The condo downpayment question — how much cash does a Singapore buyer actually need on day 1 — sounds simple, but it is where most first-time buyers underestimate by S$50,000 or more. The answer depends on three overlapping rules (LTV, minimum cash, and stamp duties), and it changes dramatically if this is your second or third property.

This 2026 guide walks through exactly what you need to write cheques for on the day you collect your condo keys, with worked tables for first-property Singaporean citizens, second-property buyers, and foreign buyers. For the regulator’s guidance, see MAS Notice 632 on residential LTV.

Quick Answer — Condo Downpayment on a S$1.5m Unit

First condo, Singapore Citizen: ~S$119,600 cash + S$225,000 CPF/cash = S$344,600 total day-1 outlay (including BSD).

Second condo, Singapore Citizen: ABSD alone adds S$300,000. Total day-1 outlay S$1,169,600.

Foreigner buyer, any property: 60% ABSD on top of a 45% LTV. Total day-1 outlay S$1,769,600.

Minimum cash: 5% of purchase price for 75% LTV; 10% for 45% or 35% LTV.

BSD & ABSD: payable in cash within 14 days of OTP (reimbursable from CPF OA after).

The Three Rules That Set Your Downpayment

Three layers combine to set the cash and CPF you need:

Loan-to-Value (LTV) ratio. MAS caps bank lending at 75% for a first housing loan, 45% for a second, and 35% for a third and beyond. The balance is your downpayment.

Minimum cash portion. MAS requires at least 5% of the purchase price in cash for a first property, 10% for second and subsequent.

Stamp duties. BSD and, where applicable, ABSD are paid in cash within 14 days of OTP. You can reimburse from CPF afterwards.

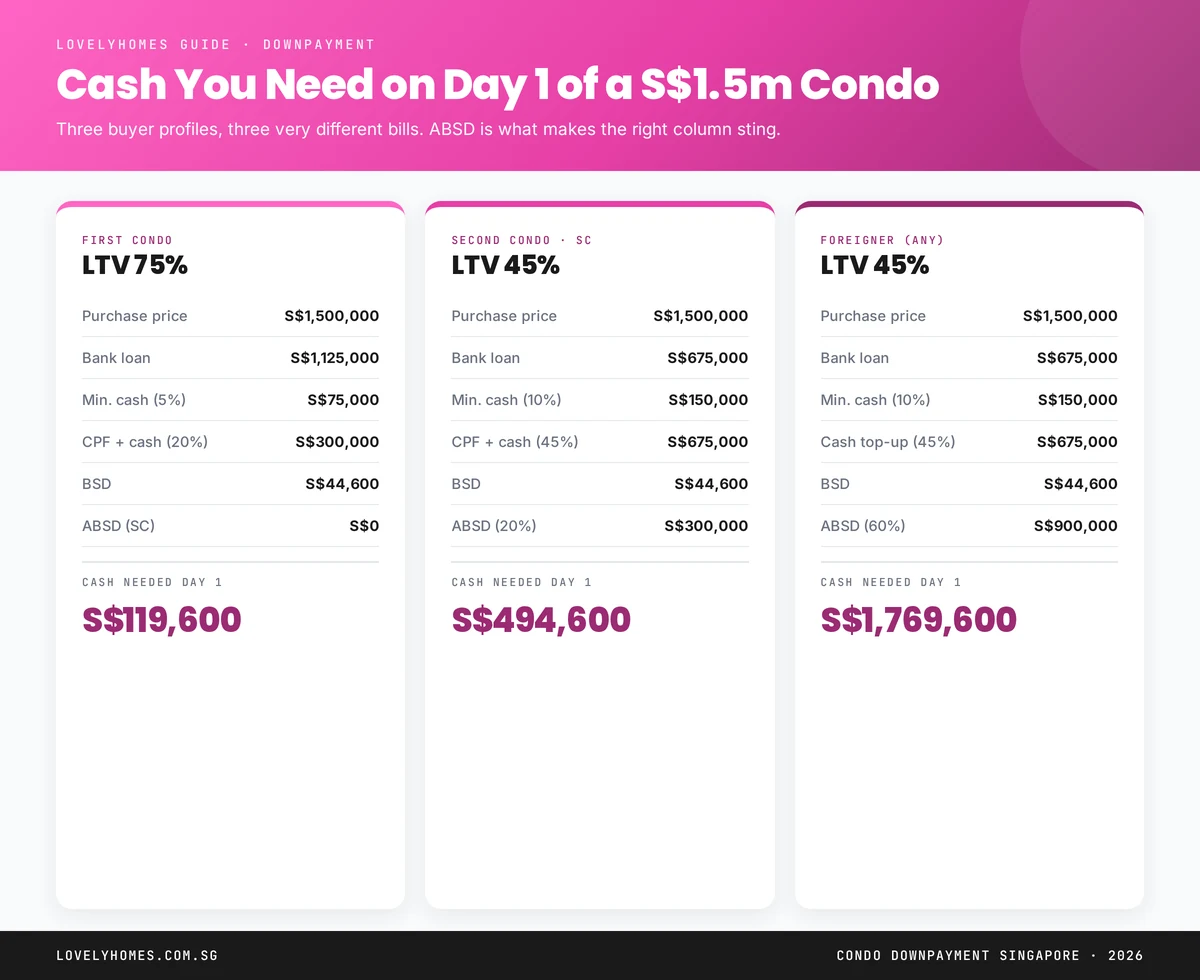

Figure 1: Same S$1.5m condo, three buyer profiles, cash needed on day 1 varies by nearly S$1.7 million.

First Property: Singapore Citizen on a 75% LTV

The easiest case. On a S$1.5m condo, an SC buying their first home gets:

Bank loan: up to S$1,125,000 (75% LTV, subject to TDSR).

Downpayment: S$375,000 split as:

Minimum 5% cash: S$75,000 — this is a hard floor, not a guideline.

Remaining 20%: up to S$300,000 can come from CPF OA, cash, or a combination.

BSD: ~S$44,600 (progressive on S$1.5m, capped at 5% at this level).

ABSD: 0% (first residential property for a Singapore Citizen).

Total cash needed on day 1: S$75,000 (min. cash) + S$44,600 (BSD) = S$119,600. BSD can be reimbursed from CPF OA after stamping.

Second Property: Singapore Citizen on a 45% LTV

Two major shifts bite here. First, LTV drops to 45% — meaning you fund 55% of the purchase. Second, ABSD kicks in at 20%.

Bank loan: S$675,000 maximum.

Downpayment: S$825,000 split as:

Minimum 10% cash: S$150,000.

Remaining 45%: S$675,000 from CPF OA, cash, or combination.

BSD: S$44,600.

ABSD (20% SC 2nd): S$300,000.

Total cash needed day 1: S$150,000 + S$44,600 + S$300,000 = S$494,600. That is before the S$675,000 of CPF/cash needed to reach the loan ceiling.

The most expensive profile. Foreign non-residents face LTV 45% (most banks drop to 40% for non-residents without local income), plus a flat 60% ABSD.

Bank loan: S$675,000 maximum.

Downpayment: S$825,000 in cash (no CPF access for foreigners).

BSD: S$44,600.

ABSD (60%): S$900,000.

Total cash needed day 1: S$1,769,600 against a S$1.5m purchase price. Many foreign buyers end up paying 100%+ cash when accounting for legal fees and renovation.

What About CPF OA?

CPF Ordinary Account can cover most of the non-minimum-cash portion of the downpayment, plus BSD/ABSD reimbursement after stamping. Critical caveats:

For private property, CPF usage caps at the Valuation Limit (purchase price or valuation, whichever lower) and the Withdrawal Limit of 120% of VL.

Every dollar used compounds at 2.5% accrued interest — see our CPF for Property guide for the full maths.

New Launch vs Resale: Different Cash-Flow Timing

For a new launch (BUC — Building Under Construction), payments are staggered via the Progressive Payment Scheme. You typically need 25% at the Sale & Purchase Agreement (5% OTP deposit + 20% at S&PA), then 10% at foundation, 10% at reinforced concrete, etc. This reduces upfront cash strain dramatically.

For a resale, the entire downpayment hits at completion — typically 10–14 weeks after OTP. You need the full amount in cash and CPF by completion day.

TDSR Still Applies

The LTV numbers above are ceilings, not entitlements. Your actual bank loan may be smaller if your TDSR maxes out first — see our TDSR & MSR guide. A couple earning S$16,000 a month may qualify for a S$1.1m loan under TDSR even if LTV would allow S$1.125m on a S$1.5m purchase. In that case, the extra S$25,000 shortfall is yours to fund in cash or CPF.

Frequently Asked Questions

Can I put down more than 5%/10% in cash?

Yes. The minimums are floors, not ceilings. Some buyers put 20%+ cash to reduce their loan quantum and future interest.

Does option fee count as part of the downpayment?

Yes. The 1% Option Money and the 4% Option Exercise Fee together form the initial 5%, which is also the minimum cash portion for a first property.

Can I borrow more than 75% LTV?

Not from a MAS-regulated bank. Some private financing vehicles lend above 75% but at materially higher rates and with punitive terms — we do not recommend this route.

Does the 75% LTV apply to under-construction properties?

Yes, but payment is progressive — you do not need the full downpayment on day 1 for a new launch.

What if I am using an HDB loan for an HDB flat, not a bank loan for a condo?

HDB concessionary loans offer up to 75% LTV with 0% minimum cash. See our HDB Loan vs Bank Loan guide for the full difference.

Disclaimer: This guide is general information, not financial advice. LTV and stamp-duty rules are subject to change. Verify current rules at mas.gov.sg and iras.gov.sg, and consult a licensed mortgage broker.

Wait-Out Period: Private property owners must wait 15 months before buying HDB resale without grant.

What are Singapore’s Property Cooling Measures?

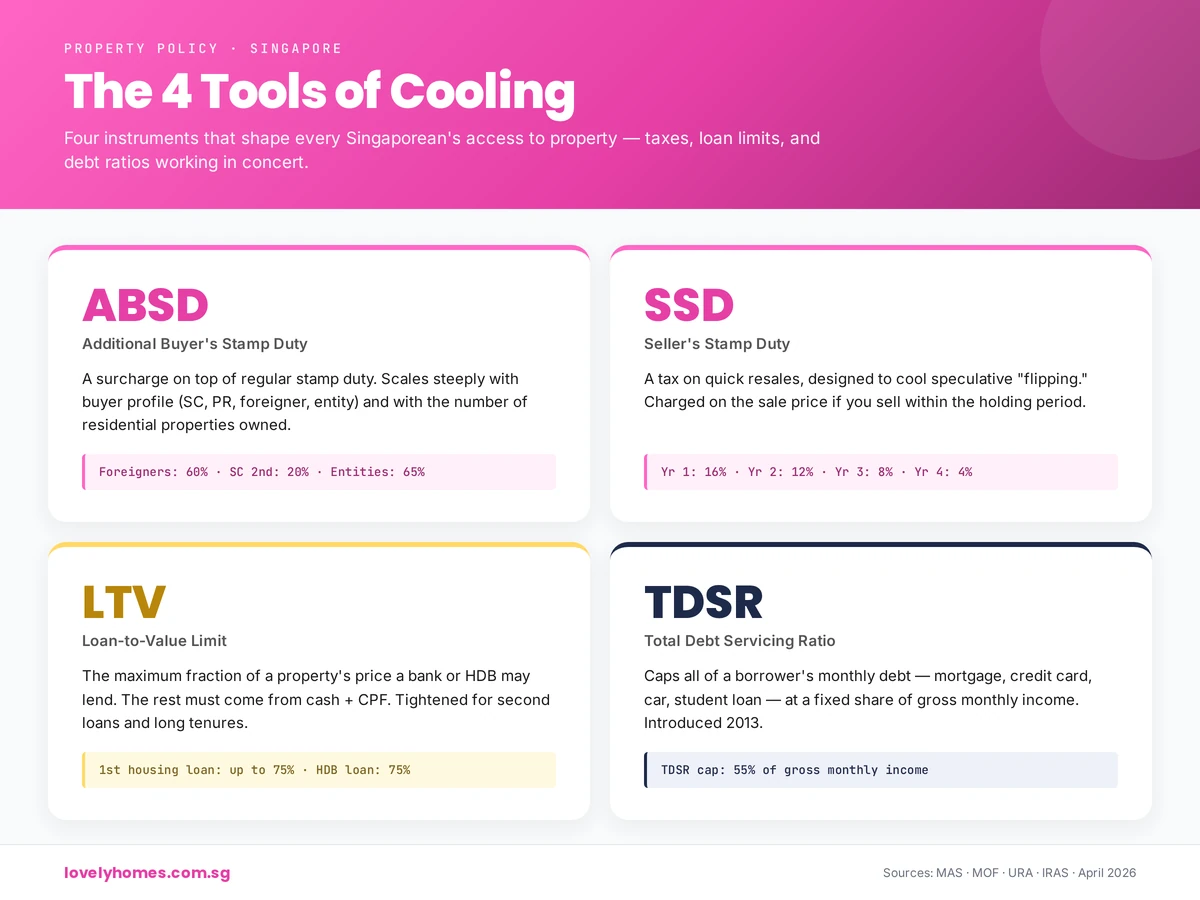

Singapore’s property cooling measures are a suite of policy tools designed to moderate demand, curb speculation, and ensure housing remains affordable. They exist because rapid property price growth can outpace wage growth, lock first-time buyers out of the market, and create unsustainable bubbles. Four key agencies administer these measures: the Monetary Authority of Singapore (MAS), the Urban Redevelopment Authority (URA), the Inland Revenue Authority of Singapore (IRAS), and the Housing and Development Board (HDB). Together, they apply tools such as stamp duties, loan limits, affordability tests, and holding periods to regulate the market and protect both buyers and the broader economy.

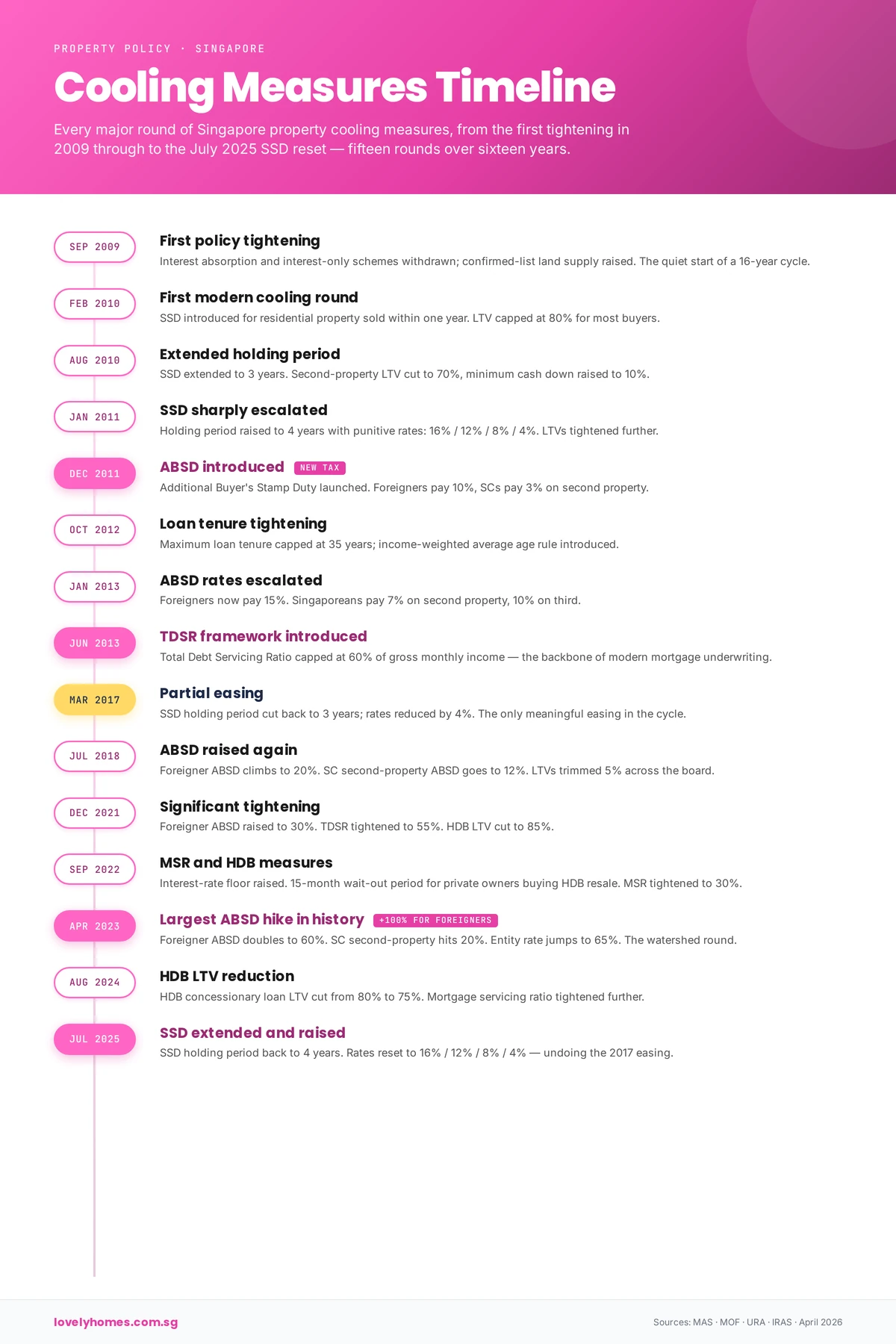

Figure 1: The 15 major rounds of Singapore property cooling measures, 2009–2026.

September 2009: The First Policy Tightening

Before the modern cooling era, the government moved to restrict lending practices. In September 2009, the Monetary Authority of Singapore (MAS) disallowed two risky loan products: the Interest Absorption Scheme (IAS) and Interest-Only Housing Loans (IOL). These products had allowed borrowers to defer principal repayment during the early years of a mortgage, increasing default risk during rate rises. By banning them, the government signalled a preference for prudent, full-amortising loans and set the stage for the more comprehensive cooling measures that would follow.

February 2010: The First Modern Cooling Round

On 20 February 2010, Singapore introduced its first comprehensive cooling package, reflecting rapid price growth and surging demand. The government introduced two major tools:

Seller’s Stamp Duty (SSD): Properties sold within one year were hit with a 3% SSD. The intent was to discourage “flipping”—rapid resale for short-term gain.

Loan-to-Value (LTV) limit: Reduced from 90% to 80%, requiring buyers to put down at least 20%. This reduced lender exposure and made buyers more cautious.

These measures reflected a key insight: when buyers can leverage heavily and exit quickly, prices can spiral. By raising the entry cost and the holding cost, the government aimed to attract only genuine buyers.

August 2010: Extended Holding Period

By mid-2010, demand remained strong. On 19 August 2010, the government extended the SSD holding period from 1 year to 3 years, raising the cost of short-term resale. For those with existing loans, the LTV limit tightened further to 70%, and cash downpayment requirements rose, particularly hurting leveraged investors.

January 2011: Sharp SSD Escalation

Recognising that the market was still overheating, the government on 8 January 2011 escalated the SSD significantly. The new structure was:

Year 1: 16%

Year 2: 12%

Year 3: 8%

Year 4: 4%

The rationale was unmistakable: hold for less than a year and lose a sixth of your sale price. LTV limits were also tightened to 60% for those with existing loans, making it much harder for property investors to string together multiple mortgages.

December 2011: ABSD Introduced

On 8 December 2011, Singapore introduced the Additional Buyer’s Stamp Duty (ABSD), its most powerful tool. ABSD was a second layer of stamp duty on top of the normal Buyer’s Stamp Duty (BSD), calibrated to buyer type:

Singapore Citizens buying a 2nd+ property: 3%

Singapore Citizens buying a 3rd+ property: 3%

Permanent Residents buying a 2nd+ property: 3%

Foreigners: 10%

Corporate entities: 10%

ABSD was revolutionary because it directly attacked investment demand, particularly from overseas. It signalled that Singapore prioritised homeownership for citizens over investment returns for outsiders.

October 2012: Loan Tenure Tightening

The Monetary Authority of Singapore further tightened lending on 19 October 2012. The maximum loan tenure was capped at 35 years, with a penalty: if LTV remained above 60% after 30 years, the LTV would be capped at 40% in year 31 onwards. This forced borrowers to repay principal faster, reducing their borrowing power and making loans less attractive.

January 2013: ABSD Escalation

On 11 January 2013, the government raised ABSD across the board:

Singapore Citizens (2nd property): 7%

Singapore Citizens (3rd+ property): 10%

Permanent Residents (2nd+ property): 10%

Foreigners: 15%

Entities: 15%

The hike reflected continued demand, particularly from foreign investors and corporate buyers. Cash downpayment requirements also rose, targeting multiple-property owners and entities.

June 2013: TDSR Framework Introduced

On 28 June 2013, the Monetary Authority of Singapore introduced the Total Debt Servicing Ratio (TDSR) framework. TDSR capped total monthly debt repayments (mortgage, car loan, credit cards, personal loans, etc.) at 60% of gross monthly income. The intention was to prevent over-leverage: even if house prices were rising, a banker couldn’t lend to someone whose entire income was going to debt service.

This was a game-changer because it wasn’t about house prices directly—it was about borrower health. It also forced banks to stress-test loans, assuming interest rates would rise, to ensure borrowers could survive a shock.

March 2017: Partial Easing

By 2016–2017, prices had stabilised and growth had slowed. On 5 March 2017, the government eased some measures:

SSD holding period reduced from 4 years to 3 years, though rates remained steep (12%/8%/4% for years 1–3).

TDSR and ABSD eased slightly for refinancing.

This signalled a shift: the government was confident the market was no longer overheating and could afford marginal relief.

July 2018: ABSD Raised Again

By mid-2018, there were signs of renewed speculative interest, particularly from foreign and corporate buyers. On 6 July 2018, the government raised ABSD sharply:

LTV limits also tightened by 5 percentage points across all categories, making down payments larger and borrowing power lower.

December 2021: Significant Tightening

After years of near-zero interest rates post-COVID, demand surged again. On 16 December 2021, the government announced a comprehensive tightening:

ABSD raised again: foreigners to 30%; entities to 35%; PR 2nd property to 20%.

TDSR tightened from 60% to 55% of gross monthly income.

Interest-rate floor for TDSR/MSR calculations raised to 3.5% for private bank loans (previously 3%).

HDB LTV limits reduced across the board.

This was a significant hardening, reflecting real concern about affordability following three years of price growth.

September 2022: MSR and HDB Measures

On 30 September 2022, the government introduced new measures targeting the HDB resale market, where first-time buyers (and upgraders) primarily shop:

Mortgage Servicing Ratio (MSR) introduced: For HDB and Executive Condominium (EC) loans, monthly mortgage payments cannot exceed 30% of gross income—stricter than TDSR’s 55%.

15-month wait-out period: Private property owners must wait 15 months after selling before buying an HDB resale flat, curbing investor demand for subsidised public housing.

Interest-rate floor for TDSR/MSR raised from 3% to 3.5% for private loans; 3% for HDB loans.

These moves directly sheltered first-time HDB buyers from investor competition.

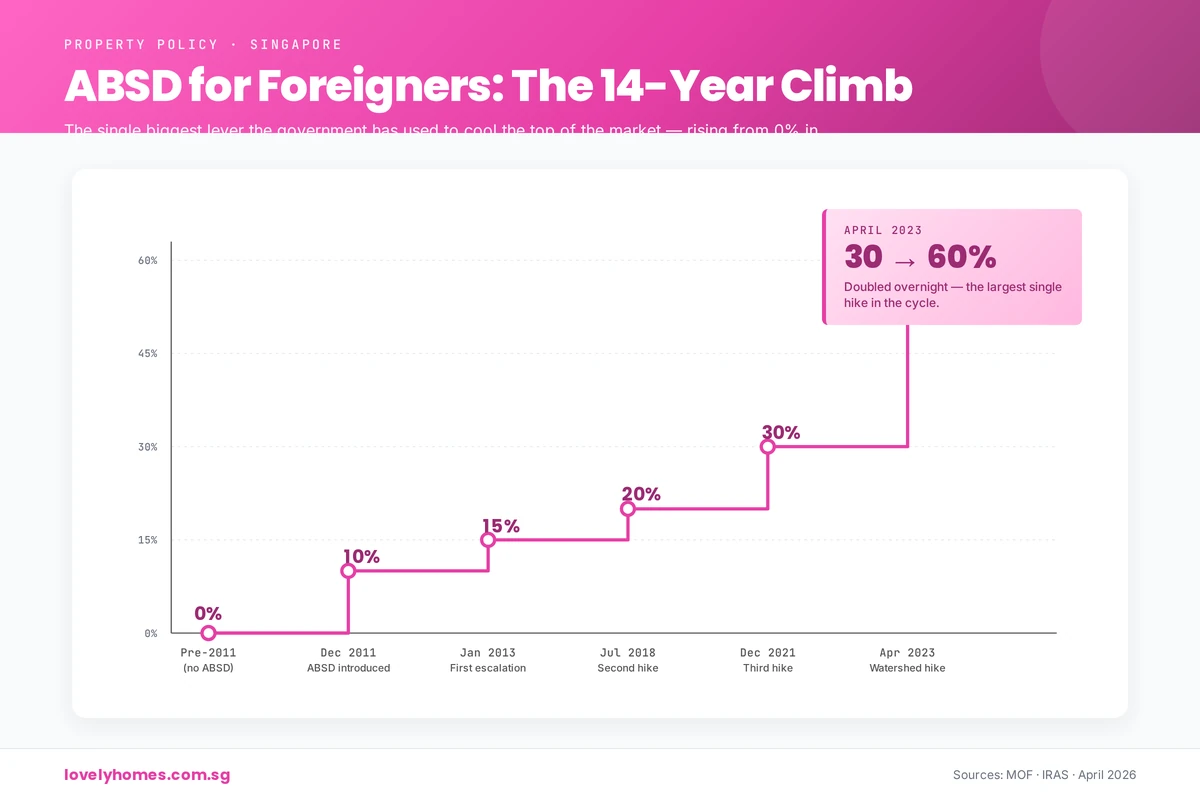

Figure 3: Foreigner ABSD climbed from 0% in 2011 to 60% in April 2023 — the largest single hike in the cycle.

April 2023: Largest ABSD Hike in History

On 27 April 2023, faced with renewed price acceleration in Q1 2023 (especially among owner-occupiers), the government announced its largest ABSD increase:

This was the most aggressive escalation since ABSD’s introduction, reflecting the government’s determination to prioritise homeownership for citizens and slow speculation. A foreign buyer purchasing a S$2 million condo now faced S$1.2 million in ABSD—an enormous barrier.

August 2024: HDB LTV Reduction

On 20 August 2024, the government reduced the Loan-to-Value (LTV) limit for HDB-granted housing loans from 80% to 75%. This meant HDB buyers now needed a 25% down payment instead of 20%, directly reducing borrowing power for this segment. Concurrently, higher CPF Housing Grants were introduced for first-time buyers to offset the impact, retaining affordability.

July 2025: SSD Extended and Raised

On 3 July 2025, the government responded to a spike in “flipping”—buyers purchasing uncompleted units (off-plan) and reselling before completion or soon after. The SSD holding period was extended from 3 years to 4 years, and rates were raised across the board by 4 percentage points:

Year 1: 20% (from 16%)

Year 2: 16% (from 12%)

Year 3: 12% (from 8%)

Year 4: 8% (from 4%)

This further discouraged short-term speculation while allowing long-term owners to exit penalty-free after four years.

Current Cooling Measures Framework (April 2026)

The current cooling-measures framework, established by the 27 April 2023 ABSD hike and subsequently adjusted by the 20 August 2024 HDB LTV reduction and the 4 July 2025 SSD restructure, remains in force as at April 2026. MAS, MND, URA and HDB jointly review the framework regularly and have repeatedly indicated they will recalibrate the measures — either tightening or easing — in response to market conditions.

Figure 2: The four core cooling tools — taxes (ABSD, SSD), loan limits (LTV) and debt ratios (TDSR) working in concert.

Let’s illustrate the impact with a hypothetical Singapore Citizen (SC) buying a second property valued at S$2 million:

Year

ABSD Rate

ABSD Cost (S$)

BSD + ABSD Total

2010 (Feb)

0%

S$0

~S$20,000 (BSD only)

2013 (Jan)

7%

S$140,000

~S$160,000

2018 (July)

7%

S$140,000

~S$160,000

2023 (April)

20%

S$400,000

~S$420,000

2026 (April)

20%

S$400,000

~S$420,000

Notice the leap from 2013 to 2023: the cost of buying a second home more than doubled in stamp duty alone, while the property value remained constant. This is the direct impact of cooling measures: they make property ownership more expensive, not by changing the property itself, but by raising friction and entry costs.

Why Have Cooling Measures Worked?

Singapore’s housing market has not crashed, despite aggressive cooling measures—a fact some cite as evidence of failure. But that misses the point. Cooling measures are designed to slow, not stop, price growth; to reduce speculation, not eliminate it; and to align prices with incomes, not freeze them.

Consider the evidence:

Slower growth: Private residential property annual price gains have typically stayed in the 2–5% range post-2013, compared to double-digit growth in the early 2010s. This moderation reflects a market rebalancing, where price appreciation has settled into a more sustainable trajectory aligned with economic fundamentals such as wage growth and rental yields.

Affordability preserved: First-time buyers, particularly HDB upgraders, have continued to buy; median house prices have not become so extreme relative to median incomes that the market has fractured. The price-to-income ratio in Singapore remains among the most manageable in developed Asia, allowing younger buyers to enter the market without undue hardship.

Comparison to global peers: Hong Kong, Vancouver, and Sydney have seen much steeper price-to-income ratios despite less stringent cooling measures. In Hong Kong, for example, a property may cost 20–30 times annual median household income; in Vancouver and Sydney, the ratio exceeds 12–15. Singapore’s pragmatic approach has kept the ratio at a more sustainable 8–10 times, making the market more accessible.

Investor activity moderated: The share of property transactions by investors (vs. owner-occupiers) has declined, indicating cooling measures are successfully crowding out speculative demand. This shift is crucial: when investors withdraw, price volatility typically decreases and stability improves.

Market resilience: The market has absorbed multiple rounds of tightening—seven major cooling packages since 2009—without experiencing a crash. This speaks to the underlying strength of Singapore’s economy and the government’s ability to calibrate policy precisely, neither so tight as to stifle the market nor so loose as to permit excess.

In short, cooling measures have succeeded in their core mission: managed, sustainable growth that preserves homeownership as an achievable goal for Singaporeans whilst safeguarding financial stability.

What Might Come Next?

Predicting future cooling measures is speculative, but several potential levers exist if the market overheats again. The government has shown it is willing to adjust policy swiftly when conditions warrant, and the following measures are within the realm of possibility:

Further LTV tightening: LTV could drop below 75% for HDB and 70% for private, forcing larger down payments. This would particularly affect HDB first-time buyers, though offsetting grants could mitigate the impact.

ABSD escalation on entities: Corporate and foreign entity purchases could face rates exceeding 70%, further discouraging institutional investors and offshore funds from treating Singapore residential property as an alternative asset class.

TDSR reduction: The 55% threshold could tighten to 50%, limiting borrowing power even further. This would reduce the quantum of debt banks could extend and force buyers to increase down payments or reduce property search prices.

Extended hold periods: SSD holding could extend beyond four years; MSR wait-out could lengthen beyond 15 months. A 5–7 year SSD period would effectively end short-to-medium-term flipping as an investment strategy.

Targeted HDB measures: Given HDB’s social mission, the government could ring-fence HDB buying further (e.g., longer wait-out periods for private owners, stricter owner-occupancy rules for upgrade purchases).

Differentiated ABSD by property type: Separate ABSD rates for landed (houses, land) vs. non-landed (condos, ECs) to focus cooling where prices are most extreme. Landed property prices have historically appreciated faster than condominiums, making them a natural target for stricter cooling.

Interest-rate floor adjustments: The MAS could raise the notional interest-rate floor used in TDSR/MSR calculations from the current 4% (private) to 4.5% or 5%, making loans seem more expensive during qualification, thereby reducing lending volumes.

These possibilities are illustrative, not predictions. The Government has consistently emphasised that cooling measures are reviewed against prevailing market conditions, and that any further recalibration — tightening or easing — will be driven by the data. Buyers and sellers should plan on the framework in force today and monitor MAS, URA, MND, IRAS and HDB announcements for updates.

Frequently Asked Questions

1. What’s the difference between ABSD and SSD?

ABSD (Additional Buyer’s Stamp Duty) is a tax paid by the buyer when purchasing a property (typically 2nd or 3rd+). It’s calibrated by buyer type (citizen, PR, foreigner, entity) and aims to dampen investment demand. SSD (Seller’s Stamp Duty) is a tax paid by the seller when selling within a holding period; it discourages flipping. Both reduce demand, but ABSD targets entry; SSD targets exit.

2. Are cooling measures permanent?

No. All cooling measures are policy tools, not constitutional laws. They can be eased or tightened depending on market conditions. For example, SSD was partially eased in March 2017, and TDSR has been adjusted twice (60% → 55%). The Government reviews the framework regularly against market conditions.

3. Can you appeal a cooling-measure penalty (e.g., SSD)?

No. Cooling measures are statutory levies applied uniformly. Once a property is sold within the SSD holding period, the duty is automatically calculated and due. There is no appeal mechanism, though you can seek professional tax advice if you believe your classification is incorrect. Early repayment of SSD (before expiry) is not available.

4. How do cooling measures affect HDB owners?

Cooling measures affect HDB owners primarily when upgrading (selling to buy private) or downgrading (selling private to buy HDB resale). HDB owners upgrading to private face ABSD. Private owners downgrading to HDB resale face a 15-month wait-out period and stricter MSR limits (30% vs. TDSR 55%). Cooling measures have also reduced HDB LTV to 75%, requiring larger down payments.

5. Do foreigners face the toughest measures?

Yes, unambiguously. Foreigners pay 60% ABSD (vs. 20% for SC 2nd property), and are excluded from some HDB categories altogether. The government’s policy framework explicitly prioritises owner-occupation for citizens and PRs over foreign investment. A foreigner buying a S$2M property pays S$1.2M in ABSD alone, making foreign residential investment significantly less attractive.

6. Will the government remove cooling measures if the market drops?

Possibly, but history suggests a “last in, first out” approach. When prices fell during COVID-19, cooling measures were retained (some were even tightened). The government views cooling measures as structural policy, not cyclical. However, if prices fell sharply and sustained (e.g., 15% decline year-on-year), measures like ABSD could be eased to stimulate demand. The government’s current stance (April 2026) is that stabilisation is preferable to rollback, unless emergency conditions warrant it.

This guide is for general information only and does not constitute legal, tax, or financial advice. Cooling measures are subject to change at any time by the relevant authorities (MAS, URA, IRAS, HDB). Interest rates, property values, and policy frameworks are subject to modification. Before entering into any property transaction, verify the current ABSD rates, SSD holding periods, LTV limits, TDSR/MSR thresholds, and any other applicable cooling measures with the Inland Revenue Authority of Singapore (IRAS), the Housing and Development Board (HDB), or the Monetary Authority of Singapore (MAS). Consult a licensed conveyancing lawyer and a qualified mortgage specialist or financial adviser to assess your personal circumstances and borrowing capacity. LovelyHomes.com.sg takes no responsibility for losses or liabilities arising from reliance on this article.

ABSD Singapore — short for Additional Buyer’s Stamp Duty — is the single largest upfront cost most buyers face when purchasing a second (or third, or fourth) residential property in Singapore. If you are buying as a foreigner, ABSD can add 60% of the purchase price to your cost. If you are a Singapore Citizen buying your second property, that figure is 20%. Get this number wrong in your budgeting, and you can very quickly wipe out years of planning.

This guide walks you through exactly how ABSD works in 2026 — who pays, how much, how it is calculated, what remissions are available, and the legitimate strategies property buyers use to manage it. All figures reflect the Government’s 27 April 2023 cooling measures, which remain the applicable framework. For the latest rates, always check the IRAS Additional Buyer’s Stamp Duty page.

Quick Answer — ABSD at a glance

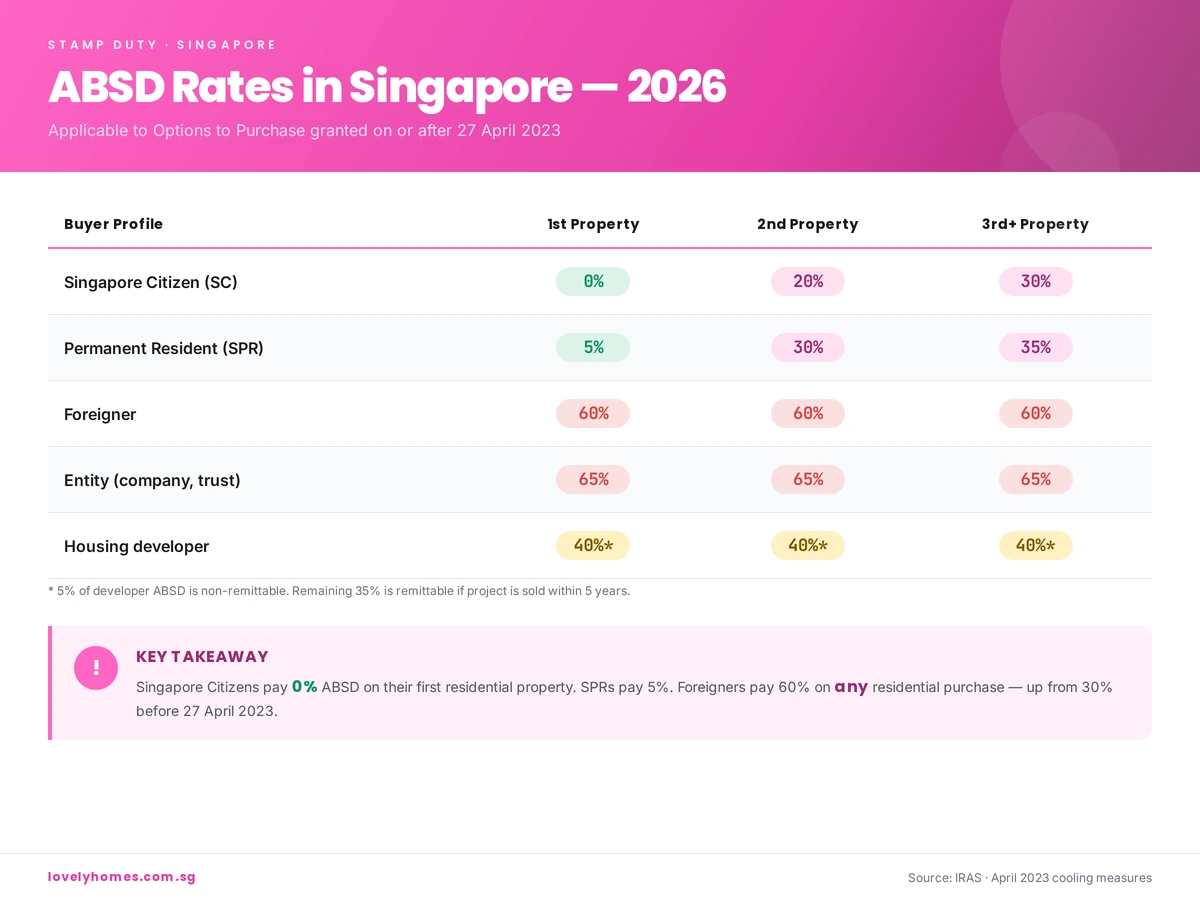

Singapore Citizens: 0% on 1st property, 20% on 2nd, 30% on 3rd+

Singapore PRs: 5% / 30% / 35%

Foreigners: 60% on any residential property

Companies, trusts and other entities: 65%

ABSD is payable within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

What is ABSD and Why Does It Exist?

ABSD is a transaction tax levied on the buyer when acquiring a residential property in Singapore. It sits on top of the regular Buyer’s Stamp Duty (BSD) that every buyer pays. Where BSD is progressive and maxes out at 6% for the portion of price above S$3 million, ABSD is a flat rate applied to the entire purchase price or market value (whichever is higher).

The tax was introduced in December 2011 as part of the Government’s suite of cooling measures — the tools Singapore uses to moderate speculative demand, manage affordability for owner-occupiers, and prevent the kind of runaway price inflation seen in other global cities. Because it targets second-and-subsequent-property buyers and non-citizens disproportionately, ABSD is the single most powerful lever in the cooling-measures toolbox. You can read more about the broader framework in our Property Cooling Measures section.

ABSD Rates in Singapore (2026)

The table below sets out the ABSD rates currently in force. Rates apply based on the profile of the buyer at the time the Option to Purchase (OTP) is granted.

ABSD rates by buyer profile — applicable to OTPs granted on or after 27 April 2023.

Buyer Profile

1st Residential Property

2nd Residential Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (non-PR individual)

60%

60%

60%

Entity (e.g. company, trustee for a trust)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of a developer’s ABSD is non-remittable. The remaining 35% is remittable subject to conditions, including selling all units in a qualifying project within five years.

How ABSD is Calculated — A Worked Example

ABSD is applied to the higher of the purchase price or the market value of the property. It is not charged on a tiered basis — the full rate applies to the entire amount.

Example: A Singapore Citizen couple already owns their first home (a 4-room HDB flat). They decide to buy a S$2,000,000 resale condominium in District 15 as an upgrader investment. ABSD on the second property for a Singapore Citizen is 20%.

Purchase price: S$2,000,000

ABSD (20%): S$400,000

BSD (progressive, on S$2m): approximately S$64,600

Total stamp duty payable: S$464,600

That S$400,000 ABSD alone would consume most of the typical upgrader’s CPF and cash reserves. This is why many Singaporean couples take the ‘sell first, buy second’ upgrade route — selling the existing HDB or condo before buying the next home — which we cover later in this guide.

Who Pays ABSD? Exemptions and Special Cases

ABSD applies when you purchase an additional residential property. Commercial property, industrial property, and pure-land parcels are not within its scope. A property is counted toward your “property count” if:

You hold the title as a sole owner, joint tenant, or tenant-in-common;

You are a beneficial owner via a trust;

You are a beneficiary of an estate that holds residential property.

Properties not counted include: properties you merely reside in but do not own (e.g. as a tenant), inherited shares in a deceased estate within the administration period, and certain industrial/commercial units.

Executive Condominiums (ECs)

For new ECs bought directly from the developer during the minimum occupation period of the scheme, ABSD is not triggered because the buyer must commit to an owner-occupier arrangement. ABSD rules apply normally if an EC is purchased on the resale market after its 5-year MOP and 10-year privatisation milestones.

Free Trade Agreement (FTA) Nationals

Citizens and Permanent Residents of countries with which Singapore has an FTA extending National Treatment on stamp duty — namely Iceland, Liechtenstein, Norway, Switzerland, and United States citizens — are accorded the same ABSD treatment as Singapore Citizens. An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%.

ABSD Remission Schemes — How to Get Some (or All) of It Back

Several remission schemes let qualifying buyers claim back part or all of the ABSD they initially pay. The big three to know are:

1. Married Couple Remission (Sale of First Residential Property)

If a Singapore Citizen (or mixed SC & SPR, SC & foreigner) couple buys a replacement home before selling their existing one, they can apply for ABSD remission provided they sell the first property within six months of the later of (a) the date of purchase of the replacement property, or (b) the TOP/CSC date if buying an uncompleted unit. This is effectively a “grace period” that allows upgraders to move without double-paying ABSD.

2. Mixed-Nationality Married Couples

An SC spouse married to a foreigner buying a matrimonial home jointly can enjoy SC rates (rather than foreigner rates) if the property will be used as their matrimonial home and conditions are met. Again, for a first joint home this means 0% ABSD.

3. Developer ABSD Remission

Licensed housing developers pay 40% ABSD upfront (5% non-remittable, 35% remittable) on land purchased for residential development. The 35% is remittable upon meeting development and sales conditions — typically completing the project and selling all units within 5 years.

Remissions must be applied for within strict timeframes (usually 14 days of the triggering event). We strongly recommend engaging a conveyancing lawyer who is experienced in stamp-duty remission applications before signing any OTP where remission will be relied upon.

ABSD vs BSD: What is the Difference?

Every property purchase in Singapore attracts Buyer’s Stamp Duty (BSD), which is a progressive tax on the purchase price:

1% on the first S$180,000

2% on the next S$180,000

3% on the next S$640,000

4% on the next S$500,000

5% on the next S$1,500,000

6% on the portion above S$3,000,000 (residential only)

BSD applies to every buyer; ABSD is the additional layer that may or may not apply depending on your citizenship status and property count. BSD and ABSD are payable together, within 14 days of signing the OTP.

The History of ABSD in Singapore (2011–2026)

Understanding how we arrived at today’s ABSD rates helps you anticipate where the Government may go next. The key milestones:

December 2011: ABSD introduced. Foreigners paid 10%; entities 10%; SPRs 3% on 2nd property; SCs 3% on 3rd+.

January 2013: First major hike. Foreigners to 15%, entities 15%, SPRs 5%/10%, SCs 7%/10% on 2nd/3rd.

July 2018: Rates raised again amid a reflating market. Foreigners to 20%, entities to 25%.

December 2021: Another round. Foreigners to 30%, entities to 35%, SPR 2nd property to 25%, SC 2nd to 17% / 3rd to 25%.

April 2023: The current regime. Foreigners doubled to 60%, entities to 65%, SPR 2nd to 30%, SC 2nd to 20%.

Each tightening has coincided with a period of accelerating private-residential price growth. For a full chronology including LTV, SSD and TDSR changes, see our comprehensive Property Cooling Measures archive.

How to Legally Minimise Your ABSD Bill

ABSD is not optional, but there are a handful of legitimate strategies buyers use to reduce the amount payable or to avoid triggering higher rates:

Sell first, then buy. For couples upgrading, timing the sale of your existing HDB or condo before the purchase of the next means you never hold two properties simultaneously and therefore pay 0% ABSD on the new first home (as an SC).

Use the matrimonial home remission. A mixed SC–foreigner couple buying their matrimonial home jointly enjoys SC rates if structured correctly.

Decouple responsibly. Where one spouse transfers their share of an existing property to the other, only the transferring spouse is freed to buy a second property as a “first” purchase. Decoupling has legal, CPF refund, and mortgage implications — always take specialist advice first.

Consider commercial or industrial property instead. Commercial and industrial properties do not attract ABSD. They have their own financing, GST, and tax considerations — but for investors focused on yield, they are worth analysing. See our Property Investment section for how commercial yields compare with residential.

Look offshore for second and third properties. Singaporeans investing in Malaysia (JB/Iskandar), Thailand, the UK, Australia, or Japan pay no ABSD to the Singapore Government for those purchases. Each destination has its own foreign-buyer regime, which we cover in our Foreign Property Investment guide.

Time your citizenship/PR application carefully. For families where PR or citizenship is in progress, the ABSD profile at the date the OTP is granted determines the rate. Moving the OTP date by a few weeks can, in edge cases, change the applicable rate by 15–25 percentage points.

Frequently Asked Questions

Is ABSD payable on the land value or the built-up value?

ABSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. For new launches, this is typically the purchase price; for resale, IRAS may apply an independent market valuation.

When exactly is ABSD due?

Within 14 days from the date of the document triggering the duty — usually the signing of the Option to Purchase (for resale) or the Sale & Purchase Agreement (for new launches). Late payment attracts penalties.

Can CPF be used to pay ABSD?

No. ABSD (like BSD) cannot be paid from CPF directly at the point of purchase — it must be paid in cash. You can, however, apply for CPF reimbursement after the stamping is complete, drawing from your Ordinary Account against the purchase price.

Do I pay ABSD if I inherit a property?

No. A property acquired by way of inheritance is not a purchase and does not attract ABSD on the transfer itself. However, an inherited property does count toward your property count for future purchases.

I already own a commercial shophouse. Do I pay ABSD on my residential condo?

The residential-only count means commercial and industrial holdings are not included in your ABSD property count. If you are a Singapore Citizen buying your first residential property while owning commercial real estate, you still pay 0% ABSD.

How does ABSD affect an Executive Condominium purchase?

Buying a new EC from the developer under the EC scheme does not attract ABSD during the initial owner-occupation period. Once an EC is privatised (10 years after TOP) and traded on the open market, normal ABSD rules apply.

What to Do Next

ABSD changes how much house you can afford, how you time an upgrade, and sometimes whether a purchase makes sense at all. If you are weighing your options right now, we suggest three next steps:

If you are an upgrader, study our Upgrader Guide — the sequencing question (sell first vs buy first) is the single biggest lever for managing ABSD.

Review current market conditions in our Property News and Property Trends sections — if further cooling measures are telegraphed, timing your OTP becomes critical.

Looking at a specific development? Our detailed condo reviews — including One Marina Gardens, Arina East Residences, and our Aurea vs Chuan Park showdown — include the full ABSD-inclusive cost breakdown for various buyer profiles, so you can see the true entry cost before committing.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. ABSD rates and remission rules change over time. Always verify the current position on the IRAS Stamp Duty page and consult a licensed conveyancing lawyer or tax specialist before acting on any property transaction.

[This article was first posted on daryllum.com on 26 Mar 2025]

You know what I find perplexing? If location is key when it comes to property investment, then why are properties in the core central region getting so little interest from developers and buyers alike? Little when comparing the interest in places like Tampines. Buyers do realise that projects like Parktown Residences are located in Tampines and Tampines is located at the east end of Singapore yup? Was the pricing so impressively attractive that buyers needed to flood the showrooms? Yes it is an integrated development but why do buyers not consider something in the core central region as well?

The highly restrictive Additional Buyers’ Stamp Duties (ABSD) levied on foreign buyers has put the brakes on almost all foreign purchases. I have always maintained that if a foreigner chooses to pay the 60% ABSD, there is something that should be scrutinised. Imagine this, a foreigner purchases an SGD$5 million property. He pays SGD$3 million as ABSD. His total acquisition cost, including the usual Buyers’ Stamp Duty and other fees amount more than SGD$8 million. As a foreigner with more than SGD$8 million, he would have choices galore. He has access to properties all around the globe. If that individual can purchase properties from all over the world, what is his motivation to pay more than SGD$8 million for something that is perhaps valued at around SGD$5 million? This means that the moment he purchases the property, the asset that he is holding is worth much less than what he paid for. This, in investing sense, is purely illogical. However, if that individual acquired his monies relatively easily, then he would not mind losing that value. Foreign buyers are almost non-existent. In fact, if I were the authorities, I would question and scrutinise the very few purchases by foreigners. I would want to understand the motivation and purpose for such a purchase. Well, if there were no clear motivation for the buyer to purchase Singapore properties then it would be prudent to scrutinise his source of funds for the property purchase.

So then, foreign property purchases have slowed to a trickle. This perverts the normal demand for Singapore properties. Foreigners would be less motivated by things like familiarity and proximity to other family members. For example, if my family members and I have been living in a certain part of Singapore, say Toa Payoh, then if there is a new property launch in Toa Payoh, I would be more likely to be enticed to make a purchase because I want to live near my family members and also to live in a part of Singapore that I am familiar with. This is why, to me, properties like Chuan Park are selling well as compared to a property like Aurea. There are fewer existing families living around Aurea as compared to Chuan Park. Hence there will be less “familiar” buyers for Aurea. Go to Chuan Park and the typical buyer will be someone who lives or lived around the area. Or has family members living in the area.

One Marina Gardens is a 99-year leasehold development. The total site area is 12,245.10 square meters. The development consists of 937 units spread across two blocks. The two blocks are 30 and 44 storeys. It will also have commercial units like 2 restaurants, 2 shop units and a childcare centre. There will be 445 carpark lots. The expected completion is in 2029.

Where is the development located?

One Marina Gardens is located along Marina Boulevard.

One Marina Gardens Location Map

It is located right next to exit 4 of Marina South MRT Station. Marina South MRT Station is one of the stations on the Thomson East Coast Line. Marina South MRT Station is not yet opened. It is scheduled to open in tandem with developments in this area. I believe that this means that when One Marina Gardens is completed, Marina South MRT Station will be operational. For the purposes of this review, we will refer to TE22 Gardens by the Bay MRT Station rather than TE21 Marina South MRT Station.

Travelling from Gardens by the Bay MRT station to Orchard MRT station would take a total of 13 minutes over 6 stations. The cost is $1.59.

Gardens by the Bay MRT to Orchard MRT

Travelling from Gardens by the Bay MRT station to Raffles Place MRT station would take a total of 5 minutes over 2 stations. The cost is $1.19.

Gardens by the Bay MRT to Raffles Place MRT

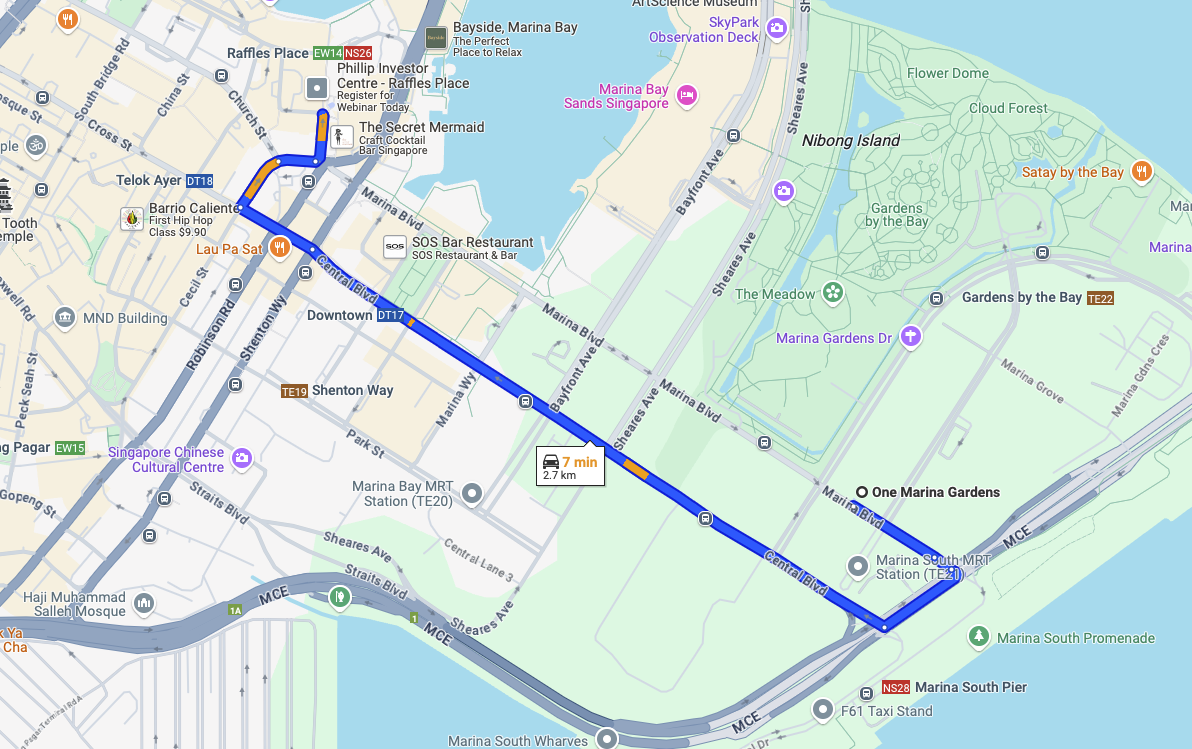

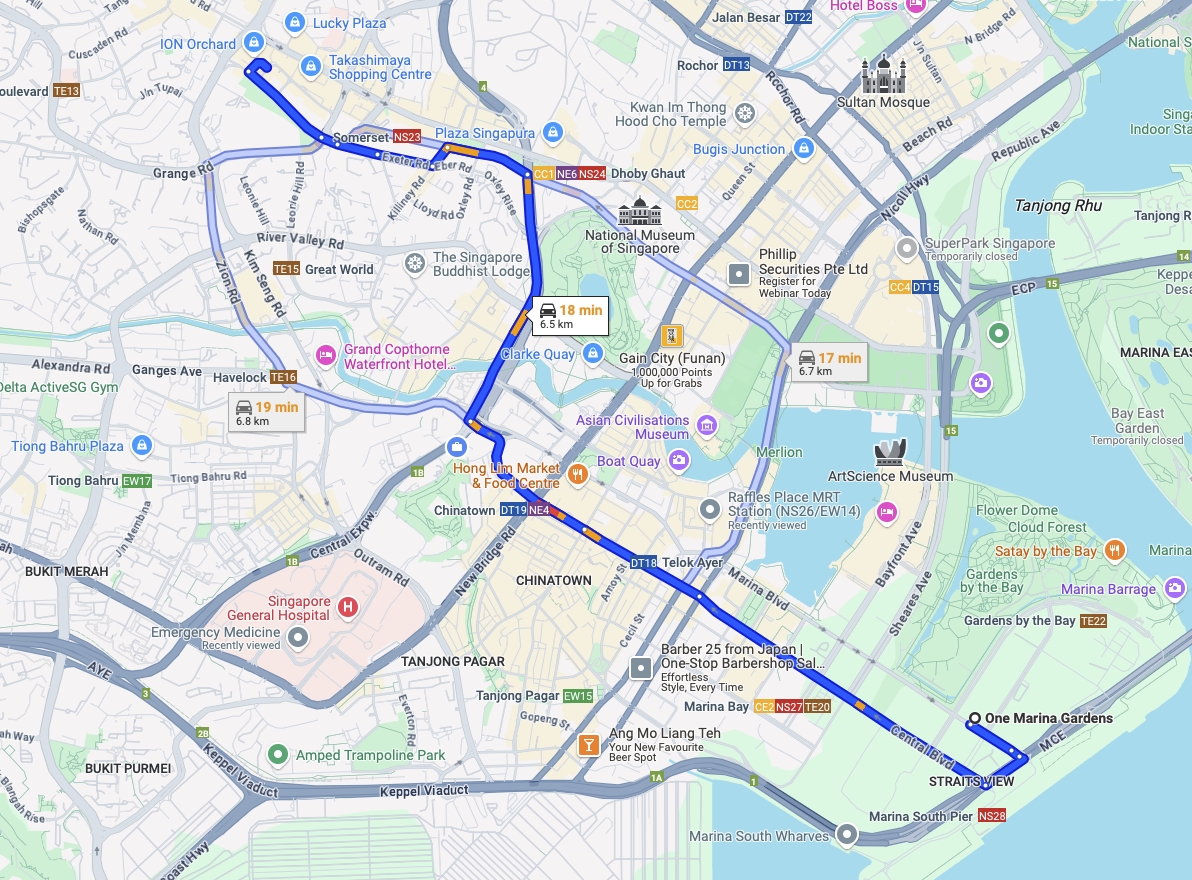

The drive from One Marina Gardens to Raffles Place would take approximately 7 minutes and the distance travelled is about 2.7 kilometres.

The drive from One Marina Gardens to Raffles Place

The drive from One Marina Gardens to Orchard Road would take approximately 18 minutes and the distance travelled is about 6.5 kilometres.

The drive from One Marina Gardens to Orchard Road

One Marina Gardens is located at the fringe of the Marina Bay Financial District. I do not think that residents would drive to Raffles Place. I believe the short train ride would be the most ideal option. As a point of reference, the Google Map query was done in the afternoon at about 4pm. Hence traffic is light. If you are driving during peak hours, do factor in additional travelling time.

Who is this development for?

I genuinely think that if you believe in the concept of catchment areas, then why are you not considering properties in and around the Marina Bay Financial District? Are your tenants not coming from people who work in offices in the area? If so, I do think that if you are looking to purchase for rent, then this is the ideal property for you. I am a person who always focuses on what is around the area. If the area is littered with offices with highly paid employees, then this is a huge plus.

One of the reasons I can offer as to why many Singaporeans do not think this way is because of the ABSD. On multiple properties, ABSD applies. Hence Singaporeans only have one property purchase which is not subject to ABSD. If so, that first property is likely to be a property in a location which they are familiar with. In certain cases where a married couple plans to have two private properties, one under the husband’s name and another one under the wife’s name, then this is an ideal second property.

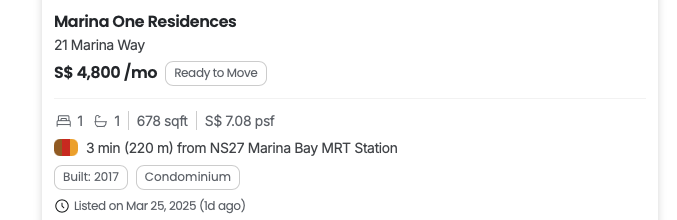

Marina One Residences One Bedroom for rent

A simple search on PropertyGuru would show that a 1 bedroom condominium at Marina One Residences is going for about $4,800 a month.

According to a recent Business Times article, the 1 bedroom units at One Marina Gardens starts at SGD$1.16 million.

Working out the yield based on an assumed rent of $4,800 a month or $57,600 per annum,

$57,600 / $1,160,000 = 4.97% per annum

Of course there are a few assumptions when it comes to my calculation. I am making the assumption that the 1 bedroom unit at One Marina Gardens can be rented out for $4,800 in about four years time. I believe my assumption is reasonable because it is likely that rents are likely to increase in the next four years, albeit at a much slower pace. The $4,800 is based off the current rent in an older development. Secondly, the purchase price is based on the lowest priced unit. However, if you factor in a higher purchase price, you would still receive a yield of more than 4%.

Ever heard the notion that yields tend to be lower in the city centre? Well not necessarily so. Especially when current property prices in the Outside Central Region (OCR) are so close to the prices in the Core Central Region (CCR) and Rest of Central Region (RCR). Try going to Chuan Park and getting a 1 bedder for less than SGD$1 million. I do not think it is possible. Then look at the prices at developments in areas that are so much closer to Singapore’s Central Business District (CBD).

Hence I firmly believe that if I were looking for a property with good rentability, One Marina Gardens is something I would look at.

The selling points of the development

Rentability and closeness to the MRT station and Singapore’s CBD. If location is the prime determinant of how much one should pay for a certain property, is the market making a mistake in looking away from developments in the Marina Bay Area?

Oh yes, heard of the Marina Bay Development Plan? The Greater Southern Waterfront?

If you need more confirmation that there will be developments in the area, this is the URA Master Plan. The reddish pink areas where One Marina Gardens sits on are zoned Residential with Commercial at 1st storey. Those in white are White sites. It is clear that this is an area slated for future development. There will be HDB flats built in this area as well. It was announced in 2023 that more homes are planned in central locations to let more people enjoy city living. Marina South is one of those areas stated. With HDB flats in the vicinity, the usual amenities that are associated with HDB neighbourhoods are likely to also follow suit. Hence, if you do not have a food centre or supermarkets in the vicinity currently, if HDB flats are built here, then all these conveniences should make their way to this neighbourhood.

URA Master Plan

Possible bad points of the development

There is another plot of land slated for development right next to One Marina Gardens. This would block, perhaps partially, the sea view of units facing the sea. However, it is likely that there will be many new developments in the area so having an unblocked view would not be a permanent thing.

One Marina Gardens

Pricing 4/5

Prices start from $1.15 million or about SGD$2,762 psf. Yes you can get a Marina One Residences unit for $1,993 psf but then for some reason there is also an outlier that transacted at $2,522 psf. The average psf for transactions within the last 1 year is $2,112. Assuming an average price of about $2,900 psf, One Marina Gardens is going for a 37% premium over Marina One Residences. Of course you are getting a new lease and this is in an area with a lot of new developments. Hence you will need to factor this into the premium that you are paying.

Marina One Residences Past Transactions

Location 4.5/5

I believe this area is going to be filled with amenities as private developments as well as HDB developments start to fill the area. One Marina Gardens is the closest you can get to the Marina South MRT Station. The thing about the URA is that once it has announced developments in the area, it is most certainly going to happen. I believe in time to come this area is going to develop into an extremely desirable area.

If there were no ABSD on purchases beyond a Singaporean’s first property, I would seriously consider a property like One Marina Gardens.