Orchard Road & Somerset Neighbourhood Guide Singapore 2026: Property Prices, MRT and Investment Outlook

Orchard Road and Somerset form the heart of Singapore’s Core Central Region (CCR). District 9 is synonymous with premium shopping malls, five-star hotels, top private schools, and a deeply liquid residential market populated by both wealthy locals and high-net-worth expatriates. Whether you are buying your first private home, upgrading from the HDB heartlands, or managing an investment portfolio, District 9 represents a distinct value proposition: scarcity, prestige, and sustained long-term capital appreciation.

This guide covers District 9 property prices in 2026, the MRT network serving Orchard and Somerset, top schools, lifestyle amenities, rental yields, a detailed investor analysis, and a worked example for upgraders. All data reflects Q1 2026 URA Realis statistics and publicly available industry information.

- Location: District 9, Core Central Region (CCR). Bounded by Scotts Road (north), River Valley Road (south), Clemenceau Avenue (west), Dhoby Ghaut (east).

- Property type mix: ~55% leasehold condos, ~45% freehold condos; no significant HDB supply in Orchard proper (limited HDB estates in Somerset fringes).

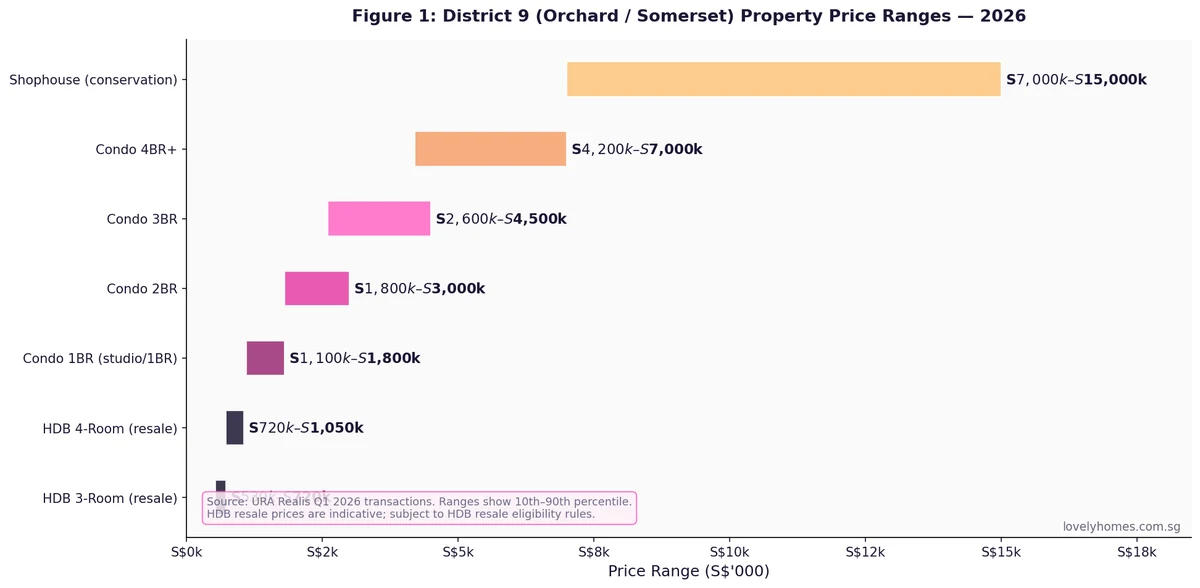

- Typical condo prices: 1BR S$1.1–1.8M; 2BR S$1.8–3.0M; 3BR S$2.6–4.5M; 4BR+ S$4.2–7.0M (Q1 2026).

- Average non-landed PSF: S$2,500–S$3,500 (freehold premium: +15–25% vs 99-yr equivalents).

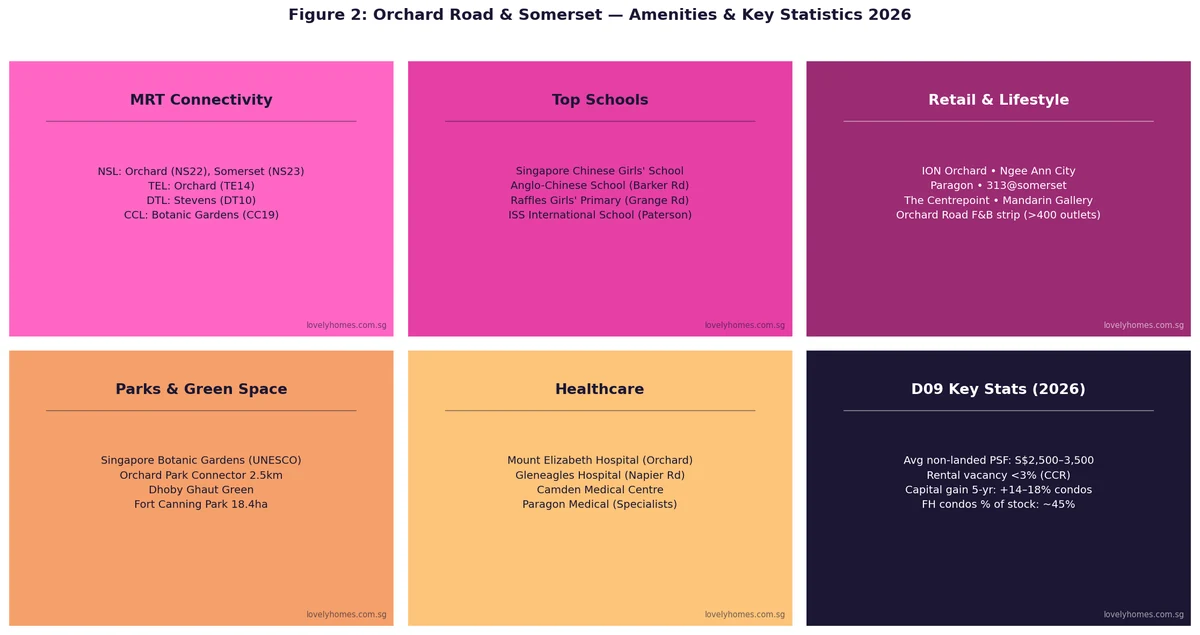

- MRT: NSL Orchard (NS22), NSL/TEL Orchard (TE14 — twin interchange), NSL Somerset (NS23), DTL Stevens (DT10), CCL Botanic Gardens (CC19).

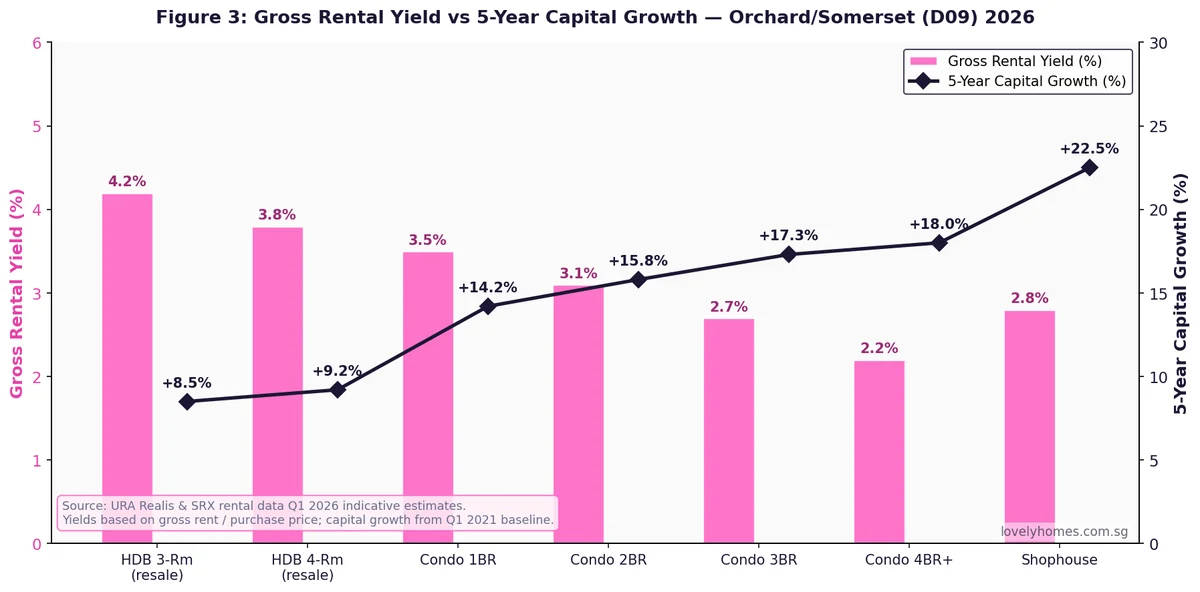

- Rental market: Vacancy <3% CCR-wide; strong expat demand from finance, tech, and diplomatic community; gross yields 2.7–3.5%.

- 5-year capital growth: +14–18% for condos; freehold units show stronger upside, especially post-en-bloc premium.

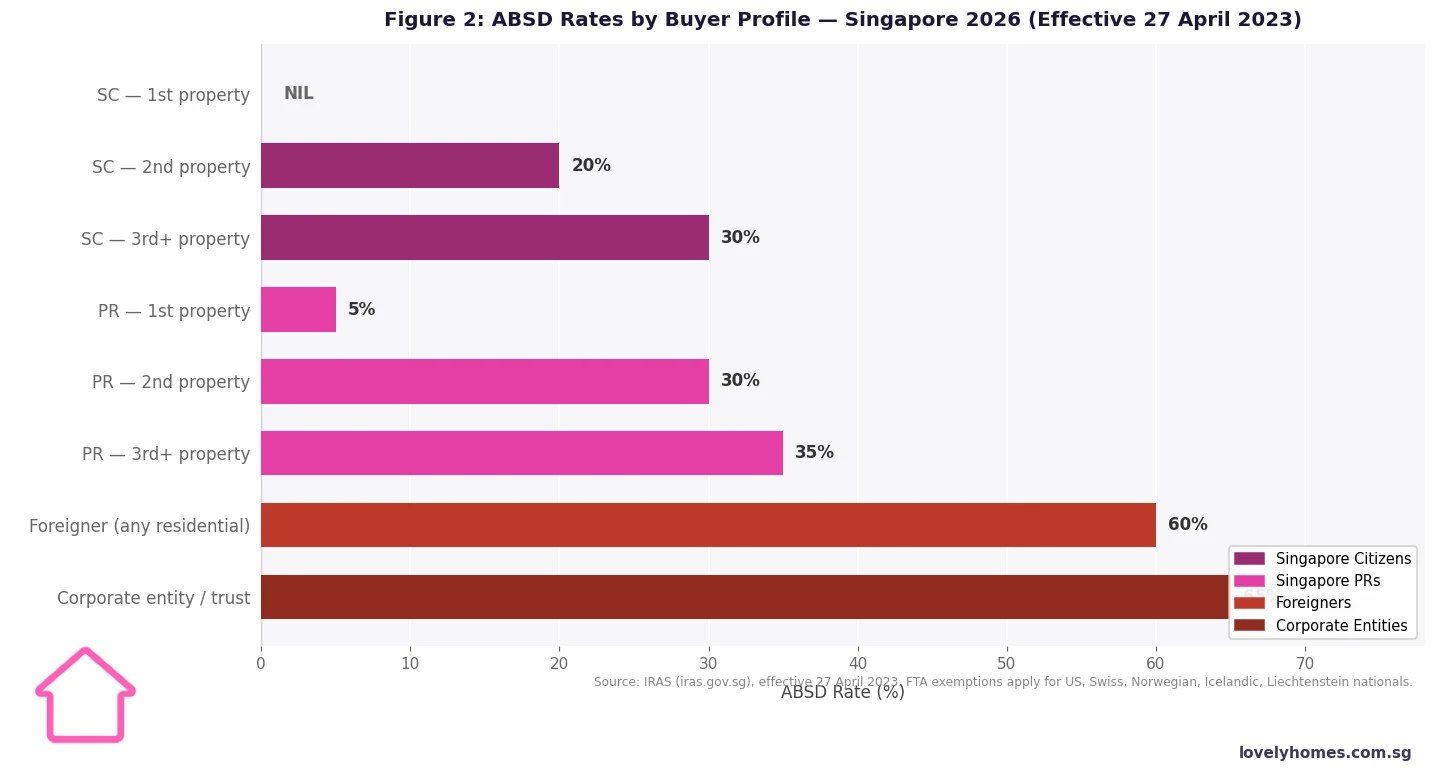

- ABSD note: Foreign buyers pay 60% ABSD on any residential property here — Singapore Citizen upgraders face 20% on a second property.

Where Exactly Is Orchard Road / Somerset — District 9 Defined

District 9 in Singapore’s URA postal district system covers the Orchard Road corridor and its immediate surrounds: Orchard, Somerset, River Valley, and the Cairnhill / Scotts Road residential enclave. It sits squarely in the CCR — the market segment that includes the most expensive residential land in Singapore.

The district is bounded to the north by Scotts Road and Dunearn Road, to the south by River Valley Road, to the west by Holland Road near its junction with Clemenceau Avenue, and to the east by the Dhoby Ghaut / Bras Basah interchange. Key residential precincts include Cairnhill (freehold conservation houses and condos), Scotts Road (ultra-luxury residential), Leonie Hill / Anthony Road (mid-to-upper-tier condos), Somerset / Oxley Road (denser condo belt), and River Valley (hybrid commercial-residential strip with shophouse clusters).

For the adjacent River Valley and Robertson Quay precinct, see our dedicated River Valley & Robertson Quay Neighbourhood Guide 2026. For the District 10 corridor (Holland Village, Tanglin, Buona Vista), see our Buona Vista & Holland Village Guide.

Property Prices in District 9 — Orchard & Somerset 2026

The typical price entry points in Orchard / Somerset are among the highest in Singapore outside of Sentosa Cove. A 1-bedroom or studio unit — favoured by investors and young expatriate professionals — transacts between S$1.1 million and S$1.8 million. At the upper end, a 4-bedroom-plus condo in a quality freehold development on Scotts Road or Cairnhill Circle commands S$4.2 million to S$7 million.

Conservation shophouses in the precinct (primarily along Orchard Road’s side streets and the Emerald Hill enclave) represent a distinct asset class: 2,200–4,500 sq ft of strata area, no ABSD for commercial and mixed-use strata titles, and scarcity driven by heritage conservation rules. Prices range from S$7 million to S$15 million or more for larger units on premium lots.

Price per square foot (PSF) benchmarks (Q1 2026):

| Development / Type | Tenure | Approx PSF (Q1 2026) | Notes |

|---|---|---|---|

| Cairnhill / Scotts Rd luxury | Freehold | S$3,200–S$4,500 | Boulevard 88, Gramercy Park |

| Orchard / Somerset mid-upper | Freehold | S$2,600–S$3,500 | Skyline @ Orchard, 8 Hullet |

| River Valley mid-tier condos | 99-yr | S$2,200–S$2,800 | Martin Modern, The Avenir |

| HDB resale (Somerset fringes) | 99-yr | S$700–S$950 | Limited supply; very few D09 HDB flats |

| Conservation shophouse | Freehold/999-yr | S$3,000–S$5,000+ | Emerald Hill, Orchard surrounds |

MRT Connectivity — Why D09 Is a Multi-Line Hub

District 9 is one of the best-served MRT districts in Singapore, sitting at the convergence of four lines. This multi-line access underpins the area’s sustained rental demand from expatriates who typically require CBD proximity and do not own cars.

The North-South Line (NSL) serves Orchard (NS22) and Somerset (NS23). Orchard is a major interchange and the line’s most commercially prominent station, with connections to the grade-level Orchard Road shopping belt. From Orchard, Raffles Place is 5 minutes; Marina Bay is 8 minutes.

The Thomson-East Coast Line (TEL) opened its Stage 2 in August 2021, delivering a new Orchard station (TE14) directly adjacent to the NSL Orchard station. The TEL gives direct access south to Great World (TE15), Havelock (TE16), Maxwell (TE18), and Shenton Way (TE19/DTL CE1) — cutting commute times to the Marina Bay financial corridor. Northwards, the TEL connects to Stevens (TE11), Caldecott (TE9), and eventually Woodlands North (TE2).

The Downtown Line (DTL) station at Stevens (DT10) is a short cab or walk from the northern fringe of D09 (Scotts Road/Dunearn Road). This line serves Bugis, Promenade, Bayfront, and the western corridor through Buona Vista and Clementi.

The Circle Line (CCL) station at Botanic Gardens (CC19) serves the western edge of the district, providing access to one-north (CC23), Harbourfront (CC29/NE1), and the eastern CCL loop.

Schools, Healthcare, and Lifestyle

Top primary schools within 1–2km: Raffles Girls’ Primary School (Grange Road, 0.9km from Orchard MRT) is perennially over-subscribed and has a significant influence on residential demand within its 1km balloting radius. Singapore Chinese Girls’ School (Springleaf Avenue, primary campus) and Anglo-Chinese School (Barker Road, primary) are also within the broader D09/D11 catchment.

International schools: ISS International School (Paterson Road) sits directly within the district, drawing enrolments from the large expatriate community in the Orchard and River Valley condos. GESS International School (Bukit Timah Road, nearby) and EtonHouse International School (Mountbatten Road) are within reasonable distance.

Healthcare: Mount Elizabeth Hospital on Orchard Road is one of Singapore’s premier private hospitals, specialising in oncology, cardiology, and complex surgical procedures. Gleneagles Hospital (Napier Road, ~1.2km) is another major private facility. Camden Medical Centre is a specialist-only medical building on Orchard Road itself. For emergency and specialist care, Singapore General Hospital (Outram) is accessible via the TEL in under 10 minutes.

Retail and F&B: The Orchard Road corridor hosts ION Orchard (Capitaland’s flagship mixed-use development), Ngee Ann City, Paragon, Mandarin Gallery, 313@Somerset, The Centrepoint, Knightsbridge, and Forum The Shopping Mall — more than 2.5 million sq ft of retail within 1.5km. The area’s F&B scene ranges from hawker centres at Killiney Road and Takashimaya Food Hall to Michelin-starred restaurants at Mandarin Oriental and Shangri-La Hotel.

Green space: The Singapore Botanic Gardens (UNESCO World Heritage Site, 82ha) is accessible via CCL Botanic Gardens, providing a world-class green lung immediately to the west of the district. Fort Canning Park (18.4ha) sits at the eastern edge of D09, offering a historic hilltop park connecting to Dhoby Ghaut and Clarke Quay. The Orchard Park Connector (2.5km) links the precinct to MacRitchie.

Rental Market and Investment Case

The Orchard / Somerset rental market is driven primarily by expatriate demand from Singapore’s finance, technology, and international trading sectors, supplemented by diplomatic and media professionals. Vacancy rates across the CCR have held below 3% since 2022, reflecting tightened expat supply (fewer new completions in D09 in the 2023–2025 cycle) and sustained rental growth.

Gross rental yields in D09 typically run 2.2–3.5% depending on unit type, reflecting the high absolute purchase prices. The 1-bedroom segment commands the highest gross yield (approximately 3.5%) because monthly rentals for 1BR units are relatively strong (S$3,500–S$6,500/month) relative to purchase prices. The 4-bedroom-plus segment yields less on a gross basis (approximately 2.2%) but benefits most from capital appreciation — freehold trophy assets in D09 showed 18–22% 5-year price growth.

The long-term investment thesis for D09 rests on land supply constraints. There are no new GLS residential sites in the Orchard Road core; all new supply must come from en-bloc redevelopment of ageing freehold buildings. Historically, en-bloc activity in D09 has been lumpy and infrequent, which means supply shocks are rare. The CCR Private Property Index has risen approximately 40% since Q1 2019 — a compounded annual growth rate of around 5.5%.

Worked Example: SC Upgrader Buying a 2BR Freehold Condo in D09

Mr & Mrs Teo are Singapore Citizens. They have sold their Tampines 5-room HDB flat (received CPF accrued interest refund, net cash proceeds S$380,000). Joint income S$17,000/month. They want to buy a 2-bedroom freehold condo on River Valley Road at S$2,200,000. They now hold zero residential properties after the HDB sale.

- Purchase price: S$2,200,000 (freehold, District 9)

- BSD: S$74,600

- ABSD: S$0 (SC first private property after HDB sale)

- Total stamp duty: S$74,600

- Loan (75% LTV, bank): S$1,650,000 @ 3.0% p.a., 25-year tenure

- Monthly instalment: approximately S$7,832/month

- TDSR check: S$7,832 / S$17,000 = 46.1% — within the 55% TDSR ceiling ✓

- 5% mandatory cash (on bank loan): S$110,000

- CPF OA drawdown (down payment balance): up to Valuation Limit (S$2,200,000 × 100% = S$2,200,000 — no restriction for private property first purchase by buyers under 55)

- Estimated total cash required at exercise of OTP: BSD S$74,600 + 1% OTP deposit S$22,000 + 5% cash component S$110,000 = approximately S$206,600 plus legal fees (~S$3,500–5,000).

- Monthly running costs: Mortgage S$7,832 + maintenance fees (est. S$500–S$800/month) + property tax (annual value ~S$36,000 → non-owner-occupied tax ~S$1,080/yr if rented; owner-occupied ~S$260/yr)

At a 3.1% gross rental yield on S$2.2M, the property could generate approximately S$5,683/month gross rent if rented out — covering approximately 73% of the mortgage outlay. After deducting management fees, maintenance, and vacancy allowance, the net cash shortfall for a buy-to-let investor would be approximately S$2,500–S$3,000/month on this particular scenario. Most D09 buyers are therefore hybrid occupier-investors who intend to live in the property for several years before potentially renting it out.

Is Orchard Road / Somerset a Good Buy in 2026?

For Singapore Citizens and PRs buying their primary residence, D09 offers a compelling value proposition if you value proximity to Orchard Road amenities, top schools in the 1km radius, and multi-line MRT access. The scarcity of new supply in the immediate Orchard precinct means existing freehold buildings tend to hold and grow value well over a 5–10 year horizon.

For pure investors managing yield expectations, the mathematics are tighter than in the OCR. A D09 condo at S$2.5M will typically yield 2.8–3.2% gross — meaningfully lower than a comparable Tampines or Bedok condo at 3.8–4.2%. The case for D09 as an investment property is therefore primarily a capital appreciation story, not a yield story.

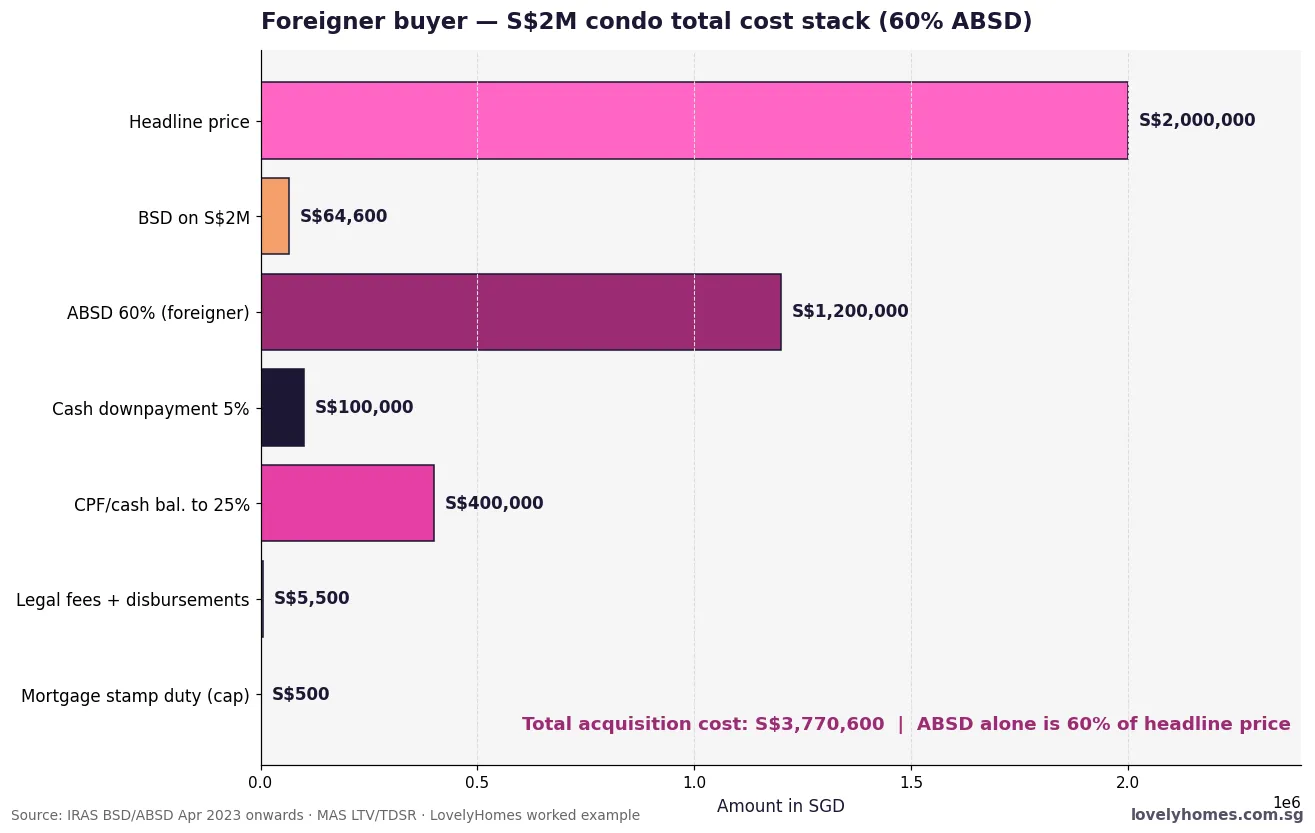

For foreign nationals considering a purchase here, the 60% ABSD makes D09 residential property a prohibitively expensive investment at current prices — unless the property will serve as a long-term primary residence in Singapore. On a S$3M property, the total upfront cost including BSD and ABSD exceeds S$2.1M in stamp duty alone. See our ABSD Complete Guide 2026 for how FTA nationals (US citizens, Swiss nationals) can mitigate this.

What Might Change in Orchard & Somerset — The Forward View

The following is analytical speculation, not official policy.

The URA’s long-term masterplan has consistently designated Orchard Road as Singapore’s premier lifestyle and shopping corridor. In the 2023 URA Concept Plan, there is mention of injecting more mixed-use and residential components into the Orchard belt — particularly along the Somerset-Dhoby Ghaut stretch — to enliven the area and support permanent resident activity. If implemented, this could bring some new residential supply to the district over the 2030–2040 horizon, but the planning quantum is unlikely to materially alter the current supply dynamics.

The TEL full opening (Stage 4 and beyond) will continue to enhance D09’s connectivity, particularly southwards to the Greater Southern Waterfront precincts. Any rebalancing of demand from the Sentosa / Harbourfront precinct back to the Orchard corridor would be a positive for D09 capital values.

Frequently Asked Questions

Is Orchard Road a good place to buy property in 2026?

For Singapore Citizens and PRs, yes — particularly if you are buying for long-term capital appreciation and benefit from the lifestyle amenities (top-tier retail, world-class healthcare, park access) and premium school catchments (Raffles Girls’ Primary 1km zone). For pure yield investors or foreign buyers facing 60% ABSD, the numbers are significantly harder. D09 suits owner-occupier-investors with a 7–10 year or longer investment horizon.

Which MRT lines serve Orchard Road and Somerset?

Four MRT lines serve D09. The North-South Line (NSL) serves Orchard (NS22) and Somerset (NS23). The Thomson-East Coast Line (TEL) provides a second Orchard interchange station (TE14), giving direct access south to the CBD and Shenton Way. Stevens (DT10) on the Downtown Line serves the Scotts/Dunearn Road fringe of the district. Botanic Gardens (CC19) on the Circle Line is at the western edge. This multi-line coverage gives D09 residents arguably the best public transport access of any residential district outside the CBD itself.

Can foreigners buy property in Orchard Road?

Yes — foreigners can purchase private condominiums and apartments in Singapore, including in District 9. However, the ABSD at 60% applies regardless of which property it is or whether it is the buyer’s first or fifth. Foreigners cannot purchase HDB flats. Citizens of the US, Switzerland, Iceland, Liechtenstein, and Norway receive SC-equivalent ABSD treatment under their respective Free Trade Agreements. Landed property in Singapore is generally restricted to Singapore Citizens; foreigners require LDAU approval to purchase landed residential property.

What are the best condominiums in Orchard / Somerset?

Benchmark developments in D09 include: Boulevard 88 (Freehold, Cuscaden Road — ultra-luxury, S$4,000–5,500 psf), Gramercy Park (Freehold, Grange Road — S$3,200–4,000 psf), The Avenir (Freehold, River Valley Road — S$2,800–3,200 psf, 376 units), 8 Hullet (Freehold, Hullet Road, boutique), Skyline @ Orchard Boulevard (Freehold, S$2,800–3,400 psf), and Martin Modern (99-yr, Martin Place — S$2,200–2,600 psf, GuocoLand, sold-out at launch). The “best” condo depends on your priority: yield, capital growth, prestige, or lifestyle fit.

How does District 9 compare to District 10 (Holland / Tanglin) as an investment?

Both districts sit in the CCR and share many characteristics (premium prices, expat rental demand, freehold stock, strong school catchments). D09 (Orchard) typically commands a PSF premium of S$200–400 over D10 (Holland Village / Tanglin) at comparable quality, reflecting its higher street-presence value, superior MRT connectivity, and denser retail-F&B ecosystem. D10 tends to offer larger unit sizes for the same budget and has traditionally attracted family-oriented buyers (larger condos, proximity to the Botanic Gardens, established landed belt). For investors focused on yield vs price, D10 is slightly more favourable; for pure capital appreciation, the two are closely matched historically.

Is there new HDB supply in Orchard Road or Somerset?

No. There is no planned HDB BTO supply in the Orchard Road or Somerset core. The very limited HDB stock that exists in the D09 area (primarily older estates on the margins, e.g. near Cairnhill) was built decades ago and rarely comes on the resale market. The Somerset-Dhoby Ghaut belt is fully committed to private residential and commercial development. HDB upgraders moving into D09 are typically accessing the private resale condominium market, not HDB flats.

Related Articles

- River Valley & Robertson Quay Neighbourhood Guide 2026: D09 Property, TEL MRT and Investment Outlook

- Novena & Newton Neighbourhood Guide Singapore 2026: D11 Prices, MRT and Investment

- Buona Vista & Holland Village Neighbourhood Guide 2026: D10/D5 Property and Investment

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Complete Guide 2026: BSD, ABSD, SSD and ACD Explained

- Singapore Bridging Loan Guide 2026: Bridging the Gap Between Selling and Buying

- Singapore Property Upgrader Guide: HDB to Private Condo — the Sequencing and ABSD Questions

Disclaimer: This guide is for general informational purposes only and does not constitute financial, legal, or tax advice. Property prices, yields, and market conditions change. Always verify the latest figures with URA Realis and HDB Resale Portal. Consult a licensed financial adviser and conveyancing lawyer before any property transaction. Stamp duty figures are indicative — verify with IRAS before transacting.