Singapore Seller’s Stamp Duty (SSD) Guide 2026: Rates, Calculations and When It Applies

Seller’s Stamp Duty (SSD) is Singapore’s principal tool for discouraging short-term property speculation. Introduced in 2010 and tightened several times since, SSD imposes a tax on sellers who dispose of their residential property within three years of purchase. It is distinct from the Buyer’s Stamp Duty (BSD) paid at purchase and the Additional Buyer’s Stamp Duty (ABSD) — SSD applies solely to the sale side of the transaction and targets holding-period behaviour. For any property investor or owner considering a sale, understanding SSD is essential before signing an Option to Purchase.

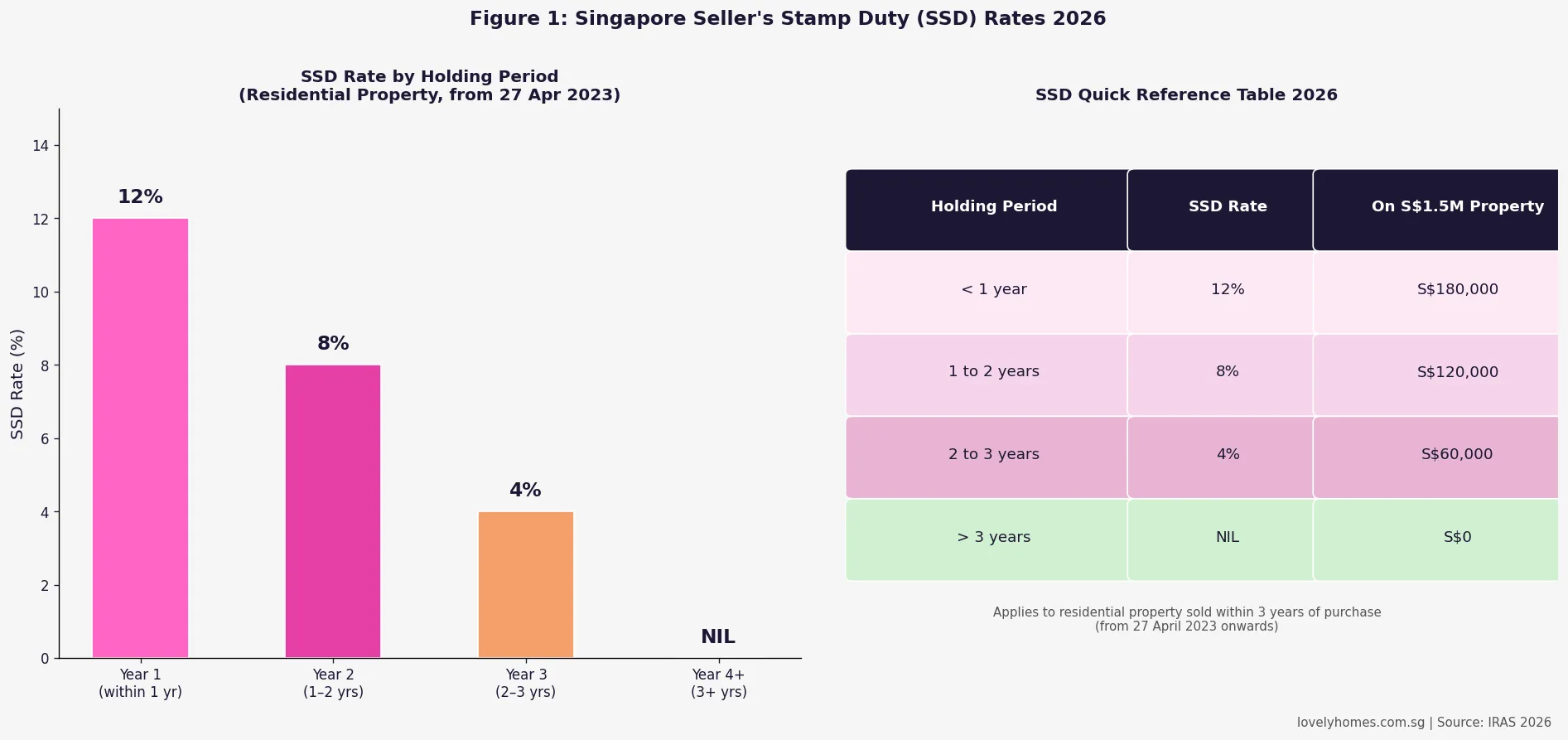

- SSD rates (from 27 April 2023): Year 1 — 12%; Year 2 — 8%; Year 3 — 4%; Year 4 and beyond — 0%.

- Who pays: The seller pays SSD, not the buyer. It is calculated on the higher of the sale price or the market value.

- Properties covered: Residential properties only — private condos, landed houses, and ECs after privatisation. HDB flats are excluded from SSD (they have the MOP instead).

- Administered by: IRAS (Inland Revenue Authority of Singapore).

- Payment deadline: Within 14 days of signing the Option to Purchase (OTP) or agreement.

- Remissions exist for death, bankruptcy, divorce, en bloc collective sale, and certain compulsory acquisitions.

- SSD is not deductible against income tax — it is a capital transaction cost.

- The holding period runs from the date of purchase (completion) to the date of sale (contract).

What Is Seller’s Stamp Duty and Who Administers It?

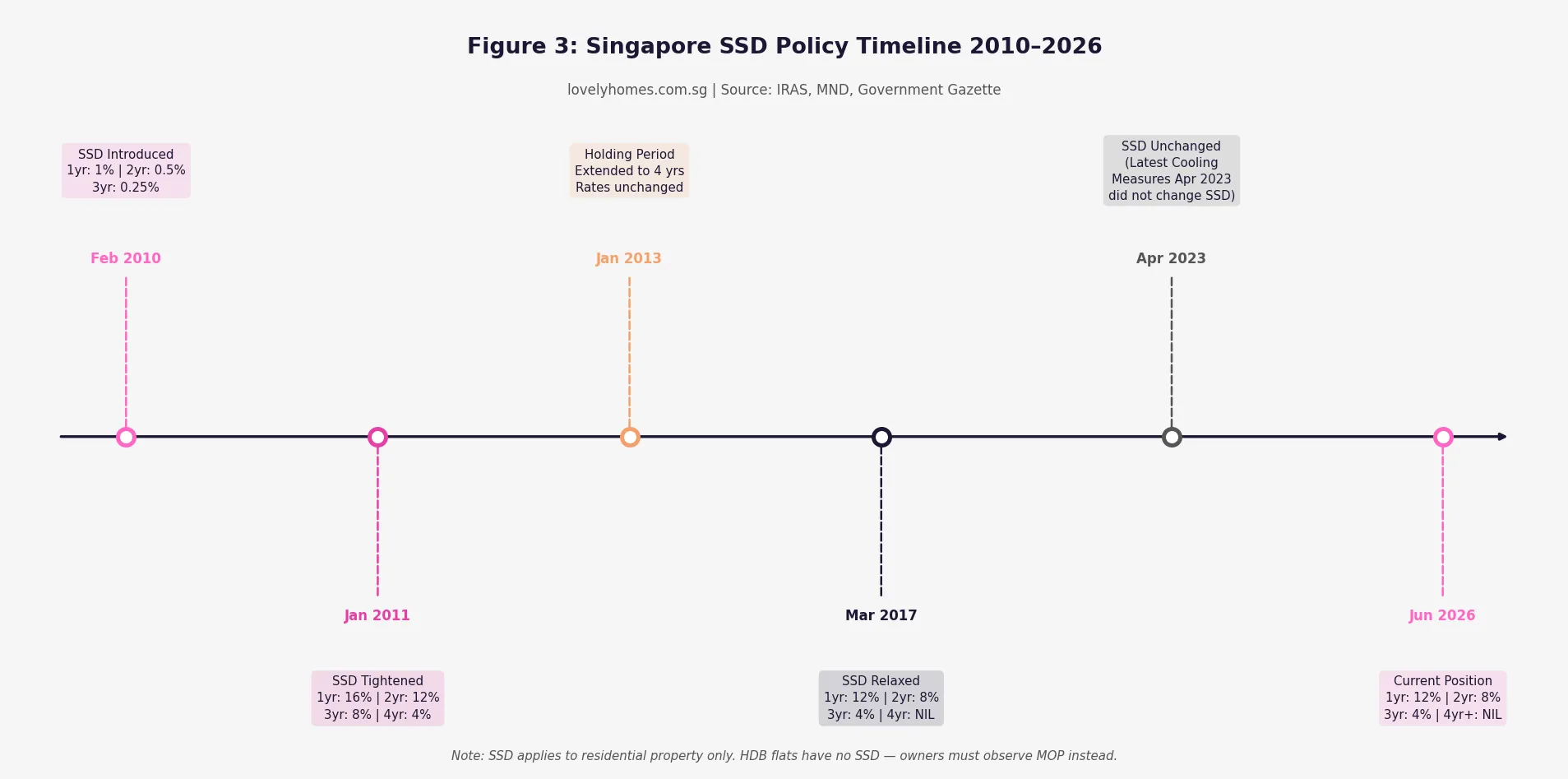

Seller’s Stamp Duty (SSD) is a stamp duty levied by IRAS on the seller of a residential property when the property is disposed of within three years of acquisition. It was first introduced on 20 February 2010 by the Ministry of Finance as part of a suite of cooling measures designed to curb short-term speculative buying and selling that had contributed to rapid price escalation in the aftermath of the 2009 property boom.

SSD is fundamentally different in purpose from BSD and ABSD. BSD is a transaction tax levied on all buyers regardless of intent. ABSD targets the demand side — discouraging multiple property ownership, especially by foreigners. SSD, by contrast, targets the supply side: it penalises sellers who sell too quickly, making “flipping” — buying property to sell within a short period at a profit — financially unattractive. The policy intent is to encourage genuine owner-occupation and long-term investment rather than short-term trading.

IRAS administers SSD. The seller’s solicitor is responsible for computing, stamping, and remitting the SSD to IRAS before the completion of the sale. SSD is a charge against the proceeds of sale and is typically deducted from the sale proceeds held by the seller’s solicitor before the seller receives the net cash.

Current SSD Rates 2026: The Three-Year Window

The current SSD rate schedule, effective from 27 April 2023, applies to residential properties acquired on or after that date. For properties acquired before 27 April 2023, the rates that prevailed at the time of acquisition apply — but since April 2023 is now more than three years ago, virtually all transactions occurring today are within the current rate schedule or have already crossed the three-year SSD-free window.

The rates are straightforward: if you sell within the first year of ownership, SSD is 12% of the higher of the sale price or market value. Between one and two years, the rate drops to 8%. Between two and three years, it is 4%. After three full years from the date of acquisition, SSD falls to zero — the property may be sold without any SSD liability. The holding period is measured from the date the seller legally acquired the property (the date of completion, or in the case of a new launch, the date of the Sales & Purchase Agreement) to the date the seller enters into the agreement to sell (the OTP date for a resale, or the S&P date for a new launch).

For a property valued at S$1.8 million, the SSD exposure is: Year 1 — S$216,000; Year 2 — S$144,000; Year 3 — S$72,000; Year 4+ — S$0. These are substantial sums that fundamentally change the investment calculus for anyone considering a quick exit.

How SSD Is Calculated: The “Higher Of” Rule

A critical nuance that many sellers overlook is that SSD is calculated on the higher of the transacted price or the market value of the property at the time of sale — not simply on the contract price. IRAS may commission its own valuation if it suspects the declared sale price is below market. This prevents sellers from artificially depressing the sale price to reduce SSD. In most arm’s-length transactions the contracted price and market value are the same, but in related-party sales (e.g. selling to a sibling at a discount), IRAS will use the higher market value figure.

The SSD formula: SSD = Applicable Rate × Higher of (Sale Price or Market Value). There are no progressive tiers within each year — the rate applies to the full consideration amount. Sellers should confirm the applicable rate with their solicitor before signing the OTP, since any change in holding-period calculation can significantly alter the tax.

Which Properties Are Subject to SSD?

SSD applies to residential properties in Singapore: these include private condominiums, apartments, landed houses (terrace, semi-detached, detached), and Executive Condominiums (ECs) that have completed their privatisation (i.e. after the 10-year privatisation milestone from TOP). Mixed-use properties where part of the floor area is residential may attract partial SSD depending on the proportion of residential use — this is assessed by IRAS on a case-by-case basis.

Notably, SSD does not apply to HDB flats. HDB flat owners are governed by the Minimum Occupation Period (MOP) instead — a 5-year MOP for standard flats and a 10-year MOP for Plus and Prime classification flats. During the MOP, an HDB owner simply cannot sell. Once the MOP is cleared, HDB resale transactions carry no SSD liability whatsoever. This distinction means that the SSD burden falls exclusively on private property owners.

Commercial and industrial properties are also exempt from SSD — these asset classes have their own regulatory frameworks but do not carry residential SSD exposure. An investor who owns a private residential unit and a shophouse must assess SSD only in respect of the residential unit.

SSD Remissions: When IRAS May Waive or Reduce SSD

IRAS provides remissions (full or partial waivers) for SSD in specific circumstances where the sale is not voluntary or speculative. The key scenarios are as follows. In the case of death, if a property is disposed of by the estate of a deceased owner or transferred to a beneficiary, SSD is remitted — the disposal is not treated as a voluntary sale. For bankruptcy, if the Official Assignee sells the property as part of bankruptcy proceedings, SSD is remitted on the forced-sale transaction. In divorce proceedings, a transfer of property between divorcing spouses pursuant to a court order (Division of Matrimonial Assets) is not subject to SSD. For en bloc / collective sale, when a building or development is sold collectively under the Land Titles (Strata) Act through an en bloc process, SSD is remitted for the individual owners in that collective sale. Similarly, properties acquired compulsorily by the state under the Land Acquisition Act attract full SSD remission.

Remissions are not automatic — they must be claimed. The solicitor managing the transaction should identify whether a remission applies and file the appropriate application with IRAS. Unsolicited sales by genuine owner-occupiers who face sudden hardship (e.g. job loss, medical emergency) do not constitute remission grounds — only the specific categories above qualify. Buyers upgrading from an HDB flat to a private property and needing to sell quickly after ABSD remission are not eligible for SSD remission on the private property side unless their circumstances fall into one of the above categories.

Summary Table: SSD At a Glance 2026

| Factor | Details |

|---|---|

| Administered by | IRAS (Inland Revenue Authority of Singapore) |

| Effective from (current rates) | 27 April 2023 |

| Year 1 rate (held < 1 year) | 12% of sale price or market value (higher) |

| Year 2 rate (held 1–2 years) | 8% |

| Year 3 rate (held 2–3 years) | 4% |

| Year 4+ (held > 3 years) | 0% (no SSD) |

| Who pays | The seller |

| Payment deadline | 14 days from OTP/agreement signing |

| Properties covered | Residential — private condo, landed, privatised EC |

| HDB flats | Exempt (MOP rules apply instead) |

| Remission scenarios | Death, bankruptcy, divorce (court order), en bloc, compulsory acquisition |

| Tax deductibility | Not deductible against income tax |

Worked Example: The Full SSD Impact on an Investment Property Sale

Mr Chen purchased a 1,000 sqft condominium unit in the Outside Central Region (OCR) for S$1,400,000 in June 2024. By December 2025 (18 months later), the development has appreciated and he receives an offer of S$1,580,000. He is tempted to sell. Let us calculate the full financial picture.

Holding period: June 2024 to December 2025 = approximately 18 months = Year 2 (1–2 years). SSD rate: 8%.

SSD on S$1,580,000 at 8%: S$126,400.

Other sale costs: agent commission at 2% = S$31,600; legal fees (seller) = S$3,000; property tax adjustment to date of completion = S$1,200. Total other sale costs: S$35,800.

Purchase costs already sunk: BSD at purchase on S$1,400,000 = S$36,600; legal fees at purchase = S$3,500; ABSD if applicable = nil (SC second property was 20% ABSD = S$280,000 — included in total outlay). Let us use a scenario where Mr Chen’s first property was an HDB flat and he sold it within the same week, triggering the ABSD remission window, so effectively 0% ABSD was paid.

Gross gain: S$1,580,000 − S$1,400,000 = S$180,000.

Net position after SSD and sale costs: S$180,000 − S$126,400 (SSD) − S$35,800 (sale costs) = net loss of S$18,200, before factoring in purchase costs (BSD, legal) and financing costs (mortgage interest paid over 18 months — at 2.5% on S$1,050,000, approximately S$26,250 in interest payments).

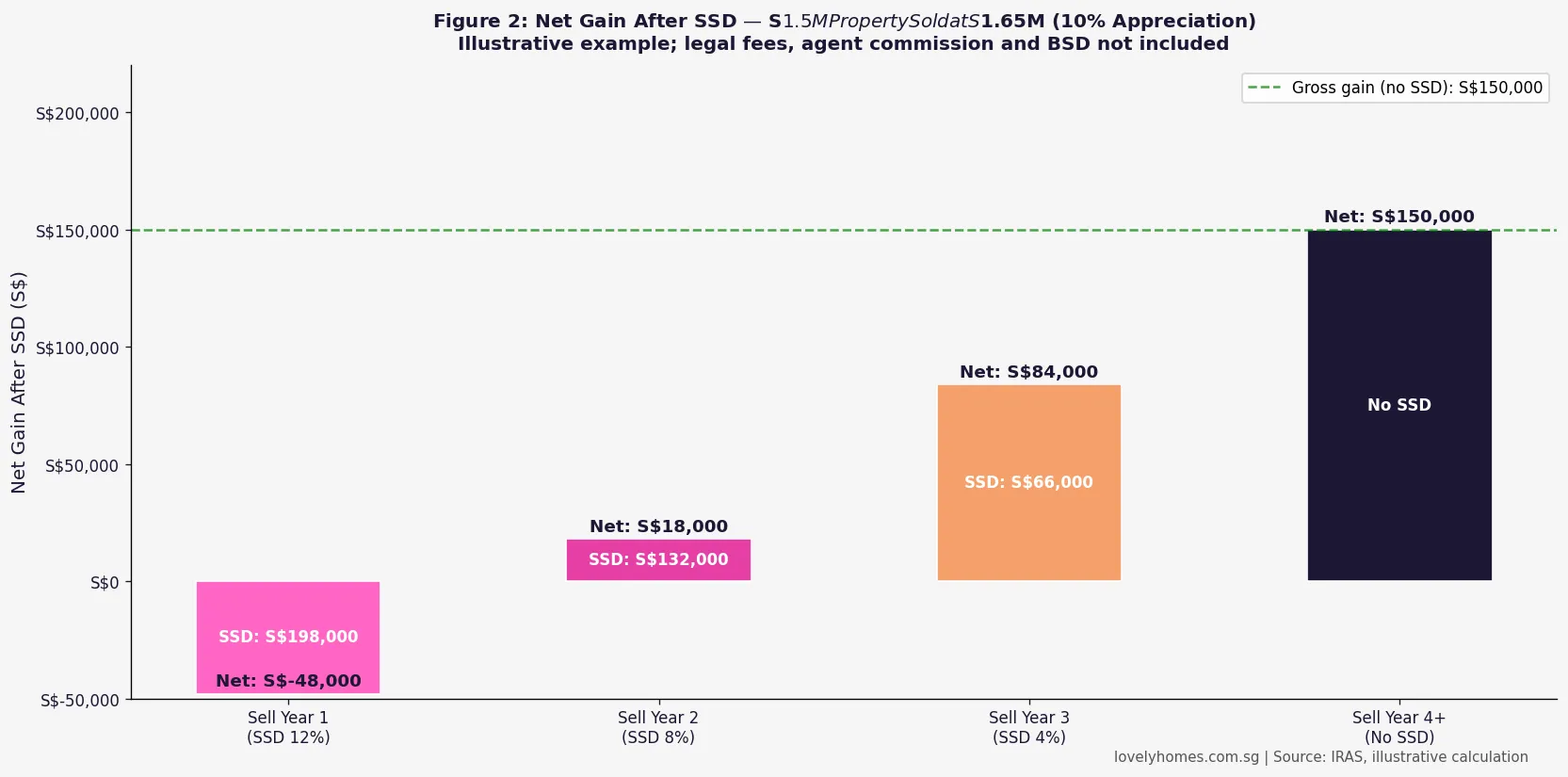

Conclusion: A sale at 18 months with 12.7% nominal appreciation results in a net loss when SSD, transaction costs, and financing costs are properly accounted for. Mr Chen would need to achieve a sale price of at least S$1,648,000 — a 17.7% appreciation — just to break even at the 18-month mark. If he waits until Month 37 (past the 3-year SSD window), the same appreciation of S$180,000 becomes a net gain of approximately S$144,200 (gross gain less sale costs and BSD, before financing). This illustrates precisely why SSD achieves its policy intent.

SSD vs ABSD: How They Interact for Property Investors

Singapore’s property investor faces a layered stamp duty landscape. At purchase, BSD (1%–6%) and ABSD (0%–65% depending on buyer profile and property count) apply. At sale, SSD (0%–12%) applies for the first three years. These taxes do not offset each other — they are separate liabilities at separate points in time.

An SC buyer of a second property pays 20% ABSD at purchase and up to 12% SSD on an early sale — a combined transactional tax burden of 32% of the purchase price in a worst-case Year 1 sale scenario, on top of BSD. At these levels, property speculation in the short term is essentially economically unviable for individual investors, which is precisely the government’s stated intention. The ABSD remission available to HDB upgraders (where the HDB is sold within 6 months of private purchase) provides relief from ABSD but does not affect SSD — the SSD clock runs from the private property acquisition date regardless.

What Might Come Next

The SSD framework has been broadly stable since the April 2023 cooling measures, which left SSD rates unchanged while tightening ABSD. Industry observers and research desks generally expect the SSD structure to remain unchanged through the rest of 2026 and into 2027, barring a significant correction in private residential prices. The government has consistently signalled that Singapore’s property cooling measures are not designed as permanent fixtures but as calibrations to market conditions — any future SSD liberalisation is more likely to come alongside ABSD relaxation in a cooling-demand environment, rather than in isolation. Buyers and investors should not plan transactions around expected SSD changes; the base case is status quo.

One area to monitor is the treatment of ECs under SSD as the government’s May 2026 EC MOP extension (from 5 years to 10 years from TOP) works through the pipeline. The interplay between the extended EC MOP and the SSD three-year clock for privatised ECs means buyers of recently privatised ECs face a narrow window where both MOP-based restrictions and SSD restrictions overlap — though by the time privatisation occurs (10 years from TOP), any SSD liability would have long since lapsed.

Frequently Asked Questions

Does SSD apply if I sell my property at a loss?

Yes. SSD is calculated on the higher of the sale price or market value, regardless of whether you make a profit or a loss on the transaction. If you paid S$2 million for a property and sell it for S$1.8 million within Year 1, the SSD is calculated on S$1.8 million (assuming that is the market value), giving an SSD liability of S$216,000 — on top of the S$200,000 capital loss. This makes early distressed sales of recently purchased property extraordinarily costly. The policy deliberately does not provide for an exemption when selling at a loss, as the government’s concern is speculative behaviour rather than the seller’s profit outcome.

When exactly does the SSD holding period start?

For a completed property (resale purchase or a completed development), the holding period starts on the date of completion — typically when the title transfers to the buyer upon payment of the balance purchase price. For a new launch (uncompleted property under progressive payment), IRAS uses the date the Sale and Purchase Agreement (S&P) was signed as the start date, not the TOP date. This means a buyer who signed an S&P in 2022 and received their keys in 2026 has already served well past the three-year window — no SSD applies on a subsequent sale. Conversely, a buyer who signed an S&P in January 2024 and sells the unit in February 2026 (before TOP) would be selling in Year 2 — an 8% SSD applies on the sub-sale price.

Can SSD be paid using CPF?

No. SSD is a charge against sale proceeds and must be paid in cash by the seller’s solicitor from the proceeds of sale. Unlike BSD, which buyers can settle from their CPF Ordinary Account, SSD is on the selling side and is deducted before the net proceeds are released to the seller. If the sale proceeds are insufficient to cover SSD (e.g. the property is heavily mortgaged), the seller must top up in cash.

How does SSD interact with an en bloc sale?

In a collective sale (en bloc) conducted under the Land Titles (Strata) Act, SSD is fully remitted for all owners participating in the collective sale — including owners who might still be within their SSD holding period. The rationale is that en bloc owners are not voluntarily choosing to sell; they are bound by the collective decision once the requisite majority approves the sale. The remission applies to all participating owners regardless of when they acquired their units, provided the collective sale is completed through the prescribed statutory process with IRAS confirmation.

Is SSD the same as the Additional Seller’s Stamp Duty (ASSR)?

There is no instrument in Singapore called “Additional Seller’s Stamp Duty (ASSR).” SSD is the only seller-side stamp duty for residential property. You may occasionally see references to SSD in older documents as distinct from “BSD-SSD” — this simply means the stamp duty payable by the seller, as opposed to the BSD payable by the buyer. Do not confuse SSD with ABSD: ABSD is paid by the buyer (not the seller) and applies based on the buyer’s residential property count, not the holding period.

I gifted my property to a family member — does SSD apply?

Yes, a gift or transfer at undervalue between related parties is still subject to SSD if the holding period has not elapsed. IRAS treats the market value of the property (not the consideration, if any) as the basis for SSD assessment. The only gift-related exemption is a transfer pursuant to a court order in divorce proceedings. A transfer to a child, sibling, or parent — even at nominal S$1 consideration — will attract SSD at the applicable rate on the market value, if the property was acquired within the past three years. This is one of the most common and costly misunderstandings around SSD.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Buyer’s Stamp Duty (BSD) Guide 2026

- Singapore Property Cooling Measures Timeline 2009–2026

- Singapore Property Financing Guide 2026: LTV, TDSR, MSR and Loan Types

- Singapore Property Due Diligence Guide 2026

- Singapore Rental Income Tax Guide 2026

- Singapore Property Land Tenure Guide 2026: 99-Year vs Freehold vs 999-Year

Disclaimer

This article is for general information only and does not constitute legal or tax advice. SSD rates, remission criteria, and payment timelines are subject to change by IRAS and the Ministry of Finance at any time. All figures and rates quoted are as of June 2026. Stamp duty calculations involve factual determinations that depend on the specific circumstances of your transaction. Readers should verify all information with IRAS (www.iras.gov.sg) and consult a licensed conveyancing solicitor before entering into any property transaction. For complex scenarios — en bloc participations, related-party transfers, divorce settlements — professional legal advice is strongly recommended.