Singapore ABSD Remission and Refund Guide 2026: SC Couple Scheme, 6-Month Window and Clawback Rules

Quick Answer: ABSD Remission & Refund Singapore 2026 — Key Takeaways

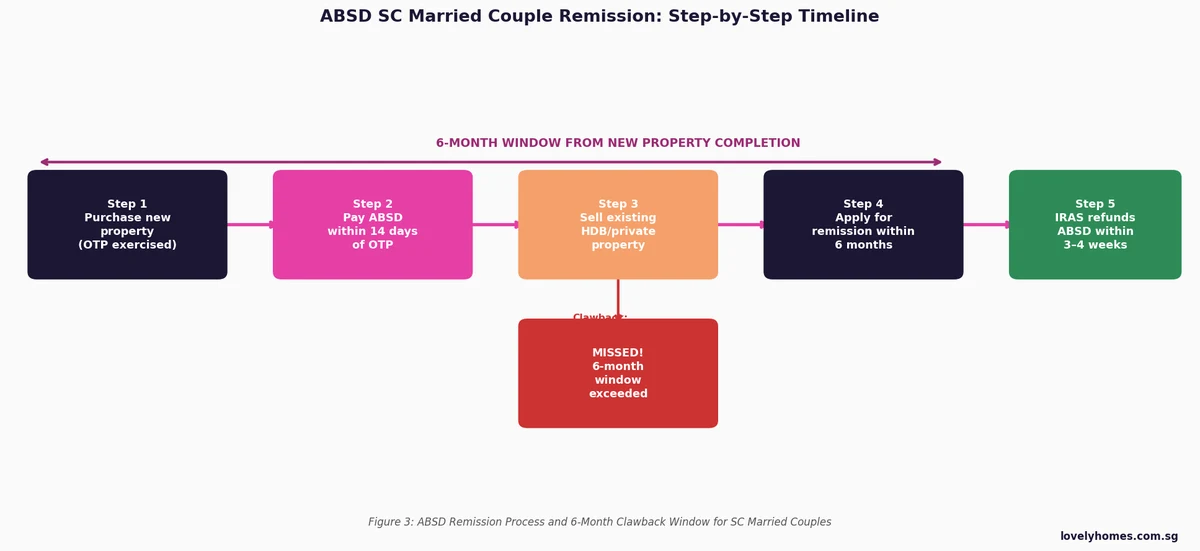

- The ABSD remission scheme for Singapore Citizen (SC) married couples allows a full refund of the 20% ABSD paid on a second residential property purchase — provided both spouses are SC and the existing property is sold within 6 months of the new purchase’s completion date.

- Remission is not automatic: you must apply to IRAS within the 6-month window. IRAS does not proactively initiate the refund.

- If the 6-month window is missed, IRAS will clawback the full ABSD plus interest at 5% per annum from the date of the original transaction.

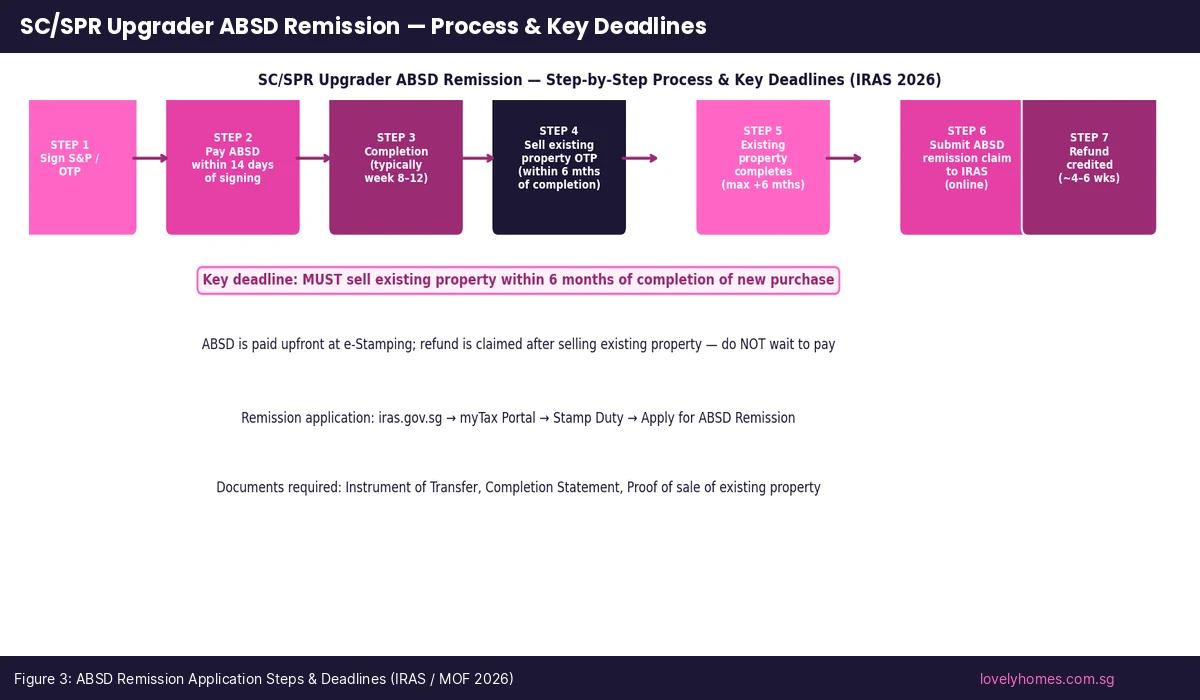

- ABSD must be paid upfront within 14 days of exercising the OTP — the remission is a refund after the fact, not a waiver at the point of purchase.

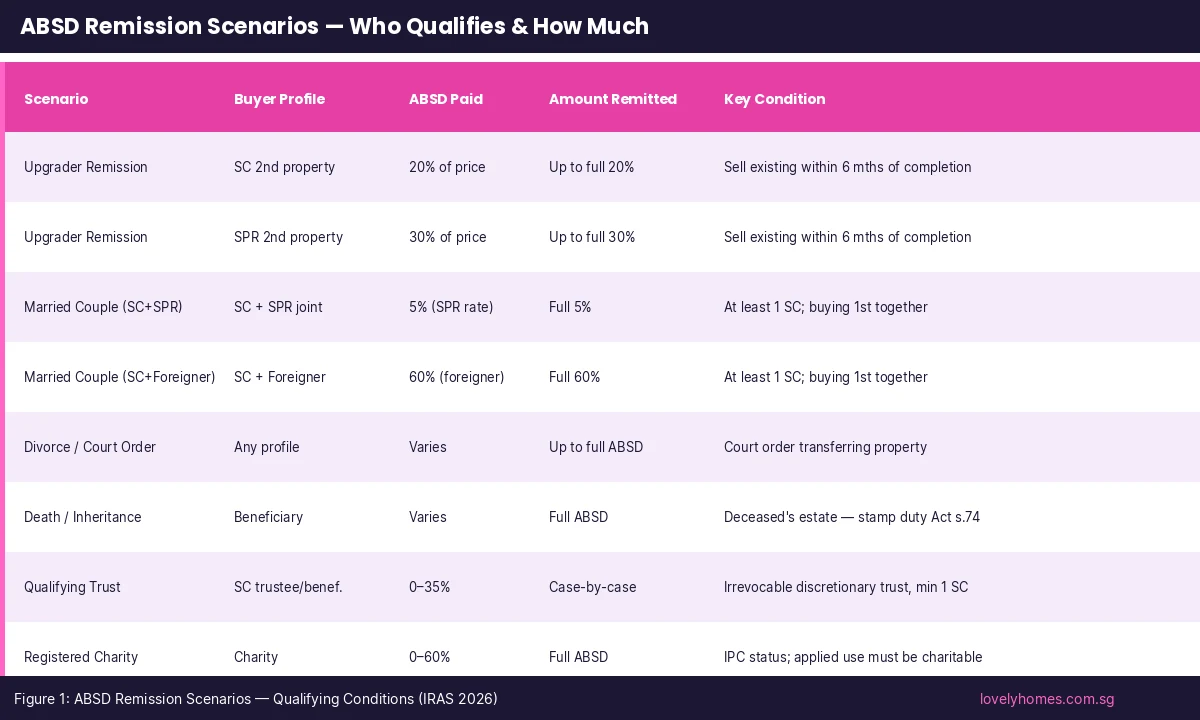

- The remission applies to the first joint property purchase by a SC married couple where both spouses are SC and neither has previously owned another residential property in Singapore simultaneously.

- For SPR married couples buying their first joint property, a separate 5% ABSD remission applies with no sale requirement.

- Developers buying residential land for development qualify for a partial ABSD remission if all units are sold within 5 years; the unsold-unit penalty is significant.

- ABSD remission is separate from BSD — Buyer’s Stamp Duty is never remitted and is always a sunk cost of purchase.

- Careful timing of the HDB sale is essential: sellers must not delay their HDB OTP exercise if they wish to stay within the 6-month window.

What Is ABSD Remission and Who Administers It?

Additional Buyer’s Stamp Duty (ABSD) is levied by the Inland Revenue Authority of Singapore (IRAS) on residential property purchases in Singapore, on top of the standard Buyer’s Stamp Duty (BSD). The ABSD rates introduced in April 2023 are among the highest in Singapore’s property history — 20% for Singapore Citizens buying a second property, 30% for SC buying a third or subsequent property, and 60% for foreign buyers on any purchase. These rates were designed explicitly to curb speculative activity and cool an overheated market.

However, recognising that many SC married couples engage in sequential upgrading — selling their HDB flat and buying a private condominium as a genuine housing upgrade rather than an investment — the government provides a remission (refund) mechanism for a specific, tightly defined buyer profile. This remission does not reduce the ABSD rate payable at purchase; instead, the full ABSD must be paid upfront, and a refund application is made after the old property is sold within the prescribed window.

ABSD remission policy is set by the Ministry of Finance (MOF) and administered by IRAS. Changes to remission criteria require an MOF announcement, usually as part of the broader set of property cooling measure adjustments. The current remission framework has been in force since the April 2023 cooling measure revision.

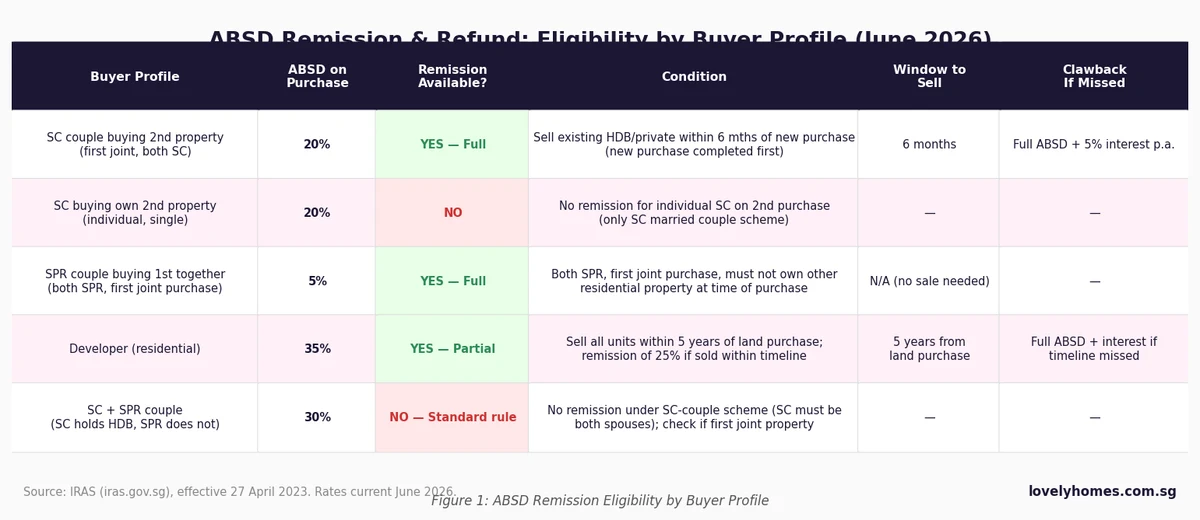

Eligibility Matrix: Who Qualifies for ABSD Remission?

The eligibility criteria are deliberately narrow. The SC married couple remission is the most widely applicable scenario and applies to upgraders transitioning from their HDB flat to a private condominium. Both spouses must be Singapore Citizens (not Permanent Residents, not foreigners) at the time of the new purchase, the new purchase must be their first jointly-owned residential property together (neither spouse may hold another residential property at the time of purchase), and the existing property — typically an HDB flat — must be sold and the sale completed within 6 months of the new property’s purchase completion date.

Critically, the “completion date” for a new launch condominium is the Temporary Occupation Permit (TOP) date, not the date the OTP was exercised or the Sales and Purchase Agreement (SPA) was signed. For resale private properties, completion is typically 10–12 weeks after OTP exercise. This distinction matters greatly for the 6-month window calculation: an SC couple who exercises an OTP on an under-construction new launch today does not begin their 6-month countdown until the project obtains TOP — which could be 3 to 5 years away. This is a significant planning advantage for new-launch buyers compared to resale buyers.

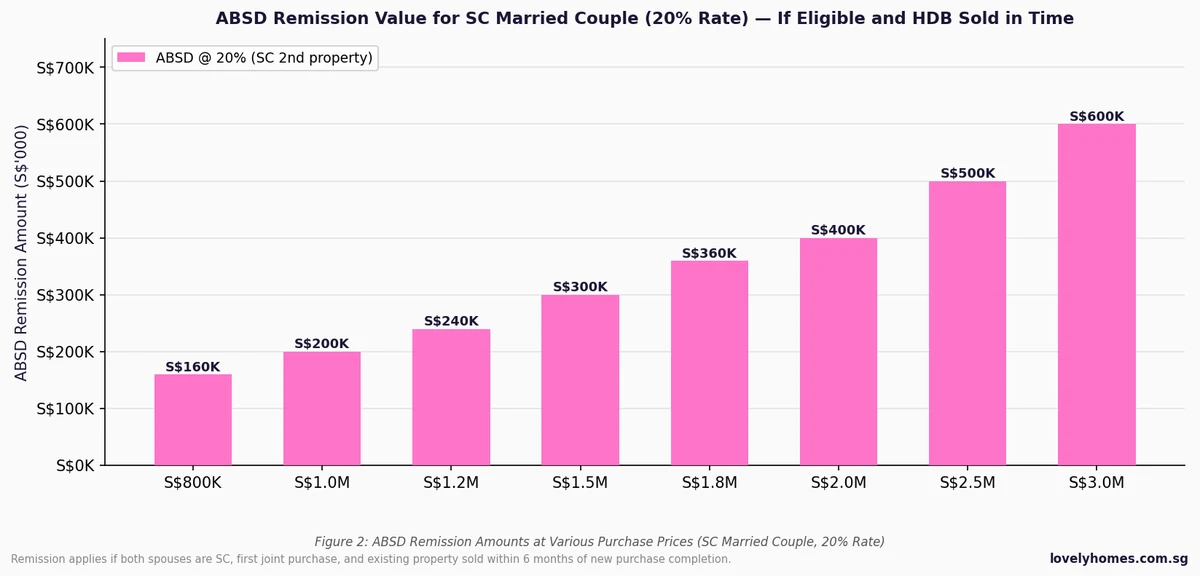

How Much Is the ABSD Remission Worth?

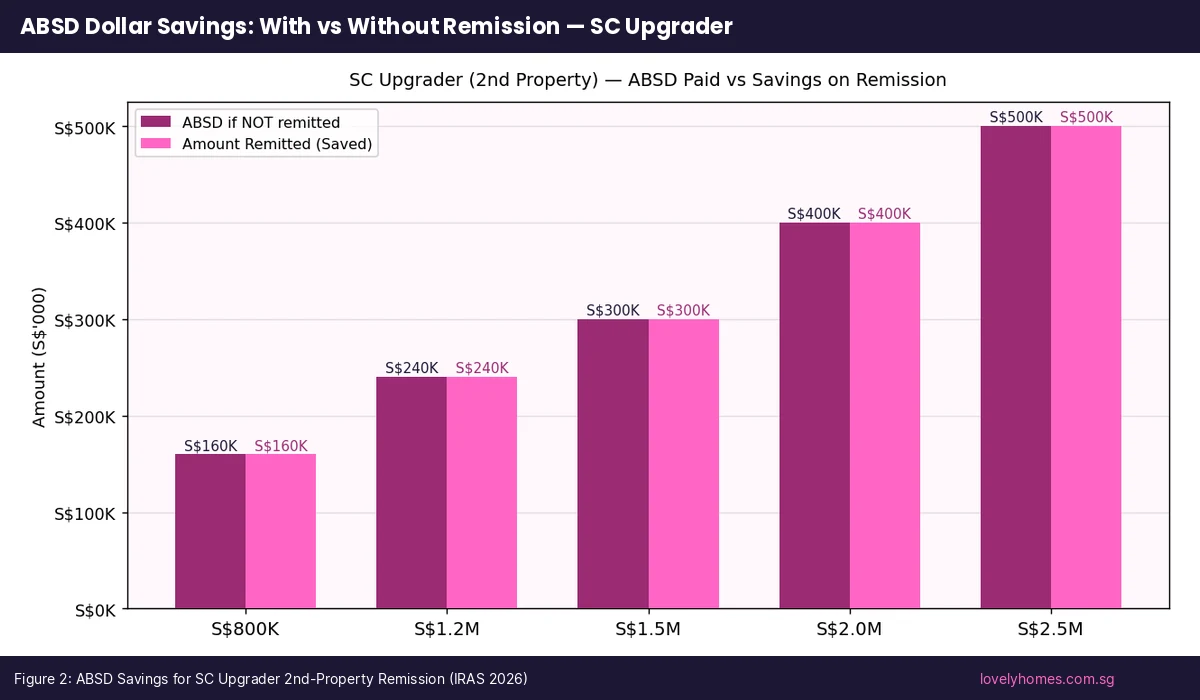

At the current 20% ABSD rate for SC buying a second property, the remission amounts are material — often exceeding the total legal, agent, and renovation costs of the purchase combined. A couple buying a S$1.5 million condominium faces S$300,000 in upfront ABSD, all of which can be recovered if the HDB flat is sold in time. At S$2 million, the recoverable ABSD is S$400,000. These are not marginal amounts: they represent a fundamental difference in the affordability and financial feasibility of the upgrade.

It is worth noting that ABSD cannot be paid from CPF — it must be paid in cash. This means a couple must have S$300,000 to S$600,000 or more in liquid cash available at the time of purchase (before the remission is received). For many upgrading households, this is the single biggest financial planning challenge of the entire transaction. Some couples structure a bridging loan to cover the ABSD temporarily, which is repaid once the HDB flat is sold and the remission is received. The cost of the bridging loan — typically at prime rate or slightly above, for 3–6 months — is a relatively small price for preserving the remission eligibility.

The 6-Month Window: How It Works and the Clawback Risk

The 6-month window begins on the completion date of the new property purchase, not from the OTP date or the SPA signing date. For a private condominium under construction, this is the TOP date. For a resale condominium, it is the completion of the property transfer — typically 10–12 weeks after OTP exercise. The existing property sale must be completed within this 6-month window, not merely contracted or in progress. A scenario where the HDB OTP is exercised on Month 5 but the HDB sale only completes on Month 7 would fail the test.

If the 6-month window is missed — whether due to a buyer falling through on the HDB flat, a delayed completion, or simply poor timeline management — IRAS will issue an assessment for the full ABSD plus interest at 5% per annum from the date of the new property’s stamp duty payment. On a S$300,000 ABSD amount, 5% interest is S$15,000 per year. If the miss is discovered and collected 18 months later, the clawback amount would be approximately S$322,500. There is no grace period and no appeal mechanism short of demonstrating exceptional extenuating circumstances, which IRAS assesses on a case-by-case basis with a high bar for approval.

ABSD Remission at a Glance: Summary Table

| Parameter | Details |

|---|---|

| Who qualifies (main scheme) | Singapore Citizen married couples — both spouses must be SC; first joint property purchase |

| ABSD rate paid upfront | 20% (SC 2nd property) — must be paid in cash within 14 days of OTP exercise |

| Remission quantum | Full 20% of purchase price refunded if conditions met |

| Condition — existing property | Existing HDB flat or private residential property must be fully sold and completed |

| Deadline to sell | Within 6 months of new property completion date (TOP for new launches; legal completion for resale) |

| How to apply | IRAS e-Stamping portal — submit remission application with documentary proof of sale |

| Refund timeline | Typically 3–4 weeks after IRAS approves the application |

| Clawback if missed | Full ABSD + 5% per annum interest from date of original stamp duty payment |

| SPR couple (1st joint) | 5% ABSD remission — no sale condition; applies to first joint purchase where neither holds residential property |

| Can CPF be used for ABSD? | No — ABSD must be paid in cash; CPF cannot be used for ABSD |

| Does BSD get remitted? | No — BSD is always payable and is not remitted under any scheme |

Worked Example: The Ng Family SC Couple Upgrade

Scenario: SC couple selling Sengkang HDB and buying a Tampines resale 3BR condo

Mr and Mrs Ng are Singapore Citizens, married, joint owners of a 5-room HDB flat in Sengkang (Market Value: S$720,000, mortgage outstanding: S$180,000, CPF drawn: S$350,000 + S$65,000 accrued interest = S$415,000). MOP cleared. They wish to upgrade to a 3-bedroom resale condominium in Tampines priced at S$1,600,000.

ABSD calculation:

Purchase price: S$1,600,000

ABSD rate (SC 2nd property): 20%

ABSD payable: S$320,000 (cash, within 14 days of OTP)

BSD: S$44,600 (can use CPF)

Legal fees: ~S$3,500

Agent commission: ~S$16,800 (if using buyer’s agent at 1%+GST)

Cash flow at purchase:

Down payment (25% of S$1.6M): S$400,000 (5% cash = S$80,000 + 20% CPF/cash = S$320,000)

ABSD: S$320,000 cash

BSD (can use CPF): S$44,600

Legal + misc: ~S$20,300

Total cash required before remission: ~S$420,300

HDB sale proceeds (to fund the purchase):

Sale price: S$720,000

Less: outstanding mortgage S$180,000

Less: CPF refund (principal + accrued interest) S$415,000

Less: legal fees + agent commission: ~S$14,800

Net cash from HDB sale: ≈S$110,200

Remission strategy:

The Ngs complete the condominium purchase on 15 July 2026. They have until 15 January 2027 (6 months) to complete the HDB flat sale. They list the HDB at S$720,000 immediately, receive an OTP from a buyer in August 2026, and the sale completes on 15 October 2026 — well within the 6-month window. They apply to IRAS for remission in November 2026 and receive the S$320,000 refund by mid-December 2026.

Net position after remission:

ABSD refunded: S$320,000

Net cash outlay (BSD + legal + agent): ~S$63,100

CPF refund reinvested to CPF OA: S$415,000 (can be redrawn for new condo mortgage servicing)

This is a financially viable upgrade — the key risk is the 6-month sale timeline.

What This Means for Upgraders: Practical Takeaways

For the vast majority of HDB upgraders — SC couples who have cleared their MOP and wish to own a private condominium — the ABSD remission scheme is what makes the upgrade financially viable. Without it, the 20% ABSD on a S$1.5 million–S$2 million condominium would represent a permanent, irrecoverable cost of S$300,000 to S$400,000, which would push many upgrades into the realm of financial imprudence. With the remission, the upgrade structure works — but only if the timing is managed with precision.

The most important practical point is that the HDB sale should not wait until the condominium purchase completes. Upgraders who procrastinate on listing their HDB flat — waiting to see if the condominium purchase proceeds, or delaying to maximise HDB rental income — run a real risk of missing the 6-month window. In a slower resale market, a flat may take 2–4 months to find a buyer and another 8–10 weeks to complete. That is already 5–6 months consumed. There is very little margin for slippage.

The comparison with HDB upgraders buying new launch condominiums is instructive: new launch buyers typically have 3–5 years before TOP, giving them ample time to sell their HDB flat — often at the most favourable market moment. Resale condominium buyers, by contrast, must manage the HDB sale on a much tighter 6-month clock.

What Might Come Next: Remission Policy Outlook

The ABSD remission framework is a carve-out within the broader ABSD system that the Ministry of Finance has maintained consistently since ABSD’s introduction in 2011, though the qualifying conditions and rates have evolved alongside each cooling measure adjustment. There is no current indication that the SC married couple remission will be abolished — it serves an important social function by supporting genuine upgrading rather than speculative multi-property accumulation. However, the remission conditions could tighten further if the government observes systematic abuse or if the market overheats again.

A potential policy direction that has occasionally been discussed in market commentary is the application of ABSD to new launch OTP exercise dates rather than TOP dates, which would eliminate the time advantage new launch buyers currently have over resale buyers in managing the 6-month HDB sale window. If implemented, this would be a material tightening that would force many upgraders to sell their HDB flat before the condominium purchase — reversing the current sequencing that most buyers prefer.

Frequently Asked Questions

Can I use CPF to pay the ABSD before receiving the remission?

No. ABSD must be paid entirely in cash — CPF Ordinary Account funds cannot be used to pay ABSD under any circumstances. This is a hard rule set by IRAS and CPF Board. Only Buyer’s Stamp Duty (BSD) and the property purchase price can be funded using CPF. If you do not have sufficient cash for the ABSD upfront, you may need to explore a bridging loan to cover the amount temporarily, which is repaid once the HDB sale completes and the ABSD remission is received. Always consult a bank or licensed financial adviser about bridging loan options and costs before proceeding.

Does the ABSD remission apply if my spouse is a Singapore Permanent Resident, not a citizen?

No. The SC married couple ABSD remission requires both spouses to be Singapore Citizens at the time of the new property purchase. If one spouse is an SPR and the other is an SC, the SC-couple remission does not apply. In this scenario, the combined SC+SPR buyer profile attracts a 30% ABSD on the second property (or the applicable rate based on the profile with the higher ABSD obligation), and no remission is available for the difference above the SPR rate. SPR married couples buying their first joint residential property can qualify for a separate full remission of their 5% ABSD — but this applies only to SPR+SPR couples on a genuinely first joint purchase where neither holds another residential property.

What if my HDB flat sale falls through after I have already purchased the condominium — can I extend the 6-month window?

IRAS does not provide an automatic extension of the 6-month window due to a failed HDB sale. However, IRAS may consider an extension in exceptional and documented circumstances — for example, if the buyer of the HDB flat absconds or commits a fundamental breach, causing the sale to abort, and the seller (you) acted in good faith to find an alternative buyer promptly. These situations are assessed individually and are not guaranteed. If a buyer falls through, you should immediately relist the flat and notify your conveyancer and IRAS in writing. In a difficult HDB resale market or if the flat is in an over-quota block (EIP), the risk of a failed sale is higher — factor this into your planning before exercising the condominium OTP.

The new launch condominium I bought has been delayed past its expected TOP. Does this affect my 6-month window?

For new launch condominiums, the 6-month remission window begins at the actual TOP date, not the projected or contractual TOP date. If TOP is delayed by 6 or 12 months, your 6-month window shifts accordingly — you have more time to sell your HDB flat. This is generally advantageous: if your HDB flat has already been sold before TOP (as many prudent upgraders do), the delay merely means you wait longer in rental or temporary accommodation before moving into the new property. However, if you have not yet sold the HDB flat and are waiting for clarity on TOP before acting, a TOP delay can compress the effective timeline between TOP and your actual start of marketing, so do not wait for the very last moment.

Is there an ABSD remission for Singapore Citizens who are not married — for example, singles or divorced individuals?

No. The full ABSD remission for a second residential property is only available to married Singapore Citizen couples. Single SC individuals, divorced SC individuals, and cohabiting SC couples (unmarried) do not qualify for the remission and must pay the full 20% ABSD on a second property purchase without any refund mechanism. This is a deliberate policy choice — the remission is designed to support the family unit’s housing upgrade, not individual investment. Singles who wish to own a private condominium after selling their HDB flat may consider selling first and then buying as a first-time private property buyer with no existing HDB — this eliminates the ABSD entirely rather than triggering and then seeking remission.

What documents do I need to apply for the ABSD remission, and how do I submit them?

The ABSD remission application is submitted through IRAS’s e-Stamping portal (mytax.iras.gov.sg). You will need: (a) the stamp duty reference number from the original ABSD payment; (b) a copy of the signed HDB resale completion documents or the private property sale and purchase agreement with evidence of completion (typically a letter from your solicitor confirming that the sale has been completed); (c) evidence that the selling party is the same person/persons who purchased the new property (NRIC details); and (d) your marriage certificate, if not already on record with IRAS. Your conveyancer or property lawyer can typically prepare and submit the remission application as part of the conveyancing engagement — confirm with them early in the process so they are ready to file as soon as the HDB sale completes.

Can the ABSD remission be used if the new property is bought in one spouse’s sole name, not jointly?

This is a nuanced point. The SC married couple remission applies to purchases made in the joint names of both spouses. If the new condominium is purchased in the sole name of one spouse only, the SC married couple scheme may not apply — the buying spouse is effectively treated as an individual, and whether the purchase constitutes a “second property” depends on whether that spouse already holds other residential property. If the buying spouse has never owned a residential property before (having sold their share in the HDB flat prior to purchase, for example), they may qualify as a first-time buyer with 0% ABSD — this is the “decoupling” strategy. Decoupling and ABSD remission are alternative approaches to the same upgrading problem; they are not typically combined in the same transaction. Consult a licensed conveyancer before choosing a structure.

Click anywhere to close