity empowers landlords to negotiate higher rents and maintain healthy momentum for lease renewals, especially with enduring luxury retailers.

A crucial metric for understanding this resilience is the occupancy cost, which measures rent as a proportion of tenant sales. For major mall operators like CapitaLand and Frasers, occupancy costs remained sustainable below 20 per cent in 2024. This suggests that for well-positioned tenants, revenues are still growing at a pace that justifies the rental costs, showcasing a clear divergence between prime and secondary retail spaces.

Future Retail Outlook: Short-Term Stability Before a Supply Wave

Looking ahead, the market is expected to experience increased tenant churn throughout the remainder of the year. Underperforming retailers may choose to exit early or simply not renew their leases upon expiration. While new store openings have historically outpaced closures, there is a growing expectation that this trend could soon reverse. This follows a challenging 2024 where store closures hit a 19-year high, indicating deep-seated structural shifts.

In the short term, rental rates and occupancy levels are likely to remain supported over the next two years. This stability is largely due to a relatively limited pipeline of new retail supply, with under 400,000 square feet of net lettable area expected annually. However, a significant wave of new supply is looming on the horizon from 2028 onwards. This future influx, led by major developments like the Marina Bay Sands expansion, will introduce over 1.2 million square feet of space, potentially reshaping the competitive landscape once more.

For now, industry experts anticipate that Orchard Road rents will likely perform at the upper end of the forecasted 1 to 2 per cent growth range for this year. Conversely, suburban rents are expected to track the lower end of that projection, reflecting the ongoing bifurcation of the market.