HDB Subletting Singapore 2026: Complete Regulatory Guide to Rules, NCQ and Approval Process

📌 Quick Answer: HDB Subletting Singapore 2026

- MOP first: You must complete a 5-year Minimum Occupation Period (MOP) before subletting your whole HDB flat. For Plus and Prime flats, the MOP is 10 years.

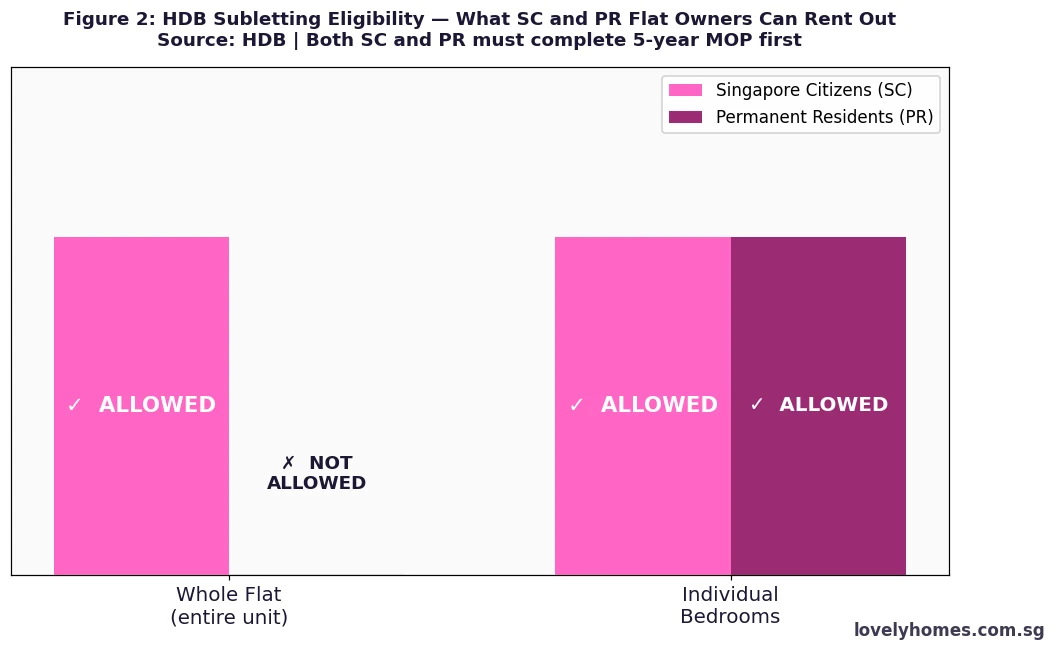

- SC only for whole flat: Only Singapore Citizens (SCs) may sublet the entire flat. Singapore Permanent Residents (SPRs) may only rent out individual bedrooms — and must continue living in the flat.

- HDB portal approval is mandatory: You must obtain written approval from HDB before the tenant moves in. Apply via SingPass at the HDB e-Services portal. Fee: S$20.

- Non-Citizen Quota (NCQ): If your tenant is a non-Malaysian non-citizen, your flat is subject to a quota of 8% (neighbourhood) and 11% (block). Malaysians are exempt.

- Subletting duration: Maximum 3 years per approved term for SG/Malaysian tenants; 2 years for other non-citizens. You must re-apply for each renewal.

- Income tax: All rental income is taxable. Deductible expenses include mortgage interest, property tax, maintenance fees, and the HDB S$20 subletting fee.

- Violation penalties: Subletting without approval or exceeding NCQ can result in fines up to S$5,000 and — in serious cases — compulsory flat acquisition by HDB.

Subletting your HDB flat is one of the most powerful financial options available to Singapore homeowners — but it is also one of the most regulated. The Housing & Development Board (HDB) administers a detailed set of rules under the Housing and Development Act (Cap 129) that govern who can sublet, to whom, for how long, and under what conditions.

This guide explains the regulatory framework for HDB subletting in 2026, from the Minimum Occupation Period (MOP) and the Non-Citizen Quota (NCQ) to the portal approval process, income tax obligations, and penalty regime. It complements our HDB Rental Landlord Guide 2026, which covers the practical experience of finding and managing tenants.

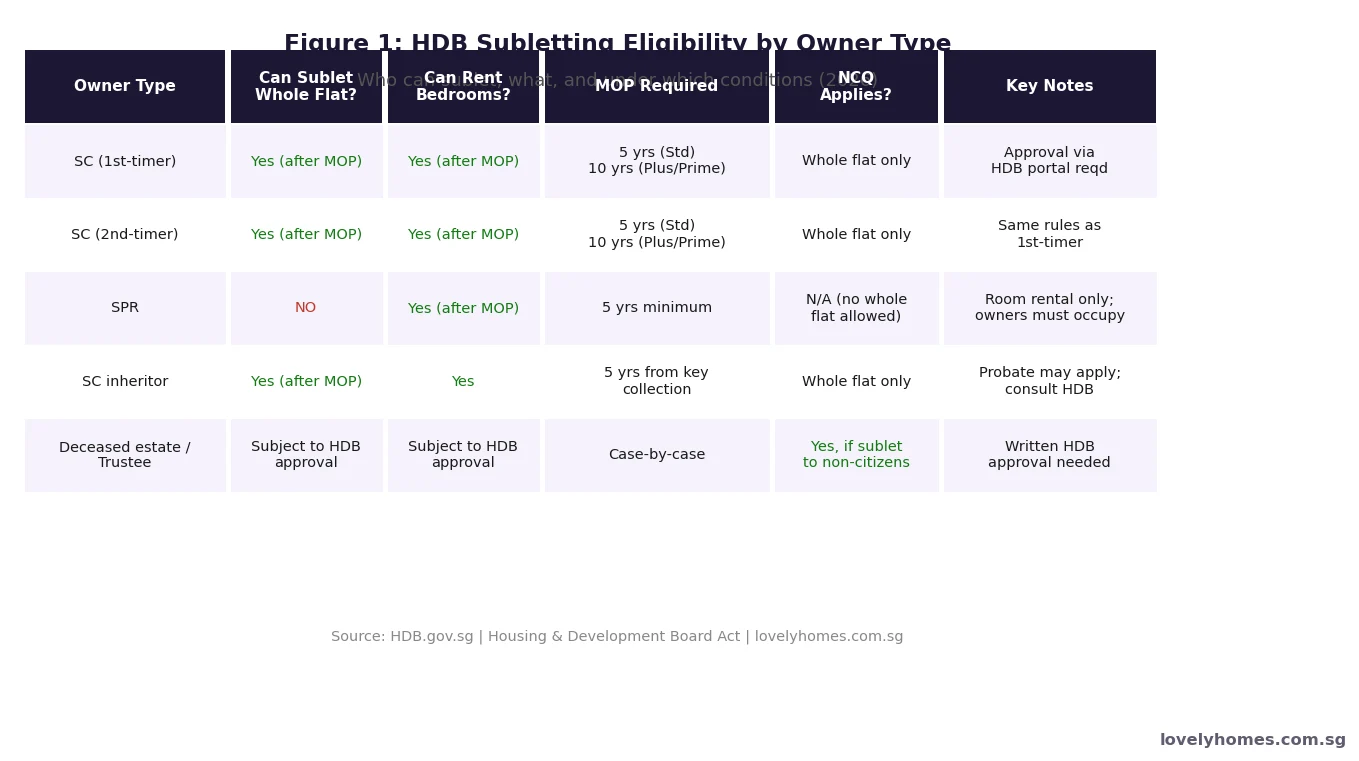

Who Can Sublet an HDB Flat — and What?

HDB imposes a strict eligibility framework based on your citizenship status and how long you have owned the flat.

Singapore Citizens (SCs)

SC flat owners who have completed the MOP may sublet the entire flat or rent out individual bedrooms. When subletting the whole flat, HDB portal approval is required before the tenant moves in. When renting out bedrooms, no formal approval is needed — but you must continue to live in the flat, and you must notify HDB within 7 days of any new tenant commencing occupancy.

Singapore Permanent Residents (SPRs)

SPRs may not sublet the whole flat at any time. This rule has been in place since January 2003 and reflects the policy intent that SPRs should personally occupy their subsidised flat. SPRs may, however, rent out individual bedrooms after the MOP — provided the SPR owner continues to reside in the flat. The Non-Citizen Quota does not apply to bedroom rental (see below).

MOP: The First Gatekeeper

The Minimum Occupation Period is the most fundamental restriction. For Standard and Plus flats, the MOP is 5 years from the date of key collection (not from application date or booking date). For Prime flats (under the PLH Model, including flats in Bishan, Bukit Merah, Toa Payoh, and other central locations), the MOP is 10 years. During the MOP, neither whole-flat subletting nor room rental is permitted. Owners who violate this rule face the possibility of compulsory flat acquisition at below-market value.

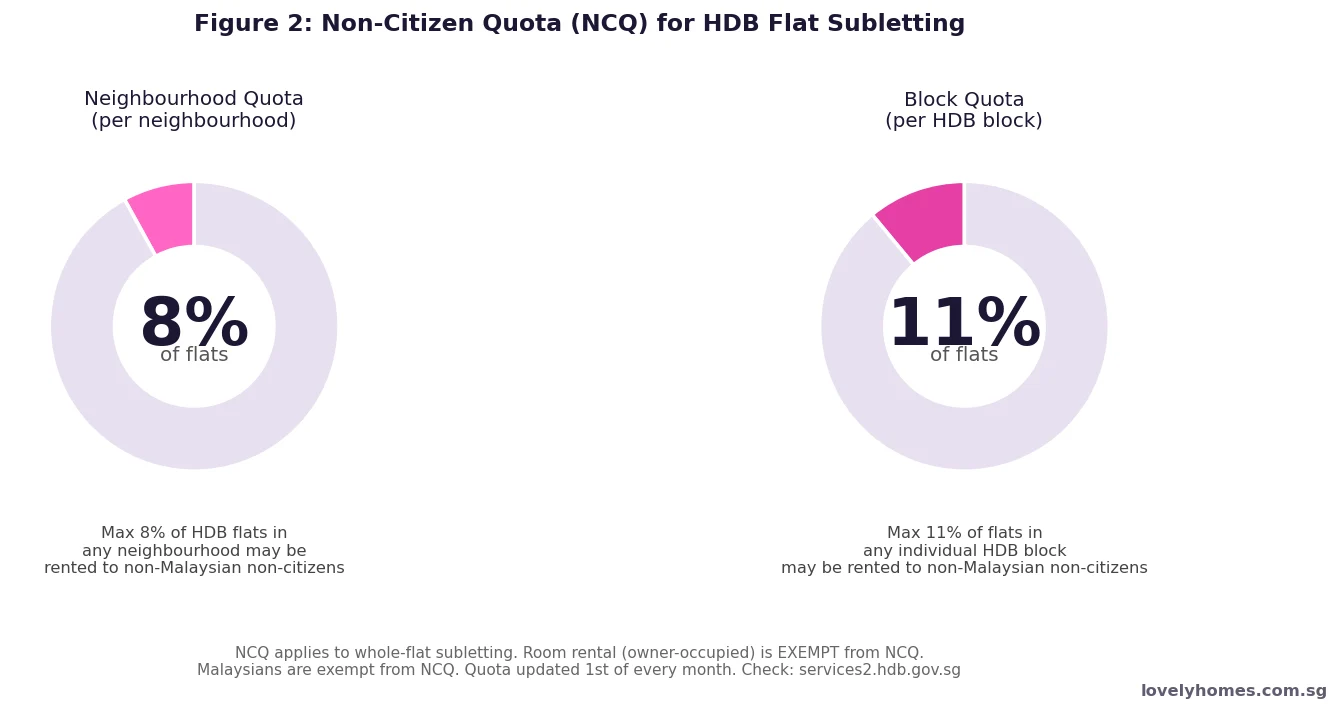

The Non-Citizen Quota (NCQ)

Introduced on 16 January 2014 to prevent the formation of foreigner enclaves in HDB estates, the NCQ applies whenever a SC owner sublets the whole flat to one or more non-Malaysian non-citizen tenants.

How the NCQ Works

The Non-Citizen Quota operates at two levels. At the neighbourhood level, no more than 8% of HDB flats may be sublet (whole flat) to non-Malaysian non-citizen tenants. At the block level, the cap is 11%. HDB updates the quota availability on the first day of every month. If your block or neighbourhood has already reached the cap, you can still sublet — but only to Singapore Citizens, SPRs, or Malaysians.

Who is Exempt from NCQ?

Malaysian nationals are explicitly exempt from the NCQ, reflecting Singapore’s historical and social ties with Malaysia. Room rental (where the owner continues to reside in the flat) is also exempt regardless of the tenant’s nationality — the rationale being that the owner’s continued presence moderates the risk of foreigner concentration. The NCQ does not apply to private residential property.

Checking Your NCQ Status

Before committing to a non-Malaysian non-citizen tenant, check the NCQ status at services2.hdb.gov.sg/webapp/BR12AWNCQuota/. Enter your block and street name. If the quota is exhausted at either neighbourhood or block level, you cannot proceed with a non-Malaysian non-citizen tenant until the quota resets (typically when another flat in the quota pool transitions back to a citizen household).

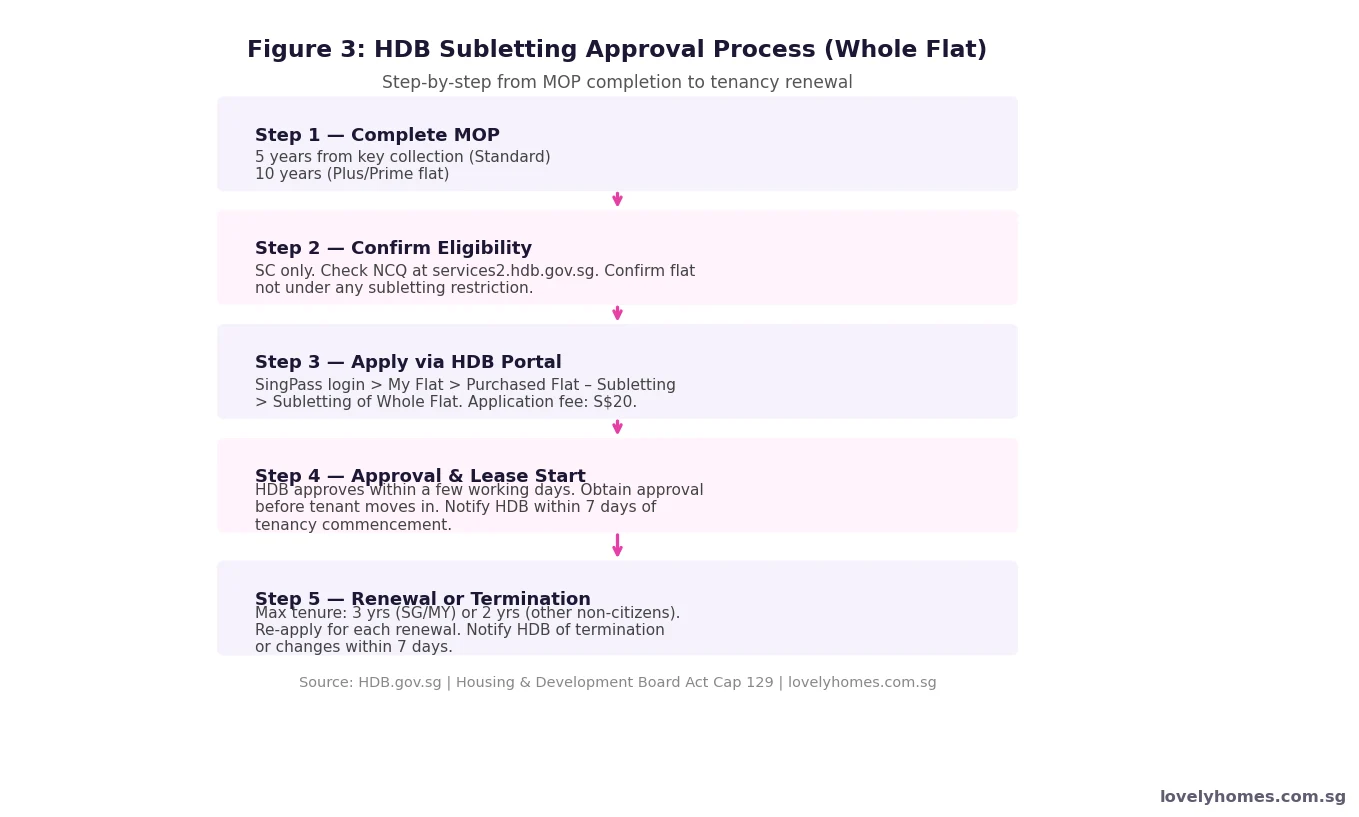

The HDB Subletting Approval Process

The approval process for whole-flat subletting is fully digital and administered through HDB’s e-Services portal. Bedroom rental operates under a lighter-touch notification regime.

Whole-Flat Subletting: Step-by-Step

After completing the MOP and confirming NCQ eligibility, the owner logs in to the HDB portal via SingPass and navigates to My Flat > Purchased Flat – Subletting > Subletting of Whole Flat. The application requires the proposed tenant’s particulars (NRIC/FIN), intended tenancy start and end dates, and rental amount. The application fee is S$20, payable online. HDB typically approves within a few working days. The tenant must not move in before approval is received. Once approved, the owner must notify HDB within 7 days of the tenancy commencement date.

Bedroom Rental: Notification Only

Renting out individual bedrooms — where the owner continues to reside in the flat — does not require prior HDB approval. However, the owner must still register the tenant with HDB via the portal and is responsible for ensuring the flat’s total occupancy does not exceed the permitted cap. As at 2026, the occupancy cap is relaxed to 8 persons per flat (extended until 31 December 2026 under a temporary government measure; previously 6 persons).

Subletting Duration and Renewal

Approval for whole-flat subletting is granted for a fixed term, capped at:

| Tenant Nationality | Maximum Approved Term | Renewal |

|---|---|---|

| Singapore Citizens | 3 years per term | Re-apply at end of each term |

| Malaysian nationals | 3 years per term | Re-apply at end of each term |

| Other SPRs | 2 years per term (subject to NCQ) | Re-apply; NCQ checked at renewal |

| Non-resident foreigners (Work Pass, EP, etc.) | 2 years per term (subject to NCQ) | Re-apply; NCQ checked at renewal |

| Tourism/Short-Stay visitors | NOT PERMITTED (min 6 months) | N/A — illegal under URA rules |

There is no limit on the number of consecutive renewals, provided eligibility requirements (MOP, NCQ, owner criteria) are met at the time of each renewal application. Owners must also notify HDB within 7 days of any early termination, change of tenant, or change in the number of occupants.

Income Tax on Rental Income

All rental income from HDB subletting is subject to Singapore income tax under the Income Tax Act (Cap 134). Rental income must be declared in your annual income tax return. The net rent (gross rent minus allowable deductions) is added to your total assessable income and taxed at the applicable progressive personal income tax rate.

Allowable Deductions Against Rental Income

IRAS permits the following as deductible expenses against HDB rental income: mortgage interest (the interest component only, not principal repayment); property tax (the annual property tax liability, not stamp duty); maintenance and conservancy charges (S&CC/management fees paid to HDB); cost of repairs and maintenance directly related to the rental; insurance premiums for the property; and the HDB S$20 subletting application fee. Furniture and fittings are not deductible as capital expenditure, though rental of furnished rooms may allow partial deduction under IRAS practice guidelines. Pre-letting expenses (advertising, agent fees) are generally deductible if the property is subsequently let.

| Item | Deductible? | Notes |

|---|---|---|

| Mortgage interest | Yes | Interest component only; principal is not deductible |

| Property tax | Yes | Annual property tax, not BSD/ABSD |

| S&CC (conservancy charges) | Yes | Monthly HDB town council charges |

| Repairs and maintenance | Yes | Must be directly related to rental unit |

| HDB subletting application fee | Yes | S$20 per application |

| Property agent commission | Yes | Where incurred to secure rental |

| Furniture / fittings | Generally No | Capital expenditure; check IRAS guidelines |

| Mortgage principal | No | Capital repayment, not an expense |

Worked Example: Calculating Net Rental Income

Mr and Mrs Tan are SC joint owners of a 4-room HDB flat in Tampines. They collected keys in April 2019, completing their 5-year MOP in April 2024. In January 2025, they moved to their new condo and applied to sublet the whole HDB flat. In February 2025, they secured a Malaysian couple as tenants at S$3,200 per month on a 2-year lease.

Gross rental income (12 months): S$3,200 × 12 = S$38,400

Less deductions:

Mortgage interest component (~S$4,800 p.a.): −S$4,800

Property tax (owner-occupier rate does not apply once sublet; AV ~S$18,000, 10% = S$1,800): −S$1,800

S&CC town council charges (~S$70/mth × 12): −S$840

HDB subletting application fee: −S$20

Agent commission (half month): −S$1,600

Net assessable rental income: S$38,400 − S$9,060 = S$29,340

This is added to their other income for YA 2026 tax assessment. At the 7% personal income tax rate (income band), the additional tax payable is approximately S$2,054 per joint owner — a manageable cost relative to the gross S$38,400 rental earned.

Note: As Malaysians, the tenants are exempt from NCQ, so the block and neighbourhood quota check was not a constraint for this tenancy.

Violations: Penalties and Enforcement

HDB takes unauthorised subletting seriously. The Housing and Development Act empowers HDB to take action against flat owners who violate subletting rules. The penalty regime in 2026 is as follows.

For subletting without HDB approval, or subletting to ineligible occupants, owners face a fine of up to S$5,000 per offence. For repeat or serious violations — particularly renting to short-stay tourists, platforms such as Airbnb (which facilitates short-term stays of less than 3 months, prohibited under URA rules), or falsifying tenant particulars — HDB may proceed to compulsorily acquire the flat at below-market value. The owner loses all equity above the acquisition price and is barred from purchasing another HDB flat for a period. As at 2026, IRAS has also announced enhanced data-sharing with HDB to identify undeclared rental income.

Why This Matters: Subletting as a Financial Strategy

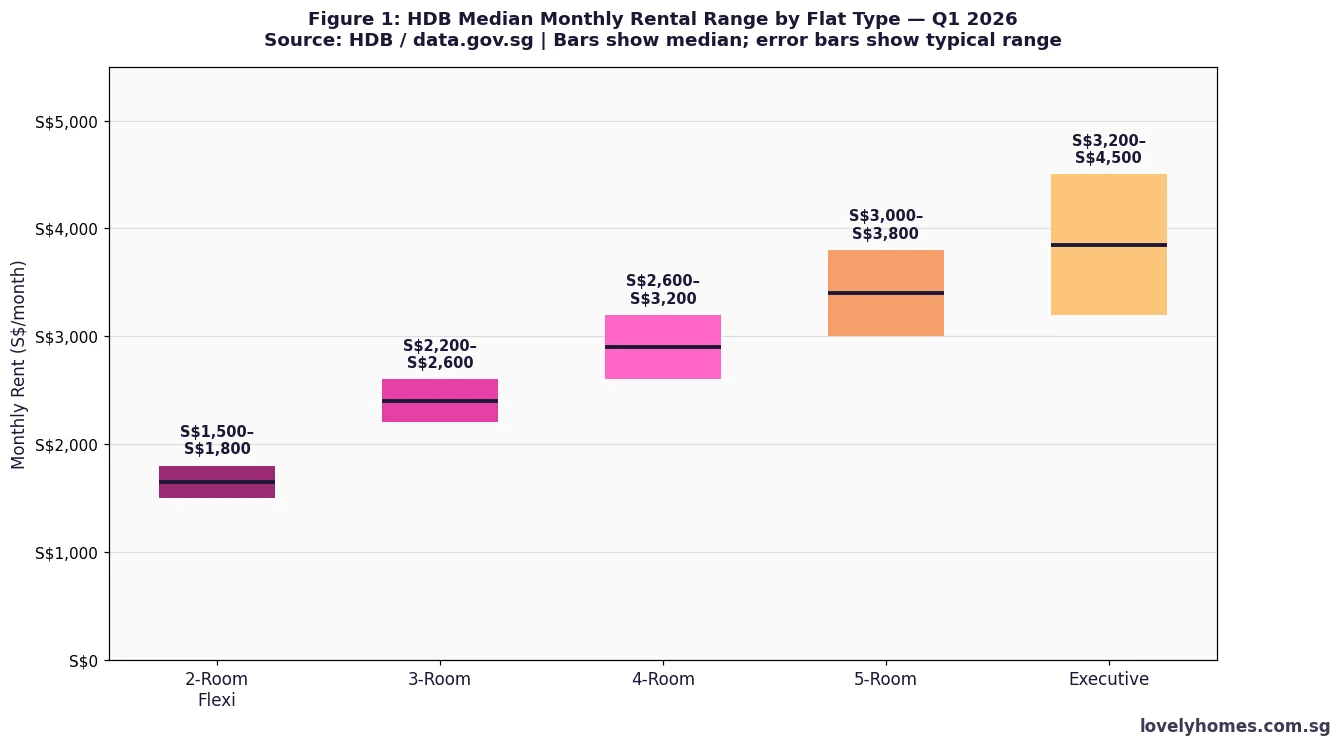

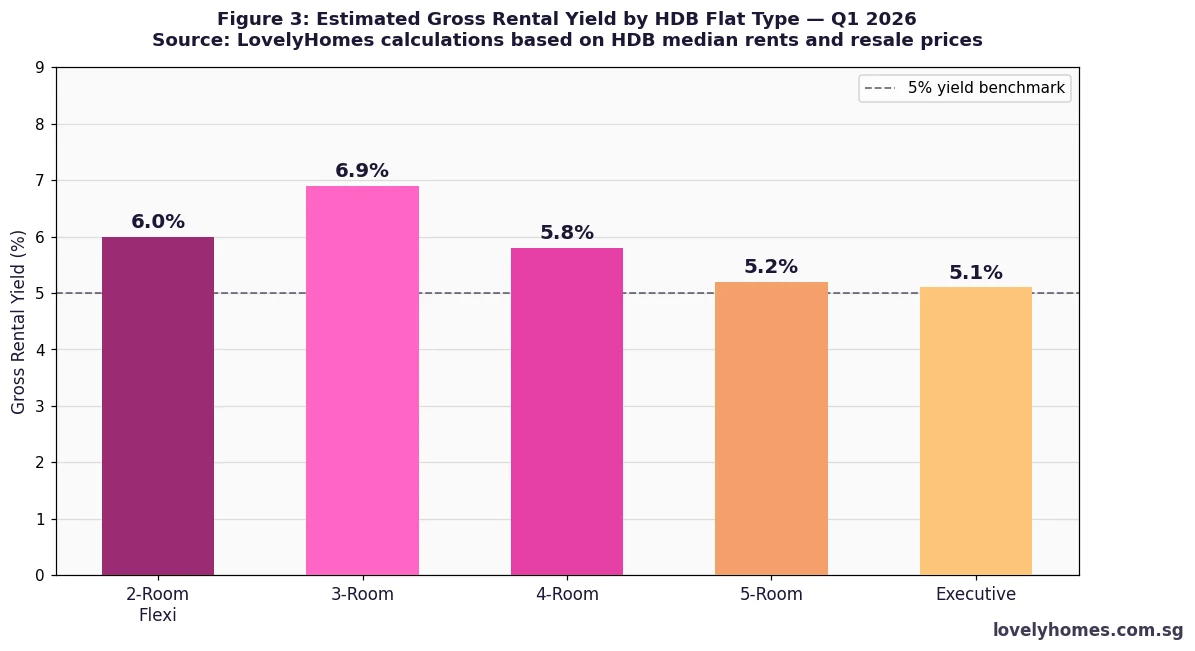

For HDB owners who have completed the MOP and moved to private property, subletting transforms a public housing asset into a yield-bearing investment. As at Q1 2026, HDB median rental yields sit at approximately 5.1–5.9% gross across flat types (see our Singapore Rental Market Guide 2026). At S$3,000–S$3,500 per month for a typical 4-room flat, the gross annual return of S$36,000–S$42,000 on a flat worth S$450,000–S$550,000 is materially better than most other asset classes available to retail investors in Singapore.

However, the regulatory framework means that subletting is only accessible to SC owners after MOP. SPRs are permanently limited to room rental — a significant constraint that affects SPRs’ ability to monetise their HDB assets. This distinction underlies much of the debate about SPR property rights in Singapore.

What Might Come Next

Based on policy trends and parliamentary discussions in 2025–2026, a few developments are worth watching. First, the temporary 8-person occupancy cap relaxation (extended to 31 December 2026) may be made permanent if government data shows no adverse outcomes. Second, HDB has indicated ongoing review of whether the Plus flat MOP of 10 years is calibrated correctly — earlier parliamentary questions have probed whether the 10-year rule unduly restricts owners’ flexibility. Third, with IRAS cross-referencing rental data more actively, there may be more enforcement actions on undeclared HDB rental income in YA 2027 tax filings. Flat owners who have been subletting informally should consider voluntary disclosure before enforcement activity increases.

Frequently Asked Questions

Can I start renting out my HDB flat before the MOP ends if I get a job overseas?

I am an SPR — can I ever sublet my whole HDB flat?

What happens if my block has reached the NCQ limit — can I still rent to a non-citizen?

I rented out my HDB flat but did not declare the income on my tax return. What should I do?

Can I use Airbnb or short-term rental platforms to rent out my HDB flat?

If my tenant damages the flat, is there any HDB recourse?

What is the minimum tenancy period for renting an HDB flat?

Related Articles

Click anywhere outside to close