Morrison Lane GLS Reserve List 2026: 205-Unit Mohamed Sultan Plot Joins Holland Plain Tender Wave

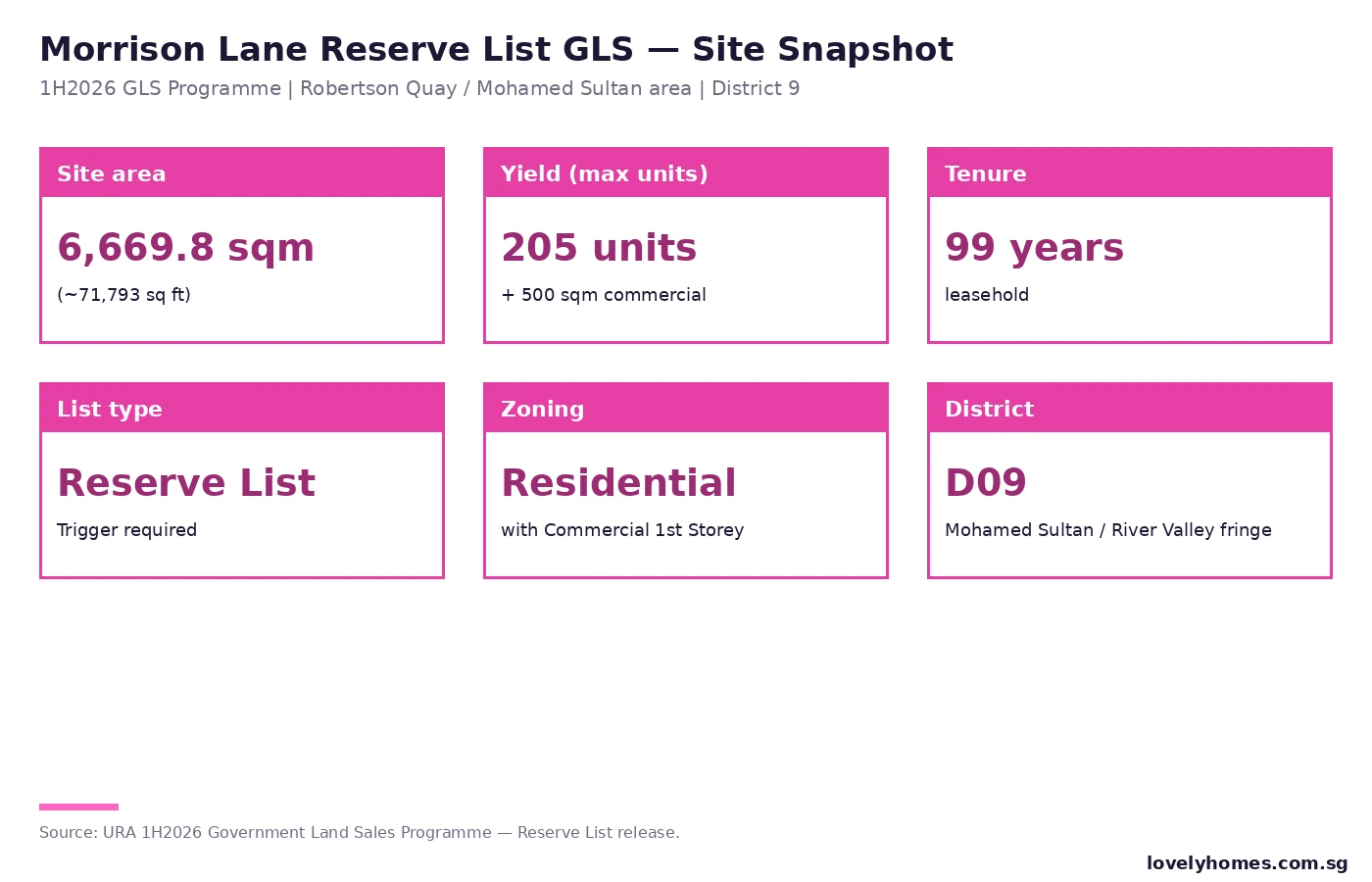

In the same week URA’s Holland Plain Confirmed-List tender prepares to close on 7 May 2026, the Authority has quietly added a second District 9 site to the live pipeline: Morrison Lane, a 6,669.8 sqm Reserve-List plot at Mohamed Sultan that can yield about 205 private residential units plus 500 sqm of first-storey commercial space. Reserve-List sites only go to tender if a developer triggers them by tabling a minimum bid the government accepts — making Morrison Lane a useful real-time read on developer appetite for the Robertson Quay / River Valley corridor at this point in the cycle.

Quick Answer

- URA has released the Morrison Lane Reserve-List GLS site at Mohamed Sultan in District 9 under the 1H2026 GLS Programme.

- Site area 6,669.8 sqm (~71,800 sq ft); maximum yield about 205 units + 500 sqm first-storey commercial.

- Tenure: 99-year leasehold; zoning Residential with Commercial at 1st Storey.

- As a Reserve-List site, it goes to tender only if a developer submits an acceptable trigger bid.

- Industry watchers see a moderate chance of trigger, dependent on the Holland Plain tender result (closing 7 May 2026) and the broader CCR launch pipeline.

- Indicative trigger price band: S$1,400–S$1,550 psf ppr, implying a launch ASP of ~S$2,800–S$3,000 psf.

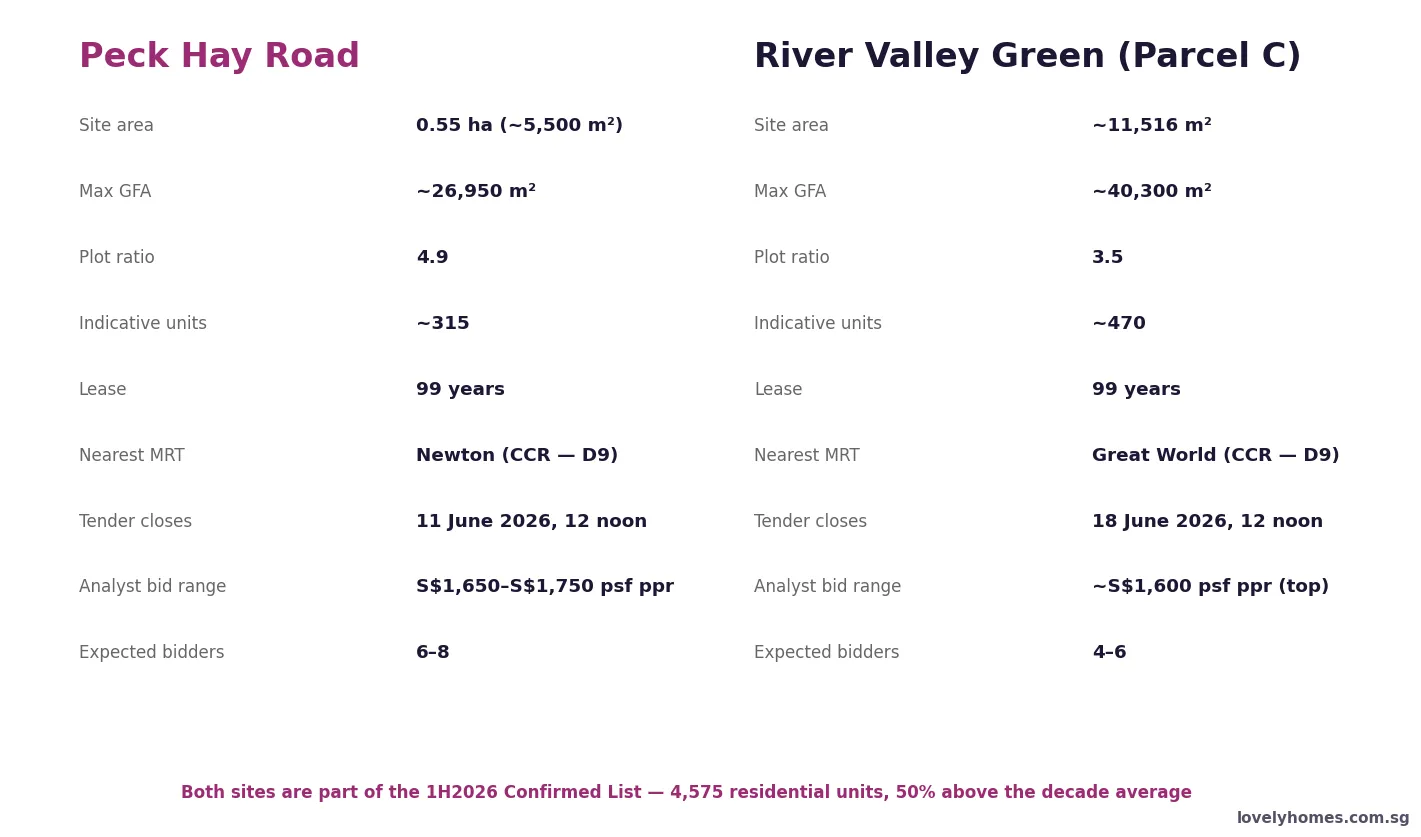

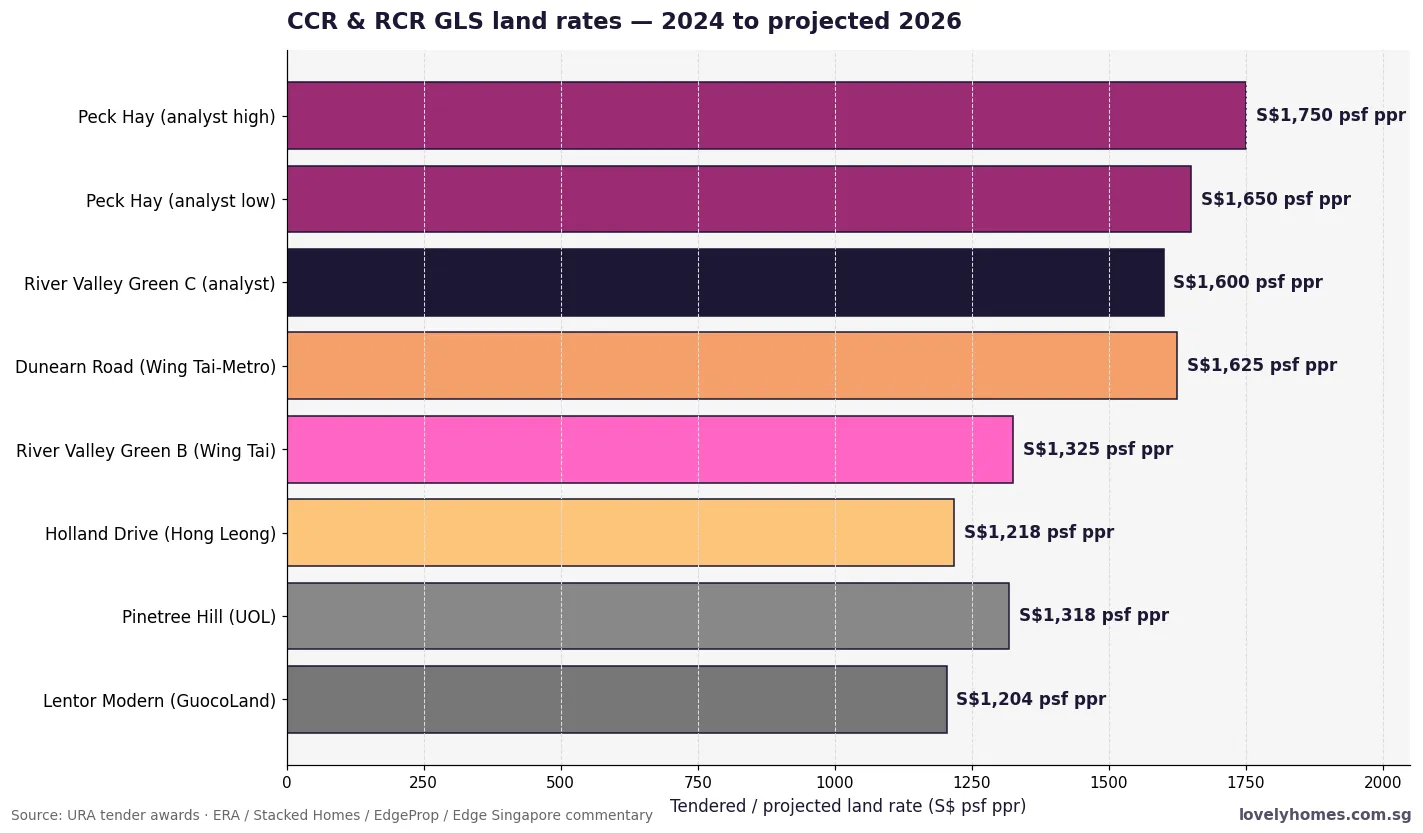

- Nearest live comp: River Valley Green Parcel C tender expected mid-2026 with Peck Hay Road also released in late April 2026.

What URA released and why it matters

The Morrison Lane site sits along Mohamed Sultan Road, on the River-Valley side of Robertson Quay, putting it firmly in the prime District 9 cluster that has driven a string of high-priced launches over the past 18 months. Reserve-List release is a deliberately softer signal than a Confirmed-List tender — URA puts the plot on offer, but only puts it to tender if a developer triggers it with a binding minimum bid the government finds acceptable.

The mechanism’s policy logic is balance: too few sites and prices spike; too many trigger-list bids and the market floods. Reserve-List release is also the cleanest way for URA to read developer appetite — a triggered site signals confidence; a sustained idle period signals capital tightness or pipeline saturation. Morrison Lane is the latest test point.

How the Robertson Quay / River Valley corridor has performed

The corridor has run hot. The most recent benchmark in the immediate area saw 84% of units cleared at an average price of S$3,050 psf on its launch weekend in late 2025. That’s a meaningful number for any Morrison Lane bidder modelling the eventual sell-through — at S$3,050 psf, a 70 sqm 2-bedroom unit prices at ~S$2.3m, well within the ABSD-conscious local-and-PR buyer pool that has been the engine of recent CCR sales.

The site’s location has additional structural pluses: a 5–10 minute walk to Great World MRT (TEL), the Robertson Quay F&B strip, and direct vehicular access to the CBD via Kim Seng / Havelock Road. Construction-noise and heritage-conservation overlays in Mohamed Sultan are well known and likely already priced into any developer’s underwriting.

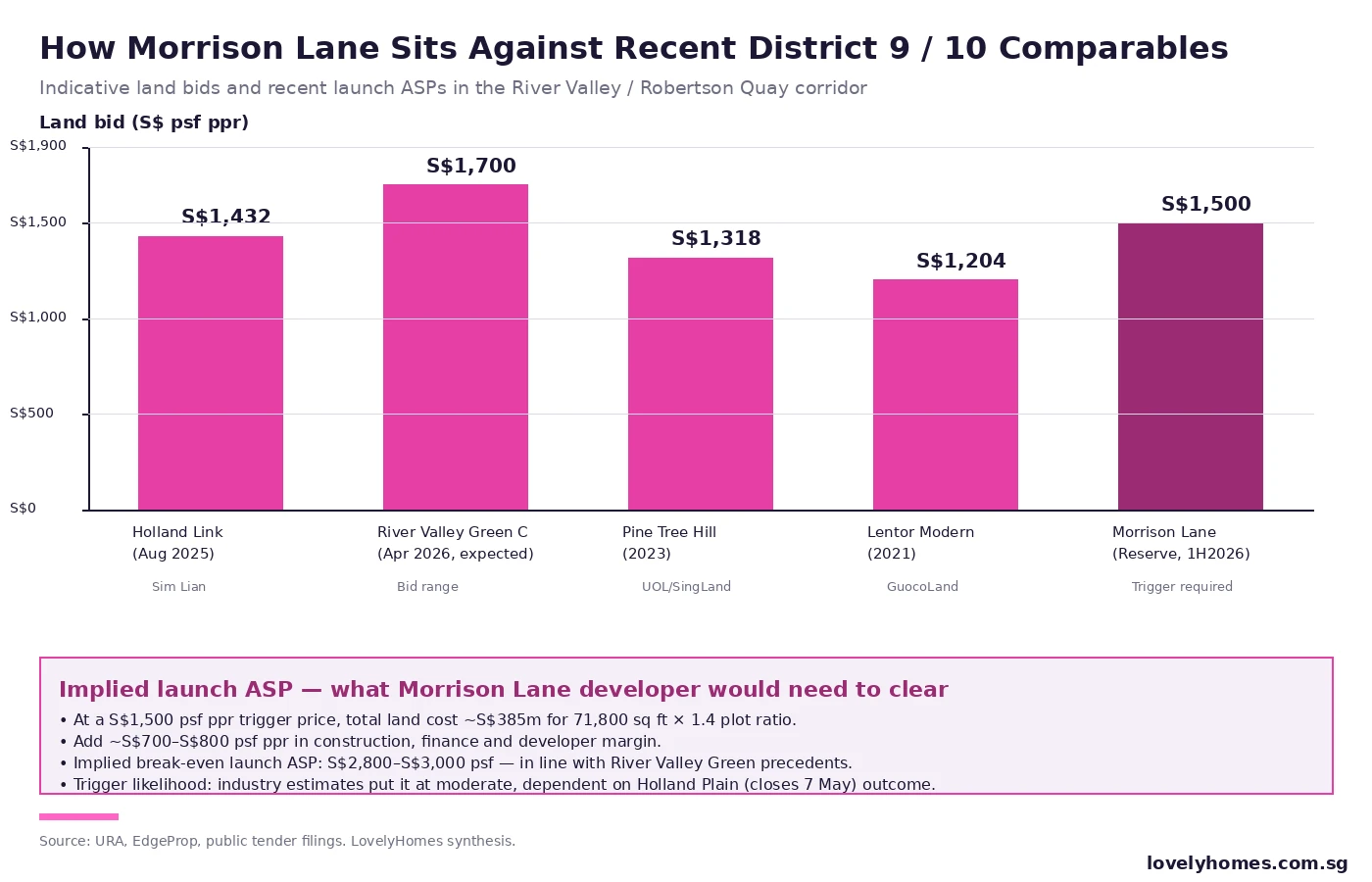

Land bid economics — what a developer would need to clear

Reverse-engineering from a S$3,000 psf launch ASP target gives a working land-bid number around S$1,500 psf ppr. At that level, total land cost on Morrison Lane would land near S$385 million — a sized cheque that mid-cap developers can take down on their own, and that the recent Sim Lian Holland Link bid of S$368.4m at S$1,432 psf ppr (Aug 2025) sits comfortably below.

What changes the math is interest carry. A Reserve-List trigger means the developer commits to the bid before knowing the full launch window; with funding rates north of 4% on most senior debt, every 12-month delay adds roughly S$15m of carry on a site of this size. That cost discipline is one reason Reserve-List sites trigger most often when developers see a clean 12 to 18-month launch path on the calendar.

Summary table — how Morrison Lane fits the 1H2026 pipeline

| Site | Units | List | Status |

|---|---|---|---|

| Holland Plain (2nd plot) | ~280 | Confirmed | Closes 7 May 2026 |

| Morrison Lane (Mohamed Sultan) | ~205 + retail | Reserve | Available — trigger required |

| Bayshore Drive (mixed-use) | ~1,800 (incl. mixed-use) | Confirmed | Closes 15 July 2026 |

| Peck Hay Road | ~340 | Confirmed | Tender live |

| River Valley Green Parcel C | ~380 | Confirmed | Tender live |

Worked Example: trigger-price scenario for a hypothetical mid-cap bidder

Site basics. 6,669.8 sqm × plot ratio 1.4 = max GFA 9,338 sqm (~100,500 sq ft). 205 residential units with average 70 sqm carpet area + 500 sqm first-storey retail.

Trigger bid scenario at S$1,500 psf ppr. 100,500 sq ft × S$1,500 = S$150.75m at the GFA cap; using the higher per-unit gross figure with allowances for void, the all-in land cost runs closer to S$385m on a site of this density.

Build cost. ~S$700–S$800 psf GFA (residential mid-luxe finish) for ~S$80m construction cost; +S$25m soft costs; +12% developer margin reserve.

Implied launch break-even ASP. Combining land + construction + soft + financing + margin lands at S$2,850–S$3,000 psf — broadly consistent with River Valley Green’s October 2025 launch at S$3,050 psf, supporting the trigger-price thesis.

Key sensitivity. Each S$100 psf ppr higher on land cost adds roughly S$170 psf on the launch ASP. The corridor’s recent absorption rates suggest the market can hold S$3,050 psf — but a trigger above S$1,600 psf ppr would push the launch break-even into a price band the corridor has not yet tested.

What this means for buyers

If you are a buyer watching Robertson Quay and Mohamed Sultan, Morrison Lane is unlikely to launch before the second half of 2027 even if triggered immediately. Closer-dated alternatives are stronger: River Valley Green Parcel C (tender live), and the next round of fringe District 9 launches that follow the Holland Plain auction outcome. The Morrison Lane release is a signal of pipeline depth, not an imminent launch event.

For investors thinking about pre-launch positioning, the more productive read is on the secondary market in nearby developments. Tightening developer margins typically front-run a price-firmness signal in the resale market — recently launched stacks within a 500m radius are worth watching for absorption velocity through the rest of 1H2026.

What might come next

Two immediate catalysts will set the tempo. First, the Holland Plain tender on 7 May 2026 — a strong field of bidders and a price north of S$1,500 psf ppr would materially raise the probability that Morrison Lane is triggered before the second half of 2026. Second, URA’s full Q1 2026 final stats have already landed; the next read is the April 2026 new-home sales data due in mid-May, which will tell us whether the Q1 +0.3% private-price uptick has carried into spring volumes.

If both signals print constructive, expect at least one or two of the 1H2026 Reserve-List sites — Morrison Lane being the highest-quality residential plot among them — to be triggered by Q3 2026.

FAQ

What is the Reserve List in URA’s GLS Programme?

Sites under the Reserve List are tendered only when a developer submits a minimum bid the government accepts. This contrasts with the Confirmed List, where URA tenders the site outright on a fixed schedule. Reserve-List release is a softer market signal that lets URA test appetite without forcing a sale.

How long does it take for a Reserve-List site to be triggered?

It varies. Some Reserve-List sites are triggered within weeks of release; others linger on the list for months or never trigger. The pace depends on developer balance-sheet capacity, the broader sales pipeline, financing costs, and how confident the market feels about end-buyer demand at the implied launch ASP.

Why is Morrison Lane considered District 9 rather than District 10?

Mohamed Sultan Road sits within the Singapore postal-district boundary for District 9, which covers River Valley, Orchard Road and Cairnhill. The neighbouring Robertson Quay area also falls in D09. District 10 starts further west, covering Bukit Timah, Holland and Tanglin proper.

When could a launch from Morrison Lane realistically happen?

If triggered in mid-2026 with a tender award by Q3, formal site planning typically takes 6 to 9 months, and pre-launch marketing 3 to 6 months. A practical earliest launch is late 2027 to early 2028. That timing also aligns with the rollout cadence of the wider Robertson Quay / River Valley pipeline through 2027.

Is the 500 sqm commercial space significant?

Five hundred square metres at the first storey is a small-to-mid-scale strata-retail footprint. It can support an F&B unit, a convenience store, a clinic and one or two service tenants. It does not transform the project’s character — this remains a residential development with a small ground-floor commercial layer typical of Mohamed Sultan’s mixed-zone overlay.

Will Morrison Lane affect prices in nearby developments?

The release alone does not move prices materially. A successful trigger and a strong land bid would tighten the margin assumption on adjacent developments, supporting firm-to-rising prices in the existing resale stock for 12 to 18 months as buyers pull forward purchases ahead of the new launch. A non-trigger or a weak final bid would have the opposite signal.

What should buyers do now?

If you are decision-time on a Robertson Quay / Mohamed Sultan unit, the Morrison Lane release tightens the supply story but does not change short-term pricing. Continue evaluating live launches and resale stock on their own merits. If you are an investor, watch the Holland Plain tender result on 7 May 2026 — that’s the highest-information event of the next two weeks.

Related Articles

- Holland Plain GLS Tender Closes 7 May 2026

- Peck Hay Road and River Valley Green Parcel C GLS

- Singapore Q1 2026 Flash Estimates

- Singapore Property Cooling Measures Timeline

- ABSD Singapore 2026 Complete Guide

Disclaimer

This article is general property-market commentary based on URA’s 1H2026 Government Land Sales Programme release and publicly available media coverage. Verify site specifications and tender procedures on the URA portal. Indicative bid prices, launch ASPs and timing scenarios are LovelyHomes synthesis based on industry comparables and should not be relied upon for purchase or investment decisions. Consult a licensed property professional and review the official URA Land Sales documentation before acting.

Tags: Morrison Lane GLS, Mohamed Sultan, Robertson Quay, District 9, URA Government Land Sales, Reserve List, 1H2026 GLS, Holland Plain GLS, Bayshore Drive, Peck Hay Road, River Valley Green, Singapore property news, land bid analysis.