Geylang Neighbourhood Guide Singapore 2026: Property Prices, Schools, MRT and Investment Outlook

Click anywhere outside to close

Quick Answer — Geylang Neighbourhood Guide 2026

- Location: District 14 (D14), central Singapore — 10 minutes to the CBD by MRT.

- HDB prices: 3-room ~S$380k, 4-room ~S$730k, 5-room ~S$850k, executive flat ~S$1.09M.

- Resale record: S$1.37M for a 5-room at 7 Pine Close (2026).

- MRT connectivity: Aljunied (EWL), Paya Lebar (EWL+CCL interchange), MacPherson & Mattar (DTL).

- Rental yields: Among the highest in Singapore at 4.0–5.0% gross for HDB units.

- Who should buy: Value-seekers wanting central proximity at OCR prices; investors targeting rental yield.

- Key consideration: Geylang’s lorongs (red-light district) are in a small sub-area and do not affect the majority of residential precincts — always inspect the specific block location.

What Is Geylang and Why Does It Matter for Property Buyers?

Geylang occupies one of Singapore’s most strategically positioned yet frequently misunderstood residential postcodes. Administered by the Urban Redevelopment Authority (URA) as part of Planning Area Geylang and spanning District 14, the estate sits squarely in the middle of the island — flanked by Paya Lebar to the east, Kallang to the west, and the Aljunied and Mattar MRT nodes to the south. With approximately 94,200 HDB residents spread across roughly 29,357 flats, Geylang is a well-established, high-density town that has long delivered above-average rental yields precisely because its central location commands strong tenant demand while its prices remain well below those of the Core Central Region (CCR).

For property buyers in 2026, Geylang presents a genuine value proposition: central Singapore proximity at Outside Central Region pricing. The completion of the Downtown Line (DTL) stations at MacPherson and Mattar significantly improved connectivity, and the Paya Lebar Quarter (PLQ) commercial hub — just minutes away — has attracted major employers including Amazon Web Services and PwC, creating a captive pool of working professionals who rent locally. This guide covers everything you need to know about buying, investing, and renting in Geylang in 2026.

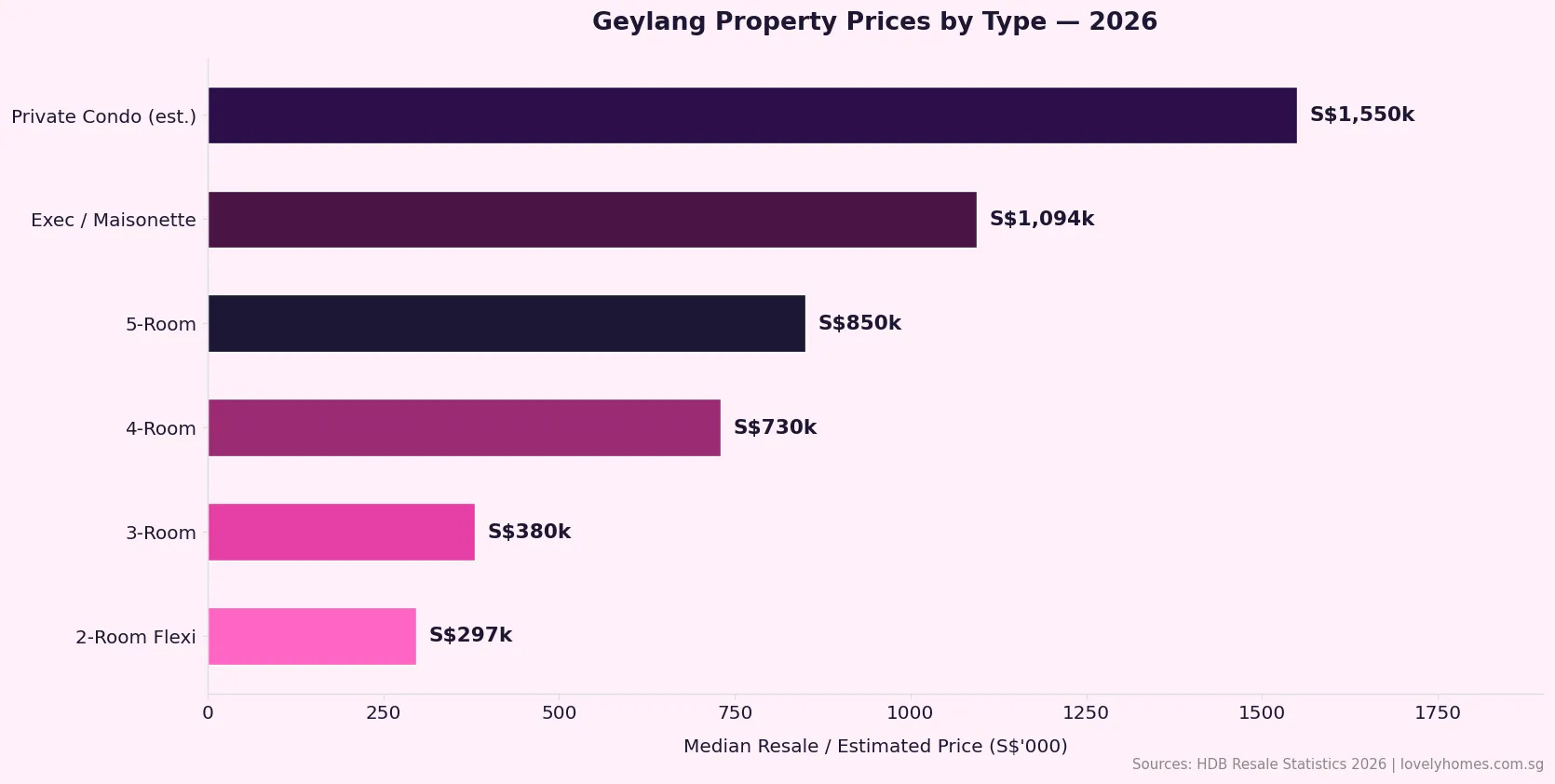

HDB Resale Market in Geylang 2026

Geylang’s HDB resale market recorded 672 transactions over the past 12 months, with a median transaction price of S$590,000 across all flat types and a median price per square foot (psf) of S$626. The town’s entry point sits at the 2-room Flexi segment at around S$297,000 — well within reach of singles and young couples applying under the Public Scheme. The 4-room segment is the most liquid, with 251 transactions recorded, reflecting broad demand from upgraders and first-time families.

The standout milestone for 2026 was the 5-room flat at 7 Pine Close (Block 7, Geylang East) which changed hands at S$1.37M (S$1,161 psf) — setting a new District 14 resale record and signalling that the estate’s premium blocks command prices competitive with less-central mature towns. Executive flats, which are concentrated in older Geylang precincts, have a median price of S$1.094M, reflecting the scarcity of larger legacy stock.

| Flat Type | Median Resale Price | Approx. PSF | Notes |

|---|---|---|---|

| 2-Room Flexi | S$297,000 | ~S$588 psf | Entry-level; available to singles |

| 3-Room | S$380,000 | ~S$607 psf | Most affordable family option |

| 4-Room | S$730,000 | ~S$620 psf | Highest transaction volume |

| 5-Room | S$850,000 | ~S$640 psf | Record: S$1.37M (7 Pine Close) |

| Executive / Maisonette | S$1,094,000 | ~S$660 psf | Scarce legacy stock |

| Private Condo (est.) | ~S$1,550,000 | ~S$1,500 psf | RCR fringe; Sims Urban Oasis benchmark |

HDB flats in Geylang are classified as Standard (5-year Minimum Occupation Period) under the new HDB flat classification framework introduced in 2024. There are no Plus or Prime-class Geylang BTO flats — all new supply entering the resale market will carry the standard 5-year MOP, giving buyers who purchased at launch relatively quick resale flexibility.

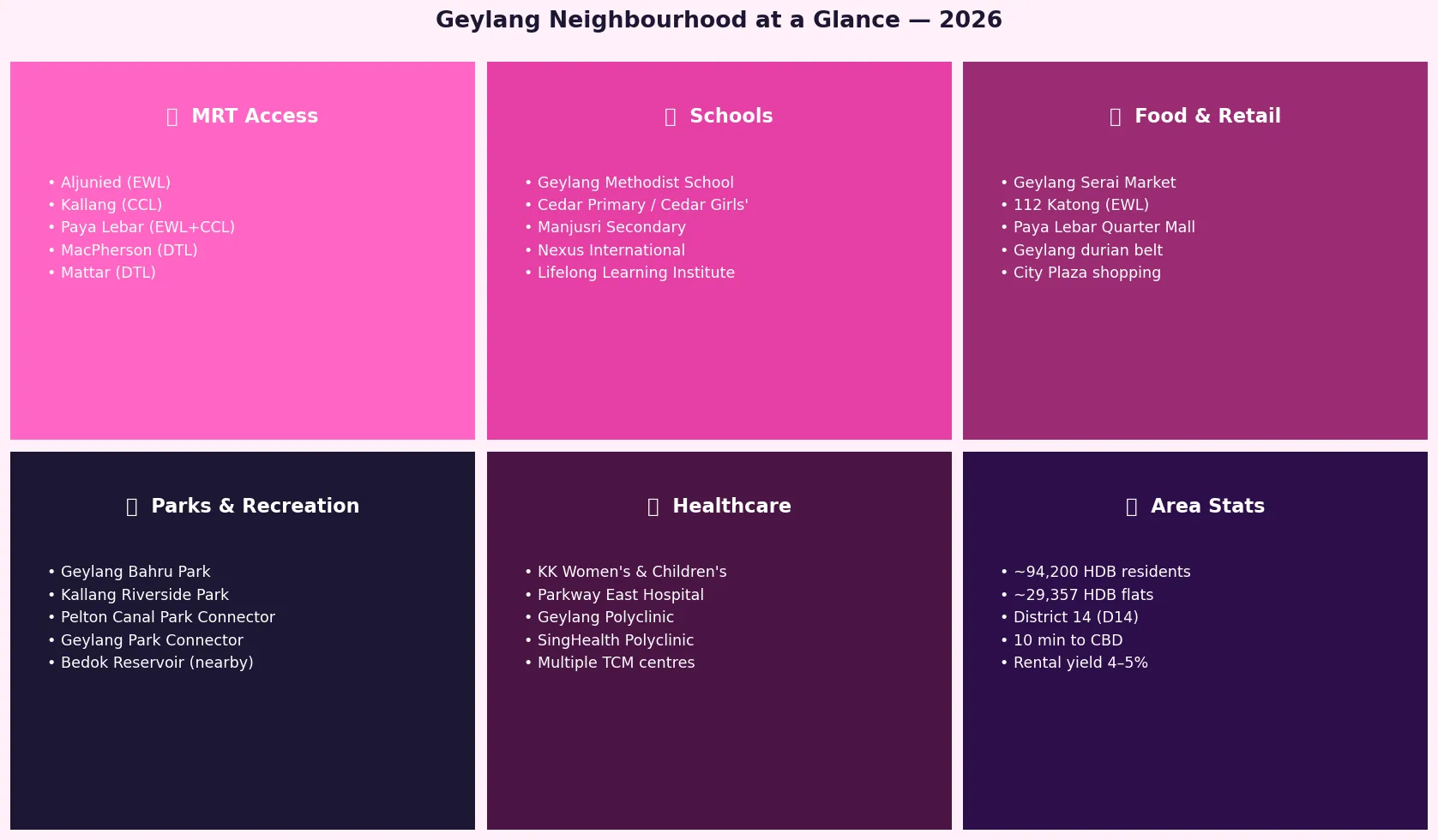

MRT Connectivity and Transport Infrastructure

Geylang’s transport network is one of its strongest selling points. The estate is served by five MRT stations across three lines, giving residents genuinely multi-directional access without the need for transfers in most cases.

On the East-West Line (EWL), Aljunied MRT and Eunos MRT bracket the heart of the estate, while the major Paya Lebar MRT interchange (EWL + Circle Line) lies at the eastern boundary — a station that places residents within 14 minutes of the City Hall CBD cluster and 9 minutes of Jurong East. The Downtown Line (DTL) added MacPherson and Mattar MRT stations, connecting Geylang directly to the Botanic Gardens, Buona Vista, and Marina Bay Financial Centre corridor without changing trains. Bus connectivity is extensive, with multiple trunk routes running along Geylang Road, Sims Avenue, and Aljunied Road into the city.

Schools, Amenities and the Geylang Serai Ecosystem

Geylang’s school landscape has improved steadily, with Geylang Methodist School (Primary and Secondary) serving as the estate’s anchor school. Cedar Primary and the well-regarded Cedar Girls’ Secondary School are within catchment distance for many Aljunied-side addresses. For families requiring secondary options, Manjusri Secondary and Tanjong Katong Secondary are accessible via public transport. The Lifelong Learning Institute (LLI), operated by the Singapore Workforce Agency, is based within the Paya Lebar precinct and offers adult upskilling programmes relevant for tenants and residents alike.

Retail and dining are Geylang’s most celebrated features. The Geylang Serai Market and Food Centre, gazetted as a heritage site, is among Singapore’s most productive hawker centres and anchors the estate’s Malay cultural identity. The Paya Lebar Quarter (PLQ) Mall — accessible within minutes — brings premium retail, a full-format supermarket, and a cinema. City Plaza on Geylang Road caters to budget clothing and electronics. The estate’s famous durian belt along Geylang Road offers seasonal durian at competitive prices, a draw that brings island-wide visitors and contributes to a uniquely vibrant street food culture.

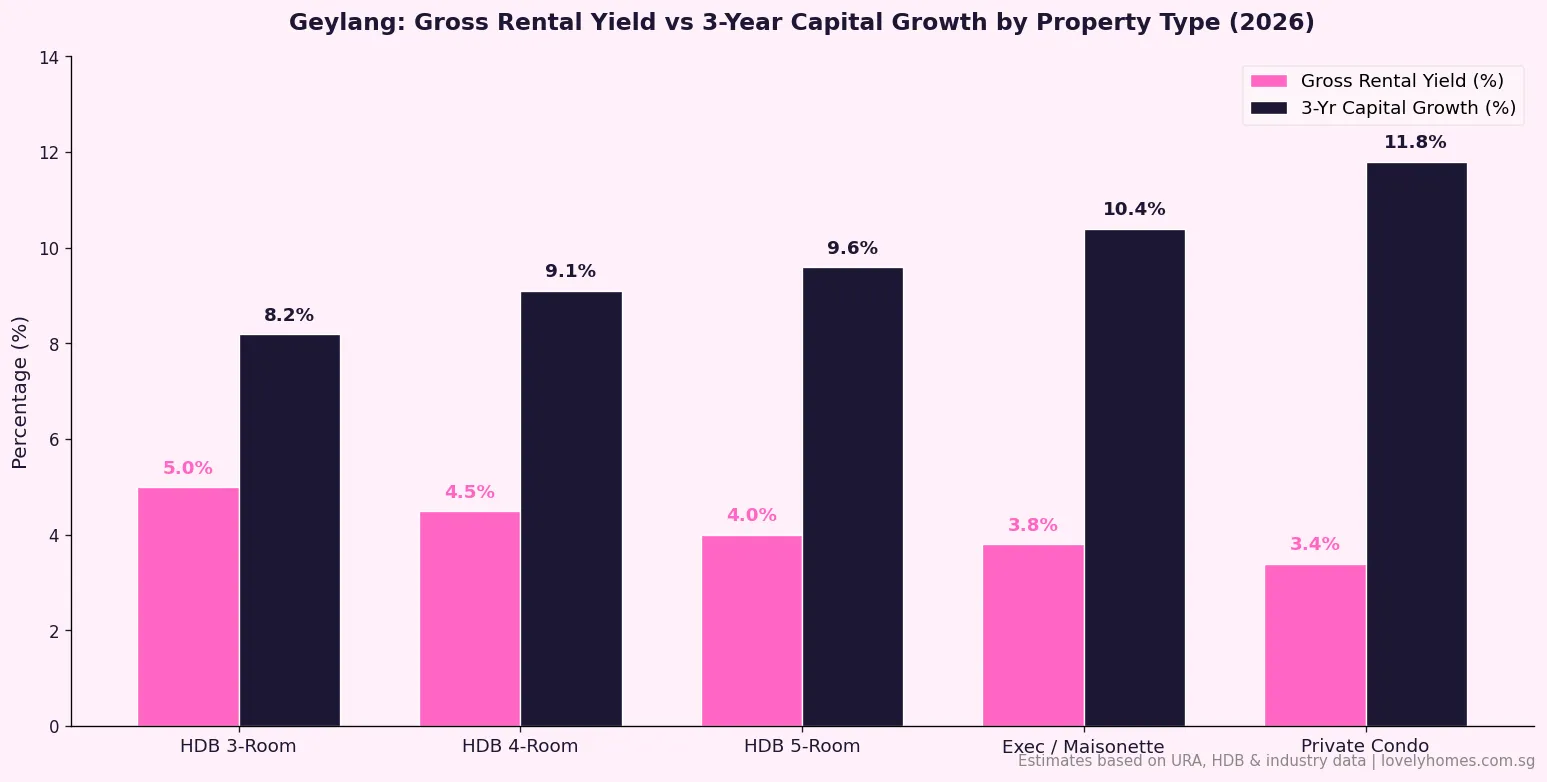

Geylang Property as an Investment: Rental Yields and Capital Growth

Geylang consistently ranks among the top-five Singapore towns for gross HDB rental yield, a function of the estate’s central location and relatively affordable entry prices. Industry data for 2026 shows 3-room flats yielding approximately 5.0% gross, 4-room flats at 4.5%, and 5-room flats at around 4.0%. These figures compare favourably to the national HDB average of approximately 3.5%, and are driven by sustained demand from working professionals employed at PLQ, Raffles Place, and the Marina Bay Financial Centre — all within a 15-minute commute.

On the capital appreciation side, HDB resale prices in Geylang grew by approximately 8–10% cumulatively over the three years to 2026, broadly in line with the national HDB resale trajectory but anchored by the estate’s scarcity of new supply and growing recognition of its investment fundamentals. Private residential prices at the RCR boundary (Sims Urban Oasis benchmark: ~S$1,500 psf resale) have appreciated by roughly 10–12% over the same period.

Worked Example — Mr & Mrs Ahmad: HDB Upgrader Buying Geylang 4-Room

Mr and Mrs Ahmad are a Singapore Citizen couple with a combined monthly income of S$9,500. They have sold their Tampines 4-room HDB flat (MOP cleared) at S$750,000 and are purchasing a centrally located Geylang 4-room resale flat at S$730,000 as their next family home.

- Purchase price: S$730,000

- BSD (Buyer’s Stamp Duty): S$1,800 + S$3,600 + S$11,100 = S$16,500 (1% on first S$180k, 2% on next S$180k, 3% on remaining S$370k)

- ABSD: S$0 — SC couple purchasing within 6 months of HDB sale, eligible for ABSD remission on first residential property

- HDB Loan (80% LTV): S$584,000 @ 2.6% p.a. over 25 years → monthly instalment ~S$2,646

- MSR check: S$2,646 ÷ S$9,500 = 27.9% — within the 30% Mortgage Servicing Ratio cap

- Upfront cash / CPF needed: 20% down payment S$146,000 + BSD S$16,500 + legal fees ~S$2,500 = ~S$165,000 (can be paid via CPF OA)

- Net position: Strong. Central location, 10-min CBD commute, gross rental yield ~4.5% if they rent out bedroom(s) after MOP.

What This Means for Buyers and Investors in 2026

Geylang’s property story in 2026 is one of revaluation. For years, the estate’s association with its restricted-entertainment lorongs (a small sub-zone in the central Geylang belt) suppressed buyer sentiment disproportionately relative to its transport and location fundamentals. That discount is narrowing. The S$1.37M resale record at 7 Pine Close is not an outlier — it reflects a broader market re-rating of mature central estates as the supply of well-connected, affordable HDB towns continues to shrink.

For yield-focused investors, Geylang’s 4.0–5.0% gross yields remain difficult to match elsewhere in Singapore without accepting significantly worse transport connectivity. The PLQ commercial district — home to major white-collar employers — sustains rental demand that is structurally durable, not cyclical. Peer comparison: Queenstown (also central) offers lower gross yields of 2.5–3.5% but higher capital growth. Toa Payoh offers similar yields (3.5–4.1%) but with fewer MRT lines. Geylang splits the difference, offering strong income returns and material capital appreciation.

For owner-occupiers, the estate’s lack of recent BTO launches means no large MOP-wave supply is imminent. The resale pool is mature and well-distributed across flat types. Families should focus their search on the Aljunied, Geylang East, and Kampong Ubi sub-zones, which offer the best balance of school proximity, transport, and distance from the restricted-entertainment belt.

What Might Come Next for Geylang (Outlook — Speculative)

This section is editorial speculation and should not be treated as confirmed policy or investment advice.

Industry observers have noted that URA’s long-range planning documents position the Geylang-Paya Lebar sub-region as an evolving live-work cluster, anchored by PLQ’s Phase 2 commercial pipeline and the potential northward extension of the Kallang River revitalisation masterplan. Should URA eventually regularise the restricted-entertainment precincts (a possibility that has been periodically floated in public consultations), the positive effect on surrounding residential values could be material. No official timeline has been announced as of May 2026.

On infrastructure, the Cross Island Line (CRL) Phase 2, scheduled for completion around 2031, is not expected to have a station within Geylang proper — but the Pasir Ris extension will improve east-west connectivity for tenants commuting across the island, indirectly sustaining rental demand at Geylang’s EWL-served addresses.

Frequently Asked Questions — Geylang Property Guide 2026

Is Geylang a good area to buy property in Singapore in 2026?

Yes — for the right buyer profile. Geylang offers central Singapore location (10 minutes to CBD by MRT) at prices well below comparable mature estates in the Rest of Central Region. Gross rental yields of 4.0–5.0% are among the highest in Singapore for centrally located HDB towns. The main consideration is block-level due diligence: flats in the Aljunied, Geylang East, Kampong Ubi, and MacPherson sub-zones are well removed from the restricted-entertainment belt, and buyers should verify the specific block address using URA’s OneMap before committing. The S$1.37M record at 7 Pine Close in 2026 demonstrates that the market is actively repricing Geylang’s fundamentals upward.

Which MRT stations serve Geylang?

Geylang is served by five MRT stations across three lines. On the East-West Line (EWL): Aljunied and Eunos MRT stations serve the central and western parts of the estate; Paya Lebar MRT (EWL + Circle Line interchange) serves the eastern boundary. On the Downtown Line (DTL): MacPherson and Mattar MRT stations provide direct access to the city and the Buona Vista cluster without transfers. The closest station to each residential block varies, so buyers should check the LTA Journey Planner for walking-time estimates to the block of interest.

What are typical HDB resale prices in Geylang in 2026?

Based on HDB resale transaction data for 2026: 2-room Flexi flats transact at a median of around S$297,000; 3-room flats at S$380,000; 4-room flats at S$730,000; 5-room flats at S$850,000; and executive/maisonette flats at S$1.094M. The estate-wide resale record was set in 2026 at S$1.37M for a high-floor 5-room at 7 Pine Close. Prices vary by block, floor, and facing: high-floor Paya Lebar-facing units in Geylang East command a 10–15% premium over equivalent stock in the Kampong Ubi sub-zone.

How does Geylang compare to Queenstown and Toa Payoh for property investment?

Geylang, Queenstown, and Toa Payoh are all mature central estates, but they cater to different investor profiles. Queenstown (District 3) commands the highest prices (4-room ~S$820k–S$1.1M) and the lowest gross yields (2.5–3.5%) but the strongest capital growth driven by MRT-CCR adjacency and the Greater Southern Waterfront catalyst. Toa Payoh (District 12) sits in the middle on prices (4-room ~S$650k–S$900k) and offers yields of 3.5–4.1%. Geylang (District 14) is the most affordable of the three for a 4-room flat and offers the highest yields (4.0–5.0%), but with somewhat more variable per-block desirability. For investors prioritising income return, Geylang is typically the strongest performer of the three; for capital growth, Queenstown leads.

Can foreigners and Permanent Residents buy property in Geylang?

Permanent Residents (PRs) can purchase HDB resale flats in Geylang subject to the standard PR eligibility rules: a minimum of 3 years’ PR status, a valid family nucleus (e.g., spouse or children), and no concurrent HDB ownership. PRs pay Additional Buyer’s Stamp Duty (ABSD) of 5% on their first residential property purchase. Foreigners cannot purchase HDB flats but may purchase private residential properties in Geylang (e.g., Sims Urban Oasis) subject to 65% ABSD. See IRAS’s official ABSD rate table for current rates applicable to your citizenship status.

Are there any upcoming BTO launches or new HDB supply in Geylang?

As of May 2026, HDB has not announced any BTO launches within Geylang. The estate is fully built-out and all new HDB supply entering the resale market consists of existing flats clearing their 5-year MOP. This supply constraint is broadly supportive of resale prices. Buyers looking for new HDB flats in the central region should monitor HDB’s June 2026 BTO exercise (covering Ang Mo Kio, Bishan, Bukit Merah, Sembawang and Woodlands) and future BTO launch announcements at the HDB website.

What is the rental income potential for a Geylang HDB flat?

Geylang HDB flats consistently generate among the highest rental yields in Singapore for a mature central estate. A 4-room flat transacting at S$730,000 and achieving a monthly rent of S$2,750–S$3,000 produces a gross yield of approximately 4.5–4.9%. Rental demand is driven by working professionals at Paya Lebar Quarter (PLQ), the CBD, and the Marina Bay Financial Centre cluster — all within a 15-minute commute. Whole-flat subletting requires MOP completion plus HDB approval; bedroom subletting is permitted during the MOP period subject to the occupancy cap (currently 8 persons for a 4-room or 5-room flat under the temporary relaxation in effect until December 2028). Rental income is subject to income tax; refer to IRAS for allowable deductions including mortgage interest, property tax, and agent fees.

Related Articles

Toa Payoh Neighbourhood Guide 2026

Stamp Duty Calculator Guide 2026

HDB Subletting Rules Singapore 2026

Rental Yield Singapore 2026 Guide

Upgrading from HDB to Private Property

ABSD Singapore 2026 Complete Guide

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or property advice. Property prices, rental yields, and market conditions are indicative and subject to change; all figures should be independently verified against official sources including the Urban Redevelopment Authority (URA), the Housing & Development Board (HDB), the Inland Revenue Authority of Singapore (IRAS), the Central Provident Fund (CPF) Board, and the Monetary Authority of Singapore (MAS). Buyers and investors should consult a licensed property agent, conveyancing lawyer, and independent financial adviser before making any property purchase decision. LovelyHomes does not receive referral fees from any property agency, developer, or financial institution.