Singapore Property Seller Complete Guide 2026: OTP, Valuation, SSD, Agent Fees and Net Proceeds

Quick Answer: Selling Property in Singapore 2026

- Minimum occupation period: 5 years for HDB flats before you can sell on the open market; no MOP for private property.

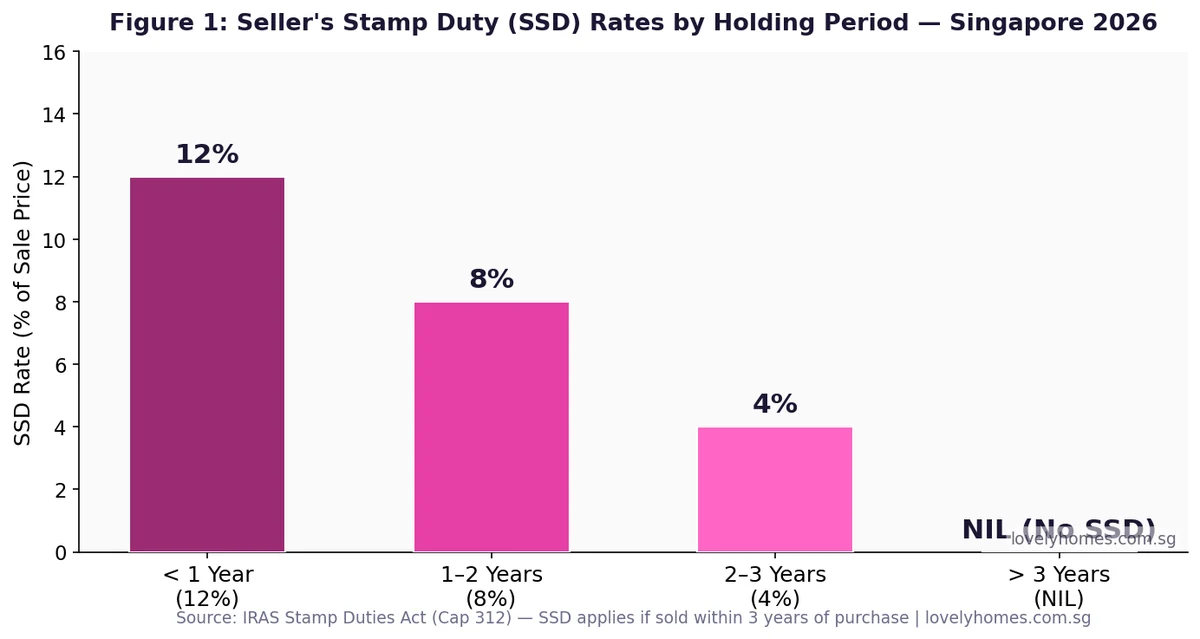

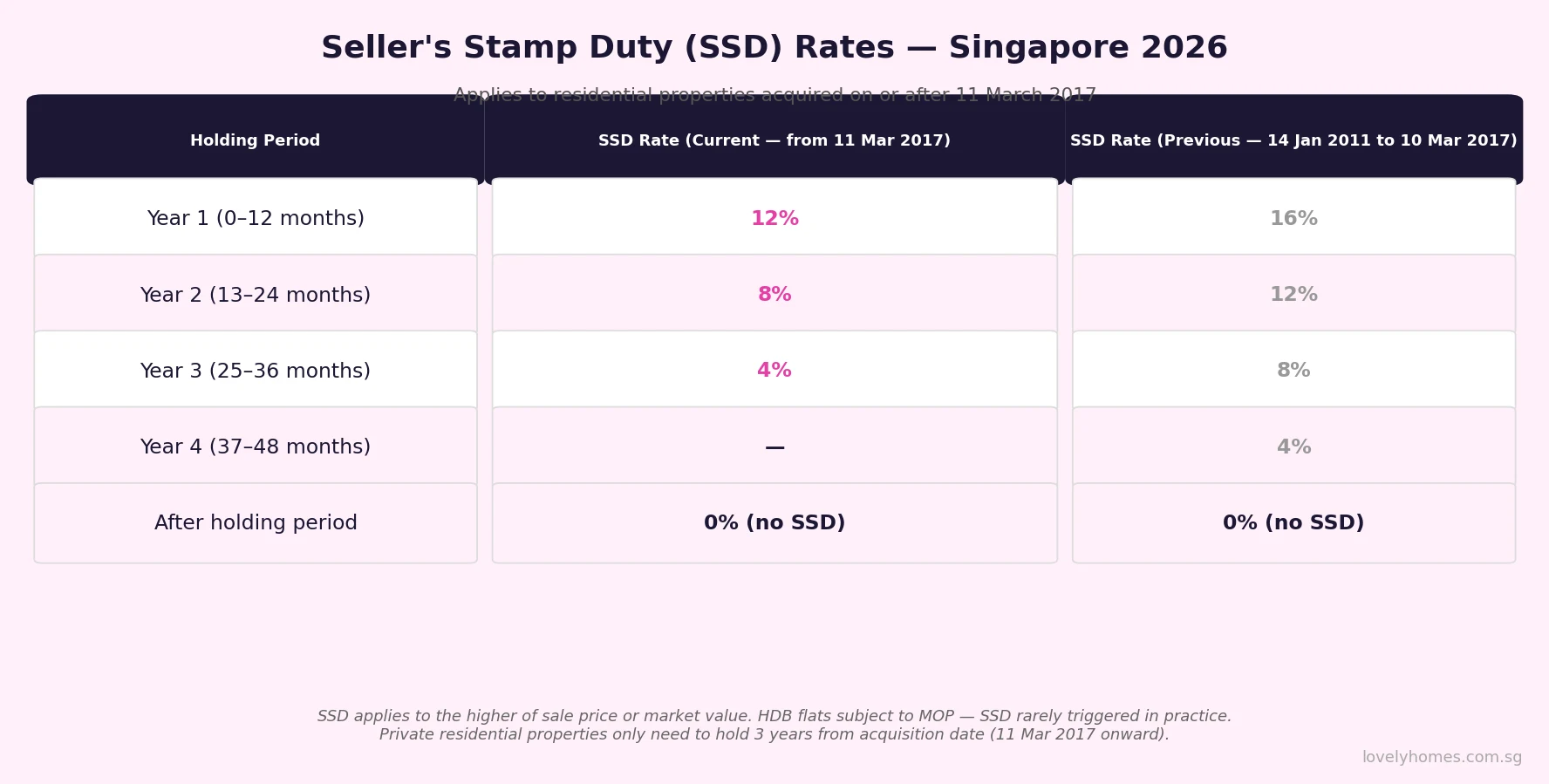

- Seller’s Stamp Duty (SSD): 12% / 8% / 4% / NIL for private property sold within Year 1 / 2 / 3 / 4+ of purchase. HDB flats are exempt from SSD.

- Agent commission: typically 1–2% of sale price for the seller’s agent; 0% for the buyer’s agent (paid by buyer).

- CPF refund: every dollar of CPF used (plus 2.5% p.a. accrued interest) must be returned to CPF at completion — this reduces your cash proceeds.

- OTP process: Seller grants a 14-day Option to Purchase; buyer pays 1% option fee; upon exercise buyer pays another 4–9%.

- Completion timeline: typically 10–16 weeks from OTP grant to key handover; HDB resale takes 8–16 weeks.

- Net proceeds formula: Sale Price − Outstanding Loan − CPF Refund (principal + accrued interest) − SSD − Agent Fee − Legal Fees = Cash in Hand.

- Valuation: Banks and HDB commission independent valuations; if you sell above valuation on an HDB flat the buyer must pay the difference (“Cash Over Valuation”) in cash.

What Does It Mean to Sell Property in Singapore?

Selling a property in Singapore is a structured, legally regulated process administered by the Urban Redevelopment Authority (URA), the Housing and Development Board (HDB), the Inland Revenue Authority of Singapore (IRAS), and the Central Provident Fund Board (CPF). Whether you are selling a Housing and Development Board flat or a private condominium, the transaction follows a defined sequence — Option to Purchase, valuation, loan redemption, stamp duty, CPF refund, legal completion — and each step carries financial consequences that sellers must understand before listing.

In 2026, Singapore’s resale property market is active but more deliberate than the pandemic-era surge. HDB resale transaction volumes have moderated, private resale prices have risen a measured 2–3% year-on-year, and the government’s Seller’s Stamp Duty framework remains in full force. This guide explains the complete selling process from the first decision to sell to the final cash deposit — and equips you to compute your actual net proceeds before you sign anything.

Step 1: Deciding to Sell — Eligibility and Timing

Before listing your property, confirm that you are legally entitled to sell. For HDB flat owners, the critical gate is the Minimum Occupation Period (MOP), which is five years from the date of key collection for most flats. Prime and Plus-classification flats (under the 2023 HDB flat classification framework) carry a ten-year MOP. During the MOP, you may not sell on the open market, rent out the entire flat, or purchase a private residential property in Singapore. Selling before the MOP ends is a serious breach of HDB regulations and can result in compulsory acquisition of the flat.

For private residential properties — condominiums, landed houses, executive condominiums after the five-year privatisation period — there is no MOP. However, the Seller’s Stamp Duty framework imposes a financial penalty for selling within three years of purchase, which effectively discourages short-term flipping.

Once eligibility is confirmed, consider the market context. Check URA’s Private Residential Property Price Index (PPI) and HDB’s Resale Price Index (RPI) for trend data. In Q1 2026, the URA PPI rose 0.9% quarter-on-quarter (+2.63% year-on-year) while the HDB RPI dipped a marginal 0.1% — the first dip since Q2 2019, though volume remains high. Timing your sale to a period of stable or rising prices, and avoiding major political or economic events, is prudent.

Step 2: Valuation — Setting the Right Price

Property valuation in Singapore has two purposes: establishing a credible asking price and satisfying bank loan requirements for the buyer. For HDB flats, HDB commissions valuations through its panel of approved valuers. For private property, banks engage their own valuers (from their panel of approved valuation firms) as a condition of the mortgage loan offer.

As a seller, you may commission your own valuation — at approximately S$300–S$700 depending on property type — to anchor your asking price. This is not compulsory but is advisable for unique properties (high-floor penthouses, large freehold units, unusual configurations) where comparable transaction data is sparse.

For HDB resale, if your agreed transacted price exceeds the HDB-commissioned valuation, the difference — known as Cash Over Valuation (COV) — must be paid entirely in cash by the buyer. COV is non-fundable from CPF or HDB loan proceeds. In the current market, COV for popular estates (Queenstown, Bishan, Buona Vista) can reach S$30,000–S$80,000, while non-mature towns typically transact at or below valuation. As a seller, setting an aspirational price above valuation is legitimate but risks a longer time-on-market.

Step 3: Engaging an Agent — What You Pay and What You Get

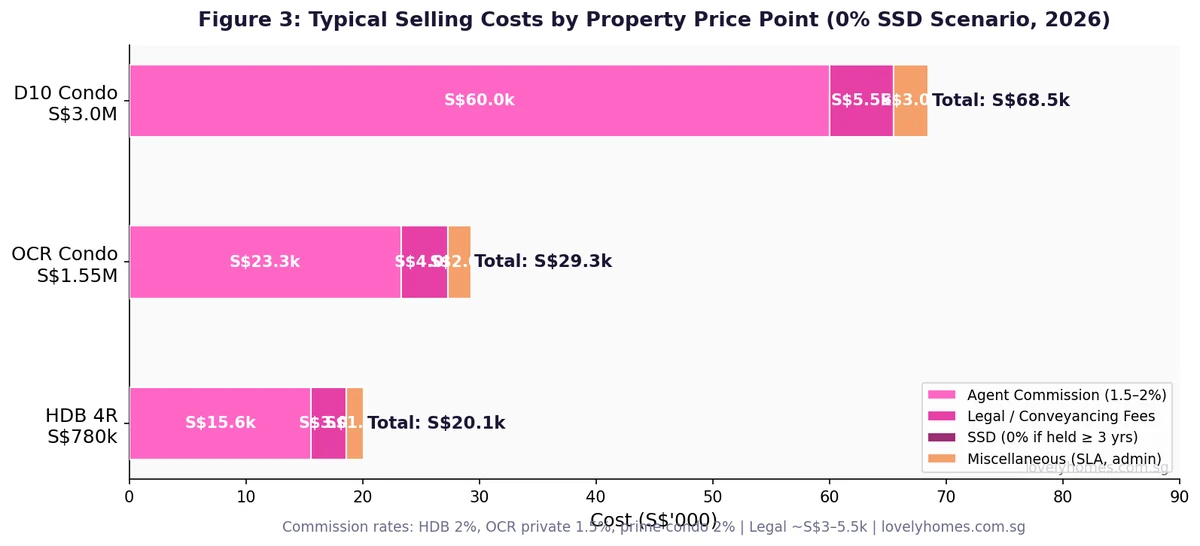

Under the Council for Estate Agencies (CEA) guidelines, property agents must be licensed and registered. CEA introduced major reforms in 2024 requiring co-broking arrangements to be disclosed and prohibiting dual representation without written consent from both parties. As a seller, you typically engage one agent (the “seller’s agent”) and pay that agent a commission of 1–2% of the transaction price, negotiated upfront in a written agreement.

The buyer’s agent commission is typically paid by the buyer, though in practice some co-broking arrangements share the seller’s commission. Always confirm in writing who pays what before signing any engagement letter.

Step 4: Marketing and the Option to Purchase

Once you have signed an exclusive agreement with your agent (usually for 3 months, though non-exclusive arrangements are permissible), your property will be listed on PropertyGuru, 99.co, and SRX. ViewThat, Carousell Property, and direct developer channels are secondary platforms.

When a buyer makes an offer you wish to accept, the transaction proceeds via an Option to Purchase (OTP). The OTP is a standardised legal document — HDB provides its own form; private property uses the CEA-prescribed format or a solicitor-drafted version. Key OTP terms:

| OTP Term | HDB Resale | Private Resale |

|---|---|---|

| Option fee (on grant) | S$1 (symbolic) to S$5,000 max | 1% of agreed price |

| Option exercise period | 21 calendar days | 14 calendar days (customary) |

| Exercise fee (on exercise) | S$5,000 − option fee (HDB loan) or up to 9% (bank loan) | 4% of agreed price |

| OTP validity | 21 days, non-extendable | 14 days; extendable by agreement |

| If buyer does not exercise | Option fee forfeited to seller | Option fee forfeited to seller |

| Administering body | HDB Resale Portal | Law Society / solicitors |

Once the buyer exercises the OTP, the transaction is binding. Both parties must engage solicitors to proceed to legal completion.

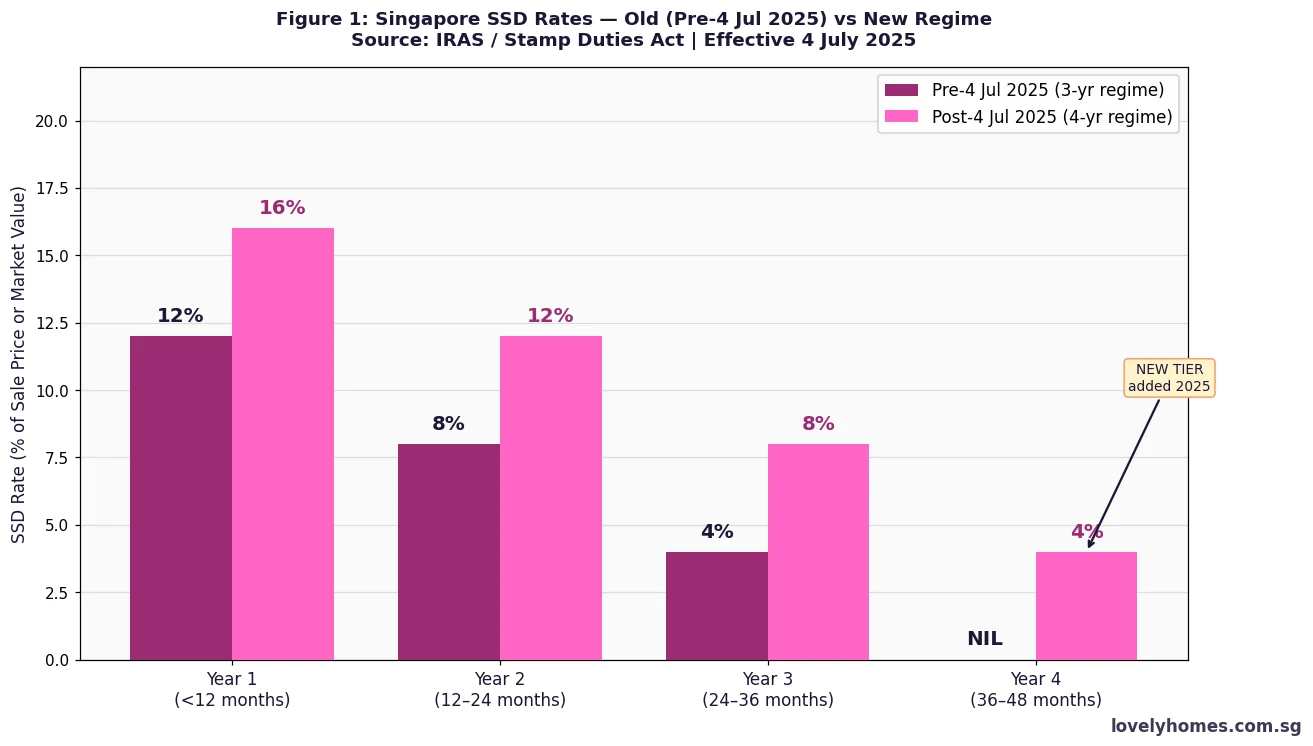

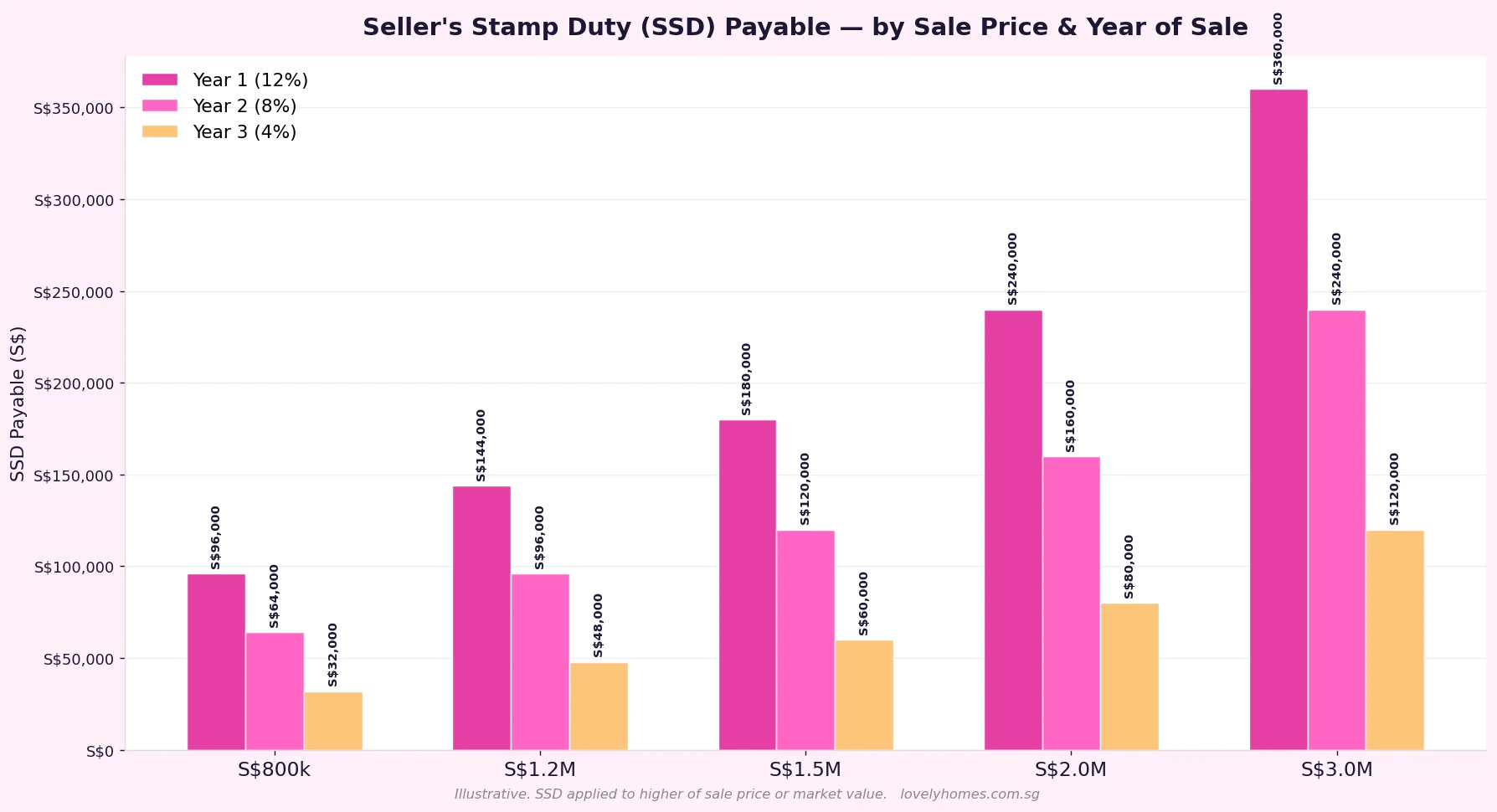

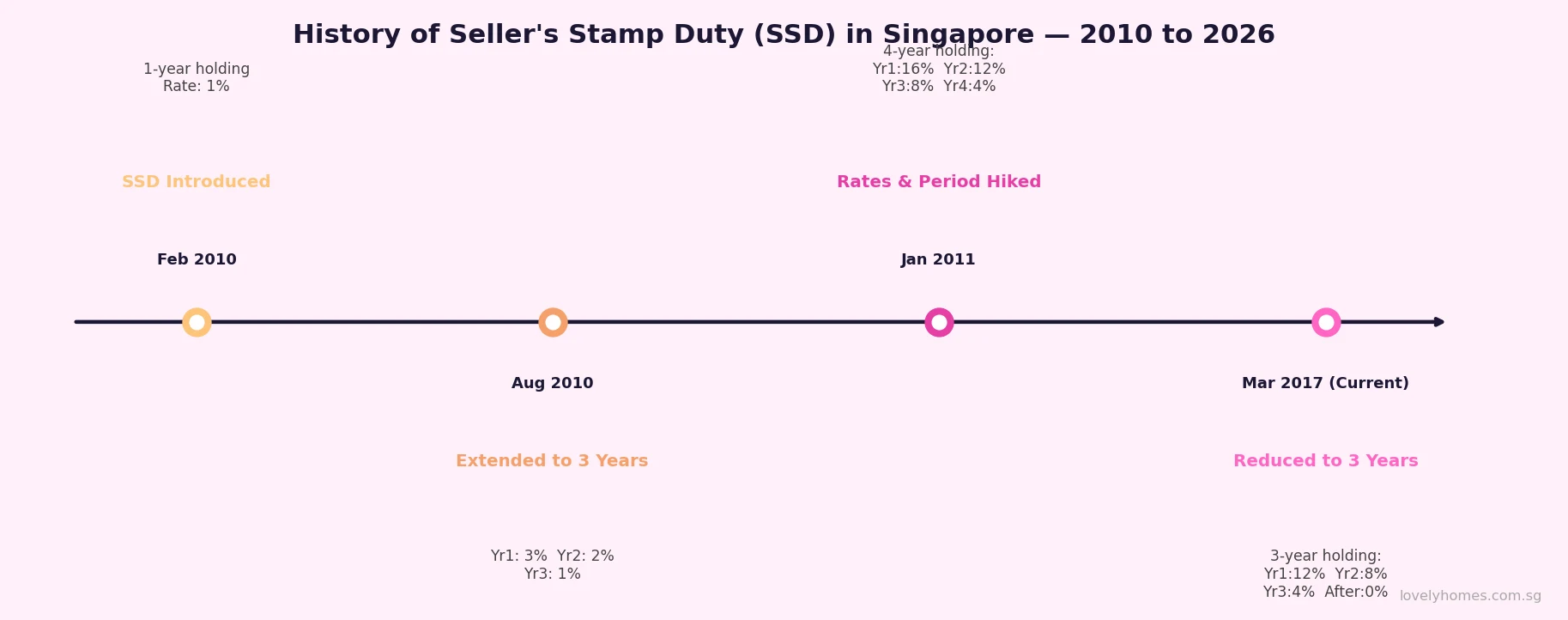

Step 5: Seller’s Stamp Duty — Know Your Exit Cost

The Seller’s Stamp Duty (SSD), administered by IRAS, applies to private residential property sold within three years of acquisition. It is calculated on the higher of the sale price or market value:

| Holding Period | SSD Rate | Example: S$1.5M Sale Price |

|---|---|---|

| Year 1 (within 12 months) | 12% | S$180,000 |

| Year 2 (12–24 months) | 8% | S$120,000 |

| Year 3 (24–36 months) | 4% | S$60,000 |

| Year 4 and beyond | NIL | S$0 |

SSD does not apply to HDB flats. For private property sellers, SSD must be paid within 14 days of the option exercise date. It cannot be funded from CPF and is payable in cash. Failing to pay SSD on time incurs a penalty of up to four times the duty owed.

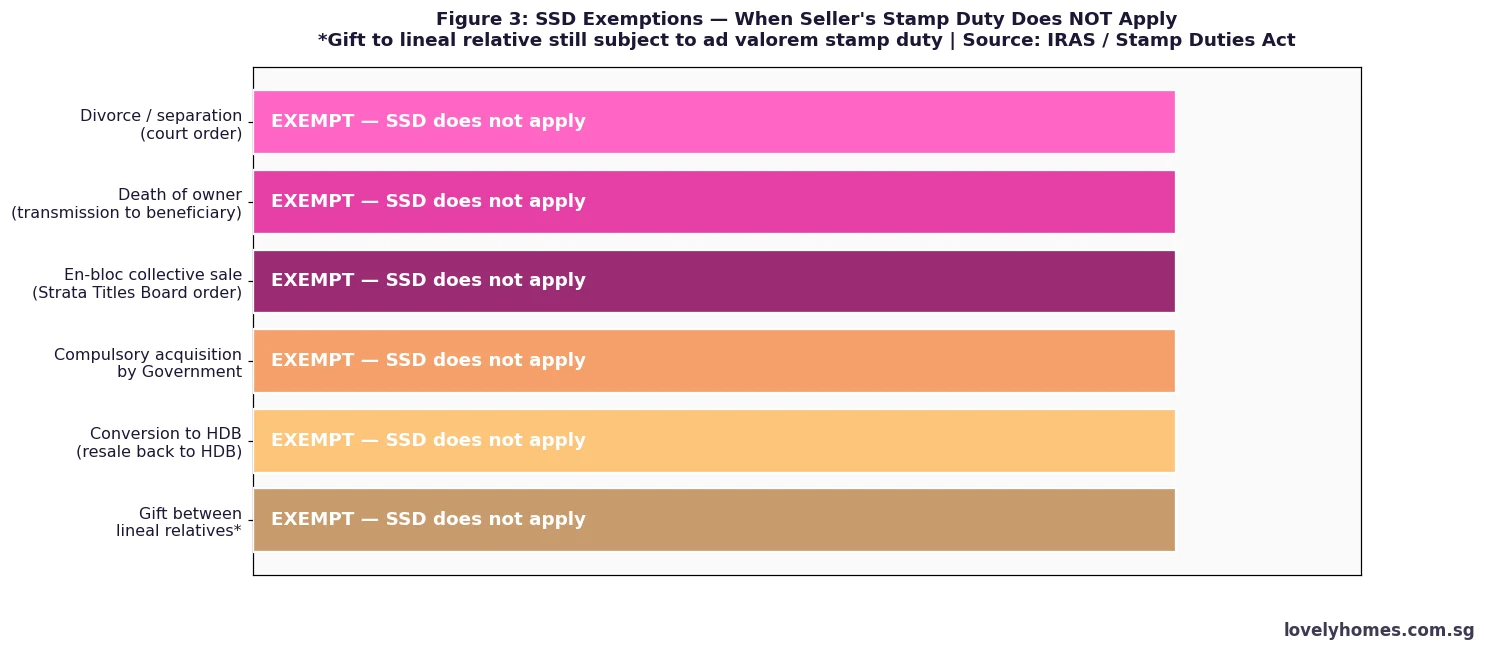

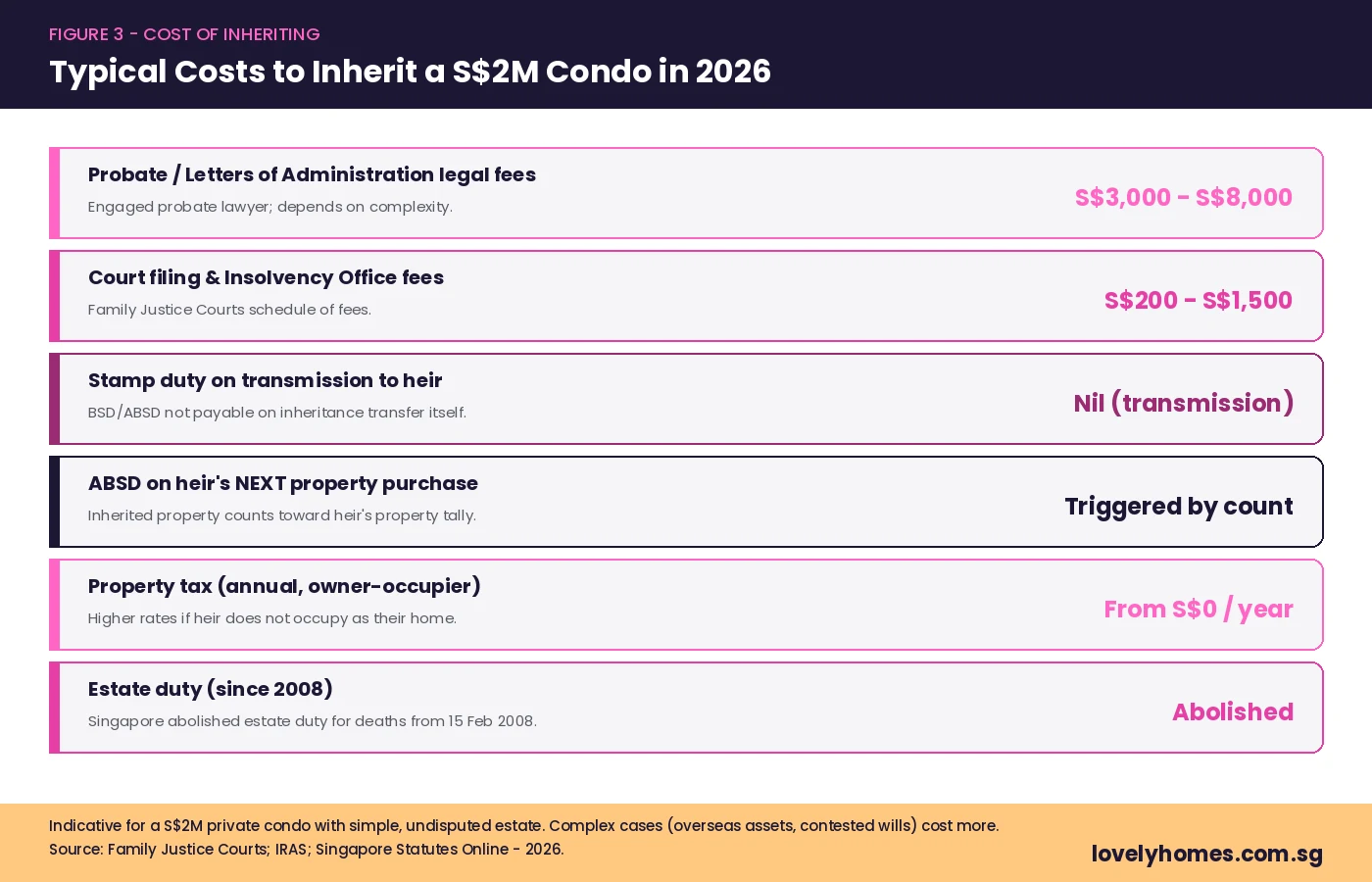

Exemptions exist for inherited property (where the holding period restarts from the date of inheritance), court-ordered sale, and transfers pursuant to divorce proceedings. Check IRAS’s e-Stamping portal for the precise holding period calculation — the clock starts from the date of OTP exercise, not the date of completion.

Step 6: CPF Refund — The Cost That Surprises Most Sellers

If you used CPF Ordinary Account (OA) savings to fund your property purchase — whether for the down payment, monthly mortgage instalments, or BSD — you are required by the CPF Act to return the full amount withdrawn, plus accrued interest at the CPF OA rate of 2.5% per annum compounded annually. This refund is deducted from your sale proceeds at completion and credited back to your CPF OA. It does not go to you in cash.

The accrued interest calculation compounds monthly over the period you held the property. On a S$300,000 CPF withdrawal held for ten years, accrued interest amounts to approximately S$83,000 — meaning S$383,000 is refunded to CPF, not the original S$300,000. Many sellers underestimate this figure and are surprised to find their cash proceeds are far lower than expected.

CPF Board’s online CPF Property Withdrawal Statement is the authoritative source for your specific CPF amount to be refunded. Request this before accepting an offer so you can compute net proceeds accurately.

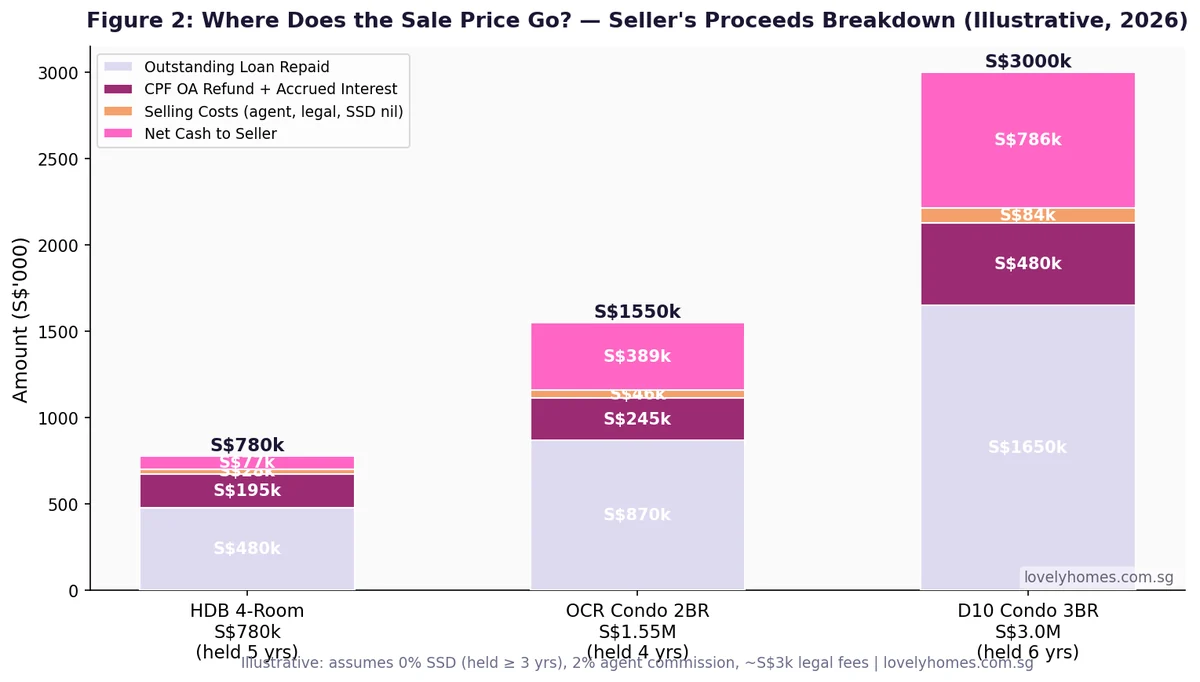

Step 7: Computing Your Net Proceeds

Your actual cash payout at completion is not your sale price. The correct formula is:

| Item | Example: HDB 4-Room S$850K Sale | Example: Condo OCR 3BR S$1.8M Sale |

|---|---|---|

| Sale Price | S$850,000 | S$1,800,000 |

| Less: Outstanding HDB/Bank Loan | −S$0 (paid off) | −S$560,000 |

| Less: CPF Refund (principal + accrued) | −S$420,000 | −S$630,000 |

| Less: Agent Commission (1%) | −S$8,500 | −S$18,000 |

| Less: Legal Fees (seller’s solicitor) | −S$3,000 | −S$5,500 |

| Less: Seller’s Stamp Duty (if applicable) | NIL (HDB exempt) | NIL (held >3 yrs) |

| Net Cash Proceeds | S$418,500 | S$586,500 |

Note that the CPF refund goes back into your CPF OA, not your bank account. If you plan to use CPF again for your next property purchase, this is neutral — but if you need cash liquidity (for retirement or other purposes), plan around this constraint.

Worked Example: The Lim Family Sell Their Tampines 5-Room HDB

Scenario

Mr and Mrs Lim, both Singapore Citizens in their early 50s, purchased their Tampines 5-room HDB flat in July 2019 for S$530,000. They took an HDB loan of S$477,000 at 2.6% per annum over 25 years. They have made regular monthly CPF contributions to service the mortgage. They are now upgrading to an OCR condominium and wish to sell the flat in July 2026 (exactly 7 years’ hold, MOP fully satisfied).

Sale agreed: S$785,000 (a COV of approximately S$18,000 above the HDB-commissioned valuation of S$767,000)

Outstanding HDB loan at completion: approximately S$362,000 (after 7 years of repayments)

CPF OA used (principal withdrawn): S$148,600

CPF accrued interest @ 2.5% over 7 years: approximately S$27,400

Total CPF refund to CPF OA: S$176,000

Agent commission (1%): S$7,850

Seller’s legal fees: S$2,800

SSD: NIL (HDB exempt)

Net cash proceeds: S$785,000 − S$362,000 − S$176,000 − S$7,850 − S$2,800 = S$236,350 cash in hand

Additionally, S$176,000 is credited to their CPF OA — available for the next property purchase.

Total equity released: S$236,350 cash + S$176,000 CPF = S$412,350 — significantly less than the S$785,000 sale price, illustrating why understanding the net proceeds formula is essential before committing to an upgrade.

What This Means for You: Key Considerations Before Selling

Singapore’s property market has historically rewarded patient long-term ownership. The government’s SSD framework, CPF accrued interest rules, and agent commission structure all work in the same direction: discouraging short-term transactions and encouraging owners to hold property for meaningful periods. Before deciding to sell, ask yourself:

- Have you satisfied MOP? (HDB sellers only — non-negotiable)

- Is SSD payable? (Private sellers within 3 years of purchase — calculate the cost against your expected gain)

- What is your actual CPF refund? (Get the exact figure from CPF Board before accepting any offer)

- Do you have a replacement housing plan? (If selling HDB and upgrading to private, the 15-month wait-out period applies if you buy first)

- Is the market timing favourable? (Track URA PPI and HDB RPI quarterly; selling in a rising quarter often justifies a short delay)

What Might Come Next: Singapore Property Market and Seller Policy Outlook

As at mid-2026, there are no credible signals of an SSD rate change or new seller-specific cooling measures. The government has consistently stated that the existing ABSD-SSD-TDSR framework is sufficient to manage speculative demand. The more likely policy development affecting sellers is the ongoing refinement of the HDB flat classification system (Standard / Plus / Prime), which introduces a subsidy clawback on resale if the flat is sold within the enhanced MOP.

For the second half of 2026, the primary variable affecting seller proceeds is interest rate direction. If the US Federal Reserve continues its easing cycle (as widely anticipated), Singapore mortgage rates — priced off SORA — should trend modestly lower, improving buyer affordability and potentially supporting seller-side pricing power in Q3 and Q4 2026. The URA Q2 2026 Flash Estimates, expected in the first week of July 2026, will provide the next definitive data point on private residential price momentum.

Summary: Seller’s At-a-Glance Table

| Item | HDB Flat | Private Property |

|---|---|---|

| Minimum Occupation Period | 5 years (standard); 10 years (Plus/Prime) | None |

| Seller’s Stamp Duty | Exempt | 12% / 8% / 4% / NIL (Yrs 1–4+) |

| Agent commission (seller pays) | 1–2% negotiable | 1–2% negotiable |

| Legal fees (seller) | ~S$2,500–S$4,000 | ~S$3,500–S$8,000 |

| CPF accrued interest | 2.5% p.a. compounded on all CPF used | 2.5% p.a. compounded on all CPF used |

| OTP option period | 21 days | 14 days (customary) |

| Completion timeline | 8–14 weeks from OTP exercise | 10–16 weeks |

| Key regulator | HDB (flat) + IRAS (stamp duty) + CPF Board | URA + IRAS + CPF Board |

| Administering portal | HDB Resale Portal | SLA e-lodgement + IRAS e-Stamping |

Frequently Asked Questions

Can I sell my HDB flat if I still have an outstanding HDB loan?

Yes. At completion, your solicitors will arrange for the outstanding HDB loan to be repaid from your sale proceeds. HDB provides a “Loan Balance Statement” that gives the exact redemption figure as at the completion date. You do not need to clear the loan before listing — the redemption is handled at the point of legal completion. However, if the outstanding loan and CPF refund together exceed your sale price, you may have a “negative sale” — meaning you would owe money at completion. This is rare but possible if you purchased at a high price and have not held long enough for equity to build. Always compute your net proceeds before committing.

What happens if I sell my property at a loss — do I still pay CPF accrued interest?

Yes, with an important exception. If your sale proceeds are insufficient to cover the full CPF refund (principal + accrued interest), CPF Board will only recover what is available from the proceeds. The shortfall is waived — you are not personally liable to make up the difference from other savings. However, if you took a bank loan and the bank’s outstanding loan is redeemed first (which is typical), the CPF amount recovered may be further reduced. This scenario arises in cases of significant negative equity, usually only following a sharp market correction or after a very short holding period with SSD also payable. For most long-term sellers, selling at a nominal loss after holding for many years is uncommon in the Singapore market, but not impossible in specialised segments like commercial shophouses or declining lease leasehold properties.

Do I need a lawyer to sell my property in Singapore?

Yes. Unlike some jurisdictions where private sales without solicitors are possible, Singapore requires conveyancing solicitors for all property transactions. As a seller, you must engage a Singapore-qualified solicitor (or a law firm with a licensed conveyancing practice) to handle the title transfer, prepare the completion documents, redeem your outstanding mortgage, arrange the CPF refund, and liaise with the buyer’s solicitors. Solicitor fees for a seller typically range from S$2,500 to S$8,000 depending on property type, transaction complexity, and whether a mortgage is involved. Always obtain a fee quote from at least two firms before engaging. The Law Society of Singapore maintains a directory of licensed conveyancing lawyers at lawsociety.org.sg.

What is the 15-month wait-out period and how does it affect HDB sellers who want to buy private?

The 15-month wait-out period, introduced in September 2022, requires that Singapore Citizens and Permanent Residents who own an HDB flat — or who have sold an HDB flat — must wait 15 months from the date of the HDB flat sale before purchasing a private residential property. The measure was designed to prevent HDB sellers from immediately using sale proceeds to compete in the private market, which was driving up private prices. If you sell your HDB flat in July 2026, you cannot exercise an OTP for a private property until October 2027 at the earliest. Note that the wait-out period applies from the date of HDB sale completion, not the date of OTP grant. Buying under a spouse’s name alone does not avoid the restriction if the spouse also owns or has owned an HDB flat. Check with your solicitor for any exemptions applicable to your specific circumstances (e.g., purchase of a completed private property where the OTP was granted before the HDB sale was completed, subject to specific conditions).

Can I grant an OTP while my flat is still within the MOP?

No. HDB does not allow you to grant an OTP, list on the open market, or accept any purchase deposit while the MOP is still running. Any such agreement would be void and could expose both buyer and seller to HDB enforcement action. For HDB resale, the HDB Resale Portal is the official platform for registering the OTP — it will reject submissions where the MOP has not been satisfied. The MOP clock starts from the date of flat purchase (key collection), not from the date of legal completion. For PLH (Prime Location Public Housing) and Plus flats launched from 2023 onwards, the enhanced MOP is ten years.

What is Cash Over Valuation (COV) and is it normal to pay it?

COV is the amount by which the agreed transaction price of an HDB resale flat exceeds HDB’s commissioned valuation. It must be paid entirely in cash by the buyer — it cannot be funded from CPF or HDB loan proceeds. COV is legal and common in desirable estates (mature towns, near MRT, high floors) but can range from zero to over S$100,000 depending on market conditions and unit specifics. As a seller, setting a price that implies COV is your right, but it narrows your buyer pool to those with sufficient cash reserves. In 2026, COV is present in popular estates but has moderated from the elevated levels seen during the 2021–2023 market peak. HDB publishes quarterly resale transaction data which allows you to benchmark transacted prices by block and floor range before setting your asking price.

When is the best time of year to sell property in Singapore?

Historically, the Singapore property market sees higher transaction volumes in Q2 (April–June) and Q3 (July–September), with Q4 (October–December) being softer as the year-end holiday period approaches and buyers delay decisions. The Chinese New Year period (January–February) is typically the quietest. However, market-wide price trends matter far more than seasonal patterns — selling in a rising market at any time of year will generally yield better proceeds than selling in a falling market during the “peak” season. If you have flexibility, tracking URA PPI and HDB RPI quarterly and listing when momentum is positive is more impactful than calendar timing. In 2026, the private market is in a modest uptrend with URA PPI at +0.9% QoQ in Q1; the Q2 flash estimates (expected July 2026) will indicate whether momentum is sustained.