The HDB upgrader guide Singapore 2026 is your complete, step-by-step resource for navigating the most financially significant move many Singaporeans will ever make: selling your Housing Development Board flat and purchasing a private condominium. Whether you are a Singapore Citizen approaching Minimum Occupation Period, or a permanent resident re-evaluating your property portfolio, understanding the full financial, regulatory, and timing picture is essential before you commit to either transaction.

Quick Answer — HDB Upgrade at a Glance

You must meet a Minimum Occupation Period (MOP) of 5 years before selling your HDB flat (resale) or renting it out entirely

Singapore Citizens buying a private condo while retaining their HDB pay 20% ABSD on the private property purchase

The sell-first strategy eliminates ABSD and is used by the majority of upgraders; the buy-first strategy preserves housing continuity but incurs ABSD upfront

Minimum cash component for a private condo: 5% of purchase price (beyond what CPF can cover)

Your Total Debt Servicing Ratio (TDSR) must not exceed 55% of gross monthly income on all loans combined

CPF Ordinary Account savings used for the HDB must be refunded with accrued interest of 2.5% per annum upon sale

Full upgrade process (sell HDB + buy private): 7–9 months on a sell-first strategy; legal completion to collect keys adds 3–5 months for new launches

A Singapore Citizen household with S$800K HDB equity upgrading to a S$1.5M condo typically needs S$350K–$420K in additional cash/CPF

What Is the HDB-to-Private Upgrade Path?

Singapore’s dual-tier housing market — public HDB flats and private residential properties — creates a well-trodden upgrade path that the Housing Development Board and Urban Redevelopment Authority have both shaped through policy. An HDB flat is built on land sold to the HDB by the State under a 99-year lease; the HDB flat grant system, CPF usage rules, and MOP together form a structured subsidy framework designed to support first-time homeownership. The private condominium market, regulated separately by the URA, operates without the same direct subsidies, but also without income ceilings, nationality restrictions (for citizens and PRs), or MOP constraints once purchased.

The “HDB upgrade” is the act of monetising the subsidised first-home equity — essentially converting the benefit of below-market pricing and CPF grants into cash proceeds — and reinvesting those proceeds into the private market. The CPF Housing Grant for resale HDB flats, administered by the Housing Development Board, can total up to S$80,000 for eligible first-time buyer households; this grant accrues interest at 2.5% per annum and must be returned to CPF upon sale. Upgraders therefore need to account for this accrued interest deduction before calculating usable equity.

MOP: When Can You Sell?

The Minimum Occupation Period is the single most important gating rule. Under HDB regulations, resale HDB flat owners must physically occupy the flat for five years from the date of possession (for resale) or five years from the date of key collection (for new BTO flats purchased directly from the HDB). During the MOP you cannot sell your flat on the open market, rent out the entire flat, or own any private residential property in Singapore.

The five-year MOP was first introduced in 2010 and has remained stable since. For Prime Location Public Housing (PLH) flats announced from October 2021, the MOP is 10 years — a significant constraint for buyers in mature estates like Bishan, Queenstown, or the Pearl’s Hill development announced by MND in March 2026. Always verify the applicable MOP from your HDB letter of offer.

ABSD and the Simultaneous-Ownership Question

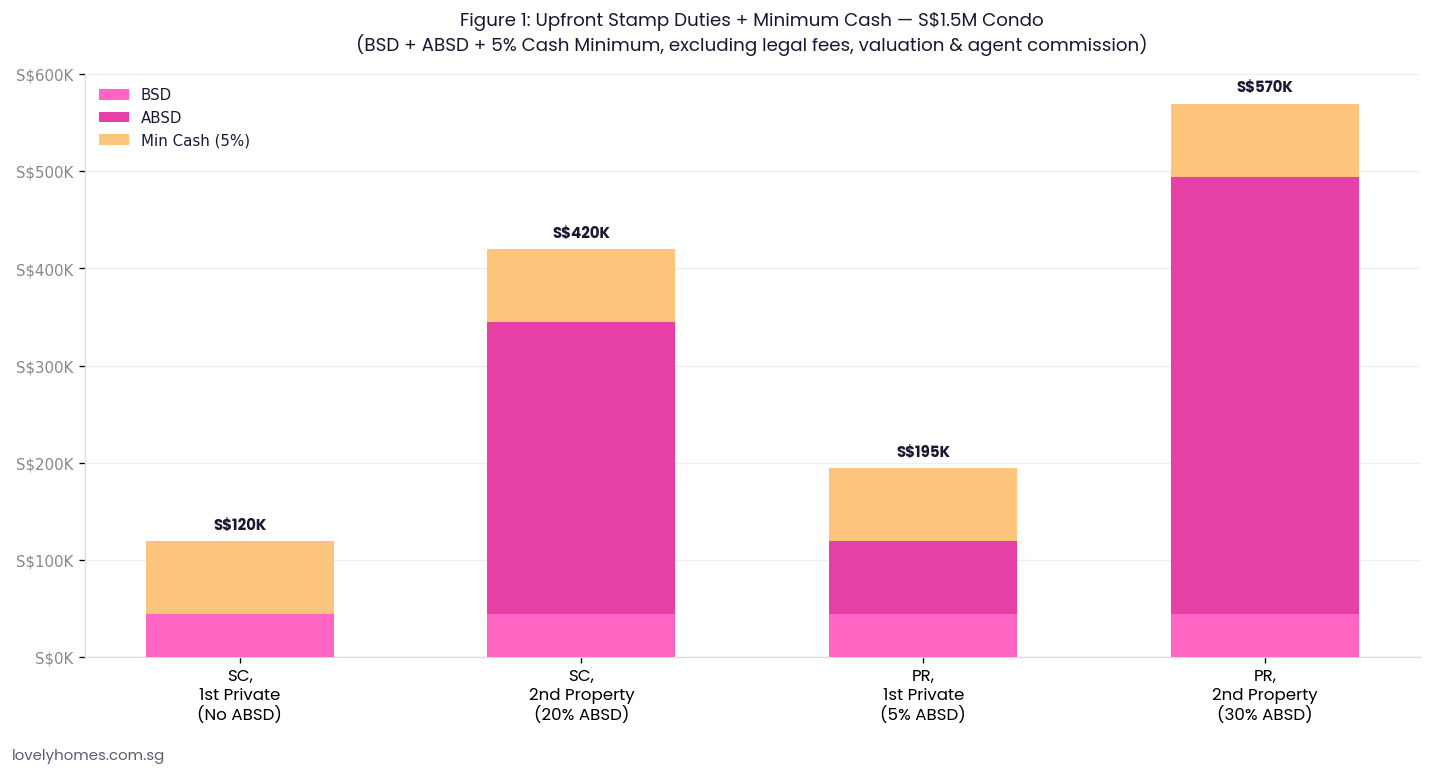

The single most expensive decision in the upgrade process is whether to sell your HDB flat before or after buying the private property. The difference is the Additional Buyer’s Stamp Duty, which is administered by the Inland Revenue Authority of Singapore (IRAS).

Figure 1: Upfront stamp duties + minimum cash for a S$1.5M private condo purchase by buyer profile. ABSD is administered by IRAS and is based on the purchase price or market value, whichever is higher.

At the current rates (effective 27 April 2023), a Singapore Citizen buying a second residential property pays 20% ABSD on the purchase price. On a S$1.5M condominium that is S$300,000 payable within 14 days of exercising the Option to Purchase. Permanent Residents buying their first private residential property pay 5% ABSD; their second attracts 30%.

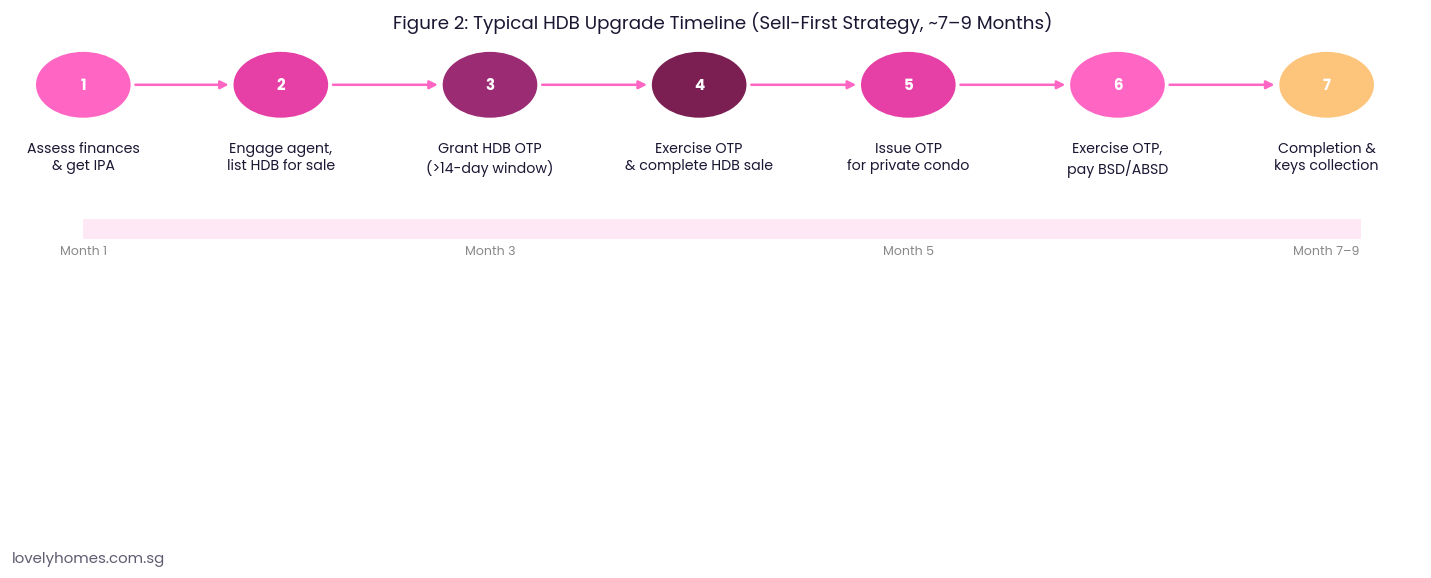

The sell-first strategy means completing the HDB sale (and receiving the full proceeds) before exercising the OTP for the private property. As long as no private residential property is in your name at the point of exercising the OTP, the ABSD charge is 0% for a Singapore Citizen’s first private purchase. This is the financially dominant path for the majority of HDB upgraders and accounts for the bulk of upgrade transactions recorded in URA caveats each year. The downside is an interim period — typically 1–4 months — between HDB completion and private condo collection, during which the family must rent or stay with relatives.

The buy-first strategy preserves residential continuity and is preferred by households with school-age children needing school proximity, or families who cannot face temporary displacement. However, ABSD is payable in full at OTP exercise. IRAS does offer a Remission Scheme for Married Couples: if at least one buyer is a Singapore Citizen and the couple sells the first property within six months of the private purchase date (resale) or key collection date (new launch), IRAS will refund the ABSD on the second property. The refund is not automatic — the couple must apply via the IRAS MyTax Portal within the six-month window.

CPF Usage, Accrued Interest, and Usable Equity

Understanding your actual usable equity from the HDB sale requires two deductions many sellers underestimate. First, the outstanding HDB loan balance (typically financed at the CPF Ordinary Account interest rate of 2.6% per annum) or bank loan must be fully repaid upon completion. Second, all CPF Ordinary Account monies used for the purchase — including the principal plus accrued interest at 2.5% per annum compounded annually — must be refunded to your CPF OA before you receive any cash proceeds. The CPF Board, as custodian of the national retirement savings scheme, enforces this return to ensure retirement adequacy is not eroded by property liquidation.

Practical example: a flat purchased in 2016 for S$500,000 where S$150,000 was used from CPF over nine years will have accrued approximately S$38,000 in interest, meaning S$188,000 must be refunded to CPF. This refunded amount is not lost — it returns to your CPF OA for future use, including towards the new private property — but it does reduce the cash-in-hand proceeds from the HDB sale.

TDSR, MSR, and How Much You Can Borrow

Private property mortgage lending in Singapore is governed by the Total Debt Servicing Ratio framework, administered by the Monetary Authority of Singapore (MAS). Under TDSR rules, the monthly repayment on all outstanding credit facilities — including the new mortgage — must not exceed 55% of the borrower’s gross monthly income. MAS also applies a stress-test rate: variable-rate loans are assessed at the prevailing rate plus a floor, and fixed-rate loans are assessed at the actual fixed rate or 3.5% (whichever is higher, as of the most recent MAS guidance). This means that even if actual SORA-pegged mortgage rates are below 3.5% today, the bank will calculate affordability as if they were 3.5%.

The Mortgage Servicing Ratio — which caps HDB loan repayments at 30% of income — does not apply to private property. However, banks typically retain their own internal MSR-equivalent underwriting floors. For a household with S$12,000 monthly gross income, the maximum monthly debt service across all credit lines is S$6,600 (55%), and after deducting any car loan or personal loan obligations, the remaining capacity determines the maximum mortgage quantum.

Figure 2: The typical sell-first upgrade timeline. Steps 1–4 cover the HDB sale; Steps 5–7 cover the private condo purchase. Total elapsed time is approximately 7–9 months for a resale private condo; add 2–5 years for a new launch.

The Loan-to-Value Framework for Private Property

Under MAS Notice 632, the maximum Loan-to-Value (LTV) ratio for a first housing loan from a financial institution is 75% of the lower of purchase price or market value, provided the loan tenure does not exceed 30 years and the borrower does not exceed 65 years of age at loan maturity. If either condition fails, the LTV drops to 55% or 45%. For upgraders who have fully repaid their HDB loan, the higher 75% LTV applies on the private condo purchase. For those with an outstanding HDB bank loan at the time of application (buy-first strategy), the LTV for the new loan may be reduced to 45%, further increasing the cash component required.

Summary Table: Key Upgrade Figures at a Glance

Parameter

Sell-First (No ABSD)

Buy-First (ABSD Remission)

ABSD (SC, 2nd property)

0% (sold HDB first)

20% upfront; refundable if HDB sold within 6 months

BSD (on S$1.5M)

~S$44,600 (both strategies)

~S$44,600

Min Cash Required

5% of purchase price

5% + 20% ABSD (cash or financing)

Max LTV

75% (no outstanding loan)

45% (outstanding HDB bank loan retained)

TDSR Limit

55% of gross income

55% of gross income

Typical Timeline

7–9 months (resale condo)

6 months from OTP exercise to sell HDB

CPF OA Accrued Interest

2.5% p.a., must refund to CPF upon HDB sale

Same

Worked Example: The Tans Upgrade from Tampines to Condo

Mr and Mrs Tan are a Singapore Citizen couple in their late thirties. They purchased a Tampines HDB 5-room resale flat in 2019 for S$620,000, using S$180,000 from CPF OA and taking an HDB bank loan for S$440,000 at 2.6% per annum. As of April 2026 — seven years into the loan — their outstanding loan balance is approximately S$360,000, and their CPF refund obligation (principal S$180,000 + accrued interest ~S$33,000) totals S$213,000. The flat is valued at S$750,000 on the open market.

Proceeds calculation (sell-first):

Sale price: S$750,000

Less: outstanding HDB loan repayment: −S$360,000

Less: CPF refund obligation: −S$213,000

Net cash-in-hand: S$177,000

CPF OA balance after refund: S$213,000 (available for new purchase)

New condo purchase at S$1.5M (sell-first, no ABSD):

BSD payable to IRAS: ~S$44,600

ABSD: S$0 (HDB sold first)

5% minimum cash: S$75,000

Loan quantum (75% LTV): S$1,125,000

CPF usable (OA): S$213,000 (can cover remaining 20% − 5% cash = S$225,000; short by ~S$12,000 in CPF — top up from cash or savings)

Combined gross household income for TDSR: S$14,000/month. Monthly mortgage on S$1,125,000 at 3.5% stress rate over 25 years ≈ S$5,630. TDSR = 40.2% — within the 55% cap. The upgrade is financially feasible.

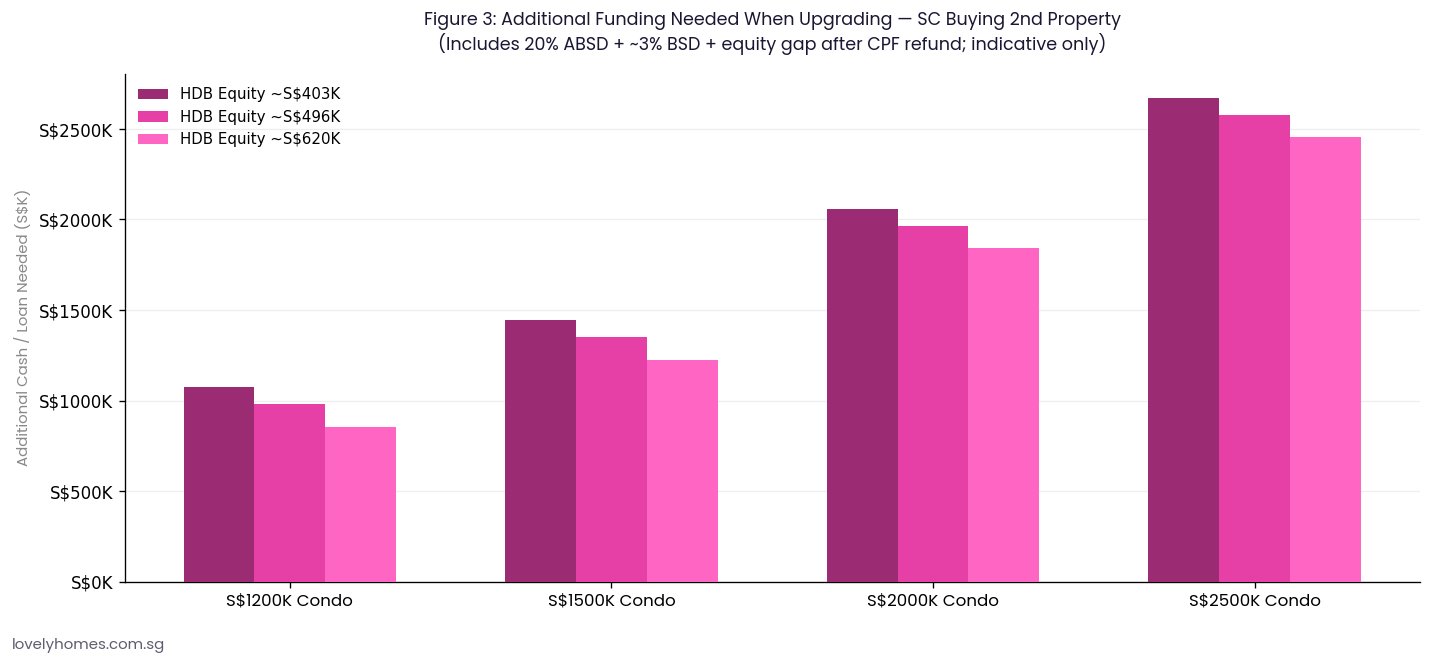

Figure 3: Additional cash or loan funding needed above HDB equity proceeds, by condo price point and usable equity level. All figures assume 20% ABSD (SC 2nd property) and 3% BSD; sell-first scenario removes the ABSD bar entirely.

Why the Upgrade Matters for Singapore Wealth Building

The HDB-to-private upgrade has historically been Singapore’s most reliable individual wealth-building step. URA transaction data consistently shows that private residential prices in the Rest of Central Region (RCR) and Core Central Region (CCR) have outpaced HDB resale price appreciation over 10-year rolling periods, particularly in proximity to MRT interchanges and integrated developments. The 2016–2026 decade saw HDB resale values rise approximately 40–55% in prime estates, while comparable private freehold or 99-year leasehold condos in the same districts appreciated 60–90%.

That said, the upgrade decision is not purely about capital appreciation. Private condo ownership typically involves higher monthly outgoings — management fees, sinking fund contributions, higher property tax under the non-owner-occupier progressive rate (administered by IRAS), and higher mortgage quantum — which compress monthly cash flow for the first 5–10 years. Households should model the cash-flow impact carefully using the actual mortgage rate (SORA + spread, typically 3.4–3.8% as of April 2026 for new floating-rate packages) rather than the stress-test rate.

What Might Come Next: Policy Watch for Upgraders

The current ABSD framework (20% for SC second property) has been in place since April 2023 and shows no sign of immediate revision. MAS and MND have both signalled that macroprudential tools will remain elevated as long as private property prices continue to rise. The URA reported a 0.9% quarter-on-quarter increase in private residential prices in Q1 2026 (full statistics released 25 April 2026), on top of a 0.6% gain in Q4 2025, suggesting sustained upward pressure that gives authorities little reason to ease ABSD. Upgraders planning their move in 2026–2027 should assume the 20% SC ABSD rate persists for the foreseeable future, and should build the sell-first timeline around that assumption.

One area to watch is the Lease Buyback Scheme and CPF use rules for older HDB upgraders (aged 55+), where CPF Retirement Account obligations create a different equity-release calculus. MND’s Committee of Supply 2026 speech hinted at ongoing reviews of CPF Retirement Sum drawdown rules for older owner-occupiers — any loosening could marginally improve equity available for the upgrade among this cohort.

Frequently Asked Questions

Can I buy a private condo before selling my HDB flat?

Yes, but as a Singapore Citizen you will be liable for 20% ABSD on the private condo purchase price, payable within 14 days of exercising the OTP. IRAS provides a Remission Scheme for married couples where at least one is a Singapore Citizen: if you sell your HDB within six months of the private condo’s key collection date (new launch) or OTP exercise date (resale), you may apply to IRAS for a refund of the ABSD paid. The refund is not automatic and requires a formal application within the stipulated window. Note that the 5% cash down payment for the private condo is still required upfront and is not refunded.

What happens to the CPF money I used for my HDB flat?

Upon selling your HDB flat, all CPF Ordinary Account monies used for the purchase — including the initial down payment, subsequent monthly instalments drawn from CPF, and any CPF Housing Grants received — must be refunded to your CPF OA with accrued interest at 2.5% per annum compounded annually. This refunded amount re-enters your CPF OA and can be used immediately for the down payment on your private condo purchase (subject to the CPF Withdrawal Limit and Valuation Limit rules). You do not lose this money — it simply remains within the CPF system rather than being paid out as cash. The CPF Board’s property portal at cpf.gov.sg provides a withdrawal calculator to estimate your exact refund obligation.

How much cash do I actually need to upgrade?

The minimum cash component for any private property purchase in Singapore is 5% of the purchase price. This must be paid in cash — CPF OA funds or bank loans cannot cover this component. For a S$1.5M condominium that is S$75,000. On top of this, you will need cash or CPF for the Buyer’s Stamp Duty (approximately S$44,600 on S$1.5M), legal fees (~S$3,000–$5,000), and a valuation fee (~S$300–$600). If you are using the sell-first strategy and have no ABSD to pay, total cash and CPF outlay to exercise the OTP is approximately S$120,000–$130,000 for a S$1.5M property, with the remainder funded by your mortgage and CPF OA balance.

Can I retain my HDB flat and buy a private condo?

Singapore Citizens and Permanent Residents are not prohibited from simultaneously owning an HDB flat and a private property, but the financial cost is high: as an SC you will pay 20% ABSD on the private property purchase, and as a PR you will pay 30% ABSD on your second property. Additionally, while you own both, the HDB flat remains subject to HDB rules including the restriction on fully subletting the flat until MOP is met (unless you are above 35, divorced, a single with the right to sublet under HDB’s rules, or have specific HDB approval). If you proceed with this dual-ownership approach, you must ensure your TDSR covers both your HDB loan instalments and the new private mortgage simultaneously.

What is the Temporary Housing Solution during the gap between HDB completion and condo collection?

Most sell-first upgraders experience a 1–6 month gap between HDB legal completion and moving into the new private property. The most common approach is a deferred completion arrangement negotiated with the HDB buyer at the point of signing the OTP — you agree to stay in the flat for a fixed rental period (typically 2–3 months at a market rate) after legal completion while your new home is prepared. Alternatively, families rent a unit in the open market at prevailing rates, or stay with extended family. Factoring rental costs of S$2,000–$4,500 per month (depending on unit size and district) into your upgrade budget is essential, particularly for the east and central regions where new launch condo waiting periods can extend to 3–5 years.

Are there specific private condos I cannot buy with my HDB equity?

There are no restrictions on which private condominium an HDB upgrader may purchase. However, two practical constraints often apply. First, Restricted Residential Properties under the Residential Property Act — Good Class Bungalows and most landed housing in Singapore — require Ministerial approval for Singapore Permanent Residents and are unavailable to foreigners entirely; Singapore Citizens may purchase without restriction. Second, if your usable CPF OA balance is below the Valuation Limit (the lower of purchase price and market value), your CPF usage will be capped; you must fund the shortfall from cash. Always check the CPF Board’s updated Valuation Limit rules at cpf.gov.sg before committing to a price point.

What happens if I cannot sell my HDB within the 6-month ABSD remission window?

If you purchased a private condo while retaining your HDB flat (buy-first strategy) and are unable to sell the HDB within six months of the private condo’s key collection date or OTP exercise date, the ABSD remission is forfeited — the 20% ABSD you paid upfront is not refunded. In practice, HDB resale transactions in Singapore typically complete within 8–16 weeks of listing, so the six-month window is generally achievable if you list the HDB promptly after exercising the condo OTP. The risk is greatest when buying a resale condo (shorter completion timeline) while your HDB is slow to sell. If you are uncertain, the sell-first strategy eliminates this risk entirely.

This article is intended for general informational purposes only and does not constitute financial, legal, or property advice. Stamp duty rates, CPF rules, HDB regulations, and MAS lending guidelines are subject to change; always verify current figures directly with the Inland Revenue Authority of Singapore (IRAS), the CPF Board, the Housing Development Board, and the Monetary Authority of Singapore. Consult a licensed property agent, bank mortgage specialist, and solicitor before making any property transaction decision. Nothing in this article should be treated as a solicitation to buy or sell any property.

A Singapore Permanent Resident can buy private condos from day one of PR status, paying 5% ABSD on the first residential purchase (30% on second, 35% on third+). HDB resale flats open to PRs only after 3 years of PR status, and require a qualifying family nucleus. PRs cannot buy new BTO, Plus, Prime or EC flats. Landed property on the mainland needs LDAU approval. If you buy an HDB flat as a PR, MOP and subletting rules mirror citizens.

Permanent Residency fundamentally changes a buyer’s property menu in Singapore — but not overnight. From day one, private property opens. HDB resale still waits three years. New HDB (BTO/Plus/Prime) and new ECs remain closed to PRs regardless of wait time.

This guide maps the PR property timeline, the full 2026 ABSD ladder for PR buyers, the most common mistakes PRs make when disposing of existing property, and the rules PRs should know before taking out a CPF loan. For the foreigner-side equivalent, see our foreigner property guide.

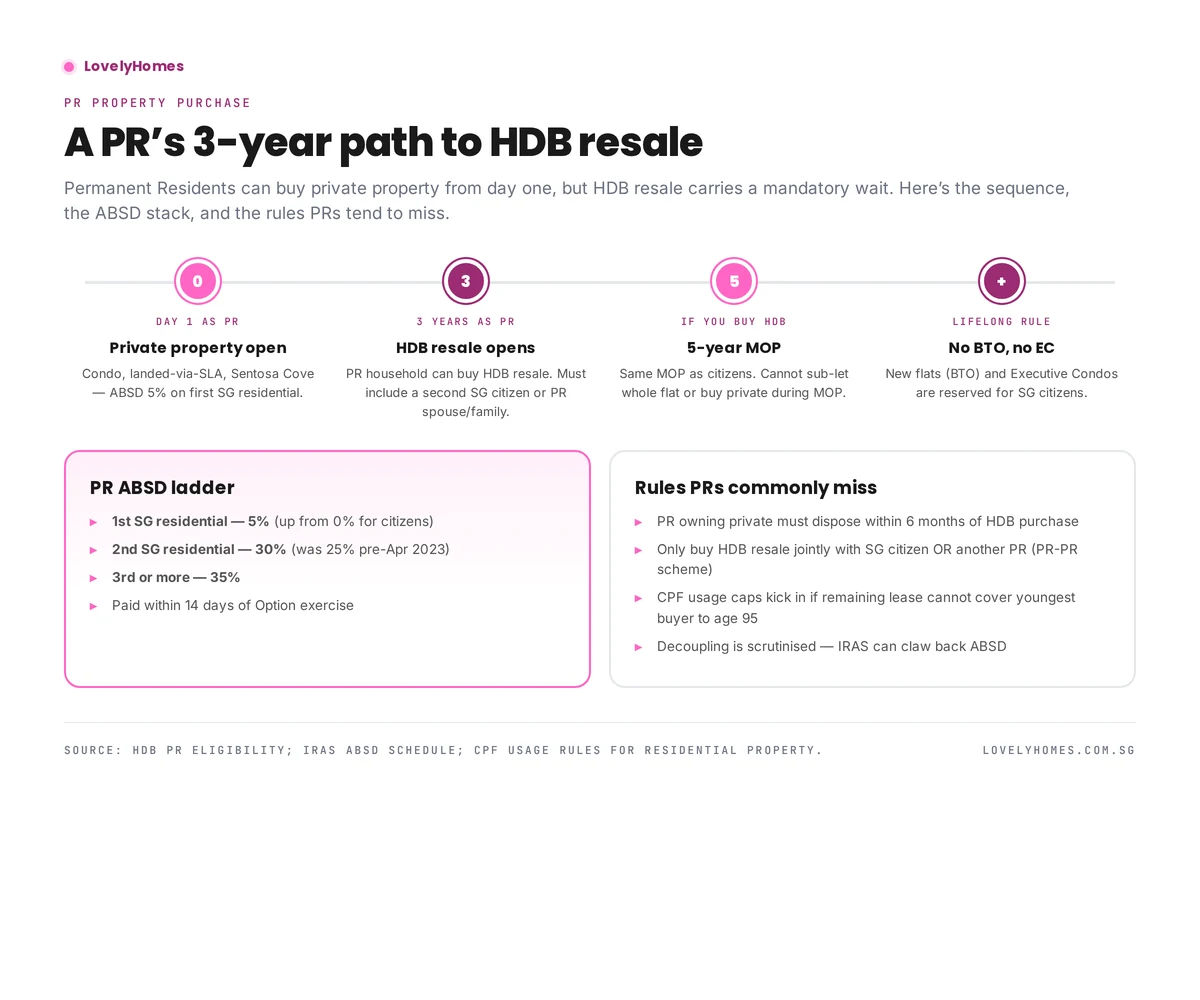

A PR’s 3-year path to HDB resale.

The PR property timeline

Day 1 as PR

Private condo, landed-via-LDAU, and Sentosa Cove landed open immediately. CPF usage opens once the PR has active OA/SA balances. LTV, TDSR and MSR frameworks are identical to citizens.

3 years as PR

HDB resale opens. A PR household must form a qualifying family nucleus — typically a PR applicant with a spouse (PR or SG citizen), or the PR-PR Scheme (both applicants PRs for at least 3 years).

5 years after HDB purchase (if you buy HDB)

Minimum Occupation Period. Same 5-year MOP as citizens. Cannot sub-let the entire flat, cannot buy private residential, cannot sell on the open market. See our MOP rules guide.

Lifetime rule

PRs cannot buy new BTO, new Plus, new Prime or new EC flats. These are reserved for SG citizens with a citizen spouse or fiancé(e). The only HDB route for PRs remains the resale market.

ABSD for PRs — the 2026 ladder

Residential count

ABSD (PR)

Notes

1st SG residential

5%

Up from 0% that citizens pay

2nd SG residential

30%

Raised from 25% in Apr 2023

3rd or more

35%

Raised from 30% in Apr 2023

ABSD is payable within 14 days of Option exercise, on top of BSD. If two PRs buy jointly, the ABSD is calculated on the highest-count profile among the buyers.

The HDB-specific rules PRs must follow

Dispose of private within 6 months

A PR who owns private residential (in Singapore or overseas) must dispose of it within 6 months of the HDB resale completion. This is usually the biggest surprise for incoming PR buyers — overseas apartments count.

CPF usage and the lease rule

CPF can fund the purchase only if remaining lease covers the youngest buyer to age 95. For older HDB stock this is a real constraint — see our CPF for property guide.

No grants (mostly)

Most HDB grants (EHG, Family Grant, Proximity Housing Grant) are reserved for SG-citizen first-timer households. A PR-PR couple does not qualify for EHG. However, a PR with an SG-citizen spouse may qualify under the standard first-timer framework — see our grants guide.

Landed and Sentosa Cove

PRs need LDAU approval under the Residential Property Act to buy landed on the mainland — rarely granted except for long-tenured PRs with strong local ties. Sentosa Cove landed is much more accessible: SLA approval is routinely granted for owner-occupation.

Common PR mistakes

Forgetting the 3-year HDB wait. Newly-minted PRs cannot buy HDB until year 3.

Holding overseas property while buying HDB. HDB will compel disposal within 6 months.

Attempting decoupling to reset ABSD. IRAS actively scrutinises PR decoupling post-2022 and may claw back ABSD. See our decoupling guide.

Using CPF on a lease-short flat. Always check the lease-to-95 calculator first.

Frequently asked questions

Can a PR buy an EC?

Not a brand new EC — that’s citizen-only. A PR can buy a privatised EC (post-10-year MOP + privatisation), because by then it is effectively private property.

Can two PRs buy HDB resale together?

Yes — under the PR-PR Scheme, both must have been PR for at least 3 years. Grants are not available.

What if I become a citizen after buying HDB as a PR?

The flat becomes a citizen-owned flat. Any remaining rules (MOP, subletting) still apply from the purchase date.

Does a PR pay the 60% foreigner ABSD?

No. PR status attracts the PR ladder (5% / 30% / 35%) — not the foreigner flat rate.

This guide is for general information only and is accurate as of April 2026. Singapore property rules, taxes and cooling measures change frequently — always verify current figures with URA, IRAS, HDB or a licensed professional before committing. LovelyHomes is not a financial, legal or tax advisor.

Foreigners in Singapore can buy private condos (subject to ABSD 60% on any residential purchase). They cannot buy HDB flats or new BTO / EC. Landed property on the mainland requires approval from the Land Dealings Approval Unit (LDAU); Sentosa Cove landed is open to foreigners with SLA approval. Five nationalities enjoy citizen-equivalent stamp-duty treatment via Free Trade Agreements: US, Switzerland, Liechtenstein, Iceland, Norway.

Singapore has always segmented residential property access by buyer profile. Since April 2023, the rules on foreign buyers have been the tightest they’ve ever been: 60% ABSD on any residential purchase — a near-doubling from the 30% pre-cooling-measure level.

This guide sets out what foreigners can and cannot buy in 2026, the full stamp-duty stack, landed approval process, and the FTA carve-out that makes five nationalities much better off. If you’re close to PR, read our PR property purchase rules for the 3-year HDB wait path.

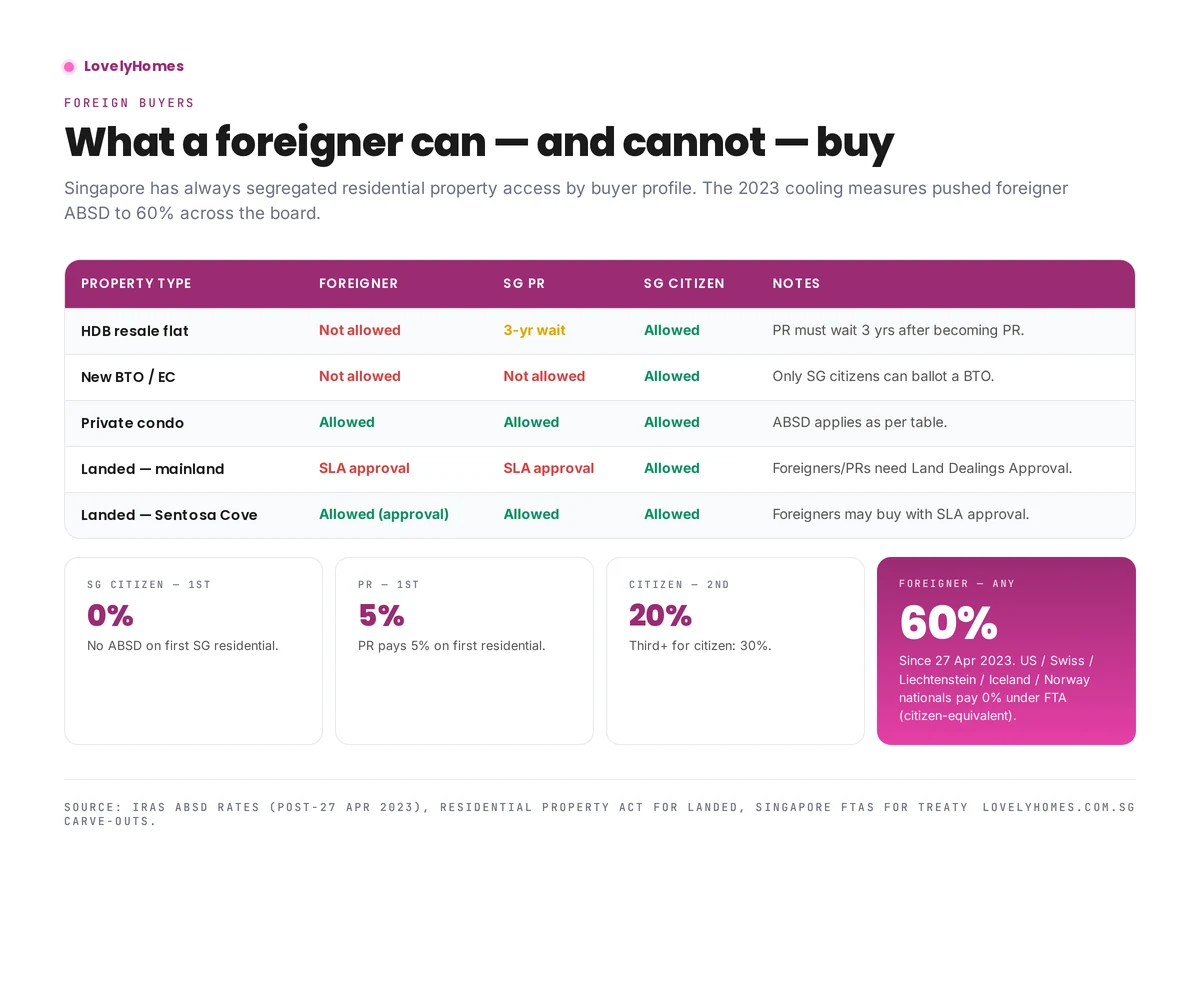

What a foreigner can and cannot buy in Singapore, with 2026 ABSD stack.

What a foreigner can (and cannot) buy

Property type

Foreigner?

Notes

Private condominium (non-landed)

Yes

Freehold or leasehold. ABSD 60%.

Executive Condominium (new, within 10-yr MOP+privatisation)

No

Only SG citizens/PRs can buy new ECs. Foreigners may buy after 10-year privatisation.

HDB resale flat

No

Not a foreign-ownership property.

HDB BTO / Plus / Prime

No

SG citizens only, with spouse requirements.

Landed — mainland Singapore

With approval

Must apply to the Land Dealings Approval Unit (LDAU) under the Residential Property Act. Rare, case by case.

Landed — Sentosa Cove

Yes with SLA approval

The only legal route for foreign ownership of landed in Singapore. Normally granted for owner-occupation.

Commercial / industrial property

Yes

Outside the Residential Property Act. No ABSD but different duty/GST treatment.

ABSD 2026 — the full stack

Buyer profile

1st residential

2nd residential

3rd+ residential

SG Citizen

0%

20%

30%

SG PR

5%

30%

35%

Foreigner

60%

60%

60%

Entity (company, trust)

65%

65%

65%

ABSD sits on top of the standard Buyer’s Stamp Duty (up to 6% at the top band in 2026). For the BSD calculation see our BSD guide.

The FTA citizen-equivalent carve-out

Under Free Trade Agreements, nationals of the following countries are treated as SG citizens for BSD/ABSD on residential property:

United States of America

Switzerland

Liechtenstein

Iceland

Norway

An American citizen on their first SG residential purchase pays 0% ABSD — the same as a Singapore citizen. IRAS requires a written claim at stamping with supporting documents.

Landed property rules

Under the Residential Property Act, landed property is restricted to citizens by default. Foreigners (and sometimes PRs) need approval from the Land Dealings Approval Unit (LDAU) within the Singapore Land Authority. LDAU approval is case by case, weighs economic contribution, and is rarely granted for pure investment purposes.

Sentosa Cove is the exception: LDAU has historically approved foreign applications fairly readily, for owner-occupation, on the 99-year landed stock.

Loans, LTV and CPF

Bank loans

Foreigners can borrow from local and foreign banks subject to the standard TDSR framework (55% of gross income). Maximum LTV is 75% for the first loan, 45% for the second, 35% for the third, unchanged from the resident framework.

CPF

Not applicable — CPF accounts require PR or citizen status. Foreigners fund the 25% down-payment entirely in cash.

Rental income and exit

Rental income is taxable in Singapore under the non-resident flat 24% rate (or progressive if resident). Capital gains on resale are not taxed. Seller’s Stamp Duty applies if the property is sold within three years — see our SSD guide.

Frequently asked questions

Can a foreigner buy a shoebox unit?

Yes — any private non-landed, subject to ABSD 60%. Our shoebox guide explains the trade-offs.

Can a foreigner inherit landed property?

Yes — but the inheritor must obtain LDAU approval to continue holding it. Without approval, they must dispose within a stipulated window.

What if I’m a dual national?

The strictest relevant nationality generally governs. If one passport gives citizen-equivalent treatment (FTA list), IRAS will honour it with documentation.

Can I use a company to avoid the 60% foreigner ABSD?

No — entities attract 65% ABSD (higher than foreigner). IRAS will look through beneficial ownership, and mis-structuring is treated as evasion.

This guide is for general information only and is accurate as of April 2026. Singapore property rules, taxes and cooling measures change frequently — always verify current figures with URA, IRAS, HDB or a licensed professional before committing. LovelyHomes is not a financial, legal or tax advisor.

99-to-1 property ownership is a structure where one party holds a 99% interest in a property and another holds 1%. It came under intense IRAS scrutiny in 2023–2024 when the tax authority identified a specific pattern being used to sidestep Additional Buyer’s Stamp Duty (ABSD). This 2026 guide separates legitimate 99-to-1 arrangements from the red-flag pattern IRAS has been reassessing, and explains how it differs from classic decoupling.

For the official IRAS guidance, see IRAS’s stamp duty page. This article explains the practical picture.

Quick Answer — 99-to-1 in 2026

The structure: one party holds 99% of a property, another holds 1%.

Legitimate uses: loan eligibility, succession planning, investment allocation among co-owners.

The flagged pattern: sole buyer signs OTP, then transfers 1% to another party within weeks.

Clawback: original ABSD + 50% surcharge = 1.5x the amount saved.

Different from decoupling: 99-to-1 happens at original purchase; decoupling happens long after purchase.

The red-flag pattern: a two-stage transfer executed within weeks of the original OTP.

Why 99-to-1 Became Attractive

A standard 99-to-1 structure lets two parties co-own a property with minimal share for one. In isolation this is unremarkable — people use it for tax planning, succession, and pooled investment.

Under Singapore’s ABSD framework, though, it can also function as a loan-qualification tool. Here is the pattern IRAS identified:

A buyer without enough income to qualify for a large bank loan wants to buy a S$2m condo.

A family member with high income but who already owns a property agrees to be named on the loan.

The high-income family member was added as a co-owner at 1%, while the main buyer takes 99%.

The bank was willing to lend based on both incomes because the family member is a co-owner.

But because the family member only owned 1%, the buyer’s main ownership would have qualified for first-timer ABSD treatment.

The effect: a high-income co-owner who already owned property was piggybacking on a first-timer buyer’s ABSD rate. IRAS identified this as a tax-avoidance pattern under the general anti-avoidance provision.

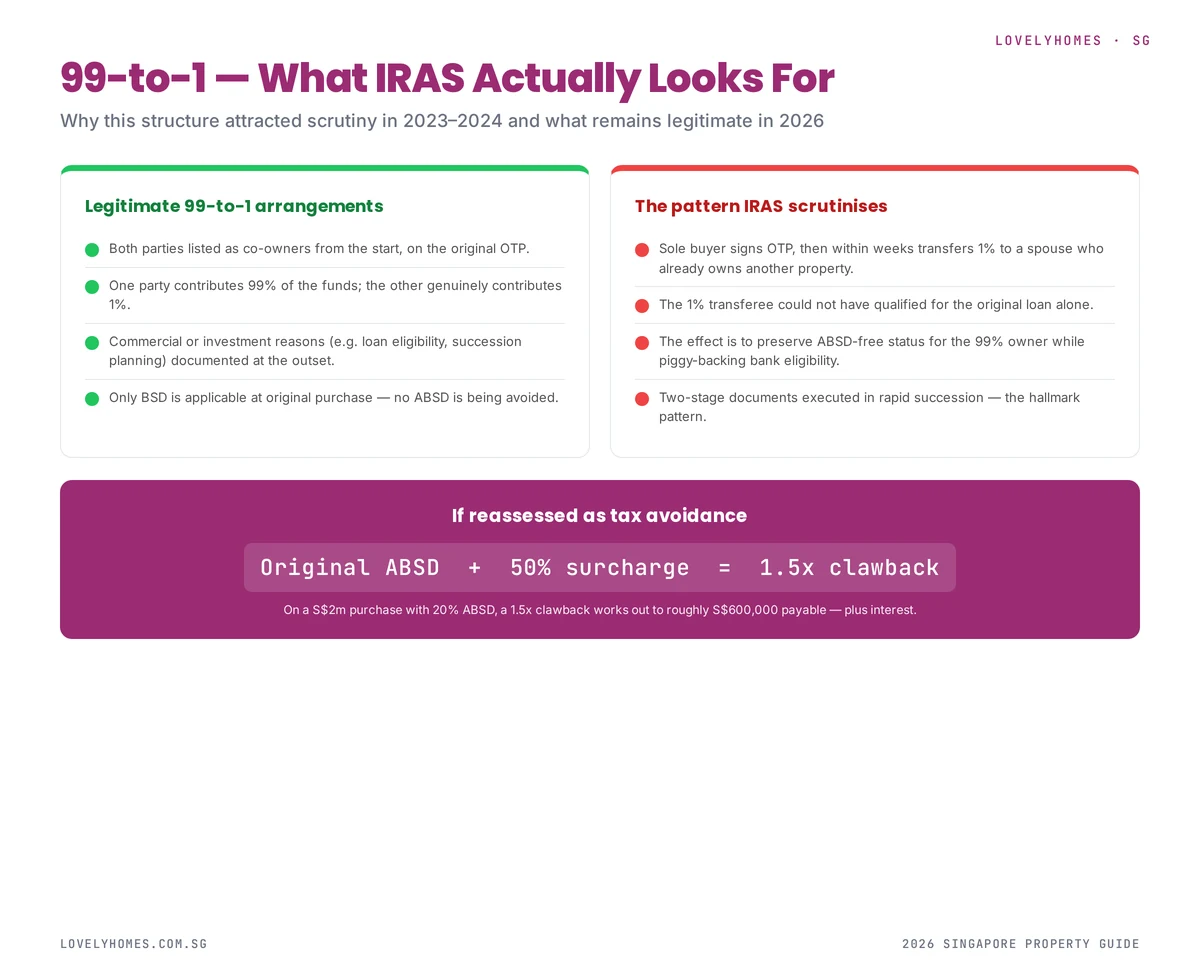

The IRAS Audit Pattern

IRAS has been targeting a specific variant of 99-to-1:

Sole buyer signs the OTP and pays BSD on the full purchase price at first-timer rates.

Within weeks of OTP, a 1% share is transferred to a second party (often a spouse or parent).

The 1% transferee already owns another property — they would have triggered ABSD if they had been on the OTP from day one.

The two-stage structure avoids the ABSD that a direct joint purchase would have incurred.

IRAS reviewed approximately 300–400 such cases in its 2023–2024 sweep. Where the pattern matched, IRAS reassessed the transaction as if the 1% transferee had been a co-owner from the start, and issued an ABSD bill plus surcharge.

The 1.5x Clawback

When IRAS reassesses a 99-to-1 arrangement as tax avoidance, the remedy is:

The full ABSD that would have applied had the transferee been on the OTP from day one

Plus a 50% surcharge on that ABSD

On a S$2m purchase where avoided ABSD was 20% = S$400,000, the clawback works out to S$400,000 + S$200,000 surcharge = S$600,000 payable, plus any interest and legal costs. This is materially more punitive than simply paying the ABSD upfront.

Legitimate 99-to-1 Arrangements

Not every 99-to-1 is a red flag. IRAS has explicitly acknowledged the pattern is legitimate when:

Both parties are co-owners from day one

If both parties sign the original OTP and are named as co-owners in the Sale & Purchase Agreement at the 99:1 split, this is a single transaction and the full ABSD applies on the 1% transferee’s share from the outset. No two-stage manoeuvre, no IRAS issue.

Genuine investment-pooling

Multiple family members pooling funds for an investment property, with each contributing in proportion to their share, is legitimate — provided the shares reflect actual contribution.

Succession planning

A parent retaining 99% and transferring 1% to a child for succession reasons is legitimate, subject to the normal BSD on the 1%. Timing is usually far removed from any property transaction, which is itself a credibility signal.

Commercial co-ownership

Business partners sharing an investment property where one partner provides 99% of the capital and the other provides 1% (perhaps in exchange for operational management) is legitimate under normal commercial logic.

How 99-to-1 Differs from Decoupling

Aspect

99-to-1

Decoupling

Timing

At or near original purchase

Years after purchase, before a new purchase

Ownership after

99:1 split persists

One party becomes sole owner

What it enables

Two parties on loan

Freed spouse buys second home

ABSD mechanism

Avoided on the 99% party

Avoided on the transferring party’s next purchase

IRAS scrutiny

2023–2024 sweep

Reviewed case-by-case

Put simply: decoupling restructures an existing joint ownership; the flagged 99-to-1 pattern manipulates a fresh purchase to sidestep ABSD that would otherwise have applied.

If You Already Have a 99-to-1 Arrangement

If you set up a 99-to-1 before 2023–2024 and have not heard from IRAS, it is almost certainly not in the audit scope. However, if you receive an IRAS query letter:

Do not respond on an informal basis. Engage a tax-focused solicitor immediately.

Compile the documentary evidence for the legitimate commercial purpose of the arrangement.

Be ready to pay the full clawback + surcharge if the pattern matches the flagged type. Appealing is expensive and the success rate has been low.

Consider restructuring if the arrangement is ongoing — though retrospective fixes rarely help once IRAS has engaged.

Current Status in 2026

As of 2026, IRAS continues to monitor two-stage transfers with a 1% residual. The 2023–2024 sweep was not a one-off — it set a precedent that routine transaction audits now look for. Structures that superficially resemble the flagged pattern are far riskier than they were before 2023.

For buyers with legitimate pooling or succession reasons, the arrangement remains viable — but put the co-owner on the original OTP, keep documentation of commercial intent, and avoid the tell-tale timing pattern.

FAQ — 99-to-1 2026

Is 99-to-1 illegal?

No. The ownership structure itself is legal. What is scrutinised is whether the specific arrangement amounts to tax avoidance under the general anti-avoidance provision.

Can I still use 99-to-1 today?

Yes, provided both parties are on the original OTP and the arrangement has a genuine commercial purpose. The risky pattern is the two-stage transfer executed soon after OTP.

How does IRAS identify flagged arrangements?

By cross-referencing stamp duty records with property ownership data. If you owned property before the 1% transfer date, IRAS’s system will flag the transaction for review.

What about 95-to-5 or 90-to-10?

The same anti-avoidance principle applies. IRAS has focused on 99-to-1 because it is the most extreme variant, but the logic extends to any split where a high-income party with existing property takes a minor share to piggyback ABSD rates.

Can I unwind an existing 99-to-1 to avoid IRAS attention?

Possibly, but consulting a tax lawyer before any action is essential. Unwinding can itself trigger stamp duty and CPF complications, and retrospective “fixes” are often viewed as evidence of avoidance intent.

Disclaimer: This article explains a complex and evolving area of Singapore tax law. Specific cases require qualified legal and tax advice. IRAS enforcement practice may shift further.

Property decoupling is the restructuring of joint ownership between spouses so that one of them becomes the sole owner of the existing property, freeing the other to buy a second home at first-timer ABSD rates (0% for SCs, 5% for PRs). In 2026, with ABSD at 20% for SCs on a second property, the savings can be substantial — but HDB flats cannot be decoupled except in divorce, and IRAS scrutinises obviously tax-avoidance arrangements.

This guide walks through how decoupling works mechanically, the costs involved, a worked example, and when IRAS is likely to push back.

Quick Answer — Decoupling at a Glance

Who: Joint owners of a private property (spouses typically).

What: One party transfers their share to the other so that the other becomes sole owner.

Why: The transferring party is now property-free and can buy a second home at first-timer ABSD rates.

HDB flats: Cannot be decoupled except under divorce court order.

IRAS risk: If the arrangement is clearly contrived, IRAS can reassess as tax avoidance.

A worked before/after on a S$1.5m second property — roughly S$300k of ABSD saved for a ~S$50k restructuring cost.

How Decoupling Works Mechanically

There are two legal pathways to decouple a property:

1. Part-purchase

One spouse buys the other spouse’s share via a sale and purchase agreement. The price must be at market value (to satisfy IRAS), and Buyer’s Stamp Duty is paid on the share being transferred. If there is a mortgage, the buying spouse typically refinances the loan in their sole name.

2. Transfer-of-ownership

Less common and typically used only in genuine gift scenarios or divorce. The share is transferred via a Deed of Transfer. Stamp duty still applies based on the market value of the share.

The common pathway is Part-purchase, because it creates a clear arms-length commercial record (helpful if IRAS later asks questions).

Costs of Decoupling

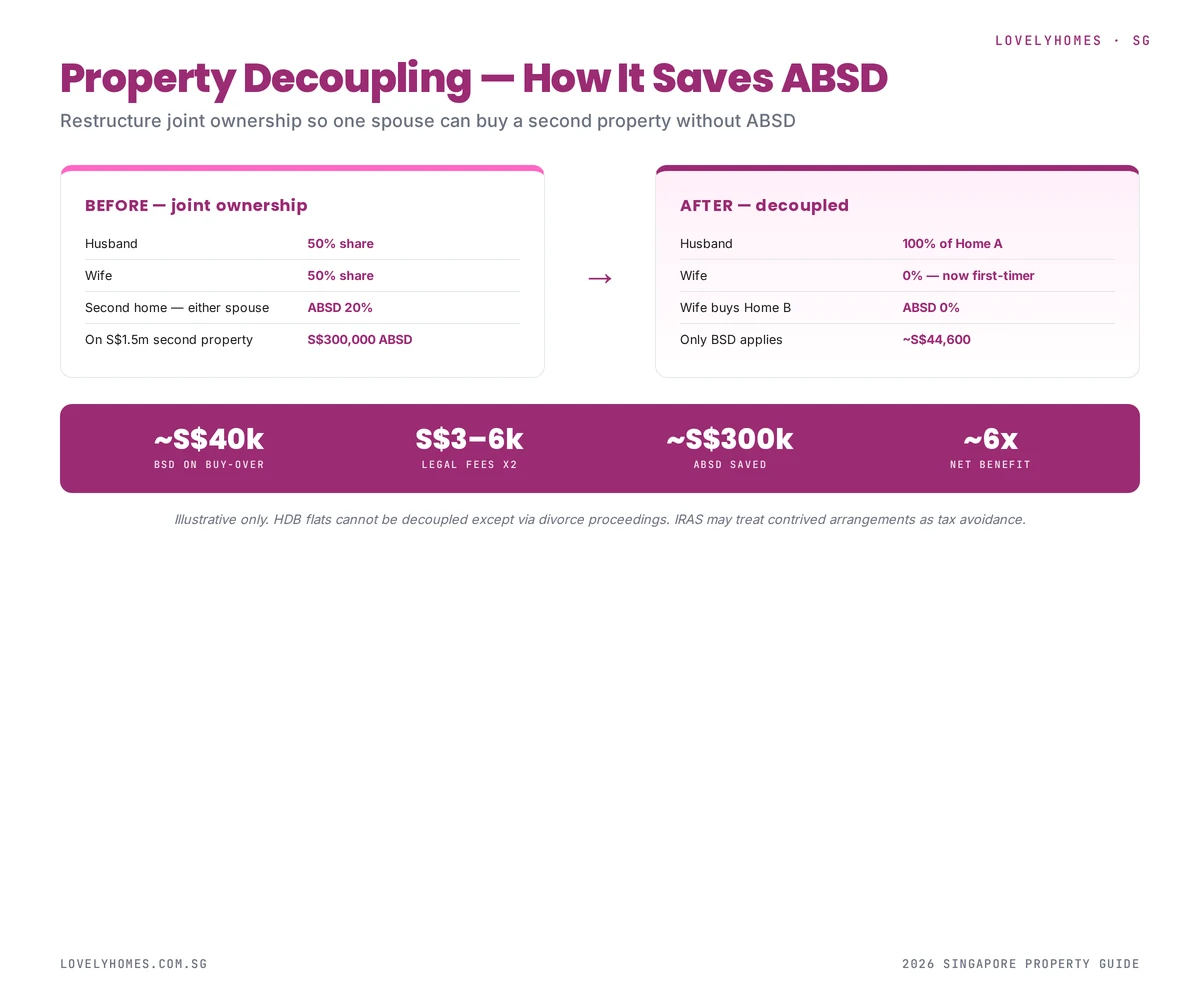

Decoupling a typical S$1.5m condo with joint ownership structured as 50:50:

Component

Amount

Property value

S$1,500,000

Share being transferred (50%)

S$750,000

BSD on S$750,000 transfer

~S$17,100

Legal fees (2 parties, separate lawyers)

S$4,000–S$6,000

Mortgage refinancing costs

S$1,000–S$3,000

CPF refund (to transferring spouse’s CPF)

Full principal + accrued interest

Total cost (excluding CPF flows)

~S$22,000–S$26,000

The CPF refund is a cash flow, not a cost — the transferring spouse’s CPF OA is topped up with their original contributions plus 2.5% annual accrued interest. They can then redeploy that CPF for the second property purchase.

Worked Example: Buying a S$1.5m Second Property

A married couple owns a S$2.5m Orchard-area condo jointly. They want to buy a S$1.5m investment unit.

Without decoupling

Both already own property → ABSD 20% applies to the second purchase

ABSD on S$1.5m = S$300,000

Plus BSD on S$1.5m = S$44,600

Total stamp duty: S$344,600

With decoupling

Husband buys out wife’s 50% share of the Orchard condo → BSD on S$1.25m = ~S$35,600

Plus legal fees and refinancing: ~S$6,000

Wife now has zero property → first-timer status

Wife buys the S$1.5m second property → ABSD 0%, BSD only

BSD on S$1.5m = S$44,600

Total stamp duty + decoupling costs: S$86,200

Net saving

S$344,600 – S$86,200 = S$258,400 saved.

HDB Flats Cannot Be Decoupled

Since 2016, HDB explicitly prohibits decoupling of HDB flats except under court order (usually in the context of divorce). The rule was introduced specifically to close the ABSD-avoidance loophole that decoupling had opened for HDB flat owners looking to buy private property.

If you own an HDB flat and want to buy a private unit without paying ABSD, the only legitimate paths are:

Sell the HDB first, buy the private unit as a first-timer (subject to MOP being fulfilled)

Dispose of HDB within 6 months of buying the private unit — the ABSD Remission Scheme refunds the ABSD you initially paid

IRAS Scrutiny: When Decoupling Becomes Tax Avoidance

Decoupling is legitimate when it reflects a genuine change in ownership. IRAS begins asking questions when the arrangement is obviously contrived for tax savings alone. Red flags include:

Back-to-back decoupling and second purchase — decouple today, OTP tomorrow

The transferring spouse had no means to be a genuine buyer (income too low to have qualified for the original loan alone)

Multiple decouplings in sequence — decouple to buy property A, decouple again to buy property B

Artificial “loan” structures where the buying spouse’s share payment is obviously funded by the transferring spouse

Under the Stamp Duties Act and the general anti-avoidance provision, IRAS can reassess the arrangement as tax avoidance and claw back the saved ABSD with a surcharge. The 99-to-1 arrangement scrutinised in 2023–2024 was a related pattern — see our 99-to-1 guide.

Is Decoupling Still Worth It in 2026?

For genuine cases — where one spouse actually wants to become a sole owner, and the other actually has the income and savings to buy a second property independently — yes. The ABSD savings on a mid-market second property (S$1m–S$2m) typically far exceed the cost of decoupling by a factor of 6 to 10.

For arrangements that are transparently tax-motivated — where the transferring spouse has no genuine interest in becoming a sole property owner — the risk calculus has changed. IRAS has shown a real willingness to reassess such arrangements, and the 1.5x clawback means a failed attempt costs more than just paying the ABSD upfront.

Practical Considerations

Timing: Complete the decoupling fully before the second property’s OTP. Back-to-back transactions draw IRAS attention.

Separate legal counsel: Each spouse should use a different lawyer. Joint counsel can be a red flag.

Market-value pricing: The share must be sold at market value, supported by a professional valuation.

Mortgage servicing: The buying spouse must independently qualify for the refinanced loan in their sole name.

CPF flows: The transferring spouse’s CPF must be refunded in the correct amount, including accrued interest.

FAQ — Decoupling 2026

Can I decouple a condo I own with my parent?

Yes, the same mechanisms apply (Part-purchase or Transfer-of-ownership). The stamp duty rates depend on the parent’s relationship, and IRAS may look more closely if the decoupling pattern is unusual.

Does decoupling affect the existing bank loan?

Yes. The bank will need to refinance the loan in the sole name of the buying spouse. If the buying spouse cannot service the full loan independently, decoupling is not viable.

How long does decoupling take?

Typically 8–12 weeks from engagement to completion. Both lawyers, the bank, and CPF must all coordinate.

Can unmarried partners decouple?

They can, but the original joint ownership would need to have had a clear commercial basis (co-investors, for instance). IRAS is more likely to scrutinise an unmarried joint ownership that decouples immediately before a second purchase.

What if IRAS does reassess?

Expect the original ABSD saved plus a 50% surcharge (1.5x clawback). On our S$300k ABSD example, that would be S$450k payable — plus interest and legal costs.

Disclaimer: This is general guidance, not legal or tax advice. Decoupling has significant tax, legal and CPF consequences specific to your household. Always engage a qualified conveyancing lawyer and a tax advisor before proceeding.