Singapore Rental Market Guide 2026: HDB and Condo Rents, Yields and Outlook Explained

- Singapore’s private residential rental index rose 0.3% in Q1 2026 (URA), recovering from a 0.5% dip in Q4 2025, but remains below the 2023 peak.

- HDB rental index eased 0.1% in Q1 2026, continuing a gradual softening from the 2023 high after two years of elevated rents.

- Median rents in Q1 2026: HDB 4-room S$2,600/mth, condominium 2-bedroom S$3,600/mth (OCR), condominium 3-bedroom S$5,200/mth.

- Gross rental yields remain attractive for HDB (4.7–5.6%) compared with private condominiums in Core Central Region (CCR) (2.6%).

- Rising supply from 2024–2025 completions is the dominant dampener; landlords must price competitively in 2026.

- Demand drivers: foreign professional workforce (Employment Pass/S Pass holders), expat families on education visas, and domestic upgraders waiting for new homes to complete.

- Short-term rentals (fewer than 3 months) remain prohibited for residential properties in Singapore under URA regulations.

- Landlords must declare rental income on their annual income tax returns to IRAS; allowable deductions include mortgage interest, property tax, and maintenance fees.

Understanding Singapore’s Rental Market

Singapore’s residential rental market is one of Asia’s most closely watched — shaped by a unique interplay of government-controlled HDB supply, private condominium completions, immigration policy, and one of the highest proportions of home ownership in the world (approximately 89%). Unlike many global cities, Singapore’s rental sector is comparatively small: most residents own their HDB flats. The rental pool is disproportionately driven by the expatriate workforce and a domestic segment of upgraders temporarily between properties.

The Urban Redevelopment Authority (URA) tracks the Private Residential Rental Index quarterly; HDB separately tracks the HDB Rental Index. Both indices are released alongside quarterly real estate statistics — the primary authoritative source for rental market data. The Q1 2026 URA statistics confirmed that private rental growth has moderated after the exceptional surge of 2021–2023, when the market rose over 50% from its COVID-era trough on the back of a supply drought and surging foreign workforce arrivals.

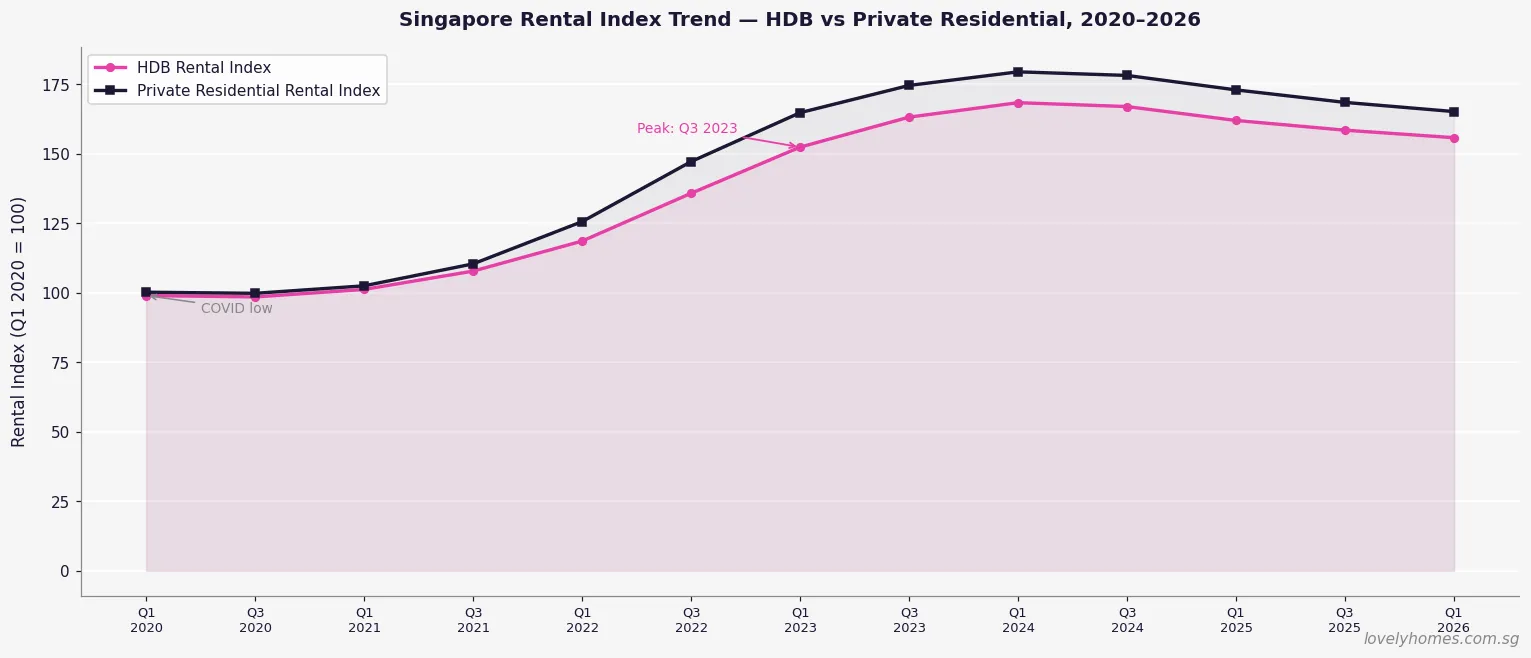

Rental Index Trend: 2020–2026

The rental cycle of this decade is one of the most dramatic in Singapore’s property history. From a base of approximately 100 in early 2020, the HDB Rental Index rose to a peak of approximately 163 by mid-2023 before softening. Private residential rents peaked near 175 in mid-2023. As at Q1 2026, both indices have retreated — the HDB index to approximately 156, the private residential index to approximately 165 — representing a correction of roughly 4–6% from peak.

The correction has been driven primarily by supply normalisation — a wave of private condominium completions in 2024–2025 (including several large integrated developments) added significant rental stock to the market, while post-COVID foreign workforce growth moderated as global companies trimmed headcount in 2024–2025. Nevertheless, rents remain approximately 55% higher in absolute terms than pre-COVID levels for most property types.

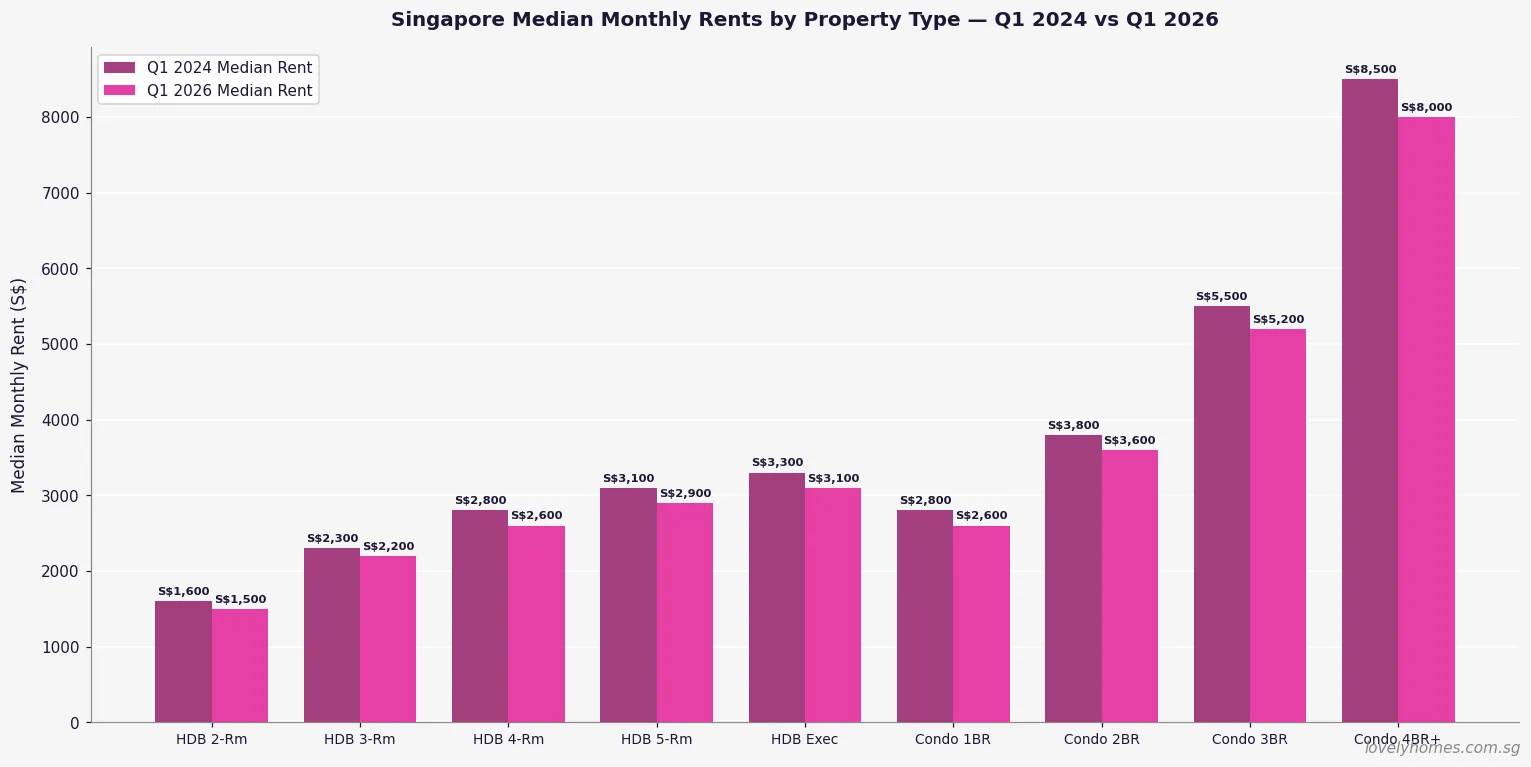

Median Monthly Rents by Property Type, Q1 2026

Industry figures from Q1 2026 show median monthly rents across property types as follows. HDB room types continue to offer the most accessible entry point for tenants, while Core Central Region (CCR) condominiums command a substantial premium reflecting proximity to the CBD and top international schools.

Key observations from the Q1 2026 data: HDB 3-room rents have eased from approximately S$2,300/mth in Q1 2024 to approximately S$2,200/mth, a modest 4.3% decline. Private condominium 3-bedroom rents have softened more noticeably from approximately S$5,500/mth to S$5,200/mth (−5.5%). Executive flat rents remain relatively sticky at approximately S$3,100/mth, reflecting persistently high demand from larger families displaced from the HDB resale market by the 15-month wait.

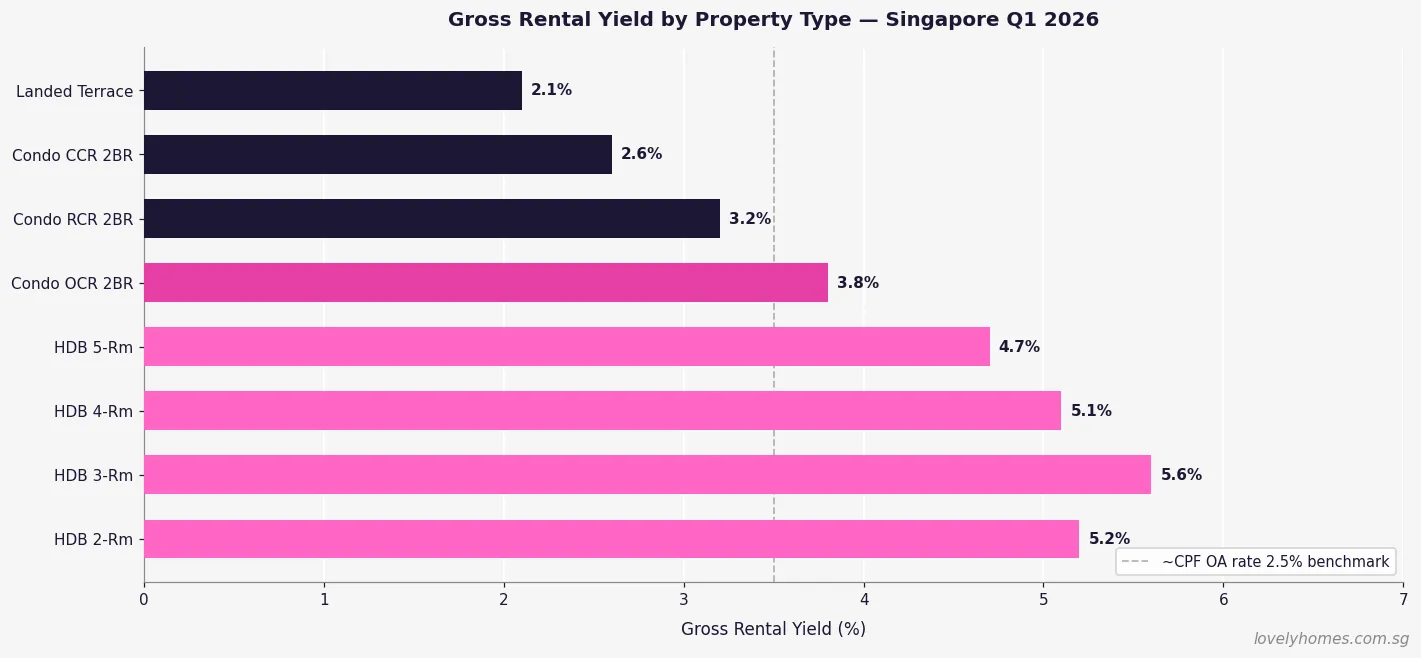

Gross Rental Yields by Property Type

Gross rental yield is calculated as annual rent divided by market value. In Singapore’s context, it is an imperfect but useful comparator — particularly when set against the CPF Ordinary Account rate of 2.5% p.a. and typical bank mortgage rates of 3.0–3.7% p.a. in 2026. Properties yielding below the mortgage rate require careful cash flow modelling; properties yielding above 4.5% can generate positive carry even at current financing costs.

HDB flats deliver the highest gross yields precisely because their prices are regulated and their transacted values remain significantly below equivalent private condominiums. A well-located 3-room HDB in Toa Payoh with a transacted rent of S$2,200/mth and a resale value of approximately S$470,000 generates a gross yield of approximately 5.6% — among the highest in Singapore’s residential market. However, HDB landlords face non-citizen quota constraints (8% or 11% per block/neighbourhood) and must comply with the Minimum Occupation Period (MOP) rules and HDB approval requirements. See our comprehensive HDB Rental Guide 2026 for full details.

Landlord Obligations and Legal Framework

Residential tenancies in Singapore are governed primarily by contract law — there is no Residential Tenancies Act equivalent to those in the United Kingdom or Australia. The standard Tenancy Agreement is a contractual document prepared by either party’s lawyer or the property agent. Key regulatory requirements for landlords include:

- Stamp duty on tenancy agreements: The tenant is liable to pay stamp duty on the tenancy agreement via IRAS e-Stamping. The rate is 0.4% of the total rent for leases of 1–4 years; for leases exceeding 4 years, the rate is 4% of the average annual rent. In practice, landlords should confirm the stamp duty is paid within 14 days of signing, as IRAS treats it as a condition for the agreement to be legally admissible in court.

- Short-term rental prohibition: URA regulations prohibit the use of private residential properties for accommodation for periods of fewer than 3 consecutive months. Platforms such as Airbnb, Agoda (short-stay listings), and similar are prohibited for residential properties. Violations carry fines of up to S$200,000 per offence.

- HDB subletting rules: HDB flat owners who have completed their Minimum Occupation Period (MOP) may sublet their whole flat or individual bedrooms, subject to HDB approval, non-citizen quota compliance, and the maximum occupancy limits (8 persons per flat until 31 December 2026 under the current temporary relaxation).

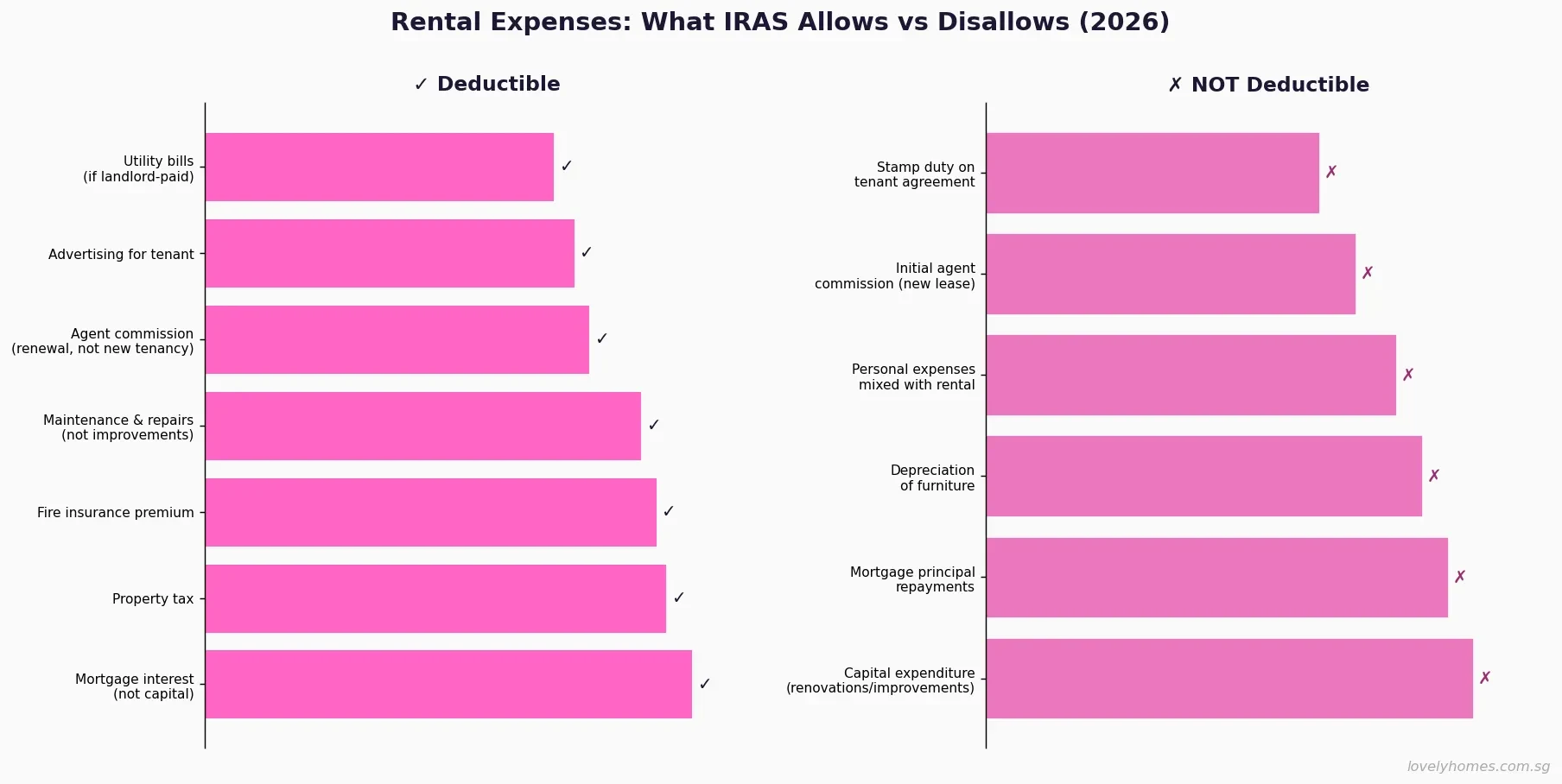

- Property tax: Landlords pay property tax at non-owner-occupier rates (typically 10–20% of the Annual Value for private properties, 10% for HDB), which is a deductible expense against rental income.

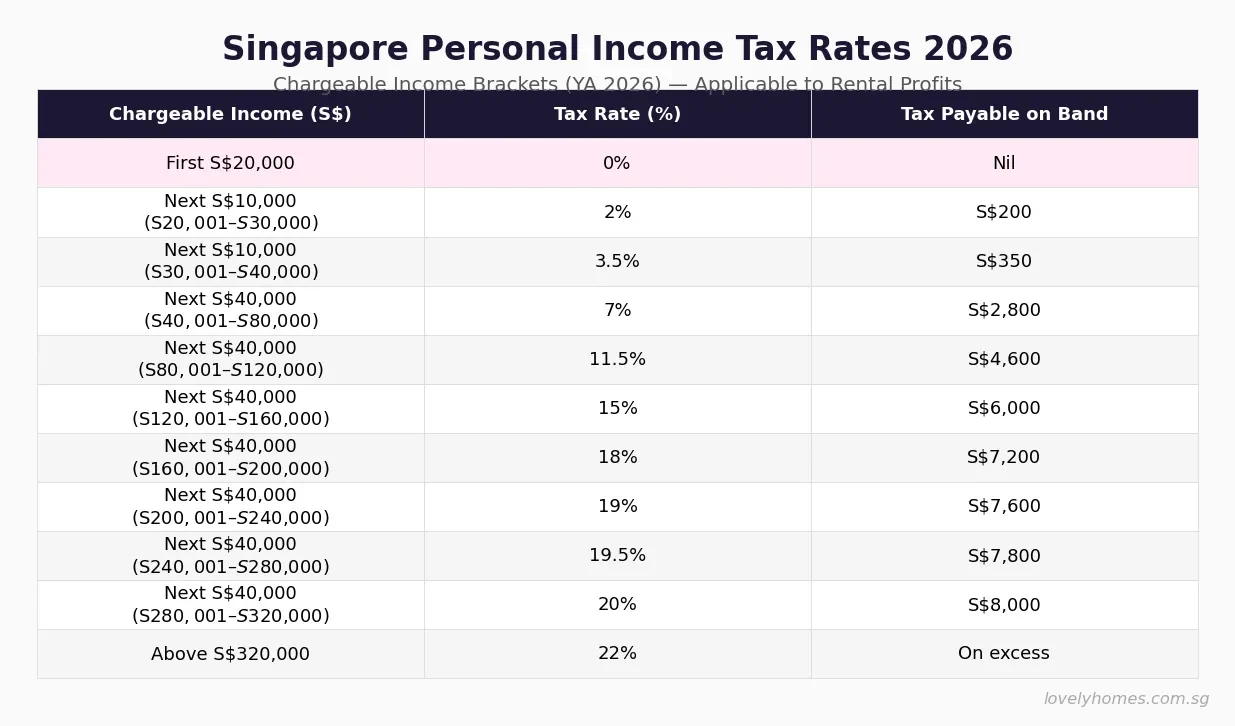

- Rental income tax: Rental income is taxable as personal income in Singapore. Allowable deductions include mortgage interest, property tax, fire insurance premiums, maintenance fees, and depreciation of approved furniture at 20% per annum declining balance.

Summary: Singapore Rental Market at a Glance, 2026

| Property Type | Typical Monthly Rent | Gross Yield | Key Tenant Profile |

|---|---|---|---|

| HDB 2-room | S$1,400–S$1,600 | ~5.2% | Singles, young couples |

| HDB 3-room | S$2,000–S$2,400 | ~5.6% | Small families, couples |

| HDB 4-room | S$2,400–S$2,800 | ~5.1% | Families, expat workers |

| HDB 5-room | S$2,600–S$3,200 | ~4.7% | Families, management expats |

| Condo 1-bedroom (OCR) | S$2,400–S$2,800 | ~3.8% | Young professionals |

| Condo 2-bedroom (OCR) | S$3,200–S$4,000 | ~3.8% | Couples, small families |

| Condo 2-bedroom (CCR) | S$4,500–S$6,500 | ~2.6% | Senior expat executives |

| Landed Terrace | S$6,000–S$10,000 | ~2.1% | High-net-worth families |

Worked Example: Mr Rajan Buys a 3-Room HDB to Rent Out in Ang Mo Kio

Mr Rajan, a Singapore Citizen, purchased a 3-room HDB resale flat in Ang Mo Kio in August 2021 for S$450,000. His MOP completed in August 2026 and he immediately lists it for whole-flat rental while upgrading to a condominium. Key figures:

- Purchase price: S$450,000 in August 2021.

- MOP completion: August 2026 (5 years from key collection).

- Estimated market rent (Q1 2026): S$2,100–S$2,300/mth for a well-maintained 3-room in Ang Mo Kio.

- Monthly gross income: S$2,200/mth (midpoint).

- Annual gross rent: S$26,400.

- Gross yield: S$26,400 / S$450,000 = 5.9% (calculated on original purchase price; current AV-based valuation ~S$480,000 gives ~5.5%).

- Property tax (non-owner-occupier): Annual Value approximately S$24,000; property tax approximately S$2,400/yr at 10%.

- Mortgage interest (if outstanding loan S$150,000 at 2.6%): ~S$3,900/yr (deductible).

- Net rental income (estimated): S$26,400 − S$2,400 (property tax) − S$3,900 (interest) − S$1,200 (maintenance, insurance) = approximately S$18,900/yr, taxable at Mr Rajan’s personal income rate.

- Stamp duty on 12-month tenancy at S$2,200/mth: 0.4% × S$26,400 = S$105.60 (tenant’s liability but landlords confirm this is paid).

The non-citizen quota check (8% neighbourhood / 11% block) must be confirmed with HDB before signing the Tenancy Agreement. HDB approval is required for whole-flat rental; approval is typically granted within 3–5 business days via the HDB Resale Portal.

What Might Come Next for Singapore Rents

The 2026 rental market is characterised by a bifurcation: HDB rents are gradually softening as more MOP flats come onto the rental market and demand moderates, while premium private rents in the CCR are proving stickier, supported by a resilient pool of senior expatriate tenants who cannot or will not rent HDB. The key upside risk to the softening thesis is a reversal in Singapore’s technology and financial services hiring cycle — any rebound in Employment Pass issuances (which fell in 2024–2025 under tighter Fair Consideration Framework scrutiny) would tighten rental supply rapidly given the low vacancy rates in well-located projects. The key downside risk is continued elevated completions through 2026–2027 from the record launch years of 2021–2022, which will maintain supply pressure on mid-market condominiums.

For investors evaluating rental yield against price appreciation potential, the OCR condominium segment offers the most balanced risk-reward in 2026: gross yields of approximately 3.5–4.0% are competitive with bank deposit rates after factoring in leverage, while capital value upside from Jurong Lake District and Cross Island Line catalysts provides a medium-term appreciation thesis. See our Singapore Property Investment Guide 2026 for a full cross-asset comparison.

Frequently Asked Questions

Are Singapore rents going up or down in 2026?

Singapore’s rental market is in a gradual softening phase in 2026. According to URA Q1 2026 data, the private residential rental index rose 0.3% quarter-on-quarter — a marginal recovery after a 0.5% dip in Q4 2025 — but remains below the 2023 peak. HDB rents eased 0.1% in Q1 2026. The dominant factors are increased supply from 2024–2025 completions and moderating foreign workforce demand. Most market observers expect rents to remain broadly flat to slightly lower through 2026, with premium CCR properties proving more resilient than mass-market OCR condominiums and HDB flats.

Can I Airbnb my Singapore condo or HDB flat?

No. URA regulations prohibit the use of private residential properties for short-term accommodation of fewer than 3 consecutive months. This applies equally to condominiums, landed properties, and HDB flats. Listing a Singapore residential property on Airbnb, Agoda short-stay, or similar platforms is a regulatory offence carrying fines of up to S$200,000 per offence. HDB additionally prohibits subletting to short-term visitors regardless of platform. The minimum tenancy period for all residential properties in Singapore is 3 months.

Do I need to declare rental income to IRAS?

Yes. Rental income is taxable as personal income in Singapore and must be declared on your annual Income Tax return. IRAS requires landlords to report gross rent received, then deduct allowable expenses: mortgage interest (on the loan for the rented property), property tax paid, fire insurance premiums, cost of maintenance and repairs (but not capital improvements), management fees, and furniture depreciation at 20% per annum declining balance on approved items. Failure to declare rental income attracts penalties of up to 200% of the tax undercharged. See IRAS’s guide at iras.gov.sg for the current rental income declaration checklist.

What is the non-citizen quota for HDB rentals?

HDB imposes a Non-Citizen Quota (NCQ) to preserve the social mix of HDB estates. The quota limits the proportion of HDB flats in each block and neighbourhood that may be rented to non-Malaysia foreigners (i.e., all non-citizens who are not Malaysian citizens). The limits are 8% at the neighbourhood level and 11% at the block level. If either quota has been met, the landlord cannot rent to a non-Malaysian foreigner regardless of HDB approval status. Malaysia citizens are exempt from the NCQ. Singapore PRs count as citizens for NCQ purposes. Always check the NCQ status on the HDB website before signing any Tenancy Agreement with a foreign tenant.

What is a diplomatic clause in a tenancy agreement?

A diplomatic clause (or Diplomatic Break Clause) is a contractual provision that allows the tenant to terminate the tenancy early if they are relocated or transferred out of Singapore by their employer — typically with 2 months’ written notice after the first year of the lease. It is commonly requested by expatriate tenants and their employers. Landlords generally accept diplomatic clauses for premium properties where the tenant pool is predominantly expatriate. The clause should specify the minimum tenancy period before it can be activated (typically 12 months), the notice period, and whether any penalty or notice fee applies. If the tenant exercises the clause, they forgo the security deposit for the unused period — the exact mechanism is a matter of negotiation.

How is stamp duty on a tenancy agreement calculated?

Stamp duty on a Tenancy Agreement is calculated under the Stamp Duties Act (Cap. 312). For a lease of 1–4 years, the duty is 0.4% of the total rent payable over the tenancy period. For a lease exceeding 4 years, the duty is 4% of the average annual rent. Example: a 12-month lease at S$3,500/mth = total rent S$42,000; stamp duty = 0.4% × S$42,000 = S$168. Payment is due within 14 days of signing via the IRAS e-Stamping portal. The stamp duty is the tenant’s liability by default, but the Tenancy Agreement may specify otherwise. An unstamped tenancy agreement is inadmissible as evidence in court, though the tenancy itself remains contractually enforceable as between the parties.

What is a typical security deposit for a Singapore rental?

The market convention in Singapore is one month’s rent as security deposit for every year of tenancy — so a 1-year lease typically requires a 1-month deposit, and a 2-year lease requires a 2-month deposit. For leases with a diplomatic clause, landlords sometimes negotiate a 2-month deposit for a 1-year lease as additional security against early termination. There is no statutory cap on the security deposit amount in Singapore — it is entirely a matter of negotiation. The deposit should be held in a separate client account by the agent or returned directly to the landlord, and must be refunded within 14 days after the end of the tenancy (less any deductions for damage or unpaid rent, supported by receipts and a condition report).

Related Articles

- Renting Out Your HDB Flat 2026: Rules, Quotas and Step-by-Step Landlord Guide

- Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth Through Property

- Singapore HDB Resale Guide 2026: Complete Guide to Buying and Selling HDB Resale Flats

- Singapore Home Loan Complete Guide 2026: HDB Loans, Bank Loans, TDSR and MSR

- Singapore Seller’s Stamp Duty (SSD) 2026: New 4-Year Holding Period and Rates Explained

- Jurong East Neighbourhood Guide 2026: Property Prices, JLD Uplift and Investment Outlook

- Singapore Property Investment Guide 2026: How to Build Wealth Through Property