Singapore HDB Upgrading Guide 2026: Costs, ABSD, CPF and Step-by-Step Process

Quick Answer: HDB Upgrading Guide 2026

- Who can upgrade? SC and PR households who have fulfilled the HDB Minimum Occupation Period (MOP) — 5 years for standard flats, 10 years for Plus/Prime flats classified from October 2024.

- Typical upgrade path: Sell HDB first (avoid ABSD), then buy a private condo. Alternatively, buy first and claim ABSD remission within 6 months of selling.

- ABSD on 2nd property: SC pays 20%, PR pays 30%, foreigners 65%. Selling HDB first means the condo is your 1st private purchase — 0% ABSD for SC couples.

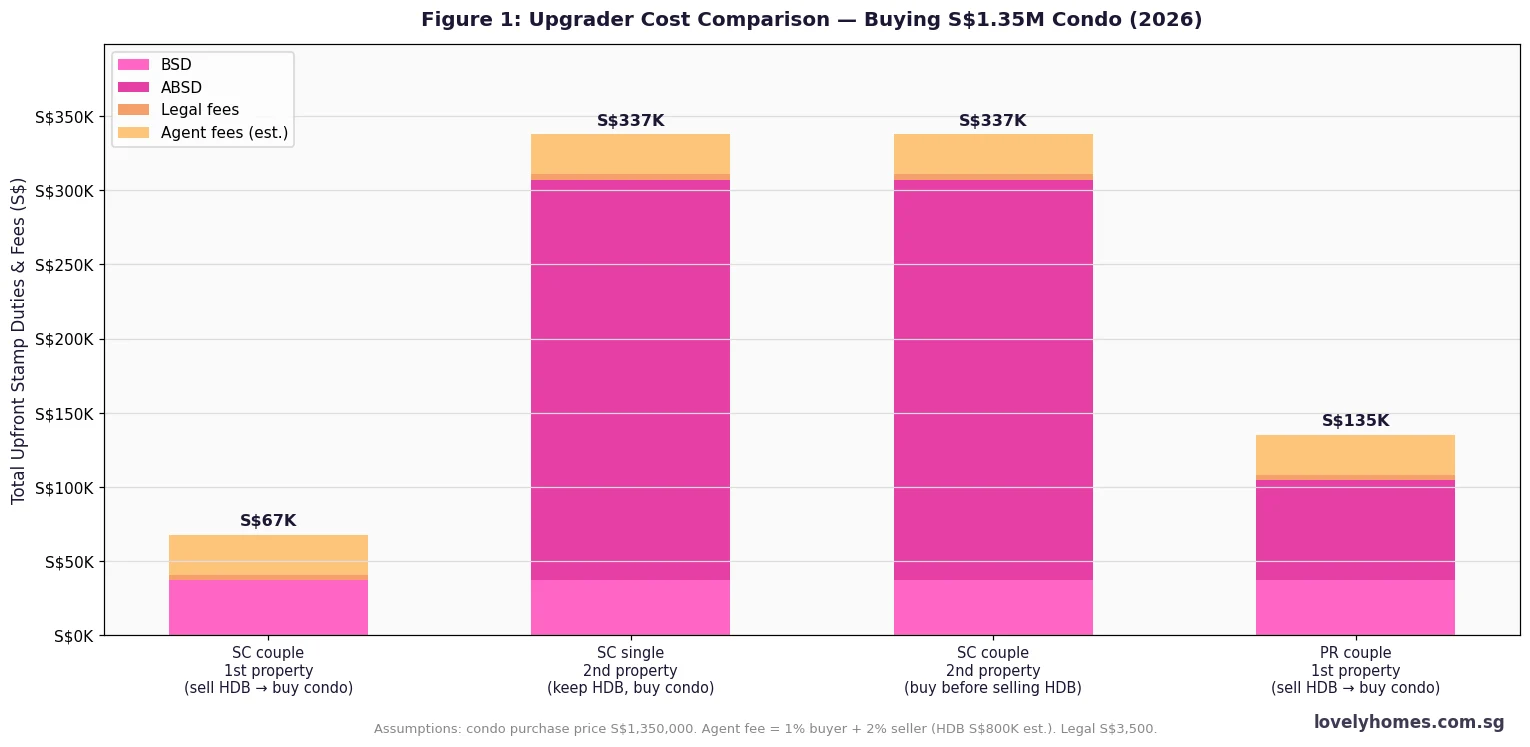

- Upgrader costs at S$1.35M condo: BSD ~S$37,200 + agent ~S$27,000 (selling + buying). No ABSD if HDB is sold first.

- CPF: All CPF used for HDB (principal + 2.5% p.a. accrued interest) must be refunded to your CPF OA on sale. Net cash proceeds fund the condo down payment.

- TDSR cap: 55% of gross monthly income. For a S$1.35M condo at 30-year tenor, monthly repayment at 3.0% is ~S$5,690 — household income of at least S$10,345/mth needed.

- Sell-first vs buy-first: Sell-first saves 20% ABSD but carries gap-period risk. Buy-first triggers ABSD upfront, claimable back within 6 months of HDB sale completion.

For many Singaporean families, the journey from an HDB flat to a private property is the single largest financial milestone of their lives. The HDB upgrading guide process — commonly called “upgrading” — involves selling your public housing flat and buying a condominium, landed property, or Executive Condominium (EC) once your Minimum Occupation Period (MOP) is met. In 2026, upgrading remains very much alive: URA Q1 2026 data shows Outside Central Region (OCR) condo prices up 2.2% quarter-on-quarter, and HDB resale volumes continue to provide upgraders with strong equity to deploy.

Upgrading is simultaneously a financial decision, a tax-planning exercise, and a lifestyle transition. This guide, updated for Singapore HDB upgrading 2026, covers everything from MOP eligibility and ABSD implications to working through the exact stamp duties, CPF obligations, and loan calculations that determine whether the numbers stack up for your household.

Who Is Eligible to Upgrade from HDB?

The primary eligibility gate is the Minimum Occupation Period administered by the Housing & Development Board (HDB) under the Housing & Development Act. For most HDB flats bought on the open market or through BTO exercises before October 2024, the MOP is 5 years from the date the keys are collected. For Plus and Prime flats classified under the new framework introduced in October 2024, the MOP is 10 years. If you purchased a Prime Location Public Housing (PLH) flat before October 2024, the MOP for that flat is also 10 years.

During the MOP, you cannot sell the flat, rent out the entire flat, or acquire any private residential property in Singapore or overseas. Once the MOP is fulfilled, these restrictions are lifted — you are free to sell your HDB and buy private property simultaneously or in sequence. Singapore Citizens (SC) have the most favourable ABSD profile for this transition; Permanent Residents (PR) and foreigners face significantly higher stamp duties on private property acquisition.

The Core Upgrade Decision: Sell-First or Buy-First?

The most consequential choice in the upgrading journey is sell-first versus buy-first. Both strategies are legal and used regularly; the right answer depends on your household’s liquidity, risk appetite, and the current market cycle.

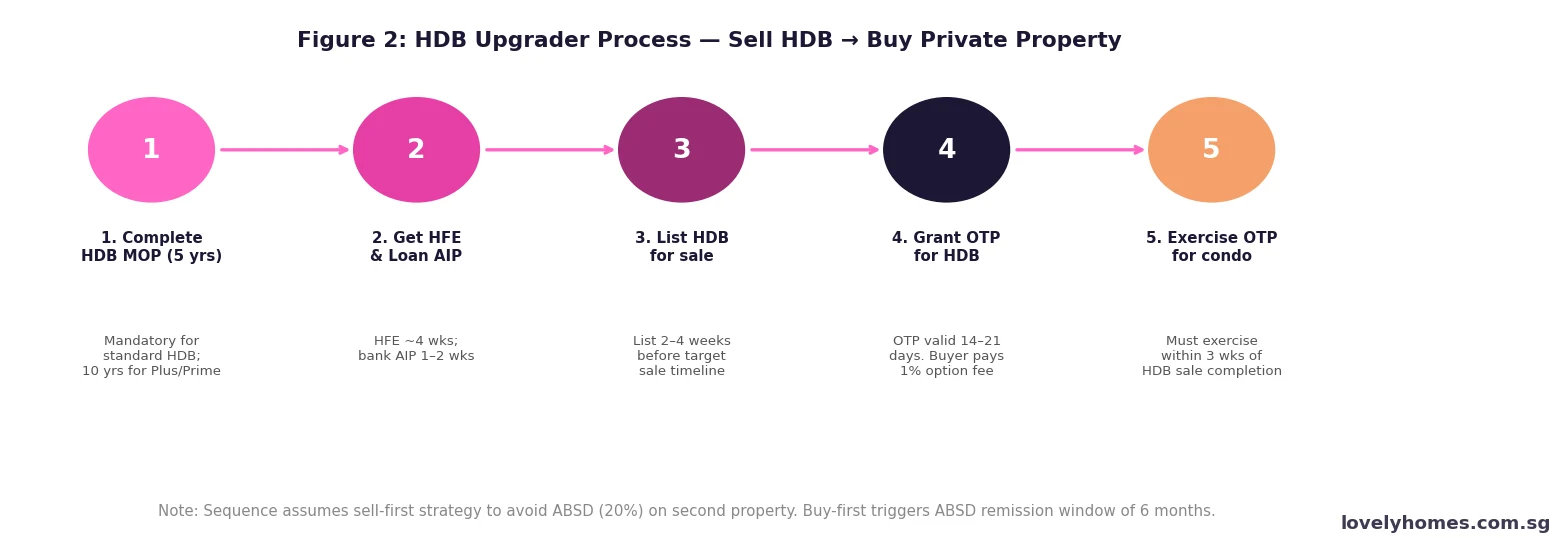

Under sell-first, you obtain an Option to Purchase (OTP) for your HDB buyer, complete the HDB sale, then use the proceeds to exercise an OTP on your chosen condo. Because your HDB is sold before you acquire private property, the condo is treated as your first private residential purchase — 0% ABSD for SC couples, 5% for PRs. The downside is a gap period between vacating your HDB and taking possession of the condo (typically 3–6 months if buying resale, or 3–5 years if buying a new launch off-plan).

Under buy-first, you exercise the condo OTP before completing the HDB sale. Because you momentarily own both properties, IRAS treats the condo as a second property and levies ABSD upfront — 20% for SC couples at the time of writing. The Inland Revenue Authority of Singapore (IRAS), however, provides a ABSD remission window of 6 months from the date the condo is purchased (or the date the condo is completed, for new launches). If you sell and complete the HDB transfer within that window, 20% ABSD is refunded in full. If you miss the 6-month window, the ABSD is forfeited.

Stamp Duties: BSD, ABSD and Seller’s Stamp Duty

Stamp duties administered by IRAS are the biggest variable cost in any upgrading exercise. Three taxes are relevant.

Buyer’s Stamp Duty (BSD) is payable by the condo purchaser on a slab-rate schedule: 1% on the first S$180,000, 2% on the next S$180,000, 3% on the next S$640,000, 4% on the next S$500,000, 5% on the next S$1,500,000, and 6% on amounts above S$3,000,000. For a S$1,350,000 purchase, BSD works out to S$37,200.

Additional Buyer’s Stamp Duty (ABSD) is levied on the acquisition of private residential property. The 2026 ABSD rates, effective since 27 April 2023, are: SC buying 1st property — 0%; SC buying 2nd property — 20%; SC buying 3rd or subsequent — 30%. For PR buying 1st — 5%; 2nd — 30%. Foreigners — 65% (with limited exemptions for nationals of countries with FTA provisions). If you sell your HDB first, your condo purchase is your 1st private property and you pay 0% ABSD.

Seller’s Stamp Duty (SSD) does not apply to HDB flats (HDB imposes its own MOP rules instead). SSD applies to private residential properties sold within 3 years of acquisition: 12% in year 1, 8% in year 2, 4% in year 3. If you are buying a new launch condo off-plan, SSD starts running from the date you exercise the OTP, not the date of key collection.

Upgrader Stamp Duty Summary

| Scenario | BSD (S$1.35M condo) | ABSD | SSD | Total Duties |

|---|---|---|---|---|

| SC couple, sell HDB first (condo = 1st private) | S$37,200 | 0% | Nil (hold >3 yrs) | S$37,200 |

| SC couple, buy-first + remission (sell HDB within 6 mths) | S$37,200 | 20% → refunded | Nil | S$37,200 net |

| SC couple, buy-first — miss 6-mth window | S$37,200 | S$270,000 (20%) | Nil | S$307,200 |

| SC single, keep HDB + buy condo (2nd property) | S$37,200 | S$270,000 (20%) | Nil | S$307,200 |

| PR couple, sell HDB first (condo = 1st private) | S$37,200 | S$67,500 (5%) | Nil | S$104,700 |

| PR couple, buy-first (2nd property, 30%) | S$37,200 | S$405,000 | Nil | S$442,200 |

Worked Example: The Tan Family Upgrade

Mr and Mrs Tan are Singapore Citizens, joint owners of a 5-room HDB flat in Tampines purchased in January 2019 at S$620,000. Their combined gross monthly income is S$14,000. The flat is MOP-cleared in January 2024. In Q1 2026, they list the flat at S$820,000 and receive an offer.

Step 1 — Net proceeds from HDB sale. Outstanding HDB loan at point of sale: S$280,000. CPF drawn (principal + 2.5% p.a. accrued interest over 7 years): S$180,000 (principal) + S$33,600 (accrued interest) = S$213,600. Agent commission at 2%: S$16,400. Legal fees (seller): S$2,800. Net calculation: S$820,000 − S$280,000 (loan) − S$213,600 (CPF refund) − S$16,400 (agent) − S$2,800 (legal) = net cash S$307,200. The S$213,600 is returned to the Tans’ CPF OA and is available for reuse on the condo purchase.

Step 2 — Condo purchase. The Tans target a 3-bedroom OCR condo at S$1,450,000. BSD: S$40,600. Agent (buyer): S$14,500 (1%). Legal (purchaser): S$3,500. Total acquisition costs: S$58,600. CPF OA balance after HDB refund: S$213,600 + regular contributions ≈ S$230,000 available. Minimum cash down at LTV 75%: 5% = S$72,500 cash + 20% CPF/cash = S$290,000 combined. Total down payment: S$362,500. Of this, S$230,000 from CPF, S$132,500 from cash. Bank loan: S$1,087,500 at 3.0% for 30 years → monthly repayment S$4,584. TDSR: S$4,584 ÷ S$14,000 = 32.7% — well within the 55% cap.

Cash position check: Net cash from HDB sale S$307,200 less cash down S$132,500 less acquisition costs S$58,600 = surplus cash S$116,100. The Tans proceed comfortably.

CPF in the Upgrading Equation

CPF is both your biggest asset and the most misunderstood element of the upgrading calculation. When you sell your HDB, the Central Provident Fund Board (CPF Board) requires you to return to your CPF OA the full amount withdrawn — principal plus accrued interest at 2.5% per annum, compounded annually. This refund is mandatory regardless of whether you have an outstanding mortgage.

The good news: the money does not disappear. It goes back into your CPF OA, where it can immediately be reused for the private property purchase (BSD, initial down payment, or progressive payments on a new launch). The CPF Withdrawal Limits on private property are governed by the Valuation Limit (VL) and the Withdrawal Limit (WL): you can use CPF OA up to the VL (property market value or purchase price, whichever is lower) freely, and up to 120% of VL if the property’s remaining lease covers the youngest buyer to age 95.

Why Upgrading Still Makes Financial Sense in 2026

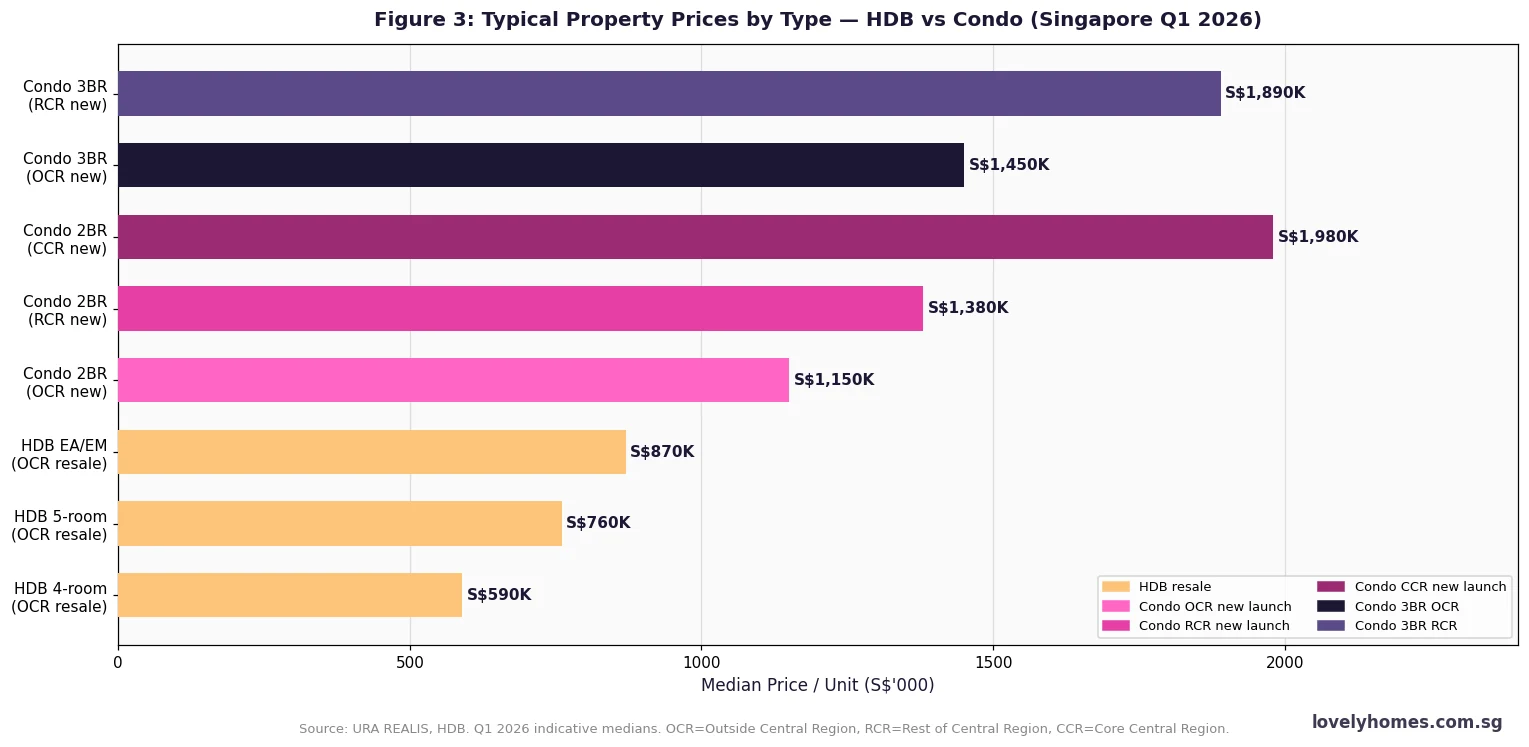

Three structural factors continue to make the HDB-to-private upgrade compelling. First, HDB resale prices have risen 41% since Q1 2019 (RPI 153.2 → 216.3 as of Q1 2026), materially increasing the equity pool available to upgraders. A household that bought a 4-room HDB in an OCR town for S$450,000 in 2018 may now realise S$620,000–S$680,000 on sale — generating S$150,000–S$200,000 in net equity above the original purchase price.

Second, OCR condo prices have appreciated 73% since Q1 2019, but entry-level 2-bedroom units in OCR developments remain accessible at S$1.0M–S$1.3M for resale or S$1.15M–S$1.4M for new launches. For a dual-income SC household earning S$12,000–S$16,000/mth, these price points sit comfortably within TDSR thresholds at current bank loan rates of approximately 3.0–3.5%.

Third, the absence of capital gains tax in Singapore means any appreciation in your private property value — whether you eventually sell, rent, or pass it on — accrues entirely to you. This structural advantage makes Singapore property one of the most tax-efficient long-term wealth vehicles available to residents.

What Might Come Next for Upgraders

This section reflects editorial analysis and is speculative in nature. The government has signalled a sustained commitment to housing supply: 19,600 BTO flats are scheduled for 2026, and the 2H 2026 GLS Confirmed List adds approximately 4,010 private residential units to pipeline supply. Greater supply should moderate new launch price growth, potentially improving affordability for upgraders who are not yet MOP-cleared. Conversely, a prolonged high-interest-rate environment (3M SORA at approximately 2.4% in mid-2026) raises mortgage servicing costs, and any reversal of ABSD policy is not anticipated — the 20% rate for a second residential property has been stable since April 2023 and serves a deliberate demand-management function.

Frequently Asked Questions

Can I buy a condo while still living in my HDB during the MOP?

No. During the MOP you cannot acquire any interest in a private residential property in Singapore or overseas. Doing so constitutes a breach of the HDB ownership conditions and may result in compulsory acquisition of the flat by HDB at below-market rates. You must wait until the MOP is fulfilled before exercising an OTP on any private property. For Plus and Prime flats (classified from October 2024 onwards), the MOP is 10 years.

What happens to my CPF when I sell my HDB?

All CPF monies withdrawn from your CPF Ordinary Account for the HDB purchase — including the down payment, progressive mortgage payments, and BSD — must be refunded to your CPF OA upon sale, together with accrued interest at 2.5% per annum compounded annually. This refund is deducted from the sale proceeds before you receive any cash. The refunded amount is then available in your OA for use on your next property purchase, subject to CPF Withdrawal Limits. It is not lost — it simply moves from property equity back into your CPF account.

Is the ABSD remission for buy-first upgraders automatic?

No. It must be applied for. After completing the HDB sale within the 6-month window, you must submit an ABSD remission application to IRAS within 6 months of the later of: (a) the date of purchase of the private property, or (b) the date of completion of the HDB disposal. IRAS will process the refund of the 20% ABSD (SC couple on 2nd property) back to you. If you miss the window or fail to apply, the ABSD is permanently forfeited. It is strongly advisable to appoint a conveyancing lawyer who tracks these timelines for you.

How does the TDSR affect how much I can borrow?

The Total Debt Servicing Ratio (TDSR), introduced by the Monetary Authority of Singapore (MAS) in June 2013, caps all debt obligations (mortgage + car loan + personal loans + credit card minimum payments) at 55% of verified gross monthly income. For a S$1.35M condo at 3.0% over 30 years, the monthly repayment is approximately S$5,690. To pass TDSR on this loan alone, a household needs gross income of at least S$10,345/mth (S$5,690 ÷ 55%). If you carry a car loan of S$1,200/mth, your required income rises to S$12,527/mth. Clear outstanding personal loans and credit card balances before applying for a bank loan to maximise your borrowing capacity.

Can I keep my HDB and buy a condo at the same time?

Yes, SC households may own one HDB and one private residential property simultaneously, provided the HDB MOP has been met. However, the condo purchase would be treated as a second property and attract 20% ABSD (SC rate) — approximately S$270,000 on a S$1.35M condo. Many owners with sufficient financial capacity choose this route to retain rental income from the HDB or for personal family use. Note that you cannot rent out the entire HDB flat during MOP; once MOP is cleared, HDB resale flat owners may apply to rent out the whole flat subject to HDB approval.

What is the difference between upgrading to a resale condo versus a new launch?

A resale condo can be occupied within 8–12 weeks of completion, eliminating the gap period. You pay the full purchase price in one tranche. A new launch (off-plan) typically takes 3–5 years to complete, during which you make progressive payments tied to construction milestones. This gives cash-flow breathing room — you do not need to fund the full purchase at once — but you carry developer and construction risk. New launches also attract a 12%/8%/4% SSD if sold within the first 3 years. Buyers purchasing at launch must ensure their financial position can sustain both any interim rental during the construction period and mortgage servicing once the loan disburses progressively.

Do ECs count as private property for ABSD purposes after privatisation?

Yes. Executive Condominiums (ECs) are considered HDB flats for the first 5 years (during MOP) and private property thereafter. After 10 years from the date of purchase, ECs are fully privatised and become indistinguishable from private condominiums for all regulatory purposes, including ABSD. If you are an EC owner past the 5-year MOP, you may buy a private property — but the EC’s privatisation status at 10 years means your EC becomes “private property held” from ABSD counting at that point. Seek legal advice on timing if you hold an EC and are planning to acquire additional private property.

Related Articles

- Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth

- Singapore Home Loan Guide 2026: HDB Loans, Bank Loans, TDSR and Best Rates

- Singapore HDB Resale Guide 2026: Complete Buyer’s and Seller’s Guide

- Singapore Property Selling Guide 2026: How to Sell Your HDB or Condo

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Stamp Duty Guide 2026: BSD, ABSD, SSD Explained

- CPF Property Withdrawal Limits Singapore 2026

- Condo vs HDB Singapore 2026: Which Is Right for You?

Disclaimer: This article is for general informational purposes only and does not constitute financial, legal, or property advice. ABSD rates, CPF rules, HDB policies, and bank lending criteria are subject to change. Always verify current rates with the Inland Revenue Authority of Singapore (IRAS) at iras.gov.sg, the Housing & Development Board (HDB) at hdb.gov.sg, the Central Provident Fund Board (CPF Board) at cpf.gov.sg, and the Monetary Authority of Singapore (MAS) at mas.gov.sg. Consult a licensed conveyancing lawyer and, where appropriate, a MAS-licensed financial adviser before making any property transaction.