HDB Resale Prices Fall for Second Consecutive Quarter in Q2 2026: RPI Slips to 202.7

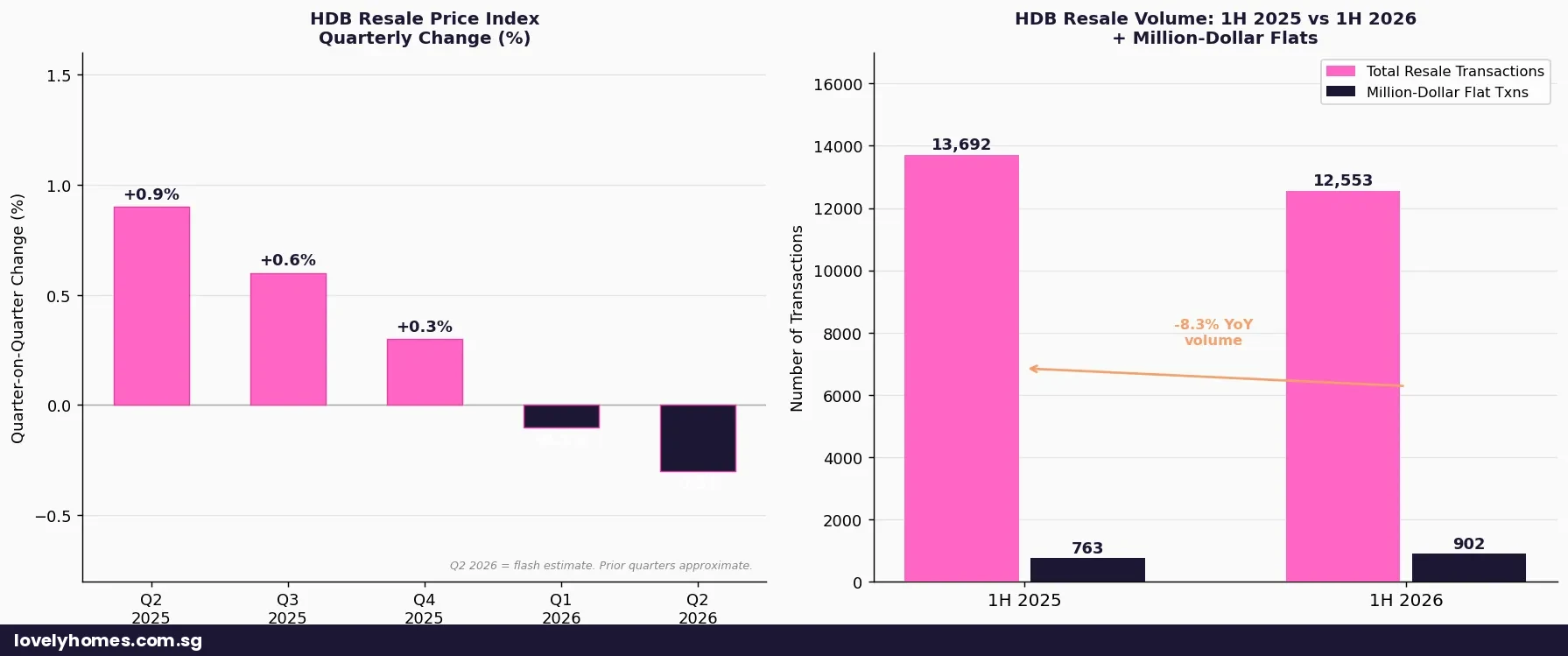

- The HDB Resale Price Index (RPI) fell 0.3% in Q2 2026 (quarter-on-quarter), bringing the index to 202.7. This is the second consecutive quarterly decline.

- Combined with Q1 2026’s −0.1%, this marks the first back-to-back decline since the four-quarter fall from Q3 2018 to Q2 2019.

- Resale volume in Q2 2026: 6,268 transactions — nearly unchanged from Q1’s 6,285, but the 1H 2026 total of 12,553 is 8.3% below 1H 2025’s 13,692.

- Million-dollar flat transactions rose to 491 in Q2 2026 alone, bringing 1H 2026 to 902 — surpassing the 763 recorded in all of 1H 2025.

- These are flash estimates released by HDB on 1 July 2026; full Q2 2026 statistics are expected around 23 July 2026.

- The decline reflects the combined impact of property cooling measures (15-month wait-out period, tightened HDB loan conditions introduced in 2023–2024) and increased BTO supply.

- Private property prices rose 0.5% in Q2 2026, widening the gap between the HDB resale and private residential markets.

HDB Resale Prices Slip for the Second Consecutive Quarter

Singapore’s public housing resale market posted its second consecutive quarterly price decline in Q2 2026, according to flash estimates released by the Housing and Development Board (HDB) on 1 July 2026. The HDB Resale Price Index fell 0.3% to 202.7, following the 0.1% dip recorded in Q1 2026.

While the absolute magnitude of the decline remains modest, the back-to-back nature of the falls is significant. Prior to Q1 2026, the HDB resale market had not recorded a single quarterly price decline since Q3 2018 — a stretch of more than six years of unbroken price appreciation that weathered the COVID-19 pandemic, successive rounds of cooling measures, and record-breaking million-dollar flat transactions.

The Q2 2026 data points to a market that is adjusting — gradually but meaningfully — to higher interest rates, an expanded BTO supply pipeline, and the cumulative weight of demand-side cooling measures introduced since September 2022. At the same time, the continued surge in million-dollar flat transactions to 491 in Q2 suggests that the prestige end of the market remains resilient, even as broad prices soften.

Reading the Data: Three Dimensions

Price: The Second Consecutive Dip

The 0.3% decline in Q2 2026 follows the 0.1% fall in Q1, giving a cumulative 1H 2026 decline of approximately 0.4% from the Q4 2025 peak. In absolute terms, the RPI at 202.7 is approximately 2.5% below the peak recorded in Q3 2023 (estimated 207.8), when a series of aggressive cooling measures first began to deflect demand. For context, the RPI stood at roughly 168 before the pandemic surge of 2020 — meaning prices are still some 20% above pre-pandemic levels even after the current decline.

Volume: Stable Quarter but Down Year-on-Year

At 6,268 transactions, Q2 2026 resale volume was broadly steady versus Q1’s 6,285. The constancy suggests that the market is softening on price, not experiencing a liquidity freeze — there is still a functioning market of willing buyers and sellers. However, the 1H 2026 total of 12,553 transactions is 8.3% below the 13,692 recorded in 1H 2025, signalling that fewer households are choosing to enter or exit the HDB resale market compared to a year ago. This may reflect buyers waiting for BTO completions, or sellers reluctant to accept lower prices.

Million-Dollar Flats: The Paradox of Rising Premium Transactions

The 491 million-dollar resale transactions in Q2 2026 is one of the highest quarterly counts on record, bringing the 1H 2026 total to 902 — compared to 763 in 1H 2025. This appears paradoxical given the broader price decline. The explanation lies in composition: a greater proportion of large, well-located flats (such as mature-estate 5-Rooms, Executive flats in Bishan, Queenstown, and Toa Payoh, and high-floor units with unobstructed views) are transacting at S$1 million or above, even as median prices for standard flat types ease. The million-dollar threshold is increasingly a function of location and flat specifications rather than broad market inflation.

Why Are HDB Resale Prices Falling?

Several structural and policy-driven factors help explain the shift:

- BTO supply ramp-up: HDB is on track to launch approximately 19,600 new BTO flats in 2026 alone, including major tranches in Tengah, Bedok, and Toa Payoh. A substantial portion of buyers who might otherwise have purchased resale flats are opting to wait for BTO completions, particularly after the government’s introduction of the Plus and Prime flat classifications in 2024 which offer new flats in desirable locations at subsidised prices.

- 15-month wait-out period: the wait-out period imposed in September 2022 — requiring owners of private residential properties to wait 15 months before purchasing a resale HDB flat — has reduced upgrader-to-downgrader demand for HDB resale. Private property owners who previously used HDB resale as a “cashing out” destination are constrained.

- Tighter HDB loan criteria: the reduction in HDB concessionary loan LTV from 85% to 80% introduced in 2023, combined with HDB’s stress test at 3.0%, has reduced the maximum loan quantum for some buyers, dampening purchasing power.

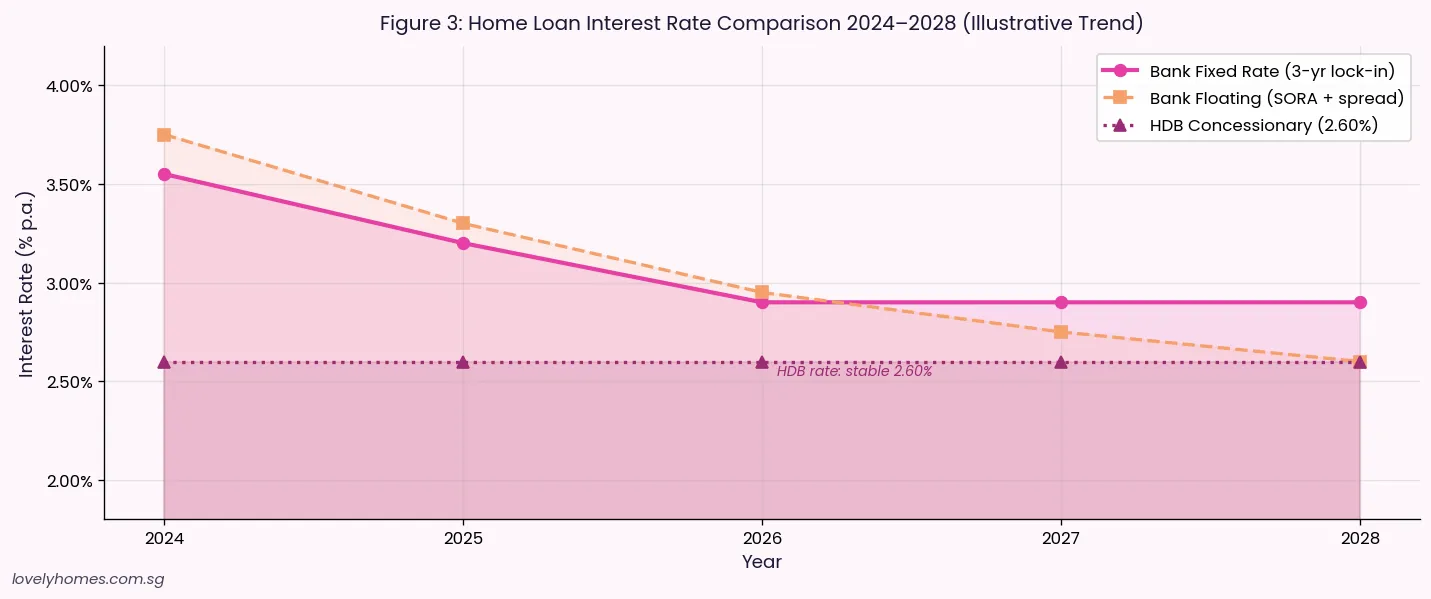

- Interest rate environment: while Singapore interbank rates have moderated from 2022–2023 peaks, bank mortgage rates remain above 2.5%, increasing monthly repayment obligations and constraining affordability relative to the 2019–2020 era when rates were near zero.

What the Data Means for Buyers and Sellers

For buyers, two consecutive declining quarters represent a modest but real opportunity to negotiate. The market is softer than at any point since 2019, and sellers are generally more realistic about pricing than during the frenzy of 2021–2023. However, buyers should not expect a dramatic correction — the fundamental demand for housing in Singapore remains strong, and government policy is explicitly designed to maintain market stability rather than to allow sharp corrections.

For sellers, the data confirms that the period of listing and achieving above-valuation prices within days has passed in most segments. Realistic pricing at or near recent transacted values — checked via HDB’s HDB Resale Flat Prices portal — is now essential for a timely sale. Premium-location flats (mature estates, near MRT, high floor) continue to command strong demand even as median prices ease.

| Metric | Q1 2026 | Q2 2026 (Flash) | Change |

|---|---|---|---|

| HDB Resale Price Index (RPI) | ~203.3 | 202.7 | −0.3% QoQ |

| Consecutive quarters of decline | 1 (first since 2018) | 2 | ↑ |

| Resale transactions | 6,285 | 6,268 | −0.3% |

| 1H 2026 vs 1H 2025 volume | 12,553 vs 13,692 | −8.3% YoY | |

| Million-dollar flat transactions | 411 (1H total partial) | 491 | 1H total: 902 (+18.2% vs 1H 2025) |

| Full data release | ~23 July 2026 (HDB full Q2 2026 statistics) | ||

Table 1: HDB Resale Market Q2 2026 Flash Estimate Summary. Source: HDB, 1 July 2026.

What Might Come Next

The full Q2 2026 HDB resale statistics — due around 23 July 2026 — will provide complete data including town-by-town breakdowns, flat-type analysis, and cash-over-valuation (COV) trends. LovelyHomes will publish a comprehensive analysis at that time.

Looking ahead, the direction of HDB resale prices through the second half of 2026 will be shaped primarily by the pace of BTO completions and move-ins (which should free up additional resale supply), the trajectory of interest rates in Singapore (closely linked to US Federal Reserve policy), and any policy adjustments HDB may announce in the August or October BTO exercises. Market consensus among analysts tracked by LovelyHomes suggests a further modest decline of 0–1% in Q3 2026 before the market stabilises around year-end.

Frequently Asked Questions

What is the HDB Resale Price Index (RPI) and how is it calculated?

The HDB Resale Price Index is a measure published by the Housing and Development Board that tracks movements in the overall level of resale flat prices in Singapore. It is calculated using a hedonic regression model that controls for factors such as flat type, floor area, storey height, remaining lease, and location, allowing like-for-like comparison across periods. The index base year is Q1 2012 = 100. A reading of 202.7 in Q2 2026 means that prices are broadly 102.7% above Q1 2012 levels. The flash estimate published in the first week of each quarter uses a partial transaction dataset; the final figure is revised approximately three weeks later when the full quarter’s data is available.

Does a second consecutive quarterly decline mean the market is crashing?

No. A cumulative decline of 0.4% over two quarters is far from a crash — by any measure it represents a gentle correction after a multi-year price surge. For context, the 2018–2019 cooling cycle saw four consecutive quarters of decline totalling approximately 4% before prices stabilised and resumed their upward trend. The current environment is different: housing supply is expanding deliberately via BTO, borrowing conditions are tighter, and government policy is actively calibrated to engineer a soft landing rather than a correction. Buyers should view the current data as a modest softening, not a distress signal.

Should I wait for further price falls before buying an HDB resale flat?

Market timing in property is notoriously difficult, even for professional analysts. If your housing need is immediate — for example, you have a growing family, your existing lease is ending, or you have just passed the five-year MOP on your current flat — then market timing is largely irrelevant: the right time to buy is when it meets your household’s needs and financial capacity. If you are buying purely as an investment or as an upgrade with flexibility on timing, then the current softening does offer a more favourable negotiating environment than 2022 or 2023. However, attempting to call the exact bottom is speculative. For personalised financial planning, consult a licensed financial adviser.

Why are million-dollar flat transactions rising even as the overall RPI falls?

The million-dollar threshold is not itself a price index — it is a count of transactions above S$1 million regardless of flat size or type. The rising count reflects several factors: more large flats (5-Room and Executive) in desirable mature estates were completed with MOP five or more years ago and are now entering the resale market; the premium placed on location, floor height, and remaining lease has widened the spread between ordinary and premium flats; and a cohort of upgrading couples with substantial CPF savings and equity from earlier BTO flats are willing to pay for well-located resale units. In essence, the prestige segment is diverging from the mass-market segment within the same index.

When will the full Q2 2026 HDB resale statistics be released?

The full Q2 2026 HDB resale statistics are expected around 23 July 2026, based on HDB’s historical release calendar. The full data will include town-by-town price indices, volume by flat type and estate classification (mature vs non-mature), median resale prices by town, and COV trends. LovelyHomes will publish a comprehensive analysis at that time — see our ongoing Singapore Private Property Market Q2 2026 coverage for context on the broader residential market.

Related Articles

- HDB Resale Price Index Q1 2026: First Quarterly Decline in Seven Years

- Singapore Private Property Prices Q2 2026: URA Flash Estimate +0.5%

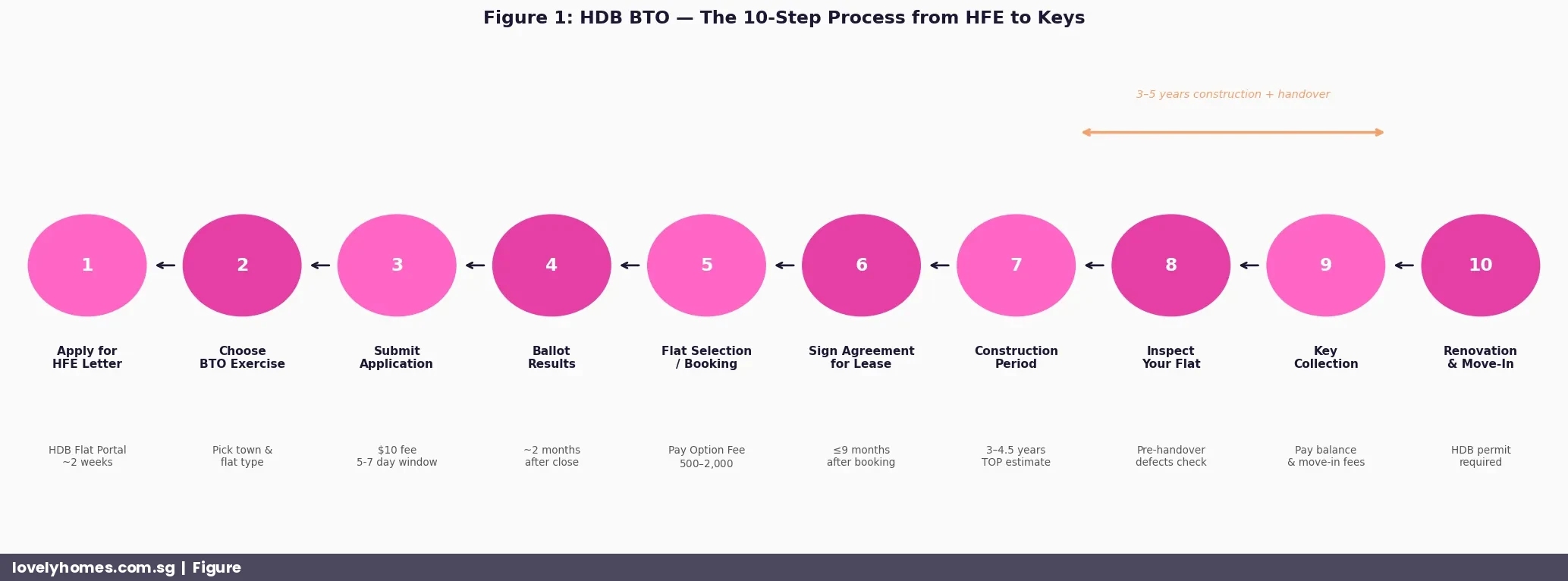

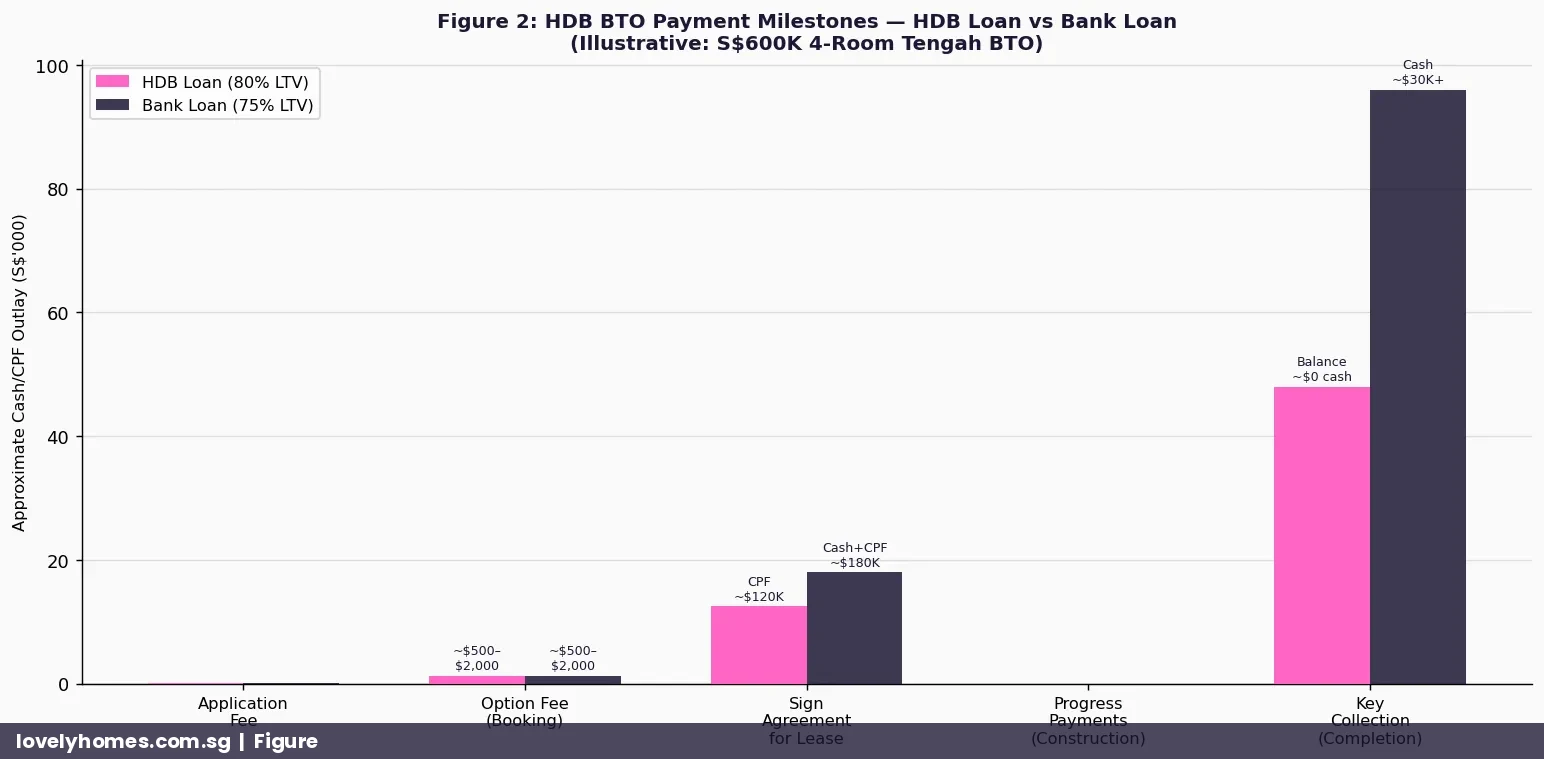

- Singapore HDB Resale Buying Process Guide 2026: Step-by-Step from HFE to Keys

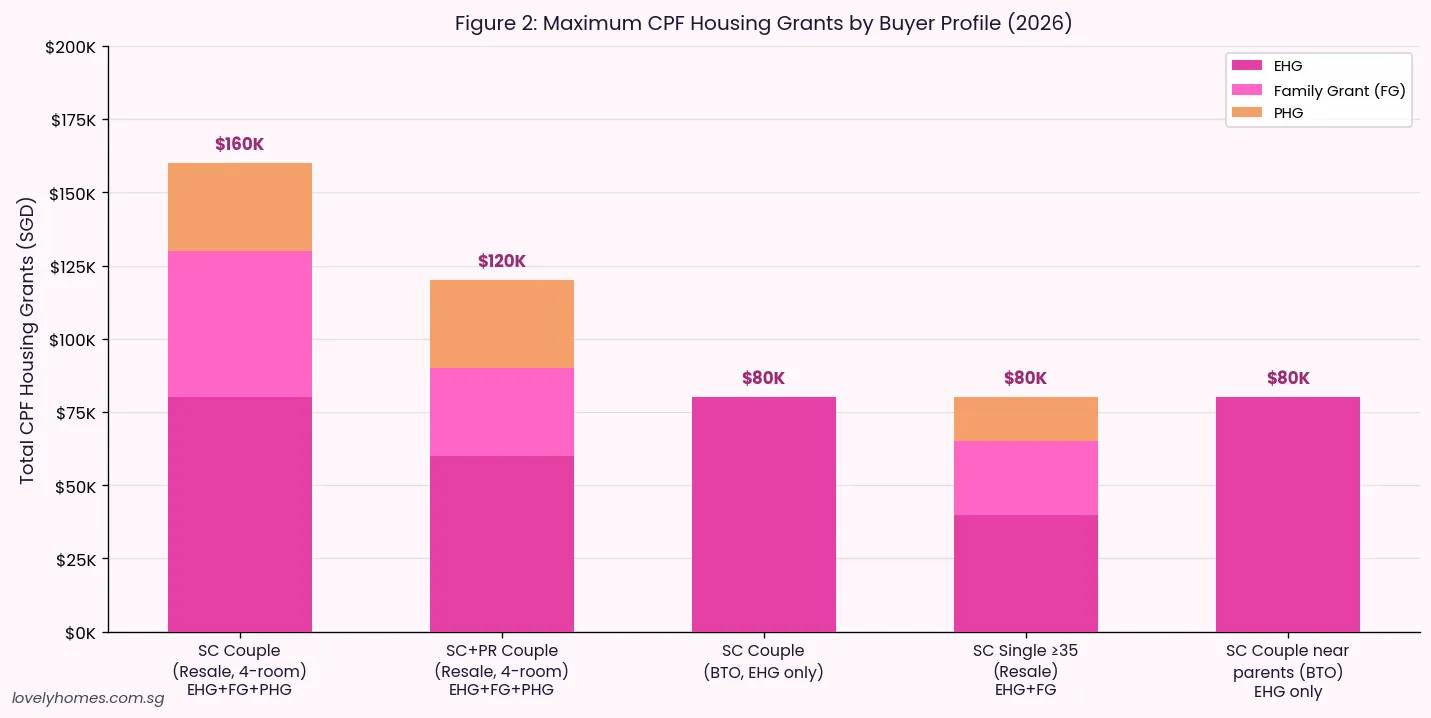

- Singapore HDB Grants Guide 2026: EHG, Family Grant, PHG and All CPF Housing Grants

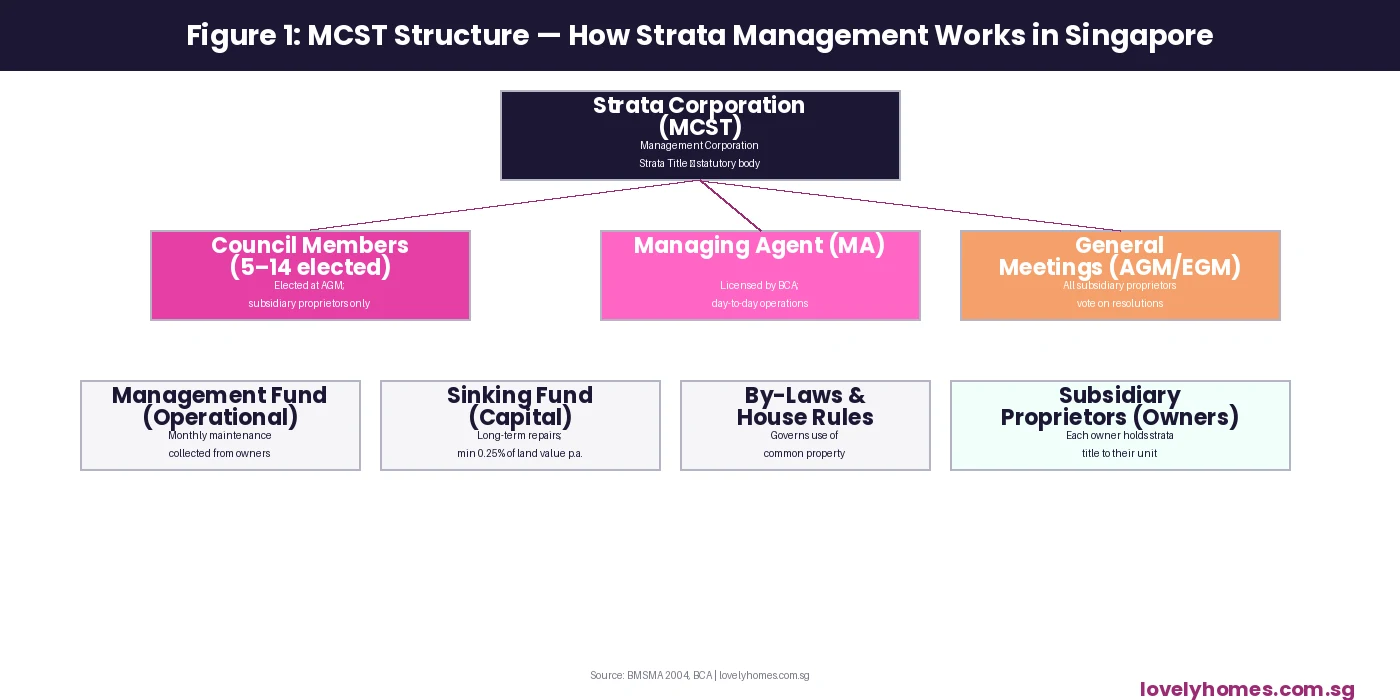

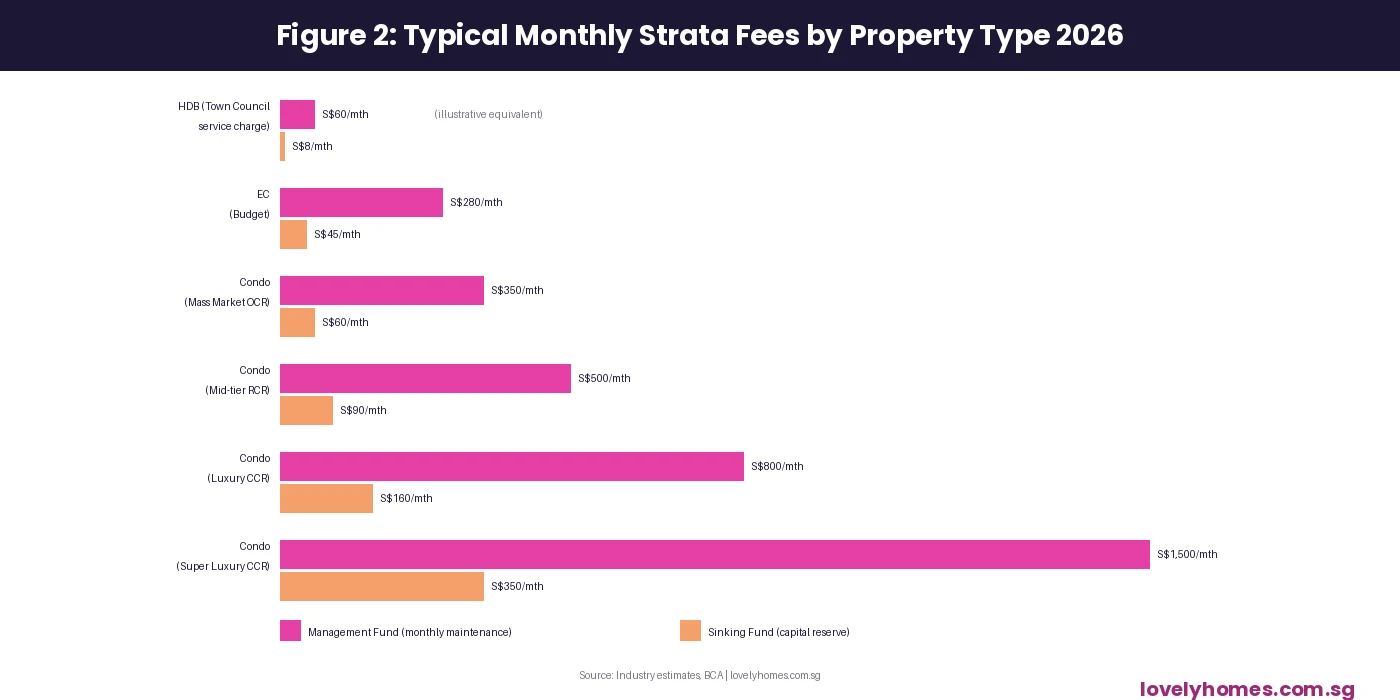

- Singapore Property Cooling Measures 2026: Complete Guide to ABSD, TDSR, LTV and SSD

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer

This article is published by LovelyHomes Editorial Team based on HDB flash estimates released on 1 July 2026. Flash estimates are preliminary and subject to revision when full Q2 2026 data is published (~23 July 2026). Price indices and transaction volumes cited are sourced from HDB.gov.sg. Prior-quarter trend comparisons for indicative RPI changes are approximate. This article does not constitute property, financial, or legal advice. Readers are encouraged to consult official HDB resources and licensed professionals before making any property decision. All figures cited are as at 6 July 2026.