Singapore home loans are now primarily benchmarked to SORA (Singapore Overnight Rate Average) — the official replacement for SIBOR, which was phased out in December 2024.

As at May 2026, the 3-month compounded SORA is approximately 2.55%, down from its 2023 peak of above 3.7%.

Major banks offer two main packages: SORA-pegged floating rates (typically SORA + 0.85–0.90%) and fixed rates (typically 2.45–2.65% for a 2-year fixed term).

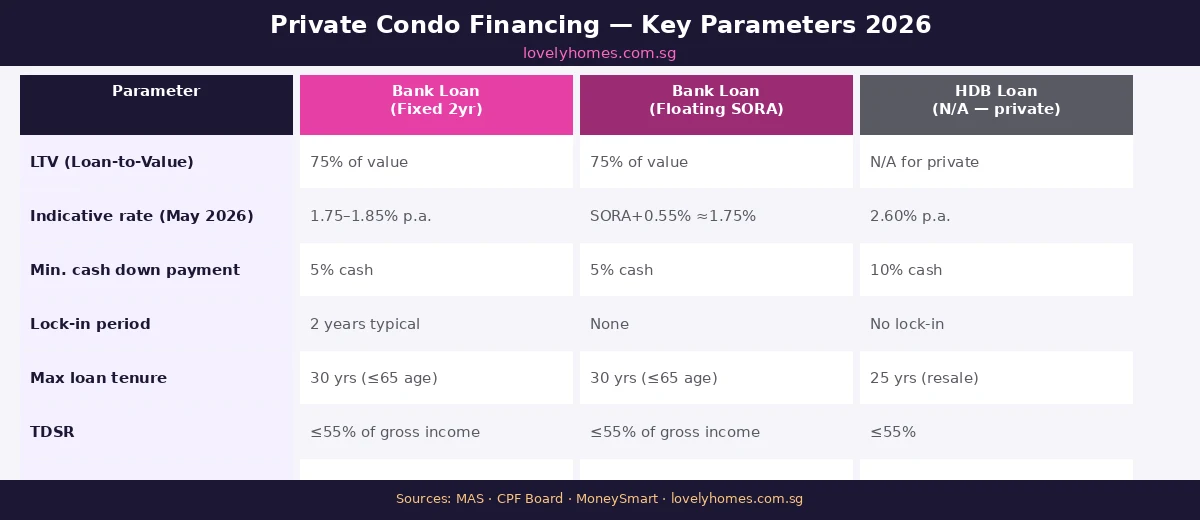

The HDB Concessionary Loan is pegged at CPF OA + 0.1%, currently 2.60%; it is available only for HDB flats and requires no lock-in period.

The Total Debt Servicing Ratio (TDSR) cap of 55% and Mortgage Servicing Ratio (MSR) cap of 30% remain in force and directly limit how much you can borrow.

Fixed rates offer payment certainty but come with a lock-in penalty (typically 1.5% of outstanding loan) if you refinance early.

SORA-pegged loans offer transparency and flexibility, but your repayment will move with rates — currently favourable as SORA trends down from its 2023 highs.

Understanding Singapore Home Loan Interest Rates in 2026

When you take out a home loan in Singapore, the single most consequential variable is the interest rate. On a S$1 million loan over 25 years, the difference between a 2.45% and a 3.40% rate translates to roughly S$470 more per month — or over S$140,000 in additional interest over the life of the loan. Yet many buyers in Singapore choose their home loan based on convenience, the advice of a mortgage broker with a vested interest, or simply whatever their bank’s relationship manager recommends at point of sale.

This guide explains how Singapore home loan interest rates are structured in 2026, what SORA is and why it replaced SIBOR and SOR, how to read bank package offers correctly, and how to decide between a floating rate and a fixed rate package given the current interest rate environment. It is written for Singaporean and Permanent Resident property buyers — the same principles apply to foreigners but their ABSD liability fundamentally alters the financing calculus.

Monetary Authority of Singapore (MAS) regulates home lending in Singapore under the Monetary Authority of Singapore Act and the Notice MAS 632 on Residential Property Loans. HDB administers the Concessionary Loan under the Housing and Development Act.

Figure 1: SORA 3-Month Compounded Average vs 2-year Fixed Rate — Major Singapore Banks, 2020–2026. Data: MAS, bank publications.

What Is SORA and Why Did It Replace SIBOR?

SORA — the Singapore Overnight Rate Average — is the volume-weighted average rate of all overnight unsecured Singapore dollar interbank transactions brokered in Singapore between 08:00 and 18:15 each business day. It is published daily by MAS and is calculated retrospectively, which makes it a backward-looking, transaction-based benchmark rather than a quote-based one like SIBOR was.

SIBOR (Singapore Interbank Offered Rate) was phased out on 31 December 2024 following a global reform of interest rate benchmarks prompted by the 2012 LIBOR manipulation scandal. SOR (Swap Offer Rate), which was partly based on USD LIBOR, was discontinued even earlier. MAS and the Steering Committee for SOR & SIBOR Transition to SORA (SC-STS) oversaw the transition, which required all existing SIBOR-pegged mortgages to be converted to SORA-linked packages by end-2024.

SORA is now used in three primary forms for home loans:

1-Month Compounded SORA (1M SORA) — reflects the past 30 days of overnight rates. More reactive to short-term rate changes.

3-Month Compounded SORA (3M SORA) — reflects the past 90 days. More commonly used by banks for home loans; provides a slightly smoother signal.

SORA Board Rates — some banks (notably UOB) have internal board rates that are partially informed by SORA movements but give the bank more discretion over repricing.

SORA-Pegged Floating Rate Packages

A SORA-pegged floating rate package ties your home loan to the prevailing 3M Compounded SORA, plus a fixed spread set by the bank. As at May 2026, spreads across major banks range from +0.85% to +0.90%:

DBS: 3M Compounded SORA + 0.85%

OCBC: 3M Compounded SORA + 0.88%

UOB: 3M Compounded SORA + 0.90%

Maybank: 3M Compounded SORA + 0.85%

With 3M SORA at approximately 2.55% in May 2026, an all-in floating rate works out to roughly 3.40–3.45%. This is broadly similar to the prevailing 2-year fixed rate, which sits at 2.45–2.65% for Year 1–2 before typically reverting to a board rate or SORA-linked rate from Year 3.

The key characteristics of a SORA floating package are:

No lock-in period — you can refinance or reprice at any time without a penalty clause.

Transparent repricing — your rate changes as SORA moves, typically with a 1-month lag for 1M SORA packages or a 3-month lag for 3M packages.

Currently in a declining environment — if MAS and the Federal Reserve continue rate normalisation through 2026, SORA is expected to drift toward 2.2–2.4% by end-2026, which would bring all-in floating rates to around 3.05–3.30%.

Figure 2: Singapore Home Loan Package Comparison — DBS, OCBC, UOB, HDB Concessionary Loan and others, May 2026. Rates indicative; verify with lender.

Fixed Rate Packages

Fixed rate packages lock in an interest rate for a specified period — typically 2 years — after which the loan reverts to a floating rate, usually SORA-linked or a bank board rate. As at May 2026, major banks are offering:

Bank

Year 1

Year 2

Year 3+

Lock-in

DBS

2.45%

2.55%

FHR8 (board rate)

2 years

OCBC

2.50%

2.60%

OHR+ (SORA-linked)

2 years

UOB

2.45%

2.55%

SORA + spread

2 years

Standard Chartered

2.48%

2.60%

Board rate

2 years

Maybank

2.50%

2.65%

SORA + spread

2 years

The 2-year fixed period provides payment certainty — you know exactly what you will pay every month for the fixed term, which makes household budgeting straightforward. The risk is that if you need to refinance during the lock-in window — for example, because you sell the property, or a better package becomes available — you will typically pay a penalty of 1.50% of the outstanding loan amount at the time of early redemption.

On a S$1 million loan, that penalty is S$15,000. This is not an insignificant sum, and it is the primary reason experienced property investors often prefer no-lock-in floating packages despite the slightly higher all-in rate today.

The HDB Concessionary Loan — A Third Option

Buyers purchasing an HDB flat have access to a third option: the HDB Concessionary Loan, currently at a flat 2.60% per annum. This rate is set at CPF Ordinary Account interest rate (currently 2.5%) plus 0.1%, and is reviewed quarterly. It has remained at 2.60% since January 2023 when the CPF OA rate was last adjusted.

The HDB Concessionary Loan is notable for several reasons:

No lock-in — you can switch to a bank loan at any time without penalty.

LTV up to 80% — the maximum Loan-to-Value for an HDB loan is 80% of the purchase price or valuation (whichever is lower), versus 75% for a bank loan.

No cash down payment requirement — the 20% down payment can be funded entirely from CPF Ordinary Account (unlike bank loans, which require at least 5% in cash).

Eligibility conditions — all owners must not own any other residential property; income ceiling of S$14,000 household income applies for most flat types (no ceiling for HDB resale). You must obtain an HDB Flat Eligibility (HFE) Letter before exercising an OTP.

TDSR and MSR — How Much Can You Borrow?

MAS introduced the Total Debt Servicing Ratio (TDSR) framework in June 2013 to ensure borrowers do not over-leverage. TDSR limits total monthly debt obligations (including the new mortgage, car loans, personal loans, credit card minimum payments and all other credit facilities) to 55% of gross monthly income. Banks apply a stress-test rate of 4.0% per annum when assessing TDSR — meaning they calculate your hypothetical monthly payment at 4.0% regardless of the prevailing rate, to ensure you can afford the loan even if rates rise.

For HDB flat purchases (both BTO and resale), the additional Mortgage Servicing Ratio (MSR) cap applies: your monthly mortgage payment must not exceed 30% of gross monthly income. MSR applies to the actual servicing payment, not a stress-tested figure.

These rules mean that on a gross household income of S$10,000 per month, the maximum monthly mortgage payment you can qualify for (under MSR for HDB) is S$3,000; and the maximum all-debt obligation under TDSR is S$5,500. Practically, if you have a car loan of S$800/month, your maximum mortgage under TDSR is reduced to S$4,700/month.

Figure 3: Monthly Repayment by Rate Scenario — S$1M Loan, 25-Year Tenure. Illustrative; based on standard annuity formula.

Worked Example — The Tan Family’s Loan Decision

Mr and Mrs Tan are Singapore Citizens purchasing a S$1.4 million OCR condominium in Tampines in June 2026. They are first-time buyers with no outstanding home loans. Their gross combined household income is S$14,000 per month. They have S$180,000 in CPF OA (combined) and S$100,000 in cash savings.

Loan quantum: 75% LTV on S$1.4M = S$1.05M bank loan. Down payment = S$350,000 (25%), of which at least S$70,000 (5%) must be in cash. The Tans comfortably clear this with S$70,000 cash + S$280,000 CPF.

BSD: S$24,600 on S$1.4M (first S$180k at 1%, next S$180k at 2%, next S$640k at 3%, remaining S$400k at 4% — total S$1,800 + S$3,600 + S$19,200 = wait, let me compute correctly: BSD on S$1.4M = 1%×S$180k + 2%×S$180k + 3%×S$640k + 4%×S$400k = S$1,800 + S$3,600 + S$19,200 + S$16,000 = S$40,600). ABSD: S$0 (first purchase, SC).

Rate comparison:

Option A — 2-year fixed at 2.45%/2.55%: Monthly in Year 1 = S$4,634; Year 2 = S$4,706. Reverts to SORA + spread from Year 3 (est. ~S$4,500–4,800 depending on SORA trajectory). Lock-in penalty if exit before 24 months: ~S$15,750 (1.5% × S$1.05M).

Option B — SORA float at SORA+0.85% ≈ 3.40%: Monthly = ~S$5,161. No lock-in. If SORA falls to 2.2% by end-2026, rate drops to ~3.05%, monthly ~S$4,956.

Option C — If they were buying an HDB resale (for illustration): HDB Concessionary Loan at 2.60% → monthly ~S$4,748 on S$1.05M, 80% LTV available.

TDSR check (Option A, Year 1): Monthly payment S$4,634. With no other debts, TDSR = S$4,634 ÷ S$14,000 = 33.1%. Well within 55%. Stress-tested at 4.0%: hypothetical monthly = S$5,534; TDSR = 39.5%. PASS.

Recommendation: Given the declining SORA environment in 2026, the Tans opt for Option A (2-year fixed) to lock in payment certainty during the early years of ownership when their cash position is most stretched. They set a calendar reminder to review and refinance in Month 20, before the lock-in expiry.

Fixed vs Floating — How to Decide in 2026

With fixed and floating rates now converging at around 3.35–3.50% all-in, the classic argument — “floating is cheaper, fixed is certain” — no longer cleanly applies. The decision framework for 2026 hinges on three questions:

How long will you hold the property? If you plan to sell within 3 years (e.g., you are buying a resale flat as a stepping stone and expect to MOP a BTO), a floating package with no lock-in avoids the exit penalty. If you plan to hold for 10+ years, the 2-year fixed-then-float cycle is largely a moot point — both packages will track the same rates over the long run.

How sensitive is your monthly budget to rate moves? If a S$300–500 increase in monthly repayment would significantly stress your household, a fixed rate gives you a planning buffer. If you have comfortable headroom under TDSR, floating is fine.

What is the SORA outlook? As at May 2026, MAS and market consensus lean toward SORA continuing a gradual decline through 2026–2027 as the global rate cycle normalises. In a declining rate environment, locking in at today’s fixed rate means you may pay slightly more than the eventual SORA level. However, the gap is likely to be narrow (0.10–0.30%) and the certainty premium may be worth it for first-time buyers.

What Might Come Next — Singapore Loan Rate Outlook

Several factors will shape Singapore home loan rates through end-2026 and into 2027. MAS operates a unique monetary policy framework — it manages the Singapore dollar nominal effective exchange rate (S$NEER) rather than directly setting an overnight rate, meaning SORA is market-determined rather than policy-set. However, SORA is strongly correlated to the US federal funds rate through Singapore’s open capital account.

The US Federal Reserve has signalled two 25-basis-point cuts in the second half of 2026, which, if executed, would likely push 3M SORA from ~2.55% toward ~2.05–2.15% by year-end. This would bring SORA-pegged all-in rates to around 2.90–3.05% — meaningfully below today’s fixed rates of 2.45–2.65% over a 2-year view. Whether banks adjust their fixed rate offerings in anticipation remains to be seen; historically, fixed rates tend to reprice down with a 1–2 quarter lag.

Summary — Home Loan Rate Comparison at a Glance

Feature

SORA Float

Fixed Rate (2yr)

HDB Concess.

All-in Rate (May 2026)

~3.40%

2.45–2.65%

2.60%

Rate Certainty

None

2 years

Stable (CPF+0.1%)

Lock-in Period

None

2 years

None

Exit Penalty

None

~1.5% of loan

None

Max LTV

75%

75%

80%

Min Cash Down

5%

5%

0% (CPF ok)

Eligible Properties

All

All

HDB only

Best For

Flexible holders; declining rate bet

First-timers; budget certainty

HDB buyers; tight cash

Frequently Asked Questions

What is SORA and how is it different from SIBOR?

SORA (Singapore Overnight Rate Average) is the volume-weighted average of unsecured overnight interbank SGD transactions, published daily by MAS. SIBOR was a forward-looking rate based on bank submissions — susceptible to manipulation, as the 2012 LIBOR scandal revealed globally. SORA is transaction-based and backward-looking, making it more robust and harder to manipulate. SIBOR was fully discontinued on 31 December 2024; all SIBOR-pegged mortgages were converted to SORA or fixed-rate packages during 2023–2024.

Should I choose a fixed or floating rate home loan in 2026?

With SORA declining toward 2.2% by end-2026 and fixed rates at 2.45–2.65%, the all-in rates are converging. For first-time buyers who need budgeting certainty, a 2-year fixed rate is sensible — it protects against any short-term rate surprise and costs only marginally more than today’s floating all-in rate. For investors and experienced buyers who plan to hold long-term or who may sell within 3 years, a no-lock-in SORA floating package avoids exit penalties and will benefit as SORA falls further. In 2026 specifically, the edge is modest either way; the bigger decision is the property itself.

What is the current SORA rate in 2026?

As at May 2026, the 3-month compounded SORA is approximately 2.55% per annum, down from its peak of above 3.74% in mid-2023. It has been declining steadily as the US Federal Reserve began its rate normalisation cycle in late 2024. MAS publishes daily SORA rates on its website at mas.gov.sg/monetary-policy/sora.

What is TDSR and how does it affect how much I can borrow?

The Total Debt Servicing Ratio (TDSR) limits your total monthly debt obligations (including the home loan, car loans, personal loans and other credit facilities) to 55% of your gross monthly income. Banks stress-test your loan at 4.0% per annum when assessing TDSR eligibility — so even if the prevailing rate is 3.0%, the bank calculates whether you could afford the repayment at 4.0%. On top of TDSR, if you are buying an HDB flat, the Mortgage Servicing Ratio (MSR) limits your monthly home loan repayment to 30% of gross monthly income.

Can I use CPF to pay my home loan?

Yes. CPF Ordinary Account savings can be used to service monthly home loan repayments for both HDB flats and private properties, subject to the Valuation Limit (generally the lower of the purchase price or valuation) and the Withdrawal Limit (up to 120% of the Valuation Limit for private properties). Note that CPF monies withdrawn for property earn accrued interest at 2.5% per annum, which must be returned to your CPF account upon sale. This accrued interest does not represent an additional out-of-pocket cost but reduces the net cash proceeds you receive when you sell.

What is a lock-in period and what happens if I break it?

A lock-in period is a contractual commitment to maintain your loan with the same bank for a set duration — typically 2 years for fixed rate packages. If you refinance, prepay or redeem the loan in full before the lock-in expires, you pay a penalty usually equal to 1.5% of the outstanding loan amount at the time of early redemption. On a S$900,000 outstanding balance, that is S$13,500. No-lock-in packages (all SORA floating packages and HDB Concessionary Loans) allow you to exit or refinance at any time without penalty.

What is the difference between refinancing and repricing?

Repricing is when you switch to a different loan package within the same bank — typically cheaper (no legal or valuation fees) but limited to that bank’s available packages. Refinancing is when you move your loan to a different bank entirely. Refinancing typically offers access to sharper rates but incurs legal fees (S$2,000–3,500), valuation fees (S$300–800), and potentially a clawback of cashback incentives if you refinance within the clawback period (usually 3 years). Both options are typically considered when a fixed rate lock-in expires.

This article is for general informational purposes only and does not constitute financial or legal advice. Interest rates quoted are indicative as at May 2026 and are subject to change by individual lenders. The SORA rate is published daily by MAS and can be found at mas.gov.sg. TDSR and MSR rules are set by MAS and are subject to regulatory revision. For personalised advice on home loan selection and eligibility, consult a licensed financial adviser or mortgage specialist regulated by MAS. All stamp duty computations are based on IRAS published rates at iras.gov.sg. HDB Concessionary Loan eligibility criteria are set by HDB and available at hdb.gov.sg. CPF rules on property usage are administered by the CPF Board at cpf.gov.sg.

ABSD Singapore — short for Additional Buyer’s Stamp Duty — is the single largest upfront cost most buyers face when purchasing a second (or third, or fourth) residential property in Singapore. If you are buying as a foreigner, ABSD can add 60% of the purchase price to your cost. If you are a Singapore Citizen buying your second property, that figure is 20%. Get this number wrong in your budgeting, and you can very quickly wipe out years of planning.

This guide walks you through exactly how ABSD works in 2026 — who pays, how much, how it is calculated, what remissions are available, and the legitimate strategies property buyers use to manage it. All figures reflect the Government’s 27 April 2023 cooling measures, which remain the applicable framework. For the latest rates, always check the IRAS Additional Buyer’s Stamp Duty page.

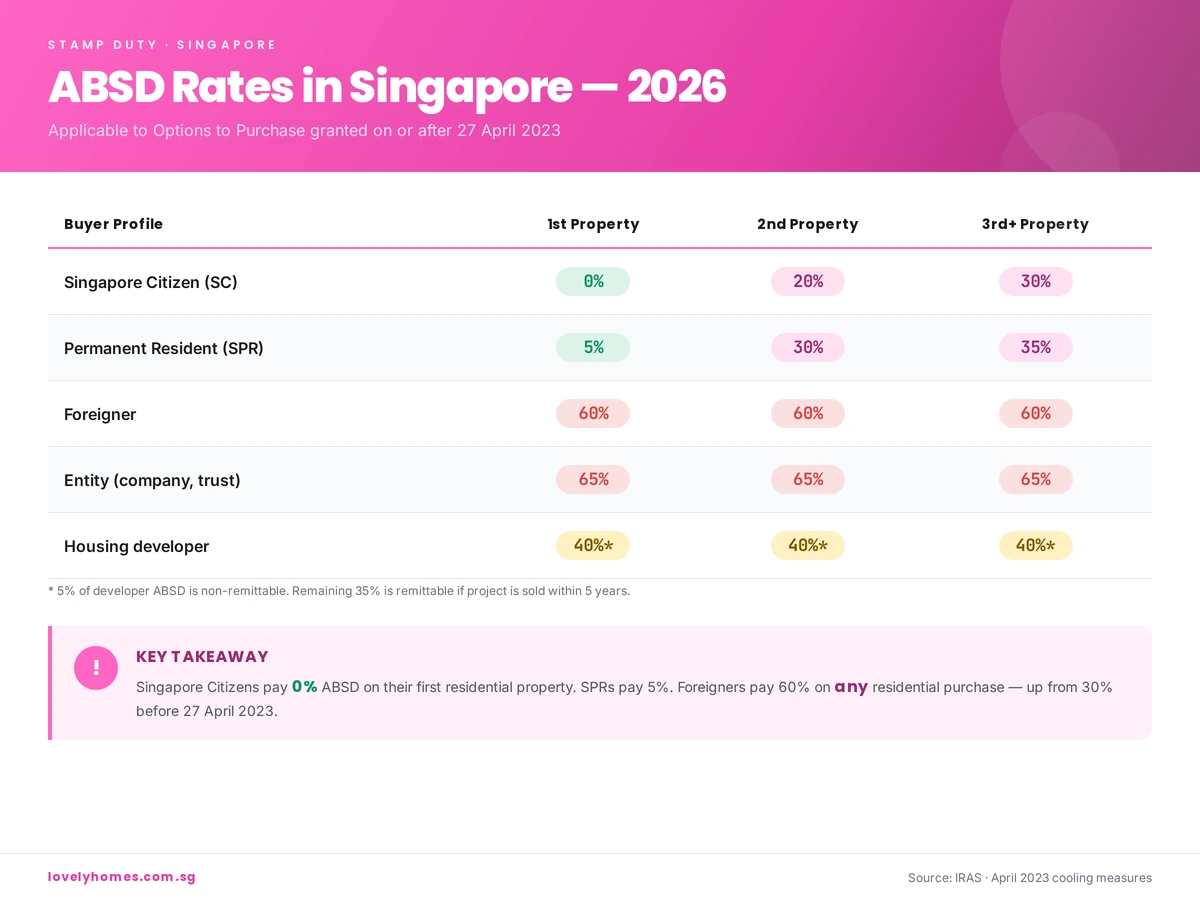

Quick Answer — ABSD at a glance

Singapore Citizens: 0% on 1st property, 20% on 2nd, 30% on 3rd+

Singapore PRs: 5% / 30% / 35%

Foreigners: 60% on any residential property

Companies, trusts and other entities: 65%

ABSD is payable within 14 days of signing the Option to Purchase (OTP) or Sale & Purchase Agreement.

What is ABSD and Why Does It Exist?

ABSD is a transaction tax levied on the buyer when acquiring a residential property in Singapore. It sits on top of the regular Buyer’s Stamp Duty (BSD) that every buyer pays. Where BSD is progressive and maxes out at 6% for the portion of price above S$3 million, ABSD is a flat rate applied to the entire purchase price or market value (whichever is higher).

The tax was introduced in December 2011 as part of the Government’s suite of cooling measures — the tools Singapore uses to moderate speculative demand, manage affordability for owner-occupiers, and prevent the kind of runaway price inflation seen in other global cities. Because it targets second-and-subsequent-property buyers and non-citizens disproportionately, ABSD is the single most powerful lever in the cooling-measures toolbox. You can read more about the broader framework in our Property Cooling Measures section.

ABSD Rates in Singapore (2026)

The table below sets out the ABSD rates currently in force. Rates apply based on the profile of the buyer at the time the Option to Purchase (OTP) is granted.

ABSD rates by buyer profile — applicable to OTPs granted on or after 27 April 2023.

Buyer Profile

1st Residential Property

2nd Residential Property

3rd & Subsequent

Singapore Citizen (SC)

0%

20%

30%

Singapore Permanent Resident (SPR)

5%

30%

35%

Foreigner (non-PR individual)

60%

60%

60%

Entity (e.g. company, trustee for a trust)

65%

65%

65%

Housing developer

40%*

40%*

40%*

* 5% of a developer’s ABSD is non-remittable. The remaining 35% is remittable subject to conditions, including selling all units in a qualifying project within five years.

How ABSD is Calculated — A Worked Example

ABSD is applied to the higher of the purchase price or the market value of the property. It is not charged on a tiered basis — the full rate applies to the entire amount.

Example: A Singapore Citizen couple already owns their first home (a 4-room HDB flat). They decide to buy a S$2,000,000 resale condominium in District 15 as an upgrader investment. ABSD on the second property for a Singapore Citizen is 20%.

Purchase price: S$2,000,000

ABSD (20%): S$400,000

BSD (progressive, on S$2m): approximately S$64,600

Total stamp duty payable: S$464,600

That S$400,000 ABSD alone would consume most of the typical upgrader’s CPF and cash reserves. This is why many Singaporean couples take the ‘sell first, buy second’ upgrade route — selling the existing HDB or condo before buying the next home — which we cover later in this guide.

Who Pays ABSD? Exemptions and Special Cases

ABSD applies when you purchase an additional residential property. Commercial property, industrial property, and pure-land parcels are not within its scope. A property is counted toward your “property count” if:

You hold the title as a sole owner, joint tenant, or tenant-in-common;

You are a beneficial owner via a trust;

You are a beneficiary of an estate that holds residential property.

Properties not counted include: properties you merely reside in but do not own (e.g. as a tenant), inherited shares in a deceased estate within the administration period, and certain industrial/commercial units.

Executive Condominiums (ECs)

For new ECs bought directly from the developer during the minimum occupation period of the scheme, ABSD is not triggered because the buyer must commit to an owner-occupier arrangement. ABSD rules apply normally if an EC is purchased on the resale market after its 5-year MOP and 10-year privatisation milestones.

Free Trade Agreement (FTA) Nationals

Citizens and Permanent Residents of countries with which Singapore has an FTA extending National Treatment on stamp duty — namely Iceland, Liechtenstein, Norway, Switzerland, and United States citizens — are accorded the same ABSD treatment as Singapore Citizens. An eligible US citizen buying their first Singapore residential property therefore pays 0% ABSD, not 60%.

ABSD Remission Schemes — How to Get Some (or All) of It Back

Several remission schemes let qualifying buyers claim back part or all of the ABSD they initially pay. The big three to know are:

1. Married Couple Remission (Sale of First Residential Property)

If a Singapore Citizen (or mixed SC & SPR, SC & foreigner) couple buys a replacement home before selling their existing one, they can apply for ABSD remission provided they sell the first property within six months of the later of (a) the date of purchase of the replacement property, or (b) the TOP/CSC date if buying an uncompleted unit. This is effectively a “grace period” that allows upgraders to move without double-paying ABSD.

2. Mixed-Nationality Married Couples

An SC spouse married to a foreigner buying a matrimonial home jointly can enjoy SC rates (rather than foreigner rates) if the property will be used as their matrimonial home and conditions are met. Again, for a first joint home this means 0% ABSD.

3. Developer ABSD Remission

Licensed housing developers pay 40% ABSD upfront (5% non-remittable, 35% remittable) on land purchased for residential development. The 35% is remittable upon meeting development and sales conditions — typically completing the project and selling all units within 5 years.

Remissions must be applied for within strict timeframes (usually 14 days of the triggering event). We strongly recommend engaging a conveyancing lawyer who is experienced in stamp-duty remission applications before signing any OTP where remission will be relied upon.

ABSD vs BSD: What is the Difference?

Every property purchase in Singapore attracts Buyer’s Stamp Duty (BSD), which is a progressive tax on the purchase price:

1% on the first S$180,000

2% on the next S$180,000

3% on the next S$640,000

4% on the next S$500,000

5% on the next S$1,500,000

6% on the portion above S$3,000,000 (residential only)

BSD applies to every buyer; ABSD is the additional layer that may or may not apply depending on your citizenship status and property count. BSD and ABSD are payable together, within 14 days of signing the OTP.

The History of ABSD in Singapore (2011–2026)

Understanding how we arrived at today’s ABSD rates helps you anticipate where the Government may go next. The key milestones:

December 2011: ABSD introduced. Foreigners paid 10%; entities 10%; SPRs 3% on 2nd property; SCs 3% on 3rd+.

January 2013: First major hike. Foreigners to 15%, entities 15%, SPRs 5%/10%, SCs 7%/10% on 2nd/3rd.

July 2018: Rates raised again amid a reflating market. Foreigners to 20%, entities to 25%.

December 2021: Another round. Foreigners to 30%, entities to 35%, SPR 2nd property to 25%, SC 2nd to 17% / 3rd to 25%.

April 2023: The current regime. Foreigners doubled to 60%, entities to 65%, SPR 2nd to 30%, SC 2nd to 20%.

Each tightening has coincided with a period of accelerating private-residential price growth. For a full chronology including LTV, SSD and TDSR changes, see our comprehensive Property Cooling Measures archive.

How to Legally Minimise Your ABSD Bill

ABSD is not optional, but there are a handful of legitimate strategies buyers use to reduce the amount payable or to avoid triggering higher rates:

Sell first, then buy. For couples upgrading, timing the sale of your existing HDB or condo before the purchase of the next means you never hold two properties simultaneously and therefore pay 0% ABSD on the new first home (as an SC).

Use the matrimonial home remission. A mixed SC–foreigner couple buying their matrimonial home jointly enjoys SC rates if structured correctly.

Decouple responsibly. Where one spouse transfers their share of an existing property to the other, only the transferring spouse is freed to buy a second property as a “first” purchase. Decoupling has legal, CPF refund, and mortgage implications — always take specialist advice first.

Consider commercial or industrial property instead. Commercial and industrial properties do not attract ABSD. They have their own financing, GST, and tax considerations — but for investors focused on yield, they are worth analysing. See our Property Investment section for how commercial yields compare with residential.

Look offshore for second and third properties. Singaporeans investing in Malaysia (JB/Iskandar), Thailand, the UK, Australia, or Japan pay no ABSD to the Singapore Government for those purchases. Each destination has its own foreign-buyer regime, which we cover in our Foreign Property Investment guide.

Time your citizenship/PR application carefully. For families where PR or citizenship is in progress, the ABSD profile at the date the OTP is granted determines the rate. Moving the OTP date by a few weeks can, in edge cases, change the applicable rate by 15–25 percentage points.

Frequently Asked Questions

Is ABSD payable on the land value or the built-up value?

ABSD is calculated on the higher of the purchase price or the market value of the property at the time of acquisition. For new launches, this is typically the purchase price; for resale, IRAS may apply an independent market valuation.

When exactly is ABSD due?

Within 14 days from the date of the document triggering the duty — usually the signing of the Option to Purchase (for resale) or the Sale & Purchase Agreement (for new launches). Late payment attracts penalties.

Can CPF be used to pay ABSD?

No. ABSD (like BSD) cannot be paid from CPF directly at the point of purchase — it must be paid in cash. You can, however, apply for CPF reimbursement after the stamping is complete, drawing from your Ordinary Account against the purchase price.

Do I pay ABSD if I inherit a property?

No. A property acquired by way of inheritance is not a purchase and does not attract ABSD on the transfer itself. However, an inherited property does count toward your property count for future purchases.

I already own a commercial shophouse. Do I pay ABSD on my residential condo?

The residential-only count means commercial and industrial holdings are not included in your ABSD property count. If you are a Singapore Citizen buying your first residential property while owning commercial real estate, you still pay 0% ABSD.

How does ABSD affect an Executive Condominium purchase?

Buying a new EC from the developer under the EC scheme does not attract ABSD during the initial owner-occupation period. Once an EC is privatised (10 years after TOP) and traded on the open market, normal ABSD rules apply.

What to Do Next

ABSD changes how much house you can afford, how you time an upgrade, and sometimes whether a purchase makes sense at all. If you are weighing your options right now, we suggest three next steps:

If you are an upgrader, study our Upgrader Guide — the sequencing question (sell first vs buy first) is the single biggest lever for managing ABSD.

Review current market conditions in our Property News and Property Trends sections — if further cooling measures are telegraphed, timing your OTP becomes critical.

Looking at a specific development? Our detailed condo reviews — including One Marina Gardens, Arina East Residences, and our Aurea vs Chuan Park showdown — include the full ABSD-inclusive cost breakdown for various buyer profiles, so you can see the true entry cost before committing.

Disclaimer: This guide is for general information only and does not constitute legal, tax, or financial advice. ABSD rates and remission rules change over time. Always verify the current position on the IRAS Stamp Duty page and consult a licensed conveyancing lawyer or tax specialist before acting on any property transaction.

⚡ Quick Answer: Buying a Private Condo in Singapore 2026

Eligibility: Any Singapore Citizen, Permanent Resident or foreigner may buy private non-landed residential property — no income ceiling applies.

Minimum cash outlay: At least 5% of purchase price must be in cash; the remaining 20% of the 25% down payment may come from CPF Ordinary Account.

ABSD: Singapore Citizens pay 0% ABSD on their first property, 20% on the second, 30% on the third. Foreigners pay 65%. (Rates effective 27 April 2023.)

BSD: Buyer’s Stamp Duty is payable by all buyers — 1% on first S$180,000; 2% on next S$180,000; 3% on next S$640,000; 4% on remainder up to S$1.5M; 5% thereafter.

Loan-to-Value (LTV): Maximum 75% bank loan for a first property. TDSR cap is 55% of gross monthly income.

Timeline: From viewing to key collection typically takes 12–16 weeks for resale, or 3–5 years for a new launch off-plan purchase.

Key milestone: Option to Purchase (OTP) must be exercised within 21 days (developer) or 14 days (resale); stamp duty is payable within 14 days of acceptance.

No CPF for overseas property: CPF OA funds may only be used for Singapore residential property.

Buying a private condominium in Singapore is one of the most significant financial decisions a household will make. Unlike HDB flats — which are heavily regulated by income ceilings, nationality rules and a Minimum Occupation Period (MOP) before resale — private residential property is open to a broader pool of buyers, but comes with its own web of stamp duties, financing constraints and legal procedures.

This guide walks through every stage of the private condo buying process in Singapore as of 2026: from assessing your eligibility and finances, through exercising the Option to Purchase (OTP), paying Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD), drawing down your bank loan and CPF, all the way to key collection and post-completion obligations. Data and regulations cited are current as at 15 May 2026.

Figure 1: The 10-step private condo buying process in Singapore 2026, from finance checks to post-completion. Source: URA, IRAS, CPF Board | lovelyhomes.com.sg

Step 1: Check Your Eligibility and Finances

Any buyer — Singapore Citizen (SC), Permanent Resident (PR) or foreigner — may purchase a private non-landed condominium. There is no HDB income ceiling for private property. However, financing is tightly regulated by the Monetary Authority of Singapore (MAS) through two key ratios:

Total Debt Servicing Ratio (TDSR): All monthly debt obligations — including the new mortgage — must not exceed 55% of gross monthly income. Banks typically stress-test the loan at a rate floor of 4% p.a. (MAS Notice 632 stress-test benchmark).

Loan-to-Value (LTV): The maximum bank loan is 75% of the lower of the purchase price or market valuation for a first residential property. This drops to 45% for a second property (if there is an outstanding housing loan) and 35% for a third or subsequent property.

Before viewing a single unit, calculate your maximum eligible loan amount and ensure your CPF Ordinary Account (OA) balance and cash savings can cover the 25% down payment, Buyer’s Stamp Duty, legal fees and renovation budget. A rough rule of thumb: budget an additional 4–5% of the purchase price on top of the down payment to cover all transaction costs.

Step 2: Obtain an In-Principle Approval (IPA)

An In-Principle Approval (IPA) — sometimes called an Approval in Principle (AIP) — is a conditional commitment from a bank that it is prepared to lend you up to a specified amount, subject to a satisfactory property valuation. Most major Singapore banks (DBS, OCBC, UOB, Standard Chartered, HSBC, Maybank) offer IPA letters valid for 30 days, renewable on request.

To obtain an IPA, the bank will assess your income documents (CPF contribution statements, IRAS Notice of Assessment, latest 3–12 months’ payslips for employed applicants), outstanding debt commitments, and credit bureau report. Processing typically takes 3–5 business days. Obtaining an IPA before you sign any OTP is strongly recommended — exercising an OTP without confirmed financing in place can result in a forfeited option fee if the loan falls through.

Buyer Profile

Max LTV

Min Cash Down

ABSD Rate (2026)

SC — 1st property

75%

5% cash

0%

SC — 2nd property

45%

25% cash

20%

SC — 3rd+ property

35%

25% cash

30%

SPR — 1st property

75%

5% cash

5%

SPR — 2nd+ property

45%

25% cash

30%

Foreigner (any)

75%

5% cash

65%

Entity / Company

75%

5% cash

65%

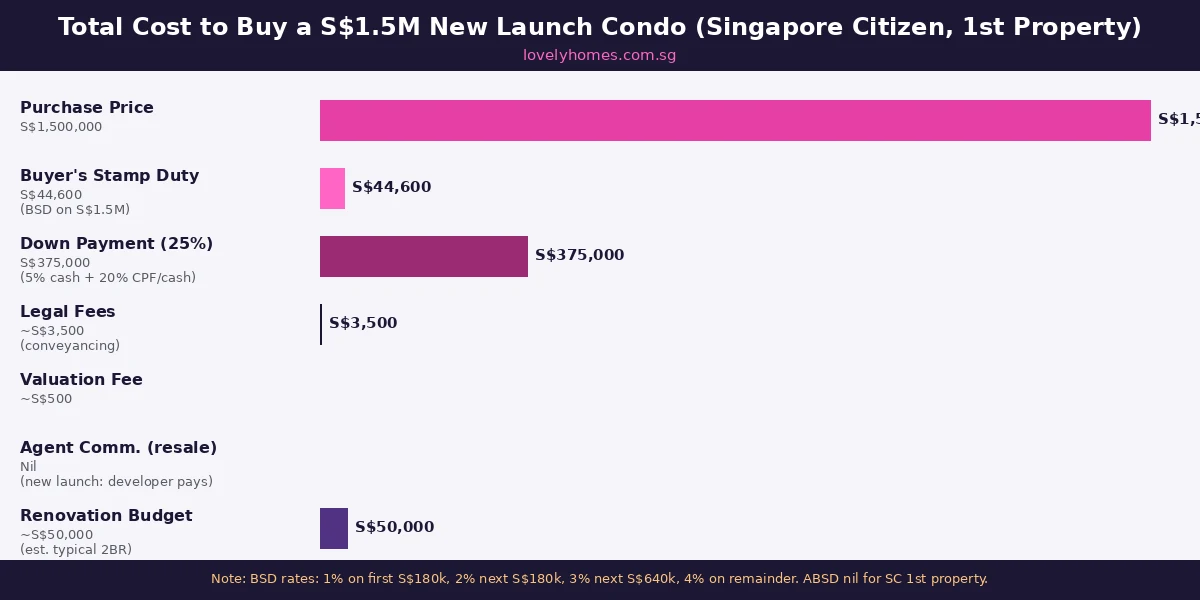

Figure 2: Full cost stack for a Singapore Citizen buying a S$1.5M new launch condo as their first property. Source: IRAS, CPF Board | lovelyhomes.com.sg

Step 3: Engage a Buyer’s Conveyancer

Unlike in some countries where a single solicitor can act for both buyer and seller (or buyer and bank), Singapore law requires separate solicitors for buyer and seller in most private property transactions. Your conveyancer — a law firm with real estate expertise — will review the Option to Purchase, the Sale and Purchase Agreement (S&P), lodge the CPF charge with the CPF Board, handle stamp duty payments and oversee the transfer of title. Engage your conveyancer before you grant or accept an OTP so they can review the documents promptly within the tight exercise windows.

Legal fees for a straightforward private condo purchase typically range from S$2,500 to S$4,500 for the buyer’s solicitor, plus the bank’s in-house or panel solicitor fees of S$800 to S$1,500 if you are taking a bank loan. Both are payable at completion.

Step 4: Search, Shortlist and View Properties

Singapore’s private residential market is segmented by location into three broad zones defined by URA: the Core Central Region (CCR — Districts 1, 2, 4, 6, 7, 9, 10, 11, and Sentosa), the Rest of Central Region (RCR — Districts 3, 5, 8, 12, 13, 14, 15, 20 and parts of others) and the Outside Central Region (OCR — all other districts). As of Q1 2026, URA data shows OCR non-landed prices led all segments with +2.2% quarter-on-quarter growth, reflecting sustained mass-market demand in towns like Tampines, Woodlands and Tengah.

For new launches, developer project websites and the URA New Sale caveat portal provide indicative price lists (PSF) before showflat visits. For resale units, URA’s Realis platform and HDB’s Resale Portal publish every caveat lodged within two weeks of an OTP being exercised. Use these sources to benchmark asking prices before negotiating.

Step 5: Grant and Exercise the Option to Purchase (OTP)

The Option to Purchase is the critical legal document that locks in the transaction. For new launches, the developer grants a 21-day OTP (extendable to a maximum of 42 days under the Housing Developers (Control and Licensing) Act). For resale, the seller grants a 14-day OTP, which may be extended by mutual agreement.

The buyer pays a 1% option fee (new launch: typically 5–10% option exercise fee as the booking fee) to receive the OTP. If the buyer decides not to proceed, the seller may forfeit the option fee. If the buyer exercises the option (by signing and returning it with the additional exercise money — typically a further 4% for resale, bringing total to 5%), the transaction is legally binding. The buyer must then pay BSD within 14 days of acceptance and sign the S&P or proceed with the developer’s standard agreement within 8 weeks (new launch) or 12 weeks (resale).

BSD is payable by every buyer on every purchase, regardless of nationality or property count. The current rates, administered by the Inland Revenue Authority of Singapore (IRAS), are progressive:

1% on the first S$180,000 of the purchase price

2% on the next S$180,000 (S$180,001 to S$360,000)

3% on the next S$640,000 (S$360,001 to S$1,000,000)

4% on the next S$500,000 (S$1,000,001 to S$1,500,000)

5% on the next S$1,500,000 (S$1,500,001 to S$3,000,000)

6% on the remainder above S$3,000,000

For a S$1.5M condo, BSD = S$1,800 + S$3,600 + S$19,200 + S$20,000 = S$44,600. ABSD is payable in addition to BSD — it must be stamped within 14 days of exercising the OTP. ABSD is not payable on a Singapore Citizen’s first property. On a S$1.5M second property for an SC, ABSD = 20% × S$1,500,000 = S$300,000. This is a material sum that must be factored into your budget before signing any OTP.

Worked Example: Mr and Mrs Tan Buy a S$1.5M Condo in Tampines (First Property)

Mr and Mrs Tan are both Singapore Citizens with a combined gross monthly income of S$14,000. They wish to purchase a new launch 3-bedroom condo in Tampines priced at S$1,500,000 as their first and only property (their HDB flat was sold to clear MOP).

BSD: S$44,600 (calculated above)

ABSD: S$0 (SC first property)

Down payment (25%): S$375,000 — at least S$75,000 (5%) must be cash; remaining S$300,000 may be CPF OA

Bank loan (75%): S$1,125,000 at 1.80% fixed for 2 years, 25-year tenure → monthly instalment ≈ S$4,634

TDSR check: S$4,634 ÷ S$14,000 = 33.1% — well within the 55% cap

Total cash needed at completion: S$75,000 (cash downpayment) + S$44,600 (BSD) + S$4,700 (legal) ≈ S$124,300 cash, plus S$300,000 from CPF OA

The Tans need to ensure their CPF OA balances (combined) are at least S$300,000 and that they have at least S$125,000 in cash savings before exercising the OTP.

Figure 3: Key financing parameters for private condos in Singapore 2026 — fixed-rate vs floating SORA bank loans. Source: MAS, CPF Board | lovelyhomes.com.sg

Step 7: Sign the Sale and Purchase Agreement and Loan Documents

The Sale and Purchase Agreement (S&P) is the legally binding contract between buyer and seller. For new launches, the developer is required by law (Housing Developers Rules) to use a standard-form S&P that specifies progressive payment milestones tied to construction stages. For resale, the S&P is drafted by the seller’s solicitor and reviewed by the buyer’s solicitor for any unusual conditions or encumbrances on the title.

Simultaneously, you will sign the bank’s Letter of Offer (loan agreement), which sets out the interest rate, tenure, prepayment conditions, lock-in penalties and any repricing rights. Under the MAS Notice on Mortgage Servicing Ratio (MSR) — which caps HDB-related loans at 30% of gross monthly income — private property loans have no MSR cap, only TDSR. Banks have typically been offering 2-year fixed rates of 1.75–1.85% p.a. as of May 2026 (SORA 3M at approximately 1.20% + spread of 0.55%).

Step 8: Pre-Completion Checks, Snagging and Handover

For new launches, Temporary Occupation Permit (TOP) is issued when construction is substantially complete. Buyers are invited to conduct a snagging inspection before key collection — a thorough walkthrough to identify and log defects (water seepage, scratched flooring, misaligned doors, non-functioning fixtures) in the developer’s Defects Rectification Form. Developers are obligated under the Building and Construction Authority (BCA) guidelines to rectify defects within 12 months of TOP. Do not waive your right to a snagging inspection; defects are far cheaper to fix before handing over deposit-linked remedies.

For resale units, arrange for an independent building inspector to inspect the unit before exercising the OTP. A structural defect discovered after signing the S&P may be difficult and expensive to resolve.

Step 9: Completion and Key Collection

Legal completion typically occurs 8–12 weeks after the S&P is signed (resale) or upon TOP for new launches. At completion, the balance of the purchase price (minus your deposit already paid and minus the loan drawn down by the bank) is transferred from your solicitor’s client account. Your CPF OA charge is lodged, the bank’s mortgage is registered, and the Transfer of Title is stamped and lodged with the Singapore Land Authority (SLA). You collect the keys (and for new launches, the developer issues your Electronic Certificate of Statutory Completion / Certificate of Fitness).

Step 10: Post-Completion Obligations

After key collection, several post-completion obligations apply. First, notify IRAS within 15 days of the change in ownership — your solicitor will typically handle this. Second, if you sold your HDB flat to fund this purchase, ensure all CPF refunds (principal + accrued interest) have been credited back to your CPF OA. Third, review your fire insurance and home contents insurance. If your unit is in a strata development, the MCST’s master fire insurance policy covers the building structure but not your contents or renovation works. Finally, if you plan to rent out the unit, notify IRAS as rental income is taxable — declare it in your annual personal income tax return.

Why the Process Matters: OCR’s S$2.2% Q1 2026 Surge and What It Signals

URA’s Q1 2026 final private residential data (released 24 April 2026) showed private property prices rising 0.9% quarter-on-quarter overall, with the OCR — the mass-market segment covering Tampines, Woodlands, Tengah and similar suburbs — surging 2.2%. This is the highest OCR quarterly gain since Q2 2024. Against this backdrop, buyers who understand every cost component of the transaction — particularly the BSD and ABSD exposure on second properties — are better positioned to make rational bid-versus-walk decisions.

The large supply pipeline ahead — URA reports approximately 55,800 private units and ECs expected to complete over the next several years, plus 4,575 units from the 1H 2026 GLS confirmed list — suggests that buyers who over-commit on today’s prices without stress-testing against a possible price correction do so at their own risk. The MAS stress-test rate of 4% p.a. is deliberately conservative for this reason.

What Might Come Next: Cooling Measure Adjustments and ABSD Calibration

Singapore’s property cooling measures have been calibrated in multiple rounds since 2009. The most recent significant revision was the April 2023 ABSD increase (foreigners to 65%, SC second property to 20%). As of May 2026, there are no confirmed further ABSD adjustments on the horizon. However, the ongoing strength of OCR prices and the record-breaking new launch weekend sales in April 2026 (Tengah Garden Residences and Vela Bay together sold over 1,200 units in 48 hours) may prompt the Ministry of National Development to revisit cooling measures should the market overheat. Buyers considering a second private property — particularly the decoupling strategy to lower ABSD exposure — should seek legal and financial advice before committing.

Frequently Asked Questions

Can I use CPF to buy a private condo in Singapore?

Yes. CPF Ordinary Account (OA) funds may be used for the down payment (above the mandatory 5% cash) and for servicing the monthly mortgage instalments, subject to the Valuation Limit (VL) and Withdrawal Limit (WL) rules. The VL is set at the lower of the purchase price or valuation at the time of purchase. You can use CPF up to the VL, and beyond that up to 120% of the VL (the WL), provided you retain the prevailing Basic Retirement Sum (BRS) in your CPF. Once the WL is reached, no further CPF can be used for that property. Note: CPF may not be used for overseas property under any circumstances.

Can foreigners buy private condos in Singapore?

Yes. Foreigners (non-Singapore Citizens, non-PRs) may purchase private non-landed residential property — including condominiums, apartments and strata-titled units — without any government approval. However, they may not purchase HDB flats, executive condominiums within the first 10 years of MOP, landed properties (detached houses, semi-detached, terrace houses) except in specific cases approved by the Singapore Land Authority, or residential properties on Sentosa Cove below a specified threshold without prior SLA approval. Foreigners pay ABSD of 65% on any Singapore residential property purchase.

What happens if I cannot exercise the OTP within the 14-day window?

If you fail to exercise the OTP within the specified period (14 days for resale, 21 days for new launches), the option lapses. The seller may forfeit the 1% option fee — it does not need to be returned to you. For new launches, the developer’s standard form typically allows forfeiture of 25% of the booking fee (which is usually 5% of the purchase price) if the buyer does not exercise. This means on a S$1.5M new launch, failure to exercise could cost you S$75,000 × 25% = S$18,750 in forfeitures. Ensure your financing is confirmed before you sign the OTP receipt.

Do I need to sell my HDB flat before buying a private condo?

No, but there are significant financial consequences if you do not. If you own an HDB flat and purchase a private condo without selling the HDB first, you will be counted as owning two residential properties — triggering ABSD of 20% on the private property (for a Singapore Citizen). To avoid ABSD on the private purchase, you would need to sell your HDB flat before or simultaneously with completing the condo purchase. If you buy first and then sell the HDB within 6 months of the condo’s completion (or TOP for new launch), there is a remission mechanism for the ABSD paid — you may apply to IRAS for a refund if you meet all the conditions (including the property being jointly or solely owned by a married SC couple buying their second residential property and they have sold the first within the 6-month window). See IRAS’s stamp duty remission guidelines.

What is the difference between a new launch and a resale private condo?

A new launch condo is sold directly by the developer from an uncompleted or newly completed project, typically at a showflat. Prices are set by the developer (in PSF terms), there are no agents on the buyer’s side (the developer pays the selling commission), and the progressive payment scheme means you pay in tranches tied to construction milestones. The wait from booking to key collection is typically 3–5 years. A resale condo is an existing completed unit being sold by a private individual or investor. You can inspect the actual unit, the condition of the development and the management corporation (MCST). Transaction timelines are much shorter (8–12 weeks to completion) but you may need to factor in renovation costs and the condition of existing fixtures. Resale condo prices are also subject to market negotiation.

How long does the private condo buying process take in Singapore?

For a resale private condo, the process from OTP issuance to legal completion typically takes 10–14 weeks. You have 14 days to exercise the OTP, then 8–12 weeks for completion. The full process from first viewing to key collection, including time to arrange financing, is typically 2–4 months. For a new launch condo purchased off-plan, the process is very different: you book a unit at the showflat (same-day for popular launches), sign the OTP and formal S&P within 3 weeks, pay progressively over the construction period of 3–5 years, and collect keys at TOP.

Can a Singapore Permanent Resident (PR) buy a private condo?

Yes, PRs may purchase private non-landed residential property. A PR buying their first residential property pays ABSD of 5% and can access up to 75% LTV. However, PRs may not use their CPF Ordinary Account to purchase property until they have been a PR for 1 year. PRs also cannot purchase HDB resale flats unless the entire purchasing household is PR-only and they meet a minimum 3-year PR residency requirement; they cannot purchase new HDB BTO flats. For a second property, the ABSD rate for PRs rises to 30%, the same as Singapore Citizens buying a third property.

Disclaimer: This article is for general informational purposes only and does not constitute legal, financial or investment advice. Stamp duty rates, ABSD rates, LTV limits, CPF rules and MAS regulatory requirements are as published by IRAS, MAS and CPF Board and are subject to change by the Singapore government at any time. Readers should verify all figures directly with IRAS (iras.gov.sg), MAS (mas.gov.sg), CPF Board (cpf.gov.sg) and URA (ura.gov.sg), and consult a licensed solicitor, a MAS-licensed financial adviser or a registered mortgage broker before making any property transaction decision. LovelyHomes is not affiliated with any property agency and does not provide brokerage services.

Singapore’s HDB system includes a category of flat specifically designed for seniors and older singles who want to right-size, reduce their mortgage burden, or access their housing equity without leaving public housing. The HDB 2-Room Flexi flat — and its cousin, the Studio Apartment — give buyers aged 55 and above a route to a smaller, more manageable home, often with significant grant support on top. If you are approaching retirement and wondering what to do with a large, nearly-paid-off flat, this guide explains every option available to you in 2026.

Quick Answer — HDB 2-Room Flexi for Seniors 2026

Who can buy: Singles aged 35+; couples where at least one party is 55+ (for Short Lease option)

Short Lease option: 15, 20, 25, 30, or 35 years — choose a lease matching your remaining life expectancy

Studio Apartments: Available at Selective En-bloc Redevelopment Scheme (SERS) sites; 30-year lease; for buyers 55+

Silver Housing Bonus (SHB): Up to S$30,000 cash when right-sizing from a larger flat

Lease Buyback Scheme (LBS): Sell part of your remaining HDB lease back to HDB; proceeds top up your CPF Retirement Account

CPF use: Proportional for short leases — you can only use CPF savings up to the value of the remaining lease

No resale market for Studio Apartments; 2-Room Flexi 99-year units can be resold after 5-year MOP

What Is a HDB 2-Room Flexi Flat?

The 2-Room Flexi flat is a Build-To-Order (BTO) flat type rolled out by HDB in 2015 to replace the discontinued Studio Apartment in new BTO exercises. It comes in two variants. The first is the Short Lease option, designed specifically for seniors aged 55 and above and singles aged 35 and above, with a lease of 15 to 35 years (in five-year increments) chosen at the point of application. The second is the Standard 99-Year Lease option, available to singles aged 35 and above and to families. Floor area is modest by design: Type 1 units are 36 sqm and Type 2 units are 45 sqm. Both include a living/dining area, one bedroom, one bathroom, a kitchen, and a service yard.

Figure 1: HDB Housing Options for Seniors 55+ — key features compared (2026)

Short Lease vs 99-Year: Which Should Seniors Choose?

The Short Lease variant is usually the financially smarter choice for buyers who are primarily right-sizing for comfort, not investment. By choosing a shorter lease — say, 25 years for a buyer aged 65 — you pay a significantly lower price for the flat. The sale proceeds from your current, larger flat are then available for other needs. CPF use on a short-lease flat is proportional: the CPF Board limits your Ordinary Account (OA) withdrawal to a fraction of the flat’s valuation based on the ratio of the chosen lease relative to 65 years. In practice, buyers on a 20-year short lease will use mostly cash and have less CPF deployed in the flat, leaving more CPF savings liquid for drawdown in retirement.

The 99-Year Lease option makes more sense for younger singles in their 30s or early 40s who want a small flat as a starter or long-term home with full resale flexibility. After the 5-year MOP, the unit can be sold on the open market.

Figure 2: CPF Use for Short Lease vs 99-Year HDB Flat — how the proportional rule works (2026)

Studio Apartments — The Legacy Option

Studio Apartments were HDB’s original senior-friendly product, built from the 1990s. They are no longer built in new BTO exercises (replaced by the 2-Room Flexi from 2015), but existing units occasionally come up through SERS (Selective En-bloc Redevelopment Scheme) rehousing exercises. Studio Apartments are typically 35–45 sqm, carry a 30-year lease from the date of offer, and are sold to buyers aged 55 and above. There is no open-market resale — you can only surrender the flat back to HDB if you need to leave.

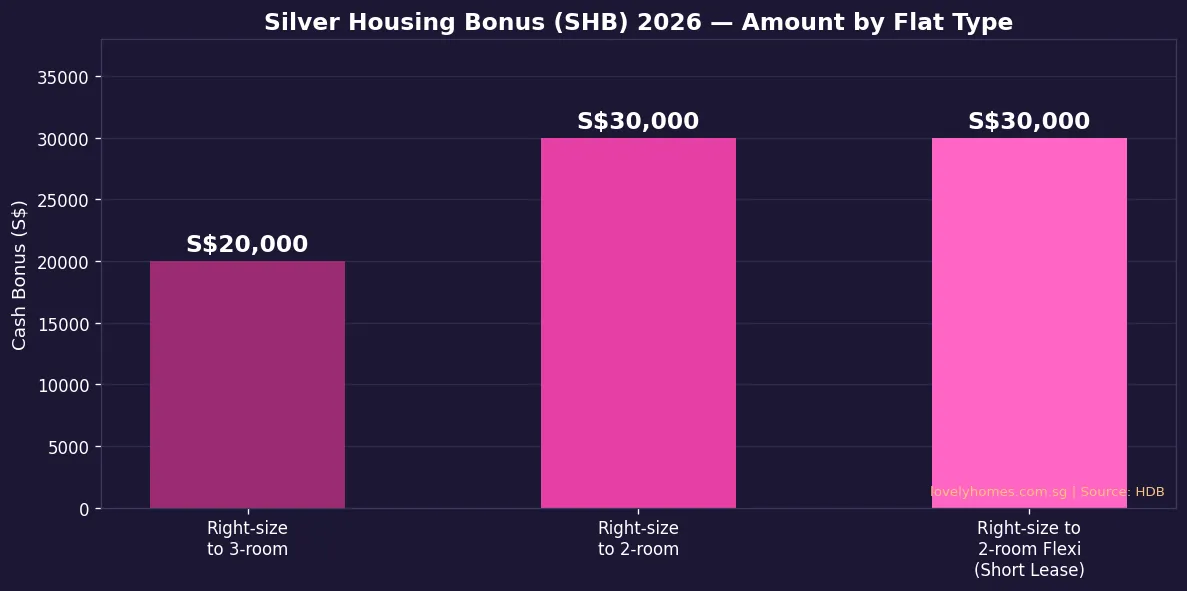

Silver Housing Bonus — Up to S$30,000 in Cash

The Silver Housing Bonus (SHB), administered by the CPF Board and HDB, provides eligible seniors with a cash bonus of up to S$30,000 when they right-size to a smaller flat. Eligibility: At least one flat owner must be a Singapore Citizen aged 55 or above. The seller must use the net sale proceeds of their current flat to top up their CPF Retirement Account (RA) up to the current Enhanced Retirement Sum (ERS). For right-sizing to a 2-room or 2-Room Flexi flat (Short Lease), the maximum bonus is S$30,000. For right-sizing to a 3-room flat, the bonus is S$20,000.

Figure 3: Silver Housing Bonus (SHB) 2026 — cash bonus amount by target flat type

Lease Buyback Scheme — Converting Your Flat’s Value to Retirement Income

The Lease Buyback Scheme (LBS) allows eligible seniors to sell part of their flat’s remaining lease to HDB for a lump sum, which is used to top up their CPF Retirement Account. The retained lease must be at least 20 years and cover the youngest owner to age 95. HDB buys the tail end of the lease at assessed market value of that lease proportion, with proceeds going into the owner’s CPF RA to meet the Full Retirement Sum (FRS) or Basic Retirement Sum (BRS) — excess is paid in cash. The couple continues living in the flat under the retained lease and receives monthly CPF LIFE payouts from the topped-up RA.

LBS is not available for 2-Room Flexi Short Lease flats because the chosen lease is already short by design. It is available for 2-Room Flexi 99-Year flats and for larger flats (3-room and above).

Summary: HDB Senior Housing Options at a Glance

Scheme

Who Qualifies

Key Benefit

Amount / Price Range

2-Room Flexi Short Lease

Singles 35+; couples with one 55+

Smaller, cheaper flat; choose lease

~S$90k–S$200k

2-Room Flexi 99-Year

Singles 35+; families

Full resale rights after MOP

~S$180k–S$350k

Studio Apartment

Buyers 55+ (SERS estates)

Below-market; 30-yr lease

~S$80k–S$150k

Silver Housing Bonus

SC 55+, right-sizing from larger flat

Cash bonus

S$20k (3-rm) / S$30k (2-rm)

Lease Buyback Scheme

SC/SPR 65+, own 3-room or larger HDB

Convert lease equity to CPF LIFE

Lump sum into RA; monthly payout

Proximity Housing Grant

Buyers near parents/children

Grant on resale purchase

S$20k (1km) / S$30k (same estate)

Worked Example — The Lim Couple Right-Sizes at 68

Mr and Mrs Lim, both aged 68, Singapore Citizens, live in a 5-room HDB flat in Bishan with 55 years of lease remaining. Their children have moved out. They right-size to a 2-Room Flexi, Short Lease (25 years) in the same estate.

Sale proceeds from the 5-room flat: S$650,000 (after refunding CPF + accrued interest of S$220,000)

Purchase price of 2-Room Flexi (25-year short lease): S$145,000

CPF use for purchase: proportional to 25/65 years ≈ 38% of flat value → S$55,000 from OA (if available)

Cash needed: S$145,000 − S$55,000 = S$90,000 cash

Silver Housing Bonus: S$30,000 cash (right-sizing to 2-room)

CPF RA top-up from sale proceeds to meet ERS (say S$190,000 per person)

Net free cash in hand after purchase, SHB, and CPF RA top-up: approximately S$235,000

Monthly CPF LIFE payout after RA top-up (ERS scheme): approximately S$2,200–S$2,500 per person

Why This Matters — Housing as a Retirement Asset

A very large proportion of household wealth in Singapore is locked inside HDB flats. The 2-Room Flexi, SHB, and LBS framework is the Government’s systematic answer: offering seniors structured, HDB-administered routes to convert housing equity into retirement cash flow without moving out of public housing. The 2026 environment makes right-sizing particularly attractive — HDB resale prices remain elevated after years of growth, while 2-Room Flexi Short Lease prices remain relatively modest, offering a significant arbitrage between what seniors receive for their existing flat and what they pay for the right-sized replacement.

What Might Come Next

HDB has been gradually expanding 2-Room Flexi supply in mature and prime estates. The Government may introduce enhancements to the Silver Housing Bonus quantum or Lease Buyback Scheme proceeds as Singapore’s population continues to age. Monitor the annual MND Budget statement, National Day Rally, and the HDB website for the latest BTO schedule and grant amounts before committing to any right-sizing decision.

Frequently Asked Questions

Can a single person buy a 2-Room Flexi short-lease flat?

Yes. Singapore Citizens and Permanent Residents aged 35 and above who are singles can apply for a 2-Room Flexi flat — both the 99-year and Short Lease variants. For the Short Lease, HDB targets it at buyers aged 55 and above, but the formal eligibility lower bound is 35. Singles are not eligible for most family-tier HDB grants, but may qualify for the Silver Housing Bonus if they are at least 55 and right-sizing from a larger flat.

What happens when the short-lease flat’s chosen tenure expires?

When the lease expires, the flat reverts to HDB with no residual value or compensation. This is by design — the flat’s utility is fully consumed during the chosen lease period. Buyers should choose a lease length covering at least to age 95 per CPF Board guidelines. If the owner passes away before expiry, the remaining lease value may be passed to eligible family members under HDB estate transmission rules.

Can I use CPF OA to buy a 2-Room Flexi Short Lease flat?

Yes, but proportionally. The CPF Board allows OA use up to the value corresponding to the lease coverage from your youngest owner’s age to 95. For a 25-year lease chosen by a 65-year-old (covering to age 90), the CPF-usable proportion is roughly 25/65 ≈ 38% of assessed value. A significant portion must therefore be paid in cash. This is intentional — it preserves CPF savings for retirement income rather than locking them into housing.

How do I apply for the Silver Housing Bonus?

The Silver Housing Bonus is administered jointly by HDB and the CPF Board. You apply at the point of booking your new (smaller) flat or during the resale application process. HDB assesses eligibility and the bonus amount based on the size of your current flat, your new flat, and whether you meet the RA top-up requirement from sale proceeds. The cash bonus is paid directly to you — not into CPF — once the transaction is completed. Check HDB’s 2-Room Flexi page for current SHB quantum and conditions.

Does the Lease Buyback Scheme work with a 2-Room Flexi flat?

LBS is available for 3-room and larger HDB flats and for Studio Apartments in SERS estates. It is not available for 2-Room Flexi Short Lease flats because the chosen lease is already short. For 2-Room Flexi 99-year flats, LBS is in principle available but less commonly used, since most LBS participants hold larger flats with more lease equity to monetise. Contact HDB directly to assess eligibility for your specific lease position.

Can I rent out my 2-Room Flexi flat?

You may rent out individual bedrooms after satisfying the MOP (5 years for the 99-year variant). HDB generally does not approve whole-unit rentals for short-lease 2-Room Flexi flats. Renting a bedroom is subject to HDB’s standard subletting approval process and tenant nationality quotas. You may not rent out the entire flat while listed as the owner-occupier.

What is the difference between the 2-Room Flexi and the old Studio Apartment?

Studio Apartments (1990s–2000s) are no longer available in new BTO exercises — replaced by the 2-Room Flexi from 2015. Studio Apartments carry a 30-year lease and are offered at SERS estates to sitting residents. The 2-Room Flexi offers greater flexibility: choice of lease from 15–35 years or a full 99-year lease, two floor-area variants, and (for the 99-year unit) open-market resale rights after MOP. Studio Apartments have no resale market. For most seniors today, the 2-Room Flexi is the primary option.

Disclaimer: This article is for general informational purposes only and does not constitute financial, legal, or professional advice. Property rules, grant amounts, eligibility criteria, and tax treatments are subject to change. Always verify current details with the relevant authorities — HDB, IRAS, CPF Board, URA — and consult a licensed professional before making any property or financial decision.

When you buy a condo or strata-titled property, you own your unit plus a proportionate share of the common property (pools, corridors, lifts, roofs).

The Management Corporation (MCST) is the statutory body comprising all unit owners. It is responsible for maintaining common property.

Maintenance fees are split between the Management Fund (day-to-day running costs) and the Sinking Fund (long-term capital works). The sinking fund must receive at least 10% of total levies.

Your share value (SV) determines how much you pay and how many votes you hold at general meetings.

The Annual General Meeting (AGM) must be held within 15 months of the previous one. Owners can vote on budgets, elect council members, and pass resolutions.

Disputes go to the Strata Titles Board (STB), a quasi-judicial tribunal under the Building and Construction Authority (BCA).

What Is Strata Title?

In Singapore, most private residential properties sold in multi-unit developments — condominiums, apartments, cluster housing, and some mixed-use commercial buildings — are sold under strata title. Strata title is a form of property ownership that allows a developer to subdivide a building into individual lots (units) and a common property lot, with each unit owner holding title to their own lot while all owners collectively share ownership of the common property.

The legal framework governing strata title in Singapore is the Land Titles (Strata) Act (LTSA) and, for the management obligations, the Building Maintenance and Strata Management Act (BMSMA) administered by the Building and Construction Authority (BCA). Together these two statutes define what you own, how common property is managed, what fees you must pay, and how disputes are resolved.

Understanding strata title matters practically because it determines your rights and obligations from the day you collect keys. Maintenance fees are a legal obligation — not a voluntary contribution. By-laws govern what you can and cannot do within your unit and the common areas. The financial health of the MCST directly affects the value of your property.

The MCST — What It Is and How It Works

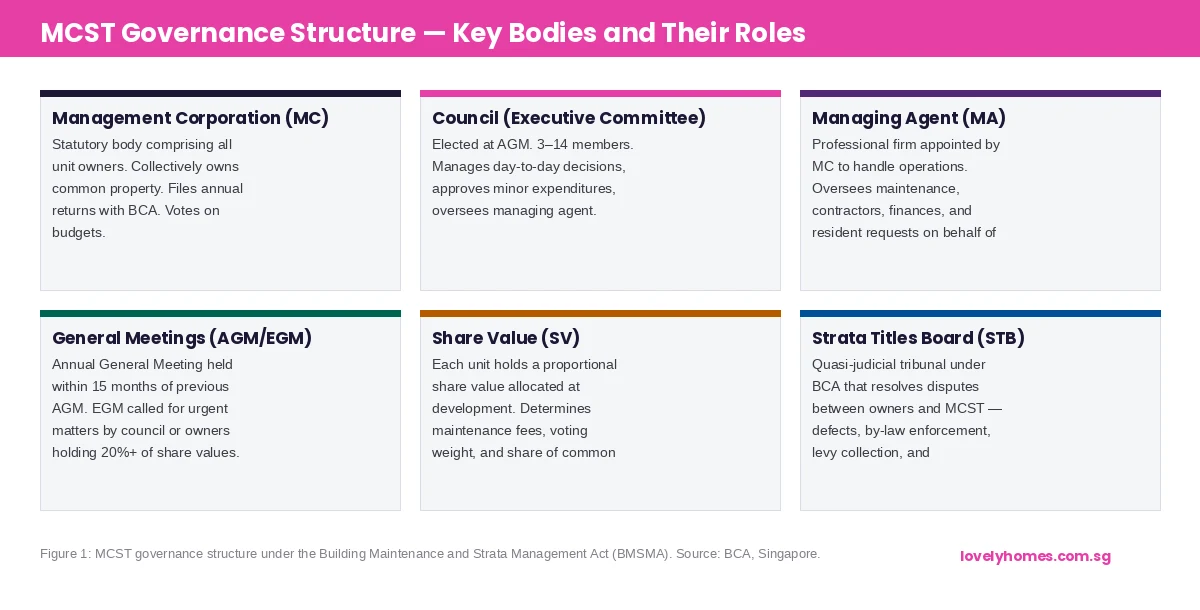

Figure 1: MCST governance structure under the Building Maintenance and Strata Management Act (BMSMA). Source: BCA.

The Management Corporation Strata Title (MCST) comes into legal existence automatically when the first unit in a strata development is sold. Every unit owner is automatically a member of the MCST — there is no opt-out. The MCST number (e.g. MCST 1234) is printed on the strata certificate of title and is registered with the Singapore Land Authority (SLA).

The MCST has a council — sometimes called the executive committee — of 3 to 14 elected members who are responsible for day-to-day management between general meetings. Council members are volunteers elected by other owners at the AGM. For large developments (above 100 units), managing the MCST professionally is a significant undertaking, which is why most developments appoint a managing agent (MA) — a licensed professional firm (regulated by BCA under the BMSMA) — to handle operations.

The managing agent is an agent of the MCST, not an independent principal. Their scope of authority is defined in the MA agreement and must be approved by the council. A managing agent can be replaced at the AGM by an ordinary resolution. Disputes about managing agent performance are common triggers for EGMs (Extraordinary General Meetings).

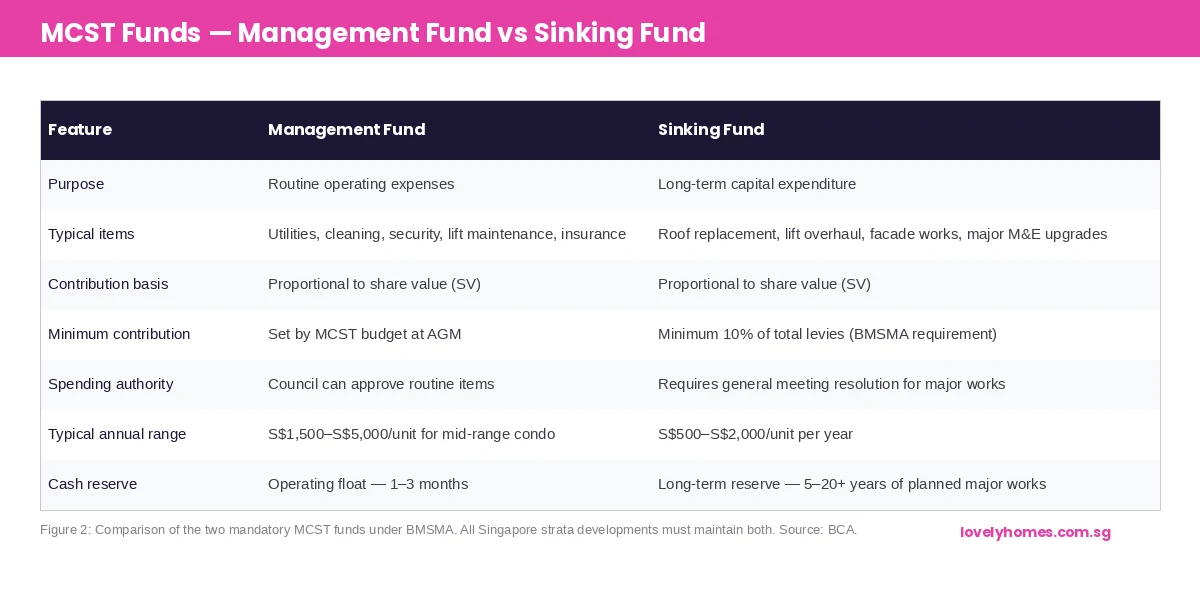

Management Fund vs Sinking Fund

Figure 2: The two mandatory MCST funds — management fund for operations, sinking fund for capital works. Source: BCA, BMSMA.

The BMSMA requires every MCST to maintain two separate funds. Understanding their purpose helps you evaluate the financial health of a development before you buy, and interpret the financial statements tabled at each AGM.

The Management Fund covers the day-to-day running costs of the development: electricity and water for common areas, cleaning contracts, security personnel, lift maintenance contracts, swimming pool chemicals and attendants, building insurance, and the managing agent’s fees. It operates like an operating budget. The council proposes the annual budget, and owners vote on it at the AGM. Contributions are collected monthly or quarterly as maintenance levies.

The Sinking Fund is reserved for major cyclical expenditure: repainting the facade, replacing lifts (typically required every 25 years), reroofing, upgrading fire-suppression systems, and replacing aged mechanical-electrical (M&E) equipment. By law, the sinking fund must receive a minimum of 10% of the total levies collected. A healthy sinking fund is one of the strongest indicators of a well-managed development — a depleted sinking fund often signals years of underfunding, leading to either special levies or deferred maintenance that depresses property values.

When evaluating a resale condo for purchase, always request the MCST’s most recent annual financial statements (obtainable from the managing agent or the outgoing owner) and check the sinking fund balance per unit relative to the age and planned major works cycle of the development.

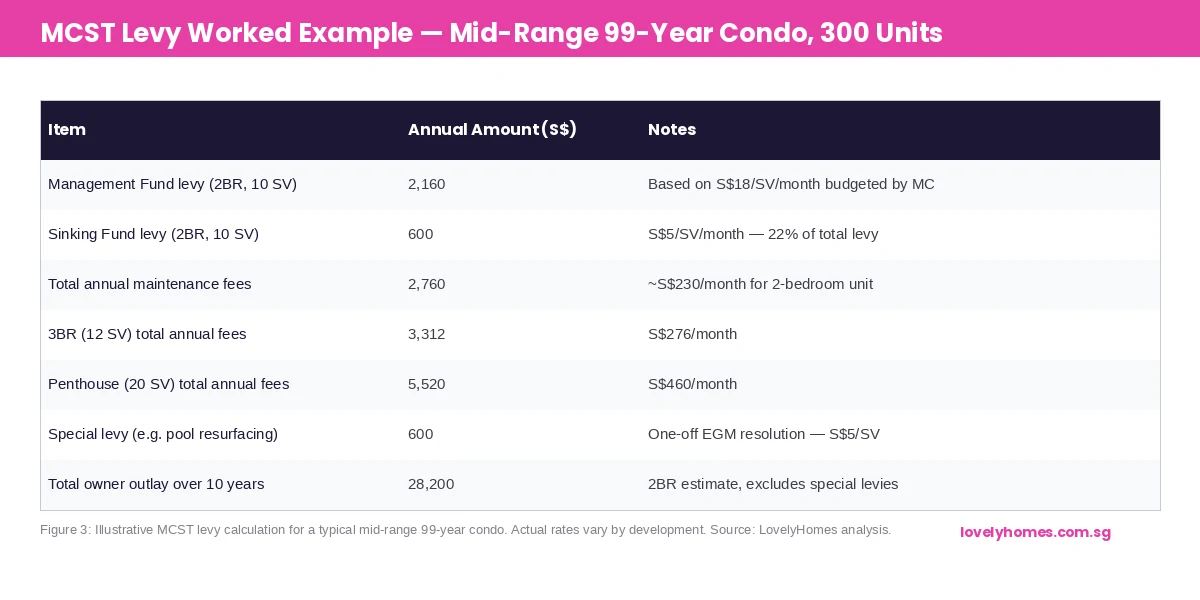

Maintenance Levies — How Much and How Calculated

Figure 3: Illustrative MCST levy for a 300-unit mid-range 99-year leasehold condo. Actual rates vary by development size and facilities. Source: LovelyHomes analysis.

Maintenance levies are calculated based on your unit’s share value (SV). Share values are fixed at the time the strata development is registered with SLA and are proportional to the floor area of each unit (with some adjustments for exclusive use areas, car parks, and other factors). A 2-bedroom unit typically carries 10 share values; a 3-bedroom 12; a penthouse 20 or more.

The formula is simple: Monthly levy = SV × (Rate per SV per month approved at AGM). In a mid-range 300-unit development in 2026, a management fund rate of S$18 per SV per month and a sinking fund rate of S$5 per SV per month is typical. For a 2-bedroom with 10 SV, that is S$230 per month or S$2,760 per year.

For luxury condos with extensive facilities (full-size Olympic pool, tennis courts, concierge, gym, multiple function rooms), rates of S$50–S$80 per SV per month are common, translating to S$6,000–S$12,000 per year for a mid-sized unit. Before buying, always verify the current maintenance fee from the MCST financial statements — the amount stated in the OTP or by the agent may be out of date if the AGM has recently approved a rate increase.

Development Type

Indicative Monthly Fee Range

Key Cost Driver

Mass-market condo (no full facilities)

S$150–S$250/month

Lower facilities overhead

Mid-range condo (pool, gym, BBQ)

S$200–S$400/month

Typical 2BR in 300-unit development

Luxury condo (full concierge, courts)

S$500–S$1,200/month

Staffing and high-spec M&E

Older development (>25 years)

Higher sinking fund component

Lift, roof and M&E replacement cycle

Small boutique development (<50 units)

Higher per-unit cost

Fixed overhead spread over fewer owners

By-Laws — What You Can and Cannot Do

Every MCST operates under two layers of by-laws: the default by-laws prescribed in the Second Schedule to the BMSMA, which apply to all strata developments unless expressly amended, and any additional by-laws passed by the MCST at a general meeting by special resolution (75% of votes by share value).

The default by-laws cover a wide range of matters that affect daily condo living, including:

Noise and nuisance. The by-laws prohibit activities that cause unreasonable noise or nuisance to other residents, particularly between 10:30pm and 7:00am. This includes power tools, loud music, and guests in common areas.

Alterations and renovations. Any renovation works that affect common property or structural elements require written approval from the MCST before commencement. This includes hacking or coring through floor slabs, installation of air-conditioner ledges, and changes to external facades. Works that do not affect common property (internal non-structural reconfigurations) require only compliance with URA/BCA requirements and notification to the MCST — not approval. See our Renovation Loan guide for the financing angle.

Pets. The default by-laws do not prohibit pets, but many MCSTs pass specific by-laws restricting pets to dogs under 10kg or prohibiting them altogether in common lifts or areas. Check the development’s specific by-laws before buying if pet ownership is important to you.

Parking. Car park lots in most condos are either strata-titled (you own the lot) or allocated by the MCST. The MCST sets the rules for allocation, usage, and visitor parking. Unauthorised parking in common lots may result in vehicles being towed at the owner’s expense.

Your Rights as an Owner — General Meetings and Voting

As a unit owner, you are automatically a member of the MCST with enforceable rights. The most important of these is your right to attend and vote at general meetings. Votes are weighted by share value — the more SV you hold, the more voting power you have. However, for most ordinary resolutions, a simple majority by share value suffices, and the practical reality is that small-unit owners collectively hold the majority of share values in most developments.

Key resolutions and their required majority:

Ordinary resolution (simple majority by SV): annual budget approval, election of council, appointment of managing agent, minor by-law amendments.

90% resolution: improvements or alterations to common property that disproportionately benefit some owners over others.

Special resolution (75% by SV with 14 days’ notice): new or amended by-laws, significant improvements to common property, major expenditure from sinking fund.

Unanimous resolution: changes that affect only certain strata lots, or that extinguish exclusive use rights.

If you believe the council has acted improperly or the MCST is not fulfilling its statutory obligations, you can requisition an EGM (with 20% of SV supporting the requisition), file a complaint with BCA, or bring a dispute to the Strata Titles Board.

Strata Titles Board — Dispute Resolution

The Strata Titles Board (STB) is a quasi-judicial tribunal established under the LTSA. It has jurisdiction over disputes between unit owners and MCSTs in three main areas:

Management disputes. Failure by the MCST to carry out its maintenance obligations, disputes over levy computation or enforcement, unauthorised alterations to common property, and by-law enforcement disputes.

Financial disputes. Recovery of unpaid levies by the MCST against defaulting owners, disputes over the validity of resolutions passed at general meetings, and challenges to special levies.

Collective sale (en-bloc). When an en-bloc sale reaches 80% owner consent by share value and floor area, the sale committee applies to the STB for an order to sell. The STB hears objections from dissenting owners and decides whether the collective sale is just and equitable. See our En-Bloc Collective Sale guide for the full process.

STB proceedings are less formal than court but legally binding. For monetary disputes, the STB can award damages and costs. For en-bloc applications, the STB’s order is final subject only to High Court appeal on points of law.

What to Check Before Buying a Strata-Titled Property

Savvy buyers treat MCST financial health as a material factor in pricing a strata purchase. Key due-diligence checks:

1. Request the MCST financial statements for the last 2–3 years. Look at the sinking fund balance per unit against the age of the development and scheduled major works. A 15-year-old condo with a sinking fund of only S$500,000 for 200 units (S$2,500 per unit) is likely underfunded for an imminent lift replacement costing S$3–5M.

2. Check for pending special levies or litigation. Ask the managing agent directly whether there are any planned or approved special levies for major works, or any STB proceedings pending. These will become your obligation after purchase.

3. Review the by-laws for specific restrictions. Pet policies, AirBnB/short-term rental prohibitions, parking allocation rules, and guest policies vary significantly between developments.

4. Note the MCSTs arrear rate. A high arrears rate on maintenance levies signals owner financial stress or poor management — both are red flags for collective governance.

What Might Come Next

BCA is actively reviewing the BMSMA framework in 2026, with a public consultation on several proposed amendments including mandatory mediation before STB proceedings, enhanced disclosure requirements for MCSTs on major works timelines, and possible standardisation of sinking fund contribution rates linked to development age rather than purely to AGM approval. These reforms, if enacted, would increase transparency for buyers and reduce the risk of discovering an underfunded sinking fund post-purchase. Buyers of resale condos in particular stand to benefit from enhanced mandatory disclosure.

FAQ 1: Can the MCST prevent me from renting out my unit on Airbnb or short-term lets?

Yes. Under the BMSMA, an MCST can pass a by-law (by special resolution — 75% of share values) prohibiting short-term rentals of fewer than a specified minimum period. Many condos have enacted such by-laws following the Urban Redevelopment Authority’s position that residential units must not be used for short-term accommodation of fewer than 3 consecutive months without URA approval. Even if your MCST has not passed a specific by-law, short-term rentals below 3 months in a private residential property require URA planning approval, which is rarely granted. Always check both URA rules and the development’s by-laws before letting on short-term platforms.

FAQ 2: What happens if I don’t pay my maintenance fees?