Singapore Double-Launch Weekend April 2026: TGR + Vela Bay Move 1,224 Homes in 48 Hours

Published 28 April 2026. Reflects developer launch-weekend announcements and Singapore property press coverage of 25–26 April 2026.

Quick Answer — what happened

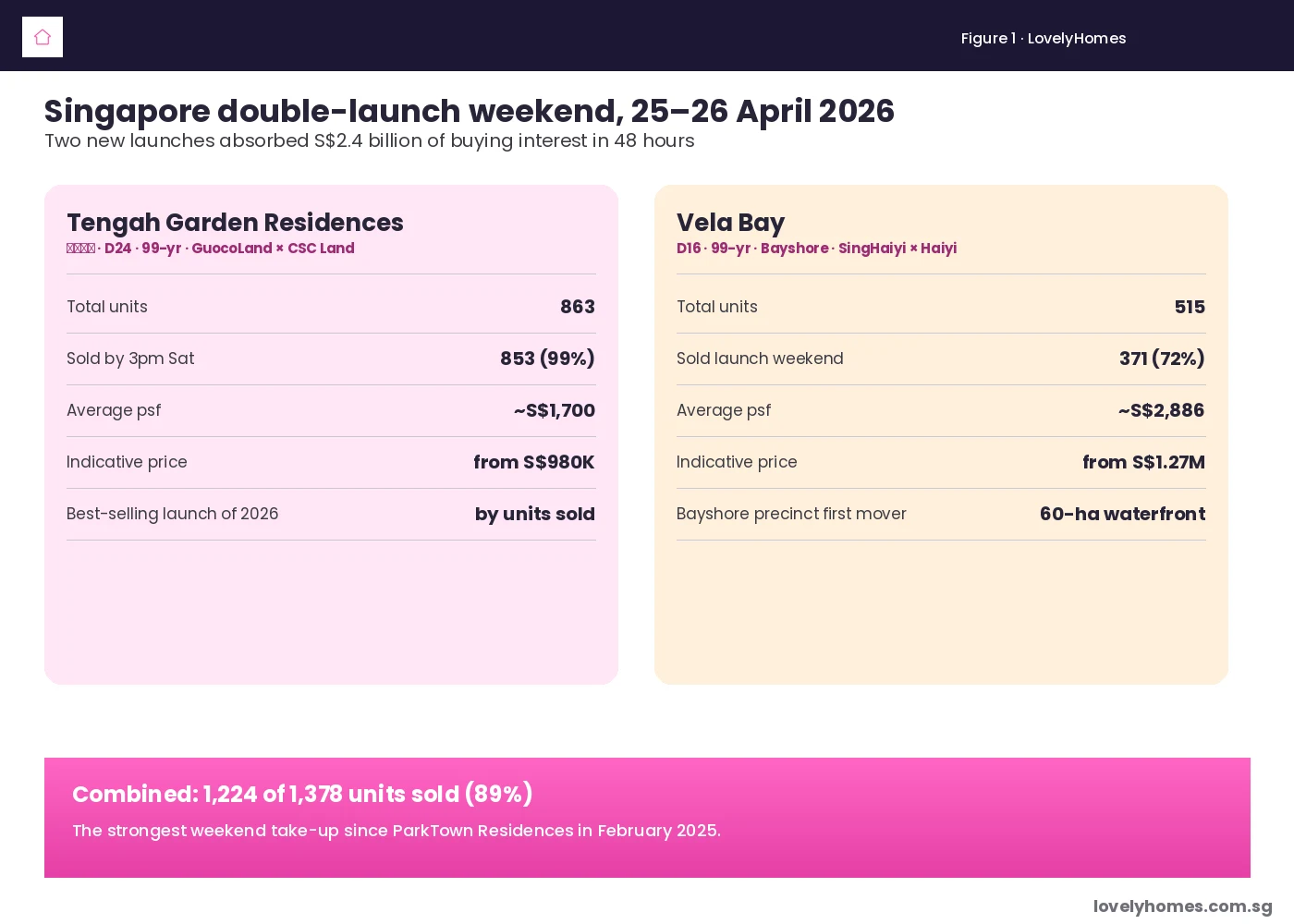

- Two major Singapore new condo launches went live on the weekend of 25–26 April 2026: Tengah Garden Residences (863 units, 99-yr leasehold, GuocoLand × CSC Land) and Vela Bay (515 units, 99-yr leasehold, SingHaiyi × Haiyi Holdings).

- Combined, the two projects sold 1,224 of 1,378 units (89%) over the launch weekend.

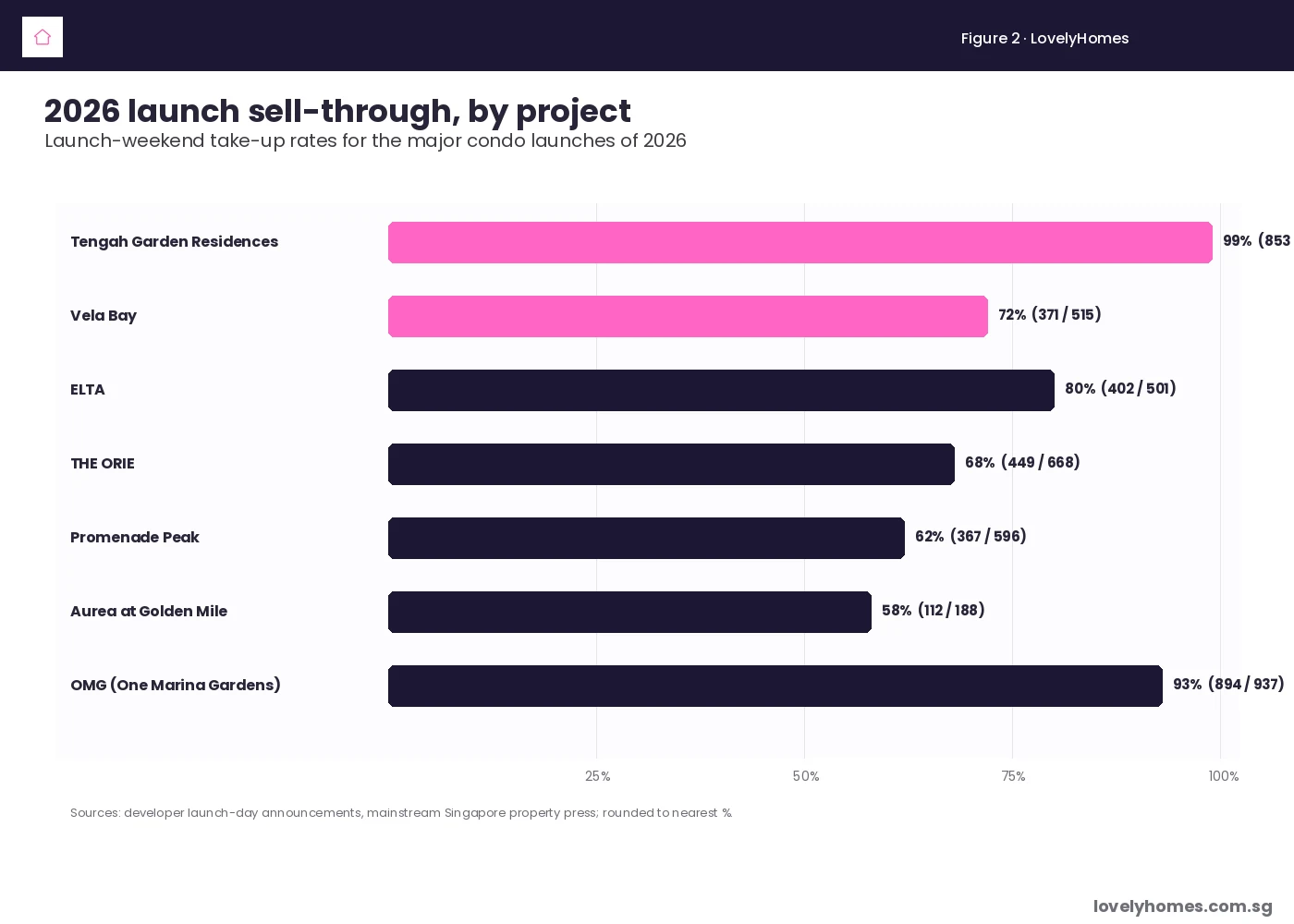

- Tengah Garden Residences cleared 853 of 863 units (~99%) by Saturday afternoon, the strongest launch-day take-up since ParkTown Residences in February 2025.

- Vela Bay sold 371 of 515 units (~72%), becoming the first private launch in the 60-hectare Bayshore waterfront precinct.

- Average prices: Tengah Garden Residences ≈ S$1,700 psf, with units from S$980,000. Vela Bay ≈ S$2,886 psf, with units from S$1.27 million.

- The weekend’s combined gross sales value is approximately S$2.4 billion, the largest dual-launch weekend on record for Singapore residential property.

The headline numbers

Singapore’s primary condo market has been described as “thin but priced firm” through Q1 2026. The weekend of 25–26 April 2026 ended that narrative with a single set of launch figures. By close of business Sunday, two new projects in different parts of the island had between them moved more units than the entire month of February 2026.

Tengah Garden Residences, the first private condominium launched inside the Tengah HDB-led new town, registered 853 sales out of 863 units — a 99% sell-through rate. Vela Bay, the first private residential launch in the Bayshore precinct in the East, sold 371 of 515 units. The two projects together absorbed buyer demand worth roughly S$2.4 billion in 48 hours.

Tengah Garden Residences — the suburb story

Developed jointly by GuocoLand and CSC Land Group on a 99-year leasehold parcel along Tengah Garden Avenue (District 24), Tengah Garden Residences was launched at indicative prices from S$980,000 for one-bedroom units. Average pricing landed at roughly S$1,700 per square foot, slotting in between recent Outside-Central-Region (OCR) launches and the older Bukit Batok mass-market resale stack.

Key drivers of the near-sellout:

- Pent-up Tengah demand. Tengah’s residential identity has been HDB-led since 2018, with no private launches inside the estate. The opening of the first private project tested an aspirational segment that had been waiting four years.

- Pricing that read as “below ParkTown”. ParkTown Residences in Tampines launched at a higher OCR psf in February 2025; the Tengah price point felt restrained by comparison.

- Singapore-Citizen-heavy buyer mix. Over 90% of buyers are reported to be Singapore Citizens, consistent with the post-2023 ABSD regime where foreign demand at OCR price points has thinned.

- Connectivity story. Future Tengah MRT (Jurong Region Line, opening 2027–2028) and the proximity of the new Tengah town centre supported the long-hold buyer thesis.

Vela Bay — the Bayshore opener

Vela Bay, by SingHaiyi Group and Haiyi Holdings, launched at average prices of around S$2,886 psf, with one-bedroom units from S$1.27 million. The 515-unit project sits inside the Bayshore precinct, an emerging 60-hectare master-planned waterfront on the East Coast.

The Vela Bay take-up of 72% is more modest than Tengah Garden Residences’ 99%, but no less interesting:

- Higher absolute price point. A typical 2-bedroom Vela Bay unit lands above S$2 million; that is a different buyer profile from Tengah.

- First-mover premium. As the only private launch in a precinct still under construction, Vela Bay’s price had to absorb the discount buyers usually demand for “go-first” risk on infrastructure delivery.

- Nine new sites in 1H 2026 GLS. URA’s 1H 2026 Government Land Sales programme released nine confirmed-list sites with capacity for ~9,185 units. The sequencing of those sites — including the Bayshore Drive mixed-use plot whose tender closes 15 July 2026 — is shaping how buyers price first-mover Bayshore stock.

- SingHaiyi balance-sheet narrative. SingHaiyi has been a heavy participant in en-bloc and GLS bids in 2026 (it was also part of the consortium that won Loyang Valley en-bloc at S$880 million); its Bayshore launch is a clear conviction trade by the developer.

What the weekend tells us about 2026 demand

| Metric | Reading | Implication |

|---|---|---|

| Combined launch-weekend take-up | 1,224 / 1,378 units (89%) | Latent demand absorbing strongly when supply opens at the right price |

| OCR launch psf — Tengah | ~S$1,700 | Below recent comparable OCR launches; a “value” anchor for 2026 OCR pricing |

| RCR/East launch psf — Vela Bay | ~S$2,886 | Setting the benchmark for the Bayshore precinct ahead of the Bayshore Drive GLS tender |

| Buyer mix | Predominantly Singapore Citizen | Foreign demand still suppressed by the 60% ABSD; the market is local-driven |

| 2026 launch pipeline | ~17 projects, ~8,100 units | 30% lower than 2025 — supply scarcity supports launch-day pricing power |

What this means for buyers

For prospective Tengah buyers who missed the launch ballot, the resale option will likely sit at a 3–7% premium once units start changing hands — typical for a near-sellout launch. Tengah Garden Residences will not have additional release tranches for some months given the sell-through.

For Vela Bay, with 144 units (28%) still available, the post-launch phase remains accessible at launch pricing. Buyers should monitor whether units in Towers 1 and 2 are released before infrastructure milestones in the Bayshore precinct — first-mover units historically appreciate as the precinct fills out, but only if pricing on later launches doesn’t undercut them.

For the broader market, the weekend confirms that well-priced, well-located new launches in Singapore can still clear at speed in 2026, against the narrative of cooling-measure overhang. The discipline is on launch-day pricing: Tengah’s near-sellout came at a psf below what some industry watchers had projected for an OCR launch this cycle. Vela Bay’s slower (but still strong) take-up suggests that buyers in the higher-price RCR segment remain willing to pay up only for clearly differentiated locations.

What might come next

Two near-term watchpoints:

- Bayshore Drive mixed-use GLS tender (closes 15 July 2026). The land bid will be read against Vela Bay’s launch psf as a price discovery point for the precinct.

- BTO June 2026 ballot (~6,900 flats). If HDB pricing continues to compress against private OCR pricing, the substitution effect supports a second wave of OCR private demand later in 2026.

The next major private launches in the calendar — Bayshore Drive (if the tender awards in 1H 2026), Sembawang Drive EC, and a likely 2H 2026 District 5 OCR launch — will tell us whether the 25–26 April weekend was a one-off catch-up after a thin Q1, or the start of a measurably stronger primary market.

Frequently asked questions

Why did Tengah Garden Residences sell so much faster than Vela Bay?

Three reasons. First, price: at ~S$1,700 psf, Tengah’s entry price of S$980,000 sits below the typical OCR launch and is reachable for HDB upgrader couples. Vela Bay at ~S$2,886 psf and S$1.27 million entry sits in a different affordability cohort. Second, Tengah is a four-year-old new town with a built-out HDB community already in occupation; Vela Bay is the first launch in a precinct still under construction. Third, Tengah was the first private launch in the new town — a one-off scarcity premium that Vela Bay does not enjoy because more Bayshore launches will follow.

Is this evidence that cooling measures aren’t working?

Not necessarily. Cooling measures (the April 2023 ABSD hike, the September 2022 LTV / TDSR tightening) have visibly suppressed foreign demand and kept investor flows thin. The April 2026 launches were powered overwhelmingly by Singapore Citizen owner-occupier and upgrader demand, which is exactly the segment policy-makers wanted to remain active. The strong take-up reflects pent-up local demand meeting limited new supply, not a re-acceleration of speculative buying.

Should buyers chase a near-sellout launch like Tengah?

Generally no. Once a launch clears 90%+, the remaining stock is typically the less attractive layouts or units, and the resale market opens at a premium. The discipline for buyers is to be at the front of the queue at launch — or wait for the resale market to settle 6–9 months later when the urgency premium has softened.

What does this mean for the Bayshore Drive GLS tender?

Vela Bay’s 72% sell-through at ~S$2,886 psf gives bidders a reference point for what a Bayshore launch can absorb at price. If the Bayshore Drive GLS tender bids land at above S$1,400 psf ppr, the implied launch psf for the next Bayshore project would be approximately S$3,000+, which is testable against Vela Bay’s revealed demand curve.

How does this compare to historical strong launches?

The 99% Tengah figure is the highest launch-weekend take-up since ParkTown Residences in February 2025, which moved 87% on launch day. Going further back, Lentor Mansion (2024), Amo Residence (2022), and Treasure at Tampines (2019) all booked similar 90%+ launch-day percentages. Each of those projects shared the same ingredients as Tengah: a clear price-point anchor, an underserved sub-market, and a strong upgrader cohort.

Will more units be released?

For Tengah Garden Residences, the developer has not announced a second tranche; with only 10 units unsold, there is little to release. For Vela Bay, the remaining 144 units (28%) will be released in batches over the coming weeks at the same indicative price band; movements above launch pricing typically follow demonstrated take-up of 80%+.