HDB Resale Levy Singapore 2026 — who pays, when, and how to plan around it.

Quick answer — the resale levy in 30 seconds

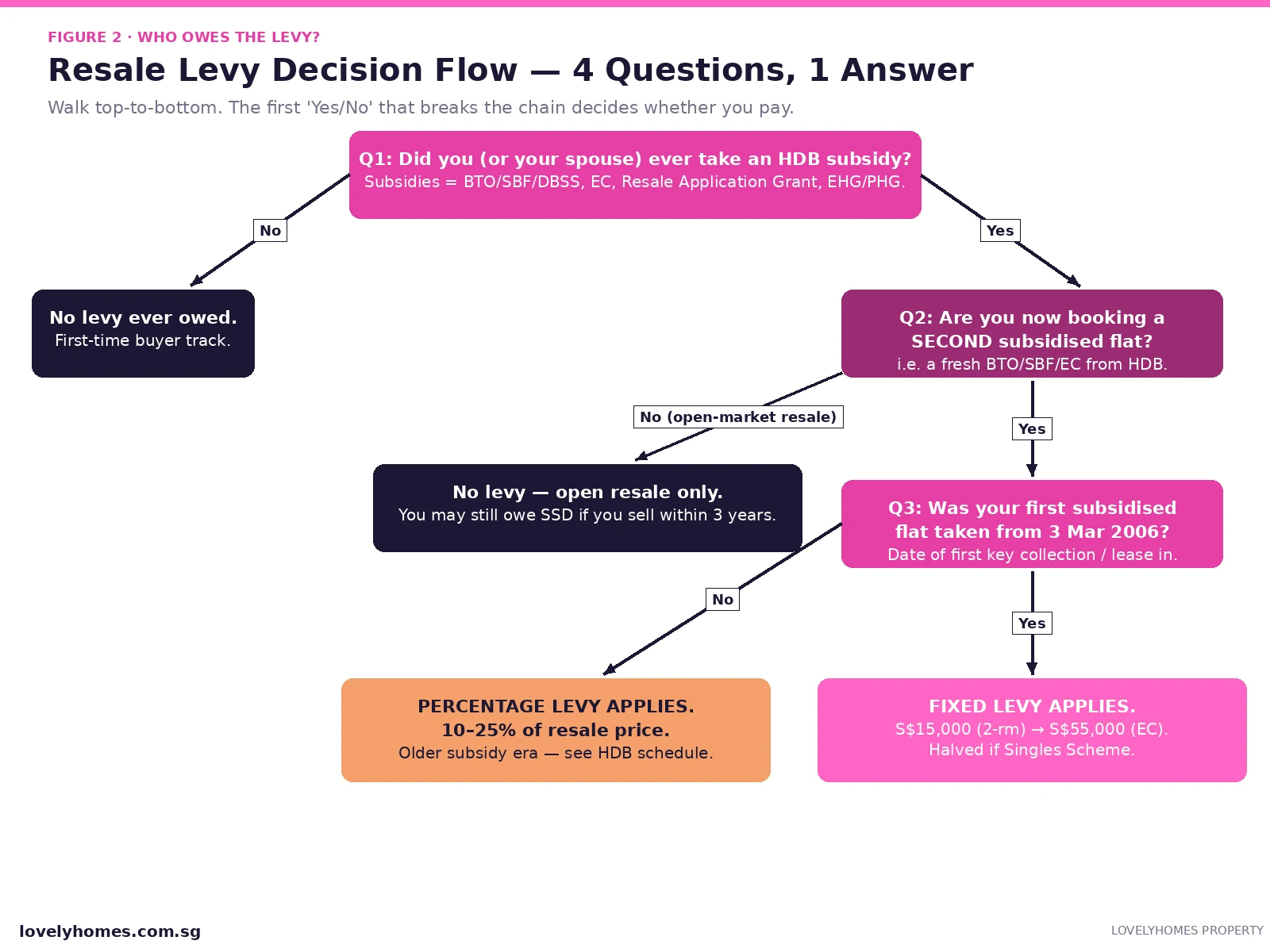

The HDB resale levy is a one-off charge on second-timer households who take a second housing subsidy from HDB (BTO, Sale of Balance Flats, or a new Executive Condominium).

It does not apply if you sell your subsidised flat and buy on the open resale market without claiming any fresh HDB grant.

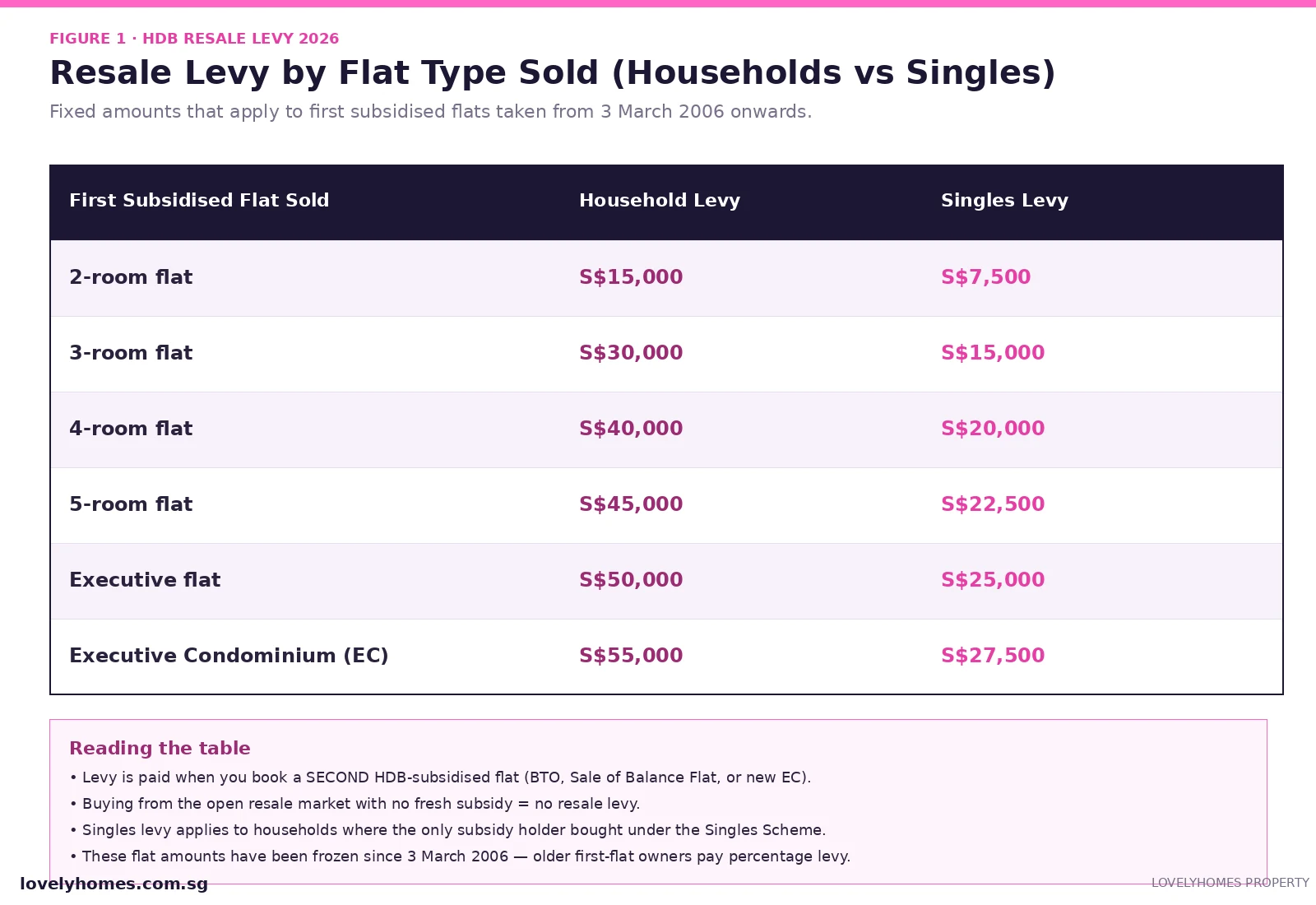

For first subsidised flats taken from 3 March 2006, the levy is a fixed amount — S$15,000 for a 2-room sold up to S$55,000 for an EC.

Households who got their first subsidy before 3 March 2006 pay a percentage levy of 10–25% of the resale price instead.

Singles Scheme buyers pay half the household amount.

The levy is paid in cash (or net cash proceeds from selling the first flat) — CPF cannot be used.

Payment is collected at the point of booking the second subsidised flat, before key collection.

Buying on the open market means no levy, but you still face BSD, ABSD (where applicable) and SSD if you sell within three years.

What is the HDB resale levy?

The resale levy is a charge that the Housing & Development Board (HDB) imposes on a household which has already enjoyed a housing subsidy and now wants a second bite at one. The Government’s logic is straightforward: public housing subsidies are taxpayer-funded, and a household should not collect them twice without contributing back. Selling the first subsidised flat is fine; what triggers the levy is the act of booking another subsidised flat — a fresh BTO, a Sale of Balance Flat, an open booking unit, or a brand-new Executive Condominium directly from the developer.

Crucially, the levy is administered by HDB, not IRAS. It is separate from Buyer’s Stamp Duty, ABSD, and Seller’s Stamp Duty. You can owe stamp duties and a resale levy in different scenarios, and they are calculated, paid, and tracked independently.

Figure 1 · Fixed-dollar resale levy amounts in force since 3 March 2006. Source: HDB.

Who actually pays the levy?

The resale levy travels with the household, not the property. If at any point in your housing history you (or your spouse, or your essential occupier) have already enjoyed an HDB subsidy, you are a second-timer in HDB’s eyes the next time you approach them for a fresh subsidy. The subsidies that count include:

A new flat purchased directly from HDB (BTO, Sale of Balance Flats, Re-Offer of Balance Flats, open-booking flats).

A Design, Build and Sell Scheme (DBSS) flat bought from a private developer.

A resale flat bought with one of the older Resale Application Grants — CPF Housing Grant for Family, Singles Grant, or Half-Housing Grant — taken before changes to the levy rules.

HUDC flats and SERS replacement flats taken under HDB schemes count similarly.

If your only subsidy was the Enhanced CPF Housing Grant (EHG) or the Family Grant on a resale flat purchased after 3 March 2006, you are not automatically deemed a levy-paying second-timer for the purpose of a future resale flat purchase — but you do pay the levy if you next buy a new flat or new EC.

How the levy is calculated

Two regimes apply, and the dividing line is the date of your first subsidised flat’s key collection (or in the case of an EC, the date you signed the Sale & Purchase Agreement).

Fixed-dollar levy (first flat from 3 March 2006)

This is the regime almost every modern buyer falls under. The amount is locked to the type of flat you sold:

First subsidised flat sold

Household levy

Singles Scheme levy

2-room flat

S$15,000

S$7,500

3-room flat

S$30,000

S$15,000

4-room flat

S$40,000

S$20,000

5-room flat

S$45,000

S$22,500

Executive flat / HUDC

S$50,000

S$25,000

Executive Condominium

S$55,000

S$27,500

The fixed amount does not move with property prices, which is good news for households whose first flat appreciated heavily in resale. A 4-room sold today for S$700,000 still owes only S$40,000 in levy — about 5.7% of the resale price.

Percentage levy (first flat before 3 March 2006)

Older second-timers face the legacy regime. Levy is set as a percentage of the higher of the resale price or 90% of the market valuation:

First subsidised flat sold

Household levy %

Singles Scheme levy %

2-room flat

10%

5%

3-room flat

20%

10%

4-room flat

22.5%

11.25%

5-room flat

25%

12.5%

Executive flat / HUDC

25%

12.5%

For a household that sold a 4-room legacy flat for S$650,000, the percentage levy lands at S$146,250 — markedly higher than the modern fixed levy. This is one reason long-time HDB owners often choose to remain in the resale market rather than ballot for a fresh BTO.

When and how the levy is paid

HDB collects the resale levy at the point of booking the second subsidised flat. In practice this means:

You sell your first subsidised flat. CPF is refunded with accrued interest; the cash balance is yours.

You ballot for, queue, and book a second BTO/SBF/SBF or sign for an EC.

HDB issues a payment notice for the levy, payable in cash only. CPF cannot be used.

Levy is paid before signing the lease agreement / S&P. Failure to pay forfeits the booking.

If the second flat is booked before the first has been sold, HDB defers the levy to the resale completion date and may require an undertaking. Some buyers structure it this way to avoid being homeless between sale and BTO completion, especially in long-build projects.

Figure 2 · Walk the four questions in order — the first answer that breaks the chain decides your outcome.

Who is exempt or partially relieved?

HDB allows a small set of waivers and concessions, and these matter most for older households and downgraders:

Buying a 2-room Flexi flat on a short lease (45 years or less) at age 55 and above. The resale levy is waived in full to encourage right-sizing.

Buying a Studio Apartment / Community Care Apartment. No resale levy applies (these are senior-targeted typologies).

Divorce settlements where one party retains the existing flat. No levy event; only one of the parties may face a levy if they later buy a fresh subsidised flat.

Sub-letting income or rental of bedrooms does not trigger the levy. The levy only fires when the subsidised flat is sold and a new subsidised flat is booked.

Open-market resale purchases without grants are not levy events. You can move from a 4-room HDB to another resale 5-room without grant, and no levy is triggered.

Resale levy vs CPF refund vs stamp duty — separating the bills

It is easy to confuse three different cash flows that all hit a second-timer household at roughly the same time. They are independent and add up:

What you pay

Who collects

Triggers

Source of funds

Resale levy

HDB

Booking second subsidised flat

Cash only

CPF accrued interest

CPF Board (refund into your OA)

Sale of any flat

Auto-deducted from sale proceeds

Buyer’s Stamp Duty

IRAS

Any property purchase

Cash + CPF allowed

Additional Buyer’s Stamp Duty

IRAS

Second / third / foreign buyer purchase

Cash + CPF allowed

Seller’s Stamp Duty

IRAS

Sale within 3-year holding period

From sale proceeds

The CPF accrued interest is not a fee — it is your own money being returned to your OA — but it shrinks the cash you can deploy on the next purchase. Plan around it the same way you plan around the resale levy.

Worked example — same family, two paths

Take a Singapore Citizen couple, married 12 years, who bought a 4-room BTO in Punggol for S$320,000 in 2014 with a Family Grant. In 2026 they have hit the 5-year MOP, the flat is valued at S$680,000, and they are deciding whether to upgrade through a fresh BTO or to buy a private resale condo.

Figure 3 · Whichever way they go, the resale levy is small relative to private stamp duty.

Path A — buying a 5-room BTO — costs S$40,000 in levy plus the new flat price of S$580,000. Path B — buying an S$1.4M open-market resale condo — skips the levy entirely but adds S$45,400 in BSD and S$280,000 in ABSD at the 20% citizen-second-property rate, totalling S$325,400 in stamp duty. The headline conclusion: the resale levy is real money, but it is dwarfed by ABSD whenever the alternative is a private-market upgrade. Couples often see this comparison only after they put pen to paper, which is why it pays to model both routes early.

Why the levy exists at all

Singapore’s housing model rests on two policy pillars: keeping public housing affordable to first-timers, and rationing taxpayer subsidies. Without a levy, a household could ride the BTO market repeatedly — cashing in on resale price growth at each cycle and stepping up to bigger flats with full subsidies each time. The levy is the friction that makes a second BTO a deliberate choice rather than a default. It also keeps queues for new BTOs balanced — first-timers always get priority, but second-timers compete for the remaining quota and pay the levy if they win one.

Compared with peer markets, the Singapore approach is unusual. Hong Kong’s Home Ownership Scheme uses a price clawback rather than a flat levy. Australia’s First Home Owner Grant has no second-time levy because grants there are smaller and time-limited. The Singaporean fixed-dollar approach is a useful piece of housing-policy plumbing that most buyers only encounter once.

What this means for you

If you are a current HDB owner thinking about your next move, the levy reshapes the decision in three concrete ways. First, it makes the open resale route surprisingly competitive — for many flat types the levy is comparable to the lawyer-and-valuer fees on a private resale and is comfortably under the BSD on a S$1.5M condo. Second, because the levy is fixed, smaller flat owners (2-room, 3-room) face a friendlier upgrade path than larger flat owners; the household that sold a 5-room or EC pays the most. Third, the levy is cash-only — that imposes a real liquidity hit at exactly the moment you are also funding the down-payment, legal fees, and renovation on the next home.

A common mistake is to treat the levy as one of many transaction costs and bake it into the budget late. Run the numbers up front, ideally on the same spreadsheet you use for down payment and LTV planning. If you are upgrading to a private property, the right comparison is the levy versus the ABSD and BSD on the alternative — almost always a smaller bill, in absolute terms, than the stamp duties on a S$1.5M+ condo.

What might come next

The fixed-dollar regime has been frozen since March 2006. Construction costs and median flat prices have roughly tripled since then, which has progressively eroded the real value of the levy. There has been periodic public commentary that the Government may reconsider the schedule — either by indexing it to a property price benchmark or by raising the EC and 5-room amounts. In the same vein, the percentage-based legacy regime continues to age out as pre-2006 first-flat owners exit the market.

Two policy directions are plausible from here. One is a recalibration that pushes the larger-flat levies upward to keep relative ratios stable as flat prices move. The other is a structural rethink that ties the levy to the resale price like the legacy regime, but capped to avoid punishing strong resale gains. Either direction would arrive with notice and a generous grace period for booked transactions; speculation is not a reason to rush a BTO ballot. The forward-looking view here is that some upward adjustment is likely over the next several years, but transparency and lead time are part of HDB’s playbook.

Frequently asked questions

Does the resale levy apply if I sell my HDB and buy a private condo?

No. The levy only triggers when you book another subsidised flat from HDB (BTO, SBF, fresh EC). Buying a private resale condo or a new condo from a developer does not engage the levy at all — although you will face full BSD plus ABSD where applicable.

Does the resale levy apply when I buy a resale flat with a CPF grant?

For first subsidised flats taken from 3 March 2006 onwards, second-timer households who buy a resale flat with grants are subject to a smaller adjustment rather than a full resale levy. Historically (pre-March 2006) a percentage levy did apply. Always check HDB’s resale flat eligibility letter for your specific case before you make an offer.

Can I pay the resale levy from my CPF Ordinary Account?

No. The levy is payable in cash. The cash you have on hand from the sale of your first flat — after CPF is refunded with accrued interest — is the typical source of funds. Some households top up with a small bridging loan to cover the gap between flat sale completion and second-flat booking.

What if my spouse and I both owned subsidised flats before marriage?

HDB looks at the household, not the individual. If either of you previously took an HDB subsidy, the next subsidised flat the new household books is treated as a second purchase. Only one resale levy is owed per household per flat sold.

Will the levy be waived if I am buying a smaller flat to right-size?

Only in tightly defined cases — chiefly the 2-room Flexi short-lease flat at 55+, and Studio Apartment / Community Care Apartment purchases. Right-sizing into a longer-lease 2-room or 3-room generally still triggers the levy if it is a fresh subsidised flat.

Does the resale levy apply to Executive Condominium buyers?

Yes — and it is the largest category, S$55,000 for households who previously sold an EC. Crucially, the levy fires on the first hand EC purchase only. After the EC’s 5-year MOP and 10-year privatisation, subsequent buyers are private-market buyers and never face the levy.

If I divorce and one of us keeps the flat, does the other party still owe the levy?

The party who retains the flat keeps the subsidy attribution; if they later remarry and book another subsidised flat, the levy applies. The other party’s eligibility is reviewed against their new household status — the levy is only assessed at the point of booking a fresh subsidised purchase.

Disclaimer: This article summarises the resale levy regime as administered by the Housing & Development Board (HDB) of Singapore. Levy amounts, eligibility rules and waivers may be updated by HDB from time to time. Always verify the current schedule against the HDB resale levy page on hdb.gov.sg, your eligibility letter, and where relevant the Inland Revenue Authority of Singapore (IRAS), the Central Provident Fund (CPF) Board, the Monetary Authority of Singapore (MAS), and SingStat for housing market data. This article does not constitute legal, financial or tax advice — speak to a licensed conveyancing lawyer, a HDB-listed mortgage advisor, or a registered financial adviser before transacting.

Seller’s Stamp Duty (SSD) of 12%, 8%, or 4% applies if you sell within 3 years of purchase (private residential properties)

Agent commission is typically 1–2% of sale price — negotiable; CEA-registered agents only

CPF funds used must be refunded to CPF OA with Accrued Interest (compounded at 2.5% p.a.) upon sale

The sale process from OTP to legal completion typically takes 10–12 weeks for private property; 8–12 weeks for HDB

Outstanding mortgage must be discharged from sale proceeds; early repayment penalty may apply (lock-in period)

No Capital Gains Tax in Singapore — profits from property sales are generally not taxed unless you are classified as a property trader by IRAS

Decoupling a property before sale may reduce ABSD on a subsequent purchase but requires careful legal structuring to avoid Section 33A anti-avoidance provisions

Selling Property in Singapore — Overview

Singapore’s property market has no Capital Gains Tax — meaning that profits from the sale of residential property are generally not subject to income tax, provided IRAS does not classify you as conducting a property trading business. However, selling a property in Singapore does involve a web of stamp duties, CPF refund obligations, agent fees, legal costs, and outstanding loan discharges. Understanding these costs upfront prevents unpleasant surprises at the point of sale.

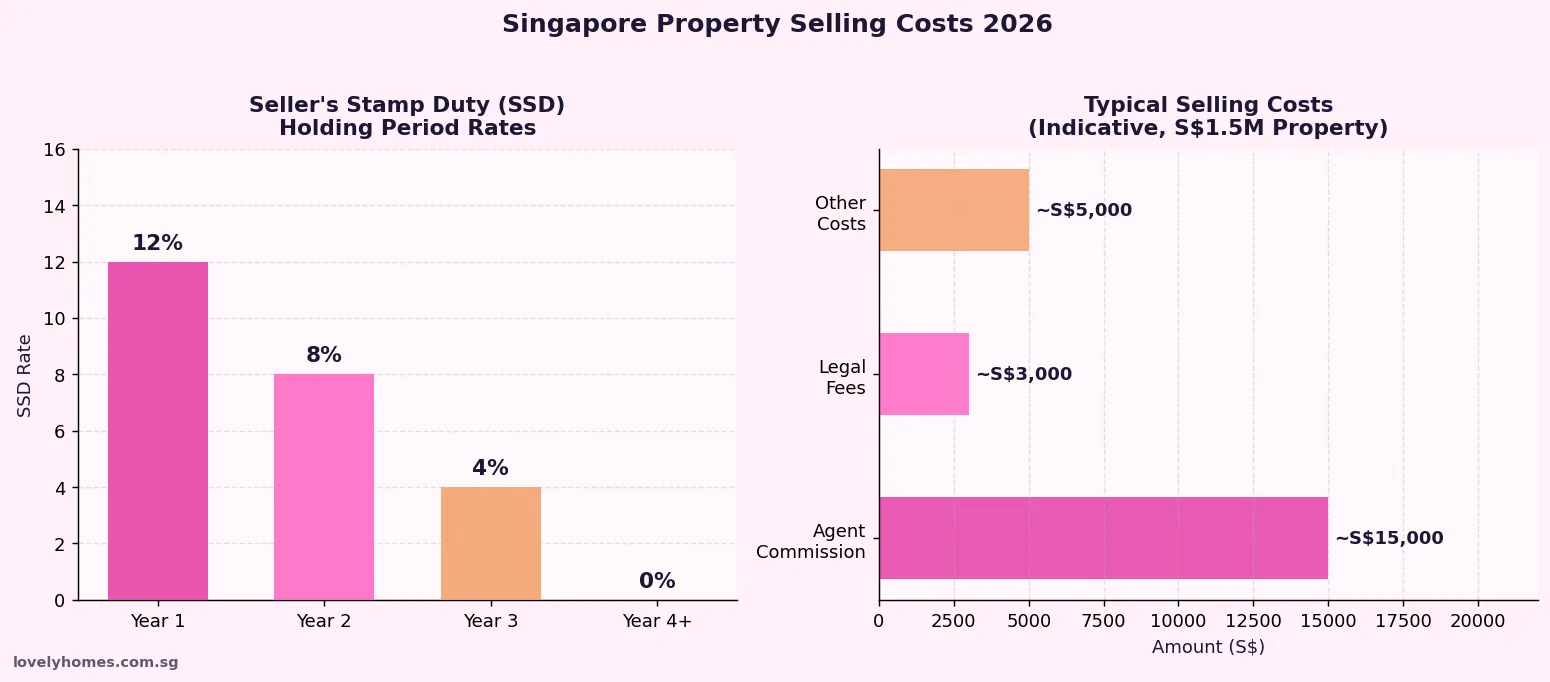

The Seller’s Stamp Duty (SSD) — introduced in January 2011 and most recently recalibrated in April 2023 — is the most significant policy lever for sellers. At 12% for properties sold within the first year of purchase, SSD is designed to deter speculative flipping. This guide covers every major cost and step for selling a private residential property (condo, landed, or HDB) in Singapore in 2026.

Figure 1: Seller’s Stamp Duty (SSD) rates and indicative selling cost components for a S$1.5M property, Singapore 2026.

Seller’s Stamp Duty (SSD) — Rates and Rules

Seller’s Stamp Duty is payable by the seller if a residential property is sold within 3 years of its purchase date (for private properties). The rates are based on the higher of the sale price or market value:

Holding Period

SSD Rate (Current, from Apr 2023)

SSD on S$1.5M Sale

Up to 1 year

12%

S$180,000

More than 1, up to 2 years

8%

S$120,000

More than 2, up to 3 years

4%

S$60,000

More than 3 years

0%

Nil

HDB flats are not subject to SSD, but have their own MOP (Minimum Occupation Period) of 5 years — during which the flat cannot be sold on the resale market at all.

All Costs When Selling Your Property

Cost

Typical Amount

Paid by / When

Agent Commission

1–2% of sale price

Seller; at completion

Legal Fees (conveyancing)

~S$2,500–S$4,000

Seller; at completion

Seller’s Stamp Duty (SSD)

0–12% of sale price (if <3 years)

Seller; within 14 days of OTP exercise

Mortgage Early Repayment Penalty

0.75–1.5% of outstanding loan (if in lock-in)

Seller; upon full redemption at completion

CPF Refund (OA + Accrued Interest)

All CPF used + 2.5% p.a. compound interest

Mandatory; deducted from proceeds at completion

Property Tax (prorated to sale date)

Varies by AV; prorated to completion date

Seller; adjusted at completion

HDB Admin Fee (HDB resale only)

S$40–S$80

Seller; to HDB

Worked Example: Selling a S$1.5M Condo Purchased 2 Years Ago

Scenario: SC seller, selling a condo purchased in April 2024 for S$1.4M, now selling in April 2026 at S$1.5M. Outstanding bank loan: S$900,000. CPF used: S$200,000 OA + S$10,000 accrued interest.

Gross Sale Price: S$1,500,000

Less SSD (8% × S$1.5M, sold in year 2): −S$120,000

Less Agent Commission (1.5%): −S$22,500

Less Legal Fees: −S$3,000

Less Outstanding Loan Redemption: −S$900,000

Less CPF Refund (S$200K + S$10K interest): −S$210,000

Net Cash Proceeds to Seller: S$1,500,000 − S$120,000 − S$22,500 − S$3,000 − S$900,000 − S$210,000 = S$244,500

Of which cash in hand (after CPF returned to CPF, not to pocket): ~S$244,500 (cash) + S$210,000 returned to CPF OA

Note: This example excludes any early repayment penalty on the bank loan. Verify with your bank and a property consultant. IRAS may treat profits as income if you are assessed as a property trader — consult a tax professional if you have sold multiple properties in recent years.

The Private Property Sale Process — Step by Step

For a private residential property (condominium or landed), the sale process broadly follows these stages over 10–12 weeks:

Appoint a CEA-licensed agent (or sell directly). Agent markets the property, manages viewings, and facilitates negotiations.

Accept an offer and grant an OTP. The buyer pays an Option Fee (typically 1% of agreed price). The OTP is valid for 14 days (standard) — extendable to 21 days by agreement.

Buyer exercises OTP — pays the balance 4–9% deposit within the OTP period. Both buyer and seller appoint conveyancing solicitors.

Solicitors conduct due diligence — title search, CPF charge check, Inland Revenue caveats, mortgagee consent if applicable.

Completion — typically 8–10 weeks after OTP exercise. Sale proceeds are disbursed, mortgage is redeemed, CPF is refunded, and keys are handed over.

Frequently Asked Questions

Is there Capital Gains Tax on property sales in Singapore?

No. Singapore does not impose a Capital Gains Tax on property sales by individuals. Profits from property sales are not taxable — provided IRAS does not classify you as a property trader (i.e. someone who buys and sells properties as a business, subject to income tax on profits). If you have sold multiple properties in a short period, consult a tax professional to confirm your IRAS classification. The Inland Revenue Authority of Singapore (IRAS) administers all property tax matters.

How is the CPF refund calculated when I sell my property?

Upon selling your property, you must refund to your CPF OA: (1) all CPF funds withdrawn for the property (down payment, monthly instalments, BSD, legal fees funded by CPF), plus (2) accrued interest at 2.5% per annum, compounded annually, on those withdrawn amounts. This refund goes back into your CPF OA — it is not a tax, but it reduces the cash proceeds you receive. The CPF Board calculates the exact refund amount at completion. For long-held properties with large CPF withdrawals, accrued interest can be significant.

What if the sale price is less than the outstanding loan and CPF refund?

If the sale proceeds are insufficient to fully redeem the outstanding mortgage and refund all CPF funds with accrued interest, you would face a shortfall. In this scenario, you would need to top up the difference in cash. This is sometimes called a “negative sale.” To avoid this situation, sellers should always compute their minimum viable sale price before listing — accounting for loan balance, CPF refund, SSD, agent fees, and legal costs.

Can I avoid SSD by transferring the property to a family member?

No. SSD applies to all legal transfers of residential property within the holding period — including transfers to family members, whether by sale, gift, or trust arrangement. IRAS treats these as disposals subject to SSD. Section 33A of the Stamp Duties Act also provides anti-avoidance powers allowing IRAS to look through artificial arrangements designed to circumvent stamp duty obligations. Seek advice from a qualified stamp duty lawyer before attempting any form of property restructuring.

What happens if I have an HDB bank loan and sell before 3 years?

Unlike private property, HDB flats carry no SSD on their own — however, HDB resale flats cannot be sold during the 5-year MOP. If you have a bank loan (not an HDB concessionary loan) on a private property, an early redemption penalty (clawback) of 0.75%–1.5% of the outstanding loan may apply if you sell during the loan’s lock-in period (typically 1–3 years). Check your bank’s loan terms carefully before committing to sell. HDB concessionary loans do not carry lock-in penalties.

Disclaimer: Information on this page is for general reference only and does not constitute professional property, legal, financial, or tax advice. Stamp duty rules, CPF policies, and property regulations may change — verify all details with IRAS (iras.gov.sg), CPF Board (cpf.gov.sg), and HDB (hdb.gov.sg) before transacting. Consult a CEA-licensed property agent and a qualified solicitor for transaction-specific advice. LovelyHomes.com.sg does not hold a real estate agency licence.

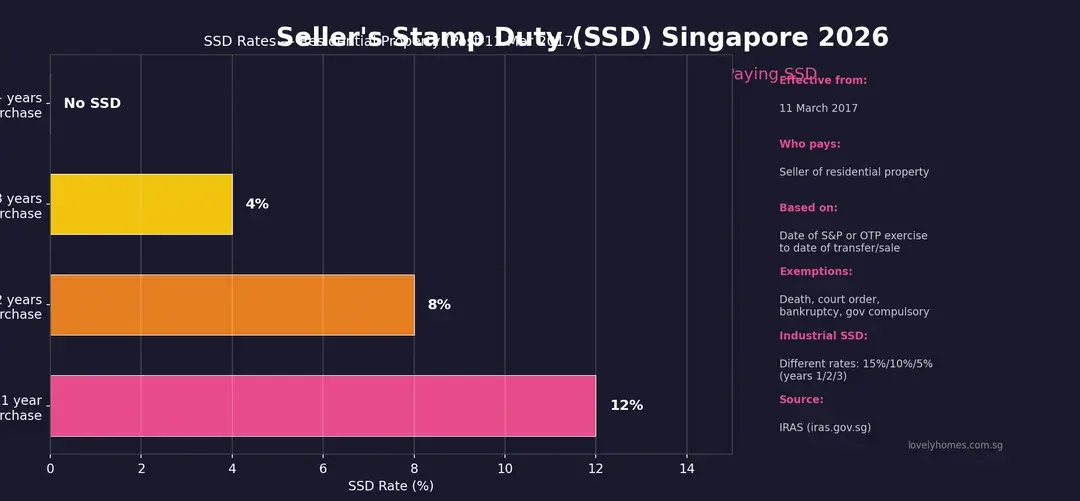

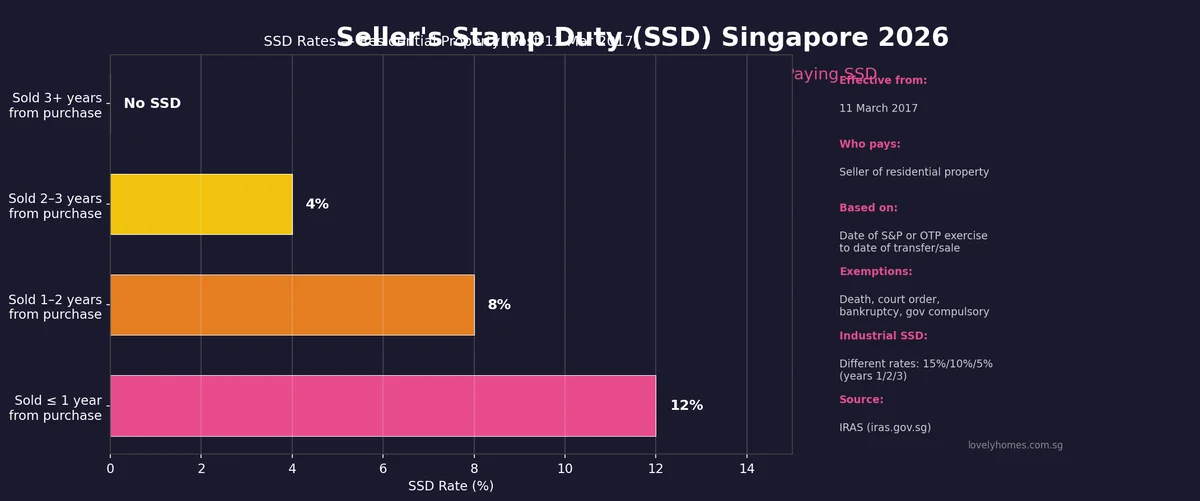

Quick Answer — Seller’s Stamp Duty (SSD) in Singapore

SSD is a tax payable by the seller of a Singapore residential property if it is sold within 3 years of purchase.

Rate is 12% if sold within 1 year, 8% if sold in Year 2, and 4% if sold in Year 3. No SSD after 3 years.

SSD is calculated on the higher of the sale price or the property’s market value at the time of sale.

Current rates have been in force since 11 March 2017 — unchanged through multiple rounds of cooling measures since.

Key exemptions: disposal by court order, bankruptcy proceedings, Government compulsory acquisition, and transfer due to death of owner.

Industrial property has different SSD rates: 15% (Year 1), 10% (Year 2), 5% (Year 3) — and a 3-year holding period applies.

Figure 1: Seller’s Stamp Duty (SSD) Singapore 2026 — rates by holding year for residential property. Source: IRAS.

What is Seller’s Stamp Duty (SSD)?

Seller’s Stamp Duty is a property transaction tax introduced by the Singapore Government as a property market cooling measure. It targets short-term speculators and property flippers — buyers who purchase residential property intending to sell quickly for a profit. The SSD creates a disincentive to sell within the first three years of purchase by imposing a tax on the sale proceeds, calibrated to be punishing in Year 1 (12%), moderately deterring in Year 2 (8%), and mildly deterring in Year 3 (4%), with no penalty after Year 3.

SSD was first introduced on 20 February 2010 during the first wave of post-Global Financial Crisis cooling measures. Since then, the rates and holding period have been revised multiple times. The current regime — 12%/8%/4% across a 3-year holding period — was established on 11 March 2017, when the Government eased the rules from the previous 16%/12%/8%/4% four-year regime. This easing was the last SSD adjustment to date; despite multiple ABSD increases in 2021, 2022 and 2023, SSD has remained unchanged.

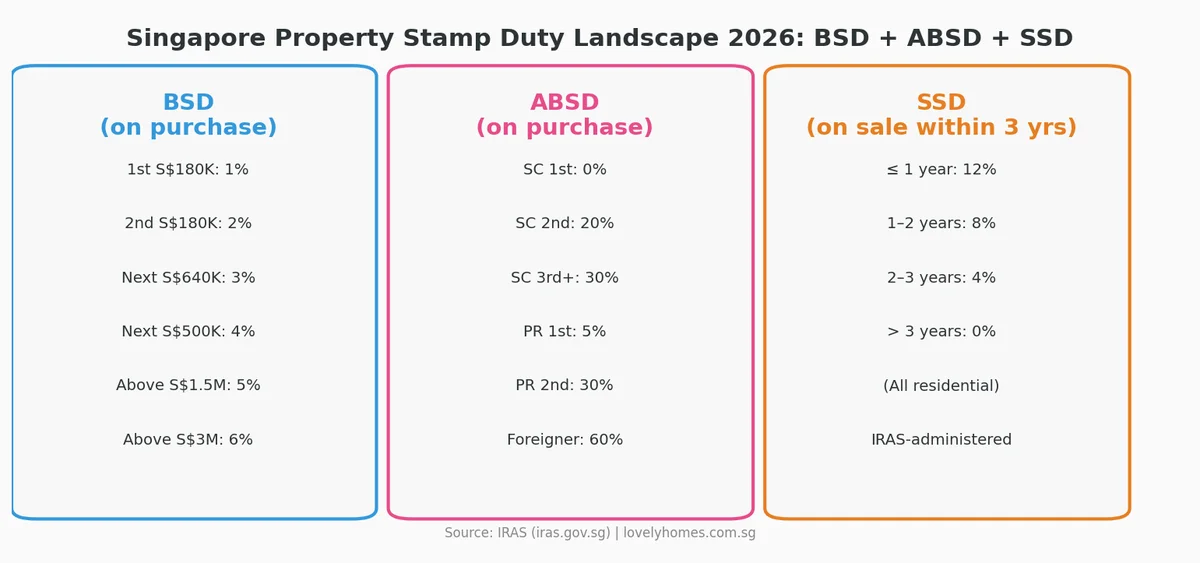

Figure 3: Singapore’s three property stamp duties at a glance — BSD (purchase), ABSD (purchase, ownership-count dependent), and SSD (sale within 3 years). Source: IRAS.

SSD rates for residential property — current (from 11 March 2017)

Holding Period

SSD Rate

Example (S$1.5M property)

Year 1 (sold within 12 months of purchase)

12%

~S$180,000 on a S$1.5M property

Year 2 (sold 12–24 months after purchase)

8%

~S$120,000 on a S$1.5M property

Year 3 (sold 24–36 months after purchase)

4%

~S$60,000 on a S$1.5M property

After 3 years (sold 36+ months after purchase)

0%

No SSD payable

SSD is calculated on the higher of the sale price or the market value at the date of sale. Assessed by IRAS. Must be paid within 14 days of signing the Option to Purchase (OTP) or Sales and Purchase Agreement (S&P).

How the holding period is calculated — critical details

The SSD holding period is measured from the date of purchase (date of execution of the OTP or S&P by the buyer) to the date of disposal (date of execution of the OTP or S&P by the seller to the next buyer). It is not measured from the date of completion, the date of lodging the caveat, or the date of transfer at the Land Titles Registry. This creates a practical implication: if you sign an OTP on 10 April 2023 and you sign another OTP granting your buyer an option on 11 April 2026 — that is exactly 3 years and 1 day — no SSD is payable.

For properties purchased under a building-under-construction (BUC) scheme (new launches where payment is tied to construction progress), the date of purchase is the date of the S&P agreement, not the date of TOP or legal completion. This means buyers who bought at the launch of a 4-year construction project — say, in 2022 for a 2026 TOP — have already been holding for 4 years by TOP and are SSD-free from the day of collection.

SSD base value — sale price vs market value

SSD is charged on the higher of: (a) the sale price, or (b) the property’s market value at the time of sale. This prevents sellers from artificially understating the sale price to reduce SSD liability. IRAS has the power to assess market value independently. In practice, for arm’s-length transactions in the open market, the sale price and market value will typically be equivalent or very close. SSD is assessed by IRAS based on the stamp duty valuation and must be paid within 14 days of the date of signing the instrument (OTP or S&P).

SSD exemptions — when you do not have to pay

IRAS recognises several circumstances where SSD is waived or not applicable:

Transfer upon death — if the property is transferred to a beneficiary under a will or intestacy, SSD is not payable by the estate.

Court-ordered transfer — divorce proceedings that result in a court-ordered transfer of residential property are exempt from SSD.

Government compulsory acquisition — if the Government acquires the property under the Land Acquisition Act, no SSD applies.

Bankruptcy proceedings — a sale by a trustee in bankruptcy is exempt from SSD.

Housing developers — a licensed housing developer that sells residential units as part of its development business is not subject to the residential SSD regime (they are subject to ABSD remission conditions instead).

HDB flat transfers within family — certain intra-family HDB flat transfers are exempt, subject to HDB approval.

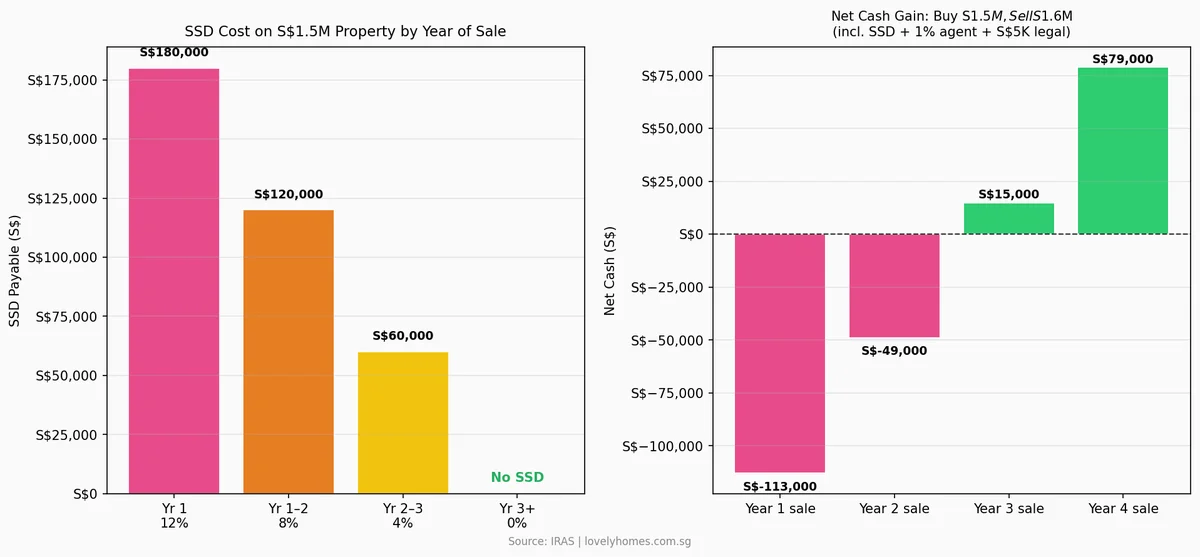

Worked example — the cost of selling early

Figure 2: Net cash outcome for a seller who buys at S$1.5M and sells at S$1.6M — showing how SSD eliminates profit in Years 1–2 and reduces it significantly in Year 3.

Consider a Singapore Citizen (first property) who buys a private condominium at S$1,500,000 on 1 April 2024 and sells at S$1,600,000 (a 6.7% gain). Assuming a 1% agent commission (S$16,000) and S$5,000 in legal fees, the net cash outcome varies dramatically by year of sale:

Sell Year 1

Sell Year 2

Sell Year 3

Sell Year 4+

Gross sale proceeds

S$1,600,000

S$1,600,000

S$1,600,000

S$1,600,000

SSD payable

S$192,000 (12%)

S$128,000 (8%)

S$64,000 (4%)

S$0

Agent commission (1%)

S$16,000

S$16,000

S$16,000

S$16,000

Legal fees (est.)

S$5,000

S$5,000

S$5,000

S$5,000

Net cash before mortgage clearance

S$−213,000 net loss

S$−149,000 net loss

S$15,000 net gain

S$79,000 net gain

Including S$100K CPF + accrued interest (8 yrs @ 2.5%)

—

—

~S$−105,000 after CPF refund

~S$−29,000 after CPF refund (10 yrs)

The example is clear: at a 6.7% gain (S$100,000 appreciation), selling in Year 1 or Year 2 produces a net loss after SSD and transaction costs. Year 3 produces a modest net gain. Year 4 and beyond is when the full gain materialises in cash. The implication for property investors: unless the property appreciates by more than 12–13% in the first year (covering SSD at 12% plus transaction costs), there is no financial case for selling within the SSD window.

SSD history — from 2010 to today

Date

Change

Detail

20 Feb 2010

SSD introduced

Holding period: 1 year; Rate: 1%

30 Aug 2010

SSD tightened

Holding period extended to 3 years; Rates: 3%/2%/1%

14 Jan 2011

SSD tightened further

Holding period extended to 4 years; Rates: 16%/12%/8%/4%

11 Mar 2017

SSD relaxed (current)

Holding period reduced to 3 years; Rates: 12%/8%/4%

27 Sep 2022

ABSD increased (SSD unchanged)

SSD rates held; ABSD for SC 2nd property raised to 20%

26 Apr 2023

ABSD increased again (SSD unchanged)

ABSD for foreigners raised to 60%; SSD unchanged

Industrial property SSD — different rules

For industrial properties (factories, warehouses, business parks, but not offices), a separate SSD regime applies with more punishing rates over a longer holding period. The current industrial SSD was introduced on 12 January 2013:

Holding Period

SSD Rate

Year 1 (≤ 12 months)

15%

Year 2 (12–24 months)

10%

Year 3 (24–36 months)

5%

Year 4+ (> 36 months)

0%

Industrial SSD is particularly relevant for buyers of strata industrial units (factories, LB1 mixed-use units) and commercial investors who may be considering the industrial sub-market as an alternative to residential. The 3-year holding period is the same as residential, but the Year 1 rate of 15% makes early disposal very costly.

SSD and decoupling — interaction with ABSD avoidance strategies

A common property structuring question is whether decoupling (transferring a jointly-owned property to one spouse, then using the other spouse’s clean slate to buy a second property without ABSD) triggers SSD. The answer: yes, if the decoupling transfer occurs within the 3-year SSD holding period. The date of the initial purchase is the reference date; if a couple purchased in 2024 and decouples (transfers one owner’s share to the other) in 2025, SSD at 8% applies on the half-share transferred. This is a significant deterrent to decoupling young properties and must be factored into any ABSD avoidance calculation. For detailed analysis of decoupling economics, see our Decoupling Property Guide.

SSD vs ABSD vs BSD — when each applies

Tax

Who Pays

When

Rate

Holding Rule

Buyer’s Stamp Duty (BSD)

Buyer

On purchase

All residential (graduated: 1%–6% on purchase price)

No holding period

Additional Buyer’s Stamp Duty (ABSD)

Buyer

On purchase

0–60% depending on citizenship and property count

No holding period (once paid, non-refundable for most)

Seller’s Stamp Duty (SSD)

Seller

On sale (if sold within 3 years)

12%/8%/4% of sale price or market value

Holding period: 3 years

Practical implications for Singapore property investors in 2026

The SSD regime fundamentally shapes Singapore’s residential property investment horizon. Here is what investors should factor into every decision:

Minimum 3-year holding period strategy — most experienced Singapore property investors budget for a minimum 3-year hold on any residential acquisition. Not because of SSD alone, but because BSD, legal fees, agent commissions and CPF accrued interest together mean you need meaningful appreciation (typically 10–15%) just to break even, and SSD on top of that makes any sub-3-year exit financially painful.

BUC purchases are already 3-4 years old at TOP — buyers of new launches in 2024–2025 with a 2028–2030 TOP will have cleared their 3-year SSD hold by the time they take possession. This means the first opportunity to sell is already SSD-free. For new launch buyers who plan to flip at TOP or shortly after, SSD is usually not a concern.

Resale condo purchases require a date check — buyers of 3-year-old or younger resale condominiums should check the prior owner’s original purchase date before assuming no SSD issue. As a resale buyer, your own 3-year SSD clock starts fresh from your purchase date.

Decoupling timing is critical — never decouple a property that is still within its 3-year SSD window without first modelling the SSD cost and comparing it to the ABSD saving from using a clean-slate buyer.

Market downturns can trap short-hold buyers — during the 2022–2023 rate-rise cycle, sellers who bought in 2020–2021 and needed to sell found themselves simultaneously facing SSD (if within 3 years) and a softer market. The SSD deterrent reduced distressed selling, which helped support Singapore property prices.

The SSD clock starts from the date of purchase — specifically, the date the buyer executes the Option to Purchase (OTP) or signs the Sales & Purchase Agreement (S&P). It does not start from legal completion, TOP, or the date of mortgage drawdown. When calculating whether you are out of the SSD window, count from the date you signed the purchase documents, not the date you got the keys.

Is SSD payable on the full sale price or only the profit?

SSD is payable on the full sale price (or market value if higher), not just the profit. This is what makes SSD so punishing: on a S$1.5M property sold at 12% SSD, you pay S$180,000 regardless of whether the property appreciated or depreciated. There is no offset for your purchase costs, stamp duties paid, or renovation expenditure.

Can SSD be avoided by gifting the property instead of selling?

No. A gift (transfer for no consideration) is still treated as a disposal by IRAS, and SSD is assessed on the market value of the property at the time of the gift. Similarly, transferring a property to a company, a trust, or a related party at below-market price does not avoid SSD — IRAS will assess based on market value.

Is SSD deductible against income tax?

For individuals holding investment properties, SSD paid is generally deductible as a cost of disposal when computing any capital gains — but since Singapore does not have a capital gains tax for individuals, this is largely academic. If a property is held as trading stock in a business (rare for individuals), SSD would be a deductible business expense. Always consult an accountant for your specific tax position.

Are HDB flat sales subject to SSD?

Yes. HDB resale flat sellers are subject to SSD if they sell within 3 years of purchase. However, HDB has its own Minimum Occupation Period (MOP) of 5 years — meaning you cannot sell a BTO or resale HDB flat on the open market for the first 5 years anyway. In practice, this means HDB resale sellers are always beyond their 3-year SSD window by the time they are legally allowed to sell, making SSD a non-issue for most HDB resale transactions.

What rate of appreciation is needed to break even after SSD?

To break even on a Year 1 sale, you need the property to appreciate enough to cover: SSD (12%) + BSD paid at purchase (~3–4% on a S$1.5M property) + agent fees (~1–2%) + legal fees (~0.3%) = approximately 17–18% appreciation in under 12 months. This is why property flipping in Singapore is economically unfeasible under the current SSD/BSD regime — the combined transaction costs are simply too high for any reasonable short-term gain.

What if I cannot afford to hold and must sell within 3 years?

If you face genuine financial hardship and must sell within the SSD window, you have limited options: (a) accept the SSD cost as the price of liquidity; (b) explore renting out the property (if permitted and the rental income covers carrying costs while you wait out the 3-year period); (c) approach IRAS for hardship consideration — in very limited circumstances (confirmed financial distress, not just suboptimal market timing), IRAS may consider remission, but this is rare and there is no formal remission channel for SSD. The best mitigation is to model your exit scenarios before purchasing.

Disclaimer: This article provides general information only and does not constitute financial, legal, or tax advice. SSD rates, holding periods, and exemptions are set by the Singapore Government and administered by the Inland Revenue Authority of Singapore (IRAS). Always verify the latest rules directly with IRAS (iras.gov.sg) or consult a licensed property agent, solicitor, and/or tax adviser before making any property transaction decision. LovelyHomes.com.sg is an independent editorial publication and is not an agent or adviser.