Singapore Property Land Tenure Guide 2026: 99-Year vs Freehold vs 999-Year Explained

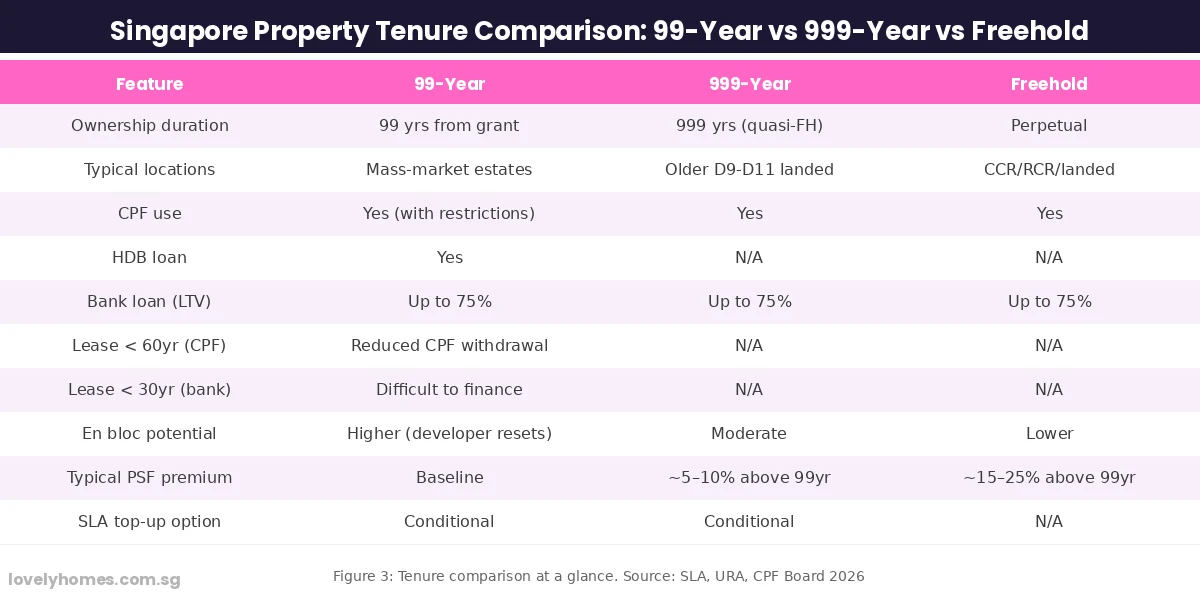

- Freehold means you own the land in perpetuity — no expiry date. More common in CCR/RCR and older landed estates.

- 999-year leasehold is functionally near-freehold for most buyers’ lifetimes; found mainly in older District 9–11 properties and some landed estates.

- 99-year leasehold is the most common tenure for HDB flats and most modern private condominiums in Singapore; lease starts from the date of grant, not your purchase date.

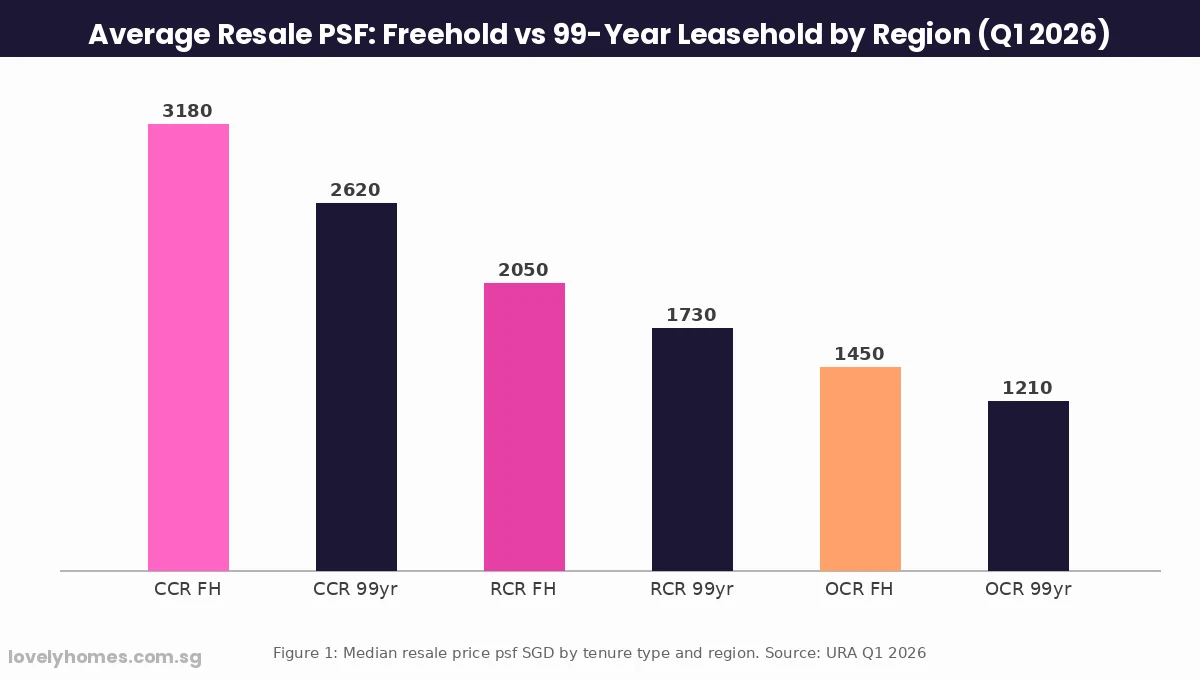

- Freehold resale properties command roughly 15–25% price premium over comparable 99-year leaseholds in the same district.

- CPF OA use and bank loan availability are restricted when a property’s remaining lease falls below 60 years (CPF) or 30 years (bank financing).

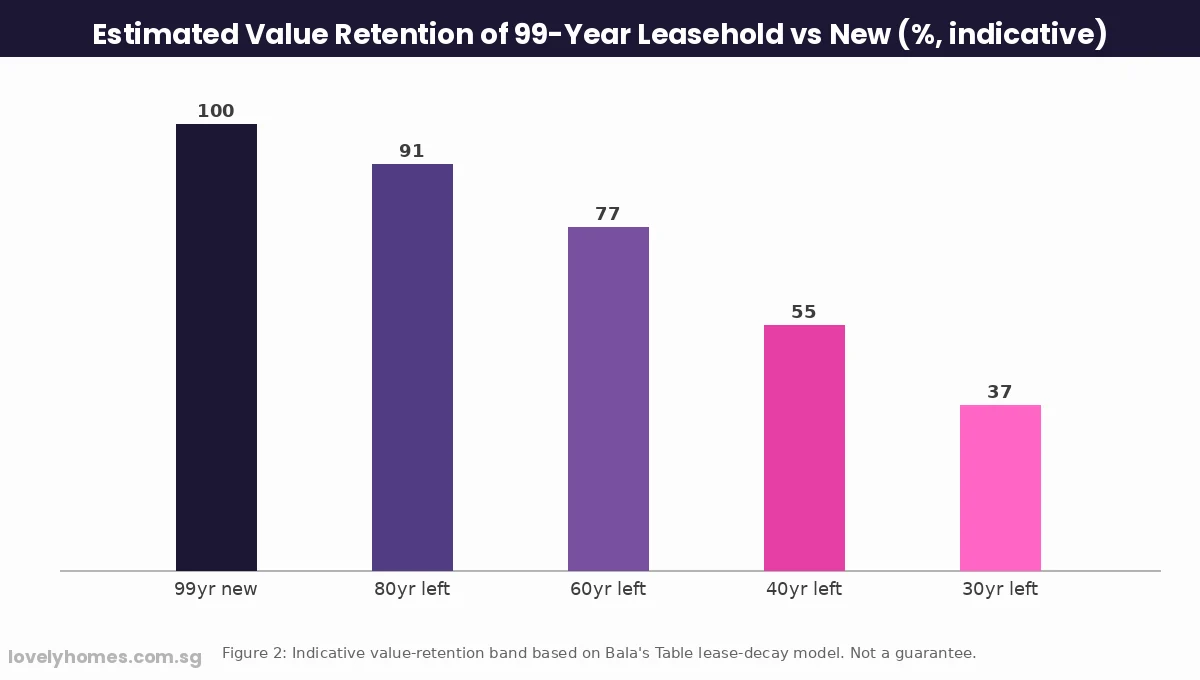

- Value decay under Bala’s Table becomes measurably steep once a 99-year lease drops below 60 years remaining — roughly equivalent to a flat purchased new in 1965.

- The Singapore Land Authority (SLA) administers all land titles; lease top-ups are discretionary and not guaranteed.

Land tenure is one of the most fundamental — and most misunderstood — concepts in the Singapore property market. When you buy a private condominium or landed home, you are not just buying bricks and mortar: you are buying a right to occupy the land beneath for a defined period. That period, and what happens as it runs down, has profound consequences for your mortgage eligibility, CPF usage, resale value, and long-term investment returns.

Singapore operates under three primary tenure types: freehold (perpetual ownership), 999-year leasehold (quasi-freehold for practical purposes), and 99-year leasehold (the dominant tenure for HDB flats and most modern private developments). Each carries different price dynamics, financing rules, and exit strategies. This guide, correct as at 24 June 2026, explains what each tenure type means, how it affects your purchase decision, and what buyers and investors need to know before signing any Option to Purchase.

What Does Land Tenure Mean in Singapore?

All land in Singapore is ultimately owned by the state. When you purchase a freehold property, the government grants you perpetual right to that parcel; when you purchase a leasehold property, you receive the right to occupy the land for a defined term. HDB flats are all built on 99-year leasehold land granted by the Housing & Development Board, which in turn holds the land from the state. Private leaseholds are similarly titled under the Land Titles (Strata) Act, administered by the Singapore Land Authority (SLA).

The practical implication is straightforward: a 99-year leasehold property bought new today will have zero land value — and may be compulsorily acquired — when the lease expires 99 years hence. A freehold property, by contrast, can theoretically be passed on to your descendants indefinitely. In practice, most Singaporeans will never own a property long enough for this distinction to matter personally, but it matters enormously to the resale market, to developers calculating en-bloc potential, and to CPF Board and bank underwriters assessing loan risk.

The Three Tenure Types: Freehold, 999-Year and 99-Year

Freehold

A freehold title in Singapore confers perpetual ownership of the land. The property can be sold, inherited, or redeveloped without any lease-expiry concern. Freehold land is disproportionately concentrated in the Core Central Region (CCR), particularly Districts 9, 10, and 11, as well as in older landed residential estates in districts like D15 (East Coast) and D19 (Serangoon Gardens). Because supply is finite — the government rarely grants new freehold sites in the Government Land Sales programme — freehold properties trade at a sustained premium over 99-year equivalents.

999-Year Leasehold

A relic of colonial land grants, 999-year leases are functionally indistinguishable from freehold for any buyer whose investment horizon is shorter than several centuries. Properties holding 999-year titles include some older landed estates in Districts 9, 10, and 11, as well as certain heritage shophouses. Banks treat 999-year and freehold identically for loan-to-value purposes; CPF Board similarly imposes no material restrictions. From a market-pricing perspective, 999-year properties command a modest 5–10% premium over comparable 99-year leaseholds, but typically trade at a slight discount to true freehold owing to the perception gap among less-informed buyers.

99-Year Leasehold

The dominant tenure for HDB flats and for most private condominiums launched since the 1980s. When a developer acquires a Government Land Sales site, the land comes with a 99-year lease running from the date of state grant — not the date the units are sold. This distinction matters: if a developer takes two years to build and TOP, the first owner enters at 97 years remaining. By the time a flat is resold five years later, the remaining lease may be only 92 years. Each transfer compresses the remaining term further.

The 99-year structure is by design: the government retains the ability to redevelop land as planning priorities evolve, and the Selective En-Bloc Redevelopment Scheme (SERS) — under which HDB compulsorily acquires older estates at market value and rehouses residents — is the clearest expression of this model. SERS compensation has historically been generous, but it is not guaranteed, and fewer than 5% of HDB estates have been selected since the programme began in 1995.

How Lease Decay Works: Bala’s Table Explained

Singapore’s property valuation profession applies Bala’s Table — a standardised depreciation formula used by licensed valuers — to determine the land value attributable to a leasehold site relative to a freehold equivalent. The table, developed by the late Chief Valuer TC Bala, accounts for the non-linear nature of lease decay: value does not fall in a straight line. Instead, the first 40 years of a 99-year lease retain the bulk of their value, while decay accelerates steeply once the remaining term drops below 60 years.

Practically, a 99-year leasehold property with 80 years remaining retains roughly 91% of its freehold-equivalent land value; at 60 years remaining, approximately 77%; at 40 years remaining, only about 55%. These are not exact market outcomes — sentiment, location, and property condition all intervene — but the directional trend is well-established. Properties approaching 30 years remaining often struggle to attract bank financing and CPF usage altogether, sharply limiting the pool of eligible buyers and putting downward pressure on price.

CPF Rules and Bank Financing by Remaining Lease

The CPF Board and commercial banks both impose restrictions tied to remaining lease duration. These restrictions become a significant pricing factor for older leasehold properties and should be front of mind for any buyer of a resale leasehold property.

CPF OA withdrawal restrictions (CPF Board, 2026): To use CPF Ordinary Account (OA) savings for a property purchase, the remaining lease must be at least 20 years. However, where the remaining lease does not cover the youngest buyer to the age of 95, CPF withdrawal is prorated based on the lease coverage ratio. Practically, a property with fewer than 60 years remaining will see meaningful CPF withdrawal restrictions. A property with fewer than 30 years remaining will typically see CPF usage restricted to very small amounts that make it effectively unusable for most buyers.

Bank loan availability: Most commercial banks in Singapore will not extend a housing loan if the remaining lease at loan maturity is less than 30 years. This effectively creates a financing cliff: properties whose leases will fall below 30 years during the expected loan tenure become very difficult to mortgage, dramatically reducing buyer pools. For a buyer seeking a 25-year loan, this means a property with 54 years remaining today (30 + 25 = 55 years minimum requirement, with slight buffer) may already face bank restrictions from certain lenders.

Price Premium: How Much More Does Freehold Cost?

The freehold premium in Singapore’s private residential market is real but variable. Across the market as of Q1 2026, URA Realis transaction data shows freehold resale properties trading at approximately 18–22% above comparable 99-year units in the same district and development class. The premium is most compressed in the OCR (Outer Central Region), where affordability constraints and the dominance of 99-year GLS supply have thinned the buyer pool for freehold stock. In the CCR, the premium is most pronounced because freehold supply is finite and demand from high-net-worth buyers and foreigners (who pay 60% ABSD and tend to prioritise tenure permanence) sustains elevated pricing.

However, the premium is not universal or permanent. Several factors compress it: strong new-launch condo launches on 99-year land in the same area; sentiment swings toward newer facilities over older freehold stock; and the government’s ABSD-driven cooling of foreign buyer demand since April 2023. Buyers should never assume that freehold status alone justifies a premium purchase — location, remaining lease (for 99-year comparables), age of building, and facility quality all matter more in the short-to-medium term.

Quick Reference: Land Tenure Rules at a Glance

| Rule / Parameter | 99-Year Leasehold | 999-Year / Freehold |

|---|---|---|

| Typical tenure start | Date of state grant (before developer build) | Perpetual (FH) / colonial grant (999yr) |

| CPF OA use (min remaining lease) | ≥ 20 years; prorated below 60 years | No restriction |

| Bank loan (min remaining at maturity) | ≥ 30 years (most banks) | No restriction |

| Typical PSF premium vs 99yr | Baseline | +15–25% (FH); +5–10% (999yr) |

| Value decay (Bala’s Table) | Accelerates below 60yr remaining | None |

| En bloc potential | High — developer resets to 99yr | Lower — developer pays FH premium |

| SLA lease top-up (discretionary) | Possible in select estates | N/A |

| ABSD treatment | Same as FH | Same as 99yr |

Worked Example: 99-Year vs Freehold — A Buyer’s Calculation

Mr and Mrs Wong are a Singapore Citizen couple in their early 40s, combined monthly income of S$16,000, with their HDB Minimum Occupation Period (MOP) recently cleared. They are considering two options for their first private condominium purchase in District 19:

- Option A — 99-Year Leasehold: A well-appointed 3-bedroom condominium at Serangoon, built in 2012, with approximately 85 years remaining on its 99-year lease. Asking price S$1.45M (S$1,380 psf).

- Option B — Freehold: A comparable 3-bedroom freehold condominium in the same neighbourhood, built in 2008. Asking price S$1.70M (S$1,620 psf) — a 17.2% premium over Option A.

Stamp duty comparison (both as 2nd property — ABSD remission strategy: sell HDB first):

- BSD on S$1.45M: S$43,800 (CPF). BSD on S$1.70M: S$56,800 (CPF).

- ABSD (SC 2nd property before HDB sale): S$290,000 (20%) vs S$340,000 (20%). Subject to ABSD remission if HDB sold within 6 months of purchase completion.

Bank financing: Both options qualify easily at 85 and freehold remaining lease. At 75% LTV: Option A loan S$1,087,500 @3.1% 30yr = S$4,685/mth (TDSR 29.3% — PASS). Option B loan S$1,275,000 @3.1% 30yr = S$5,497/mth (TDSR 34.4% — PASS).

20-year resale outlook: If Bala’s Table decay holds, Option A at 65 years remaining (in 20 years) retains roughly 80% of its current freehold-equivalent land value; Option B retains 100%. At a 3% compound annual capital appreciation baseline before decay effects, Option B’s perpetual tenure provides a structural hedge against the lease-decay headwind that will increasingly weigh on Option A beyond year 20.

The verdict for the Wongs: If they plan to exit within 10–12 years, Option A’s lower entry price and higher TDSR headroom make it the pragmatic choice — lease decay will be minimal in that window. If their horizon extends to 20+ years or they plan to pass the property to children, the S$250,000 upfront premium of Option B may be justified by the absent lease-decay risk.

What This Means for Buyers and Investors

For most Singaporeans whose investment horizon is under 15 years, the 99-year vs freehold debate is largely academic. In that window, location, property condition, and market sentiment dominate returns; lease decay makes only a marginal dent. The freehold premium, however, means you are paying a significant sum for insurance against a risk you may never face. The rational framework is straightforward: buy freehold if you plan to hold generational wealth or if you are purchasing in a location where supply of 99-year land is abundant and freehold is genuinely scarce. Otherwise, the 99-year product — particularly in new launches with modern facilities — offers better entry economics.

For investors targeting en-bloc exit, the calculus flips. Ageing 99-year leasehold condominiums with plot ratios below the current Master Plan allowance and lease starting to decay offer the highest en-bloc probability — developers need to reset the lease to 99 years from acquisition, making older leaseholds disproportionately attractive for collective sale. For an en-bloc investor, freehold status can actually reduce probability of a successful bid because developers pay a higher land price for equivalent redevelopment potential.

What Might Come Next: Policy and Market Outlook

Several policy trends will shape the tenure premium over the next decade. First, the government’s confirmed intent to replenish the SLA lease top-up scheme selectively — most recently applied to the Farrer Road and Boon Lay clusters — suggests that some 99-year leaseholds nearing the 40-year remaining mark may receive top-ups, partially arresting decay. However, these are discretionary, site-specific, and not widely available. Second, as Singapore’s urban redevelopment continues to pivot land away from landed and low-density uses toward mixed-use and transit-oriented development, freehold landed estates in the Core Central Region may face increasing redevelopment pressure — paradoxically making their freehold status more valuable as a negotiating chip in collective sale proceedings.

Third, the government’s ongoing review of HDB flat pricing and subsidy structures — including the HDB’s recent commentary on asset enhancement aspirations vs housing-as-a-home objectives — is likely to produce further policy signals on whether the 99-year model for public housing will be extended, supplemented, or restructured. Any formal announcement of an expanded SERS programme or a new lease buyback extension scheme would meaningfully affect the value calculus for older 99-year stock.

FAQ: Singapore Property Land Tenure

Does tenure type affect how much ABSD I pay?

Can I use my CPF OA to buy a 99-year leasehold property?

What happens when a 99-year HDB lease expires?

Is a 999-year leasehold really as good as freehold?

Can I apply to the SLA to extend my 99-year lease?

How does an en-bloc sale affect leasehold properties differently from freehold?

Does tenure matter when renting out a property?

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Property Cooling Measures Guide 2026: ABSD, TDSR, LTV and SSD Explained

- Singapore En Bloc Seller’s Guide 2026: Collective Sale Process Explained

- Singapore Property Decoupling Guide 2026: How to Save ABSD

- Singapore Joint Property Ownership Guide 2026: Joint Tenancy vs Tenancy in Common

- Singapore Property Portfolio Guide 2026: ABSD, Yields and Strategy

- Singapore Sellers’ Stamp Duty Guide 2026: SSD Rates and Exit Strategy