Tenancy Agreement Singapore 2026: A Landlord and Tenant’s Complete Guide to the Rental Contract

Last updated 28 April 2026. Reflects IRAS lease stamp duty rules current as at FY2026 and standard market norms reported by URA’s quarterly rental statistics.

Quick Answer — 30-second takeaways

- A Singapore tenancy agreement is the binding contract between a landlord and tenant. It is governed by Singapore contract law and the principles of the Civil Law Act and the Conveyancing and Law of Property Act.

- Standard residential terms are 12 or 24 months. Anything shorter than 3 months risks being treated as serviced accommodation, which is regulated separately.

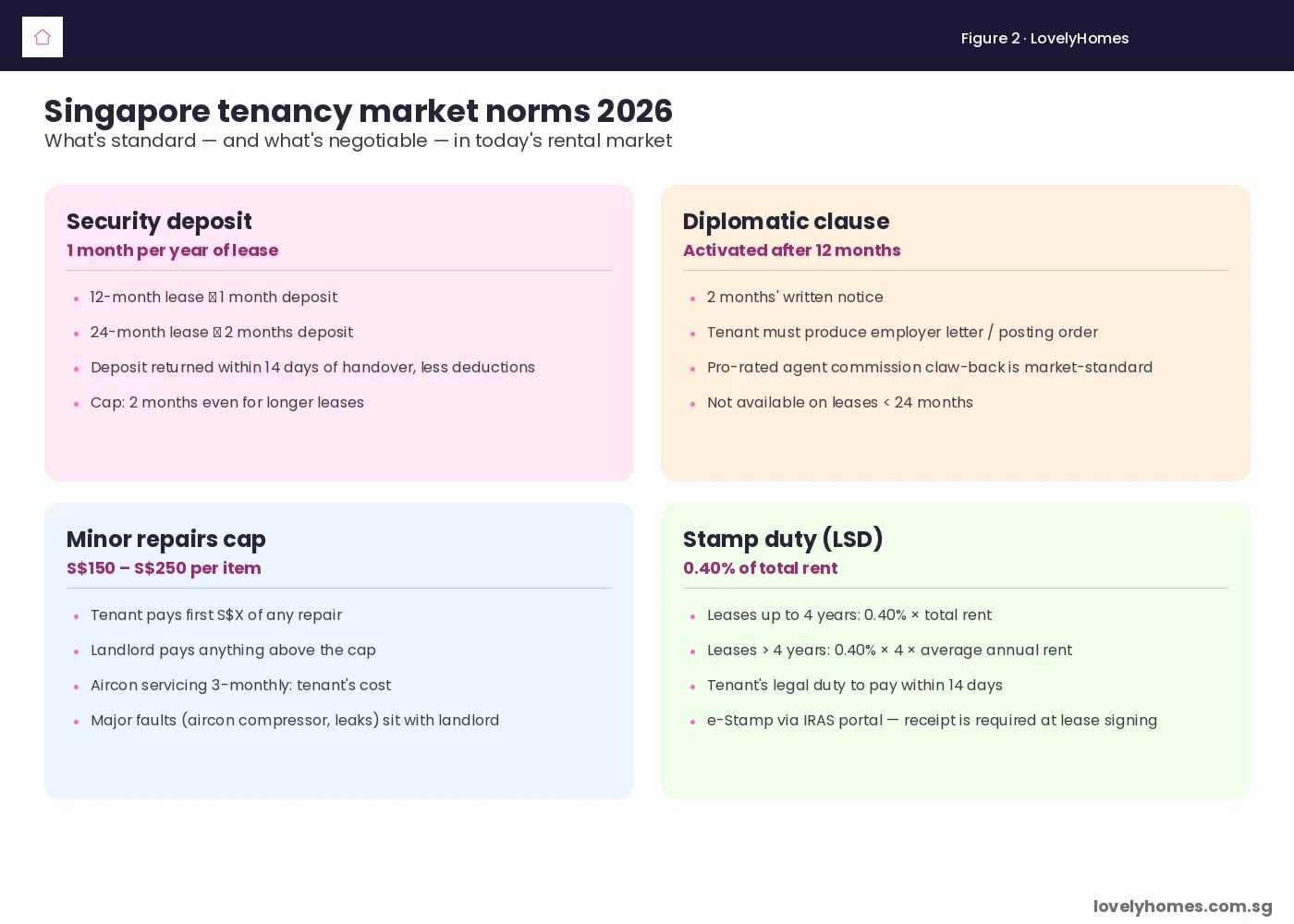

- Security deposit: typically 1 month’s rent per year of lease, capped at 2 months. Refundable within 14 days of handover, less reasonable deductions.

- Diplomatic clause: standard on 24-month leases, lets the tenant terminate after 12 months on 2 months’ notice if posted out of Singapore.

- Lease stamp duty (LSD): 0.40% of total rent across the lease term, payable by the tenant within 14 days of execution, e-stamped at iras.gov.sg.

- Minor repairs cap: tenant pays first S$150–S$250 of any repair; landlord pays the excess. Aircon servicing 3-monthly is the tenant’s cost.

- Disputes ≤ S$30,000 can be heard at the Small Claims Tribunals (SCT) with both parties’ consent. Larger disputes go to the State Courts.

What a tenancy agreement is — and what it isn’t

A tenancy agreement (often abbreviated TA) is the written contract that creates a legal lease between a property owner (the landlord) and an occupant (the tenant). It records the parties, the property, the term, the rent, the deposit, and the rules for living in and looking after the home.

Singapore does not have a dedicated Residential Tenancy Act. Tenancy agreements are governed by general contract law, supplemented by the Civil Law Act 1909, the Conveyancing and Law of Property Act 1886, and — for HDB rentals — by the rules of the Housing and Development Board. This means that what is “standard” in a Singapore tenancy is largely set by market practice and by widely-used template clauses, not by statute. Landlords and tenants who do not read every clause carefully can find themselves bound by terms the other side considers normal but they did not expect.

A tenancy agreement is not a Letter of Intent (LOI). The LOI is the pre-contract document the prospective tenant submits with a good-faith deposit. The TA is the binding lease that follows once the LOI is accepted. Stamp duty is payable on the TA, not the LOI.

Who can be a landlord, and who can be a tenant

For private property, any property owner can lease their unit, subject to building by-laws and the conditions of any mortgage. The Urban Redevelopment Authority requires a minimum lease of 3 months for private residential property; below that threshold the lease is treated as short-stay accommodation and is generally not allowed unless the unit is licensed serviced apartment stock.

For HDB flats, the rental rules are stricter:

- The flat must have met its Minimum Occupation Period (MOP), which is typically 5 years for new flats and 5 years for resale flats with grant.

- The owner must apply for HDB approval to rent out the whole flat or individual rooms.

- Rentals to non-citizen households must respect the Ethnic Integration Policy (EIP) and Singapore Permanent Resident (SPR) quota.

- Maximum 6 unrelated occupants per flat (4 for 1- and 2-room flats).

- The minimum rental period is 6 months for whole-flat HDB rentals.

Tenants can be Singapore Citizens, Permanent Residents, work-pass holders, students or any other lawfully present individual. For non-resident tenants, landlords must verify that the tenant holds a valid pass throughout the lease — leasing to an individual without a valid pass is an offence under the Immigration Act.

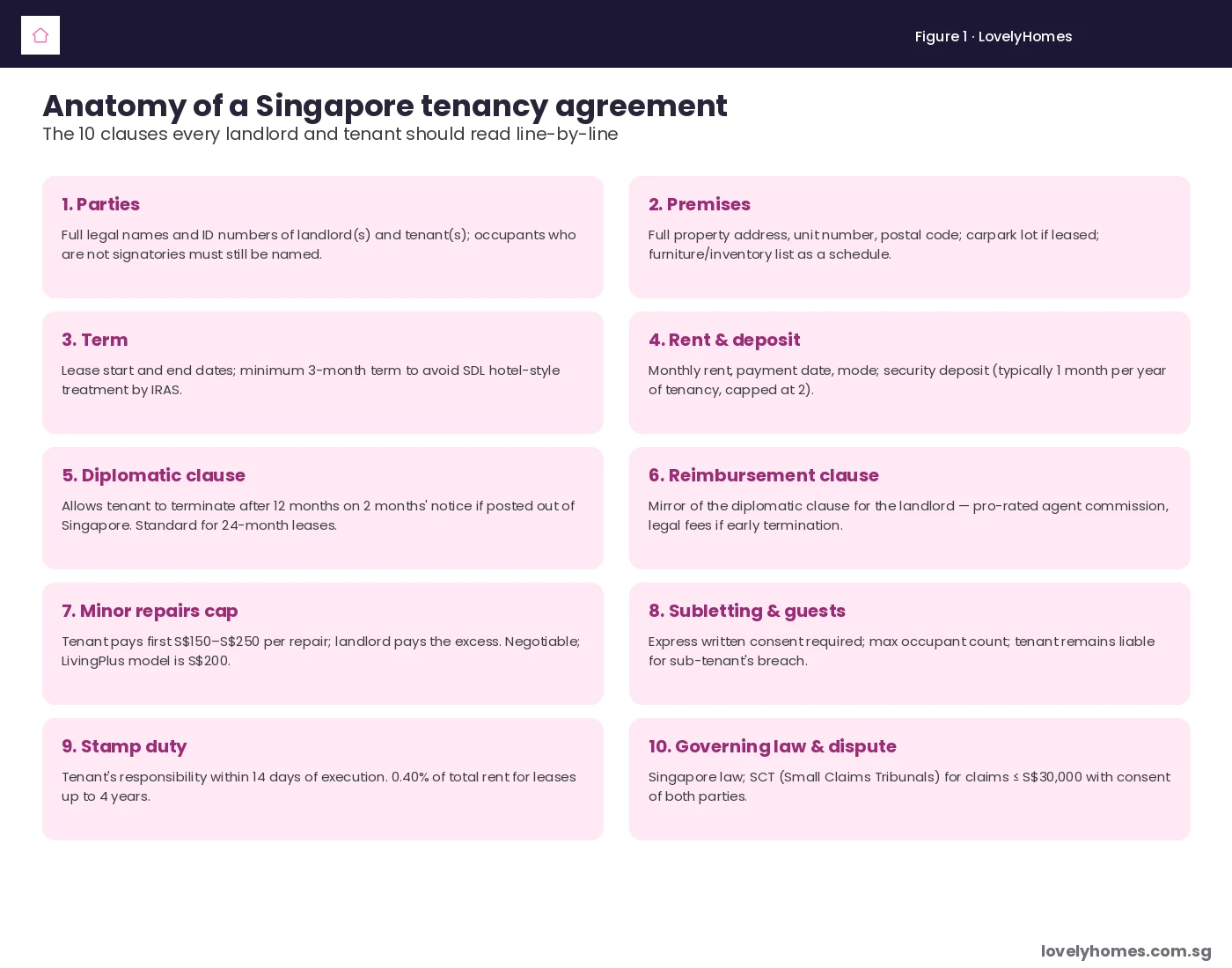

The 10 clauses that do all the work

A typical Singapore residential TA runs to 8–14 pages. Most of the legal heavy-lifting happens in ten clauses, summarised in Figure 1 above and explored below.

Term and renewal

The lease term is fixed: it has a defined start date and end date. Holding-over (continuing to occupy after expiry without a new TA) creates a tenancy at will, which is terminable on short notice and offers neither party much protection. Most landlords negotiate renewal 2–3 months before expiry; the LSD on the renewal lease must be re-stamped at the new rent.

Rent and security deposit

Rent is payable monthly in advance. The market norm for the security deposit is 1 month’s rent per year of lease, capped at 2 months. The deposit secures the landlord against damage beyond fair wear and tear, unpaid rent, and unpaid utility bills. It is refunded within 14 days of handover, less itemised deductions. Disputes over deposit deductions are the single most common Singapore tenancy dispute, and the Small Claims Tribunals see hundreds each year.

Diplomatic clause and reimbursement clause

The diplomatic clause allows a tenant to terminate after 12 months on 2 months’ written notice if they are required to leave Singapore (typically because of a job posting or visa cancellation). It is market-standard on 24-month leases and rare on 12-month leases. The mirror is the reimbursement clause: if the tenant terminates early, they must reimburse the landlord on a pro-rated basis for the agent’s commission and legal fees of the original lease.

Minor repairs cap

Tenants are responsible for minor repairs up to a contractual cap, typically S$150–S$250 per item. Landlords pay the excess. The clause prevents petty disputes about light bulbs and tap washers, while keeping major repairs (aircon compressor failure, roof leaks, structural defects) on the landlord’s account. Air-conditioner servicing every 3 months is the tenant’s cost; receipts must be produced at handover.

Inventory and handover

An inventory list — usually a schedule attached to the TA — records every item of furniture, every appliance, and every fixture provided. At move-in, both parties walk through and sign off. At move-out, deductions for missing or damaged items are calculated against this list. Photo evidence at both ends saves arguments.

Stamp duty clause

The TA will state which party is responsible for paying lease stamp duty. By Singapore market practice and IRAS guidance, the tenant pays. Failure to e-stamp within 14 days exposes the lease to a penalty of 4 times the duty or S$10, whichever is higher, and the unstamped lease is inadmissible as evidence in a Singapore court (the duty must be paid before the lease can be relied on in litigation).

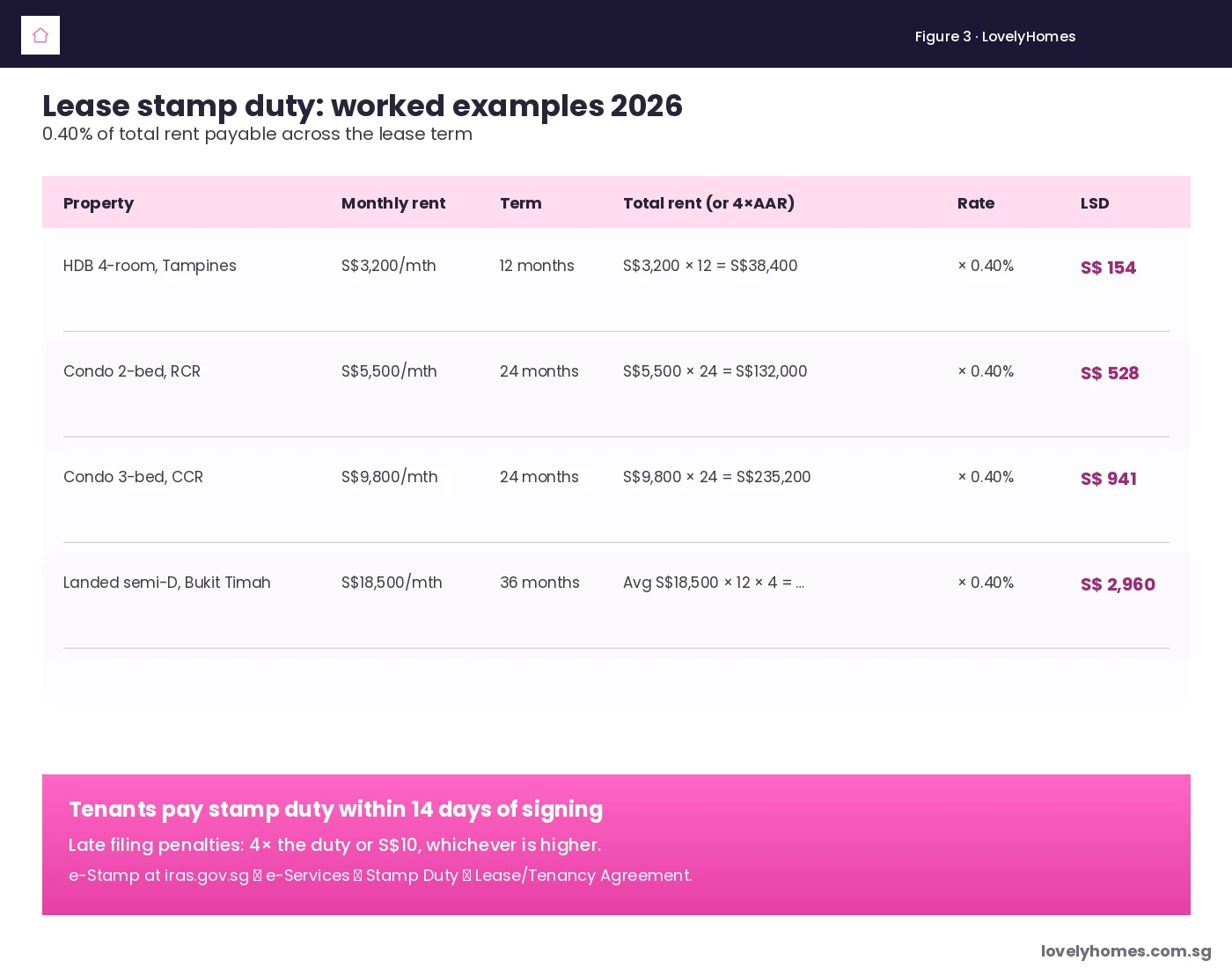

Lease stamp duty: the maths

Lease stamp duty (LSD) is the only tax on a Singapore tenancy. It is levied at 0.40% of total rent across the lease term, capped at four times the average annual rent for leases longer than 4 years. The duty is the tenant’s legal obligation under section 33 of the Stamp Duties Act, payable within 14 days of execution.

| Lease term | Stamp duty formula | Notes |

|---|---|---|

| ≤ 4 years | 0.40% × total rent across the term | Most common; covers all 12- and 24-month leases |

| > 4 years | 0.40% × 4 × average annual rent | Caps the duty for long leases |

| Lease with premium / variable rent | BSD-style staircase rates apply to premium; LSD on the rent component | Rare in residential — common in commercial |

The IRAS portal e-stamps the lease in real time. The tenant pays via PayNow, eNETS or credit card, prints the certificate, and brings the original to the lease signing. Many landlords now make production of the e-stamp certificate a precondition to handing over keys — a sensible safeguard, because once keys are handed over the landlord’s leverage drops sharply.

Negotiating the lease — what to push on, what to leave alone

Singapore tenancy agreements are negotiable. The points that move most often:

- Diplomatic clause activation date. Tenants often ask for activation at month 9 instead of month 12. Landlords typically refuse. The 12-month default holds.

- Minor repairs cap. Tenants ask for S$300; landlords often want S$150. The S$200 LivingPlus number is the comfortable middle.

- Whitegoods inclusion. Whether refrigerator, washer, dryer, microwave, oven, vacuum and rice cooker are included is line-by-line negotiation. List each item by brand and model in the inventory schedule.

- Repainting before handover. A clause requiring the tenant to repaint before move-out used to be standard. It is increasingly replaced by a fixed reinstatement fee (S$300–S$800) plus normal wear-and-tear treatment.

- Pet clause. “No pets” is the default. Tenants with pets must negotiate a specific carve-out and an additional deposit. HDB has its own approved-breed list for flats.

- Smoking. “No smoking inside the unit” is now standard, and landlords reasonably claim against deposit if walls and curtains carry residual smoke odour.

What happens if things go wrong

The Singapore framework for tenancy disputes is informal but well-trodden:

- Small Claims Tribunals (SCT). Hears disputes ≤ S$20,000 (or up to S$30,000 with both parties’ consent in writing) for tenancies of up to 2 years. Hearings are tenant- and landlord-friendly: no lawyers in the courtroom, fees from S$10, decisions usually within 4–6 weeks. The most common claims are deposit deductions, damage to inventory, and unpaid rent.

- State Courts. Larger disputes, longer leases, and complex commercial-residential overlaps. Lawyers represent both sides; costs follow the event.

- HDB and the Housing & Estate Disputes Resolution Centre. For HDB rental disputes specifically, HDB will mediate before parties resort to the SCT.

- Mediation via the Singapore Mediation Centre. Voluntary and confidential. Useful where the parties want to preserve a working relationship — for example, a landlord who wants the tenant to stay another year.

What this means for you

For tenants: read every clause. Push back on anything ambiguous. Pay LSD on time and keep the certificate. Photograph the unit on move-in and move-out. Save every WhatsApp message about repairs — these are evidence in any future SCT claim.

For landlords: use a template TA from a Singapore conveyancing lawyer (not a generic internet template). Check the tenant’s pass status throughout the lease. Inspect the unit twice during a 24-month lease — once at month 6, once at month 18 — with proper notice. Reply in writing to repair requests. The landlord’s deposit deduction is much harder to defend in the SCT if the inspection trail is thin.

What might come next

The Ministry of National Development has been studying the case for codifying residential tenancy law in Singapore — the United Kingdom, Australia and several jurisdictions in continental Europe have moved in this direction. As at April 2026, no draft Bill has been tabled. The likeliest medium-term reforms are: a statutory deposit scheme along the lines of the UK Tenancy Deposit Scheme; a standard tenancy agreement template published by URA or HDB; and clearer rules on the deductibility of fair wear and tear. None of these are imminent, but landlords and tenants who structure their TAs around the existing market norms are well-positioned for any future statutory framework.

Frequently asked questions

Who pays the property agent’s commission?

Singapore market practice is that each side pays its own agent. The landlord pays the landlord’s agent (typically 1 month of annual rent on a 24-month lease, half a month on a 12-month lease). The tenant typically pays the tenant’s agent only on shorter or smaller-rent leases (under S$3,500/month) where the landlord’s agent’s fee is too thin to share. CEA’s Code of Ethics and Professional Client Care requires written disclosure of who pays whom before any signing.

Can a tenant break the lease before the diplomatic clause activates?

Only if the landlord agrees, or if the landlord is in fundamental breach (uninhabitable conditions, refusal to make repairs, harassment). Otherwise, an early termination is a breach of contract. The tenant remains liable for rent until the landlord re-lets the unit; the security deposit is forfeited; the original agent’s commission is clawed back pro-rata. Most landlords are willing to release a tenant if a replacement tenant on equivalent terms is presented.

Can the landlord enter the property without notice?

No. The TA grants the tenant exclusive possession. The landlord may enter only with reasonable notice (typically 24 hours in writing) and at reasonable times, except in emergencies (fire, flood, gas leak). Repeated unannounced visits are a breach of the covenant for quiet enjoyment and can support a tenant’s claim for damages.

What if the tenant has overstayed or won’t leave?

Self-help eviction is unlawful in Singapore. The landlord must give the contractual notice (or, if the lease has expired, a notice to quit), and if the tenant still does not leave, file for a Writ of Possession at the State Courts. Locking the tenant out, removing belongings, or cutting utilities is a criminal offence under the Protection from Harassment Act 2014 and the Distress Act 1872.

Does GST apply to residential rent?

No. Residential rent is exempt from GST under the Fourth Schedule to the GST Act. GST applies only to commercial leases — and only when the landlord is GST-registered (i.e., turnover above S$1 million in a 12-month period).

Can a tenant sub-let to a third party?

Only with the landlord’s written consent. Most TAs have an express anti-subletting clause. Even where consent is given, the head tenant remains liable to the landlord for the sub-tenant’s behaviour, rent and damage. For HDB rentals, all sub-letting must additionally have HDB approval; unauthorised sub-letting is a serious offence and can result in compulsory acquisition of the flat.

Is a verbal lease enforceable?

A verbal residential lease for 3 years or less is technically enforceable under the Conveyancing and Law of Property Act, but in practice it is almost impossible to prove the terms. For any lease over 3 years, the law requires a written, signed deed, registered with the Singapore Land Authority. As a landlord or tenant, you should never proceed without a written, e-stamped TA.