Singapore Buyer’s Stamp Duty (BSD) 2026: Rates, Calculations and Worked Examples

📌 Quick Answer: Buyer’s Stamp Duty (BSD) in Singapore 2026

- BSD is paid by every buyer of property in Singapore — residential or commercial — regardless of nationality, residency, or how many properties they own.

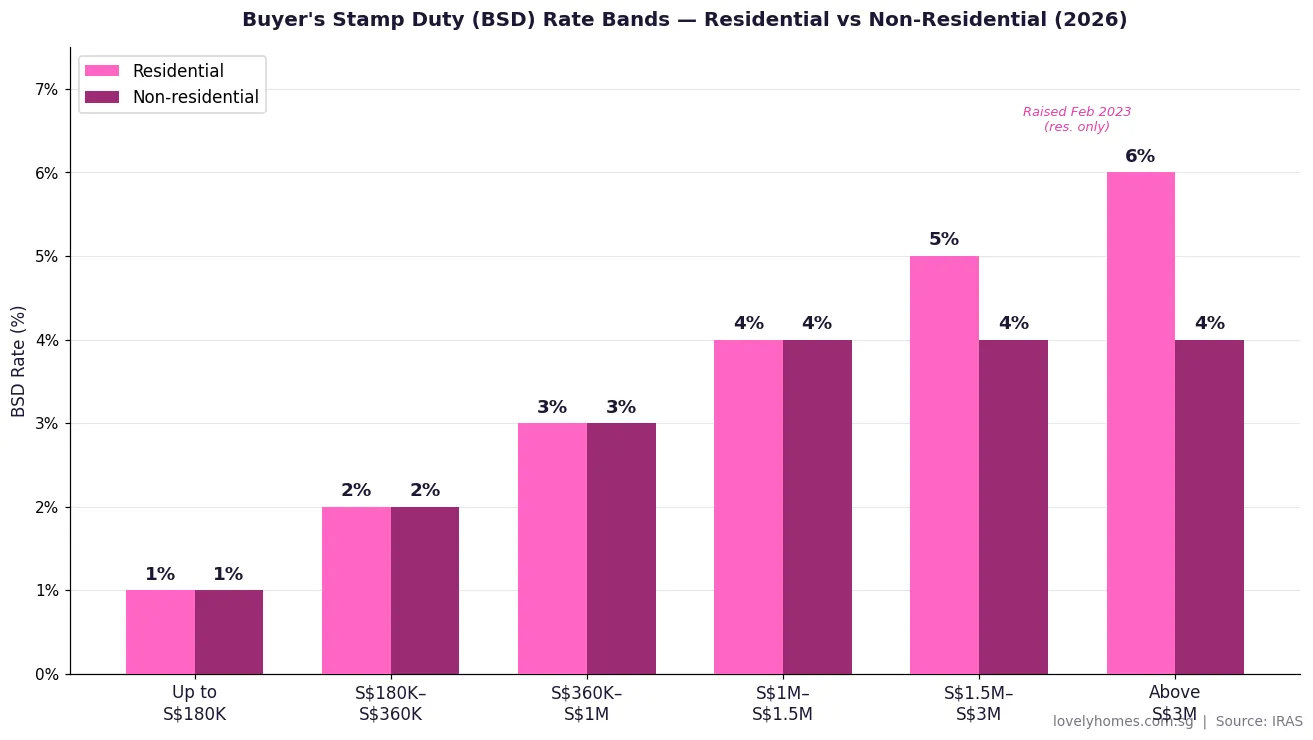

- Residential BSD rates are progressive: 1% on the first S$180,000, rising to 6% on amounts above S$3 million (rates raised in February 2023 Budget).

- Non-residential BSD is capped at 4% (no 5% or 6% tiers apply).

- BSD must be paid within 14 days of exercising the Option to Purchase (OTP) or signing the Sale & Purchase (S&P) agreement.

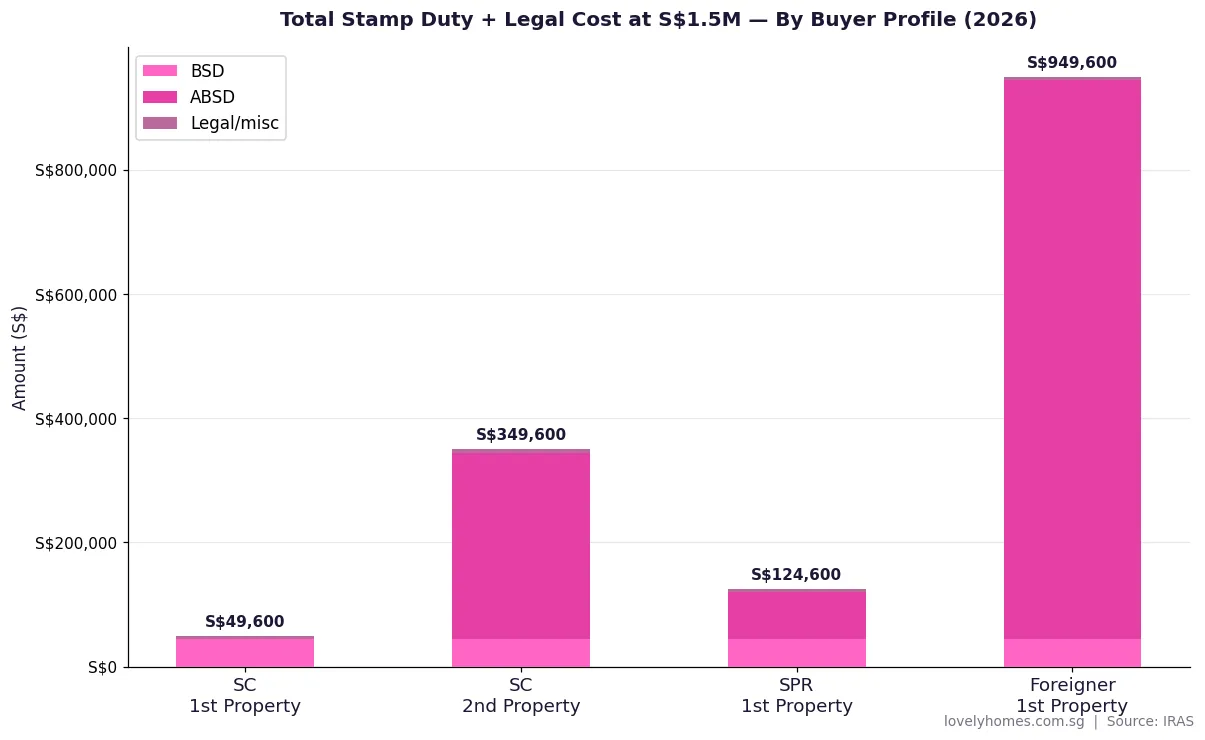

- On a S$1.5 million condo, BSD is S$44,600 — that is before any Additional Buyer’s Stamp Duty (ABSD) kicks in.

- BSD is separate from ABSD: ABSD applies only to second or subsequent properties (for Singapore Citizens) or all properties (for Permanent Residents and foreigners).

- No exemptions for first-time buyers — BSD applies to everyone; only certain inherited or court-ordered transfers are exempt.

- CPF Ordinary Account funds may be used to pay BSD on eligible residential properties.

What Is Buyer’s Stamp Duty (BSD)?

Buyer’s Stamp Duty (BSD) is a tax levied by the Inland Revenue Authority of Singapore (IRAS) on every purchase or acquisition of property in Singapore. Unlike the Additional Buyer’s Stamp Duty (ABSD) — which applies only to certain buyers — BSD is universal: it falls on every transaction regardless of whether the buyer is a Singapore Citizen (SC), Permanent Resident (PR), foreigner, or corporate entity, and regardless of how many properties they already own.

BSD is calculated on the higher of the purchase price or the market value of the property. IRAS uses the property’s assessed annual value and recent comparable sales to determine market value; if your agreed price is below market value, IRAS will compute BSD on the higher market-value figure. The tax is administered under the Stamp Duties Act (Cap. 312) and must be paid promptly — late payment attracts penalties.

The February 2023 Budget introduced new higher rate tiers for residential property, bringing the top marginal rate to 6% for portions of the price above S$3 million. For non-residential property (commercial, industrial, mixed-use), the maximum rate remains 4%. Understanding BSD is therefore a mandatory step in any property budget — you cannot legally complete a purchase without stamping the documents.

BSD Rates for Residential Property (2026)

The following progressive rate schedule applies to all residential property purchases from 15 February 2023 onwards (Budget 2023). Note that the rates are marginal — each band applies only to the portion of the price falling within that range, not the entire purchase price.

| Purchase Price Band | BSD Rate | Maximum BSD in Band |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 (S$180,001 – S$360,000) | 2% | S$3,600 |

| Next S$640,000 (S$360,001 – S$1,000,000) | 3% | S$19,200 |

| Next S$500,000 (S$1,000,001 – S$1,500,000) | 4% | S$20,000 |

| Next S$1,500,000 (S$1,500,001 – S$3,000,000) | 5% | S$75,000 |

| Remaining amount (above S$3,000,000) | 6% | Unlimited |

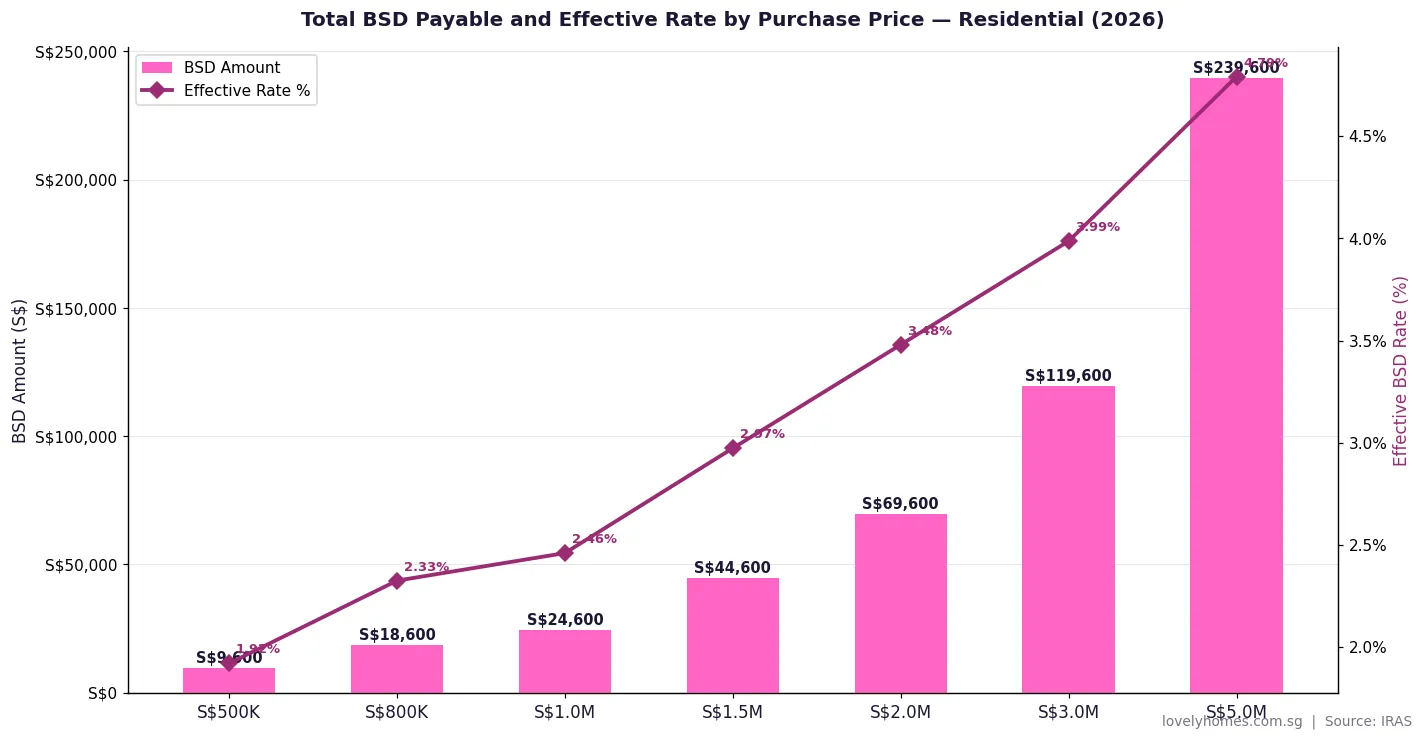

The cumulative BSD payable at the top of each band is S$1,800 → S$5,400 → S$24,600 → S$44,600 → S$119,600 and beyond. For a S$1 million property the BSD is exactly S$24,600; for a S$1.5 million property it is S$44,600; for a S$3 million property it is S$119,600.

BSD Rates for Non-Residential Property (2026)

Industrial, commercial, and mixed-use properties follow a different schedule that was last revised in 2018. The rates are lower and the top marginal rate is capped at 4%, reflecting government policy to keep transaction costs manageable for business property buyers.

| Purchase Price Band | BSD Rate | Maximum BSD in Band |

|---|---|---|

| First S$180,000 | 1% | S$1,800 |

| Next S$180,000 (S$180,001 – S$360,000) | 2% | S$3,600 |

| Next S$640,000 (S$360,001 – S$1,000,000) | 3% | S$19,200 |

| Remaining amount (above S$1,000,000) | 4% | Unlimited |

On a S$2 million shophouse, for instance, the BSD is S$24,600 (the S$1 million cumulative) plus 4% of S$1 million = S$40,000 → total S$64,600. Compare this to a residential property of the same price where BSD would be S$69,600. The difference is modest at S$2 million but widens materially at S$5 million and above.

How to Calculate BSD Step by Step

BSD is a progressive tax, so the calculation requires applying each marginal rate to the corresponding band of the purchase price. The cleanest method is to use the marginal-band approach. Consider a S$1,800,000 residential property:

- 1% × S$180,000 = S$1,800

- 2% × S$180,000 = S$3,600

- 3% × S$640,000 = S$19,200

- 4% × S$500,000 = S$20,000

- 5% × S$300,000 (the remaining S$1.8M − S$1.5M = S$0.3M) = S$15,000

- Total BSD = S$59,600

IRAS also publishes a shortcut formula for common brackets. For residential properties priced between S$1 million and S$1.5 million the formula is: BSD = (4% × price) − S$15,400. For S$1 million: (4% × S$1M) − S$15,400 = S$40,000 − S$15,400 = S$24,600 ✓. These formulae are available in IRAS’s stamp duty calculator at iras.gov.sg.

When and How to Pay BSD

BSD must be paid within 14 days of the document being signed or executed — that is, within 14 days of exercising the Option to Purchase (OTP) for resale properties, or within 14 days of the date of the Sale & Purchase agreement for new launches. Late payment attracts a penalty of S$10 or the unpaid duty, whichever is higher, plus additional penalties of up to 4× the original duty for prolonged non-payment.

Payment is made through e-Stamping at the IRAS portal, accessible via Singpass. Solicitors acting for buyers routinely handle this on their clients’ behalf. The stamped document is legal evidence of the transaction; an unstamped instrument cannot be admitted as evidence in court.

BSD may be paid using CPF Ordinary Account (OA) funds for eligible residential properties — subject to the CPF withdrawal limit and valuation limit rules. If paying by CPF, the CPF Board will typically release the BSD payment to IRAS directly on completion. Cash payment via GIRO, credit/debit card, or bank transfer is also accepted. Foreigners without a Singpass account must pay through their appointed solicitor.

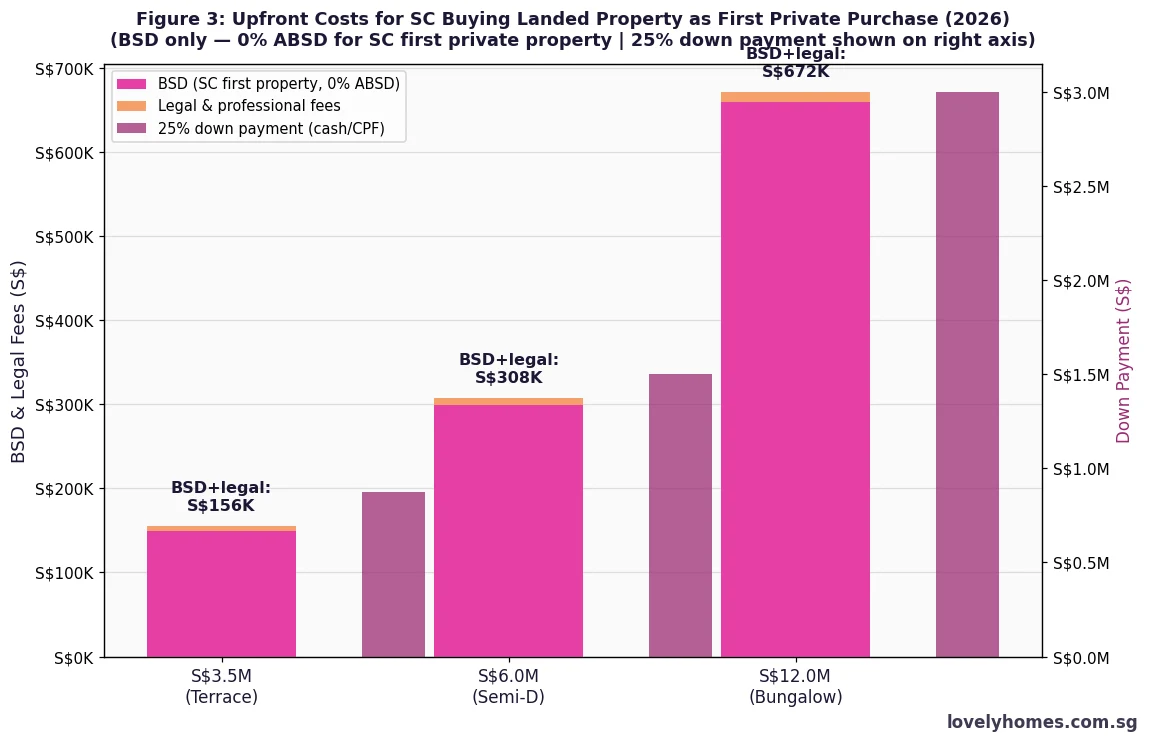

📌 Worked Example: Mr & Mrs Nair — D11 Condo S$2,200,000

Mr Nair is a Singapore Citizen; Mrs Nair is a Singapore Permanent Resident. This will be their first property. They are purchasing a 3-bedroom condominium in Newton / Novena (D11, RCR) at S$2,200,000. The solicitor will compute BSD as follows:

- 1% × S$180,000 = S$1,800

- 2% × S$180,000 = S$3,600

- 3% × S$640,000 = S$19,200

- 4% × S$500,000 = S$20,000

- 5% × S$700,000 (S$2.2M − S$1.5M) = S$35,000

- Total BSD = S$79,600 (effective rate: 3.62%)

ABSD position: because this is a joint purchase and Mrs Nair is a PR, the joint ABSD rate is determined by the buyer with the higher rate. SC buying 1st property = 0%; PR buying 1st property = 5%. As a mixed-citizenship couple, IRAS applies the higher rate — so ABSD of 5% × S$2,200,000 = S$110,000 applies. (They may request an ABSD remission if they intend to occupy the property, but remission is not automatic for SC/PR joint purchases on first property.)

Combined stamp duties: BSD S$79,600 + ABSD S$110,000 = S$189,600. Legal fees approximately S$5,500. Total transaction costs at completion: approximately S$195,100 (excluding down payment and financing costs).

Bank loan (SC income S$18,000/mth): 75% LTV = S$1,650,000 at 3.0% p.a. over 30 years → monthly instalment S$6,955. TDSR: (S$6,955 ÷ S$18,000) = 38.6% ✓ (below 55% TDSR limit).

Why BSD Matters: The True Cost of Buying Property in Singapore

BSD is a non-negotiable transaction cost that must be factored into every property budget from day one. At S$1 million, BSD alone is S$24,600 — roughly 2.5% of the purchase price. At S$3 million, it reaches S$119,600. For buyers stretching their budget to the maximum under Total Debt Servicing Ratio (TDSR) rules, forgetting to account for BSD can push a deal beyond their financial reach. Solicitors and mortgage advisers always incorporate BSD into the cashflow calculation alongside down payment, valuation fees, legal fees, and agent commissions.

Compared to peer jurisdictions, Singapore’s BSD is moderate but has been rising. Hong Kong’s stamp duty on residential property ranges from HK$100 to 4.25% of the price for the basic rate, with additional buyer’s stamps up to 30% for non-residents. Australia’s stamp duty varies by state and can exceed 5% in New South Wales and Victoria. Singapore’s BSD at an effective rate of around 2.5–4% for typical residential purchases sits within the regional norm, though the additional ABSD layers make total stamp costs for repeat or foreign buyers among the highest globally.

📊 What Might Come Next: BSD Outlook

This section is speculative and based on publicly available signals. It is not investment advice.

The February 2023 BSD increase targeted high-value transactions (above S$1.5 million), nudging effective rates higher for luxury properties. In the near term — through 2026 and into 2027 — industry observers do not anticipate a further upward revision to BSD, given that ABSD rates (raised to 60% for foreigners and 20% for SC second properties in April 2023) already provide strong price-stability signals. However, should the private residential price index continue its upward trajectory into the upper percentiles, a further adjustment to the S$3 million+ band (currently at 6%) cannot be ruled out in a future Budget.

For commercial and industrial BSD, a revision has been discussed informally in property finance circles, particularly given that strata industrial and shophouse prices have risen sharply since 2021. Any Budget announcement would take effect immediately on the date of the Budget speech, as has historically been the case.

Frequently Asked Questions: Buyer’s Stamp Duty Singapore

Does BSD apply to HDB flat purchases?

Yes. BSD applies to all residential property acquisitions in Singapore, including HDB resale flats and new BTO flat purchases. However, most HDB flats are priced well below S$1 million, so the effective BSD rate is typically 1–2%. For a S$600,000 4-room resale HDB flat, BSD is: (1% × S$180,000) + (2% × S$180,000) + (3% × S$240,000) = S$1,800 + S$3,600 + S$7,200 = S$12,600. The BSD on HDB purchases is significantly lower than on private condominiums. Note that for HDB purchases, CPF OA funds are routinely used to pay BSD, and the HDB will typically manage the stamping process on your behalf.

Is BSD different from ABSD? Can I avoid one but not the other?

BSD and ABSD are two separate taxes levied by IRAS. BSD applies to every buyer on every property — there is no exemption for first-time buyers. ABSD is an additional tax that applies to: Singapore Citizens buying a second or subsequent residential property (20% for second, 30% for third or more); Singapore PRs buying any residential property (5% first, 25% second and beyond); all foreigners buying any residential property (60% as of April 2023, with limited FTA exemptions for certain nationalities). It is impossible to avoid BSD; ABSD can be avoided by Singapore Citizens on their first property and in certain limited circumstances (e.g., FTA exemptions, ABSD remission for married couples). BSD is always payable on both residential and non-residential acquisitions.

What is the BSD deadline and what happens if I pay late?

BSD must be paid within 14 days of the date the relevant instrument is executed or signed. For resale properties, this means within 14 days of exercising the Option to Purchase (OTP). For new launch properties, within 14 days of signing the Sale & Purchase agreement. IRAS imposes penalties for late payment: S$10 or the unpaid duty (whichever is higher) for the first default, scaling up to 4× the outstanding duty for extended non-payment. In practice, conveyancing solicitors almost always handle BSD stamping within the 14-day window as a standard part of their service. You should therefore ensure you have the BSD funds ready to transfer to your solicitor’s client account well before the stamping deadline.

Can I use CPF to pay BSD in Singapore?

Yes, for eligible residential properties. CPF Ordinary Account (OA) savings may be used to pay BSD, subject to the applicable CPF withdrawal limits. The property must be used as a principal place of residence, and the purchase must satisfy CPF Board criteria (e.g., remaining lease of the property must meet the minimum occupation period requirements). CPF cannot be used to pay BSD on non-residential property purchases (shophouses, industrial, commercial). If you are using CPF for BSD, inform your solicitor at the start of the conveyancing process so they can arrange the CPF withdrawal in time. Any CPF withdrawn for BSD forms part of your total CPF withdrawal and attracts accrued interest at the OA rate of 2.5% per annum, which must be refunded to your CPF upon the eventual sale of the property.

Are there any exemptions from BSD in Singapore?

BSD exemptions are narrow. Transfers pursuant to a court order (e.g., divorce proceedings under section 112 of the Women’s Charter) may be exempt or subject to ad valorem duty on a different basis. Inherited property transferred via probate or letters of administration under intestate succession is also exempt from BSD (as it is a transmission, not a purchase). Government land acquisitions under the Land Acquisition Act are exempt. However, gifts of property between family members (including parents, siblings, and children) are generally not exempt unless effected as a court order; such transfers attract BSD at market value. There is no general first-time buyer exemption and no BSD discount for owner-occupiers — every voluntary purchase triggers the full progressive rate.

Is BSD based on the purchase price or the market value?

BSD is computed on the higher of the purchase price or the market value as assessed by IRAS at the time of the transaction. If you purchase a property below its assessed market value — for example, buying from a relative at a discounted price or acquiring a distressed-sale unit below prevailing comparable prices — IRAS will compute BSD on the market value, not the agreed price. Conversely, if you pay above market value (rare, but possible in competitive bidding situations), BSD is based on the actual price paid. IRAS cross-references the Urban Redevelopment Authority’s (URA) caveats database and the HDB resale transaction data to assess market value. Disputes about assessed value may be referred to the Stamp Duties Appeal Board.

Does BSD apply to property acquired through a company?

Yes. When a company — whether a Singapore-incorporated or foreign-incorporated entity — acquires property, BSD applies on the same basis as for individual buyers. The company must pay BSD on the higher of the purchase price or market value. In addition, corporate buyers are subject to ABSD at 65% for residential property (as of April 2023), making entity-held residential acquisitions extremely expensive. For commercial and industrial property, companies pay BSD at the non-residential rates (up to 4%) with no ABSD. Transfers of shares in a property-holding company may also attract stamp duty under Section 15 of the Stamp Duties Act; the rules are complex and specialist tax advice is recommended for such structures.

Related Articles on Singapore Property Taxes and Buying Costs

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Seller’s Stamp Duty (SSD) 2026: New 4-Year Holding Period and Rates Explained

- Singapore Property Conveyancing Guide 2026: OTP, S&P, Legal Fees and Timelines

- Singapore Foreign Buyer Property Guide 2026: ABSD 60%, Eligibility and Stamp Duties

- Singapore Home Loan Complete Guide 2026: HDB Loans, TDSR, MSR and Best Rates

- Singapore Property Decoupling Guide 2026: Save ABSD, Costs and Step-by-Step Process

Disclaimer

This article is for general informational purposes only and does not constitute legal, financial, or tax advice. BSD rates and rules are set by the Inland Revenue Authority of Singapore (IRAS) and may change with each annual Budget. Always verify current rates and your personal BSD and ABSD obligations at iras.gov.sg before transacting. For a formal computation and to ensure timely stamping, engage a licensed Singapore conveyancing solicitor. LovelyHomes is not a licensed financial adviser or solicitor; no reliance should be placed on this article as a substitute for professional advice tailored to your specific circumstances.