Singapore Property Inheritance Law Guide 2026: Intestate Succession, CPF Nomination and Estate Planning Explained

When a property owner dies in Singapore, what happens to their flat or condo depends on three things: how the property is held, whether there is a valid Will, and whether CPF was used to finance the purchase. Get any one of these wrong and the outcome can be starkly different from what the owner intended — delays of months or years, unintended beneficiaries, or unexpected stamp duty costs for heirs. This guide explains Singapore property inheritance law in plain English: the Intestate Succession Act, CPF nomination, survivorship rules for Joint Tenancy and Tenancy-in-Common, the probate process, and the estate-planning steps every property owner should consider.

Quick Answer — Key Takeaways

- No estate duty in Singapore since 15 February 2008 (Estate Duty Act repealed).

- CPF monies are NOT part of your estate — they pass via CPF nomination and bypass your Will entirely.

- Joint Tenancy triggers the right of survivorship: the surviving co-owner receives the deceased’s share automatically, overriding any Will.

- Tenancy-in-Common means your share forms part of your estate and is distributed per your Will or the Intestate Succession Act (Cap 146) if you die without one.

- Without a valid Will, the Intestate Succession Act governs distribution — it does not follow the wishes of the deceased.

- Probate (Grant of Probate or Letters of Administration) is required for TiC shares and sole-ownership properties before the property can be transferred.

- Inherited property may attract ABSD if the beneficiary already owns residential property in Singapore.

- Muslims in Singapore are governed by Islamic Inheritance Law (Faraid) under the Administration of Muslim Law Act — the Intestate Succession Act does not apply to them.

What Governs Property Inheritance in Singapore?

Singapore property inheritance sits at the intersection of three legal regimes. The Intestate Succession Act (Cap 146), administered by the Ministry of Law, governs who receives a deceased’s estate when there is no valid Will — or when a Will does not dispose of all assets. The Conveyancing and Law of Property Act (Cap 61) and the Land Titles Act (Cap 157) govern how the registered title in a property is dealt with on death, including the operation of survivorship in Joint Tenancy. Finally, the Central Provident Fund Act governs CPF monies separately — CPF savings, including amounts used for property, are handled via a CPF nomination and sit entirely outside the estate.

The result is that two co-owners of the same property can have their shares pass in completely different ways depending solely on whether they hold as Joint Tenants or Tenants-in-Common. Understanding this distinction is arguably the single most important estate-planning decision a Singapore property owner can make.

Intestate Succession: Who Inherits If There Is No Will?

If you own a property share (or own solely) and die without a valid Will, your share passes according to the Intestate Succession Act. The Act lays down a fixed priority order — spouse, children, parents, siblings, and so on — and the proportions are non-negotiable. You cannot “informally” direct assets to a partner, a sibling you are close to, or a charity: only a valid Will achieves that.

A few critical points the Act does not protect against. If you are in a long-term relationship but unmarried, your partner receives nothing under the ISA. If you have step-children but never legally adopted them, they too receive nothing. And if you have children from a prior relationship, the Act distributes equally between all biological children — which may not match your intentions at all. A properly drafted Will, reviewed by a Singapore-qualified solicitor, is the only reliable remedy.

| Scenario | Spouse Receives | Children Receive | Parents Receive |

|---|---|---|---|

| Spouse only (no children, no parents) | 100% | — | — |

| Spouse + children | 50% | 50% equally | — |

| Spouse + parents (no children) | 50% | — | 50% |

| Children only (no spouse) | — | 100% equally | — |

| Parents only (no spouse, no children) | — | — | 100% |

| No spouse, no children, no parents | Siblings → uncles/aunts → grandparents → Government (bona vacantia) | ||

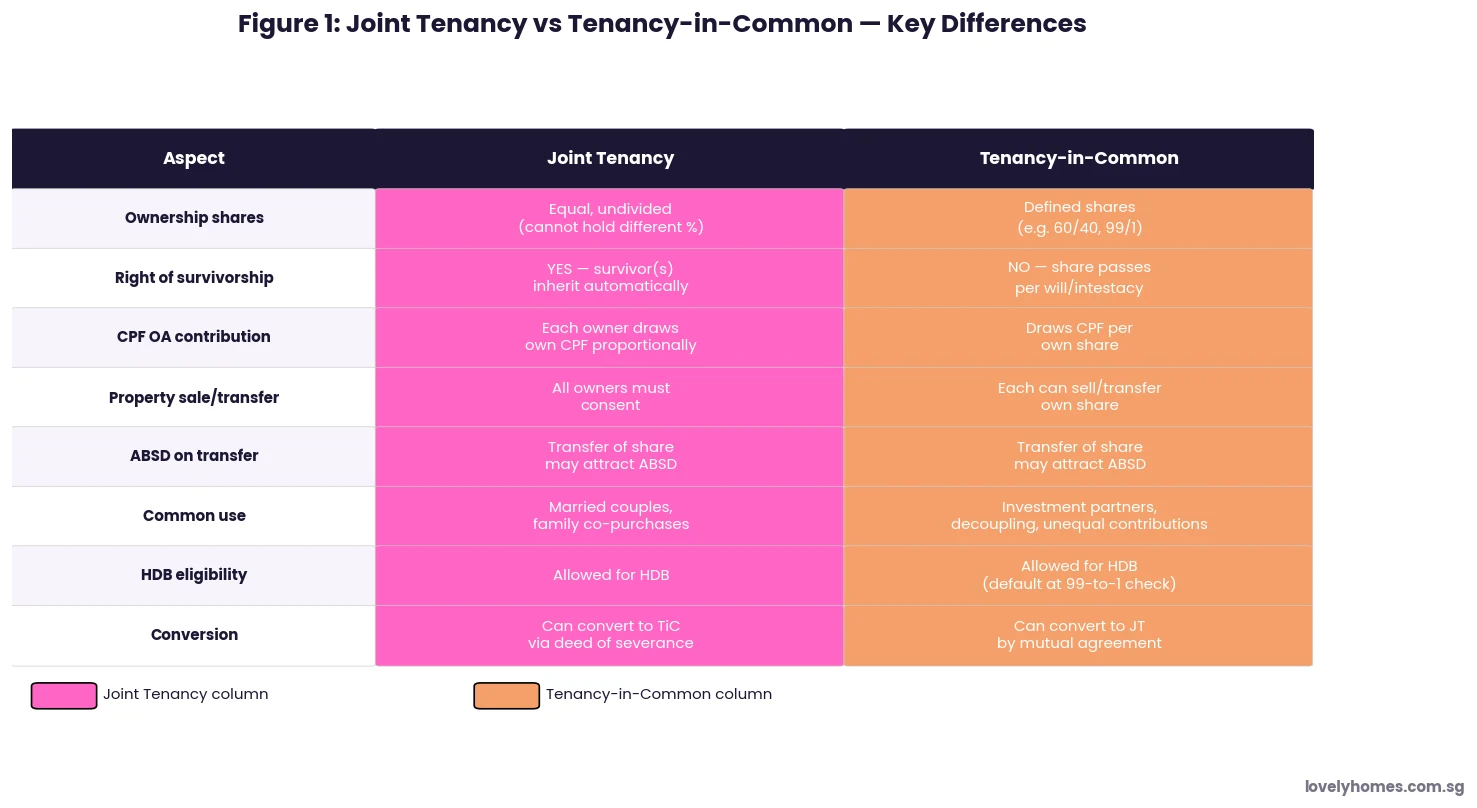

Joint Tenancy vs Tenancy-in-Common: The Death Outcome

How a property is co-owned is registered in the Certificate of Title held by the Singapore Land Authority (SLA). The two modes — Joint Tenancy and Tenancy-in-Common — have diametrically different consequences on death.

In a Joint Tenancy, all co-owners hold the property as a single, undivided whole. On the death of one co-owner, their interest extinguishes and vests automatically in the surviving co-owner(s) by the right of survivorship. This transmission is recorded by SLA via a statutory declaration — no Grant of Probate is needed, no estate administration is required. Critically, a Joint Tenant cannot bequeath their “share” in a Will because they do not hold a severable share to give: the moment you die, it is gone. This makes Joint Tenancy an extremely efficient mechanism for a married couple intending the property to pass to the surviving spouse, but a potentially inflexible one if their wishes are more nuanced.

In a Tenancy-in-Common, each co-owner holds a defined percentage share (e.g., 60%/40%). That share is a distinct legal asset belonging to the individual. On death, it forms part of their estate and passes per their Will — or per the ISA if there is no Will. The estate must go through probate before the share can be transferred to a beneficiary. This extra step takes time and costs money, but it gives the property owner complete flexibility over who receives their share.

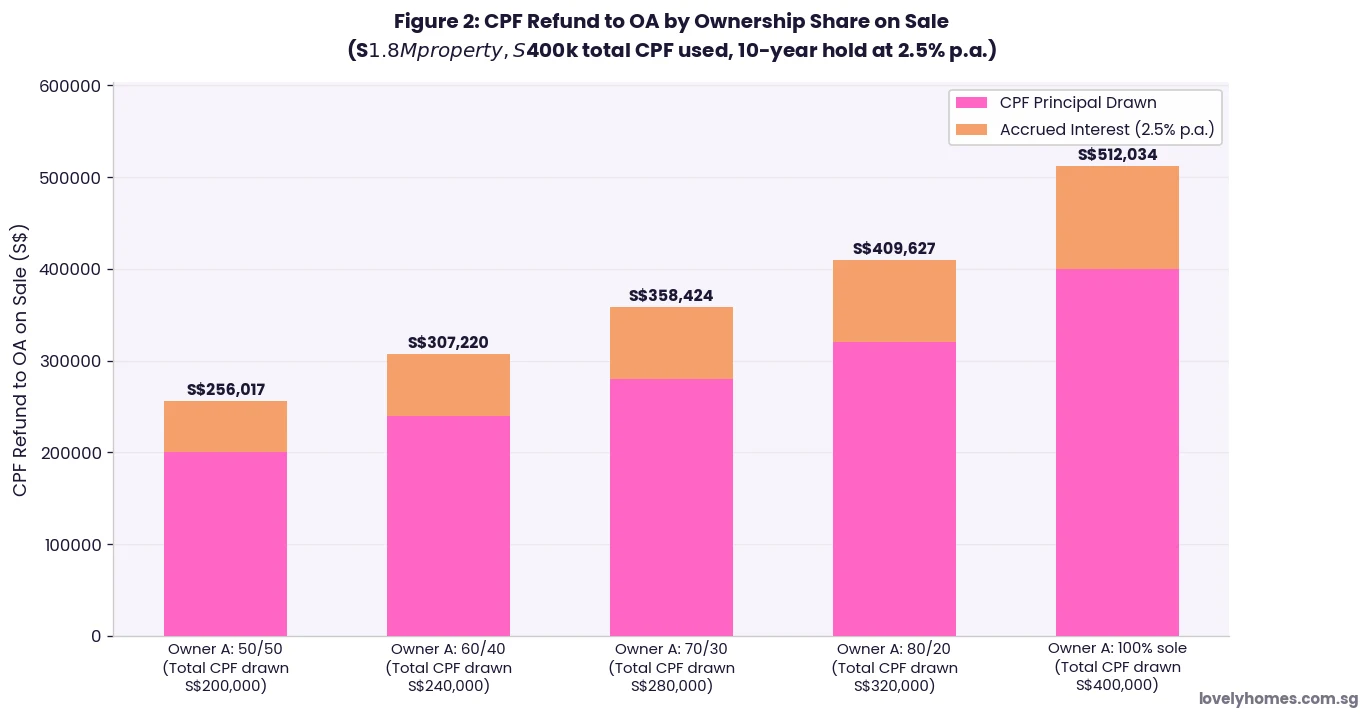

CPF Nomination: The Asset That Bypasses Your Will

Many Singaporeans do not realise that CPF savings — including amounts used for property under the Public Housing Scheme or the Private Properties Scheme — are not part of the estate on death. Under the Central Provident Fund Act, CPF savings are distributed by the CPF Board directly to nominees in the proportions specified in a CPF nomination form. If no nomination is made, the monies are transferred to the Public Trustee for distribution under the ISA. They cannot be directed by a Will.

This creates a common planning gap. Suppose a homeowner uses S$200,000 of CPF OA to pay for a flat over 15 years. When they die, that S$200,000 (with accrued interest) does not form part of the property — it is a CPF debt secured against the estate. CPF will require the estate to refund the principal plus 2.5% per annum accrued interest before the property net proceeds are distributed. If the CPF nomination names different beneficiaries from the Will’s property beneficiaries, the two streams can conflict: the property proceeds go one way, the CPF refund goes another. Co-ordinating CPF nominations and Will provisions is essential.

The Probate and Estate Administration Process

For any property that passes via the estate — either sole ownership or a Tenancy-in-Common share — the personal representative must obtain a Grant of Probate (if there is a Will) or Letters of Administration (if there is no Will) from the Family Justice Courts before title can be transferred to beneficiaries. The process is administered under the Probate and Administration Act (Cap 251) and the Family Justice Act.

The timeline for an uncontested, straightforward Singapore estate is typically two to six months from death to completion. Complexity arises when assets are held overseas, when there are disputes between beneficiaries, when the deceased held property under a trust, or when the Will itself is challenged. Cross-border estates involving property in multiple jurisdictions (e.g., a Singapore condo plus a Malaysian property) require re-sealing of the Singapore Grant of Probate or separate proceedings in each jurisdiction.

One important point: no estate duty has applied in Singapore since 15 February 2008. The Estate Duty Act was repealed and the IRAS no longer requires any filing of estate duty returns. This makes Singapore one of the most estate-duty-friendly jurisdictions in Asia.

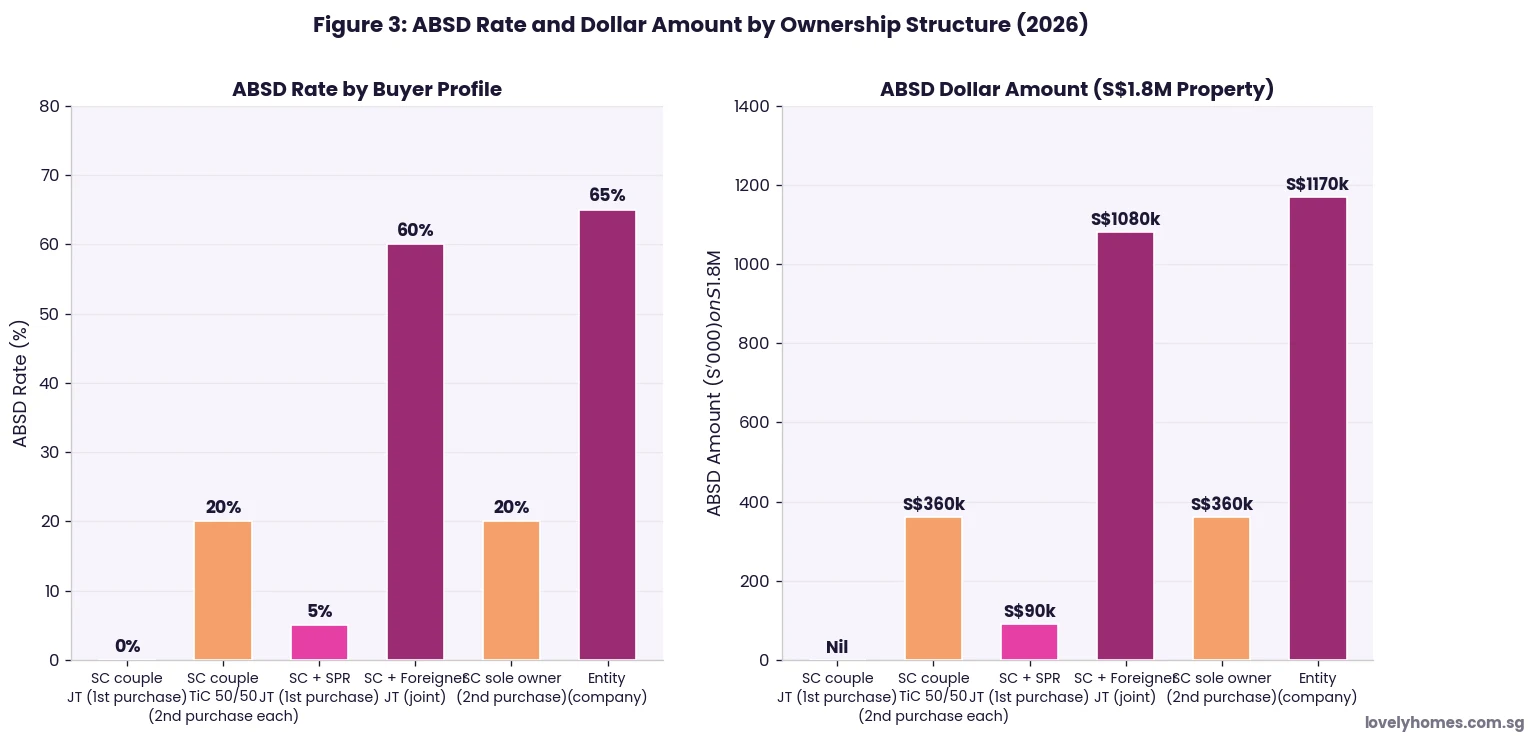

ABSD on Inherited Property

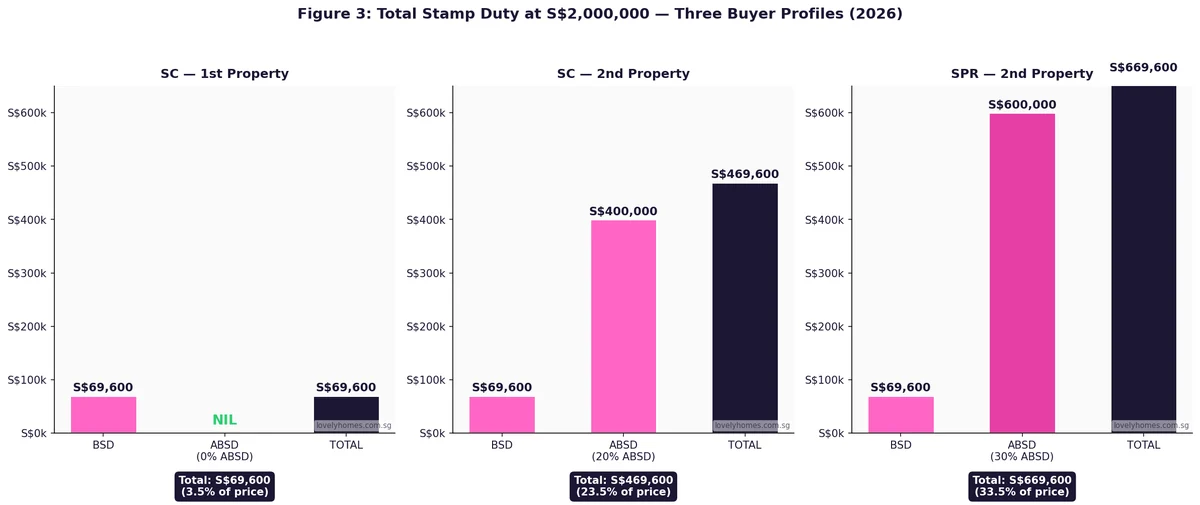

Receiving a property share by inheritance does not exempt you from Additional Buyer’s Stamp Duty. IRAS treats an inheritance as an acquisition just as any other transfer. If, at the date you inherit the property, you already own one or more residential properties in Singapore, ABSD applies at the rate corresponding to your profile and the number of properties you will then own. As at 2026, for Singapore Citizens, a second residential property attracts ABSD at 20%, and a third or subsequent property attracts 30%.

| Buyer Profile | 1st Residential Property | 2nd Residential Property | 3rd+ Residential Property |

|---|---|---|---|

| Singapore Citizen (SC) | 0% | 20% | 30% |

| Singapore PR (SPR) | 5% | 30% | 35% |

| Foreigner | 60% | 60% | 60% |

| Entity (company/trust) | 65% | 65% | 65% |

There is a limited ABSD remission for married couples who inherit through a deceased spouse under the Joint Tenancy survivorship mechanism: survivorship does not constitute a separate acquisition, so no ABSD is payable on the automatic transmission to the surviving spouse. However, where a beneficiary inherits via a Will or the ISA and is already a property owner, ABSD is payable.

Worked Example: The Lim Family Estate

Background. Mr Lim Ah Kow (SC) passed away on 1 March 2026. He owned two properties: a 4-room HDB flat in Ang Mo Kio (held in Joint Tenancy with his wife, Mrs Lim) and a 40% share in a D15 condo held as Tenants-in-Common with his brother (60% share).

HDB flat (Joint Tenancy). Mrs Lim, the surviving Joint Tenant, lodges a statutory declaration of survivorship with SLA. The HDB flat vests automatically in Mrs Lim. No probate needed. No ABSD (survivorship is not a fresh acquisition). Total time: approximately 3–4 weeks for SLA to update the title. The HDB flat does not go through Mr Lim’s estate at all.

D15 condo share (40%, Tenancy-in-Common). Mr Lim had a valid Will leaving his entire estate to Mrs Lim. The executor (Mrs Lim’s solicitor) applies for a Grant of Probate at the Family Justice Courts. This takes approximately 6–8 weeks. Once the Grant is issued, SLA transmission orders the condo share registered in Mrs Lim’s name. Because Mrs Lim already owns the HDB flat (her first property), this condo share is her second residential property. ABSD at 20% is payable on the market value of the 40% share. If the condo’s value at the date of transmission is S$2,200,000, the 40% share = S$880,000 × 20% ABSD = S$176,000 payable by Mrs Lim.

CPF refund. Mr Lim used S$95,000 CPF OA principal for the condo, accumulated over 8 years. Accrued interest at 2.5% p.a. ≈ S$21,000. Total CPF refund required from the estate: S$116,000. This is deducted from the condo share’s net sale/transfer proceeds before the estate is distributed.

Takeaway. A well-drafted Will and advance CPF nomination review could have positioned the transfer differently — for example, placing the condo share in trust for adult children who do not yet own property, potentially deferring or eliminating the ABSD exposure.

Why This Matters: Estate Planning for Singapore Property Owners

Singapore’s property market is one of the most valuable wealth stores for middle-class families in Asia. Many households have 70–80% of their net worth locked in residential property. Despite this, surveys consistently find that a large majority of Singaporeans do not have a valid Will. The combination of no estate duty and a straightforward probate system means that the barriers to basic estate planning are genuinely low — a simple Will costs as little as S$200–S$500 through a qualified solicitor, or slightly more through the Public Trustee’s office.

The stakes are high. A Joint Tenant who wants to leave their share to their children (not the co-owner) must first sever the Joint Tenancy — converting to Tenancy-in-Common — before a Will can take effect. Failing to do so means the survivorship mechanism overrides the Will entirely. Conversely, a Tenancy-in-Common owner who wants an immediate, hassle-free transfer to a spouse may benefit from converting to Joint Tenancy to remove the probate burden.

Compared to many Asian jurisdictions, Singapore has no forced heirship rules for non-Muslims (Malaysia, Indonesia, and others do). This means a Singapore resident can, subject to the Inheritance (Family Provision) Act (Cap 138), effectively direct their entire estate to whomever they wish — provided they do so in a valid Will. The flexibility is a planning opportunity that many families leave on the table.

What Might Come Next: Estate Planning Trends in Singapore

Several developments on the horizon are worth monitoring. The Ministry of Law’s ongoing review of the Electronic Wills framework — proposed to allow remote witnessing of Wills in certain circumstances — may reduce friction for Singaporeans who live overseas or who lack access to a physical notary. Any reforms here would be welcome given that Singapore’s expatriate and overseas-resident community is large and mobile.

On the ABSD front, there is no current indication that the government intends to introduce an inheritance exemption for residential property. The ABSD regime, which was significantly tightened in April 2023, continues to treat all acquisitions — including inheritances — on the same footing. Families with complex multi-generation property holdings should seek specialist legal and tax advice rather than assuming future policy relief.

Finally, as more Singapore property assets are held through family trusts and private trust companies — a structure increasingly popular with high-net-worth families — the interaction between trust law and property transmission will become more important. The Trustees Act (Cap 337) and the Variable Capital Companies Act 2018 provide a sophisticated toolkit for those with sufficient assets to justify the complexity.

Frequently Asked Questions

If I hold my HDB flat as Joint Tenants with my spouse, does it still go through my estate when I die?

No. The right of survivorship operates automatically on your death. Your share extinguishes and vests in your surviving spouse without any need for probate or Letters of Administration. The surviving spouse simply files a statutory declaration of survivorship with the Singapore Land Authority (SLA). This process takes approximately three to four weeks. The HDB flat does not form part of your estate and cannot be directed by your Will.

Can I override the Intestate Succession Act by naming someone in my CPF nomination?

No — CPF nominations and the Intestate Succession Act operate on entirely separate assets. A CPF nomination directs only your CPF monies (Ordinary Account, Special Account, Retirement Account, and MediSave), not your property. If you die intestate, your property share passes according to the ISA regardless of what your CPF nomination says. To direct your property to a specific person outside the ISA rules, you must make a valid Will. The two instruments complement each other but address different assets.

My father died without a Will and held his condo solely. How long will it take before I can sell the property?

For an intestate estate (no Will), the appointed administrator must apply for Letters of Administration at the Family Justice Courts. In uncontested cases where the estate is straightforward, this typically takes four to eight weeks from the filing date. Once the Letters are issued, the administrator can instruct solicitors to transfer title to beneficiaries (or to sell). If the estate must first be distributed to multiple beneficiaries who then need to agree to sell, the process can take several months longer. Total timeline from death to sale completion in a typical uncontested case: approximately four to eight months.

Will I have to pay ABSD when I inherit a property from a deceased family member?

It depends on your existing property holdings. IRAS treats an inheritance as an acquisition. If you already own one or more residential properties in Singapore, you will pay ABSD at the applicable rate on the inherited share’s value. The only exception is where property passes via Joint Tenancy survivorship to the surviving co-owner — that automatic vesting is not treated as a fresh acquisition for ABSD purposes. For all other transmissions (Will, intestate succession), ABSD applies. Always seek IRAS and legal advice before accepting an inherited property if you already own residential property.

What is the difference between a Grant of Probate and Letters of Administration?

A Grant of Probate is issued by the Family Justice Courts when the deceased left a valid Will naming an executor, who then applies for the grant. It confirms the Will is valid and authorises the executor to administer the estate. Letters of Administration are issued when there is no Will (intestate), or when the named executor is unable or unwilling to act. An administrator is appointed — usually the next of kin according to a statutory priority order — and letters are issued authorising them to administer the estate. Both documents carry the same practical legal effect: they authorise the holder to deal with the deceased’s assets, including transferring Singapore property via SLA.

Can a Singapore foreigner or Permanent Resident own inherited landed property?

Foreigners (non-Singapore Citizens) are generally prohibited from owning restricted residential property in Singapore, including most landed housing on the mainland (detached houses, semi-detached houses, terrace houses), under the Residential Property Act (Cap 274). However, the RPA contains an exemption for property acquired by inheritance — a foreigner who inherits a restricted property does not automatically breach the RPA. The foreigner has a reasonable period to divest the property. The Singapore Land Authority will generally allow a temporary exemption for estate administration, but the beneficiary should seek legal advice promptly on the timeline and conditions.

Does Singapore recognise foreign Wills for Singapore property?

Singapore courts generally recognise a foreign Will if it is validly executed according to the law of the place where it was made, the place where the testator was domiciled, or the law of Singapore, under the Wills Act (Cap 352). However, even with a recognised foreign Will, a Grant of Probate must still be obtained from the Family Justice Courts (or a foreign grant re-sealed in Singapore) before property in Singapore can be transferred. The practical advice is to make a separate Singapore Will if you own Singapore property and are domiciled overseas — this significantly reduces delay and cost for your estate.