En-Bloc Sale Process Singapore 2026: A Homeowner’s Step-by-Step Guide

Quick Answer

- An en-bloc (collective) sale is when the majority of owners in a strata development sell the entire site to a single buyer, normally a developer planning redevelopment.

- The legal framework is the Land Titles (Strata) Act 1967 (Cap. 158) and the regulator is the Strata Titles Board (STB).

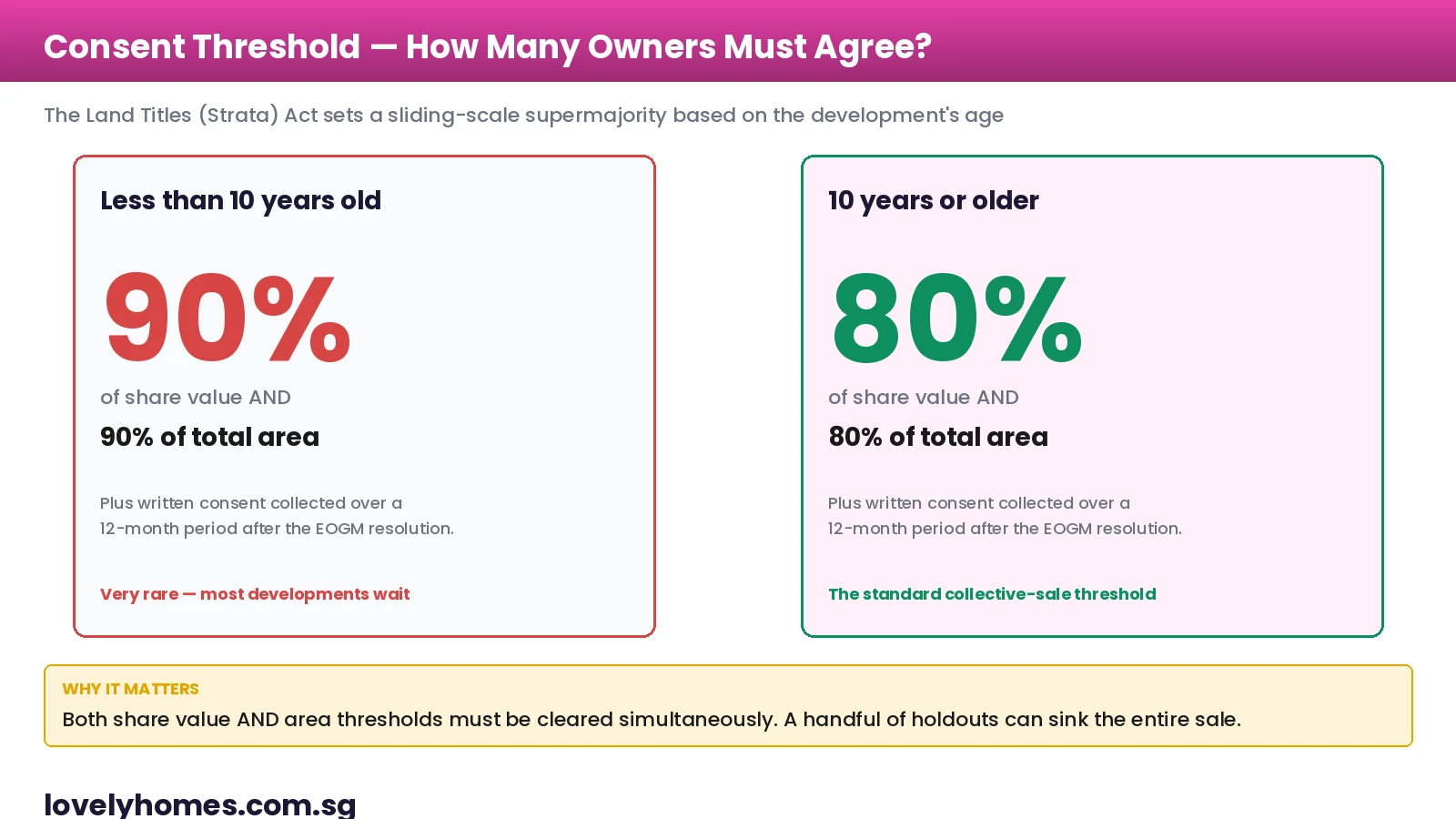

- The consent threshold is 80% of share value AND 80% of total area for developments at least 10 years old; 90%/90% for younger developments.

- The full process from idea to payout takes 18 to 30 months if everything goes well; failed attempts still consume 12-18 months of effort.

- Owners must elect a Sale Committee (CSC) at an EOGM. The CSC appoints a tender consultant and a lawyer through a competitive tender.

- Loyang Valley sold for S$880m in March 2026 — the largest residential en bloc since Thomson View. Activity is otherwise subdued; only two residential collective sales completed in 2025.

- Owners pay no stamp duty on the sale itself but ABSD applies on any replacement property; consider lease decay, tax leakage and the ABSD trap before voting yes.

What an En-Bloc Sale Actually Is

An en-bloc — short for “en bloc” — sale is a collective sale of every unit in a strata-titled development to a single buyer. Once the supermajority of owners agree and the Strata Titles Board approves the sale, the ownership of the entire estate transfers and the development is typically demolished and rebuilt at a higher density. The Singapore framework sits between two competing public-policy goals: protecting individual owners’ property rights, and freeing up well-located but ageing land for renewal so the city can densify.

The mechanism was created by the Land Titles (Strata) Act 1967 and significantly tightened in 1999 and again in 2007 after a wave of acrimonious sales. The current law gives owners robust procedural rights — STB scrutiny, mediation, the right to be heard — but the underlying economic deal is binary: 80% (or 90%) of share value and area must agree, and the remaining minority is then bound by the supermajority’s decision.

Who Initiates an En-Bloc Attempt?

Almost every successful collective sale begins with a small group of owners — usually two to five — who privately agree the development is undervalued, ageing, and primed for redevelopment. They circulate a paper at the next AGM, gauge interest informally, then call for an Extraordinary General Meeting (EOGM) to authorise the formation of a Collective Sale Committee.

The CSC is elected by simple majority and is bound by strict statutory duties of good faith. It must consist of at least three owners, ideally with a mix of demographics — younger families, retirees, investor-owners — so the committee credibly represents the development. The CSC is not paid; members serve voluntarily, although the tender consultant’s fee (between 0.5% and 1.0% of the sale price) is a substantial professional cost that comes out of the proceeds.

The Numbers That Decide Everything

An en-bloc sale lives or dies on two consent percentages and two financial numbers.

The consent percentages. These come from the Sixth Schedule of the Land Titles (Strata) Act. Below 10 years old, you need 90% of share value and 90% of total area. From the 10th anniversary onwards, the threshold drops to 80%/80%. Both numbers must clear simultaneously, calculated against the date the last owner signs the Collective Sale Agreement (CSA). The CSC has up to 12 months from launch to collect the signatures.

The reserve price. This is the lowest price the CSC is authorised to accept on the public tender. Set it too high and the tender fails outright; set it too low and minority owners can credibly argue at STB that the CSC did not act in good faith. The reserve price is supported by an independent valuation report from a SISV-accredited valuer and is normally pegged to a “redevelopment land value” benchmarked off recent comparable GLS bids.

The breakeven psf. This is the developer’s target — purchase price plus 35% land ABSD plus construction plus financing plus a target margin, divided by the gross floor area allowed by URA. If the breakeven psf comes out higher than what new launches in the same micromarket are achieving, no developer will bid.

The payout per unit. This is what each owner receives, calculated by a formula in the CSA — usually a hybrid of strata-area weighting, share-value weighting, and a uniform per-unit premium. The CSA must specify the formula on day one; you cannot change it after signing.

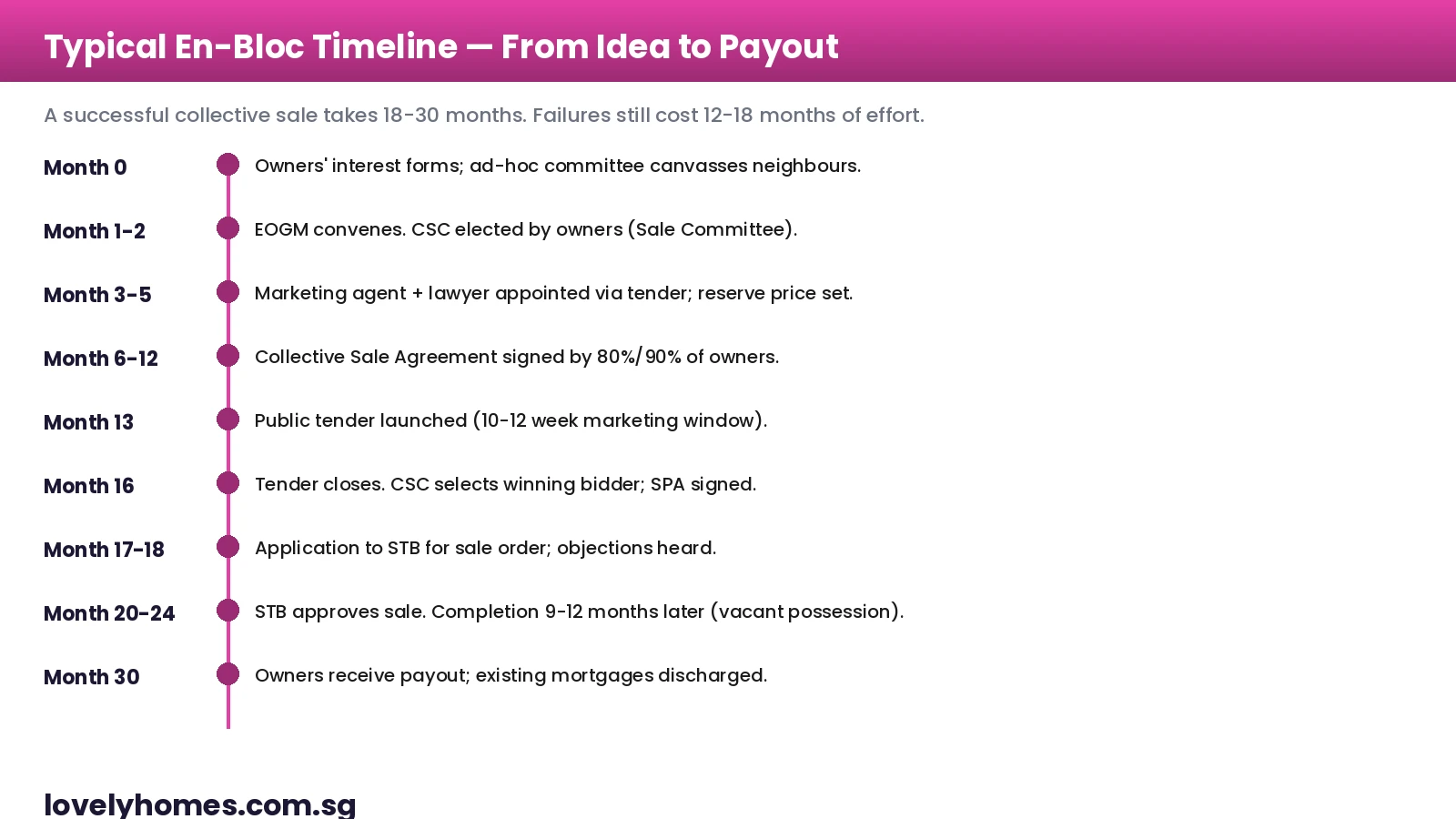

The Process Step by Step

Step 1 — Preliminary canvassing (Months 0-2). Informal interest forms; CSC elected at EOGM by simple majority; statutory affidavits filed.

Step 2 — Professional appointments (Months 3-5). CSC tenders the tender consultant appointment and the lawyer appointment. Both run on a no-deal-no-fee or lightly weighted fixed-fee basis. Parallel valuation engagement; reserve price drafted and agreed.

Step 3 — Collective Sale Agreement (Months 6-12). The CSA is the master contract that all consenting owners sign. It contains: the reserve price, the apportionment formula, the tender-consultant fees, the legal fees, the powers granted to the CSC, the cooling-off period (5 days), and the time-bar for revocation. STB will scrutinise this document closely.

Step 4 — Public tender (Months 13-16). The tender consultant runs a 10-12 week tender. Developers submit sealed bids. The CSC selects the highest acceptable bid above the reserve price; a Sale & Purchase Agreement (SPA) is then signed with the winning bidder, normally subject to STB approval.

Step 5 — STB application and hearing (Months 17-24). The CSC files Form 1 with the Strata Titles Board within four weeks of the SPA. STB serves notice on every owner; objecting minority owners may file written objections. Mediation typically follows; if no settlement, a contested hearing.

Step 6 — Completion and payout (Months 25-30). Once STB issues a sale order, vacant possession is delivered (typically 9-12 months later). Each owner’s outstanding mortgage and CPF Accrued Interest are repaid first; the net proceeds are then released to the owner.

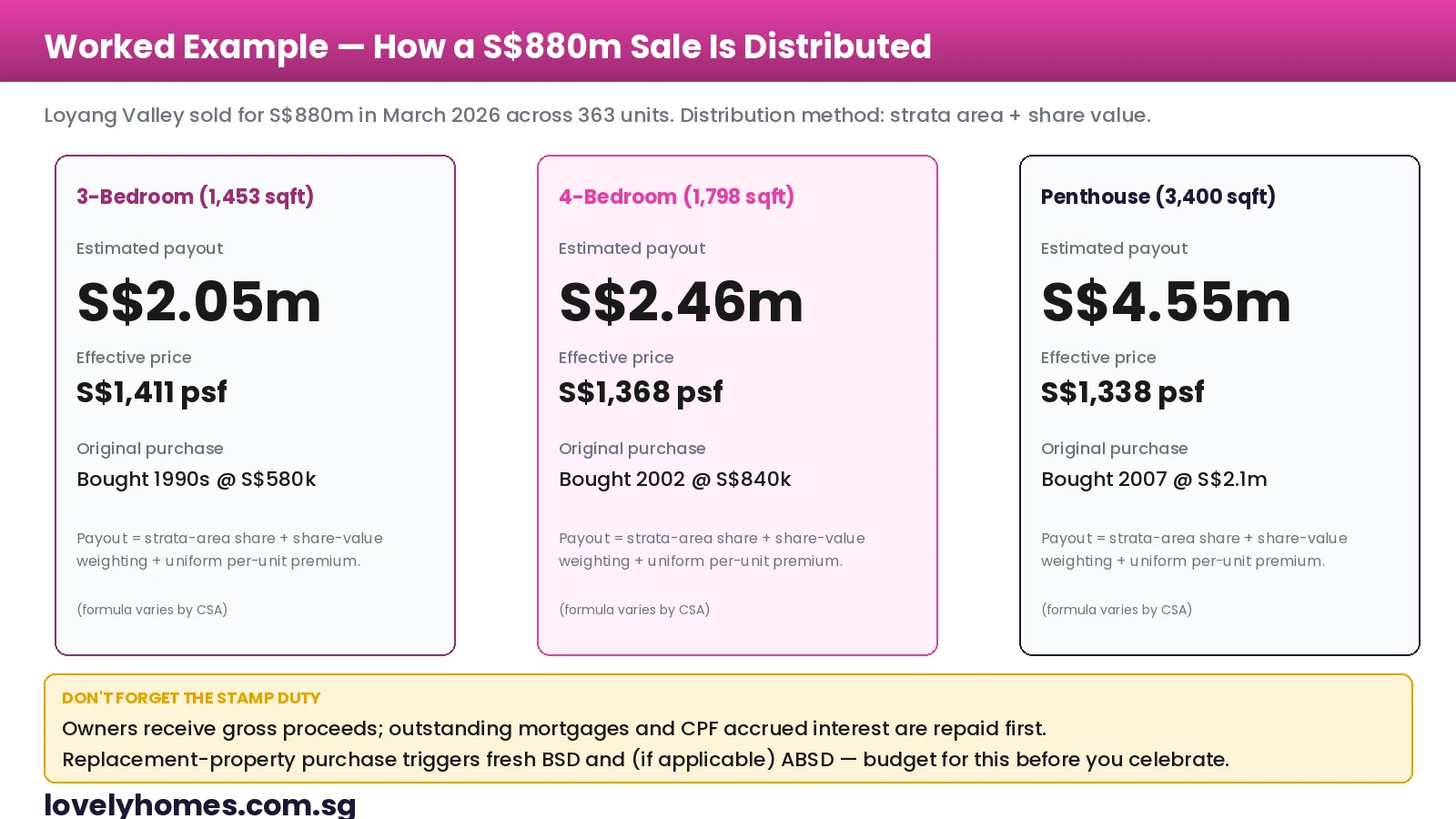

Worked Example — Distributing a S$880m Sale

Loyang Valley, the 363-unit Yio Chu Kang Road development that sold to SingHaiyi for S$880m in March 2026, illustrates the payout mechanics. The CSA used the standard hybrid formula: roughly 50% weighting on strata floor area and 50% on share value, with a small uniform per-unit premium. A 1,453 sqft three-bedder bought in the early 1990s at around S$580,000 walked away with approximately S$2.05m gross — a 3.5x return on the original purchase before adjusting for inflation. A 3,400 sqft penthouse received roughly S$4.55m.

The gross numbers are the headline, but the math owners actually care about runs net. Outstanding mortgage and CPF Accrued Interest are repaid before any cash leaves the lawyer’s escrow account. CPF Accrued Interest in particular has been compounding at 2.5% for decades, so an owner who used S$200,000 of CPF in 1995 is now seeing roughly S$590,000 deducted at completion.

The ABSD Trap That Catches Replacement Buyers

The single most common surprise for en-bloc sellers is the Additional Buyer’s Stamp Duty bill on their replacement property. Owners assume the en-bloc sale and the replacement purchase are the “same transaction”; the law says they are not. Once the en-bloc completes and the proceeds land, you are a Singapore citizen buying your second property — which currently attracts 20% ABSD on the new purchase price.

The remission you may be thinking of is for married couples buying a single matrimonial home: provided you sell your first property within six months of the new purchase, the ABSD on the second property is refunded. But the en-bloc payout schedule (typically 9-12 months for vacant possession) means the existing flat is sometimes not fully extinguished by the time you have committed to the new home. Sequence the purchase carefully and consult a conveyancing lawyer before signing the Option to Purchase on a replacement.

Why En-Bloc Activity Is Subdued in 2026

The market in 2025-2026 has been notably quiet, with only two successful residential collective sales completing in 2025 and Loyang Valley headlining the early-2026 cycle. Three structural forces are at work.

Land ABSD at 35%. Developers buying en-bloc sites pay 35% ABSD on the land cost (with a 5-year remission if all units in the new development are sold within five years of the date of contract). On a S$700m site that is S$245m of upfront cash. Combined with construction inflation, the breakeven psf for redeveloped units is S$2,800-3,200 — uncomfortable in many OCR submarkets.

Abundant GLS supply. The 1H 2026 Government Land Sales programme is large. Developers prefer GLS sites because they are pre-zoned, free of strata-title messiness, and avoid the ABSD payable on en-bloc land. Anecdotally, the same developer often will not bid for both a collective sale and a parallel GLS tender; they pick one.

Owner expectations. Owners have watched their estates rise at 5-7% per annum on the URA Property Price Index and now expect en-bloc premiums of 20-30% over individual market value. Developers can rarely price that.

Pros and Cons for the Individual Owner

| Pros | Cons |

|---|---|

| Premium of 20-40% over individual market value (when conditions are right) | Time and emotional cost — 18-30 months of meetings and uncertainty |

| Liquidity event for older owners with most of their wealth tied up in the home | Forced relocation; very few replacement options at the same psf in mature estates |

| Resets the lease clock — buyer normally redevelops on a fresh 99-year tenure | ABSD bill on replacement property if not sequenced carefully |

| Releases capital that may be redeployed into smaller, newer or yield-bearing assets | CPF Accrued Interest has compounded for decades; net cash often less than expected |

| Avoids ageing-estate maintenance levies and lift/cladding upgrades | For minority objectors, the supermajority decision is binding once STB approves |

What Minority Objectors Can Actually Do

If you are in the 20% who voted no, your statutory protections are real but narrow. You may file a written objection at the STB hearing on grounds set out in section 84A(7) of the Land Titles (Strata) Act: that the transaction is not in good faith having regard to the sale price, the method of distribution of the proceeds, or the relationships between the parties. You may also object on the grounds that the proceeds will be insufficient to redeem your outstanding mortgage and CPF — STB has historically given weight to genuine financial hardship in this scenario.

What you cannot do is force a higher sale price or insist on staying. If STB rules the sale was made in good faith, you must convey within the SPA’s completion period. Costs of objection are usually modest because STB is meant to be accessible to lay parties, but engaging a property lawyer is strongly recommended.

What Might Come Next

The en-bloc cycle in Singapore tends to swing on five-year horizons. The 2017-2018 cycle saw 38 successful sales in 18 months before cooling-measure tightening squeezed it. The 2021-2022 cycle saw a smaller wave. The current 2025-2026 cycle is so far measured in single-digit completions per year. The next significant catalyst would be either a meaningful cut in land ABSD for collective-sale sites, or a cut in the 80%/80% threshold to 75%/75% — both have been floated by industry but neither is on the legislative pipeline as of April 2026.

For owners in eligible developments, the practical advice is to sequence the conversation rather than wait for a perfect cycle. The base rate of CSCs that achieve a successful sale on the first attempt is below 30%, so plan for the long arc. For developers, sites with low plot ratios that can be uplifted under the latest URA Master Plan remain the only consistently viable plays.

Frequently Asked Questions

What is the difference between an en-bloc sale and a collective sale?

The two terms are used interchangeably in Singapore. “En bloc” is the historic French legal term that appears in older case law; “collective sale” is the term used in the Land Titles (Strata) Act and STB’s published forms. The mechanism is identical: the supermajority of owners selling the whole development as one parcel.

Can I refuse to sign the Collective Sale Agreement?

Yes. Signing the CSA is voluntary. If you do not sign, you are simply not part of the consent percentage. However, if the supermajority is achieved without you and STB approves the sale, you are still bound by the order to convey your unit at the apportioned price — refusal to sign the CSA only removes your voice from the proceeds-distribution negotiations, not your obligation to convey.

How is the share value of my unit calculated?

Share value is fixed at the time the development is granted strata title and is recorded in the strata roll held by the MCST. It is broadly proportional to floor area but with adjustments for unit type (penthouses and shop units typically get a slightly higher share value per sqft). You can check your share value on your management corporation’s records or on a recent maintenance-fee invoice.

What if my outstanding mortgage exceeds my en-bloc payout?

This is a “negative equity” scenario and is rare in Singapore but possible at older luxury sites where buyers paid peak prices. The mortgagee bank’s redemption is paid first; if the proceeds are insufficient, you owe the bank the shortfall. STB has historically given some weight to genuine financial hardship objections under section 84A(7) but cannot order a higher price.

Do I have to pay stamp duty on the en-bloc sale?

No. The en-bloc seller pays no stamp duty on the sale itself — stamp duty (BSD and, where applicable, ABSD) is payable by the buying developer on the purchase price. However, you do pay BSD and possibly ABSD on any replacement property you purchase. Plan the timing so that the matrimonial-home ABSD remission applies to the new purchase if you qualify.

Can the tender consultant guarantee a successful sale?

No, and any agent who promises one should be avoided. The tender consultant’s role is to run a competitive tender, advise on the reserve price, and prepare the marketing pack. Whether developers actually bid above the reserve depends on market conditions, the development’s location and density potential, and prevailing land ABSD rates. Fees are typically structured as no-deal-no-fee precisely because of this uncertainty.

What happens to my tenants if my unit is going through an en-bloc sale?

Existing tenancies survive the change of ownership but the new buyer (the developer) is unlikely to renew them. Most tenancies have a “redevelopment” or “early termination” clause anyway. If yours does not, the tenant is entitled to remain until the lease expiry; the developer will typically negotiate an early-termination payment to deliver vacant possession.