Singapore HDB Grants Guide 2026: EHG, Family Grant, PHG and All CPF Housing Grants Explained

⚡ Quick Answer — HDB CPF Housing Grants at a Glance (2026)

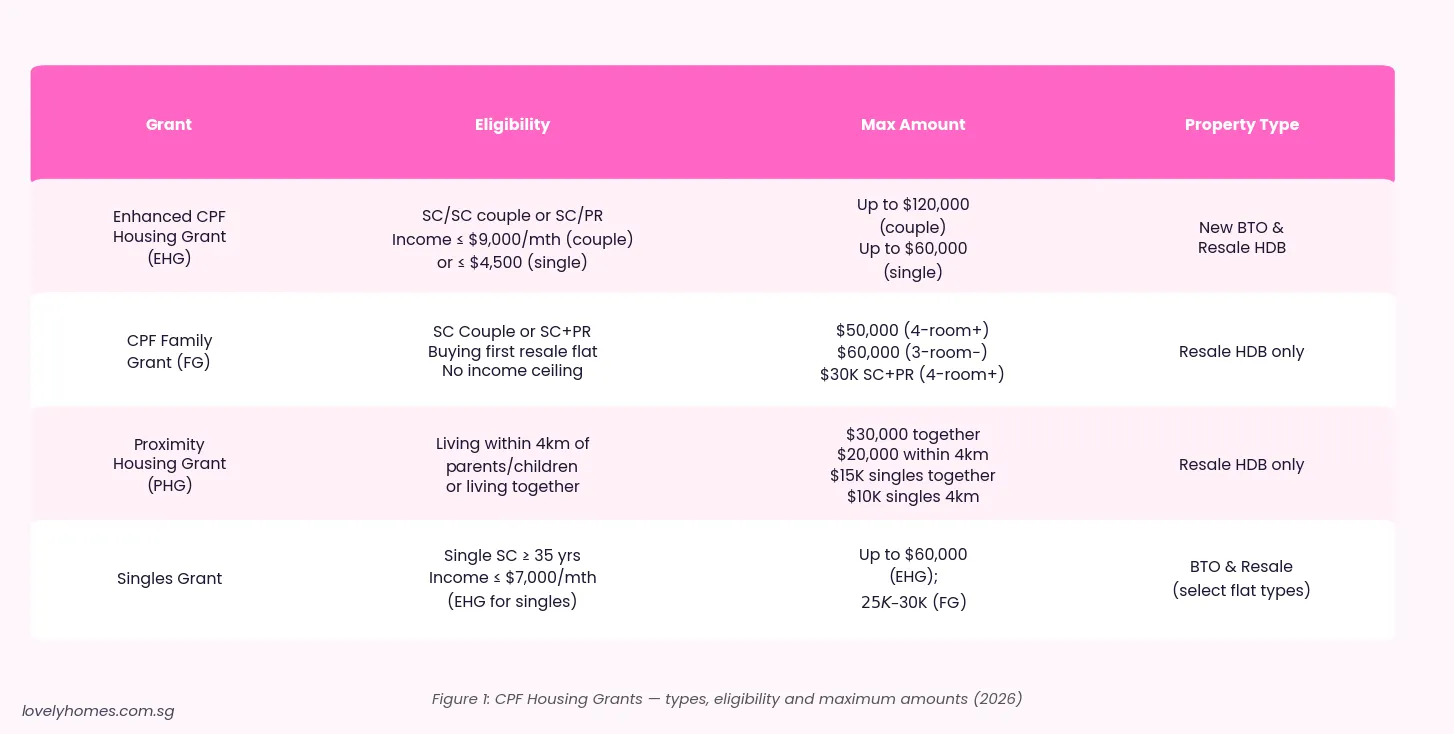

- Enhanced CPF Housing Grant (EHG): up to $120,000 for eligible couples; $60,000 for singles — applies to both BTO and resale flats, income ceiling $9,000/mth (couple).

- CPF Family Grant (FG): $50,000–$60,000 for eligible SC-SC couples buying a resale flat; no income ceiling applies.

- Proximity Housing Grant (PHG): up to $30,000 to live with or near parents/children — resale flats only.

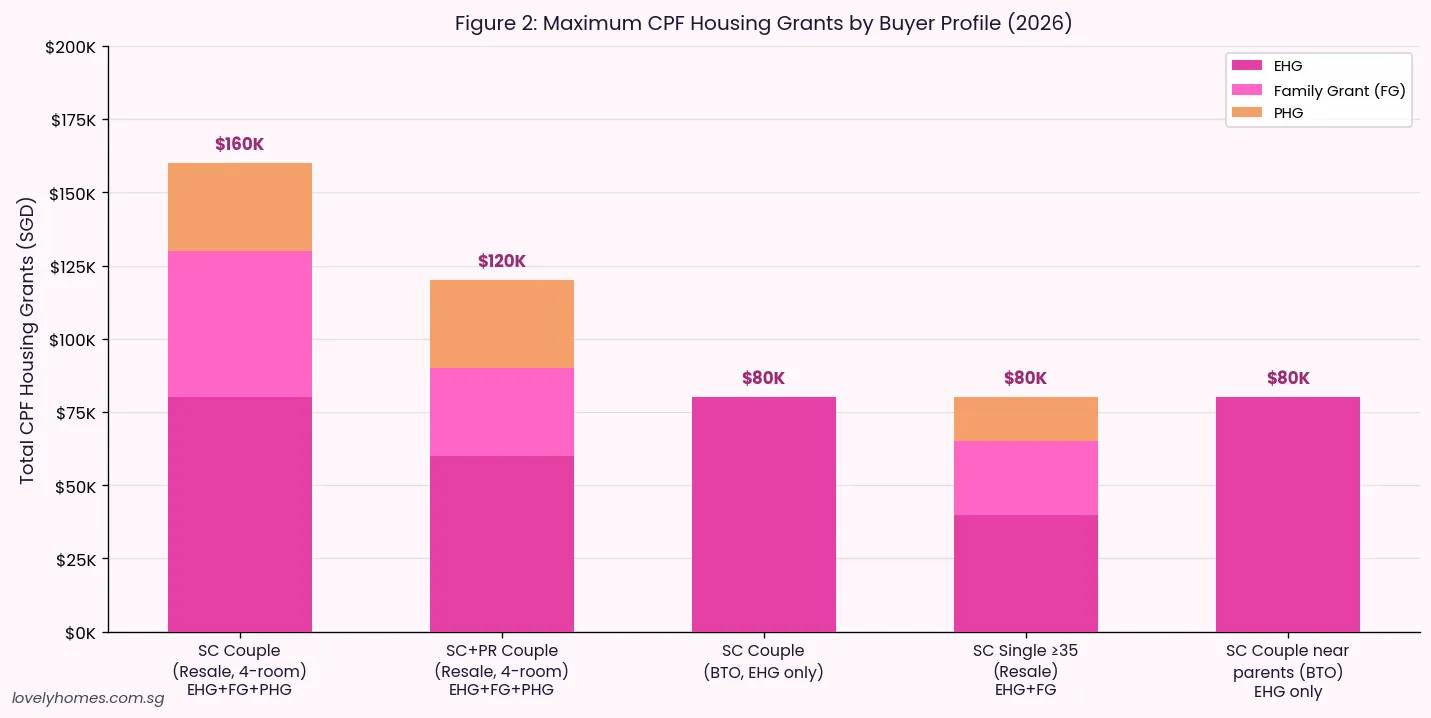

- Grants can be stacked: a first-timer SC couple buying a resale flat near parents could qualify for EHG + FG + PHG = up to $160,000 in total grants.

- Grants are credited to CPF Ordinary Account (OA) and deducted from the purchase price; they reduce your outstanding loan and accrued interest.

- Second-timers may still access PHG (resale only) and a reduced FG if one party is a first-timer.

- All grants are administered by HDB and disbursed via CPF Board — you apply through the HDB Flat Portal after obtaining an HDB Flat Eligibility (HFE) letter.

What Are CPF Housing Grants?

CPF housing grants are cash subsidies that the Singapore Government channels through the Central Provident Fund (CPF) Ordinary Account to help eligible buyers afford Housing & Development Board (HDB) flats. Unlike the earlier Building & Construction Authority rebates or direct handouts, these grants go directly into the buyer’s CPF OA and are credited against the flat’s purchase price — reducing the loan quantum and, over the life of the mortgage, the accrued interest the buyer ultimately owes CPF.

The grant framework has evolved significantly since the early 2000s. The Additional CPF Housing Grant (AHG) and Special CPF Housing Grant (SHG) were consolidated and superseded on 11 September 2019 by the Enhanced CPF Housing Grant (EHG), which provides a single, tiered subsidy that scales down with household income. The Family Grant and Proximity Housing Grant, both introduced in 2015 for resale flat buyers, remain active. Together, these three grant streams — EHG, FG, PHG — form the backbone of Singapore’s HDB affordability architecture in 2026.

Enhanced CPF Housing Grant (EHG) — The Foundation Grant

The EHG, introduced in September 2019, is the primary income-based subsidy for first-timer buyers. Unlike its predecessors, the EHG applies to both new BTO flats and resale flats, eliminating a long-standing disparity where resale buyers received less support than BTO buyers. HDB administers the scheme; CPF Board disburses the funds.

EHG Eligibility Criteria

To qualify for EHG, the household must meet all of the following:

| Criterion | Couples / Families | Singles (≥ 35 years old) |

|---|---|---|

| Citizenship | At least one Singapore Citizen | Singapore Citizen |

| Gross Monthly Income | ≤ $9,000/month | ≤ $4,500/month |

| Prior Housing Grant | Must not have received AHG or SHG previously | Same |

| Flat Type (BTO) | Any HDB flat type (2-room Flexi to 5-room) | 2-room Flexi (BTO) only |

| Flat Type (Resale) | Any eligible resale flat | 2-room or 3-room resale only |

| Continuous Employment | At least one applicant employed for ≥ 12 months continuously | Same |

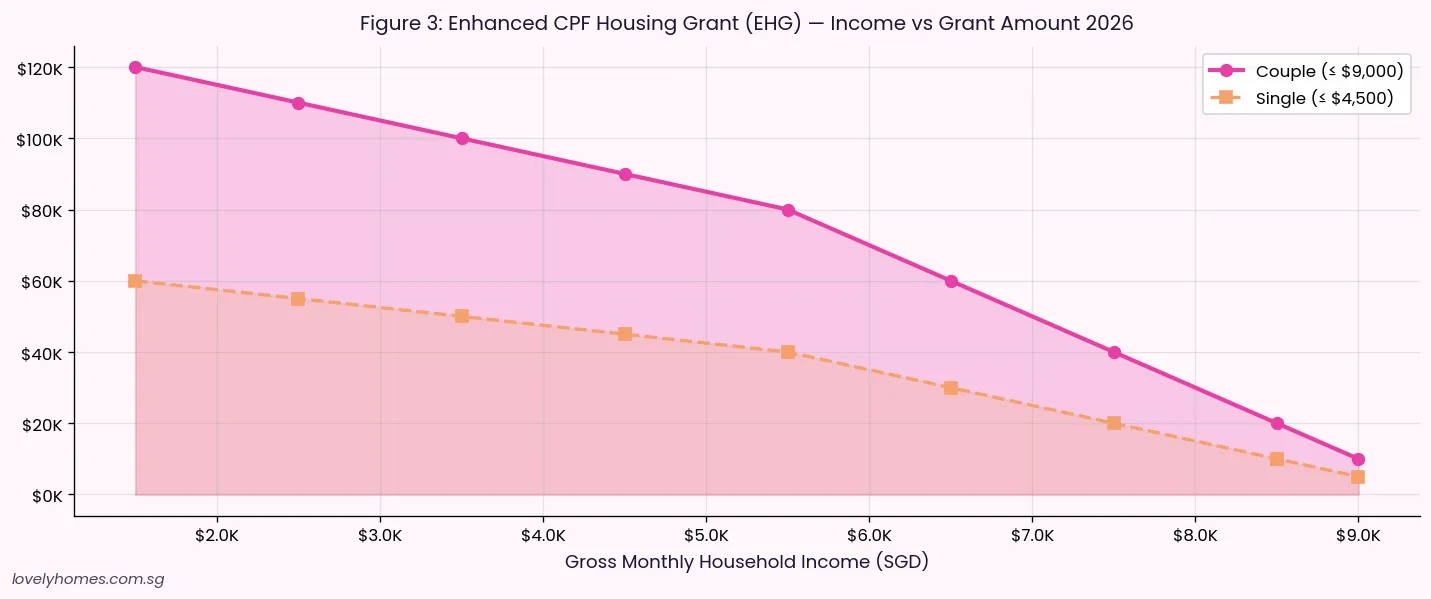

The EHG quantum scales inversely with income: buyers at the bottom of the income band receive the maximum grant, while those approaching the $9,000 ceiling receive the minimum. The grant is calculated based on the average gross monthly household income over the preceding 12 months.

EHG Grant Amounts

For couples with a household income at or below $1,500/month, the maximum EHG is $120,000. The grant steps down by $5,000 for every additional $500 in household income until it reaches a minimum of $5,000 at the $8,500–$9,000 income band. Singles receive exactly half the couple quantum at each band (maximum $60,000 at ≤$750/month income). The EHG is credited to the buyer’s CPF OA and applied to the purchase price at completion.

CPF Family Grant (FG) — For Resale Flat Buyers

The CPF Family Grant targets first-timer buyers purchasing a resale HDB flat and does not have an income ceiling — making it accessible to middle-income households that earn too much for the EHG. The Family Grant replaced the Additional CPF Housing Grant (Resale) in 2015 and has remained structurally unchanged since.

Family Grant Amounts by Flat Type and Household Composition

| Buyer Profile | Resale Flat ≤ 3-room | Resale Flat 4-room+ |

|---|---|---|

| SC + SC Couple (first-timer) | $60,000 | $50,000 |

| SC + PR Couple (first-timer SC) | $40,000 | $30,000 |

| SC Single (≥ 35 yrs, first-timer) | $30,000 | $25,000 |

Where one spouse is a second-timer and the other is a first-timer, the couple may receive half the applicable Family Grant. The Family Grant is not available for BTO flats — that distinction is important for buyers weighing resale against new launches.

Proximity Housing Grant (PHG) — Living Near Loved Ones

The Proximity Housing Grant encourages multi-generational living arrangements by subsidising buyers who choose to live with, or within 4 kilometres of, their parents or children. Available for resale flats only, it was introduced in 2015 to address Singapore’s social goal of strengthening family ties and providing informal eldercare support networks.

PHG Amounts

| Living Arrangement | SC-SC Couple | SC-PR or Single |

|---|---|---|

| Living with parents / child (in same flat) | $30,000 | $15,000 |

| Living within 4 km of parents / child | $20,000 | $10,000 |

The PHG is granted based on the residential address of the parent or child at the time of application. There is no income ceiling. However, buyers must satisfy a 5-year occupation requirement: if they move away from the stated proximity within 5 years of flat completion, the grant is subject to clawback by HDB.

Step-Up CPF Housing Grant (SHG)

The Step-Up CPF Housing Grant is a smaller, targeted subsidy of up to $15,000 for second-timer households who currently live in 2-room flats and are upgrading to a larger BTO flat (3-room or bigger) in a non-mature estate. Unlike EHG, FG and PHG — which are first-timer grants — SHG is specifically for second-timers making an upward move. The household income ceiling for SHG is $7,000 per month.

SHG is far less commonly used than the three main grants, but it plays an important role for low-income second-timer families who need more space but cannot afford private property.

Summary: All HDB Grants at a Glance

| Grant | Max Amount | Income Ceiling | BTO? | Resale? | First-timer? |

|---|---|---|---|---|---|

| EHG (couple) | $120,000 | $9,000/mth | ✓ | ✓ | Yes |

| EHG (single) | $60,000 | $4,500/mth | ✓ (2-room) | ✓ (≤3-room) | Yes |

| Family Grant (SC-SC) | $60,000 | None | ✗ | ✓ | Yes (both) |

| Family Grant (SC-PR) | $40,000 | None | ✗ | ✓ | Yes (SC spouse) |

| Proximity Housing Grant | $30,000 | None | ✗ | ✓ | Both tiers |

| Step-Up Grant (SHG) | $15,000 | $7,000/mth | ✓ (≥3-room) | ✗ | Second-timer |

Worked Example: How Much Can a First-Timer Couple Receive?

📺 Case Study — the Wong Family

Profile: Mr and Mrs Wong, both Singapore Citizens, both first-timers. Combined gross income $6,200/month. Buying a 4-room resale flat in Ang Mo Kio for $650,000. Mrs Wong’s parents live in the same estate (within 4 km).

EHG: Income $6,200 → falls in $6,000–$6,500 band → EHG = $60,000.

Family Grant (FG): SC-SC couple, 4-room resale → $50,000 (no income ceiling).

Proximity Housing Grant (PHG): Living within 4 km of Mrs Wong’s parents → $20,000.

Total grants = $130,000 credited to their combined CPF OA.

Effective purchase price: $650,000 − $130,000 = $520,000.

HDB Loan (80% LTV on $520,000 effective): $416,000. Monthly instalment at 2.60% p.a. over 25 years ≈ $1,886/month. MSR check: $1,886 / $6,200 = 30.4% — marginally above 30% MSR. The couple reduces their loan to $390,000 using additional CPF savings, bringing the monthly instalment to $1,770/month (MSR 28.5%, PASS).

Key takeaway: Without the grants, the Wongs would need a $520,000 loan; with grants, their effective loan burden drops by 25%. Grants reduce lifetime accrued interest by an estimated $48,000 over 25 years.

Why Housing Grants Matter for Singapore’s Property Affordability

Singapore’s CPF housing grant framework is one of the most generous owner-occupier subsidy systems in developed Asia. The EHG alone — at up to $120,000 for eligible couples — represents roughly 15%–20% of the purchase price of a 4-room or 5-room flat in many non-mature estates. When stacked with the Family Grant and PHG, the aggregate subsidy can exceed $160,000, decisively reducing the loan quantum and monthly servicing burden for lower- and middle-income families.

The policy rationale is threefold. First, it sustains home-ownership rates: Singapore’s resident home-ownership rate has remained above 88% for over two decades, among the highest globally, partly because of demand-side grants that reduce the effective cost to buy. Second, grants embedded in CPF rather than cash reduce the risk of inflation in the resale market — sellers cannot directly “see” the grant quantum and adjust prices accordingly in the way they might with a cash handout. Third, by tiering EHG to income and removing the income ceiling on FG, HDB broadens access across the income spectrum: lower-income families get the largest EHG; middle-income families (who earn too much for EHG) still benefit from FG.

The PHG specifically addresses Singapore’s demographic challenge: with a rapidly ageing population, encouraging younger families to live near or with their parents reduces formal eldercare costs while maintaining social cohesion in mature estates. HDB data has historically shown a meaningful uptick in resale transaction volumes in estates with a large elderly population whenever PHG quantum is adjusted upward.

What Might Come Next: Grant Outlook

The EHG has not been adjusted since its introduction in September 2019. With Singapore’s median household income rising steadily — the median resident household income grew from $9,520 in 2019 to approximately $11,200 by 2025 — the real coverage of the EHG income ceiling has gradually eroded. An increasing share of first-timer households now earn above $9,000/month and are therefore ineligible for EHG even for their first BTO flat.

Industry observers anticipate that the next round of grant revisions could raise the EHG income ceiling or adjust the grant quantum bands, possibly linked to a broader review of BTO pricing and the housing affordability framework. HDB has historically reviewed grant levels every five to seven years. With the next review potentially due in 2025–2027, buyers with incomes close to the current ceilings should monitor MND/HDB announcements closely. Any upward revision to EHG or FG would directly benefit middle-income first-timers locked out of the current framework.

FAQ: HDB CPF Housing Grants 2026

Can I receive CPF housing grants for a BTO flat and a resale flat in my lifetime?

Only if you are a genuine first-timer for each purchase — which is almost never possible, since receiving the EHG for your BTO flat makes you a grant recipient and therefore ineligible for EHG again. However, you may qualify for PHG (resale only, no income ceiling) as a second-timer if you meet the proximity requirement. First-timer status resets only in very limited circumstances, such as divorce where neither party retains the flat and no grant was previously disbursed.

Does receiving a CPF housing grant affect how much I need to repay CPF when I sell?

Yes. Grants credited to your CPF OA are treated as CPF withdrawals. When you sell the flat, you must refund the principal grant amount plus accrued interest at the CPF OA rate (currently 2.5% per annum, compounded annually) back into your CPF account. This does not mean you “lose” the money — it remains in your CPF for retirement — but it does reduce the net cash proceeds you receive on sale. Buyers often underestimate this accrued-interest obligation, particularly for long holding periods.

Can I use CPF housing grants to pay for ABSD?

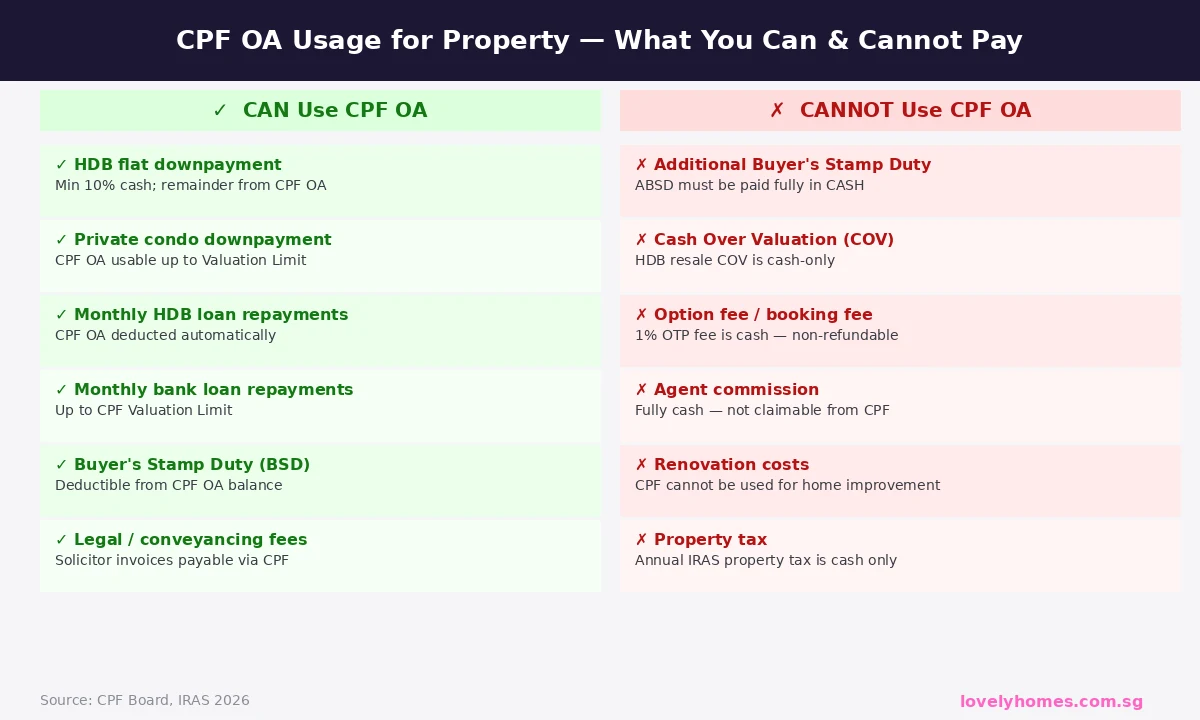

No. Additional Buyer’s Stamp Duty (ABSD) must be paid in cash within 14 days of signing the Agreement for Lease (for BTO) or the Sales & Purchase Agreement (for resale). CPF funds — including housing grants — cannot be used to pay ABSD, stamp duties, or Cash Over Valuation (COV). Only Buyer’s Stamp Duty (BSD) may be paid via CPF OA.

Can Singapore Permanent Residents (PRs) receive CPF housing grants?

PRs are ineligible for CPF housing grants on their own. However, a SC-PR couple buying their first resale HDB flat together qualifies for the Family Grant (reduced quantum — $30,000 for 4-room+, $40,000 for 3-room or smaller) provided the Singapore Citizen spouse is a first-timer. PRs are not eligible for EHG or PHG in their own right. PRs also cannot purchase new BTO flats.

What happens if I sell my flat within the Minimum Occupation Period (MOP)?

HDB grants are linked to the Minimum Occupation Period. If you sell your flat before satisfying the MOP (5 years for most BTO and resale flats; 10 years for PLH BTO flats under the Prime Location Public Housing model), you must refund all housing grants received, on top of repaying the CPF principal and accrued interest. Early sale also attracts resale levy obligations for subsidised flat owners.

Are grants available for Executive Condominiums (ECs)?

Yes, but only the Family Grant and an EC-specific variant. First-timer SC-SC couples buying a new EC may receive a Family Grant of $30,000. The EHG is not applicable to ECs. EC buyers must also satisfy the EC income ceiling of $16,000/month gross household income, and must not own or have disposed of any private residential property in the 30 months before the EC application.

How do I apply for CPF housing grants?

Grants are applied for through the HDB Flat Portal (flat.gov.sg) as part of the HDB Flat Eligibility (HFE) letter application — or via the Sales of Balance Flats / BTO application process. You do not need to file a separate grant application; HDB assesses your eligibility automatically based on the information submitted in the HFE or flat application. The HFE letter will specify the grants you qualify for and the indicative amounts before you commit to a purchase.