Singapore Joint Property Ownership Guide 2026: Joint Tenancy, Tenancy-in-Common, ABSD and CPF Rules

📌 Quick Answer: Joint Property Ownership in Singapore (2026)

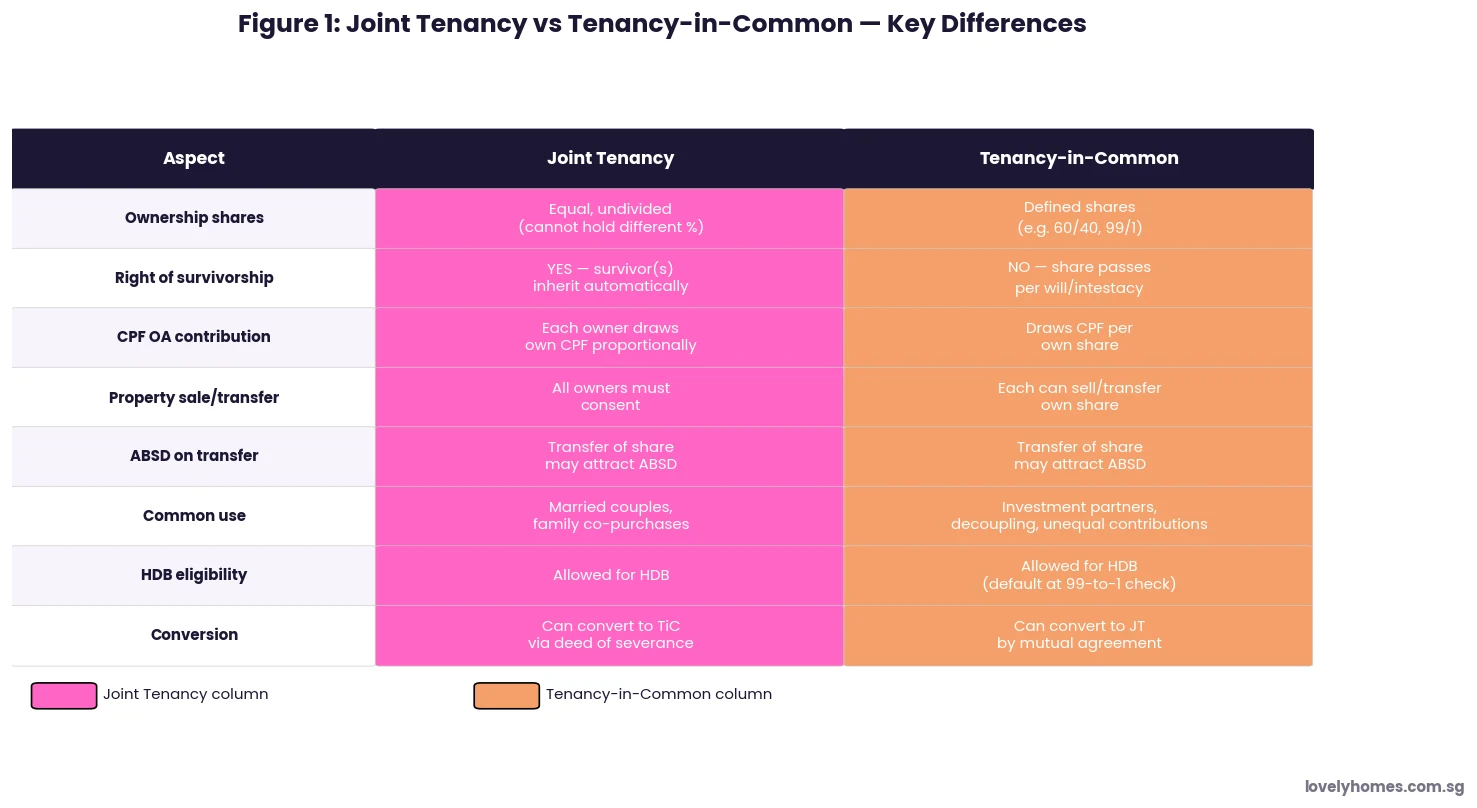

- Two ownership structures exist: Joint Tenancy (JT) — equal, undivided shares with automatic survivorship; and Tenancy-in-Common (TiC) — defined shares that can be unequal, with no survivorship right.

- HDB flats default to joint tenancy for married couples; tenancy-in-common is permitted and commonly used for investment structuring (e.g. 99/1 split), though IRAS scrutinises artificial arrangements.

- ABSD applies per buyer — each co-owner’s ABSD rate is based on their own individual property count. A transfer of share between co-owners may attract ABSD and BSD on the transferred portion.

- CPF Ordinary Account usage is allocated per owner’s share. Each owner refunds their own CPF drawn — principal plus 2.5% p.a. accrued interest — to their own OA upon sale.

- Decoupling (transferring one spouse’s share to the other) allows one party to then purchase a second property with a lower ABSD rate as a “first-time buyer” — but costs BSD on the half-share and requires full bank refinancing checks.

- Intestacy risk: Under tenancy-in-common, your share passes via your will (or the Intestate Succession Act if you die without a will). Under joint tenancy, the surviving owner inherits automatically regardless of your will.

Joint Property Ownership in Singapore: An Overview

Purchasing property with a spouse, family member, or investment partner is common in Singapore. Whether you are a married couple buying your first HDB flat, siblings co-investing in a private condo, or business partners acquiring a shophouse, the legal form of co-ownership you choose has significant consequences for your stamp duties, CPF usage, mortgage liability, inheritance planning, and future asset reallocation strategy.

Singapore property law recognises two main forms of co-ownership: joint tenancy and tenancy-in-common. These are derived from English common law and codified in Singapore’s Land Titles Act (Cap. 157). They differ fundamentally in the nature of the ownership interest each party holds and in how that interest passes on death.

Understanding which structure applies to your purchase — and whether switching between them makes sense at different life stages — is essential for anyone who co-owns or intends to co-own property in Singapore.

Joint Tenancy: Equal Ownership with Survivorship

In a joint tenancy, every co-owner holds an equal and undivided interest in the entire property. There are no defined percentage shares — each joint tenant owns 100% of the property, concurrently with the other joint tenants. This may sound paradoxical, but it is precisely this conceptual structure that enables the right of survivorship: when one joint tenant dies, their interest does not form part of their estate but instead vests automatically in the surviving joint tenant(s), regardless of what their will says.

For married couples purchasing their matrimonial home, joint tenancy reflects the expectation of mutual commitment: neither party can unilaterally dispose of their share without the other’s consent, and neither party can bequeath the property to a third party outside the marriage while the other spouse survives. This makes joint tenancy the default and legally preferred form for HDB flat ownership by married couples.

Practical implications of joint tenancy:

- A court order (e.g. in a divorce or a creditor’s claim) can sever a joint tenancy and convert it to a tenancy-in-common, enabling the sale of one party’s share.

- Banks typically treat all joint tenants as jointly and severally liable for the mortgage. If one party defaults, the other is fully liable for the outstanding debt.

- All joint tenants must consent to a sale or mortgage. This is both a protection and a constraint.

- For CPF purposes, each joint tenant is deemed to have drawn CPF in proportion to their purchase price contribution, even though the legal title is held equally.

Tenancy-in-Common: Defined Shares and Investment Flexibility

In a tenancy-in-common, each co-owner holds a separate, defined fractional interest in the property. The shares need not be equal — they can be set at any percentage that reflects the parties’ respective financial contributions or commercial agreement: 50/50, 70/30, 90/10, even 99/1. Each tenancy-in-common share is a distinct, transferable legal interest. An owner can sell, mortgage, or bequeath their share independently of the others.

No right of survivorship exists under tenancy-in-common. If you die with a 40% share in a property, that 40% passes according to your will. If you have no will, it is distributed under the Intestate Succession Act (Cap. 146) — which may not align with your wishes. This is a frequently overlooked planning gap, particularly for unmarried co-owners or investment partners.

Tenancy-in-common is commonly chosen for:

- Investment properties where each co-owner contributes a different amount and wants a proportionate return.

- Decoupling strategies where one spouse later transfers their share to the other to free up their ABSD count for a second purchase.

- Multi-generational purchases involving parents and children with different financial contributions.

- Sibling or business-partner purchases where the parties are not romantically involved and have independent estate plans.

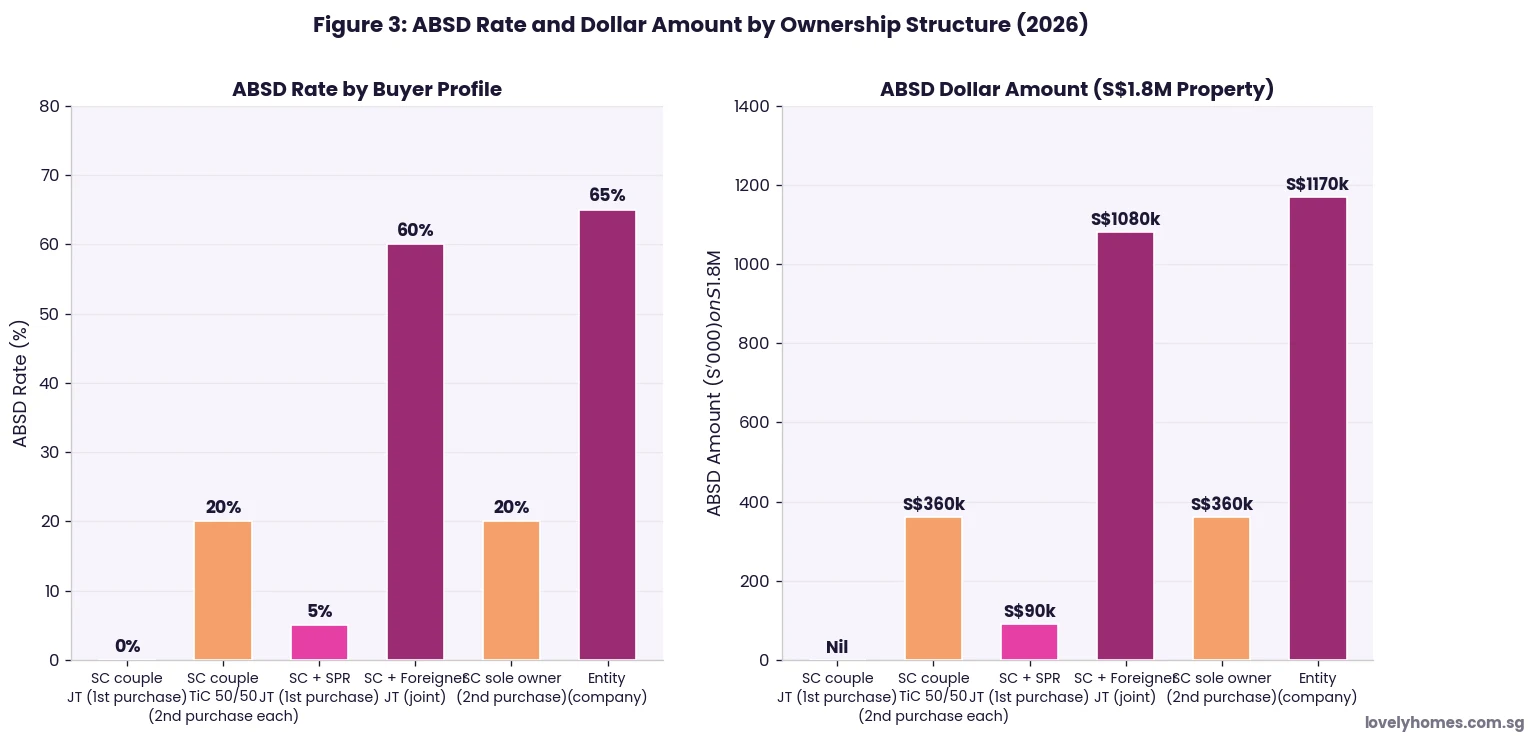

ABSD Implications: How Co-Ownership Affects Your Stamp Duty

Additional Buyer’s Stamp Duty (ABSD) is charged on the full purchase price of the property, not on each buyer’s share. However, the applicable ABSD rate for each buyer is determined by their own individual residential property count in Singapore at the time of purchase. This creates important nuances in co-ownership situations.

For example, if Singapore Citizen Mr Lim (first property) and Permanent Resident Ms Chen (first property for her) jointly purchase a condo, the ABSD rate is the higher of the two applicable rates — in this case, 5% (SPR rate for first property) — applied to the full purchase price. The system does not split the ABSD proportionally; the most onerous applicable rate prevails.

| Co-ownership Profile | ABSD Rate | ABSD on S$1.8M | Note |

|---|---|---|---|

| SC + SC (both first property) | 0% | Nil | SC first-property exemption |

| SC (first) + SPR (first) | 5% | S$90,000 | Higher rate (SPR) applies |

| SC (second) + SC (first) | 20% | S$360,000 | Higher rate applies; payable in full on 100% price |

| SC + Foreigner | 60% | S$1,080,000 | Foreigner rate applies to full price |

| Company / entity | 65% | S$1,170,000 | No remission available for entities |

Source: IRAS, effective as of June 2026.

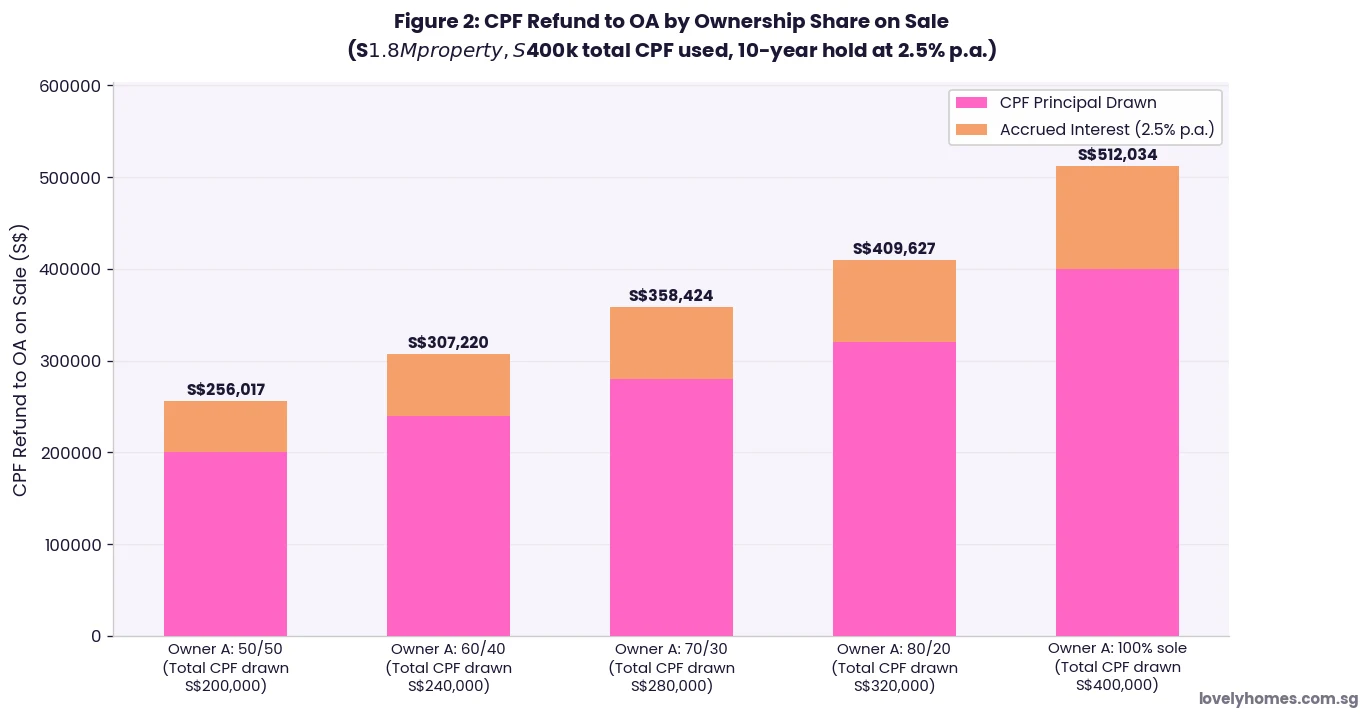

CPF Usage Under Co-Ownership: Shares and Refund Rules

When a property is co-owned, each party may contribute their own CPF Ordinary Account (OA) funds towards the purchase — for the down payment, monthly mortgage instalments, BSD, and legal fees. The amount each co-owner can draw is subject to the usual CPF Valuation Limit (VL) and Withdrawal Limit (WL) constraints, applied to their proportionate share of the property.

Under tenancy-in-common, CPF contributions are tracked per owner’s defined share. Under joint tenancy, CPF draws are typically in proportion to the purchase price contribution, even though legal ownership is equal and undivided. On sale of the property, each owner must refund their own CPF principal plus accrued interest at 2.5% per annum into their own Ordinary Account. This refund is mandatory regardless of whether the sale price exceeds the purchase price.

Decoupling: Converting Tenancy to Free Up ABSD Count

Decoupling refers to the process of transferring one co-owner’s share to the other, so that the transferring party becomes a zero-property owner and can subsequently buy a new property at a lower ABSD rate. This strategy is most commonly used by married couples who co-own a private property and wish to purchase a second investment property without incurring the 20% ABSD on the second purchase.

The transfer attracts BSD on the transferred share at prevailing rates. For example, if the transfer value of the half-share is S$900,000, BSD is approximately S$26,600. Legal fees for the decoupling conveyancing typically run S$4,000–S$8,000 plus GST. ABSD is also payable on the transferee’s side if it triggers a property count increase.

Since April 2023, IRAS has applied heightened scrutiny to 99-to-1 arrangements — where one party buys 99% and the other 1% specifically to exploit ABSD count. Arrangements that IRAS determines to be artificial may result in the ABSD being levied on the full value rather than the proportionate share. Buyers should seek proper legal advice and ensure their co-ownership structure reflects genuine commercial intent.

Worked Example: Mr & Mrs Wong — Converting JT to TiC for Decoupling

📄 Worked Example — Married SC Couple Converting Ownership for Second Purchase

Background: Mr & Mrs Wong, both Singapore Citizens, jointly own a Bishan private condo purchased in 2021 for S$1,600,000. Outstanding loan: S$880,000. Mr Wong’s CPF OA drawn: S$180,000 (principal). Mrs Wong’s CPF OA drawn: S$120,000 (principal). Property current market value: S$2,000,000. Ownership: joint tenancy 50/50.

Goal: Purchase a second investment condo (S$1,500,000 in OCR) without paying 20% ABSD (S$300,000).

Step 1 — Convert JT to TiC: Mr & Mrs Wong execute a deed of severance to convert joint tenancy to tenancy-in-common in equal shares. Cost: approximately S$800 in SLA fees + legal disbursements.

Step 2 — Decouple: Mrs Wong transfers her 50% share (value: S$1,000,000) to Mr Wong. BSD on S$1,000,000: S$24,600. Mrs Wong’s CPF refund obligation: S$120,000 × (1.025)^5 ≈ S$135,900. Legal fees: S$5,500. Total decoupling cost: approximately S$30,100 + CPF refund.

Step 3 — Mr Wong refinances: Bank reassesses TDSR on sole ownership. New mortgage S$1,120,000 (existing S$880,000 + S$240,000 top-up for decoupling costs). Monthly S$4,711 @3.2% 30yr — Mr Wong’s income S$14,000/month, TDSR 33.7% PASS.

Step 4 — Mrs Wong buys second condo: As a Singapore Citizen first-property buyer, Mrs Wong pays 0% ABSD on the S$1,500,000 OCR condo. ABSD saving vs joint purchase: S$300,000. Net saving after decoupling costs: S$269,900.

Note: This is an illustrative example. Actual ABSD/BSD rates, CPF drawdown, TDSR assessment, and legal costs may vary. Seek legal and financial advice before executing any property transfer.

Joint Ownership and Estate Planning: The Survivorship Risk

One of the most consequential differences between joint tenancy and tenancy-in-common is the estate-planning dimension, which is frequently overlooked by younger buyers focused on financing and stamp duties.

Under joint tenancy, your interest in the property does not exist as a separate asset in your estate. When you die, your joint tenancy interest extinguishes and the survivors’ interests expand to absorb it. Your will cannot override this. If you are a joint tenant and die, the property belongs entirely to the survivor, regardless of your wishes. This is protective in a stable marriage but potentially damaging in an estranged or second-marriage scenario, where you may prefer a portion of the property to pass to children from a prior relationship.

Under tenancy-in-common, your defined share is an asset in your estate. It passes per your will, or per the Intestate Succession Act if you die intestate. This gives you full testamentary control over your property share but requires that you actually execute a valid will and keep it updated. Unmarried co-owners and investment partners should always hold as tenants-in-common and maintain current wills.

What Might Change Next: Ownership Structure Policy Outlook

The following is editorial analysis and is not government policy. The government’s tightening of 99-to-1 arrangements in April 2023 signalled that IRAS will continue to scrutinise co-ownership structures that appear designed primarily to circumvent ABSD, rather than reflecting genuine co-ownership intentions. Future refinements may include clearer IRAS guidance on acceptable tenancy-in-common ratios, or legislative changes to deem artificial structures as ABSD-liable on the full purchase value. Buyers considering unconventional co-ownership splits for tax planning purposes should seek specific legal advice in the current regulatory environment.

Frequently Asked Questions

Can HDB flat owners hold as tenants-in-common?

Does a joint tenancy convert to tenancy-in-common automatically on divorce?

If my co-owner refuses to sell, can I force a sale?

Does ABSD apply when a parent transfers a property share to a child?

Can a Singapore Permanent Resident co-own an HDB flat as a tenant-in-common?

What is the difference between “tenancy” (as in renting) and “tenancy-in-common”?

Should I hold investment property as joint tenancy or tenancy-in-common?

Related Articles

Click anywhere outside to close