Singapore Property Decoupling Guide 2026: Save ABSD, Costs, Risks and Step-by-Step Process

Quick Answer: Property Decoupling Singapore 2026

- What is decoupling? One co-owner transfers (sells) their ownership share to the other, leaving the transferee as sole owner — free to purchase a second property as a “first-time” buyer and pay 0% ABSD (SC).

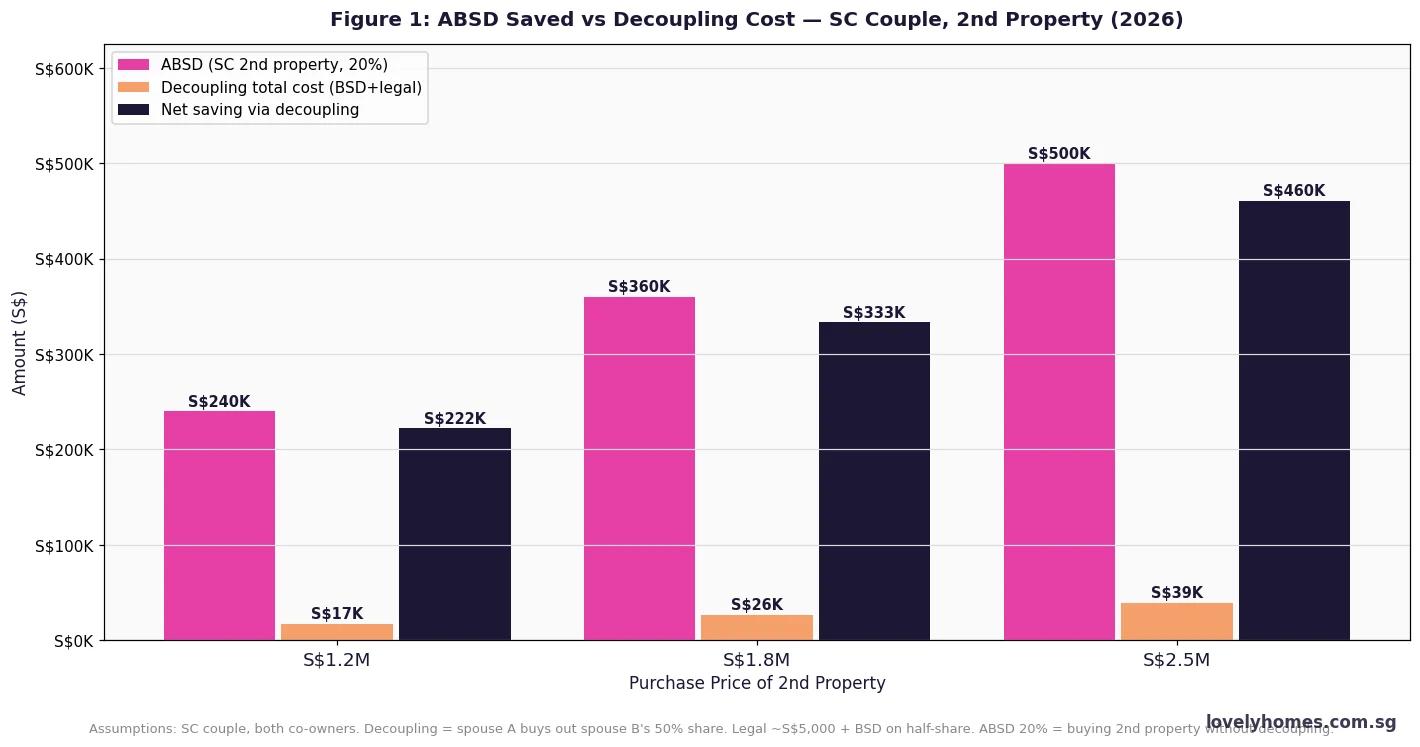

- Why decouple? To avoid the 20% Additional Buyer’s Stamp Duty (ABSD) on a second residential property — worth S$240,000 on a S$1.2M purchase, S$360,000 on S$1.8M.

- Cost of decoupling: Buyer’s Stamp Duty on the half-share transferred + conveyancing legal fees (~S$4,000–S$6,000) + CPF accrued interest refund considerations. BSD on a 50% share of S$1.5M = approximately S$20,100.

- CPF complication: The transferor must refund CPF OA monies (principal + 2.5% p.a. interest) back to their CPF account on the part-disposal. This reduces the available cash to the couple.

- Who can decouple? Any co-owners of a private property — married couples, siblings, business partners. HDB flats cannot be decoupled (HDB must approve any ownership change and will not approve part-share sales to achieve ABSD avoidance).

- Timeline: Typically 6–10 weeks from legal instruction to registration of transfer with the Singapore Land Authority (SLA).

- Risk: IRAS assesses BSD on market value, not agreed price. Undervaluing the transfer to minimise BSD exposes both parties to penalties and back-taxes.

Property decoupling Singapore refers to the legal process of one co-owner divesting their share in a jointly-owned property to the other, with the primary objective of allowing the transferee (or the transferor, if they are the one moving on) to purchase a subsequent property as a sole first-time owner, thereby avoiding ABSD. The strategy became widely discussed after the April 2023 cooling measures raised ABSD on a second property for Singapore Citizens to 20% — equivalent to S$270,000 on a S$1.35M condominium.

Decoupling is entirely legal. IRAS does not prohibit the practice; it merely requires that BSD be paid correctly on the transferred share at market value. What IRAS does scrutinise is any attempt to transact at artificially low prices to reduce stamp duty. The Stamp Duties Act (Cap. 312) empowers IRAS to assess BSD on the market value of the interest transferred, regardless of the stated consideration — so proper valuation is not optional; it is mandatory.

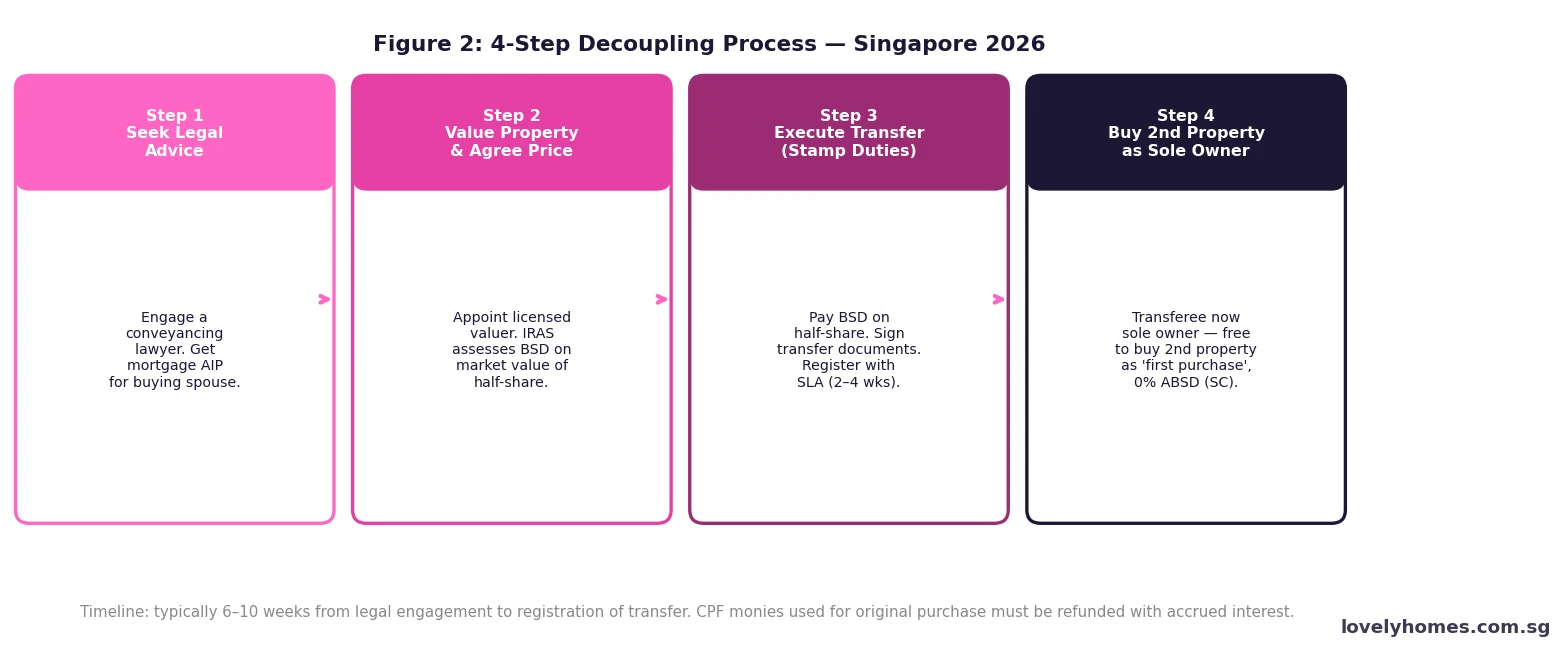

How Decoupling Works: The Legal Mechanics

In a typical residential decoupling, a married couple owns a condominium together — say, as tenants-in-common in equal 50/50 shares, or as joint tenants. One spouse (the transferor) agrees to sell their 50% share to the other spouse (the transferee). The transaction is treated by IRAS as a sale at arm’s length: BSD is levied on the consideration paid or the market value of the half-share, whichever is higher.

The parties instruct a conveyancing lawyer who: obtains a formal valuation of the property from a licensed valuer, calculates the BSD payable on the half-share, prepares the Transfer Instrument, and lodges it with the Singapore Land Authority (SLA) for registration. BSD is paid electronically to IRAS before lodgement. The entire process takes 6–10 weeks under normal conditions.

Once registered, the transferee is the 100% sole owner of the property. The transferor holds no residential property in Singapore and is classified as a first-time buyer for ABSD purposes. They may now purchase a new private property — condominium, landed, EC (after MOP) — and pay 0% ABSD as a Singapore Citizen buying their first private residential property.

Decoupling Costs: BSD, Legal Fees and CPF

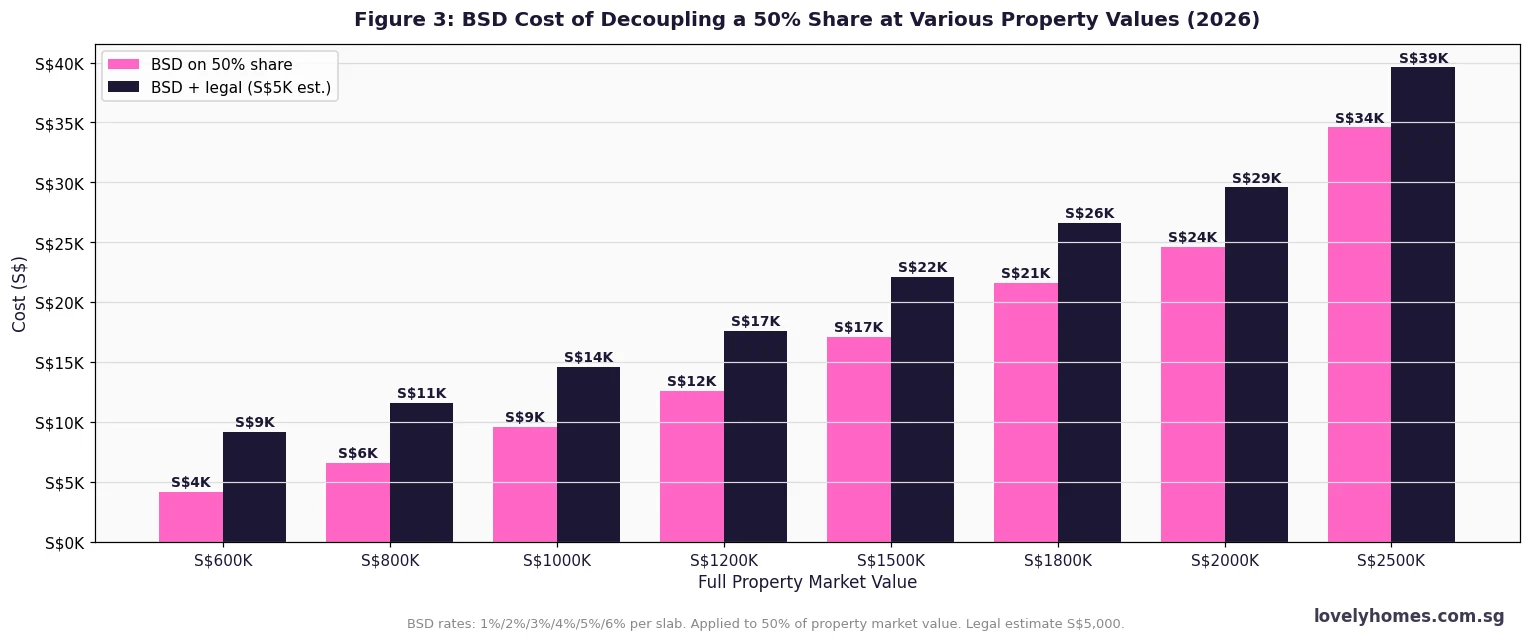

Three cost categories apply to a decoupling exercise. The first and largest is Buyer’s Stamp Duty on the transferred share. BSD is calculated on the market value of the 50% interest: 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, 4% on the next S$500,000, and so forth. For a property valued at S$1,500,000, the half-share is S$750,000 and the BSD is approximately S$20,100. For a S$2,000,000 property, the half-share is S$1,000,000 and BSD is approximately S$29,600.

Second, conveyancing legal fees for both sides (a lawyer is typically appointed for each party to avoid conflicts of interest, though one firm may act for both if both parties provide informed consent under the Legal Profession Act). Expect S$2,500–S$3,500 per side — total S$4,000–S$6,000.

Third, CPF complications arise when the transferor used CPF Ordinary Account funds to finance the original purchase. On a part-disposal of a property, CPF Board requires the transferor to refund the proportionate CPF drawn (including accrued interest at 2.5% p.a.) back to their CPF account. This refund may need to be funded by cash from the transferee — that is, the transferee pays the transferor for their 50% share, and the transferor uses that cash to repay CPF. The net position depends on how much CPF was drawn and how long ago.

Decoupling Cost Summary at Key Property Values

| Property Market Value | 50% Share | BSD on Half-Share | Legal Fees (est.) | Total Decoupling Cost | ABSD Saved (SC 20%) | Net Saving |

|---|---|---|---|---|---|---|

| S$800,000 | S$400,000 | S$9,600 | S$5,000 | S$14,600 | S$160,000 | S$145,400 |

| S$1,200,000 | S$600,000 | S$15,600 | S$5,000 | S$20,600 | S$240,000 | S$219,400 |

| S$1,500,000 | S$750,000 | S$20,100 | S$5,000 | S$25,100 | S$300,000 | S$274,900 |

| S$1,800,000 | S$900,000 | S$24,600 | S$5,000 | S$29,600 | S$360,000 | S$330,400 |

| S$2,000,000 | S$1,000,000 | S$29,600 | S$5,000 | S$34,600 | S$400,000 | S$365,400 |

| S$2,500,000 | S$1,250,000 | S$42,100 | S$5,000 | S$47,100 | S$500,000 | S$452,900 |

Worked Example: The Lee Couple

Mr and Mrs Lee are Singapore Citizens who jointly own a condominium in the River Valley area, purchased in 2019 at S$1,600,000. Current market value: S$2,100,000. Outstanding bank mortgage: S$900,000. CPF drawn (Mr Lee’s OA): S$200,000 principal + S$28,000 accrued interest (7 years at 2.5% p.a.) = S$228,000 to be refunded.

Mr Lee transfers his 50% share to Mrs Lee. Half-share value: S$1,050,000. BSD on S$1,050,000: 1%×S$180,000 + 2%×S$180,000 + 3%×S$640,000 + 4%×S$50,000 = S$1,800 + S$3,600 + S$19,200 + S$2,000 = S$26,600. Legal fees both sides: S$5,500.

Consideration paid by Mrs Lee to Mr Lee: S$1,050,000 (half the market value). Of this, S$450,000 represents Mr Lee’s half of the outstanding mortgage (which Mrs Lee refinances into her sole name), and S$600,000 is cash/CPF to Mr Lee. Mr Lee refunds S$228,000 back to his CPF OA. Net cash Mr Lee receives: S$600,000 − S$228,000 = S$372,000. Mrs Lee’s bank refinances the full S$900,000 mortgage into her sole name (subject to TDSR).

Total decoupling cost to the Lees: BSD S$26,600 + legal S$5,500 = S$32,100. Mr Lee is now a first-time property purchaser. He buys a S$1,800,000 new launch condo: BSD S$53,600, ABSD 0%. Without decoupling, ABSD would have been 20% × S$1,800,000 = S$360,000. Net saving: S$360,000 − S$32,100 = S$327,900.

When Does Decoupling Make Sense?

Decoupling is financially worthwhile when the ABSD saved on the intended second purchase materially exceeds the BSD and legal costs of the transfer. Since ABSD is a flat percentage of the full purchase price and BSD is levied on only half the existing property value at a slab rate, the saving grows steeply with the price of the intended acquisition. At 2026 rates, decoupling is almost always cost-positive for SC couples buying a second property above S$600,000 — the break-even point sits well below the median condo transaction price of approximately S$1.3M (OCR).

Decoupling becomes less attractive — or potentially impossible — in three scenarios. First, when the transferee cannot service the full mortgage alone after TDSR assessment (the bank may require refinancing into the transferee’s sole name, and their income alone may not support the loan quantum). Second, when significant CPF accrued interest reduces the net cash benefit below the headline numbers. Third, when the ownership structure is joint tenancy (which does not recognise distinct shares) and the couple must first convert to tenancy-in-common before the transfer can proceed — a process that also carries legal costs and SLA registration fees.

Can HDB Flats Be Decoupled?

No. HDB resale flats cannot be decoupled in the same way as private properties. Under the Housing & Development Act, any change in ownership of an HDB flat requires HDB approval. HDB will not approve an ownership transfer whose purpose is clearly to circumvent ABSD on a subsequent private property purchase. Any attempt to do so constitutes a breach of HDB rules and may result in the flat being compulsorily acquired. Executive Condominiums during their MOP period are also governed by HDB and cannot be decoupled. After the EC’s 5-year MOP, it transitions to private property status and decoupling becomes legally permissible.

Decoupling Versus Other ABSD Strategies

Decoupling is one of several legally recognised methods for managing ABSD exposure. Alternatives include: the ABSD remission buy-first strategy (SC couple buys second property, pays 20% ABSD upfront, then sells HDB within 6 months and claims remission from IRAS — works only for upgraders selling an HDB); purchasing property in a company structure (ABSD does not technically apply to entities, but Additional Conveyance Duties apply to residential property held by companies, and the rates are punitive); and staggered purchase timing (one spouse buys in their sole name today, the other waits until the first property is sold). Each strategy carries its own cost-benefit profile, legal requirements, and risks. Professional legal and financial advice is essential before committing to any of them.

What Might Come Next for Decoupling in Singapore

This section reflects editorial analysis and is speculative in nature. The Singapore government has been aware of decoupling as a practice for many years. It is sanctioned by law — IRAS collects BSD on every transfer — and there is no indication of an imminent legislative move to prohibit or penalise the practice. However, any significant increase in BSD rates (the last upward revision to the top tier was in February 2023, adding a 6% slab for properties above S$3M) would raise the cost of decoupling proportionally. Conversely, if ABSD rates were ever to be reduced — which would require a material cooling of demand — the financial case for decoupling would diminish but not disappear. For now, decoupling remains a rational and widely-used tax-planning tool for property-owning couples in Singapore.

Frequently Asked Questions

Does IRAS allow decoupling, or is it considered tax evasion?

Decoupling is fully legal and explicitly recognised by IRAS. The Stamp Duties Act requires BSD to be paid on the higher of the agreed consideration or the market value of the transferred interest — IRAS simply ensures the correct amount of stamp duty is paid. What is prohibited is undervaluing the transaction to reduce BSD. Provided the transfer is done at or above market value (supported by a licensed valuation), decoupling is not tax evasion. It is tax planning — the use of lawful structures to minimise tax, as distinct from illegal concealment or misrepresentation.

What does the bank say about decoupling my mortgage?

The bank’s primary concern is that the remaining borrower (the transferee) can independently service the full outstanding mortgage. The bank will reassess the transferee’s TDSR, credit history, and income documentation as if they were applying for the loan afresh. If the transferee’s income alone does not support the existing loan quantum, the bank may require a partial repayment to bring the outstanding loan within acceptable limits. It is advisable to obtain a conditional bank approval before instructing lawyers to proceed with the transfer.

Can unmarried co-owners (e.g. siblings) decouple?

Yes. Decoupling is not restricted to married couples — any co-owners of private property may execute a part-share transfer. The same rules apply: BSD at market value, conveyancing via a licensed lawyer, SLA registration, and CPF refund obligations if applicable. There is no marital relationship requirement. The ABSD saving accrues to whichever party emerges as sole owner and subsequently purchases another property as their “first” private residential acquisition.

Do I need to convert from joint tenancy to tenancy-in-common before decoupling?

Yes, if your property is held as joint tenants. Joint tenancy confers equal undivided ownership with right of survivorship — there are no distinct percentage shares that can be separately transferred. Before a decoupling transfer can proceed, the parties must first sever the joint tenancy and convert to tenancy-in-common (typically 50/50). This severance is registered with SLA and carries a separate fee of approximately S$200–S$500. The lawyer handling the decoupling will usually do this simultaneously as part of the same exercise.

What are the Seller’s Stamp Duty (SSD) implications of decoupling?

If the property being decoupled was acquired less than 3 years ago, the transfer of the half-share may trigger SSD. SSD rates are 12% (if sold in year 1), 8% (year 2), and 4% (year 3) of the higher of the sale price or market value of the interest transferred. For a S$1M half-share disposed of within 2 years of original purchase, SSD could add S$80,000. Most couples planning to decouple therefore wait until their property has been held for at least 3 years. The SSD clock runs from the date of the original purchase, not from the date of decoupling.

What happens to CPF accrued interest when I transfer my share?

When the transferor disposes of their interest in the property (even a 50% share), CPF Board requires the proportionate refund of CPF monies withdrawn for that property — both principal and accrued interest at 2.5% per annum compounded annually. The refund goes back into the transferor’s CPF OA. The amount can be significant on properties held for 10+ years: S$200,000 of CPF drawn at 2.5% compounded annually for 10 years accrues to approximately S$256,000 — meaning the effective CPF refund obligation is S$256,000, not S$200,000. Plan this cash-flow carefully before executing the transfer.

After decoupling, when can the transferor buy a new property?

The transferor can purchase a new property as soon as the decoupling transfer is registered with SLA — typically 6–10 weeks after engaging the lawyers. There is no mandatory waiting period after the transfer. However, it is critical not to exercise the OTP on the new property before the decoupling transfer is registered; doing so could mean you technically hold a 50% share in the existing property at the time of the new purchase, triggering ABSD. The sequencing is: complete decoupling → register transfer → only then exercise OTP on new purchase.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Guide 2026: BSD, ABSD and SSD Explained

- Singapore HDB Upgrading Guide 2026: Costs, ABSD, CPF and Step-by-Step Process

- Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth

- Singapore Property Inheritance Guide 2026

- CPF Property Withdrawal Limits Singapore 2026

- Singapore Home Loan Guide 2026: HDB Loans, Bank Loans and TDSR

- Singapore Property Tax Guide 2026

Disclaimer: This article is provided for general informational purposes only and does not constitute legal, financial, tax, or property advice. Decoupling involves complex stamp duty, CPF, mortgage, and legal considerations that are specific to each individual’s circumstances. BSD and ABSD rates, CPF rules, and HDB policies are subject to change without notice. Always verify current rates and rules directly with the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg, the Singapore Land Authority (SLA) at sla.gov.sg, and the Central Provident Fund Board (CPF Board) at cpf.gov.sg. You should engage a licensed Singapore conveyancing lawyer before proceeding with any property transfer or stamp duty planning strategy.