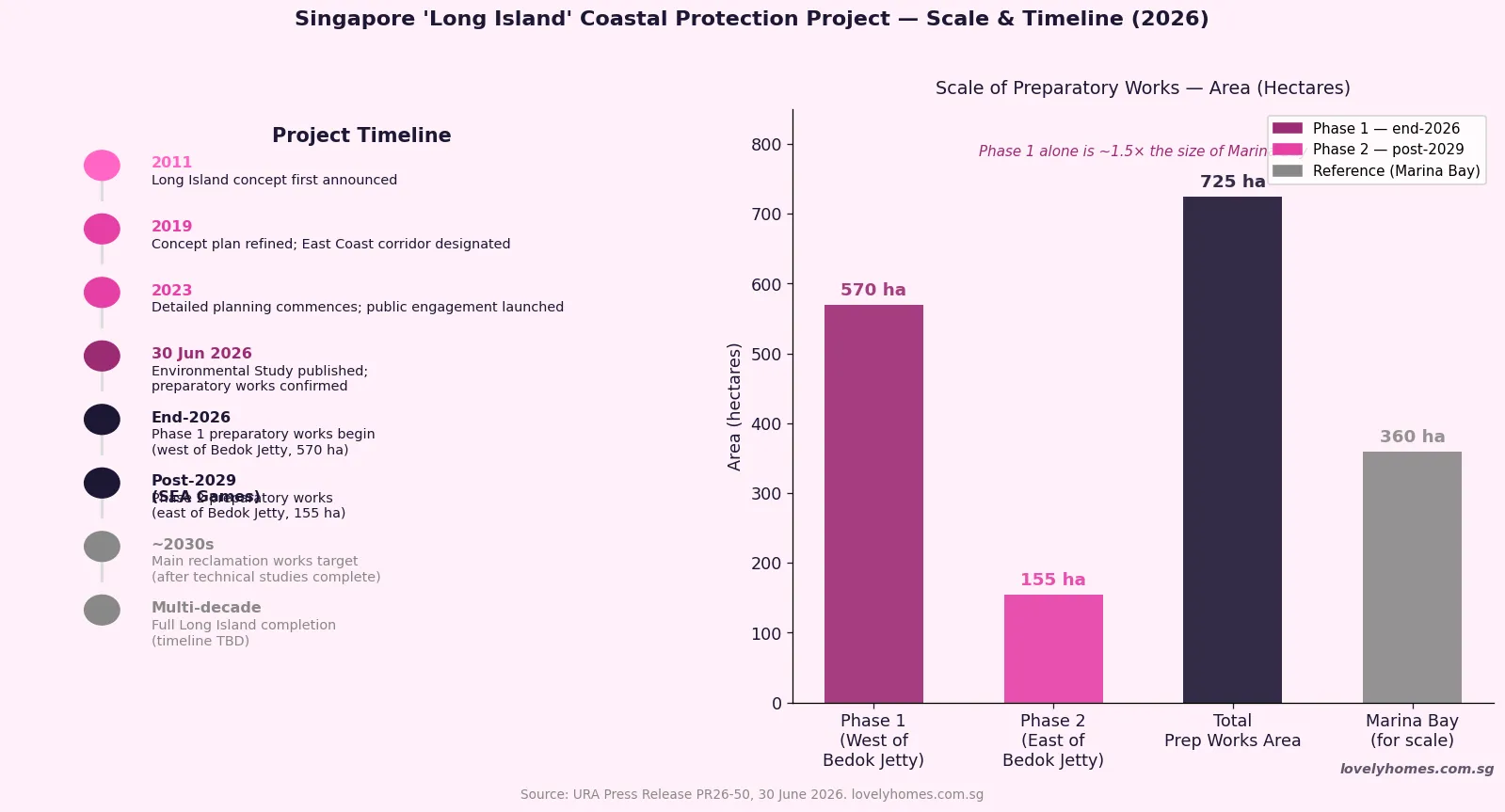

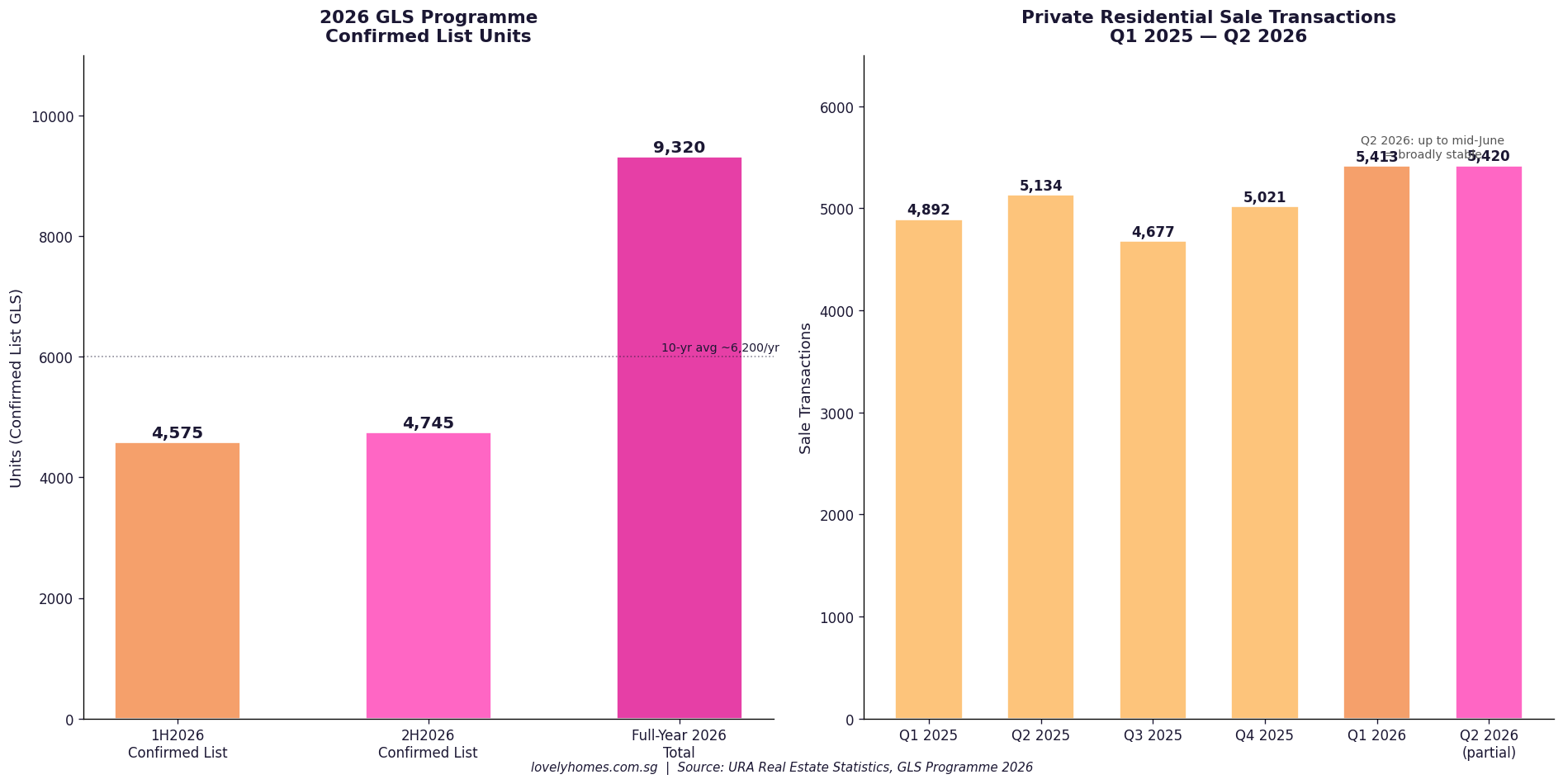

JLD White Site Launched 3 July 2026: Up to 1,200 Homes and 186,000 sqm Mixed-Use Development at Jurong Lake District

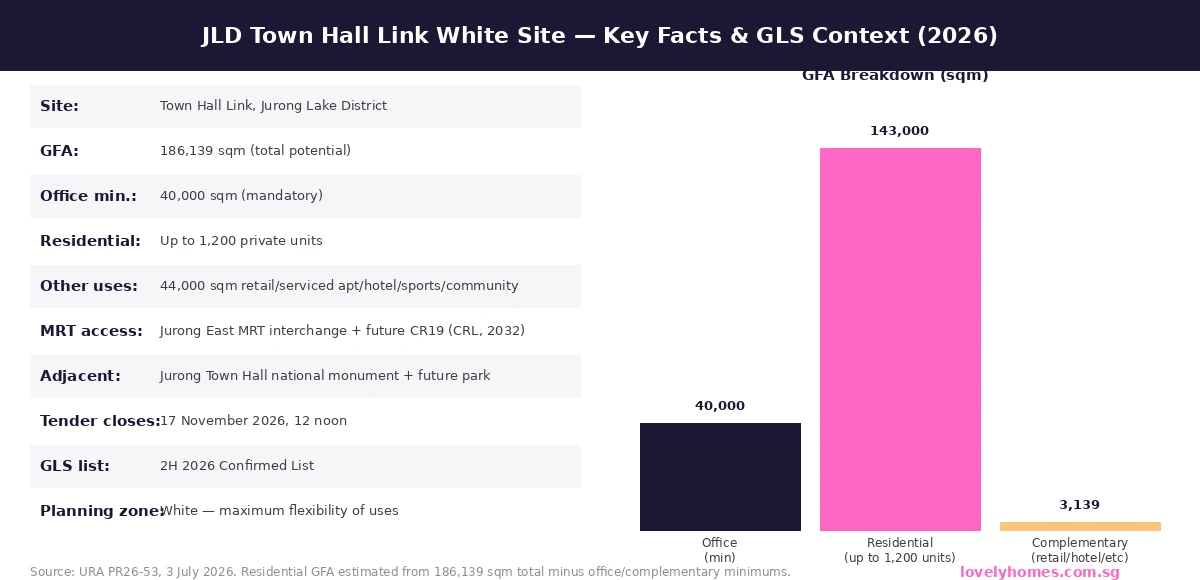

Singapore’s Jurong Lake District (JLD) took a significant leap forward on 3 July 2026 when the Urban Redevelopment Authority (URA) launched the tender for a major White site at Town Hall Link under the second-half 2026 Government Land Sales (GLS) Confirmed List. The site, adjacent to the Jurong Town Hall national monument and flanked by two MRT lines, is earmarked for up to 1,200 private residential units and a minimum of 40,000 sqm of office space within a total potential Gross Floor Area (GFA) of 186,139 sqm. It is the most significant new residential supply announcement for JLD in several years, and it reinforces the Government’s long-standing commitment to transforming the Jurong corridor into Singapore’s largest mixed-use business district outside the city centre.

Quick Answer — JLD White Site at a glance

- What: URA has launched a GLS tender for a White site at Town Hall Link, Jurong Lake District.

- Scale: 186,139 sqm total GFA — minimum 40,000 sqm office, up to 1,200 residential units, 44,000 sqm complementary uses.

- MRT access: Direct connection to Jurong East MRT interchange (EWL + NSL + JRL) and the future CR19 Cross Island Line station (2032).

- Context: Part of Singapore’s decentralisation strategy; JLD is targeted to become the largest mixed-use business node outside the CBD.

- Tender close: 17 November 2026, 12 noon.

- Property implication: First major new private residential supply in the JLD precinct for several years; expect strong developer interest and premium pricing on award.

What Is the JLD White Site and Why Does It Matter?

A White site in Singapore’s GLS framework is a land parcel where the developer is given significant flexibility in determining the mix of uses, subject to minimum requirements. At Town Hall Link, the developer must deliver at least 40,000 sqm of office space (non-negotiable) and may add up to 1,200 private residential units alongside 44,000 sqm of complementary commercial uses such as retail, serviced apartments, hotel, sports and recreational facilities, community spaces, medical clinics, or visitor attractions. The White classification is typically reserved for strategically significant sites where the Government wants the market to determine the optimal product mix — making this tender a test of developer confidence in the JLD vision.

The significance of this announcement extends well beyond the site itself. JLD has been a Government-backed transformational project for more than a decade, anchored by the relocation of Singapore’s second CBD away from the congested city core. The area has seen the revitalisation of the 90-hectare Jurong Lake Gardens, the completion of the Jurong Region Line (JRL), and plans for the Cross Island Line (CRL) station at CR19 in the heart of the precinct (targeted for opening in 2032). The Town Hall Link White site is “seamlessly connected” to the Jurong East MRT interchange via multi-level pedestrian linkages, according to URA.

The JLD Vision: Decentralisation in Action

Singapore’s decentralisation strategy is a long-held urban planning objective. Concentrating economic activity exclusively in the Central Business District and Orchard Road corridor creates congestion, inflates commercial rents, and forces workers into lengthy commutes. JLD is the flagship expression of the alternative vision: a large-scale, self-sustaining regional centre in the west of Singapore, integrating employment, retail, housing, and recreational space in a single walkable precinct.

The Government has invested heavily in the infrastructure backbone. The Jurong Lake Gardens, opened in phases from 2019, provides 90 hectares of recreational greenery wrapping around Jurong Lake and the Chinese and Japanese Gardens. The JRL, opened in stages from 2026, connects the precinct to Tengah, Choa Chu Kang, and Boon Lay. The forthcoming CR19 station on the Cross Island Line will add a further orbital connection in 2032, making JLD one of the best-connected suburban nodes in Singapore’s rail network.

Complementing the White site, two major anchor projects are already under development nearby: the New Science Centre (relocating from its Jurong East home of four decades) and the Jurong Gateway Hub, an integrated development comprising a bus interchange, offices, shops, a library, a community club, and sports facilities. Together with the White site, these projects will define the physical character of the precinct for the next generation.

What the White Site Means for Property Buyers and Investors

| Dimension | Detail | Property Implication |

|---|---|---|

| New supply | Up to 1,200 private residential units at Town Hall Link | First significant new private supply in the JLD precinct for several years; relieves latent demand from west Singapore buyers |

| Price premium | JLD White site is likely an RCR or OCR premium location; comparable JLD projects (J’den, Lake Grande) have traded at S$2,000–S$2,500 psf | Expect developer ask price in the S$2,200–S$2,800 psf range on new launch; potential for appreciation as JLD matures |

| MRT connectivity | Jurong East interchange (3 lines) + future CR19 (CRL, 2032) | Transport connectivity among the best in any non-central precinct; key demand driver for both owner-occupiers and investors |

| Tender timeline | Tender closes 17 November 2026; award ~January 2027; launch likely 2027–2028; TOP ~2032–2033 | Buyers planning a JLD purchase should not expect keys before 2032; factor progressive payment schedule and interim housing into planning |

| Office anchor | Min. 40,000 sqm office must be delivered; targets MNC tenants and financial/professional services firms | Office anchor strengthens daytime population and amenity spending, supporting residential values in the precinct |

| Government commitment | New Science Centre, Jurong Gateway Hub, JRL, CRL CR19 all delivering 2026–2032 | Infrastructure already committed; limited execution risk vs speculative master plans in other regions |

JLD Property Market Context

The private residential market in the JLD corridor has been characterised by limited new supply in recent years. J’den (formerly JEM 2 / Jurong Point 2 site), launched in 2023, sold briskly at an average of approximately S$2,450 psf at launch, underscoring demand from west Singapore buyers seeking integrated development proximity. Older condominiums in the area (Lake Grande, Parc Westlake, Lakeville) have traded resale at lower psf levels but have appreciated meaningfully over their launch prices.

The White site at Town Hall Link is a different proposition: a larger, more prominent, and better-connected site adjacent to both heritage (Jurong Town Hall) and nature (the future park). Developers tendering for this site will need to deliver a mixed-use product integrating office, residential, and retail — a complex brief that typically appeals to the largest developers with integrated development track records. The 1,200-unit residential cap, while meaningful, represents a medium-density residential component within a predominantly commercial site.

For buyers tracking west Singapore property, the White site tender provides a clear signal: JLD is still an active, Government-supported investment in Singapore’s urban future. The tender award (expected early 2027) and any subsequent launch announcement will be significant market events for the west corridor.

What to Watch Next

The tender closes on 17 November 2026. Bids are expected from Singapore’s major developers, and possibly consortia given the scale and complexity of the White site requirements. The tender award will reveal the market’s view of JLD land value — a key data point for pricing expectations on the eventual new launch. Any premium bid above market expectations would signal high developer confidence in JLD residential absorption; a cautious single bidder would suggest more measured enthusiasm.

Separately, the full Q2 2026 URA private residential data release (expected ~24 July 2026) will include CCR, RCR, and OCR transaction data that contextualises JLD’s position in the wider market. The Q2 flash estimate showed overall prices up +0.5% with CCR leading — a context in which a well-connected, large-scale JLD development arriving in 2027–2028 could attract strong demand from both upgraders and investors seeking alternatives to pricier CCR addresses.

Frequently Asked Questions About the JLD White Site

What is a White site in Singapore’s GLS programme?

A White site is a land parcel sold by URA under the Government Land Sales programme where the developer has flexibility to incorporate a range of uses — residential, commercial, hotel, recreational, and community — subject to minimum requirements set by URA. The White classification is used for strategic locations where the Government wants the private market to determine the most commercially viable use mix, while ensuring a minimum anchor use (in this case, 40,000 sqm of office) is delivered to support the Government’s planning goals. White sites are typically larger and more complex than single-use residential or commercial sites, and they attract the largest and most financially capable developers.

When will the JLD White site residential units be available for purchase?

The tender closes on 17 November 2026. Following award (likely early 2027), the developer will typically spend 12–18 months on design, approvals, and construction preparation before launching for sale. A reasonable estimate for launch to the public is late 2027 to 2028. Construction of a mixed-use development of this scale typically takes 4–5 years, suggesting Temporary Occupation Permit (TOP) around 2032–2033 — which coincides with the opening of the CR19 Cross Island Line station in the heart of JLD. Buyers interested in this project should plan for a progressive payment schedule over this period and interim housing arrangements.

How does the JLD White site compare to other west Singapore property options?

The JLD White site will deliver a qualitatively different product from most west Singapore residential projects. Its direct connection to the Jurong East interchange (which currently serves the East-West Line, North-South Line, and Jurong Region Line) and the future CR19 station makes it exceptionally well-connected — comparable connectivity exists in only a handful of suburban locations in Singapore. The adjacent Jurong Town Hall national monument and future park provide irreplaceable location attributes. However, buyers should note that the residential component is capped at 1,200 units within a larger commercial development, meaning the residential element is not a standalone condominium but part of an integrated mixed-use project — similar to Duo Residences in Bugis or Marina One Residences at Marina Bay. Pricing will reflect this premium integrated product positioning.

Is Jurong Lake District a good area for property investment?

JLD has strong structural fundamentals as a long-term investment: committed Government infrastructure, rail connectivity improving through 2032, a large employment base (Jurong East, International Business Park, Biopolis in one-stop range), and a diversified demographic base. The risk factors are the long development timeline (appreciation is gradual rather than immediate), competition from other west corridor supply (Tengah, Bukit Batok, Jurong East BTO supply is meaningful), and execution risk on the commercial components of the mixed-use development. Industry analysts generally view JLD as a medium-term (5–10 year) capital appreciation story rather than a short-term trading position. The announcement of the White site tender strengthens the longer-term investment case. As with all property investments, buyers should assess their own holding capacity and financial position carefully before committing.

What is the Cross Island Line and why does it matter for JLD?

The Cross Island Line (CRL) is a new MRT line currently under construction by the Land Transport Authority. It will run across Singapore from Changi in the east to Jurong in the west, passing through several major nodes including Clementi, Jurong Lake District, and Ang Mo Kio. The CR19 station, located in the heart of JLD, is planned to open in 2032. When operational, CR19 will add a key orbital connection to the existing East-West Line and North-South Line services at Jurong East interchange, effectively giving JLD three distinct MRT lines through the precinct. This level of rail connectivity is rare outside the central area of Singapore, and it is a significant long-term demand driver for both commercial and residential property in JLD.

Related Articles

- URA Q2 2026 Flash Estimates: Singapore Private Home Prices Rise +0.5%

- Singapore Property Cooling Measures 2026: Complete Guide to ABSD, TDSR and LTV

- Singapore New Launch Condo Buying Guide 2026: Showflat, Balloting and Progressive Payments

- Singapore Condo Buying Process 2026: Step-by-Step from Offer to Keys

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

Disclaimer: This article is based on URA press release PR26-53 dated 3 July 2026 and publicly available Government data. Residential unit count, GFA figures, and MRT opening dates are as stated by URA and LTA and are subject to change. Price projections, investment analysis, and developer interest assessments represent editorial analysis only and do not constitute financial advice. Readers should conduct their own due diligence and consult licensed professionals before making any property purchase decision. For the authoritative site details, visit URA Land Sales. LovelyHomes does not provide financial or property advisory services.