HDB Ethnic Integration Policy (EIP) Singapore 2026: Quotas, Eligibility and What Buyers Must Know

⚡ HDB EIP at a Glance — Quick Answer

- What it is: The HDB Ethnic Integration Policy (EIP) is a quota system introduced in 1989 to maintain racial integration in HDB estates by capping the proportion of each ethnic group in any given block and neighbourhood.

- Who administers it: HDB (Housing & Development Board), under the Ministry of National Development.

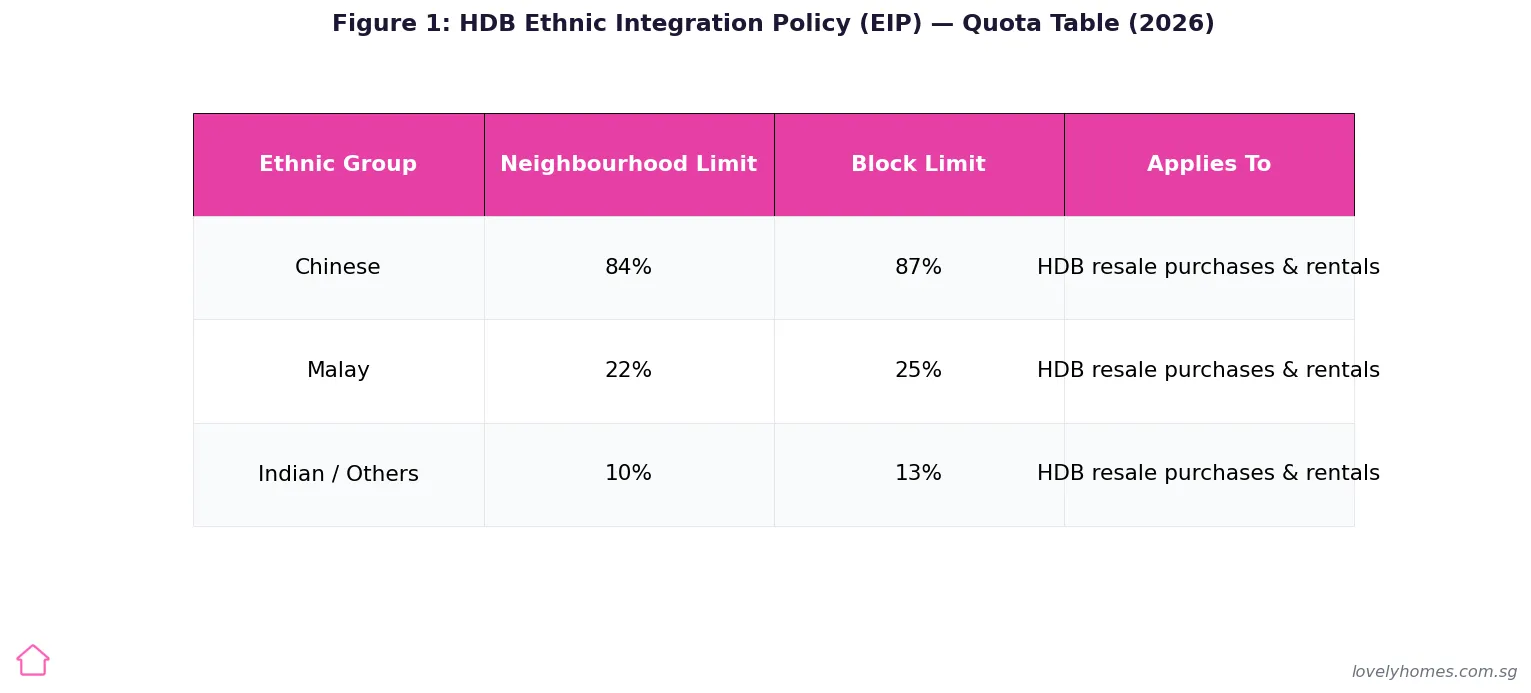

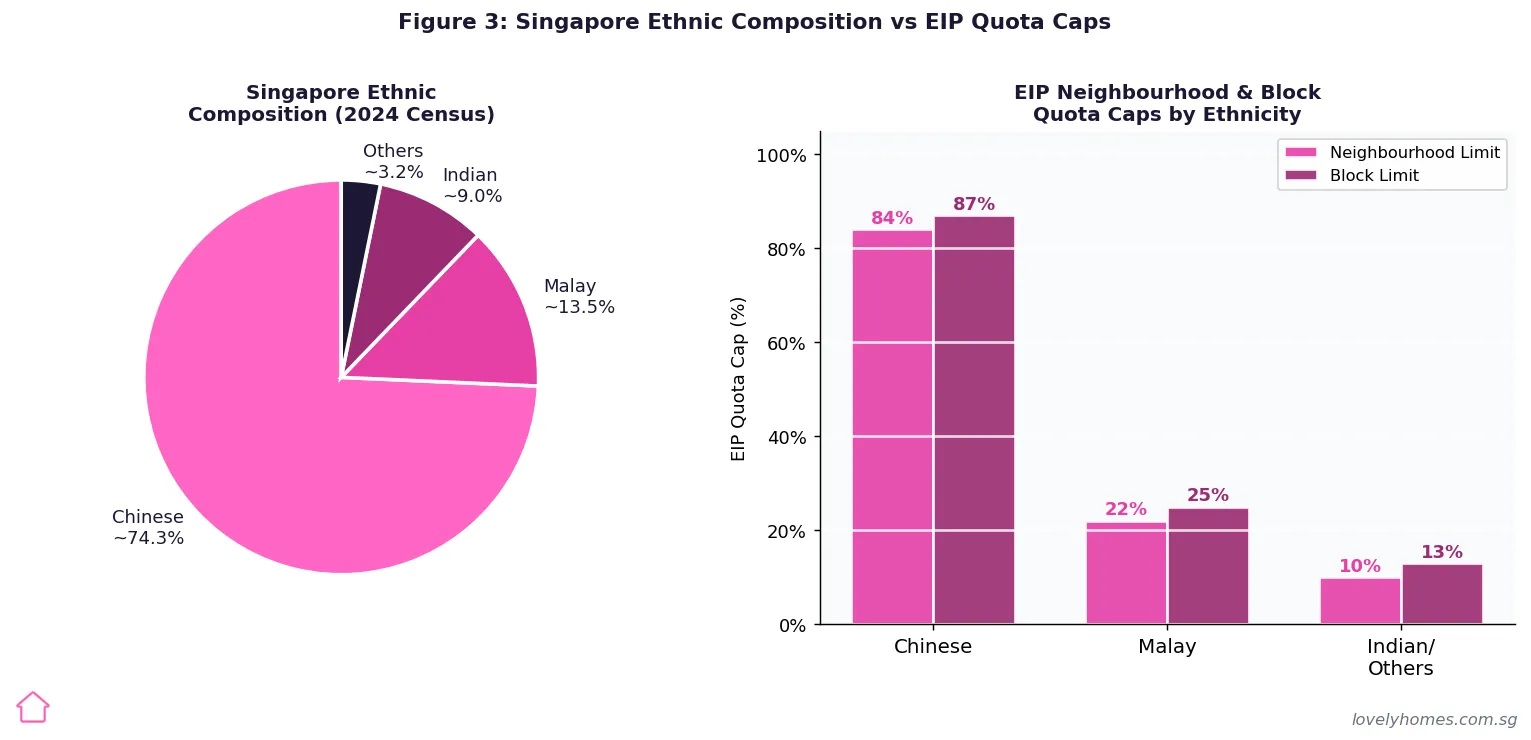

- Quota limits: Chinese — 87% (block) / 84% (neighbourhood); Malay — 25% / 22%; Indian/Others — 13% / 10%.

- Who is affected: Anyone buying or renting an HDB resale flat in Singapore — Singapore Citizens (SCs), Singapore Permanent Residents (SPRs), and HDB flat owners renting out.

- Key risk: If a block or neighbourhood has reached the quota for your ethnic group, you cannot complete the resale purchase for that flat, even after exercising the OTP.

- How to check: Via the HDB Resale Portal or by calling HDB directly — always check before signing any Option to Purchase (OTP).

- SPR angle: SPRs face an additional SPR Quota (SPR households cannot exceed 5% of flats per block and 8% per neighbourhood) on top of the EIP.

- Rental applies too: HDB flat owners must also comply with EIP quotas when renting out their flat or bedrooms.

When Singaporeans buy an HDB resale flat, most focus on price, lease, and proximity to amenities. Far fewer remember to check the Ethnic Integration Policy (EIP) — until they discover, after exercising the Option to Purchase, that the block has already met the quota for their ethnic group.

The EIP is one of Singapore’s most consequential yet least-explained housing policies. Introduced in 1 March 1989 by the HDB under the Ministry of National Development, it was designed to prevent the racial self-segregation that had been emerging in certain estates — a pattern the government concluded was contrary to Singapore’s long-term social cohesion. The policy works by capping the proportion of each ethnic community in any given HDB block and neighbourhood, effectively requiring that no single group dominates any residential area.

For property buyers and sellers, the EIP creates a real constraint: it can limit the pool of eligible buyers for your flat and, conversely, rule out flats you want to purchase. Understanding how it works — and how to check before you sign — is essential for anyone navigating the HDB resale market in 2026.

Origins and Policy Background

By the late 1980s, HDB estates had begun to show ethnic clustering — not through any discriminatory housing allocation, but through the natural tendency of communities to live near one another. Surveys showed that certain blocks in Queenstown and Toa Payoh were becoming more than 90% Chinese or more than 80% Malay. The government, mindful of the 1964 and 1969 racial riots in Singapore’s early independence years, concluded that residential segregation — even voluntary — risked weakening inter-ethnic relationships over time.

The EIP was the policy response. From 1 March 1989, every HDB resale transaction required HDB’s approval, contingent on the buyer’s ethnicity not exceeding the established quota for that block and neighbourhood. The quota limits were set to approximate the national ethnic composition at the time: Chinese ~77%, Malay ~22%, Indian and others ~10% — with built-in flexibility at the block level to allow minor deviations.

The policy has remained largely unchanged in structure since 1989, though HDB reviews the specific quota percentages periodically. The last substantive adjustment was in 2010, when HDB reviewed the neighbourhood-level caps. In 2026, the figures remain: Chinese 84% / 87%, Malay 22% / 25%, Indian/Others 10% / 13% (neighbourhood / block).

How the EIP Works in Practice

The EIP operates at two levels simultaneously: the neighbourhood level and the block level. A buyer’s ethnicity must be within quota at both levels for a transaction to proceed.

Neighbourhood vs Block

A neighbourhood is a planning cluster of approximately 1,000–2,000 HDB households — roughly what most Singaporeans think of as a “precinct” or estate zone. A block is the individual HDB building. The block limit is slightly higher than the neighbourhood limit to give HDB flexibility in managing transitions.

If a Malay buyer wishes to purchase a flat in a block where Malay households already constitute 24% of the block’s flats, the block limit of 25% is not yet breached. However, if the neighbourhood (the surrounding cluster) already has 22% Malay households, the neighbourhood limit is met and the transaction cannot proceed — even though the block itself has room.

Who is Classified as What Ethnicity?

The classification follows the buyer’s (and co-buyers’) NRIC race declaration. For mixed-race individuals or couples, HDB uses the race of the primary buyer — generally the person listed first in the application. For joint purchases by couples of different ethnicities, HDB determines the applicable ethnicity based on its established criteria (generally the husband’s declared race in traditional family arrangements, though this has evolved to reflect modern applicant structures — buyers should check with HDB directly for their specific combination).

The SPR Quota: An Additional Layer for Permanent Residents

Beyond the ethnic-group quota, Singapore Permanent Residents (SPRs) face a separate SPR Quota. This quota caps the number of SPR households in any HDB block at 5% and in any neighbourhood at 8%. The rationale: HDB flats are subsidised public housing primarily for citizens, and excessive SPR concentration in any area is seen as inconsistent with that purpose.

Practically, this means SPR buyers face two quota checks before any resale purchase: (1) the ethnic-group EIP check, and (2) the SPR Quota check. Either can block a transaction. In more popular estates — Queenstown, Bishan, Toa Payoh, Tampines — SPR quotas can be reached at certain blocks, limiting options for SPR buyers even when the EIP quota is not an issue.

SPRs also cannot buy new BTO flats or Executive Condominiums during the initial launch period. Their housing options are largely confined to HDB resale flats (subject to both quotas) and private residential properties.

EIP Impact on HDB Resale Sellers

For sellers, the EIP can materially affect saleability. If a Chinese seller owns a flat in a block where the Chinese quota has already been met, the pool of eligible buyers is restricted to non-Chinese buyers only — significantly narrowing demand and potentially suppressing the resale price.

This dynamic is known informally as an “EIP-affected” flat. Industry data (from URA and HDB transaction records) suggests that EIP-affected blocks can see resale prices 5–12% below comparable non-affected blocks in the same estate, as the effective buyer pool is reduced. The discount reflects the liquidity premium buyers demand for taking on an asset with constrained future resalability.

EIP and HDB Rentals

The EIP applies not only to resale transactions but also to approved whole-unit and bedroom rentals of HDB flats. When an HDB flat owner applies to rent out the entire flat or individual bedrooms, HDB checks whether the rental would cause the block or neighbourhood quota for the tenant’s ethnicity to be exceeded. If so, HDB will not approve the rental application for that particular tenant.

This has practical implications for landlords in popular rental estates. A Malay landlord renting to a Malay tenant in a block near its Malay quota limit may have the application declined, requiring them to seek tenants of other ethnicities. The rental EIP check is done through the HDB Resale Portal and typically takes 7–14 business days for approval.

EIP Compliance Summary for Buyers and Sellers (2026)

| Scenario | EIP Check Required? | SPR Quota Check? | How to Check | Consequence of Breach |

|---|---|---|---|---|

| SC buying HDB resale | Yes | No | HDB Resale Portal / call HDB | Transaction cannot proceed |

| SPR buying HDB resale | Yes | Yes (both) | HDB Resale Portal / call HDB | Transaction cannot proceed |

| Foreigner buying HDB | N/A | N/A | N/A | Foreigners cannot buy HDB |

| SC/SPR renting out flat | Yes (for tenant) | Yes if tenant is SPR | HDB Resale Portal (rental) | Rental application declined |

| Flat owner listing for sale | No — buyer’s responsibility | No | Inform buyers to check before OTP | Buyer may back out post-OTP |

| New BTO purchase | Not applicable | Not applicable | N/A | HDB allocates based on ballot; no EIP for BTO |

Worked Example: EIP Blocking a Resale Purchase

👥 The Rajan Family — Indian SC Couple, Tampines

Situation: Mr and Mrs Rajan (both SC, Indian, classified as “Indian/Others” under HDB’s ethnic categories) have identified a 5-room HDB resale flat at Tampines Street 81 for S$748,000. They have obtained an In-Principle Approval (IPA) from OCBC and are ready to exercise the OTP.

EIP check result: Before signing, Mr Rajan checks the HDB Resale Portal. He finds that Block 837, Tampines Street 81 has Indian/Others households at 12.8% of total flats — just below the 13% block limit. However, the neighbourhood ethnic composition shows Indian/Others at 10.2% — exceeding the 10% neighbourhood limit.

Outcome: Even though the block itself has not reached the 13% block cap, the neighbourhood cap of 10% has been breached. HDB would not approve the resale transaction if the Rajans proceed. They must look elsewhere.

Alternative strategy: Mr Rajan checks two neighbouring blocks in the same estate. Block 821 has Indian/Others at 8.9% (block) and the neighbourhood is at 9.6% — both within limits. The Rajans find a comparable 5-room flat there for S$742,000 and proceed with that transaction instead.

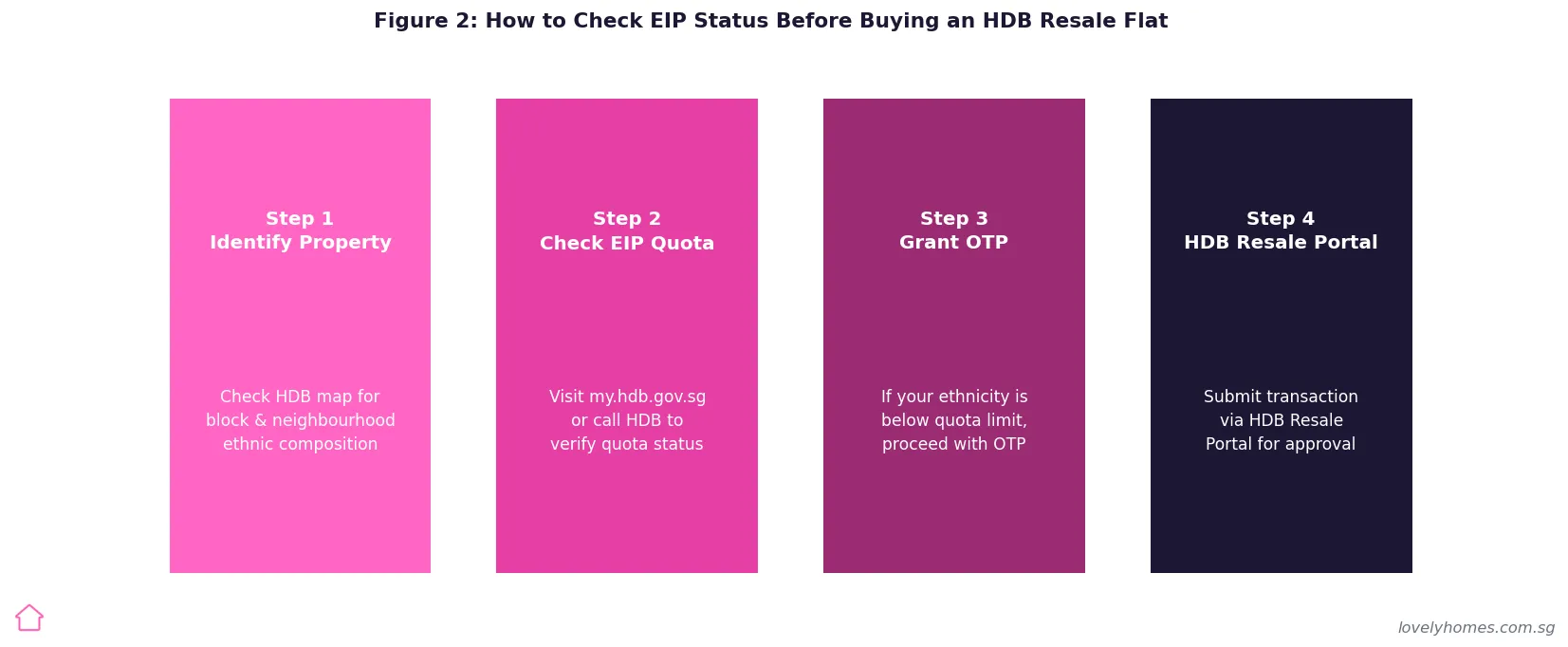

Key lesson: Always run the EIP check on the specific block and neighbourhood before exercising the OTP. HDB’s Resale Portal provides this check in real time. If in doubt, ask HDB to confirm in writing before you commit.

Why the EIP Matters for Property Buyers and Investors in 2026

The EIP is one of a small number of housing policies with no private-sector equivalent anywhere in the world — an active government intervention in the resale market to shape residential demographics. Its continued existence in 2026 reflects Singapore’s view that racial integration in housing is a public good that market forces alone will not maintain.

For buyers, this has three practical implications:

1. Pre-OTP due diligence is mandatory. Unlike stamp duty (which is always payable) or CPF usage (which always applies up to the withdrawal limit), the EIP can create an absolute bar to a transaction. There is no waiver, no appeal, and no workaround. The check is free and takes minutes on the HDB Resale Portal — there is no excuse for not doing it before any OTP is signed.

2. Resale value may be constrained. A flat in a block where one ethnic group’s quota is near saturation has a structurally smaller buyer pool. Over time, as Singapore’s ethnic composition shifts slightly (the 2020 and 2030 Censuses have shown gradual changes in distribution), these constraints may ease or tighten. Buyers should assess whether the block they are purchasing in is near any quota caps — not just for their own purchase, but for future resalability.

3. Rental yield could be affected. Landlords whose target tenant demographic is near the block quota may find their rental application declined and be forced to seek tenants from a different group — potentially limiting rental demand and yields in certain micro-locations.

What Might Change: Possible EIP Developments (Speculative)

The EIP has been in place for 37 years as at 2026 and has rarely been publicly debated in Singapore’s political discourse. However, several developments could prompt a policy review in the years ahead:

- Shifting ethnic composition: Singapore’s 2020 Census showed modest shifts in ethnic composition — the Chinese share declined slightly from 76.8% (2010) to 75.9%; the Malay share remained at ~15%; Indian/Others grew slightly. If these trends continue, HDB may adjust quota caps to reflect the updated demographic baseline.

- New citizen intake: Singapore’s naturalisation programme brings in citizens from a variety of ethnic backgrounds not represented in the original EIP framework. If new citizen categories grow significantly, HDB may need to refine how “Indian/Others” is classified.

- Digital OTP reforms: HDB has been digitising the resale process. It is plausible that future HDB Resale Portal upgrades will integrate real-time EIP checks directly into the OTP workflow, reducing the risk of buyers unknowingly exercising an ineligible OTP.

Frequently Asked Questions

Can I buy any HDB resale flat I want, regardless of the EIP?

No. The EIP creates a hard quota that HDB enforces at the point of resale approval. If your ethnic group’s quota has been reached at either the block or neighbourhood level, HDB will not approve the transaction. The OTP is a private agreement between buyer and seller, but HDB’s approval is required for the actual transfer of the flat — so exercising an OTP on an EIP-blocked flat effectively voids the transaction, and the buyer may lose the OTP option fee (typically 1% of the purchase price, capped at S$1,000). Always check before you sign.

Does the EIP apply to new BTO flats?

No. The EIP does not apply to HDB BTO (Build-to-Order) flat purchases. BTO allocation is managed through HDB’s ballot system, and HDB itself manages the ethnic balance during the initial allocation process. The EIP only becomes relevant when BTO flat owners subsequently sell in the open resale market during or after the Minimum Occupation Period (MOP). At that point, the resale flat enters the open market and EIP rules apply to the buyer’s purchase.

What happens if I am of mixed ethnicity?

HDB uses the race as declared on your NRIC for EIP purposes. For mixed-race individuals, the NRIC declaration (made at birth or at the point of citizenship registration) governs which quota is checked. If you have changed your race declaration on your NRIC (permissible under certain circumstances), the updated declaration applies. For couples where both buyers are of different ethnicities, HDB determines the applicable ethnic classification based on its guidelines — typically the primary applicant’s declared race. If this creates ambiguity for your situation, call HDB directly to confirm before exercising any OTP.

Can EIP quotas be waived or appealed?

Generally, no. The EIP is a statutory policy administered by HDB, and there is no formal waiver or appeal process for buyers who cannot meet the quota for a particular block or neighbourhood. The solution is to identify an alternative block or neighbourhood where the quota has not been reached. HDB occasionally adjusts the boundaries of planning neighbourhoods when redevelopment occurs, which can change quota calculations for affected blocks — but this is an administrative restructuring, not an individual waiver.

Does the EIP affect Executive Condominiums (ECs)?

ECs are a hybrid housing type — publicly developed by HDB but privately managed after completion. The EIP does apply to ECs during their public-housing phase (the first 5 to 10 years, prior to full privatisation). Once an EC has been privatised (after the 10-year mark), it is treated as private residential property and the EIP no longer applies to resale transactions. Given the EC MOP change in May 2026 (MOP extended from 5 to 10 years, privatisation extended from 10 to 15 years), the EIP-applicable period for new ECs has in effect been extended alongside these changes.

How do I check the EIP status before buying an HDB resale flat?

The fastest method is to log in to the HDB Resale Portal (resale.hdb.gov.sg) using your SingPass, navigate to the “Check Resale Conditions” section, and enter the block and street address of the flat you are interested in. The portal will return the current ethnic composition percentages and confirm whether your ethnic group is within the quota. Alternatively, you can call HDB at 1800-225-5432 (toll-free) and request an EIP check for the specific address. Always get confirmation in writing (via email or the portal’s printable report) before exercising your OTP.

Does the EIP affect the resale value of HDB flats?

It can. A flat in a block where the dominant ethnic group’s quota has been met effectively has a smaller eligible buyer pool — only buyers of the non-dominant ethnic groups can purchase. This structural limitation on demand can depress the flat’s market price relative to comparable flats in non-quota-affected blocks. The discount is hard to quantify precisely (it varies by estate, ethnic mix, and local demand), but it is a real consideration for buyers making a long-term investment decision. Before purchasing, assess not just your own EIP eligibility, but whether the block’s current composition suggests that future resalability may be constrained.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial, or property advice. The Ethnic Integration Policy (EIP) is administered by the Housing & Development Board (HDB) under the Ministry of National Development. EIP quotas and eligibility criteria are subject to change by HDB at any time. Readers must verify the current EIP status of any specific block and neighbourhood directly with HDB via the HDB Resale Portal (www.hdb.gov.sg) or by calling HDB at 1800-225-5432 before exercising any Option to Purchase. Ethnic classification rules may vary for individuals in specific circumstances — consult HDB directly for your situation. LovelyHomes recommends consulting a CEA-registered property agent and a qualified legal adviser before entering into any property transaction.

Click anywhere to close