CPF for Property Singapore 2026: OA, Accrued Interest & HPS Explained

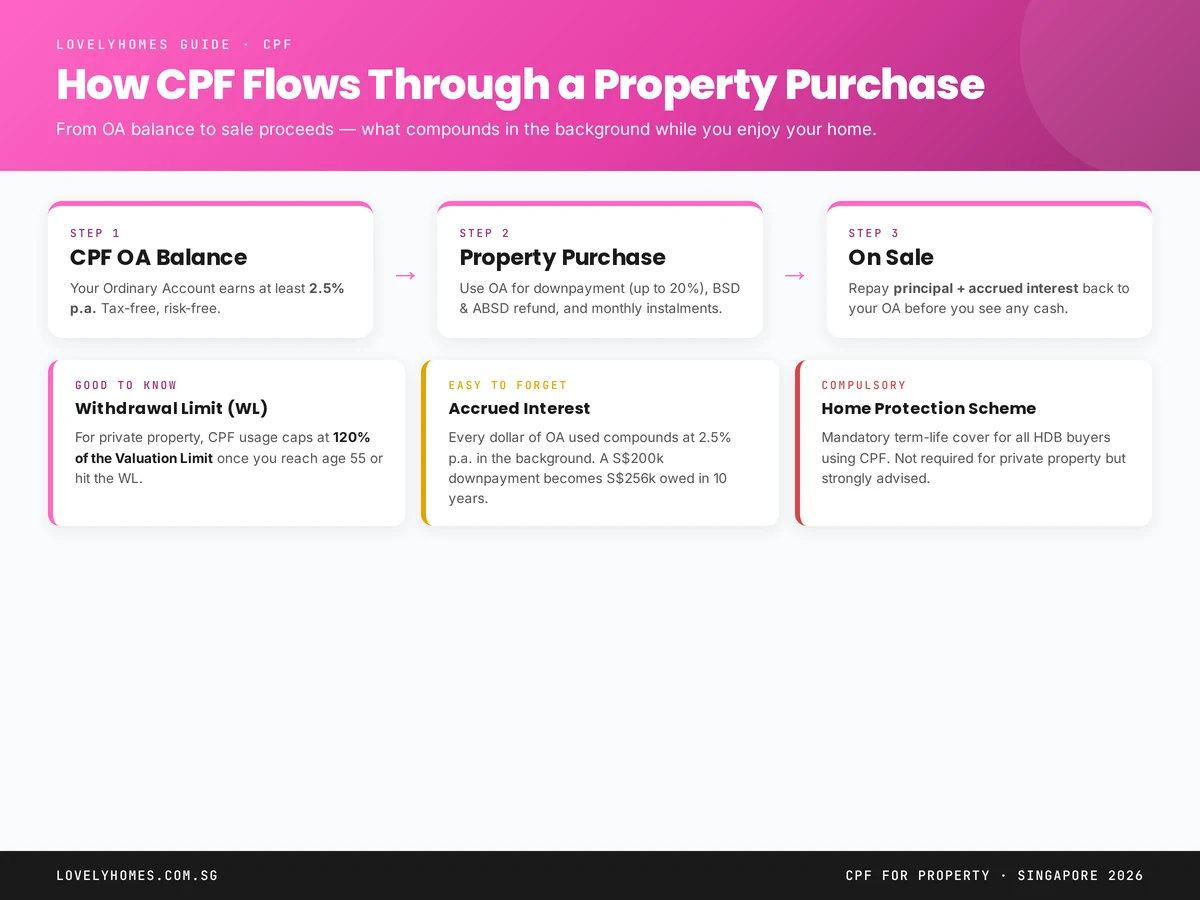

Using CPF for property in Singapore is so routine that most buyers treat the Ordinary Account as a second bank account. That casual mental model is the source of nearly every CPF surprise at resale time — because CPF money put into a home does not behave like cash. It compounds in the background at 2.5% a year and must be repaid, with interest, the moment you sell.

This 2026 guide walks through how CPF flows into a purchase, what the withdrawal and valuation limits actually mean, how accrued interest is calculated, when the Home Protection Scheme is compulsory, and what lands in your pocket when you sell. For the authoritative rulebook, see the CPF Board’s home ownership pages.

Quick Answer — CPF for Property at a Glance

- CPF Ordinary Account (OA) can be used for downpayment, stamp duties, monthly instalments, legal and valuation fees.

- Interest rate: OA earns at least 2.5% per annum — and every dollar used for property continues to accrue at 2.5% in the background until repaid.

- Withdrawal Limit (WL): CPF usage on private property caps at 120% of the Valuation Limit once you reach age 55 or exhaust the WL.

- Home Protection Scheme (HPS): Mandatory term-life cover for HDB buyers using CPF. Not required for private property.

- At sale: Principal plus accrued interest must be refunded to your OA before any cash reaches you.

What You Can Use CPF For

Your CPF Ordinary Account can be deployed at six points in the property journey:

- Downpayment. For an HDB loan, CPF can fully fund the 20% minimum downpayment. For a bank loan, at least 5% must be cash and the remainder (up to 20% for a first property) can come from CPF.

- Buyer’s Stamp Duty (BSD). Payable in cash initially but reimbursable from CPF after stamping.

- Additional Buyer’s Stamp Duty (ABSD). Also reimbursable from CPF after stamping — cash up front, then drawn down from OA.

- Monthly loan instalments. Direct GIRO from OA covers principal + interest. You can choose partial cash/CPF if you want to preserve OA for other uses.

- Legal fees. Conveyancing fees capped at S$675 per transaction are reimbursable from CPF.

- Property tax, renovation, utilities: Not covered by CPF. Always cash.

Valuation Limit, Withdrawal Limit & Why They Exist

CPF imposes two caps on how much OA money can be used for a private property:

- Valuation Limit (VL): the purchase price or valuation of the property, whichever is lower, at the time of purchase.

- Withdrawal Limit (WL): 120% of the Valuation Limit.

Up to the VL, you can use CPF freely. Between the VL and the WL, you can continue using CPF if you are below 55 or above 55 with your Basic Retirement Sum (BRS) set aside. Once the WL is hit, no further CPF can service the property loan — you must switch to cash.

For HDB flats bought with an HDB concessionary loan, the VL/WL framework does not apply in the same way — there is no cap beyond what the loan quantum supports.

Accrued Interest: The Silent Compounding

This is the single most misunderstood part of CPF for property. Every dollar of OA you use for a property is treated as if it had stayed in your OA, continuing to earn 2.5% compounded annually. When you sell, you must refund principal + accrued interest to your OA before any cash reaches your pocket.

Worked example: S$200,000 used over 10 years

Assume you use S$200,000 of CPF OA for your downpayment and contribute another S$1,500/month from OA to servicing the loan. After 10 years:

- Total CPF deployed (downpayment + 120 monthly payments): S$200,000 + S$180,000 = S$380,000

- Accrued interest at 2.5% compounded: approximately S$77,500

- Total refund to OA on sale: roughly S$457,500

If your sale proceeds after repaying the outstanding bank loan are only S$420,000, there is a S$37,500 negative sale — the shortfall is waived but you walk away with no cash, even though the property “made money” in headline terms.

Home Protection Scheme (HPS)

HPS is a term-life insurance scheme administered by CPF that covers the outstanding housing loan in the event of death, terminal illness, or total permanent disability. It is compulsory for HDB buyers using CPF to service the loan.

HPS is not required for private property — bank home loans are typically paired with privately purchased Mortgage Reducing Term Assurance (MRTA) instead. You can compare MRTA against HPS using the illustrative premium tables on the CPF HPS page — for most buyers below 45, privately sourced MRTA is cheaper.

Voluntary Housing Refund (VHR): Paying Down Accrued Interest Early

You can voluntarily refund cash into your OA at any time to reduce the accrued-interest trap. Every dollar you refund stops compounding — effectively giving you a 2.5% risk-free return on that cash. In a 3-4% deposit-rate environment, the maths sometimes wins for your home-loan net position; in a 0.5% environment, it is a clear winner.

VHR is especially useful in the final 3–5 years before a planned sale, when accrued interest is compounding hardest. Speak to your CPF servicing officer before making a lump sum refund.

CPF at 55: What Changes

At 55, two things shift:

- The Retirement Account (RA) is created and funded with your Full Retirement Sum (FRS) — or Basic Retirement Sum (BRS) if you own property and pledge it.

- OA usage for property becomes capped at the 120% Withdrawal Limit, and only if FRS/BRS is already met in the RA.

For most homeowners near 55 with significant mortgages, this means they transition to cash servicing for instalments. Plan for this 5 years ahead.

Frequently Asked Questions

Can I use CPF OA to pay ABSD?

Yes, but only as a reimbursement after you have paid the ABSD in cash and the property has been stamped. You cannot draw CPF directly to IRAS.

What happens to accrued interest if I die?

Accrued interest is written off on death. The CPF member’s nominees inherit whatever is in the OA at that time; no refund from the property is required.

Can I use my CPF OA to buy a second property?

Yes, once the Full Retirement Sum has been set aside in your RA (at 55) or if you are below 55 — but CPF usage on the second property only kicks in after you reach the Basic Retirement Sum for the first.

Does accrued interest continue to compound after I pay off the loan?

Yes. As long as the property is in your name and CPF money has been used, accrued interest compounds until sale or your death.

Is there any way to avoid HPS?

Applications to opt out are considered only if you have equivalent private insurance covering the loan. CPF assesses case-by-case — the default position is compulsory participation.

What to Do Next

CPF shapes not just affordability but also upgrade strategy and retirement planning. Your next reads:

- TDSR & MSR 2026: Home Loan Affordability Explained — how much your CPF + income actually borrows.

- HDB Loan vs Bank Loan — CPF usage differs between the two.

- CPF for Property — more deep dives on CPF’s role in housing.

Disclaimer: This guide is for general information and not financial advice. CPF policies are updated regularly. Verify current rules on cpf.gov.sg and speak to a licensed financial adviser before making CPF-related property decisions.