Strata Living in Singapore 2026: MCST, Sinking Fund & Condo Management — Complete Guide

Quick Answer: Strata Living Key Facts

- Every private residential condominium and flat development in Singapore with 3 or more units is governed by the Building Maintenance and Strata Management Act (BMSMA), administered by the Building and Construction Authority (BCA).

- A Management Corporation Strata Title (MCST) is the legal body comprising all subsidiary proprietors (unit owners) that manages the common property.

- All owners pay monthly contributions to two mandatory funds: the Management Fund (day-to-day operations) and the Sinking Fund (long-term capital work), proportional to their share value.

- The Sinking Fund contribution must be at least 10% of the Management Fund contribution — BCA may require higher percentages for ageing developments.

- A Management Council of 3–14 elected members runs the MCST between Annual General Meetings (AGMs). Owners are entitled to attend all AGMs and vote on motions.

- Disputes between unit owners or between owners and the MCST are heard by the Strata Titles Board (STB) — a specialist tribunal under the Ministry of Law.

- Singapore’s building stock is ageing: the BCA’s Building Condition Rating system and upcoming BMSMA amendments are expected to raise maintenance standards and minimum sinking fund requirements.

Introduction: What Is Strata Living?

When you purchase a private condominium unit or a strata-titled flat in Singapore, you own two things simultaneously: your individual unit (your strata lot), and a proportionate share in the development’s common property — the swimming pool, gymnasium, lobbies, lifts, car park, security systems, and landscaping that all residents share. This shared ownership model is called strata title, and it comes with both rights and obligations that every condo owner must understand.

The governance framework for strata living in Singapore is prescribed by the Building Maintenance and Strata Management Act (BMSMA), first enacted in 2004 and significantly amended in 2017. The BMSMA creates a corporation — the MCST — the moment a strata development is registered. From that point, the MCST is the legal owner of the common property and has the power to levy charges, enter into contracts, and enforce by-laws.

With over 4,000 registered MCSTs in Singapore as of 2026 (BCA data), and tens of thousands of condo owners paying monthly contributions, understanding how strata management works is no longer optional knowledge — it is essential for anyone who owns, buys, or rents in a private residential development.

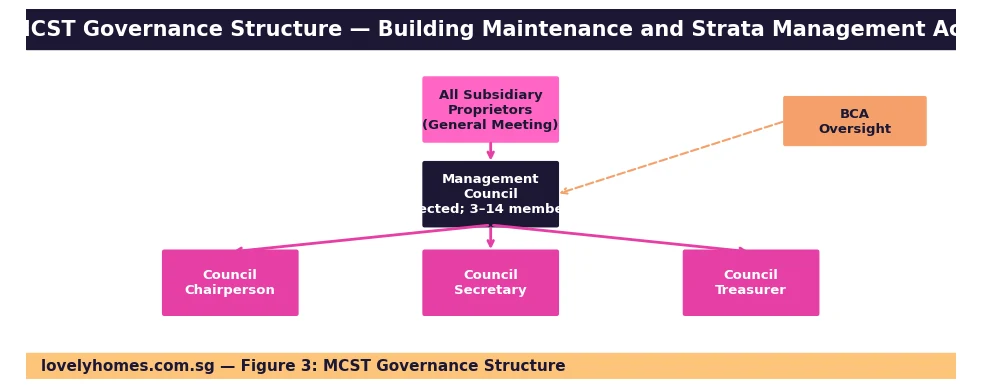

The MCST: How It Is Formed and How It Works

A Management Corporation Strata Title (MCST) is automatically constituted when a strata development is registered at the Singapore Land Authority (SLA). The MCST number (e.g., MCST 1234) is assigned at registration. The MCST is a legal entity — it can sue, be sued, enter contracts, and own the common property in its own name.

The Management Council

The day-to-day governance of the MCST is delegated to a Management Council comprising between 3 and 14 subsidiary proprietors elected at the Annual General Meeting. The council must meet at least quarterly and is responsible for:

- Approving budgets and setting the annual contribution schedule.

- Engaging a licensed Managing Agent (MA) to handle day-to-day management (optional but near-universal in Singapore developments).

- Enforcing by-laws relating to use of units and common property.

- Commissioning periodic building condition inspections and major maintenance works.

- Maintaining proper financial records (audited annually).

The council elects a Chairperson, Secretary and Treasurer from among its members. These office-holders have specific statutory duties — for example, the Secretary must convene the AGM within 15 months of the previous AGM and circulate financial statements at least 14 days before the meeting.

The Annual General Meeting (AGM)

The AGM is the supreme decision-making body for the MCST. All subsidiary proprietors are entitled to attend and vote. Key decisions at the AGM include:

- Adoption of annual financial statements.

- Election of the Management Council.

- Approval of the annual budget and contribution rates.

- Passing special resolutions (e.g., amending by-laws; requires 90% majority by share value at a properly convened meeting).

- Engaging or dismissing the Managing Agent.

Every subsidiary proprietor has voting power proportional to their share value — a number assigned at the development’s inception that reflects the relative size and value of each unit. Owners of larger, more valuable units typically have higher share values and thus greater voting weight.

Management Fund and Sinking Fund: How Much Do You Pay?

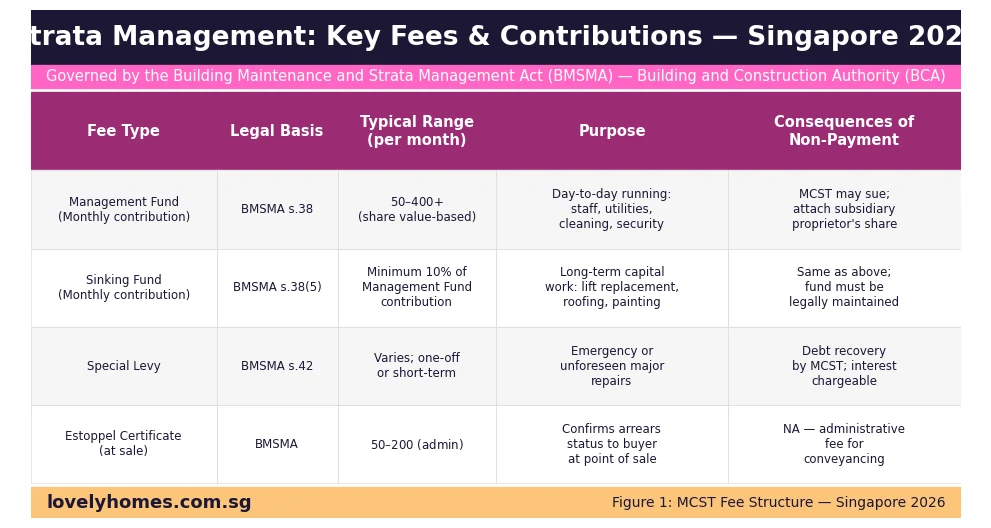

Every subsidiary proprietor must pay monthly contributions to two mandatory funds under the BMSMA:

Management Fund

The Management Fund covers the development’s recurring operational costs: security staff, cleaning, lift maintenance, utilities for common areas, insurance for common property, landscaping, and the Managing Agent’s fees. Monthly contributions are calculated proportionally based on each unit’s share value relative to the total share value of the development.

Sinking Fund

The Sinking Fund is a long-term capital reserve mandated by law. It must be used exclusively for capital expenditure — major items such as repainting the external facade, replacing lift systems, repairing waterproofing, or upgrading fire safety systems. Importantly, the Sinking Fund cannot be used for routine operational expenses.

The BMSMA requires the Sinking Fund contribution to be at least 10% of the Management Fund contribution. For older developments or those undergoing major upgrades, the BCA may direct a higher percentage. A well-funded sinking fund is a hallmark of a well-managed development — buyers should always request the latest sinking fund balance before purchasing a resale unit.

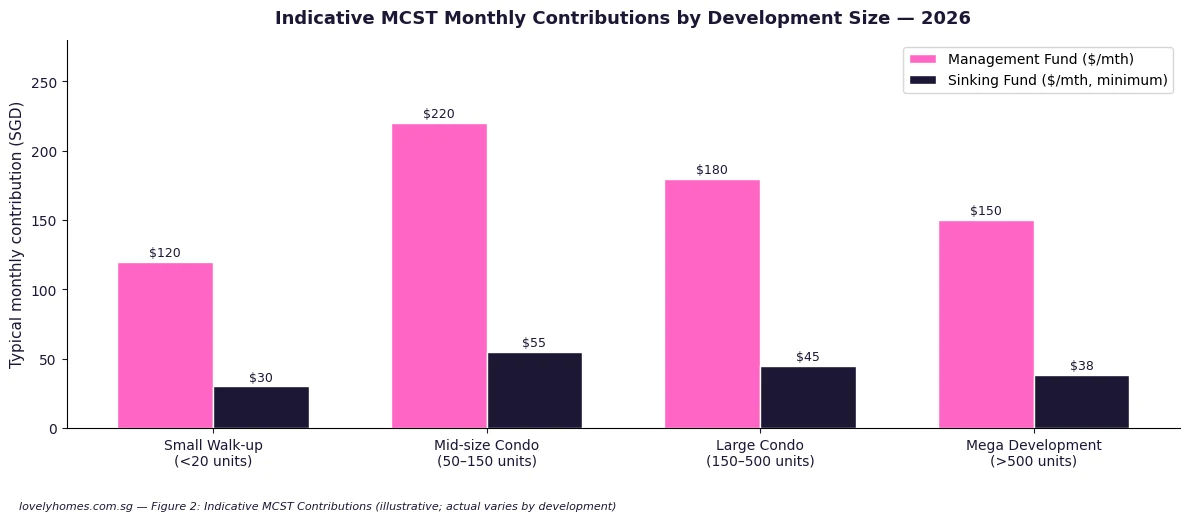

Contribution Rates: What to Expect

| Development Type | Typical Management Fund ($/mth) | Typical Sinking Fund ($/mth) | Notes |

|---|---|---|---|

| Walk-up / small condo (<20 units) | $80–$150 | $20–$40 | Lower amenities; higher per-unit cost for shared items |

| Mid-size condo (50–150 units) | $180–$280 | $45–$80 | Typical mass-market or OCR condo; pool, gym, BBQ pits |

| Large condo (150–500 units) | $150–$250 | $40–$70 | Economies of scale; facilities-to-unit ratio diluted |

| Mega development (>500 units) | $120–$200 | $30–$55 | Large-scale facilities; strong economies of scale |

| Luxury CCR condo | $350–$600+ | $90–$150+ | Concierge services, premium finishes, higher utilities |

Note: Contribution rates vary widely. Figures above are indicative only. Always check the actual budget prepared by your development’s MCST before purchase.

By-Laws: Rules Every Condo Resident Must Follow

Every MCST has a set of by-laws governing the use of units and common property. Singapore’s MCSTs operate under a two-tier by-law framework:

- Prescribed by-laws — default rules set out in the Second Schedule to the BMSMA. These cover noise, pets, renovation works, use of common facilities, and prohibited conduct in common areas. They apply automatically to every MCST unless specifically modified.

- Additional by-laws — rules adopted by the MCST at a general meeting (by special resolution) to supplement or modify the prescribed by-laws. Common additions include rules on airbnb-style short-term lettings, bicycle storage, deliveries, and smoking.

All by-laws are lodged with the SLA and are legally binding on all subsidiary proprietors, lessees (tenants), and occupants of the development. Breach of a by-law can result in a fine of up to $1,000 per offence, imposed after a Strata Titles Board order.

Renovation: MCST Approval Required

Renovation work that affects the common property, external facade, or structural elements requires MCST approval — in addition to any HDB or BCA permits where applicable. Even seemingly minor works — installing an additional air-conditioning unit, changing the main door design, or adding a glass panel to the balcony — may require written MCST consent. Always check with the Managing Agent before commencing any renovation.

Worked Example: Buying into a 200-Unit Condo — The True Monthly Cost

Mei Lin purchases a 2-bedroom, 800 sq ft unit in a 200-unit condominium in Bishan for $1.4M. The development was completed in 2012 and is 14 years old at the time of purchase.

| Item | Amount | Notes |

|---|---|---|

| Mortgage (25 yr, 3.2% p.a. bank loan) | ~$4,800/mth | Assuming 75% LTV ($1.05M loan); illustrative rate |

| MCST Management Fund contribution | ~$220/mth | Based on unit share value; includes security, cleaning, utilities |

| MCST Sinking Fund contribution | ~$55/mth | Minimum 10% of Management Fund; may be higher given building age |

| Property tax (owner-occupied) | ~$1,200/yr (~$100/mth) | At 2026 progressive owner-occupier rates (IRAS) |

| Home contents insurance (est.) | ~$25/mth | General contents coverage for a mid-range condo unit |

| Total monthly housing cost | ~$5,200/mth | Excluding ad hoc special levies; excluding utilities |

Note that for a 14-year-old building, the MCST may have already accumulated significant sinking fund reserves — or, conversely, may be facing a major capital cycle (external repainting, lift replacement, roof waterproofing) within the next 5–10 years. A well-managed MCST will present a 5-year capital expenditure plan at AGMs. Mei Lin should request the latest sinking fund balance, financial statements and AGM minutes before committing to purchase.

Resolving Strata Disputes: The Strata Titles Board

When disputes arise — between subsidiary proprietors, between an owner and the MCST, or between owners and the managing agent — the first port of call is mediation through the Singapore Mediation Centre or the Community Disputes Resolution Tribunal. If mediation fails, the Strata Titles Board (STB) provides a specialist adjudicative forum.

Common STB applications in Singapore include:

- Orders compelling the MCST to carry out repairs to common property.

- Applications challenging invalid AGM proceedings or improperly passed resolutions.

- Orders for recovery of unpaid contributions.

- Applications to invalidate by-laws or compel the MCST to enforce by-laws against a neighbour.

- Collective sale (en-bloc) consent orders (under the Land Titles (Strata) Act).

The STB has jurisdiction over disputes with a value up to $250,000. More complex or higher-value disputes are referred to the High Court. Legal fees in STB proceedings are generally lower than in court litigation, and many matters are resolved at the mediation stage without a full hearing.

Why Strata Management Standards Matter for Your Investment

Singapore’s private condo stock is maturing rapidly. The BCA’s Building Condition Rating (BCR) system — which evaluates developments on a 1–5 scale — shows that a significant proportion of condominiums completed in the 1990s and early 2000s are reaching critical maintenance thresholds. A poorly managed MCST with depleted sinking funds, deferred maintenance and acrimonious AGMs can materially reduce the market value and rental attractiveness of units within the development.

Conversely, a development with transparent governance, well-funded reserves, regular maintenance programmes and competent professional management commands a premium in both the resale and rental markets. Industry figures show that buyers increasingly request MCST financial statements and building condition reports as part of their due diligence — a trend that experienced conveyancing solicitors confirm has intensified since 2022.

The BCA’s Building Maintenance Masterplan, released in 2020 and updated in 2023, signals a regulatory direction towards mandatory 5-year building condition assessments and minimum sinking fund adequacy ratios for developments older than 20 years. These changes — if enacted — would directly affect contribution levels in older condominiums across Singapore.

What Might Change: BMSMA Amendments Expected

The Ministry of National Development (MND) and BCA have signalled further amendments to the BMSMA. Possible changes include: mandatory minimum sinking fund adequacy ratios (not just a 10% floor); reformed proxy voting rules to prevent vote concentration by a small number of owners; clearer rules on professional managing agent licensing; and improved transparency requirements for MCST financial reporting. These are under consultation as of June 2026 and have not yet been tabled in Parliament.

Frequently Asked Questions

Can I refuse to pay MCST contributions if I am unhappy with the management?

No. MCST contributions are a statutory obligation under the BMSMA — they are not discretionary. An unhappy owner’s recourse is to attend the AGM, vote against the incumbent council, stand for election to the Management Council, or apply to the STB if contributions have been improperly levied. Withholding contributions exposes the owner to legal action by the MCST, which can recover arrears (including interest and legal costs) through the courts or, ultimately, through enforcement against the unit.

How do I check the sinking fund balance before buying a resale condo?

Ask your conveyancing solicitor to request an estoppel certificate from the MCST as part of the purchase process. The estoppel certificate confirms (among other things) the outstanding contribution arrears attributable to the unit and the current state of the sinking fund. You may also request the most recent audited financial statements from the MCST or the managing agent — these are public documents that any subsidiary proprietor (and prospective buyer through their solicitor) is entitled to inspect.

What is a “special levy” and when can the MCST charge one?

A special levy is a one-off (or short-term) additional contribution levied on all subsidiary proprietors to fund an urgent or unplanned capital expense — for example, emergency structural repairs after an inspection reveals a defect, or to top up a depleted sinking fund ahead of a major cyclical maintenance programme. Special levies must be approved by a general meeting resolution. Like regular contributions, they are legally enforceable and pro-rated by share value.

Do I need MCST approval to renovate my condo unit?

For works confined entirely within your unit that do not affect the common property, structural elements or external appearance, MCST approval is generally not required — though you should notify the MCST and comply with renovation hours. However, any works that involve hacking structural walls, changing external finishes, altering air-conditioning condensers on external ledges, or modifying plumbing that serves common risers typically require written MCST approval. Always check with the managing agent before engaging any contractor, as unauthorised works can result in a reinstatement order at your cost.

Can my MCST ban short-term rentals (e.g., Airbnb) in my development?

Yes. An MCST may pass a by-law at a general meeting (by special resolution — 90% majority by share value) prohibiting short-term residential letting within the development. Many Singapore condominiums have passed such by-laws since the URA’s 2017 crackdown on unlicensed short-term accommodation. Even without a specific MCST by-law, letting a private residential property for fewer than 3 consecutive months requires URA approval (which is rarely granted for residential properties). Owners found subletting without URA approval face fines of up to $200,000 under the Planning Act.

What happens to the MCST and my contributions if the development goes en-bloc?

When a collective sale (en-bloc) is approved by the STB and completed, the MCST is dissolved. Sinking fund balances are distributed to subsidiary proprietors pro-rata by share value at the point of dissolution, after settling outstanding liabilities. This is a significant financial benefit of a successful en-bloc — the sinking fund distribution is in addition to the sale proceeds. Management fund balances are also distributed in the same way. All contributions stop on the date the sale is completed.

How do share values work and who sets them?

Share values are assigned by the developer at the point of the strata development’s registration, based on a prescribed formula in the Land Titles (Strata) Act. The formula takes into account each unit’s floor area, its floor level, and its entitlement to car park lots and other exclusive facilities. Once assigned, share values cannot be changed except through a court order. They determine each owner’s contribution quantum, voting weight at general meetings, and entitlement to sinking fund distributions on dissolution.

Related Articles

- Singapore En-Bloc Sale Guide 2026: Everything You Need to Know

- Singapore Property Buying Checklist 2026

- Conveyancing Guide Singapore 2026

- Singapore Stamp Duty Complete Guide 2026

- ABSD Singapore 2026: Complete Guide

- Singapore Home Loan Complete Guide 2026

- Singapore Property Tax Guide 2026

Disclaimer: This article is for general information only and does not constitute legal or financial advice. MCST governance, contribution rates and by-laws vary between developments. Readers should obtain the specific MCST financial statements and by-laws for any development they are considering purchasing or already own a unit in. Official resources: Building and Construction Authority (BCA), Ministry of Law (STB), Singapore Land Authority (SLA). Information accurate as of 10 June 2026.

Click anywhere to close | lovelyhomes.com.sg