HDB Resale Levy Singapore 2026: Amounts, Who Pays, Exemptions and How It Works

- The HDB Resale Levy is a payment required when a second-timer household buys a new subsidised HDB flat or an Executive Condominium (EC) unit after previously enjoying a housing subsidy.

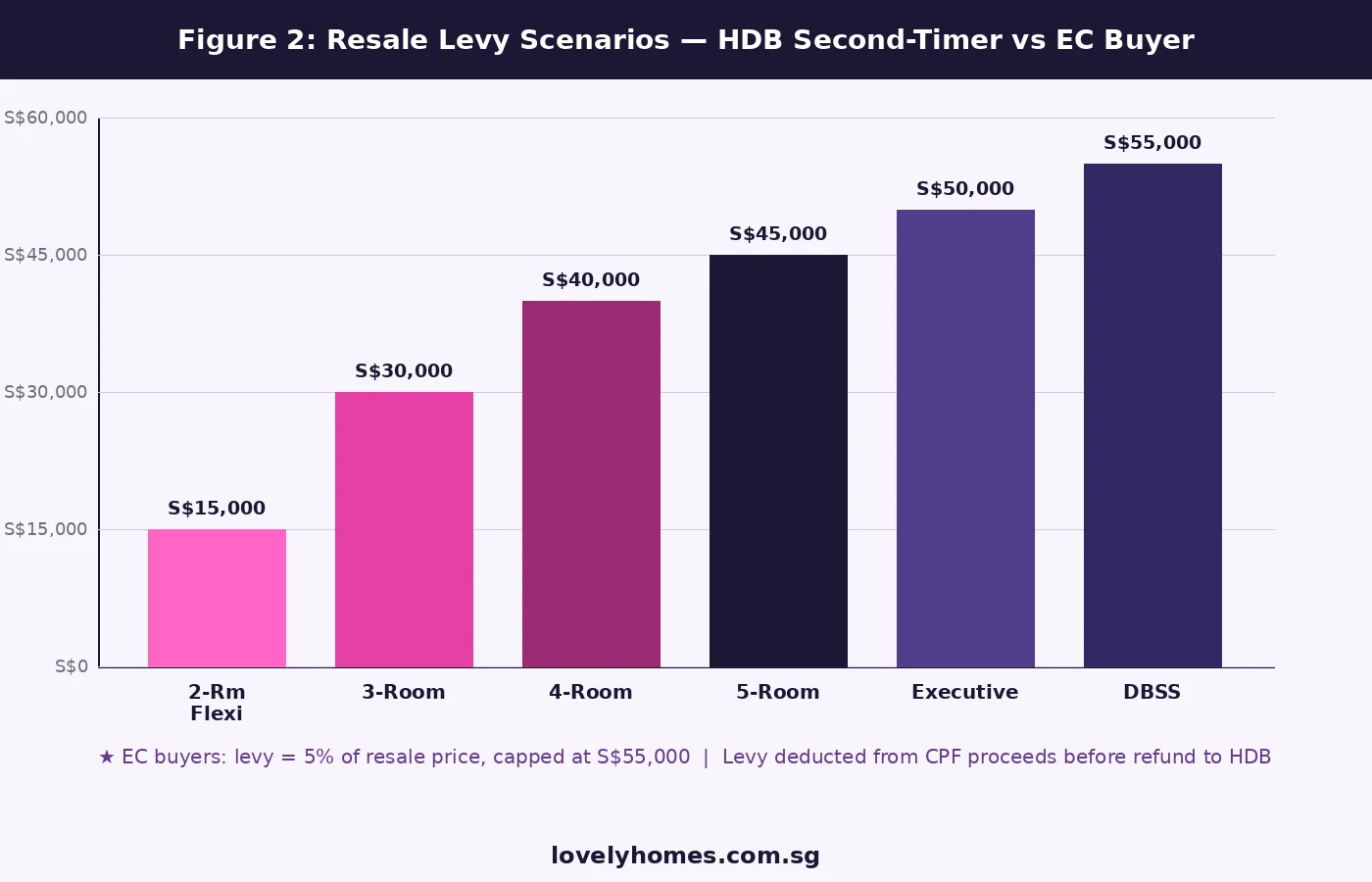

- Levy amounts range from S$15,000 (for a 2-Room Flexi sold) to S$55,000 (for a DBSS flat sold), with EC buyers paying 5% of resale price (capped at S$55,000).

- It is paid by deduction from the CPF refund when your first flat is sold — you do not write a cheque.

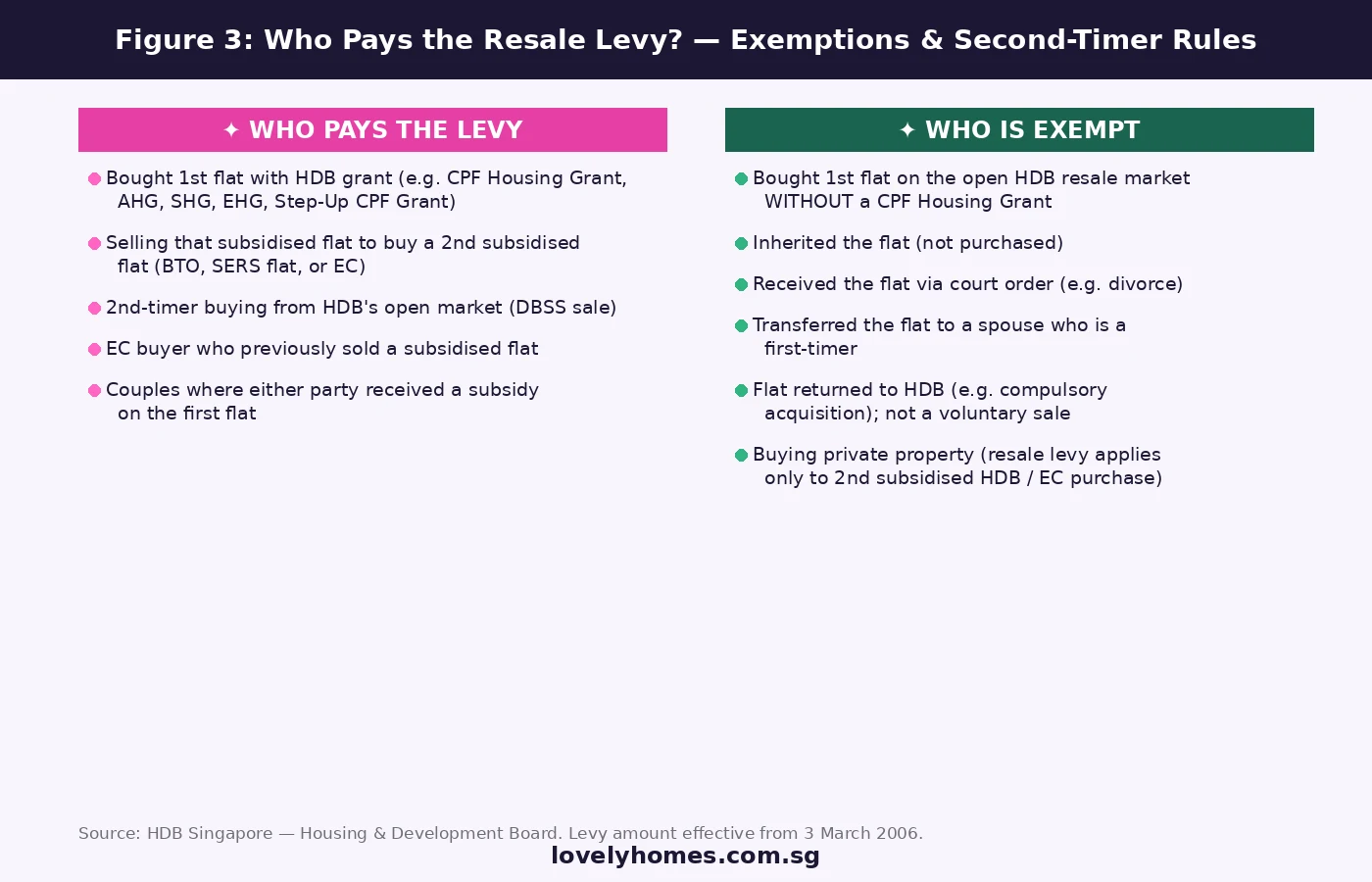

- Exemptions apply if you bought your first flat on the resale market without any CPF Housing Grant, inherited the flat, or received it via a court order.

- The levy does not apply when buying a private property — only a second subsidised HDB flat or EC triggers it.

- Getting the levy wrong can delay your second flat booking and result in owing HDB cash if your CPF proceeds are insufficient.

- From 3 March 2006, all levy amounts were fixed at the flat-type level — they are not a percentage of the first flat’s resale price (except for EC).

What Is the HDB Resale Levy?

The HDB Resale Levy is a subsidy recovery mechanism administered by the Housing & Development Board (HDB) under Singapore’s public housing framework. When the government provides a housing subsidy — such as the Central Provident Fund (CPF) Housing Grant, the Additional CPF Housing Grant (AHG), the Special CPF Housing Grant (SHG), or the Enhanced CPF Housing Grant (EHG) — it does so on the understanding that this benefit is tied to one subsidised flat per household. If that household later purchases a second subsidised flat or Executive Condominium unit, they are required to “return” a portion of the earlier subsidy benefit in the form of the resale levy.

The policy was introduced to ensure that public housing subsidies are targeted at households that genuinely need them and to maintain the long-term sustainability of Singapore’s public housing system. HDB administers the levy and collects it automatically at the point of sale of the first flat — it is not a separate bill sent to you but a deduction from your CPF Ordinary Account (OA) proceeds before they are refunded.

As at July 2026, the levy framework has remained stable since the flat-type rate schedule was fixed on 3 March 2006. Understanding it correctly is essential for any second-timer household planning to upgrade or right-size within the public housing system.

Who Pays the HDB Resale Levy?

You are required to pay the resale levy if all three of the following conditions are met:

- You (or your co-applicant, spouse, or essential occupier) previously purchased a subsidised HDB flat — meaning you received a CPF Housing Grant, AHG, SHG, EHG, Step-Up CPF Grant, or bought directly from HDB at a subsidised price in a Build-To-Order (BTO) or Selective En-bloc Redevelopment Scheme (SERS) exercise.

- You subsequently sold that subsidised flat (or are in the process of doing so).

- You are now applying to buy a second subsidised flat from HDB — either a new BTO flat, a SERS flat, a Design, Build and Sell Scheme (DBSS) unit, or an Executive Condominium (EC) unit from a developer.

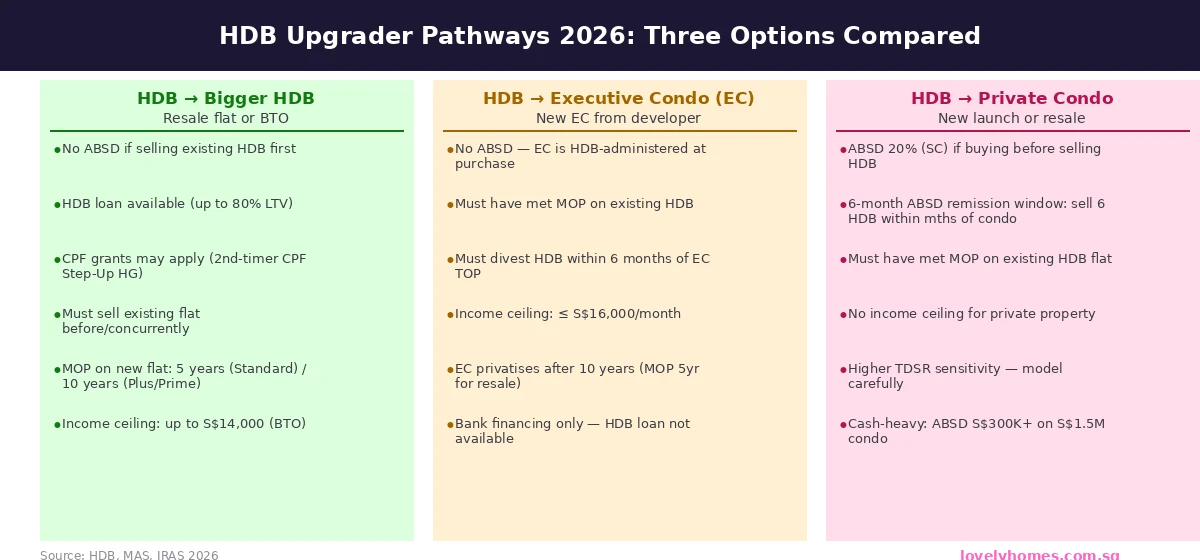

The key point is that the levy applies to subsidised second-time purchases only. If your second property is a private condominium, a landed home, a resale HDB flat (from the open market), or any commercial property, no resale levy is chargeable. Many upgraders mistakenly believe the levy applies whenever they buy a second property — it does not. It is specifically a tax on accessing public subsidies a second time.

Couples and Joint Applications

For married couples and joint flat buyers, the resale levy status of either party is taken into account. If either the main applicant or the co-applicant previously received a housing subsidy, the levy is applicable to the household. This prevents a household from circumventing the levy simply by swapping the person listed as main applicant on the second purchase. The rule is designed to capture the household’s cumulative subsidy benefit, not merely the individual’s.

Singles

Singles purchasing under the Single Singapore Citizen (SSC) scheme — eligible for 2-Room Flexi BTO flats — are also subject to the levy if they previously benefited from a housing subsidy. As the levy amount for a 2-Room Flexi flat is S$15,000, it is still a meaningful cost for solo buyers planning to upsize.

HDB Resale Levy Amounts (2026)

The levy amount depends on the type of flat you previously sold. Since 3 March 2006, the rates have been fixed at the following flat-type level:

| Flat Type Sold (First Flat) | Resale Levy Payable | Notes |

|---|---|---|

| 2-Room Flexi | S$15,000 | Applies to subsidised 2-Room Flexi BTO flats |

| 3-Room | S$30,000 | — |

| 4-Room | S$40,000 | Most common upgrader profile |

| 5-Room | S$45,000 | — |

| Executive Flat | S$50,000 | HDB Executive flat (not EC) |

| DBSS Flat | S$55,000 | Design, Build and Sell Scheme (discontinued) |

| EC (Executive Condominium) | 5% of resale price | Capped at S$55,000; applies after the EC’s 5-year MOP when sold on the open market |

One common source of confusion is that the levy is based on the type of flat you sold, not on its resale price. Whether you sold your 4-Room flat for S$500,000 or S$900,000, the levy is always S$40,000. The EC rule is the sole exception: there the levy is 5% of the EC’s resale price (i.e. the proceeds from selling the EC), subject to a maximum of S$55,000.

How and When Is the Resale Levy Paid?

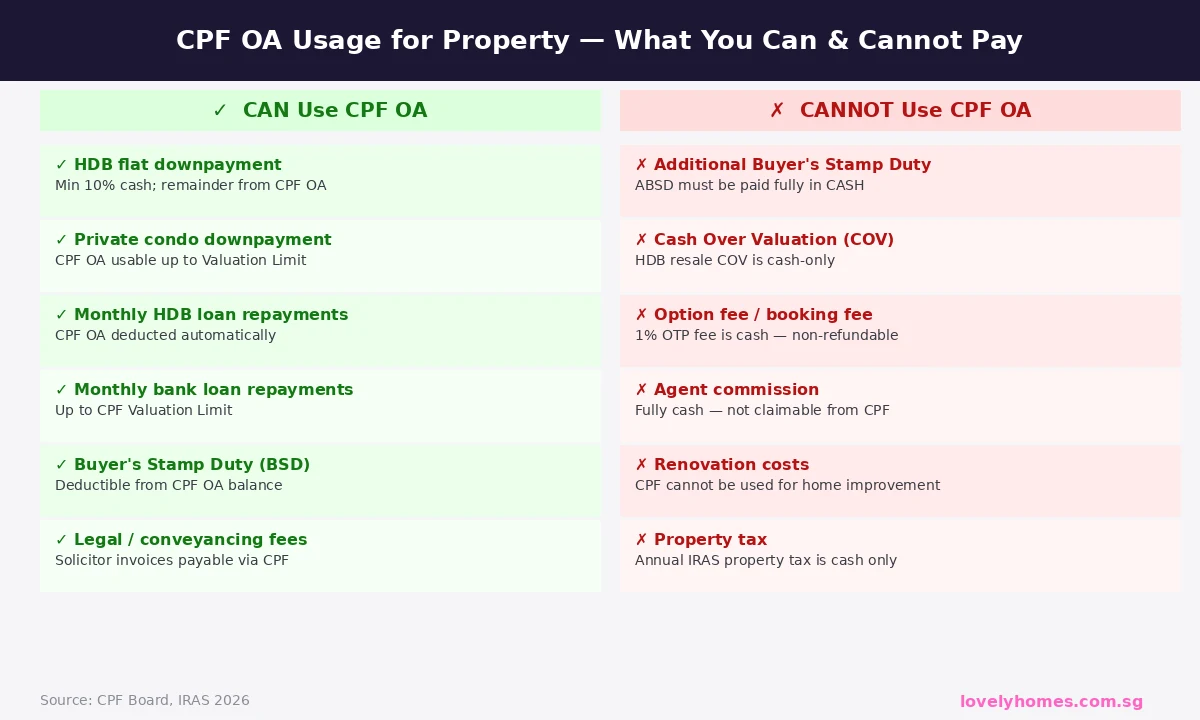

The resale levy is settled automatically at the completion of the sale of your first flat. HDB deducts the levy amount from the CPF Ordinary Account (OA) refund you would otherwise receive when the flat sale is completed. You do not receive a separate invoice from HDB and you do not make a cash payment at any counter.

Here is how the sequence works:

- Apply to buy second flat: When you apply for a BTO flat or EC as a second-timer, HDB identifies your levy status at the point of application.

- HDB confirms levy payable: HDB notifies you of the levy amount in the appointment letter for your second flat booking.

- First flat sold: On the day of the legal completion of your first flat sale, the CPF Board refunds your OA principal and accrued interest as usual — but before the refund is credited to you, HDB deducts the levy amount directly from those CPF proceeds.

- Balance returned: The net CPF refund (after levy deduction) is credited to your OA account.

What If Your CPF Refund Is Less Than the Levy Amount?

This can happen in rare situations — for instance, if the outstanding HDB loan and CPF accrued interest together consume most of the sale proceeds. In such cases, the shortfall must be made up in cash. HDB will require you to pay the difference out-of-pocket before the second flat booking proceeds. This is one reason why financial planning ahead of an upgrade is important: always model your net CPF position against the levy amount before committing to a second BTO application.

Who Is Exempt from the HDB Resale Levy?

Not everyone who has previously owned an HDB flat will be required to pay the resale levy. Key exemptions include:

- Resale flat purchased without a CPF Housing Grant: If you bought your first flat on the open HDB resale market and did not receive any CPF Housing Grant (Family Grant, Enhanced Housing Grant, Proximity Housing Grant, or any earlier-generation grant), you are not a “subsidised” flat owner for levy purposes. The levy reflects subsidy recovery — without a subsidy, there is nothing to recover.

- Inherited flat: If the flat was left to you in a will or through intestacy, you did not receive a direct purchase subsidy, so the levy does not apply.

- Court order transfer: Flats transferred to one party as part of a divorce settlement are generally exempt because the transfer is not a voluntary purchase attracting a subsidy.

- Private property purchasers: The levy applies only when the second purchase is a subsidised BTO flat or EC. Upgraders to private property are not subject to the levy — though they face ABSD (Additional Buyer’s Stamp Duty) instead.

- Flat returned to HDB involuntarily: If your first flat was compulsorily acquired by the government (e.g. for road widening or MRT works), this is not considered a voluntary sale and the levy is not triggered.

Worked Example: The Tan Family’s Second BTO Application

Mr and Mrs Tan (both Singapore Citizens) purchased a 4-Room BTO flat in Tampines in January 2019 at S$420,000, using a CPF Housing Grant of S$40,000. They have fulfilled the 5-year Minimum Occupation Period (MOP) and sell the flat in July 2026 for S$710,000.

They are applying for a new 5-Room BTO flat in Tengah at a subsidised price of S$620,000 — a second subsidised HDB purchase, making them second-timers.

Levy Calculation

| Flat type sold | 4-Room |

| Resale Levy payable | S$40,000 |

| Sale price of 1st flat | S$710,000 |

| Outstanding HDB loan (est.) | S$235,000 |

| CPF principal + accrued interest refund | S$278,000 |

| Levy deducted from CPF refund | – S$40,000 |

| Net CPF refund after levy | S$238,000 |

| Net cash proceeds | S$710,000 − S$235,000 (loan) − S$278,000 (CPF) = S$197,000 cash |

The Tans’ second flat purchase proceeds normally. The S$40,000 levy is handled automatically by HDB and CPF Board; neither party needs to make a separate payment. The net cash received is S$197,000, which can go toward the downpayment and costs of the new flat.

Special Situations and Edge Cases

EC Owners Selling and Buying a Second BTO

If you bought an EC (fully privatised after 10 years) and now wish to purchase a new BTO flat, you are subject to the resale levy at 5% of the EC’s resale price, subject to a maximum of S$55,000. Because EC prices have risen significantly — many ECs in mature estates now resale at S$1.2M–S$1.8M — the effective levy is almost always the capped S$55,000. For example, an EC sold for S$1.4M would attract a levy of S$70,000 in the absence of the cap; the cap holds it at S$55,000.

SERS Flat Recipients

Households that received a replacement flat under the Selective En-bloc Redevelopment Scheme (SERS) are treated as having received a housing subsidy. If they subsequently wish to buy a second new flat from HDB or an EC, the levy applies based on the type of flat they were re-housed in.

Divorce and Reassignment of Flat Ownership

When a flat is transferred to a divorced spouse under a court order, that spouse is considered a second-timer if the transferred flat was a subsidised purchase. If they later apply for a new BTO flat, the levy will apply. Seeking early legal advice on how divorce asset division affects CPF and HDB subsidy status is advisable.

Concurrent Applications

Some second-timers apply for a BTO flat while still occupying their first flat. HDB allows this — but the levy is held in reserve and deducted at the point of the first flat’s sale completion. You must sell your first flat within 6 months of collecting the keys to the second (this is the standard condition for second-timers purchasing new flats).

Why the Resale Levy Matters for Your Upgrade Strategy

The resale levy is one of several interlocking costs that second-timer households must budget for when planning an upgrade within the public housing system. It is easy to overlook because it is deducted automatically from CPF, making it feel invisible — but it directly reduces the cash and CPF resources available for your second flat.

Consider the total cost of a 4-Room BTO upgrade: beyond the flat price itself, a second-timer household must account for the Buyer’s Stamp Duty (BSD) on the new flat, legal fees, potential income grant reductions (second-timers receive smaller EHG amounts than first-timers), renovation costs, and the S$40,000 resale levy. These costs collectively can reduce the effective CPF buffer you have on hand.

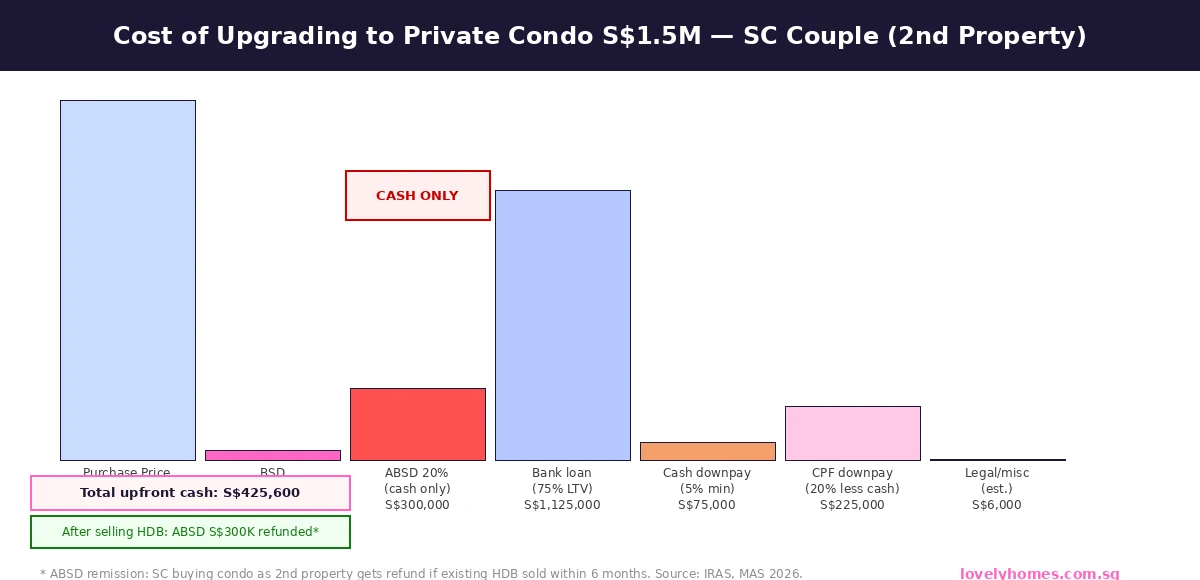

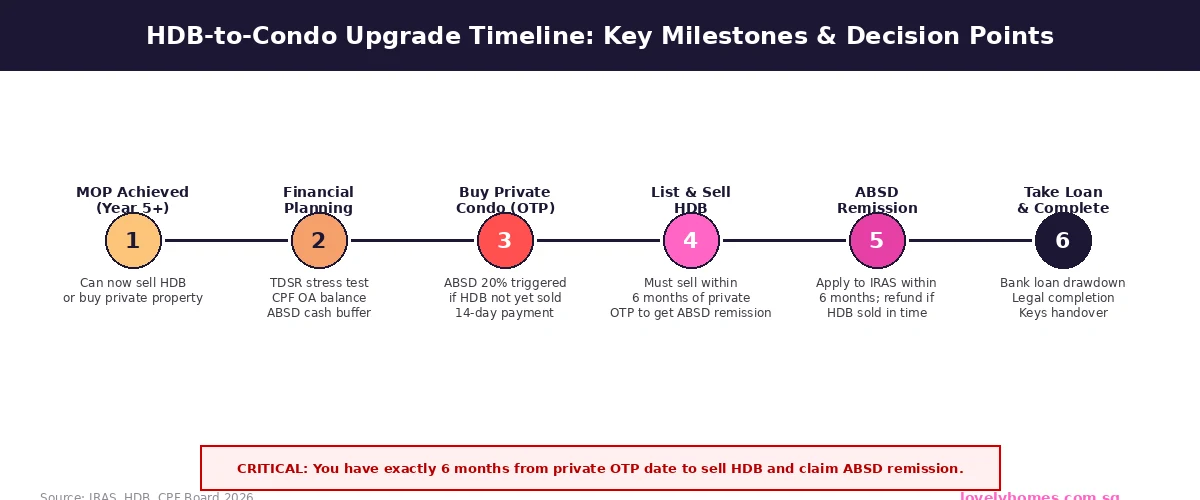

In contrast, upgrading to private property involves no resale levy — but attracts ABSD of 20% as a second property purchase (if you own the HDB flat at the time of buying private, and have not yet sold it). The ABSD on a S$1.5M private property would be S$300,000 — a very different magnitude. Households navigating this choice should consider the full cost picture of each route. Our ABSD Singapore 2026 Complete Guide and HDB Upgrader Guide 2026 cover the private-property upgrade path in detail.

Frequently Asked Questions — HDB Resale Levy 2026

Q1. Can I avoid the resale levy by selling my flat before applying for the BTO?

No. Your levy status is determined by your subsidy history, not by the sequence of sale and purchase. Whether you sell before or after booking the BTO flat, the levy still applies because you previously received a CPF Housing Grant. Selling early may give you more CPF OA funds to draw on, but it does not remove the levy obligation.

Q2. My spouse is a first-timer. Does the household still pay the levy?

Yes. HDB assesses the household as a unit. If either the main applicant or co-applicant has previously received a housing subsidy, the entire household is classified as a second-timer for levy purposes. There is no mechanism to apply as a “first-timer” household if one party is a second-timer. However, in this situation, the household may be eligible for a reduced levy in some cases — consult HDB directly for your specific profile.

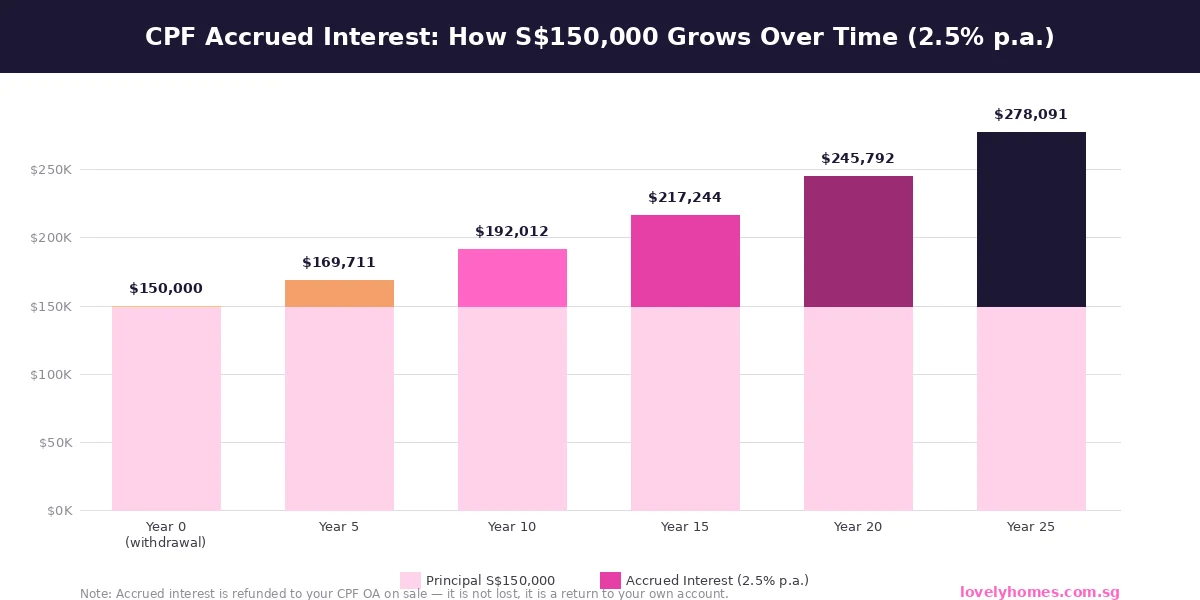

Q3. Is the resale levy the same as the CPF accrued interest I must return?

No — these are two completely different obligations. CPF accrued interest (at 2.5% p.a.) is the amount you owe your own CPF account for the OA savings you withdrew to pay for the flat. It is returned to your OA upon sale — you are repaying yourself. The resale levy, in contrast, is paid to HDB as a subsidy recovery charge. Both deductions happen at the point of sale, but they serve entirely different purposes and go to different places.

Q4. Can I use CPF to pay the resale levy, or must it come from cash?

The levy is deducted automatically from the CPF OA refund you receive when your first flat is sold. You do not need to arrange a separate cash payment unless your CPF refund is insufficient to cover the levy — in which case HDB will require the shortfall in cash before releasing the booking fee for your new flat. Always check your estimated CPF refund against the applicable levy amount before committing to a second BTO booking.

Q5. Does the resale levy apply if I buy an EC as a first-time EC buyer but sold an earlier subsidised flat?

Yes. If you are buying an EC and you previously sold a subsidised HDB flat, the resale levy is payable. The EC levy is the higher of: 5% of the resale price of your sold flat or (if you are selling a non-EC subsidised flat) the flat-type levy amount — unless you are selling the EC itself, in which case it is 5% of the EC’s resale price (capped S$55,000). HDB’s levy assessment letter, issued before your EC booking, will specify the exact amount applicable to your situation.

Q6. Has the HDB resale levy changed recently? Will it increase?

The flat-type levy rates have been unchanged since 3 March 2006. As at July 2026, there has been no announcement by HDB or the Ministry of National Development (MND) of any impending change to the levy framework. Given that BTO prices have risen considerably since 2006, some analysts have speculated that a levy increase is overdue — but this is speculative. Decisions on the levy are policy matters resting with MND. Monitor HDB press releases and MND Budget announcements for any changes.

Q7. What happens if I cannot sell my first flat in time to pay the levy before the second flat completion?

Second-timers purchasing a new HDB flat must generally sell their existing flat within 6 months of collecting the keys to the new flat. If you have not sold your first flat by the time you need to complete the purchase of the new flat, HDB may defer key collection or require you to arrange an interim cash payment for the levy amount. Contact HDB directly if your sale is delayed — they may grant a time extension in genuine cases, but this is not guaranteed and is assessed case by case.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- HDB Upgrader Guide 2026: Steps, Costs, ABSD Remission and Timing

- HDB MOP Singapore 2026: Complete Guide to the Minimum Occupation Period

- Singapore CPF for Property Guide 2026: OA, Valuation Limits and Accrued Interest

- HDB Downpayment Guide 2026: How Much Cash Do You Need?

- Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained

- Singapore Property Cooling Measures 2026: ABSD, TDSR, LTV and SSD