June 2026 BTO Launch Preview: 6,900 Flats Across 7 Projects in 5 Towns

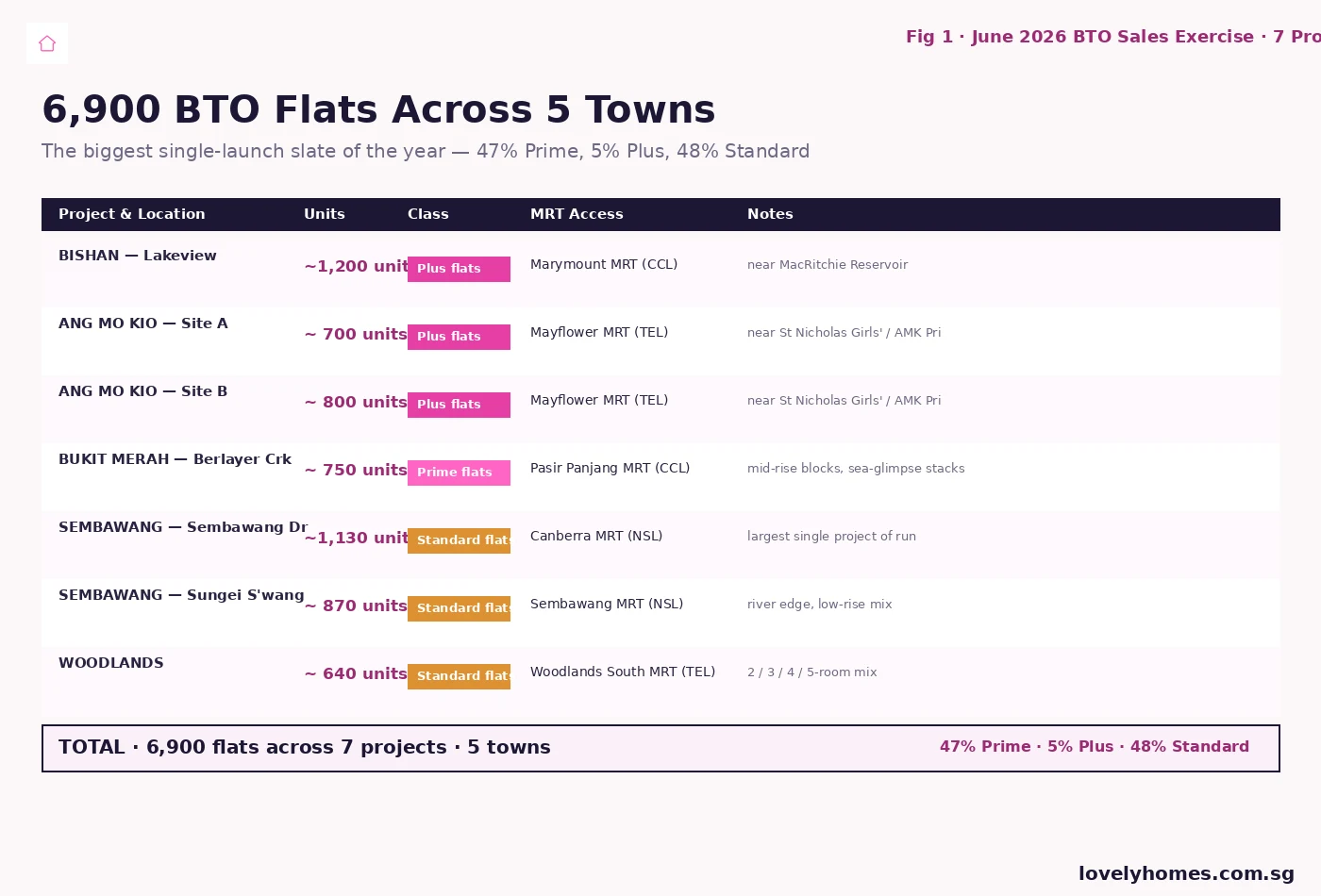

HDB has unveiled the June 2026 Build-to-Order (BTO) sales exercise — the largest single launch of the year and the broadest geographic spread Singapore has seen in the post-classification era. Roughly 6,900 flats across seven projects in five towns will go on sale in the second week of June 2026, with the headline names being the first BTO at Lakeview (Bishan) in over forty years, the Berlayer Crescent project in Bukit Merah, two Plus-class projects in Ang Mo Kio, two big-supply Standard projects in Sembawang, and a 640-unit Standard project in Woodlands. About 47% of the supply has been classified Prime, 5% Plus, and the remaining 48% Standard — which means most of June’s launches will sit under HDB’s tighter resale framework with 10-year MOP and subsidy clawback.

This preview consolidates what HDB has confirmed, what industry research desks are guiding on indicative prices, and what Lovelyhomes’ own readers are likely to weigh up before the BTO portal opens. Application closes 15 June 2026 (rounded — exact date in HDB’s portal); ballot results follow approximately three weeks later.

Quick Answer — June 2026 BTO at a glance

- Total supply: ~6,900 flats across 7 projects.

- Towns: Bishan, Ang Mo Kio, Bukit Merah, Sembawang, Woodlands.

- Mix: ~3,250 Prime (47%), ~370 Plus (5%), ~3,280 Standard (48%).

- First-of-kind: first BTO at Lakeview in over forty years; first Pasir Panjang Prime since the classification framework launched.

- Indicative 4-room price range: ~S$360k Sembawang/Woodlands → ~S$820k Bishan Lakeview, before EHG / PHG.

- MOP: 10 years (Prime, Plus); 5 years (Standard).

- Resale buyer income ceiling: S$14,000/month for Prime and Plus; none for Standard.

- Application window: opens approximately 11 June 2026; closes mid-June; ballot ~early July.

The Seven Sites

The June launch is dominated by two town clusters. The first is the Sembawang–Woodlands northern corridor, contributing roughly 2,640 of the 6,900 flats. Sembawang Drive alone is the single largest site of the run at around 1,130 units, with the smaller Sungei Sembawang project adding another ~870 units along the river edge near Sembawang MRT. Woodlands South contributes the remaining ~640 units. All three are Standard-class — the cheapest segment, the shortest MOP, and the largest pool of eligible resale buyers come 2031–32.

The second cluster is the central-mature corridor: Bishan’s Lakeview project (~1,200 units, Prime), the twin Ang Mo Kio sites near Mayflower MRT (combined ~1,500 units, Plus), and Bukit Merah’s Berlayer Crescent project near Pasir Panjang MRT (~750 units, Prime). This is where the headline-grabbing prices will sit. Indicative talk on Lakeview 4-room flats has run as high as S$820,000 before grants — a level that historically would have been a Bukit Merah or Tiong Bahru number, not a Bishan one. The Lakeview supply is the first BTO at the site since the late 1970s, and the project is positioned to be the tallest in its immediate area, with stacks oriented for MacRitchie Reservoir views.

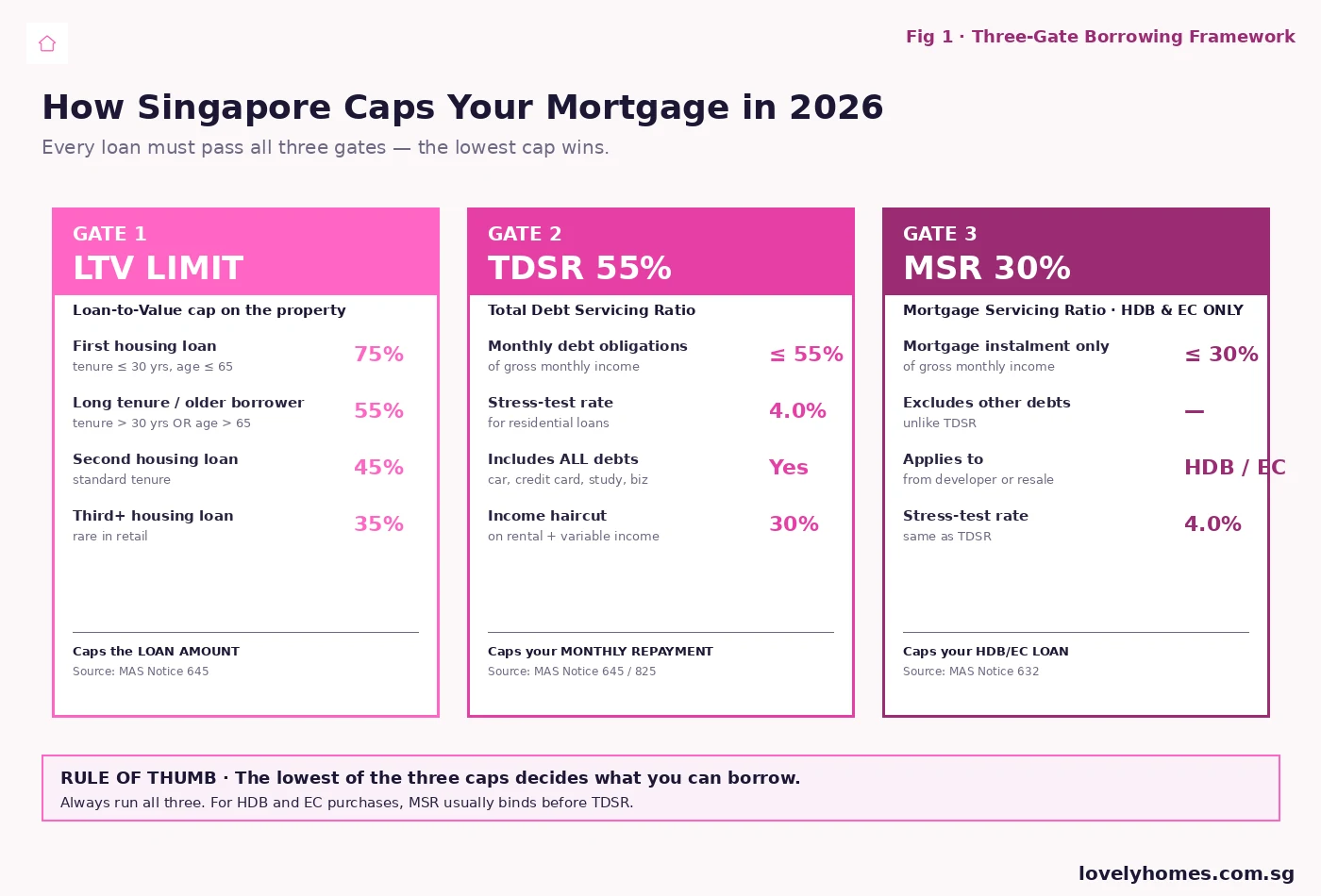

Classification — Three Different Resale Worlds

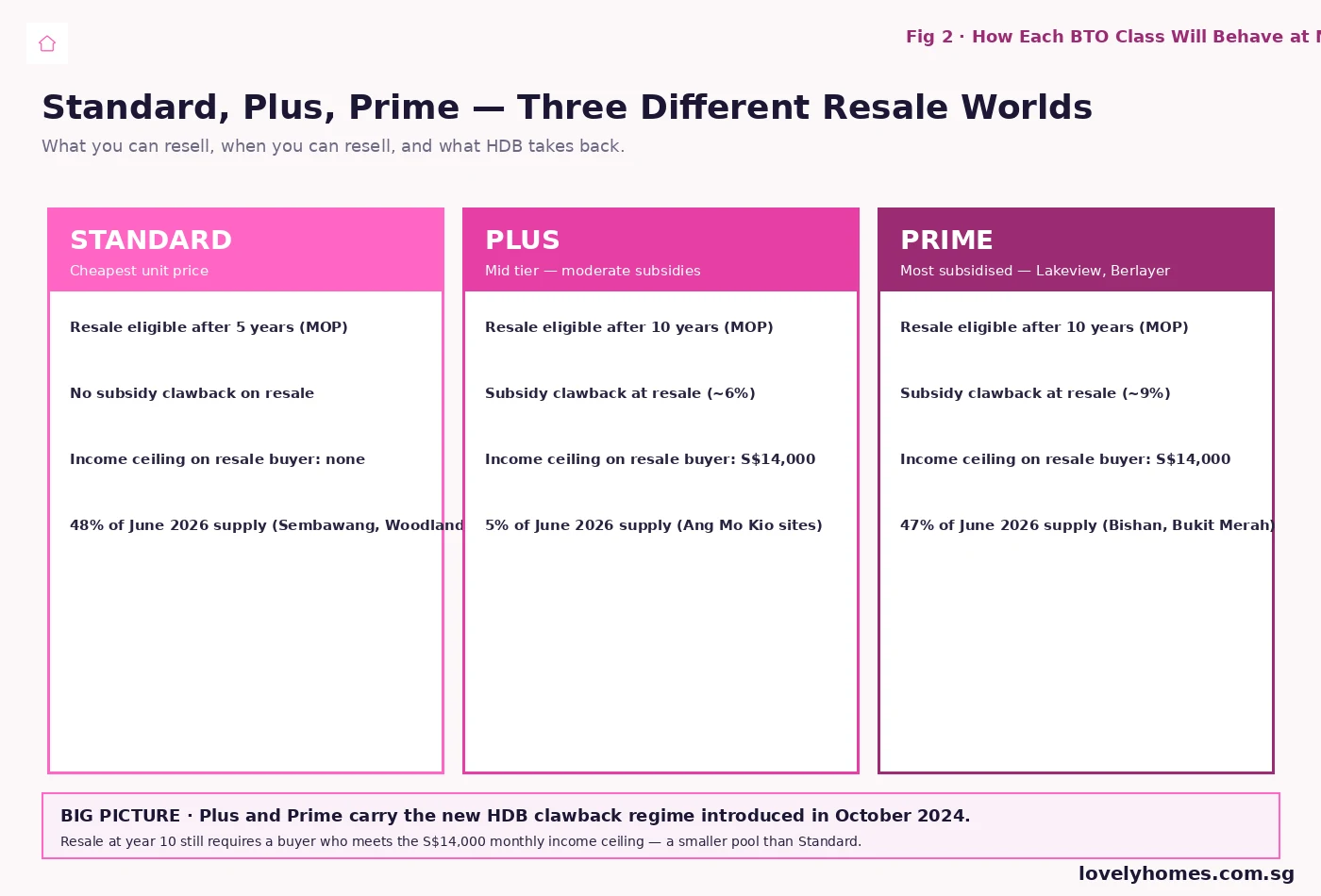

HDB’s October 2024 classification framework is in full effect for the June 2026 launch. The Standard class behaves like the BTOs of the last two decades: 5-year MOP, open resale market on graduation, no clawback. The Plus class — represented in June by the Ang Mo Kio twin — carries a 10-year MOP, a ~6% subsidy clawback at first resale, and a S$14,000 income ceiling on the resale buyer. The Prime class — Lakeview, Berlayer Crescent — runs the same 10-year MOP and S$14,000 buyer ceiling, with a heavier ~9% clawback on first resale to reflect the deeper original subsidy.

The implication for buyers is that Plus and Prime are explicitly engineered as long-hold homes with a smaller resale pool. Standard is the one that retains the historical “BTO as wealth-builder” pattern. For first-time-buyer households running the affordability vs upside arithmetic, Standard at Sembawang or Woodlands is structurally different from Prime at Bishan — even before the price difference is factored in.

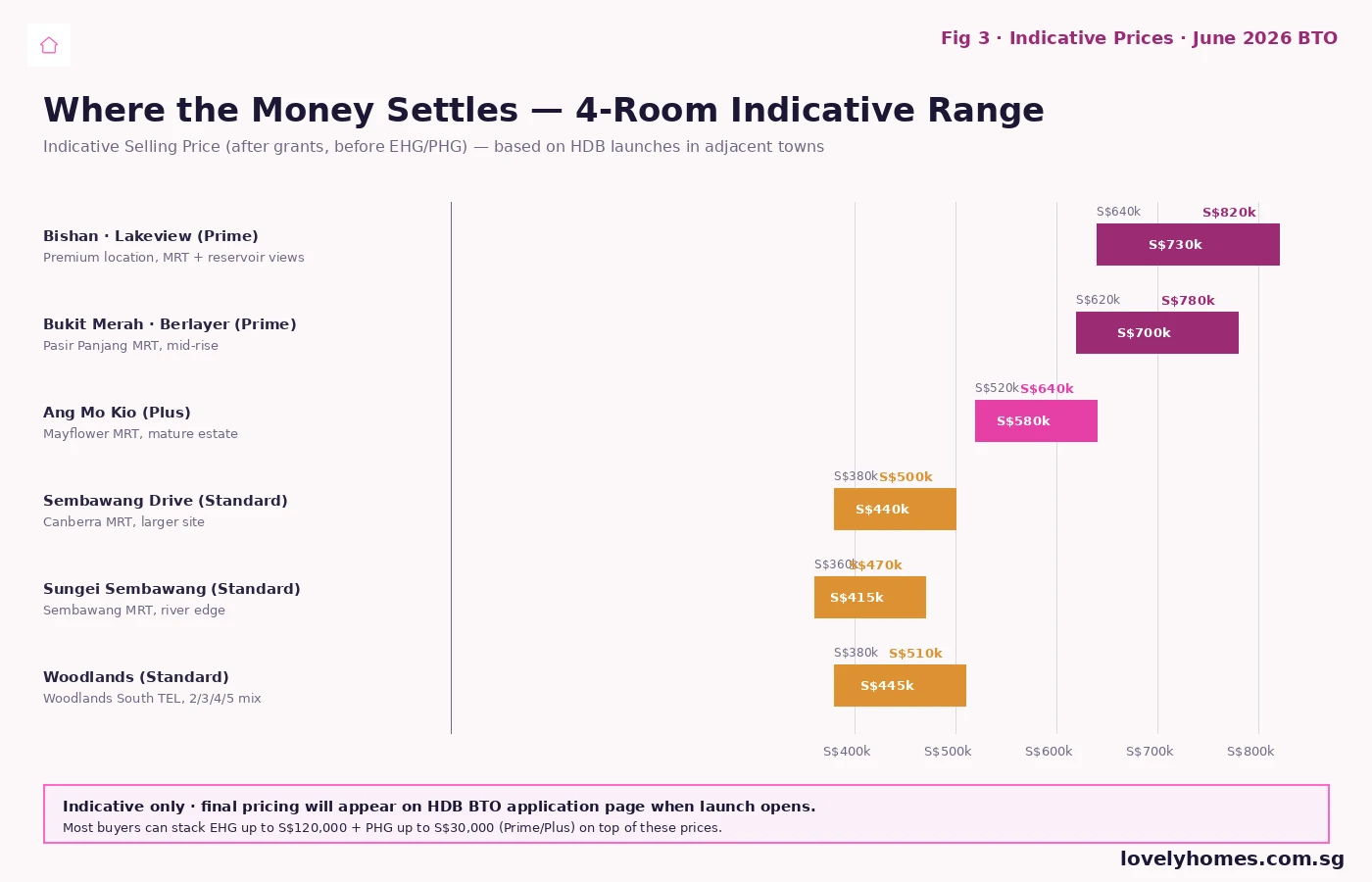

Indicative Pricing — Where the Money Lands

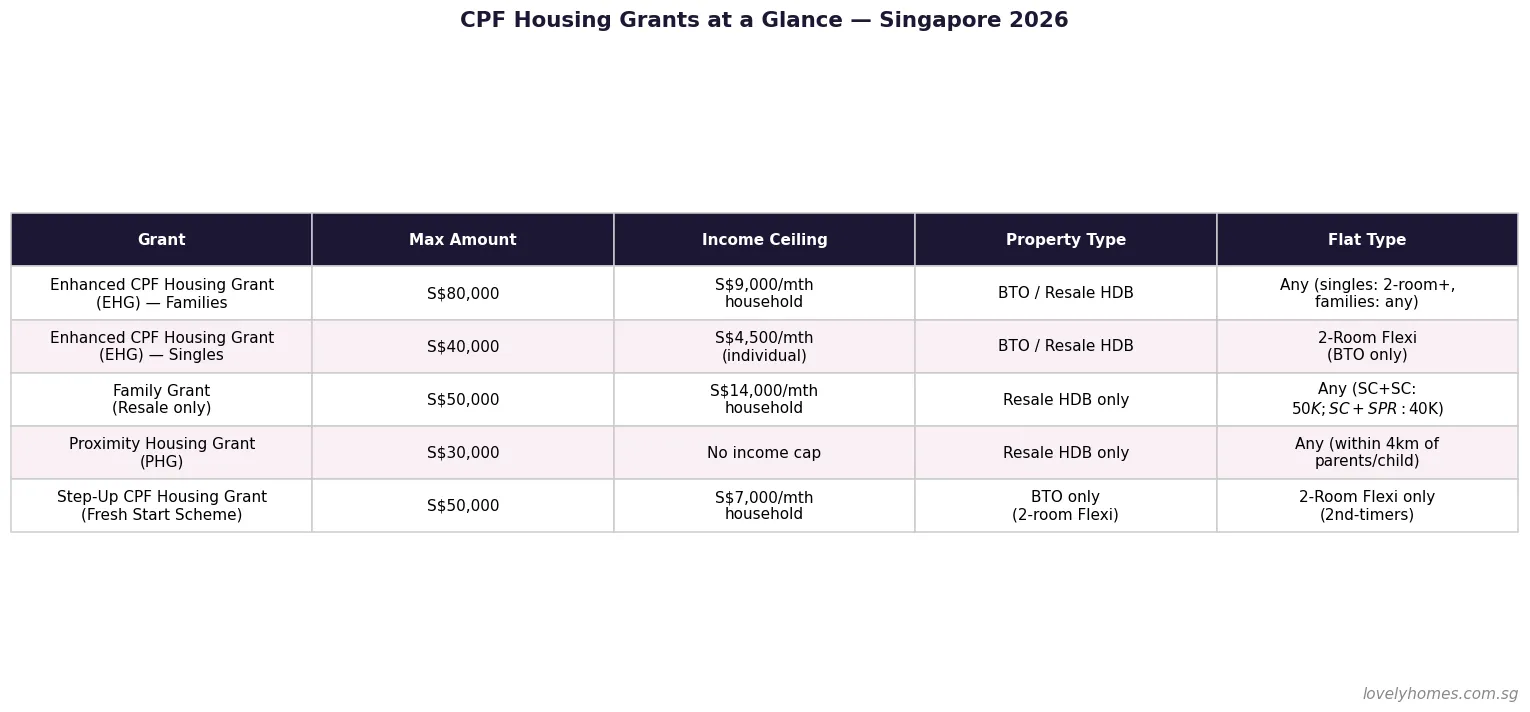

HDB will publish the firm price tables when the application window opens. The indicative ranges sit roughly as follows for 4-room flats: Bishan Lakeview at S$640,000 to S$820,000; Bukit Merah Berlayer Crescent at S$620,000 to S$780,000; Ang Mo Kio at S$520,000 to S$640,000; Sembawang sites at S$360,000 to S$500,000; Woodlands at S$380,000 to S$510,000. These are mid-launch indications drawn from neighbouring BTO comparables and the early-2026 launch curve, not committed HDB figures. The Enhanced CPF Housing Grant (EHG) of up to S$120,000 and the Proximity Housing Grant (PHG) of up to S$30,000 are still claimable on top — meaning eligible first-timer households at Sembawang could see net selling prices as low as S$240,000 for a 4-room.

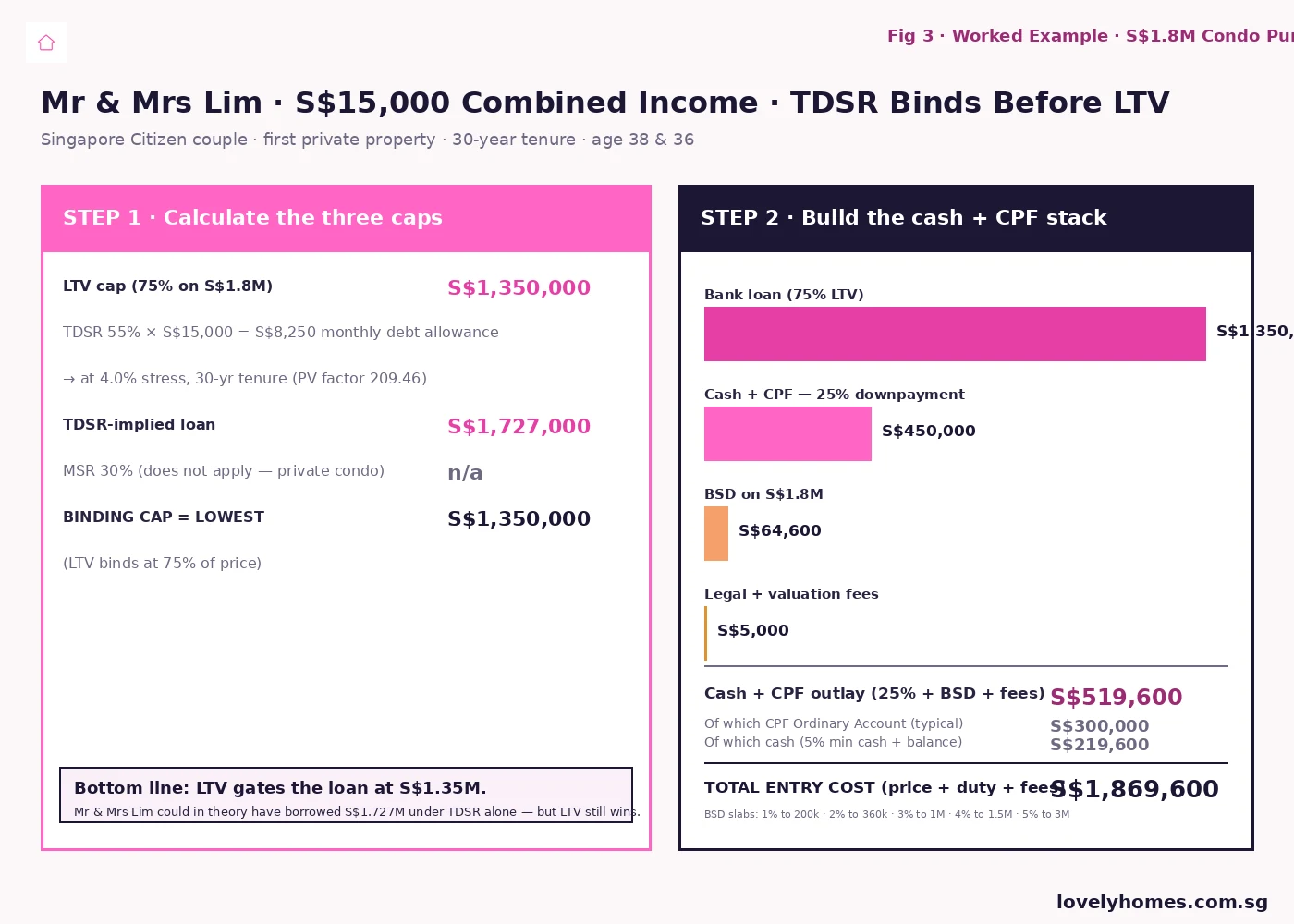

Worked Example — The Lim Household at Lakeview

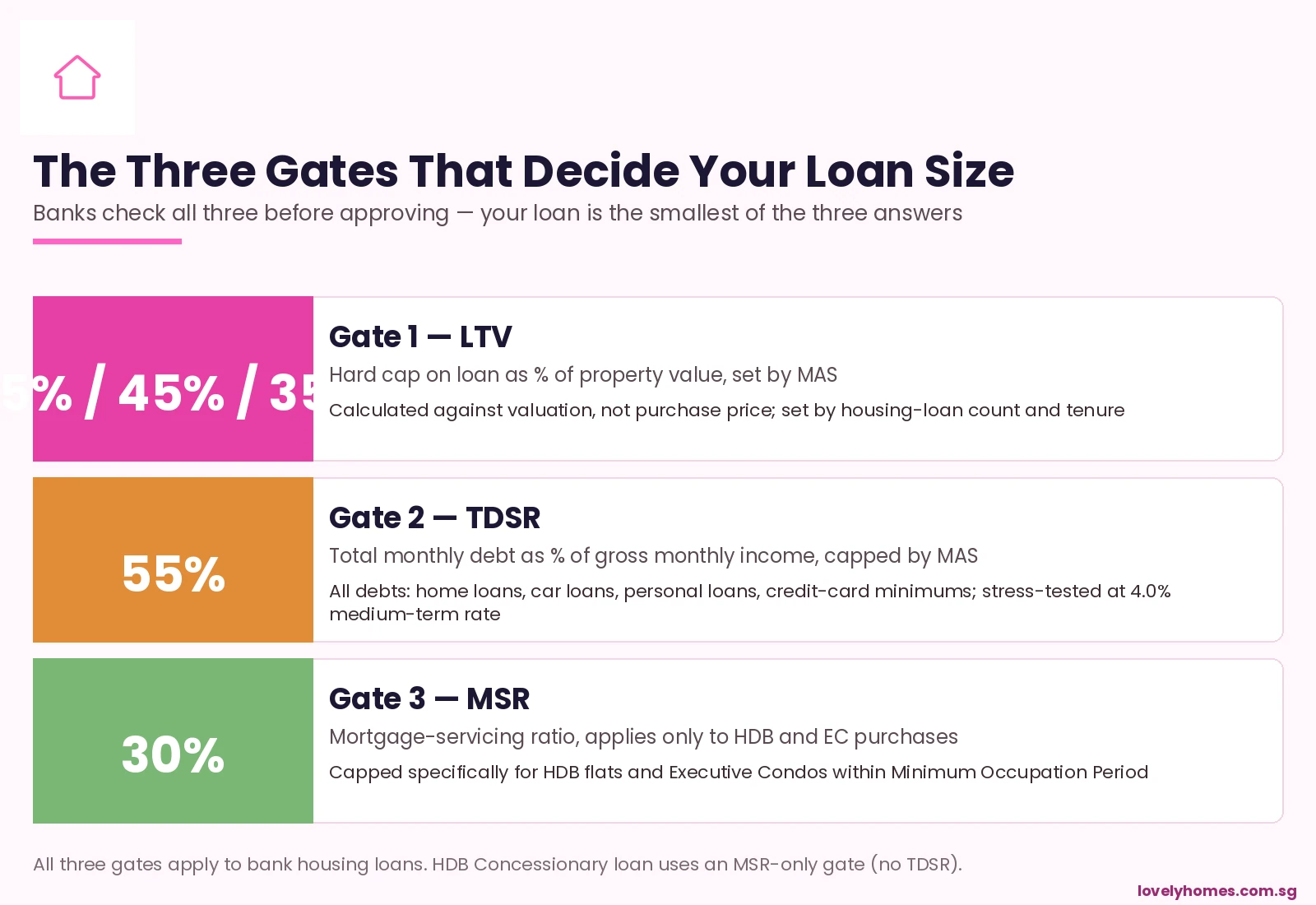

Consider Mr Lim (33) and Mrs Lim (31), Singapore Citizens, first-timers with combined gross household income S$8,500/month. They apply for a 4-room flat at the Bishan Lakeview Prime project. Indicative price: S$760,000. They qualify for EHG of S$30,000 (combined-income tier) — Prime/Plus PHG of S$30,000 if Mrs Lim’s parents live within 4km, which they do. Net price: S$700,000. CPF OA balance: S$110,000. They opt for an HDB Concessionary Loan at 80% LTV (S$560,000 loan, S$140,000 downpayment).

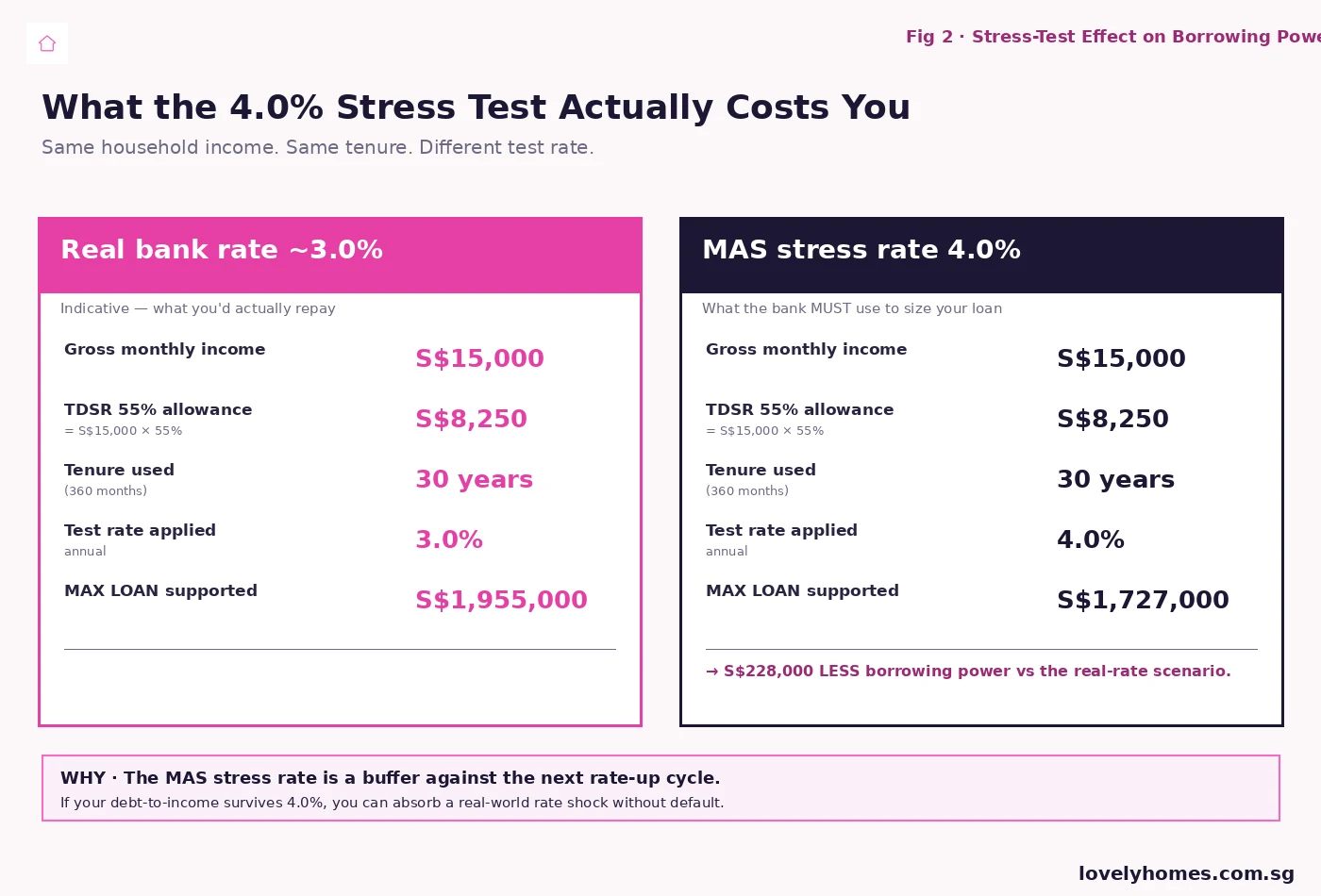

The MSR check: at HDB’s stress rate of 4%, an S$560,000 loan over 25 years yields a monthly instalment of approximately S$2,956. That is 34.8% of S$8,500 — above the 30% MSR cap. To pass MSR, they must lengthen tenure to 30 years (instalment drops to ~S$2,672 / 31.4% — still over) or accept a smaller loan (~S$481,000 / S$2,539 / 29.9% — clears MSR). The MSR is the hardest constraint here, and at S$8,500 income the Lakeview Prime price point is right at the edge of affordability. Households below S$8,000/month will struggle to pass MSR at S$760,000 even with the maximum-tenure stretch; households at S$10,000–11,000/month clear it comfortably.

What this means for the ballot: Lakeview Prime will draw a higher-income applicant pool than typical first-timer BTO. Sembawang Standard at S$420,000 list pulls a much wider applicant pool that easily clears MSR at S$5,000–6,000/month combined. Application strategy follows the price gradient.

Comparison Table — June 2026 vs Recent Quarters

| Sales Exercise | Total Flats | Towns | Prime / Plus / Standard |

|---|---|---|---|

| Feb 2026 BTO | ~5,500 | Bedok, Bukit Batok, Hougang, Tengah, Toa Payoh | ~22% / ~10% / ~68% |

| May 2026 BTO (preview) | ~3,800 | Bukit Merah, Tampines, Tengah, Woodlands | ~30% / ~12% / ~58% |

| June 2026 BTO | ~6,900 | Bishan, AMK, Bukit Merah, Sembawang, Woodlands | ~47% / ~5% / ~48% |

| Oct 2026 BTO (announced) | ~7,200 | Toa Payoh-Caldecott, Punggol, Yishun, others TBC | TBC |

What This Means for Different Buyer Profiles

First-time HDB buyer at S$5,000–7,000 combined income. Sembawang Drive, Sungei Sembawang, and Woodlands are the right fit. Standard class, 5-year MOP, prices that pass MSR comfortably with EHG-stacked subsidies. The northern corridor will face heavy first-timer demand but the supply is large enough to keep ballot odds reasonable for first-timers.

First-time HDB buyer at S$8,000–11,000 combined income. Ang Mo Kio Plus is the sweet-spot. Mature estate, MRT proximity, school catchment, and a price band that clears MSR with margin. The 10-year MOP and S$14,000 resale-buyer ceiling are real downsides if the household is upgrade-minded, but for buy-and-hold it is the strongest value-for-money in the launch.

First-time HDB buyer at S$11,000+ combined income. Bishan Lakeview and Bukit Merah Berlayer Crescent become serious. The Prime classification means the household must accept a long hold and a smaller resale pool, but the locations are in the top decile of HDB-accessible neighbourhoods. Affordability at S$760,000–820,000 only works at the higher income tier.

Second-timers and upgraders. The Plus and Prime sites apply the second-timer 70/30 quota; second-timers should expect lower ballot odds at Lakeview and Berlayer specifically. Standard sites at Sembawang and Woodlands are more accessible to second-timers because of the larger supply and the absence of the income ceiling on resale.

What Might Come Next

HDB has guided 19,600 BTO flats across 2026 (Feb + May/June + October). The October 2026 exercise is expected to be even larger than June, anchored by the Toa Payoh West / Caldecott MRT project (~1,600 flats including 240 Community Care Apartments) and supplementary supply at Punggol and Yishun. With Pearl’s Hill (60 storeys, ~1,700 flats) confirmed for the 2027 pipeline as Singapore’s tallest public housing, the next 18 months are looking like the highest-supply year of the post-COVID cycle. Whether that supply pulls down the HDB Resale Price Index — which slipped 0.1% in Q1 2026, the first quarterly decline in seven years — is the watch-point analysts will be tracking through 2H 2026.

Worked Example — Sembawang Drive Standard for the Median Household

Mr & Mrs Wong, both 30, combined income S$6,500/month, apply for Sembawang Drive Standard 4-room at indicative S$430,000. They claim EHG S$70,000 (combined income tier) — net price S$360,000. HDB Concessionary Loan at 80% LTV (S$288,000 loan; S$72,000 downpayment, fully claimable from CPF Ordinary Account). MSR at 4% / 25 years on S$288,000 = approximately S$1,521/month, which is 23.4% of S$6,500 — clears MSR with margin. TDSR not relevant for HDB Concessionary Loan. Cash outlay at completion: roughly S$5,000 of legal and stamp-duty incidentals. This is the median-income BTO arithmetic that the Standard class is engineered to deliver — and Sembawang Drive is one of the cleanest examples of it in the entire 2026 calendar.

Frequently Asked Questions

When does the June 2026 BTO application open and close?

HDB will open the application portal in the second week of June 2026, typically running for one calendar week. Ballot results follow approximately three weeks after the close. The exact dates appear on the HDB BTO application page once the launch is live; this preview was prepared from HDB’s announcement timeline and will be updated when firm dates are published.

What is the difference between Prime, Plus, and Standard?

HDB’s October 2024 framework defines three classes by location desirability and subsidy depth. Prime (~47% of June supply) carries the deepest subsidies, a 10-year MOP, a ~9% subsidy clawback on first resale, and a S$14,000/month income ceiling on the resale buyer. Plus (~5% of June supply) sits one tier below — same 10-year MOP and S$14,000 resale ceiling, with a lighter ~6% clawback. Standard (~48% of June supply) is the historical BTO model — 5-year MOP, no clawback, no resale ceiling.

Can I stack EHG and PHG on a Prime or Plus flat?

Yes. The Enhanced CPF Housing Grant (EHG) of up to S$120,000 for first-timer families is available across all three classes. The Proximity Housing Grant (PHG) of S$30,000 (married applicants living within 4km of parents) and S$10,000 (single applicants) is also available across all classes. Step-up Grant and Family Grant follow the same rules. Grant stacking does not change the MOP or clawback rules.

Why is Bishan Lakeview so much more expensive than Sembawang?

Three reasons. First, the location quality — proximity to MRT, mature estate amenities, and reservoir views — drives a higher base price band before subsidy. Second, Lakeview is Prime, which means HDB is delivering a larger absolute subsidy on a higher base price; the indicative price you see is already net of that subsidy. Third, redevelopment or land-cost factors specific to a central site push the underlying construction and tendering cost above an outer-town site like Sembawang Drive.

What is MSR and will I clear it?

MSR (Mortgage Servicing Ratio) caps your HDB or EC mortgage instalment at 30% of gross monthly income, computed at HDB’s 4% stress-test rate over your chosen tenure. For a 4-room flat at S$760,000 (Lakeview indicative) with an 80% loan and 25-year tenure, MSR clears at roughly S$8,800/month combined household income or higher. At S$420,000 (Sembawang indicative) the clear-MSR threshold drops to roughly S$5,000/month combined. See the LovelyHomes TDSR Singapore 2026 guide for the detailed mechanics.

Can I sell my Plus or Prime BTO before MOP?

Generally no. The MOP for Plus and Prime is 10 years from key collection, during which you cannot sell, rent out the entire flat, or buy a private property. Limited exceptions exist for divorce, financial hardship, and bereavement — applied case by case by HDB. Renting out individual rooms is permitted from the start, subject to HDB’s room-rental rules.

Related Articles

- Lakeview & Shunfu BTO June 2026 — the deeper review of the Lakeview project alone

- Pearl’s Hill BTO: Singapore’s Tallest Public Housing — the headline 2027 supply

- BTO May 2026 Launch Preview — the prior month’s slate

- HDB Resale Prices Slip in Q1 2026 — the demand-side context

- TDSR Singapore 2026 — the 55% income-debt cap that runs alongside MSR

- HDB Million-Dollar Flats Singapore 2026 — the resale-side context for Plus and Prime

Disclaimer: This preview is based on HDB’s published announcements and industry-research-desk indications as of 04 May 2026. Final unit counts, classifications, indicative prices, and application dates appear on the HDB BTO application page once the sales exercise opens. All figures should be verified against the official HDB website before acting on them. This guide is for general information only and does not constitute legal, tax, or financial advice. Consult a licensed mortgage broker or HDB officer for advice specific to your circumstances.