Bayshore Drive GLS Tender Closes: What It Means for D16 East Coast Property (July 2026)

📌 Quick Answer — Bayshore Drive GLS Tender Closes (15 July 2026)

- URA closed the tender for its Government Land Sales site at Bayshore Drive today, 15 July 2026. The site was launched for public tender on 30 March 2026.

- Bids have been received from developers; URA will evaluate them before announcing the award — expected within four to six weeks of the tender closing date.

- Bayshore Drive is in District 16 (East Coast / Bedok), adjacent to the Bayshore Road corridor served by Bayshore MRT station on the Thomson-East Coast Line (TEL), which opened in December 2023.

- The award will reveal land rates — the price per square metre of permissible Gross Floor Area (GFA) — which imply future launch prices and signal developer confidence in the Bayshore precinct’s long-term potential.

- URA’s Bayshore planning vision includes high-rise residential development near the waterfront, improving public transport connectivity and green corridors to East Coast Park.

- Comparable nearby GLS awards: Peck Hay Road (D09, June 2026) awarded at approximately S$18,600 psm GFA; River Valley Green Parcel C (D09, June 2026) awarded at S$18,622 psm GFA. D16 awards will be significantly lower.

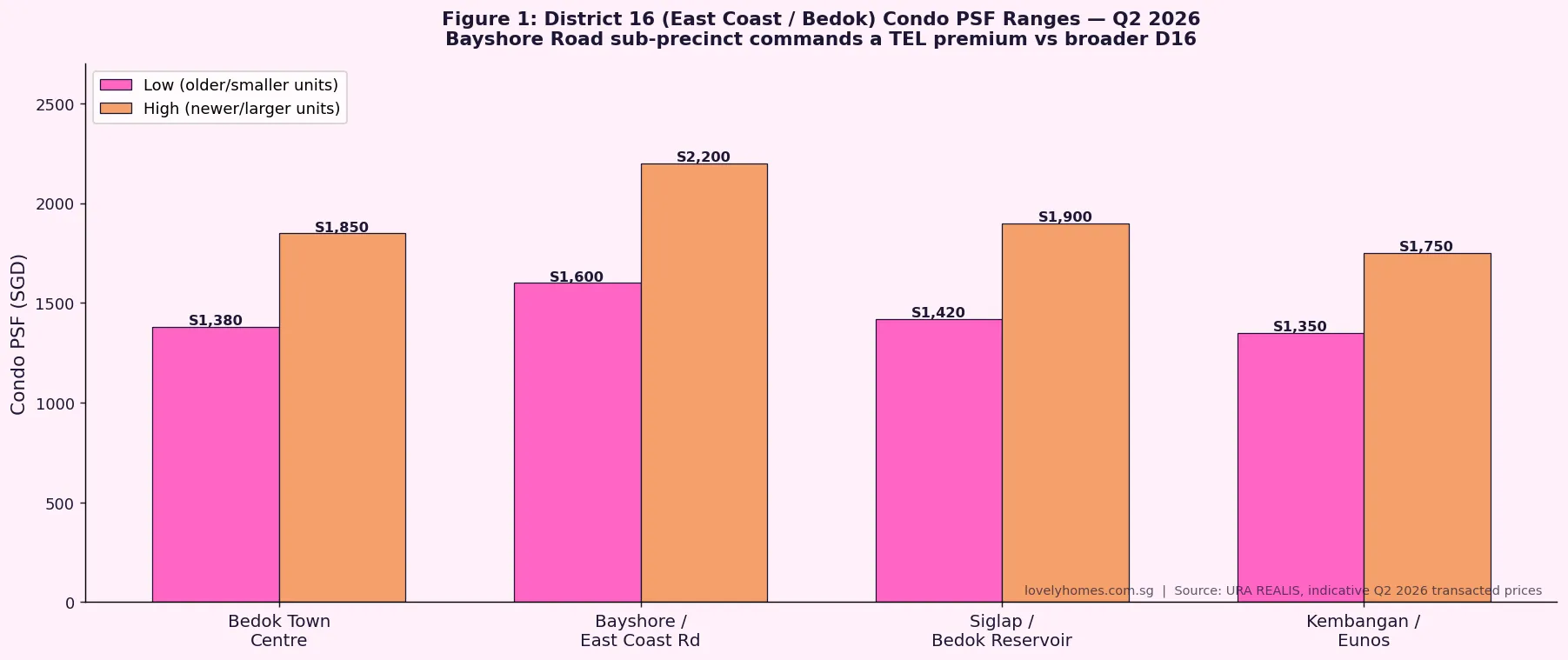

- Condo PSF in the Bayshore / East Coast Road sub-precinct currently ranges from S$1,600 to S$2,200 psf (Q2 2026), a premium over broader Bedok at S$1,380–S$1,850 psf, driven by the TEL connectivity uplift.

The Urban Redevelopment Authority (URA) confirmed on 15 July 2026 that it has closed the tender for its sale site at Bayshore Drive and received bids from developers. The site was launched for sale on 30 March 2026 as part of URA’s Government Land Sales (GLS) programme. The formal award decision will be made after URA evaluates all bids and is expected to be publicised within weeks.

For property watchers tracking Singapore’s East Coast corridor and District 16, this tender closing is a significant data point: the eventual award will reveal how bullish developers are on the Bayshore precinct’s long-term value, anchor a price floor for future launches in the area, and signal what residents and investors can expect from new developments in this rapidly evolving part of Singapore.

What Is the Bayshore Drive GLS Site?

The Bayshore Drive site is located in the Bayshore planning precinct, a stretch of District 16 between East Coast Parkway and the Bedok Reservoir corridor. The precinct sits at the end of the Thomson-East Coast Line’s Stage 3 extension, with Bayshore MRT station — opened in December 2023 — providing direct rail access to the Marina Bay Financial Centre (approximately 18 minutes), Orchard Road (approximately 22 minutes), and Marina South Pier.

URA’s 2019 Master Plan and subsequent Draft Master Plan 2025 envision Bayshore as a “car-lite, waterfront-connected” residential precinct with mid-to-high-rise residential towers, enhanced pedestrian links to East Coast Park, and a network of cycling paths. The precinct is designed to be compact and walkable, with community amenities sited within walking distance of the MRT. It is one of several new waterfront residential clusters — alongside Marina South, Mount Pleasant, and Jurong Lake District — that URA is actively seeding through the GLS programme.

Why the Award Will Matter for D16 Property

GLS award prices set a cost floor for developers — they must build, sell, and profit above the land cost. Historically, each S$1,000 psm GFA in land cost translates to roughly S$150–S$200 psf in final launch price, depending on development intensity and construction costs. When URA announces the Bayshore Drive award, it will include the site area, maximum GFA, and the award price per square metre GFA — all of which allow market-watchers to estimate the developer’s minimum viable launch PSF.

Current condo transactions in the Bayshore Road corridor — covering developments such as Costa Del Sol, The Bayshore, and One Amber — show transacted PSF of approximately S$1,600–S$2,200 in Q2 2026. The higher end of this range reflects newer, well-maintained units near the MRT; the lower end reflects older developments with shorter remaining leasehold tenure. A new development on the Bayshore Drive GLS site, built on a 99-year lease commencing 2026–2027, would likely target a launch PSF of S$2,200–S$2,600 depending on the land rate achieved, construction cost escalation, and developer margin requirements.

GLS Site Summary

| Parameter | Detail |

|---|---|

| Site location | Bayshore Drive, District 16 (East Coast / Bedok) |

| Nearest MRT | Bayshore MRT (TEL Stage 3, opened Dec 2023) |

| Tender launched | 30 March 2026 |

| Tender closed | 15 July 2026 |

| Bids received | Yes (number and amounts to be published with award) |

| Award expected | Approximately 4–6 weeks from 15 July 2026 |

| Tenure | 99 years leasehold (expected) |

| Comparable award: RVG Parcel C (Jun 2026) | S$18,622 psm GFA (D09 CCR) |

| D16 condo PSF range (Q2 2026) | S$1,380–S$2,200 psf depending on sub-area and age |

The TEL Effect: Why Bayshore Commands a Premium Over Broader Bedok

The Thomson-East Coast Line has been one of the most significant infrastructure catalysts for District 16 property values since the Cross Island Line announcement in 2019. Bayshore station — situated on the TEL’s Stage 3 extension — provides a single-seat ride to Gardens by the Bay East, Marina Bay Financial Centre, Shenton Way, and Caldecott (where the TEL intersects with the Circle Line and North-South Line). For East Coast residents who previously depended on buses and the EWL interchange at Tanah Merah, the TEL has materially reduced commute times to the CBD.

Industry analysis of TEL-adjacent transactions suggests a 10–20% PSF premium for units within 400 metres of a TEL station, compared with otherwise comparable units further away. This premium has been sustained since Bayshore station opened in December 2023 and shows no sign of diluting, as demand from young professionals working in the CBD has remained firm.

What Might Come Next

Once URA announces the Bayshore Drive award — likely in August or September 2026 — market-watchers will have a clearer sense of how bullishly the successful developer has priced the land. A high land bid (above S$10,000 psm GFA, which would be the implied benchmark for an OCR/RCR D16 waterfront site) would signal strong developer confidence and likely push neighbouring resale prices higher as buyers anticipate a premium new launch competitor. A more modest land rate would suggest developers are cautious about launching above the S$2,200 psf threshold in a market where OCR softening was a theme in the first half of 2026.

LovelyHomes will report on the award the day it is published by URA. Sign up for our property news alerts to be notified when the Bayshore Drive GLS award is announced.

Frequently Asked Questions

What is the GLS tender process and when will the Bayshore Drive award be announced?

Under Singapore’s GLS programme, URA invites developers to submit sealed bids for a site during a specified tender period. After closing, URA evaluates each bid on price and compliance with tender conditions. The awarded bidder is typically the highest compliant bid. URA normally announces the award within four to six weeks of the tender closing — so a Bayshore Drive award can be expected in August or early September 2026. The announcement will include the bid price, site area, maximum GFA, and the developer’s name.

Should I buy in the Bayshore area now or wait for the new launch?

This is a personal financial decision that depends on your budget, loan eligibility, and timeline. Buying an existing resale unit now locks in a price before any award-driven uplift in sentiment. Waiting for the new launch means purchasing a 99-year lease commencing 2026–2027 at a potentially higher PSF, but with the benefits of modern specifications, full warranties, and a fresh lease. First-time buyers should also consider the ABSD implications — if you already own property, a new launch purchase attracts ABSD — versus the grant eligibility for HDB buyers. Consult a licensed financial adviser before making any decision.

What other GLS sites are currently in the pipeline near District 16?

As at July 2026, the Bayshore Drive site is the primary GLS tender in the East Coast corridor. The Kitchener Link site (D08, launched 25 June 2026 as part of the same GLS batch as Lorong Puntong/Sin Ming) is in a different district but relevant for those tracking city-fringe supply. URA’s 2H 2026 GLS programme also includes the landmark Jurong Lake District (JLD) White Site, which closes for tender in November 2026. No other D16 or adjacent OCR sites are currently on the Confirmed List for 2026.

How do developers price new launches relative to the GLS land rate?

Developers price new launches to cover: the land cost (GFA × award rate), construction costs (typically S$350–S$500 psf of Gross Floor Area in 2026), financing costs during construction, and a margin of approximately 10–18%. For a residential site, if the GFA-equivalent land cost is S$1,200 psf and construction adds another S$450 psf, the developer’s breakeven is approximately S$1,800–S$1,900 psf — meaning a launch at S$2,200–S$2,400 psf provides a 15–20% developer margin at that volume. Award prices significantly above or below this range will shift launch pricing accordingly.

Is the Bayshore Drive site near the East Coast Park beach?

Yes. The Bayshore precinct sits between the East Coast Parkway (ECP) and the existing residential belt along Bayshore Road and East Coast Road, with East Coast Park accessible on foot or by cycling path. URA’s plans for the precinct include improved pedestrian connections under or over the ECP to reach the park directly. Future residents of the Bayshore Drive development should have convenient access to the East Coast Park waterfront, Changi Airport cycling trail, and the planned Bayshore Park connector.