Refinancing Home Loan Singapore 2026: Lock-In, Claw-Back and the Break-Even Test

Refinancing is the act of redeeming an existing home loan and replacing it with a new one — either with the same bank (a re-pricing) or a different bank (a refinance proper). Done well, it can save a Singapore homeowner tens of thousands of dollars over the life of the loan. Done badly, it can lock in penalties, clawed-back subsidies and notice-period interest that wipe out the gains. This guide walks through the entire 2026 mechanic — lock-in penalties, the four-gate decision sequence, the break-even maths, the TDSR re-test under MAS Notice 645, and a worked example on a S$1.2 million outstanding loan that captures a 1.95-percentage-point rate cut.

Quick Answer

- You can refinance once your lock-in period ends — most Singapore packages run 1–3 years; outside lock-in there is no redemption penalty.

- Switch bank or re-price the same bank if the new all-in rate beats the old by at least 0.5 percentage points AND the Year-1 saving covers the legal/valuation cost of about S$2,000–2,500.

- Banks claw back subsidies — legal fees and any cash rebate or interest credit — if you exit within 3 years of disbursement, even after lock-in ends.

- Send the redemption notice 3 calendar months before the switch; missing it costs one extra month of interest.

- Every refinance is re-stress-tested at 4.0% medium-term rate (MAS Notice 645) — your TDSR must still clear 55% of gross monthly income at that stressed rate.

- Start the comparison roughly 4 months before lock-in expiry; banks accept formal application 2–3 months before completion.

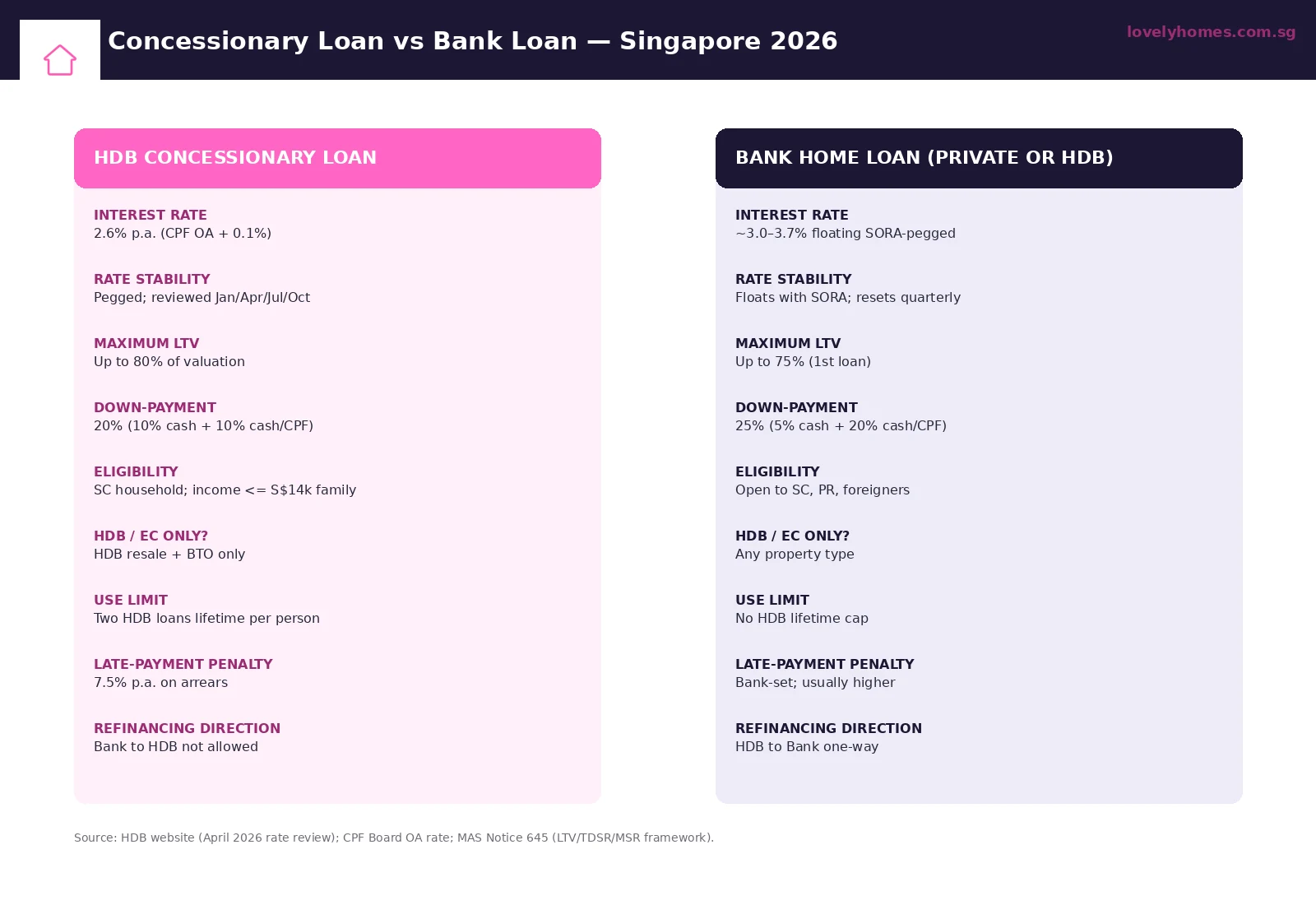

- HDB concessionary loan holders can refinance to a bank loan (one-way only — there is no path back to the 2.6% concessionary rate).

What “Refinancing” Actually Means in Singapore

In Singapore the word refinance covers two related but distinct moves. The first is a re-pricing — staying with the same bank but switching to one of its newer packages. The second is a refinance proper — redeeming the old loan and originating a fresh loan with a different bank. The economic logic is the same: capture a lower all-in rate or move from a floating package onto a fixed one. The legal and procedural overhead, however, is different. Re-pricing requires only an internal approval and a small admin fee. Refinancing involves a full credit re-underwrite, a new mortgage instrument lodged with the Singapore Land Authority, and conveyancing work that the new bank usually subsidises.

The key actors in any Singapore refinance are the bank, which sets the package and the claw-back rules; the law firm, which discharges the old mortgage and registers the new one; the valuer, instructed to confirm the property’s market value; and the Monetary Authority of Singapore, whose macro-prudential rules — TDSR, MSR (for HDB and EC) and the 4.0% medium-term stress rate — have to be met all over again on the refinance. It is the MAS rules, not the bank’s appetite, that often decide whether a refinance can proceed.

The 2026 Rate Environment

Refinancing demand follows the rate cycle. Through 2022–2024, three-month compounded SORA climbed from below 0.20% to a peak above 3.70%, dragging floating-rate mortgages into the 4–5% range and prompting a wave of homeowners to lock in fixed rates as a defensive move. Through 2025 and into early 2026, MAS’ policy-band re-centering and softer global rates pulled SORA back down sharply. By the first quarter of 2026, three-month compounded SORA was trading near its cyclical lows in the low single digits, with major retail banks publishing 1- and 2-year fixed rates in the 1.40%–1.80% band — a level that has not been routinely available to Singapore homeowners since the pandemic-era trough of 2020–2021.

That cyclical fall has flipped the refinancing logic. Anyone who locked in a fixed rate of 3.50%–4.00% in 2023 or who sat on a SORA-plus-spread package that re-priced higher through 2024 is now sitting on a meaningful gap to current pricing. The largest savings in 2026 are concentrated among loans originated in mid-2022 to early-2024 with three-year fixed periods that are now expiring or with floating-rate packages that have just left lock-in. The window does not stay open forever — fixed-rate pricing is highly path-dependent on swap-curve moves, and a single MAS policy meeting or a US Treasury sell-off can re-price the offer board within a week.

The Four Penalty Mechanics

Before computing any savings number, you have to know what the existing bank will charge you to leave. There are four levers, and a refinance only makes economic sense if the savings net of all four still beats zero.

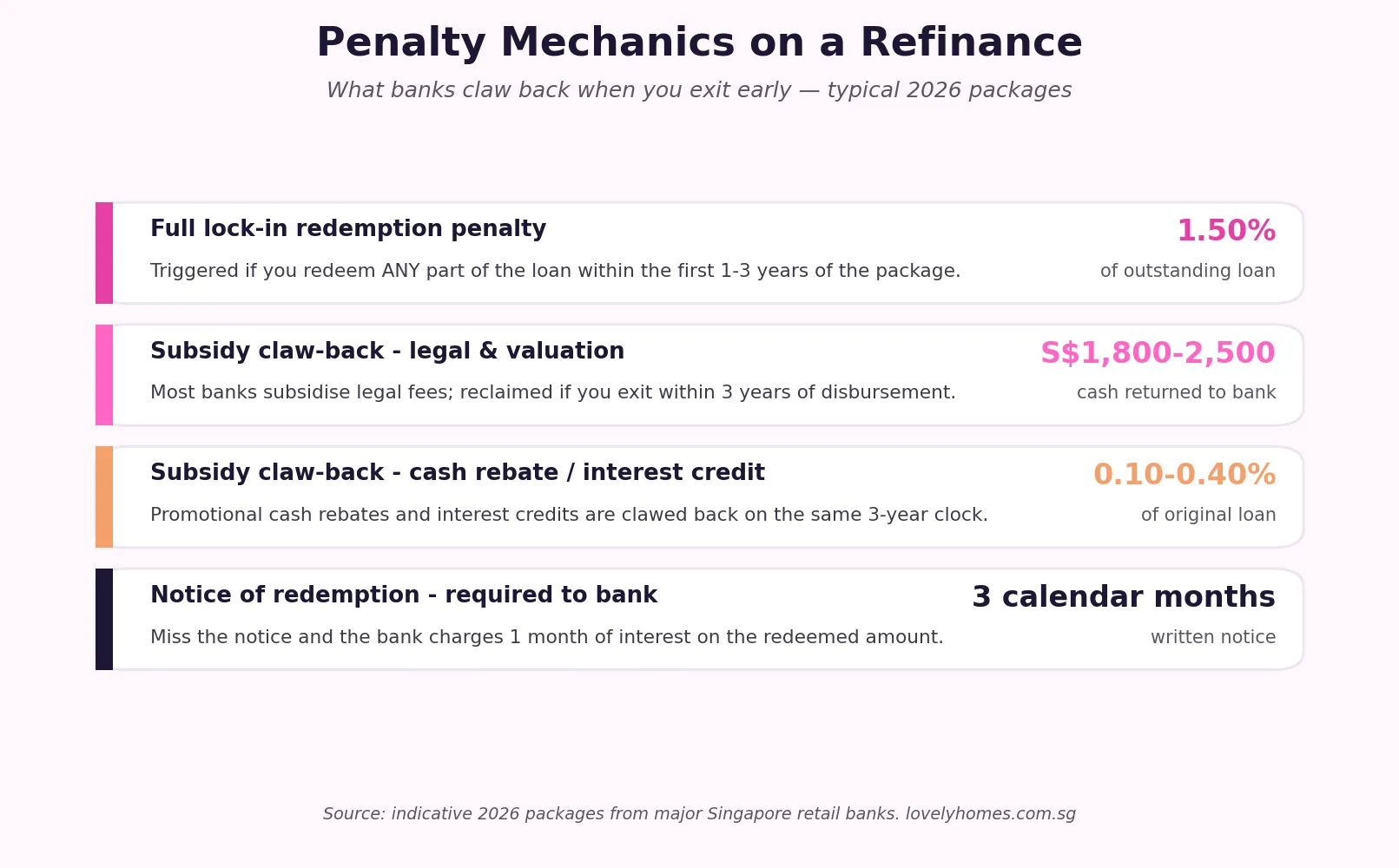

1. Full lock-in redemption penalty

Singapore banks typically charge 1.50% of the outstanding loan as a redemption penalty if you redeem any part of the loan inside the lock-in period — usually the first 1, 2 or 3 years of the package. On a S$1.2 million outstanding balance, that is S$18,000 cash. The penalty is not waived by partial redemption; it triggers on any reduction. The only legal carve-out is a forced sale (e.g. on divorce settlement under court order) and most banks negotiate around even that.

2. Subsidy claw-back — legal and valuation

To win the loan, the bank typically subsidises S$1,800–2,500 of legal and valuation cost. The contract clawback says: if you exit within three years of disbursement, you return that subsidy in cash. This is the most-missed cost line in homeowner refinance maths.

3. Subsidy claw-back — cash rebate / interest credit

Some 2024–2025 packages carried promotional cash rebates of 0.10%–0.40% of the original loan or interest credits worth a similar magnitude. Same three-year clock. If you took a 0.40% cash rebate on a S$1.2 million loan, that is a further S$4,800 returned if you refinance in Year 2.

4. Notice of redemption

The mortgage deed requires 3 calendar months’ written notice of redemption. If you give less notice, the bank is entitled to charge one additional month of interest at the prevailing rate on the redeemed sum. On a S$1.2 million loan at 3.50%, that is roughly S$3,500 — easily avoidable with proper sequencing, but routinely missed when borrowers chase a fast switch.

Cost of Switching — Itemised

| Item | Refinance (new bank) | Re-price (same bank) |

|---|---|---|

| Discharge of existing mortgage | S$300–500 | Nil |

| Conveyancing on new mortgage | S$1,800–2,500 (usually subsidised) | Nil |

| Valuation report | S$300–600 (often absorbed) | Nil to S$300 |

| CPF withdrawal / refund admin | S$30 per CPF Board form | Nil |

| Stamp duty on mortgage instrument | 0.4% of loan, capped S$500 | Nil |

| Net out-of-pocket (typical) | S$2,000–2,500 | S$300–800 (admin fee) |

The headline number — out-of-pocket cost of about S$2,000–2,500 — is the figure that has to be cleared before any savings start to flow to the borrower. Note also the asymmetry: a re-price with the same bank is materially cheaper, but the rate offered is rarely the bank’s sharpest. Re-pricing is the right play when lock-in expiry is too close to coordinate a clean external switch, or when the savings gap is small enough that conveyancing cost would erase it.

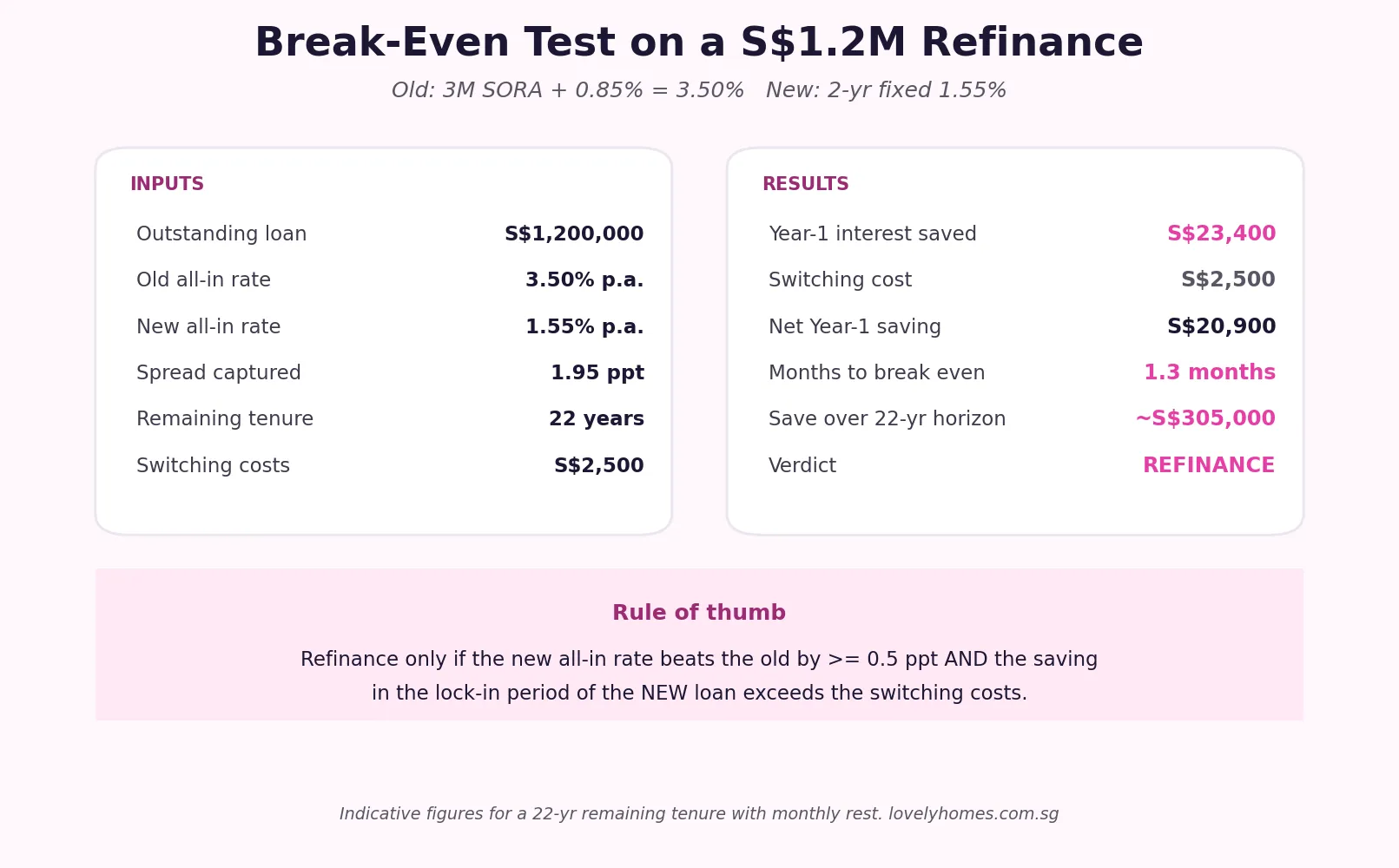

Worked Example: Mr and Mrs Goh, 22 Years Remaining

Mr and Mrs Goh own a 3-bedroom condominium in District 16, originally purchased for S$1.65 million in March 2021. Their original 30-year, 75% LTV bank loan of S$1.2375 million is now S$1,200,000 outstanding after five years of monthly amortisation. The loan was on a 3-year fixed rate of 1.95% from disbursement; that fixed period rolled in May 2024 onto a SORA-plus-0.85% floating package, which through 2025 floated up to a peak of 3.50% all-in. Their current monthly instalment is S$5,866.

It is now May 2026. The Gohs are out of lock-in. A 2-year fixed package is being offered by another bank at 1.55% all-in, with subsidised legal fees of S$2,500 and free valuation. Their original 2024 floating package never carried a cash rebate, so subsidy claw-back is nil.

Year-1 interest comparison. On a S$1,200,000 outstanding balance over 22 remaining years, year-one interest at 3.50% is approximately S$41,200. At 1.55% it falls to approximately S$17,800. The interest saving in Year 1 is S$23,400. The monthly instalment drops from S$5,866 to S$5,200 — about S$666 less per month, or roughly S$8,000 in cash flow per year, with the rest of the S$23,400 saving showing up as faster principal reduction.

Costs. Out-of-pocket cost is S$2,500 (the subsidy still partly applies but the Gohs need to top up). With the new bank’s lock-in starting again at 2 years, they would only refinance again in May 2028. The break-even point on the S$2,500 outlay is reached in 1.3 months of interest savings.

Verdict. Refinance. Total interest saving over the 22-year remaining tenure, assuming rates stay near 1.55%, is approximately S$305,000 in present value terms. Even if SORA reverts higher in Years 3–5, the locked 2-year fixed period means the Gohs capture most of the saving up-front. They should serve their 3-month redemption notice today, target completion at end-July 2026, and submit the new bank’s full credit application with payslips, bank statements and CPF contribution histories not later than the second week of June 2026.

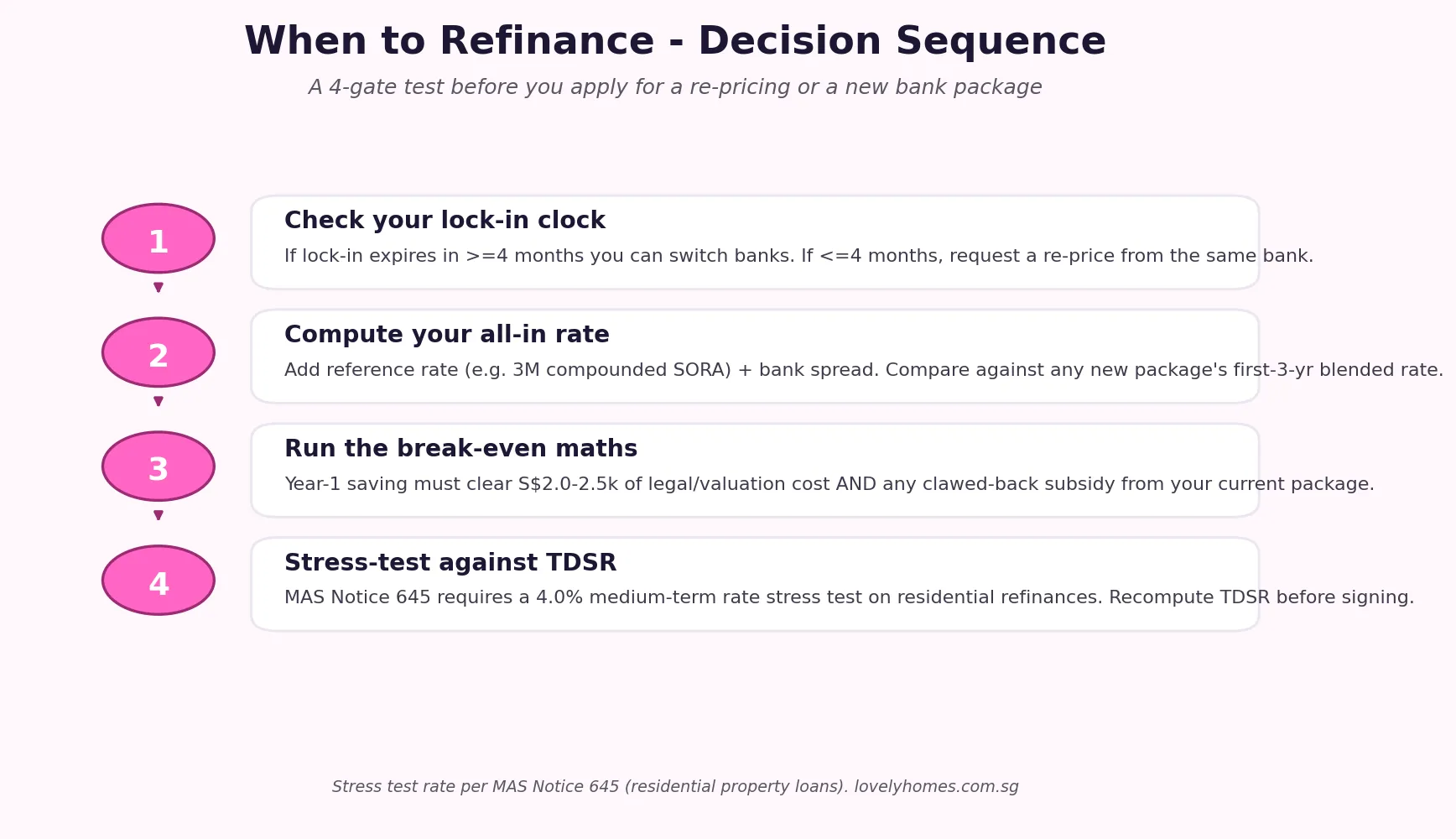

The Four-Gate Decision Sequence

Before any of the above is set in motion, every refinance candidate should pass four gates in order. Skipping a gate is how borrowers end up with a pretty rate but a worse outcome.

Gate 1 — Lock-In Clock

Pull your facility letter, identify the lock-in window, and count months to expiry. If lock-in ends in 4 months or more, you have time to run a full external comparison, give 3 months’ redemption notice, and switch banks cleanly. If lock-in ends in less than 4 months, the cleaner play is to ask your existing bank for a re-price first; you can switch later if their offer is uncompetitive.

Gate 2 — Compute Your True All-In Rate

Marketing rates and contractual rates are different things. Always compute your true all-in rate as reference rate + bank spread. For SORA-pegged packages, the reference is three-month compounded SORA published by MAS; for 2024-vintage packages it might be the bank’s Board Rate or its now-deprecated SIBOR series. Compare against the new package’s average rate over its first 3 years, not just the teaser Year-1 rate.

Gate 3 — Break-Even

The break-even formula is straightforward: (Old rate − New rate) × Outstanding loan × 1 year must comfortably exceed the sum of switching cost, claw-backs and notice-period interest. Anything where break-even falls outside the new lock-in period is a red flag — it means the bank can re-price you back up before you have recouped the cost of moving.

Gate 4 — MAS Notice 645 Stress Test

Every Singapore refinance is treated as a fresh credit decision. The Total Debt Servicing Ratio (TDSR) cap of 55% is recomputed using a stressed interest rate of 4.0% per annum for residential property loans (3.5% for non-residential), under MAS Notice 645. If your gross monthly income has fallen since origination, or your other debts (car loan, credit-card revolving balances, education loans) have grown, the new bank may decline the application even though the new rate is lower. Borrowers near the TDSR limit should rehearse the calculation before applying.

Re-Pricing vs Refinancing — Choosing the Right Move

| Dimension | Re-Price (same bank) | Refinance (new bank) |

|---|---|---|

| Out-of-pocket cost | S$300–800 admin | S$2,000–2,500 net |

| Time to completion | 3–4 weeks | 10–14 weeks |

| Rate sharpness | Usually 0.10–0.30 ppt above market | At market |

| Credit re-underwrite | Soft (TDSR re-check only) | Full — payslips, IRAS, CPF, credit bureau |

| Best when | Lock-in expiring <4 months; small spread; income volatility | Lock-in clean; spread > 0.5 ppt; sharp 2-yr fixed window open |

Special Cases — HDB Concessionary Loans, Joint Tenancies, Couples Decoupling

An HDB concessionary loan at the 2.6% statutory rate (CPF OA + 0.10%) cannot be refinanced back from a bank loan. The move is one-way. Households should compute very carefully: 2.6% is materially higher than the 1.40%–1.80% currently available from banks, but the HDB loan permits up to 80% LTV (versus the 75% bank cap), allows full CPF OA usage with no MSR-tightening on a refinance, and waives the MAS Notice 645 stress test. Younger households on tight cash flow often keep the HDB loan even when bank rates are lower, simply for the LTV and the safety of the statutory floor.

Joint-tenancy mortgages can be refinanced without disturbing the title, but any change in the borrowing party (for example, a mid-tenancy decoupling under tenancy-in-common) requires the property to be retitled at SLA before the new mortgage can be lodged. Couples planning a decoupling for ABSD reasons should sequence the title change first and the refinance second; doing both in parallel routinely fails because the new bank cannot register a charge against a title that is still being amended.

Why This Matters

Singapore homeowners frequently treat the original bank package as a sunk decision. It is not. With monthly instalments that run S$3,500–S$8,000 on typical condominium loans and total interest paid over 25 years that comfortably exceeds the original purchase price, every 0.5-percentage-point of rate captured is worth tens of thousands of dollars in lifetime cost. The mistake is not refinancing too often; it is forgetting that the option exists. Diligent homeowners run the four-gate test once a year, set a calendar reminder six months before lock-in expiry, and treat the refinance discussion as an ordinary part of household financial hygiene rather than a discretionary act.

What Might Come Next

The 2026 rate environment is unusually friendly to refinancers but not necessarily stable. Three forces could compress the window. First, sustained US Federal Reserve hold-or-cut signalling could pull SORA lower still and create even sharper fixed-rate packages — good for borrowers who wait, bad for those who lock in too early. Second, MAS’ policy band re-centering decisions taken in October 2025 and April 2026 are still working through the swap curve; a hawkish surprise at the next semi-annual review would push fixed rates back to the 2% range within weeks. Third, regulators have been studying whether to recalibrate the 4.0% medium-term stress rate now that the cyclical low is well-established; any reduction would expand TDSR headroom for marginal refinance candidates. The base case for 2026 is “refinance now, lock 2 years, re-evaluate in 2028” — but borrowers should rehearse the calculation rather than assume.

Frequently Asked Questions

When should I start comparing refinance packages?

Begin formally comparing packages roughly four months before your lock-in period ends. Banks accept refinance applications and issue Letters of Offer up to three months before the expected completion date, but credit underwriting takes 10–14 weeks. Starting earlier gives you the full window to negotiate the spread and re-stress your TDSR with comfort.

Can I refinance during my lock-in if the savings are enormous?

Mathematically yes — practically rarely. A 1.50% redemption penalty on a S$1.2 million loan is S$18,000 cash, plus subsidy claw-back of S$2,500–7,000, plus a forfeited month of interest. The new package would have to be at least 1.5–2.0 percentage points sharper than your current rate before the maths clears even in Year 1. In nearly every Singapore case, it is cheaper to wait the lock-in out.

Does refinancing reset the loan tenure?

Not by default. The new bank can match your remaining tenure (e.g. 22 years if that is what you have left). Resetting back to 25 or 30 years lowers the monthly instalment but increases total interest over the life of the loan; it also runs into the MAS-imposed maximum loan tenure of 30 years for HDB and 35 years for private property, with the borrower’s age at the end of the loan capped at 65 (or face a tighter LTV). For most refinancers the right move is to keep the existing remaining tenure and capture the rate cut as accelerated principal reduction.

Will my CPF be affected when I refinance?

If you used CPF Ordinary Account funds for the original property purchase, the accrued interest on those CPF withdrawals continues to accumulate regardless of which bank holds the mortgage. The CPF Board has to be notified of the change in mortgagee — your conveyancing lawyer files Form 1A on completion. There is no mid-tenancy refund or top-up triggered solely by a refinance.

What if my income has fallen since I bought the property?

Then the MAS Notice 645 stress test at 4.0% medium-term rate becomes the binding constraint, not the rate itself. If your gross monthly income today, stress-rated, no longer clears the 55% TDSR cap, the new bank will decline. Two practical fallbacks: (a) re-price with the existing bank, since re-pricing applies a softer TDSR re-check rather than a full underwrite; or (b) request a tenure extension on the new loan to compress the stress-test instalment, accepting the long-tenure trade-off.

Are fixed or floating rates better in 2026?

It depends on your conviction about SORA over the next 24 months. With three-month compounded SORA near cyclical lows, a 2-year fixed package locks in the saving and removes uncertainty — appropriate for households on tight cash flow or those who plan to sell within the lock-in period. A SORA-plus-spread floating package is sharper if you believe rates are still drifting down. Most homeowners in mid-2026 are choosing 2-year fixed, on the basis that further rate falls would not save much more in absolute dollars but rate rises could materially hurt.

Can I refinance from an HDB loan to a bank loan and back?

Refinancing from HDB concessionary to bank is a one-way move. Once the HDB loan is discharged, the household cannot return to the 2.6% statutory rate even if bank rates later spike higher. Households on tight cash flow should weigh that irreversibility carefully — the HDB loan also waives the MAS 4.0% stress test and permits 80% LTV. For borrowers with excellent buffers and a long horizon of expected low rates, the bank-loan route saves real money; for everyone else, the HDB loan’s optionality is worth keeping.

Related Articles

- TDSR Singapore 2026: How the 55% Cap and 4.0% Stress Test Decide Your Home Loan

- HDB Concessionary Loan Singapore 2026: The 2.6% Rate, 80% LTV and Two-Loan Lifetime Cap

- SORA-Pegged Mortgage Rates Singapore April 2026

- CPF for Property Purchase Singapore 2026

- Conveyancing Process Singapore 2026

- Decoupling Property Singapore 2026

Disclaimer

This article is editorial commentary for general information only and does not constitute mortgage advice, financial advice, tax advice or legal advice. Mortgage rates, package availability, claw-back schedules and credit policies vary by bank and change frequently. Always verify the current package terms directly with the lender’s Letter of Offer, consult MAS at mas.gov.sg for the prevailing macro-prudential rules including TDSR and the medium-term stress rate under MAS Notice 645, consult the CPF Board at cpf.gov.sg for CPF accrued interest and refund rules, and engage a qualified mortgage broker, financial adviser, or solicitor for any actual refinance decision. SORA fixings are published by MAS on its public benchmarks page; consult HDB at hdb.gov.sg for HDB concessionary loan terms.