Long Island Singapore Preparatory Works 2026: What It Means for East Coast Property

Key Takeaways: Long Island Preparatory Works 2026

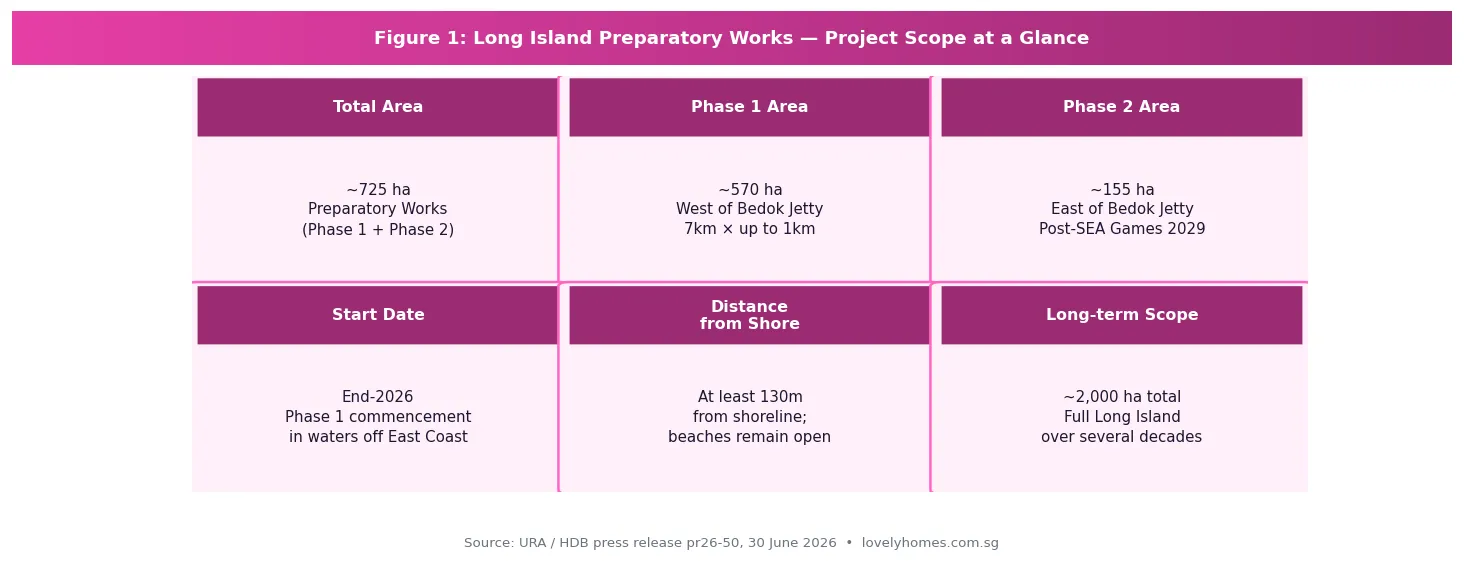

- What: Preparatory marine works for Singapore’s large-scale ‘Long Island’ coastal protection and land reclamation project, to begin end-2026 off East Coast Park

- Phase 1: ~570 ha, west of Bedok Jetty, starts end-2026; 7km long, up to 1km wide, at least 130m from shoreline

- Phase 2: ~155 ha, east of Bedok Jetty — deferred until after the Southeast Asian (SEA) Games 2029

- Public impact: Beaches at East Coast Park remain open throughout; near-shore swimming continues; sea sports (especially kiteboarding) will be temporarily displaced

- Environmental study: Water quality expected to meet marine criteria; minor impacts on coral and seagrass beds; dust and sediment managed by silt screens and EMMP

- Property implications: East Coast (D15) property holders should view Long Island as a long-term positive catalyst — ultimately creating new land, extended waterfront, and a future reservoir adjacent to Singapore’s most liveable eastern corridor

- Full reclamation: The preparatory works area is NOT the final Long Island profile; detailed plans will be developed through further technical studies and public engagement over the coming years

Singapore took a significant step forward on its most ambitious coastal infrastructure project on 30 June 2026, when the Urban Redevelopment Authority (URA) and the Housing & Development Board (HDB) jointly announced that preparatory marine works for the ‘Long Island’ project will begin from end-2026. For property owners and buyers along the East Coast corridor — particularly in District 15 (D15), Bedok (D16), and the Tampines/Pasir Ris eastern stretch — the announcement marks the formal start of a multigenerational transformation that will ultimately reshape Singapore’s entire southern coastline.

LovelyHomes has previously covered the Greater Southern Waterfront (GSW) — the western bookend of Singapore’s coastal transformation — in our Tanjong Pagar Neighbourhood Guide and East Coast Neighbourhood Guide. Long Island is the eastern counterpart: a critical flood protection measure that will eventually create new land and a future reservoir east of Bedok, protecting the entire East Coast from rising sea levels over the coming century.

What Are the Preparatory Works, Exactly?

Long Island is Singapore’s planned response to climate change and rising sea levels along its vulnerable East Coast. The full project — which will ultimately involve major land reclamation to create a new island and a freshwater reservoir — is a decades-long undertaking. What begins at end-2026 is the preparatory phase: essential marine construction works that lay the groundwork for eventual reclamation, but do not yet constitute reclamation itself.

The preparatory works involve three primary activities: removal of seabed obstructions (historical debris, hazards); construction of temporary sand bunds (underwater containment structures); and sand infilling within the bunded areas. These works will take place entirely offshore, at least 130 metres from the shoreline, and will be clearly demarcated by silt screens and floating barriers visible from the beach.

The works are split into two phases:

| Phase | Location | Area | Dimensions | Timing |

|---|---|---|---|---|

| Phase 1 | Waters west of Bedok Jetty | ~570 ha | ~7km long × up to 1km wide | Commences end-2026 |

| Phase 2 | Waters east of Bedok Jetty | ~155 ha | TBC | After SEA Games 2029 completion |

| Full Long Island | Entire East Coast offshore zone | ~2,000+ ha (indicative) | TBC through technical studies | Over several decades |

The deferral of Phase 2 until after the 2029 SEA Games is a deliberate accommodation: the waters east of Bedok Jetty are currently used for water sports and will host major aquatic events for the SEA Games. This sequencing shows that the government is managing the project’s community impact thoughtfully — a signal that should give East Coast residents some comfort about near-term disruption.

Environmental Findings: What the Study Revealed

HDB commissioned a formal Environmental Study covering the preparatory works, consulting nature groups on scope. The study’s key findings are reassuring for the majority of East Coast users:

Water quality: No significant changes expected; water will continue to meet Singapore’s prevailing marine water quality criteria throughout the works.

Currents and waves: Slight localised changes near Bedok Jetty are expected to have minimal impact on near-shore activities. Swimming can continue along the entire East Coast stretch.

Air quality and visibility: Up to minor visual impact from sand infilling operations; intermittent sediment plumes and dust are expected, mitigated by silt screen deployment and active dust monitoring under the Environmental Monitoring and Management Plan (EMMP).

Biodiversity: Some coral and seagrass beds found near the work site may experience short-term, localised impact from sediment plumes. However, the majority of coral and seagrass — including Sisters’ Islands Marine Park — is assessed as largely unaffected. HDB has committed to EMMP monitoring throughout.

Sea sports displacement: This is the most tangible near-term impact for active East Coast users. Kiteboarding is most affected; other sea sports face minor to moderate displacement. Agencies are working with affected user groups to identify alternative sites within the sea space east of Bedok Jetty in the interim.

What This Means for East Coast Property Buyers and Owners

For property owners in the East Coast corridor — covering D15 (Katong, Tanjong Katong, Marine Parade), D16 (Bedok, Siglap, Upper East Coast), and the eastern planning areas (Tampines, Pasir Ris, Changi) — the Long Island announcement is a long-term positive with a short-term noise caveat.

Short-term (2026–2029): Managed Disruption

The preparatory works will generate visible marine activity offshore — construction vessels, sand infilling operations, and temporary bunds. From the shoreline, this will be noticeable but distant (at least 130m offshore). Air quality impacts are expected to be minor and intermittent. Beaches remain open. The practical implication for property values is minimal in the short term: these works are a public infrastructure programme, not a lifestyle degradation, and they come with an explicit government commitment to environmental monitoring and mitigation.

Medium-term (2029–2035): Planning Uplift Begins

As the preparatory phase completes and the URA begins formal planning for Long Island’s reclamation profile, the East Coast will progressively benefit from the same planning-uplift dynamic that has historically preceded major Singapore waterfront transformations. When Marina Bay was being planned in the 1980s and 1990s, property in D1 and D2 began appreciating in anticipation of the new precinct long before a single building was complete. Long Island represents a similar, though slower, catalyst for the D15/D16 corridor.

Long-term (2035+): Transformative Uplift

When the full Long Island reclamation creates new land along the East Coast — including a future reservoir — the implications for D15 and D16 property are substantial: extended waterfront promenade access, reduced flood risk (supporting insurance and bank valuations), new residential parcels potentially creating supply (a risk to existing owners) but also major new amenity and connectivity (a positive for the precinct as a whole). The 2026 URA Q2 price data already showed D15 benefiting from TEL Stage 4 connectivity; the Long Island catalyst is additive to this structural tailwind over the 2030s and beyond.

| Horizon | Impact on East Coast Property | Key Risk |

|---|---|---|

| 2026–2029 (prep works) | Neutral to marginally negative optics; no material price impact expected | Marine activity visible from beachfront; minor sea-sport disruption |

| 2029–2035 (early planning) | Positive sentiment as Long Island masterplan solidifies; planning uplift begins | Timeline may slip; full reclamation profile remains unconfirmed |

| 2035+ (reclamation & beyond) | Transformative — new waterfront, reduced flood risk, new amenity corridors | New residential supply on Long Island may moderate prices on existing stock |

Public Engagement and What Comes Next

The URA reiterated in the 30 June 2026 announcement that Singapore’s commitment to public engagement on Long Island planning remains firm. The government has engaged more than 14,000 people to date on Long Island’s vision. From end-2026, a new phase of public engagement will invite Singaporeans to shape key planning topics including recreational uses along the new coastline, the design of the future reservoir, and the character of new precincts that will eventually emerge.

Crucially, the URA clarified that the area used for preparatory works is not the final Long Island land profile. The reclamation profile will be determined through subsequent technical studies — covering environmental impact assessments for the actual reclamation, engineering studies, and further public engagement — expected to take several more years. Main reclamation works will only commence after these studies are complete and mitigation measures are determined.

The Environmental Study report was published for public feedback for four weeks from 30 June 2026. Members of the public may view it and submit feedback at go.gov.sg/long-island.

Frequently Asked Questions: Long Island and East Coast Property

Will the preparatory works affect East Coast Park beach access?

No. All beaches along East Coast Park will remain open throughout the preparatory works. Near-shore swimming can continue along the entire stretch of the East Coast. Exercise paths and tracks for jogging and cycling also remain fully accessible. The works are offshore (at least 130m from the shoreline) and cordoned off for public safety. Safety advisories will be posted at East Coast Park and on government agency websites.

How might Long Island affect property values in D15 and D16?

In the short term (2026–2029), the preparatory works are unlikely to have a material impact on property values in D15 (Marine Parade, Katong, Tanjong Katong) or D16 (Bedok, Upper East Coast, Siglap). The works are offshore, temporary, and environmentally monitored. In the medium to long term, Long Island is broadly a positive catalyst for the East Coast corridor — creating new waterfront, improved flood protection, and eventually new amenities. However, buyers should note that full Long Island reclamation is decades away and carries execution and timeline uncertainty. Purchase decisions should be based on the neighbourhood’s existing merits, with Long Island treated as optionality, not a near-term price driver.

What is the difference between the preparatory works and the main Long Island reclamation?

The preparatory works (beginning end-2026) involve seabed clearance, temporary bund construction, and sand infilling — foundational marine works that create the conditions for eventual reclamation without being the reclamation itself. The area used for preparatory works is not the final land profile of Long Island. The main reclamation works — which will actually create the new island — will only commence after the government completes further technical studies, determines mitigation measures, and incorporates feedback from additional public engagement rounds. This could be many years away. Think of the preparatory works as clearing and grading a site before construction, not as the construction itself.

Will Long Island create new HDB or private residential areas in the future?

Long Island’s ultimate land use profile — including any residential development — has not been finalised. The URA has noted that planning will incorporate findings from technical studies and public engagement, and that the government retains flexibility to meet evolving national needs. Historically, Singapore’s reclaimed land has been used for a mix of residential, commercial, and infrastructure purposes. It is reasonable to expect that some Long Island land will eventually be developed for housing, but the specific profile, tenure, and density remain undecided. Any residential development on Long Island is likely to be 15–25 years away.

Can I still use East Coast Park for water sports during the works?

Most water sports can continue, but with some adjustment. Near-shore swimming is unaffected. However, sea sports that require more sea space — particularly kiteboarding — will be the most significantly impacted, as the Phase 1 work area covers much of the sea space west of Bedok Jetty. Agencies are working with affected groups to identify alternative sites, including the sea space east of Bedok Jetty (until Phase 2 begins post-2029). Recreational paddling, kayaking, and water skiing in near-shore areas should be largely unaffected, though users should maintain safe distances from vessels and the cordoned work area.