Singapore HDB Lease Top-Up Guide 2026: Eligibility, Premium Costs and How to Apply

Quick Answer: HDB Lease Top-Up in Singapore 2026

- The HDB Lease Top-Up Scheme lets eligible flat owners extend their flat’s lease back to 99 years by paying a market-rate premium to HDB.

- Eligibility: Singapore Citizen, aged 55 or older, must own (not tenancy-in-common) the flat, no outstanding arrears, flat has 20–49 years remaining on lease.

- The premium is calculated by HDB using an independent valuer and reflects the cost of restoring the unexpired lease period to 99 years.

- Payment can be made in cash, CPF Ordinary Account (OA), or a combination of both.

- A lease top-up unlocks CPF usage and improves resale marketability — but does not guarantee a higher resale price.

- A separate scheme — the Lease Buyback Scheme (LBS) — applies to flat owners who want to monetise their lease (sell the tail end back to HDB for a cash top-up to CPF); this is a different transaction from a Lease Top-Up.

- Application is made directly with HDB; the entire process takes approximately 3–5 months.

What is the HDB Lease Top-Up Scheme?

The HDB Lease Top-Up Scheme is administered by the Housing & Development Board (HDB) and allows eligible flat owners — specifically senior Singapore Citizens aged 55 and above — to extend their HDB flat’s lease from its current unexpired term back to a full 99 years from the original date of lease. In exchange, the flat owner pays a premium to HDB based on an independent market valuation of the lease restoration.

Singapore’s HDB flats come with 99-year leases that began at the point of construction. Many flats built in the 1970s, 1980s, and early 1990s now have fewer than 60 years remaining on their leases. A flat with a short remaining lease faces significant consequences: CPF withdrawal is curtailed, bank financing becomes difficult or unavailable, and resale values are suppressed because buyers — particularly younger buyers relying on CPF — cannot service the purchase effectively.

The Lease Top-Up Scheme was introduced to give senior flat owners a way to restore their flat’s value and their own retirement flexibility. As of 2026, this scheme remains an important but selective instrument: not all flats qualify, and HDB reserves the right to decline applications. It is distinct from the Lease Buyback Scheme (LBS), under which flat owners aged 65 and above can instead sell the tail-end of their lease to HDB in exchange for proceeds deposited into their CPF Retirement Account, retaining the right to live in the flat for the remainder of a shorter retained period.

How Does HDB Lease Remaining Affect CPF and Resale?

The CPF Board applies a pro-ration formula when a flat’s remaining lease does not cover the youngest buyer to the age of 95. Specifically, for a 40-year-old buyer, the flat must have at least 55 years remaining (to cover that buyer to age 95). If the lease falls short, CPF usage is pro-rated. If the remaining lease covers fewer than 20 years, CPF cannot be used at all.

Bank financing follows a similar logic under Monetary Authority of Singapore (MAS) rules: the loan tenure cannot exceed the flat’s remaining lease less 35 years, and lenders typically require the lease to cover the youngest borrower to at least age 65. A flat with 35 years remaining, for example, offers a younger buyer essentially no loan financing and no CPF. This drastically narrows the buyer pool to those who can transact in cash — usually older buyers downsizing for retirement purposes.

An HDB loan — offered only for HDB flats — similarly requires that the loan period does not extend beyond the flat’s remaining lease. A flat at 38 years’ lease remainder offers a buyer at most a 38-year HDB loan, but HDB’s maximum loan tenure is 25 years, so effectively the loan can still be drawn down; however, the flat must be valued sufficiently and the flat must not be below 20 years remaining to even qualify for CPF usage.

Who is Eligible for the HDB Lease Top-Up Scheme?

As of 2026, the HDB Lease Top-Up Scheme has five core eligibility criteria, each of which must be satisfied simultaneously:

| Criterion | Requirement | Notes |

|---|---|---|

| Citizenship | Singapore Citizen (all owners) | SPR co-owners must become SC first or one SC owner must apply alone |

| Age | At least one owner aged 55 or above | All co-owners who participate must meet age requirement |

| Ownership structure | Joint tenancy (not tenancy-in-common) | TiC flat owners must convert to JT first or one sole owner applies |

| Minimum tenure held | Owned the flat for at least 5 years | Aligned with MOP; effectively always satisfied if MOP is met |

| Financial standing | No outstanding arrears (conservancy, mortgage, etc.) | All charges must be settled before application is accepted |

There is no income ceiling for the Lease Top-Up Scheme — unlike the Lease Buyback Scheme, which does restrict eligibility to flat owners whose household income does not exceed S$14,000 per month. The Lease Top-Up is, in theory, available regardless of income — the flat owner simply needs to have, or be able to pay, the market-rate premium.

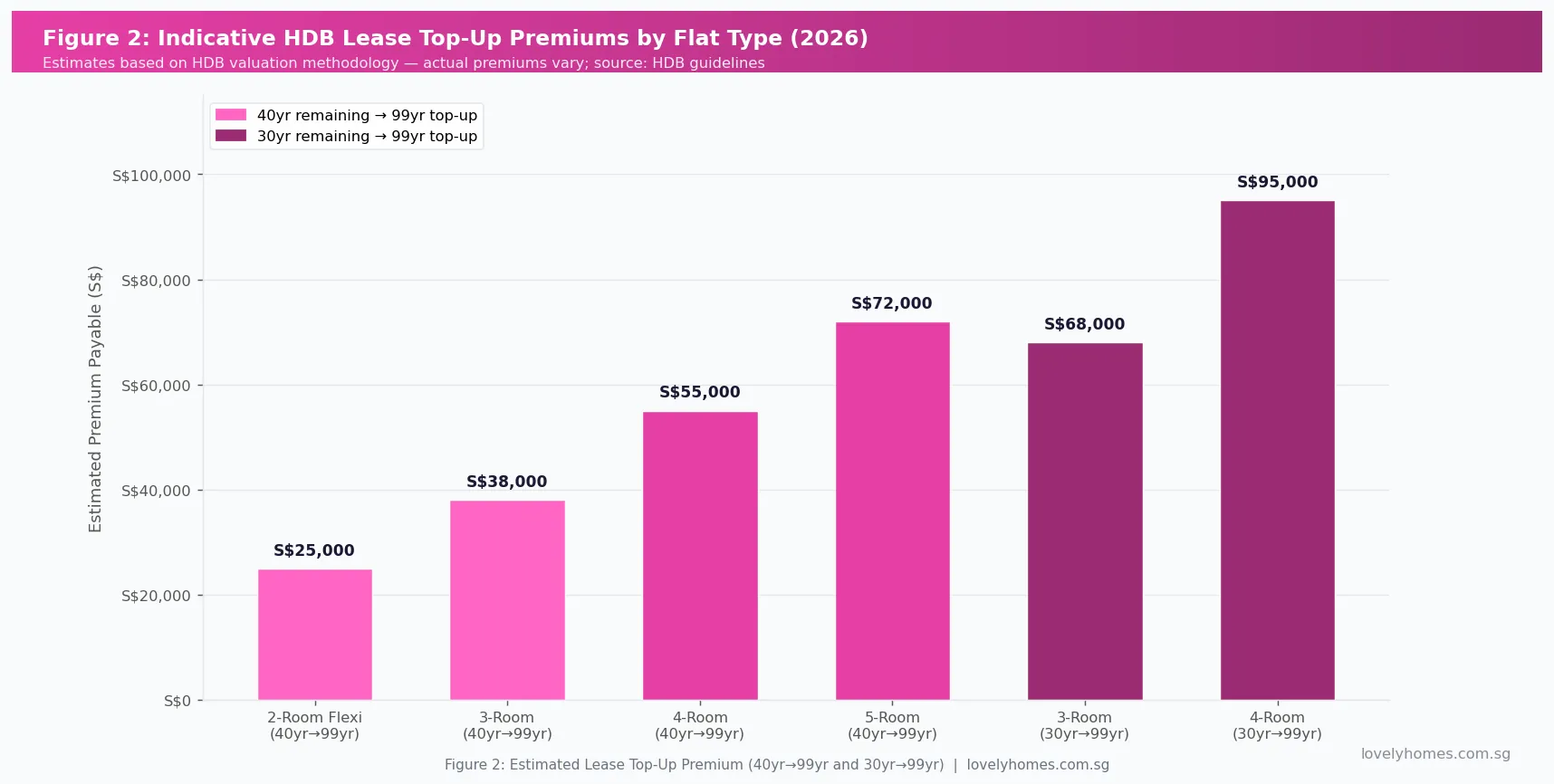

How is the Lease Top-Up Premium Calculated?

HDB engages an independent registered valuer to determine the market value of the lease restoration. In practice, the premium reflects what the lease extension is worth in the open market — that is, the increment in the flat’s value from having a short lease restored to 99 years. The premium is not fixed and depends on:

- The flat type and size (3-room vs 5-room);

- The flat’s location (mature vs non-mature estate);

- The current remaining lease (the shorter the lease, the larger the value gap to be bridged);

- Prevailing HDB resale market conditions at the time of assessment.

As an indicative guide, industry observers in 2026 note that premiums for a typical 4-room flat in a mature estate (such as Toa Payoh, Queenstown, or Geylang) with approximately 40 years remaining typically fall in the range of S$40,000–S$65,000, while a flat with only 30 years remaining would command a significantly higher premium — sometimes exceeding S$90,000. These figures are estimates only; HDB’s actual assessments may differ materially. The flat owner has 30 days from HDB’s offer letter to accept or decline the premium before the offer lapses.

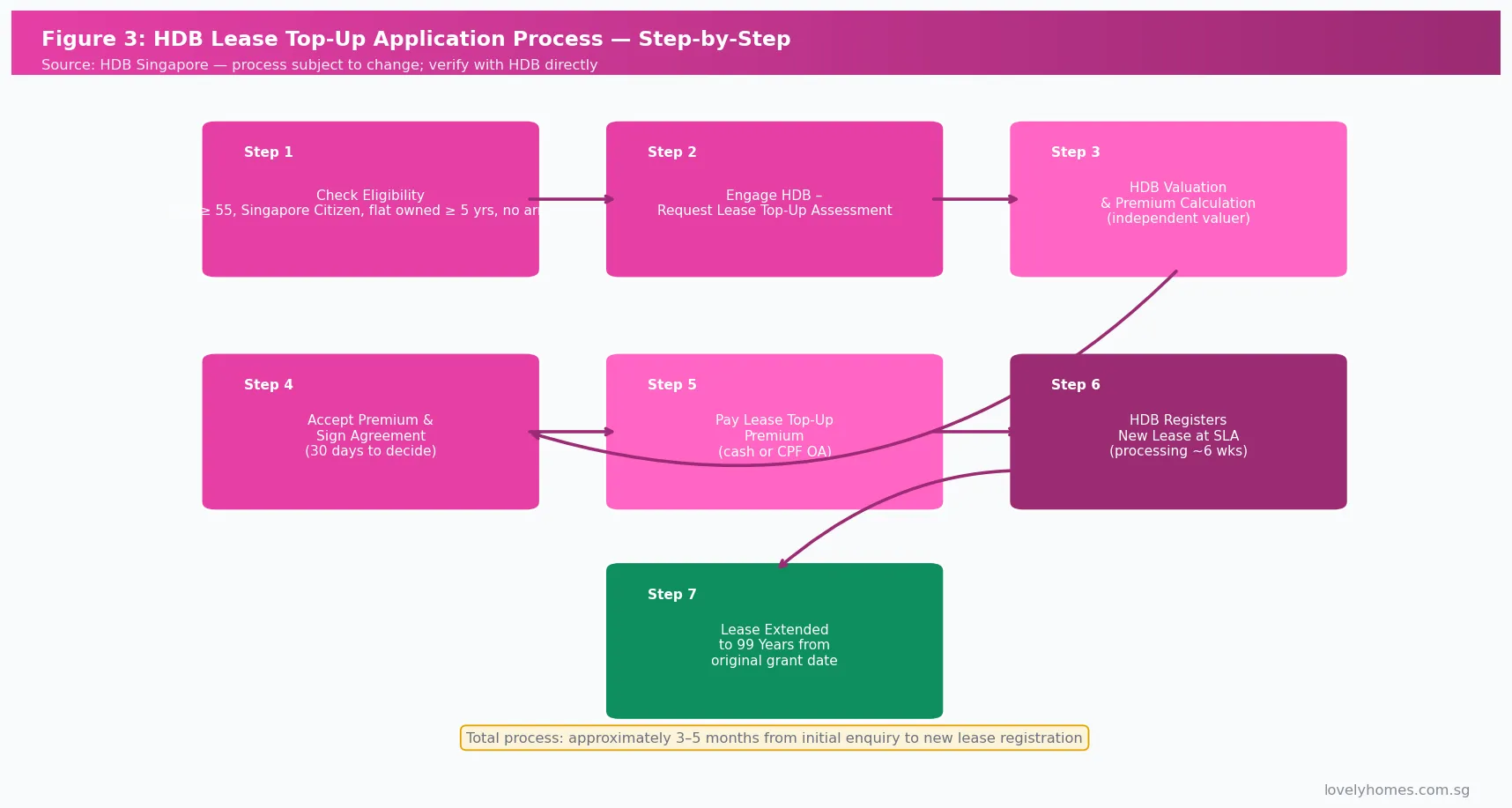

How to Apply for the HDB Lease Top-Up

The application process involves direct engagement with HDB through the HDB Branch or the My HDBPage portal. The key steps are outlined below. The entire process typically takes 3–5 months from initial enquiry to registration of the new lease at the Singapore Land Authority (SLA).

Paying the Lease Top-Up Premium

The premium can be paid using cash, CPF Ordinary Account (OA) savings, or a combination of both. There are important nuances:

- CPF OA usage: Permitted, but only after the flat owner’s Basic Retirement Sum (BRS) in the CPF Retirement Account (RA) is set aside. Senior flat owners should check their CPF balance before assuming OA funds are fully available. The CPF Board’s 55+ scheme means that OA savings beyond the BRS are accessible.

- Cash: No minimum cash component is mandated — unlike the downpayment rules for bank loans. The entire premium can be paid in CPF OA if sufficient funds exist.

- No stamp duty: The Lease Top-Up is not a transfer of title — it is a restoration of lease duration. No BSD or ABSD is payable on the premium itself.

- No GST: The premium is not subject to goods and services tax as it is an HDB transaction.

Lease Top-Up vs Lease Buyback Scheme: Key Differences

These two schemes are sometimes confused because both involve the HDB lease and apply to senior flat owners. They are structurally opposite transactions:

| Feature | Lease Top-Up Scheme | Lease Buyback Scheme (LBS) |

|---|---|---|

| Direction of transaction | Flat owner pays HDB to extend lease | HDB pays flat owner to buy back tail-end of lease |

| Resulting lease | Extended to 99 years (full restoration) | Retained period of 30 or 45 years |

| Purpose | Restore asset value; improve CPF/financing; improve resale | Monetise flat for retirement income (LBS proceeds go to CPF RA/CFS) |

| Minimum age | 55 years | 65 years |

| Income ceiling | None | S$14,000/month household income |

| Flat types eligible | All HDB flat types | 2-room Flexi to 4-room only (5-room excluded) |

| CPF top-up bonus | Not applicable | Yes — up to S$30,000 CPF top-up bonus if RA is below FRS |

Worked Example: The Nguyens, Toa Payoh 4-Room Flat

Mr and Mrs Nguyen, both Singapore Citizens aged 63 and 61, own a 4-room HDB flat in Toa Payoh. They purchased it in 1990. As at June 2026, the flat has 63 years remaining on its lease — still comfortable territory for CPF and financing. However, in contemplating a sale, they observe that the flat’s age and trajectory is a concern for younger buyers planning ahead: if unsold for another 10 years, the flat will have only 53 years remaining, approaching the threshold where CPF usage begins to be meaningfully curtailed.

In a different scenario, suppose the Nguyens’ neighbours — Mr and Mrs Tan, also in their early 60s — own a nearby 4-room flat built in 1981. That flat has approximately 54 years remaining. Under current CPF rules, a 35-year-old buyer could still use full CPF OA (since 54 years covers that buyer to age 89, though under the CPF Board’s “flat must cover buyer to 95” rule, the usage is pro-rated for a 35-year-old). The Tans consult HDB. HDB’s independent valuer assesses the lease restoration premium at S$58,000. The Tans have S$95,000 in their combined CPF OA accounts (above the Basic Retirement Sum). They pay S$58,000 from CPF OA. Total cash outlay: nil. Total time: 4 months. The flat’s lease is restored to 99 years from 1981 — meaning a new expiry of 2080. The market value of the flat increases by an estimated S$40,000–S$60,000 in the resale market — somewhat less than the premium paid, but the flat is now significantly more liquid.

Does a Lease Top-Up Guarantee a Higher Resale Price?

Not necessarily — and this is an important caveat. The Lease Top-Up restores the flat’s CPF and financing eligibility, which broadens the buyer pool. Empirically, flats with shorter leases trade at discounts in the HDB resale market, and restoring the lease removes that discount. However, the flat owner typically pays a premium that is priced by an independent valuer at close to the market value of the lease extension, meaning the economic gain from the transaction is marginal at best.

The primary beneficiaries of the Lease Top-Up tend to be:

- Flat owners who plan to keep living in the flat for their retirement and want the security of a full lease rather than a depreciating asset;

- Flat owners who wish to pass the flat on to their children (by will or inter vivos transfer) with a longer residual lease;

- Flat owners who want to unlock CPF usage or financing for an existing loan or refinancing situation.

Flat owners looking for a purely financial investment play — buy cheap short-lease flat, top up, and resell at a profit — will typically find the economics thin. HDB’s pricing mechanism is designed to capture the market value of the lease restoration at the outset, leaving limited arbitrage opportunity.

What Might Come Next: Lease Top-Ups and Ageing Estates

This section contains speculation and forward-looking commentary. It does not constitute financial or policy advice.

As Singapore’s oldest public housing estates — many built in the 1960s, 1970s, and early 1980s — approach the midpoint of their 99-year leases, the policy question of what happens to ageing HDB flats is becoming increasingly pressing. Two principal mechanisms exist today: the Lease Top-Up (owner-initiated, at cost) and the Selective En-Bloc Redevelopment Scheme (SERS, government-initiated, with generous compensation). A third possible outcome — flats simply depreciating to zero at lease expiry — remains politically and socially sensitive, and the government has been careful to distinguish between the exceptional nature of SERS and any broader expectation of state intervention.

Industry commentators have raised the possibility that the government might expand eligibility for the Lease Top-Up beyond age 55, or reduce the minimum premium threshold, to encourage uptake. Others suggest a tiered subsidy might be introduced for lower-income seniors whose flats are their primary retirement asset. These remain speculative; as at June 2026, no such policy changes have been announced.

FAQ: HDB Lease Top-Up Singapore 2026

Can I do a Lease Top-Up if my flat has an outstanding HDB mortgage?

Yes, in principle — having an outstanding mortgage does not disqualify you from applying for a Lease Top-Up. However, any outstanding arrears (which are different from a current active mortgage) will prevent approval. You should also note that if you are paying down a bank loan, the bank may need to be notified of and may consent to the lease restoration, as it affects the security value of the property. Check with your lender before applying.

Does a Lease Top-Up affect my ABSD position if I also own a private property?

A Lease Top-Up is not a transfer of ownership — you are not acquiring a new property. Therefore, no Additional Buyer’s Stamp Duty (ABSD) or Buyer’s Stamp Duty (BSD) is triggered. Your property count for ABSD purposes remains unchanged. However, if you are also considering selling the flat or purchasing another property around the same time, consult a lawyer to ensure no inadvertent ABSD exposure arises from the timing of related transactions.

Will the Lease Top-Up increase my annual property tax?

Potentially yes, marginally. IRAS bases property tax on Annual Value (AV), which is the estimated annual rent the flat could fetch. A flat with a restored 99-year lease is more valuable and may attract slightly higher AV assessments over time. That said, owner-occupied HDB flats currently benefit from a zero property tax rate on the first S$8,000 of AV, and most HDB flats — even after a lease restoration — are unlikely to see AV exceed this threshold materially. In practice, for most flat owners, the property tax impact of a Lease Top-Up is negligible.

What happens if HDB declines my Lease Top-Up application?

HDB retains the discretion to decline applications, typically because of town planning considerations (for example, if the estate is earmarked for future redevelopment under SERS or the Home Improvement Programme). If declined, HDB will provide a reason. Flat owners in this situation have no formal appeal mechanism within the Lease Top-Up scheme — they may, however, enquire separately about SERS eligibility, which would typically involve a relocation package with a replacement flat and compensation. Given the relatively few SERS exercises in recent years, a decline based on planning reasons should not automatically be read as a precursor to SERS.

Can I use the Silver Housing Bonus scheme together with a Lease Top-Up?

The Silver Housing Bonus (SHB) is a separate scheme designed for seniors who downsize their HDB flat to a smaller flat and use the proceeds to top up their CPF Retirement Account. It is not directly related to the Lease Top-Up Scheme. However, a senior who first tops up the lease — improving the resale value and buyer pool of their existing flat — and subsequently sells it to downsize could potentially benefit from both measures in sequence: a better resale price from the lease-extended flat, and then the CPF top-up bonus from the Silver Housing Bonus. You should consult an HDB officer and a CPF adviser to model this sequence carefully before committing.

My flat is a tenancy-in-common with my sibling. Are we eligible?

Tenancy-in-common (TiC) ownership is not eligible under the current Lease Top-Up Scheme; only joint tenancy (JT) ownership qualifies. If you and your sibling own the flat as TiC, you would need to first convert the ownership structure to joint tenancy before applying for a lease top-up. Converting from TiC to JT requires both parties to agree and to execute a Deed of Declaration or instrument of transfer at the SLA. Legal costs are typically S$500–S$1,500. Note also that converting to JT has implications for inheritance (survivorship replaces testamentary distribution of the flat) — consult a lawyer before proceeding.

Is the Lease Top-Up available for DBSS or EC flats?

The HDB Lease Top-Up Scheme is only available for HDB flats. Design, Build and Sell Scheme (DBSS) flats are HDB flats — they carry 99-year HDB leases and are therefore eligible in principle if the owner meets all other criteria. Executive Condominiums (ECs), however, are private properties after their 10-year privatisation. ECs carry strata titles governed by the Land Titles (Strata) Act, not HDB leases, and are not eligible for the HDB Lease Top-Up Scheme. EC flat owners approaching lease expiry would need to rely on a collective sale (en-bloc) or the private redevelopment market.

Related Articles

- HDB Minimum Occupation Period (MOP) Singapore 2026: Complete Guide

- HDB Loan vs Bank Loan Singapore 2026: Rates, LTV and Which Saves You More

- Singapore HDB BTO Application Guide 2026: Eligibility, Balloting and Key Collection

- Singapore HDB Subletting Guide 2026: Rules, NCQ and Approval Process

- Singapore Annual Property Tax Guide 2026: Annual Value, IRAS Rates and Rebate

- Singapore CPF Housing Grant Guide 2026: EHG, PHG, Family Grant Explained

- Singapore Property Downpayment Guide 2026: How Much Cash and CPF You Need

- Renting Out Your HDB Flat 2026: Rules, Quotas and Step-by-Step Landlord Guide

Disclaimer

This article is intended as a general educational resource only and does not constitute legal, financial, or property advice. HDB’s Lease Top-Up Scheme policies, eligibility criteria, and premium calculation methodology are subject to change. All figures, eligibility criteria, and premiums quoted in this article reflect LovelyHomes’ understanding as at June 2026 based on publicly available HDB guidelines. Readers should verify current information directly with HDB at www.hdb.gov.sg, the CPF Board at www.cpf.gov.sg, and IRAS at www.iras.gov.sg. You should engage a licensed property agent, lawyer, or financial adviser for advice specific to your circumstances.