Holland Plain GLS Tender Closes 7 May 2026: ~280 Units in Prime District 10

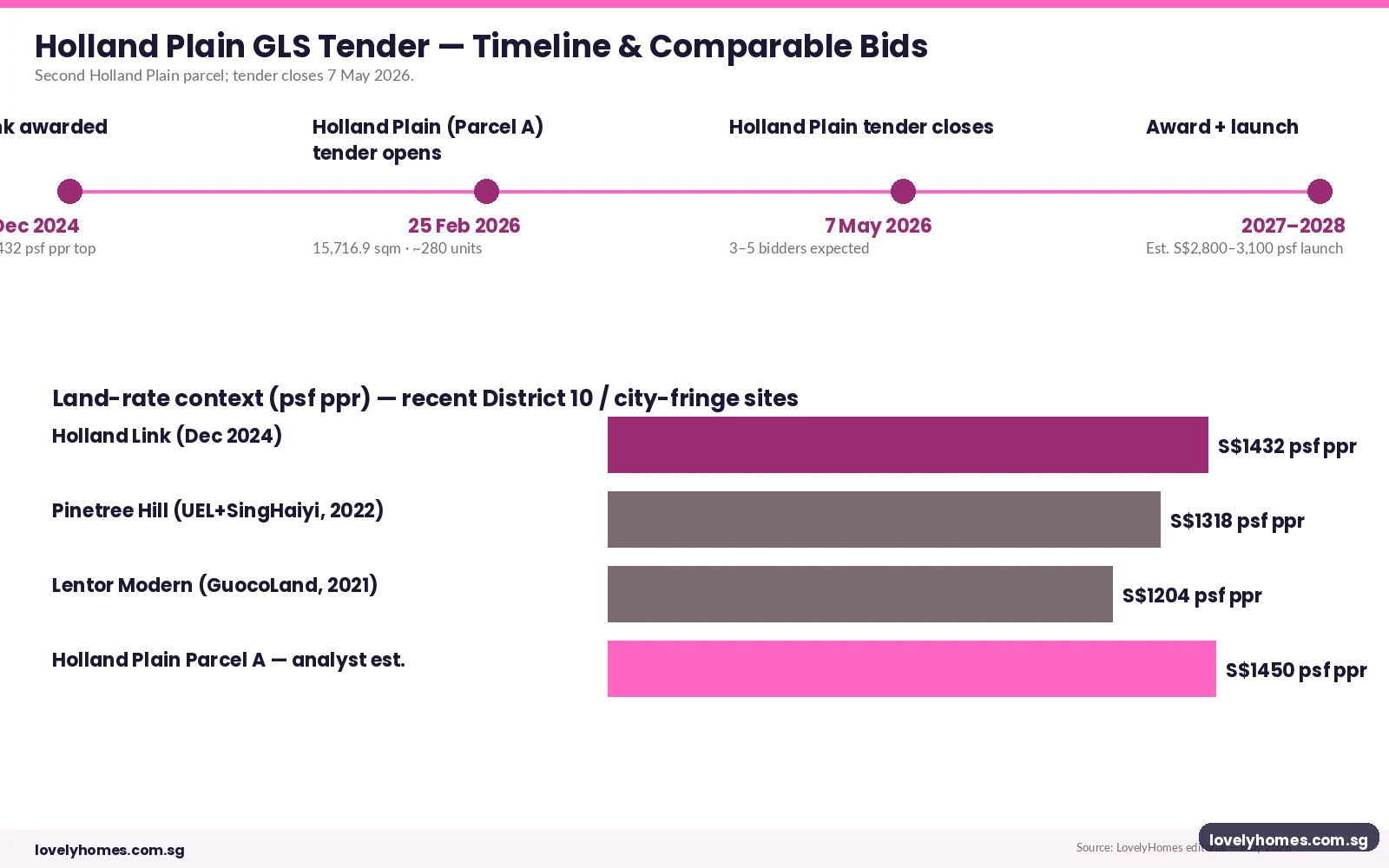

The tender for the second Holland Plain Government Land Sales (GLS) parcel closes at noon on 7 May 2026, four days from the time of writing. The 15,716.9 square-metre site, sitting on Parcel A of the Holland Plain area within prime District 10, is expected to yield around 280 private residential units at completion. Industry analysts are pencilling in three to five bidders and a top land bid in the S$1,400 to S$1,500 per square foot per plot ratio band — broadly tracking the precedent set by the adjacent Holland Link parcel awarded in late 2024.

This is the first Confirmed List parcel to be released under the 1H 2026 GLS Programme to actually go to closing in 2026. URA also opened a separate Reserve List application for the Morrison Lane site in the same window, signalling a coordinated push to refresh the central-area land bank ahead of the 2027–2028 launch cycle.

Quick Answer — Holland Plain GLS at a glance

- Site: Holland Plain (Parcel A), prime District 10.

- Tender opens: 25 February 2026 · Closes: 7 May 2026 (12:00).

- Site area: 15,716.9 sqm. Maximum GFA: 28,291 sqm. Plot ratio: 1.8.

- Estimated unit yield: ~280 private residential units.

- Tenure: 99-year leasehold from award.

- Connectivity: King Albert Park MRT (Downtown Line) anchors the area today; future Cross Island Line interchange is the structural upgrade.

- Analyst land-bid band: S$1,400–1,500 per sq ft per plot ratio (psf ppr).

- Implied launch range: S$2,800–3,100 psf at sale, depending on bid level and 2027–2028 market conditions.

The Site

Holland Plain Parcel A occupies a Holland Village-adjacent residential plot in prime District 10. The land is bounded by mature low-rise residential to the south and west, with King Albert Park MRT station on the Downtown Line approximately a 600-metre walk away. The plot ratio of 1.8 yields a maximum gross floor area of 28,291 square metres, supporting around 280 private homes — a relatively modest density for the location, consistent with the area’s low-rise character.

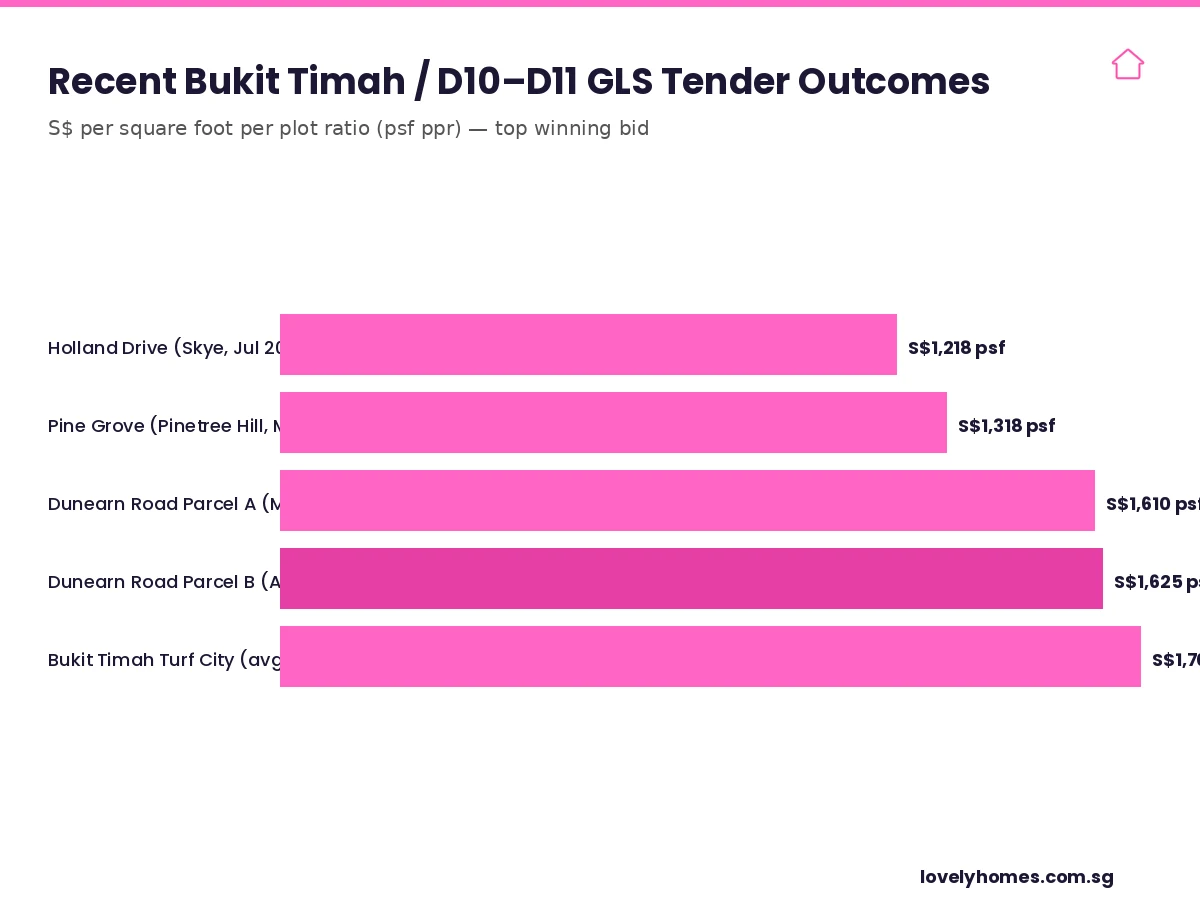

The plot is the second on Holland Plain to be released, following the Holland Link parcel awarded in December 2024 to a developer consortium at S$1,432 per square foot per plot ratio against five competing bids. Holland Link is now under construction; together the two parcels will add roughly 600 new private homes to the Holland Plain micro-precinct over the 2027–2029 horizon.

Timeline and Comparable Bids

The relevant comparables are limited. Holland Link in late 2024 set the most recent benchmark at S$1,432 psf ppr; it remains the cleanest direct precedent. Pinetree Hill in 2022 cleared at around S$1,318 psf ppr at a comparable city-fringe location, since launched and now selling steadily. Lentor Modern in 2021 closed at S$1,204 psf ppr in a different sub-market and a different rate environment. Allowing for the move in average land rates and the slight upgrade in connectivity story (Cross Island Line confirmed since the Holland Link tender), an analyst band of S$1,400–1,500 psf ppr is internally consistent.

Summary Table — Tender Specifications

| Parameter | Detail |

|---|---|

| URA reference | 1H 2026 Confirmed List, Holland Plain Parcel A |

| Tender opens | 25 February 2026 |

| Tender closes | 7 May 2026, 12:00 |

| Site area | 15,716.9 sqm |

| Maximum GFA | 28,291 sqm (plot ratio 1.8) |

| Estimated unit yield | ~280 units |

| Tenure | 99-year leasehold from award |

| Expected bidders | 3–5 |

| Estimated top bid | S$1,400–1,500 psf ppr |

| Anticipated launch | 2027–2028 at S$2,800–3,100 psf |

Why This Tender Matters

Three reasons. First, it is a temperature read on developer appetite for prime-district land in a market that has just digested two divergent quarterly prints — a +0.9% URA private-property index and a −0.1% HDB index for Q1 2026 (covered in our URA Q1 2026 final analysis). A bid count below three or a top bid notably under S$1,400 psf ppr would suggest developers see the prime-district premium narrowing; a bid count of five or more at the upper end of the analyst range would re-confirm structural demand.

Second, it is a forward signal on launch pricing. With S$1,400 psf ppr land plus typical construction, financing, and developer margin, the implied launch psf on the resulting condominium falls in the S$2,800–3,100 band. That price point would slot Holland Plain alongside other prime-fringe launches and well above OCR averages, but materially below the recent CCR ultra-prime tier. For pricing context across the market, see our Singapore Property Market Outlook 2026.

Third, it speaks to the Cross Island Line investment thesis. The CRL station planned within the Holland Plain estate is the single largest accessibility upgrade for District 10 since the Downtown Line opened. Developers paying up at this tender are betting partly on that connectivity upgrade, and partly on the durability of school-belt and Holland Village amenity demand. If the bid clears in the upper band, it tells you the institutional money is comfortable with both the timing and the magnitude of the CRL effect.

What to Watch on Tender Day

- Bid count. Five or more = strong; three to four = consensus expectation; one or two = a meaningful negative surprise that would feed into the broader land-bank pricing narrative.

- Top bid level. Above S$1,500 psf ppr would indicate aggressive Cross Island Line pricing; below S$1,350 psf ppr would suggest developers are pricing in margin compression.

- Identity of bidders. JV consortia versus standalone bids; the presence (or absence) of large-format developers usually associated with prime District 10 launches.

- Morrison Lane Reserve List. Whether anyone triggers the application before the Holland Plain award is a separate signal of land-bank tightness.

How Singapore Compares

Singapore’s GLS programme remains an unusually transparent and disciplined supply mechanism. Hong Kong’s land-sale schedule is more opportunistic; Sydney and Melbourne lack a directly comparable systematic release programme; Tokyo’s premium-district plots are typically transacted privately rather than via competitive public tender. The combination of a published Confirmed List 12 months ahead, fixed tender windows, and full disclosure of all bids on closing day means the Holland Plain print on 7 May 2026 will be a clean, comparable data point.

Frequently Asked Questions

What is Holland Plain Parcel A?

Holland Plain Parcel A is a 15,716.9 square-metre 99-year leasehold residential plot on the URA 1H 2026 GLS Confirmed List, located in prime District 10, Holland Village-adjacent, with a plot ratio of 1.8 and an estimated yield of around 280 private residential units. It is the second parcel released under the Holland Plain GLS sub-programme, following Holland Link in 2024.

When does the tender close?

The tender closes at 12:00 on 7 May 2026. URA will announce the bids received and the top bidder on the same day. The actual award (subject to government acceptance) typically follows within four to eight weeks, after which the developer has 24 to 30 months to launch and 60 months from award to issue Temporary Occupation Permit on the resulting development.

What is the expected launch price for the resulting condominium?

If the tender clears at S$1,400–1,500 per square foot per plot ratio, an indicative launch range is S$2,800–3,100 per square foot at sale, depending on the developer’s margin assumptions and 2027–2028 market conditions. The actual launch price will be set by the awarded developer and may differ from any analyst projection.

How does Cross Island Line affect this site?

The future Cross Island Line interchange — with a planned station within the Holland Plain estate — will materially improve connectivity to Jurong Lake District, the western industrial corridor, and the cross-island east-west route. The station is not operational at the time of tender; developers are pricing the future-state benefit. This is one of the largest accessibility upgrades for District 10 in two decades.

How does this tender compare to Holland Link in 2024?

Holland Link was awarded in December 2024 at S$1,432 psf ppr against five bidders. Holland Plain Parcel A is similar in profile (location, tenure, plot ratio band) but benefits from incremental information — CRL planning maturity, more recent market context. Analysts expect the bid range and bidder count to be roughly comparable, with a marginal upward bias on land rate.

What is the Morrison Lane Reserve List parcel?

Morrison Lane is a separate Reserve List residential parcel made available for application during the same tender window. Reserve List sites are released for tender only when a developer triggers the application by lodging a minimum bid acceptable to the Government; it is a developer-initiated release mechanism rather than a scheduled tender.

Where can I track the tender outcome?

URA publishes Government Land Sales tender outcomes on its official site immediately after the tender closes. Industry research desks at the major real estate firms typically publish their analysis within 24 hours; the leading Singapore property news outlets (EdgeProp, The Business Times, Channel News Asia property desk, The Edge Singapore) will carry headline coverage on the day.

Related Articles

- URA Q1 2026 Private Home Prices Rise 0.9%

- Dunearn Road GLS Wing Tai × Metro S$533m 2026

- Kallang Close GLS — Frasers × Mitsubishi 2026

- Singapore Property Market Outlook 2026

- Singapore Condo Supply Crunch 2026

- ABSD Singapore 2026 Complete Guide

Disclaimer

This article is general news and analysis on the Holland Plain GLS tender as at 3 May 2026 and does not constitute investment, financial, or legal advice. Tender details, dates, plot specifications, and analyst bid ranges are drawn from URA announcements and industry research-desk commentary; figures may be revised by URA up to closing. For purchase, financing, or development-side advice, engage a licensed Singapore conveyancing solicitor and (where relevant) a chartered tax practitioner. Prospective home buyers considering the eventual launch should also refer to the IRAS stamp duty pages, the Monetary Authority of Singapore mortgage rules, and the CPF Board for funding mechanics.