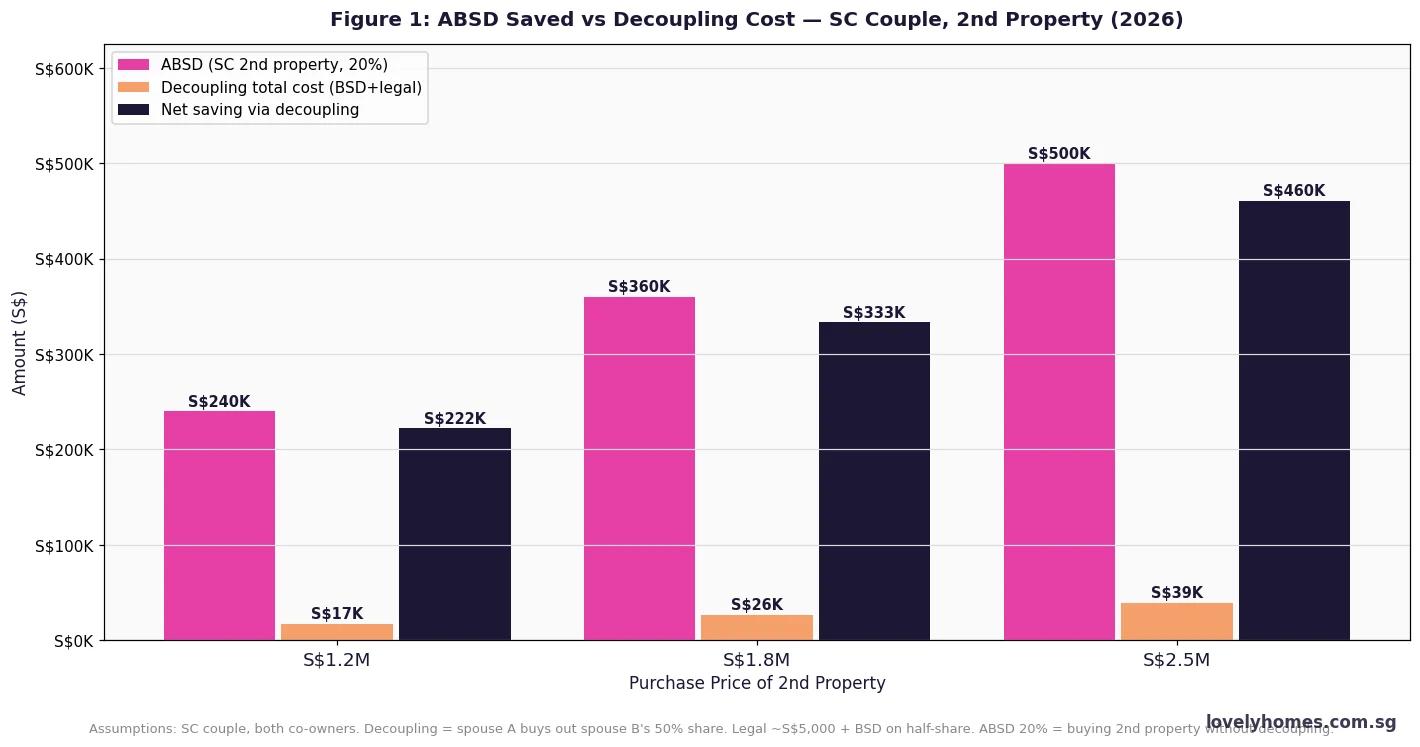

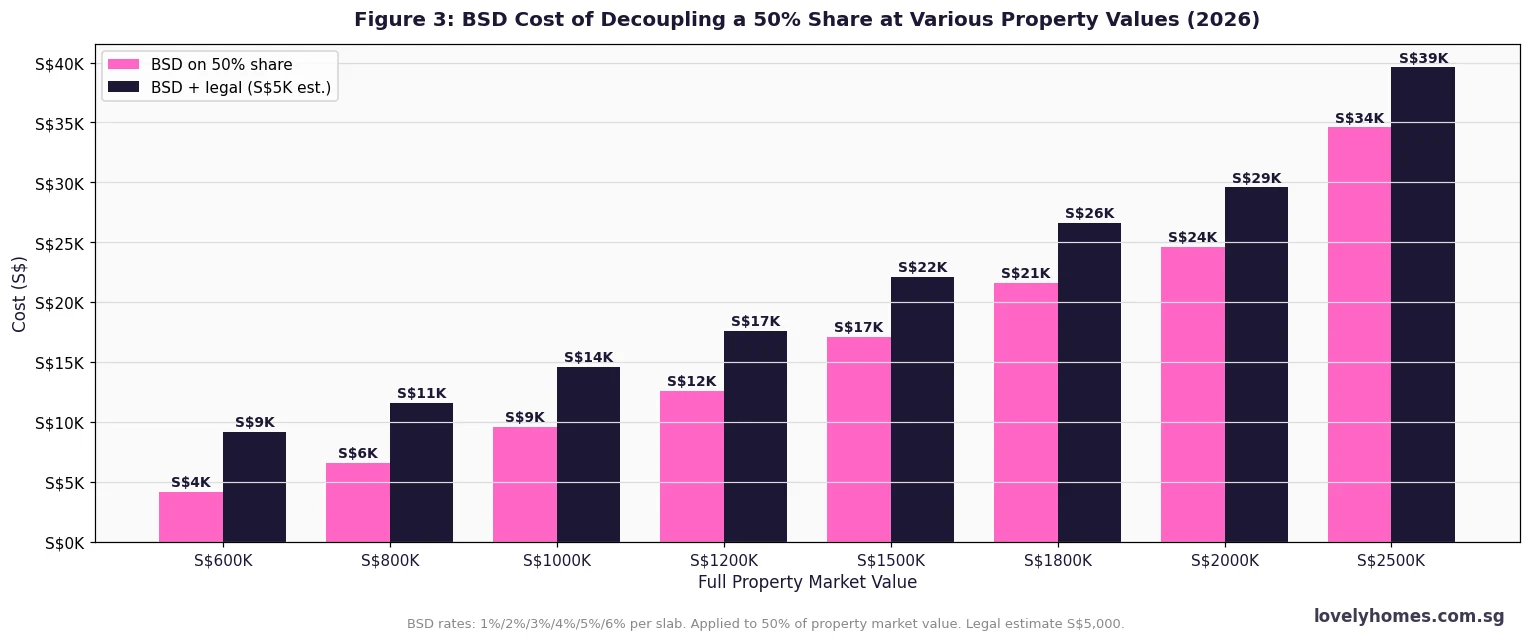

Singapore Seller’s Stamp Duty (SSD) 2026: New 4-Year Holding Period, Rates and Exemptions Explained

- What is SSD? Seller’s Stamp Duty is a tax on residential (and industrial) property sellers who dispose of their property within a specified holding period. Administered by IRAS.

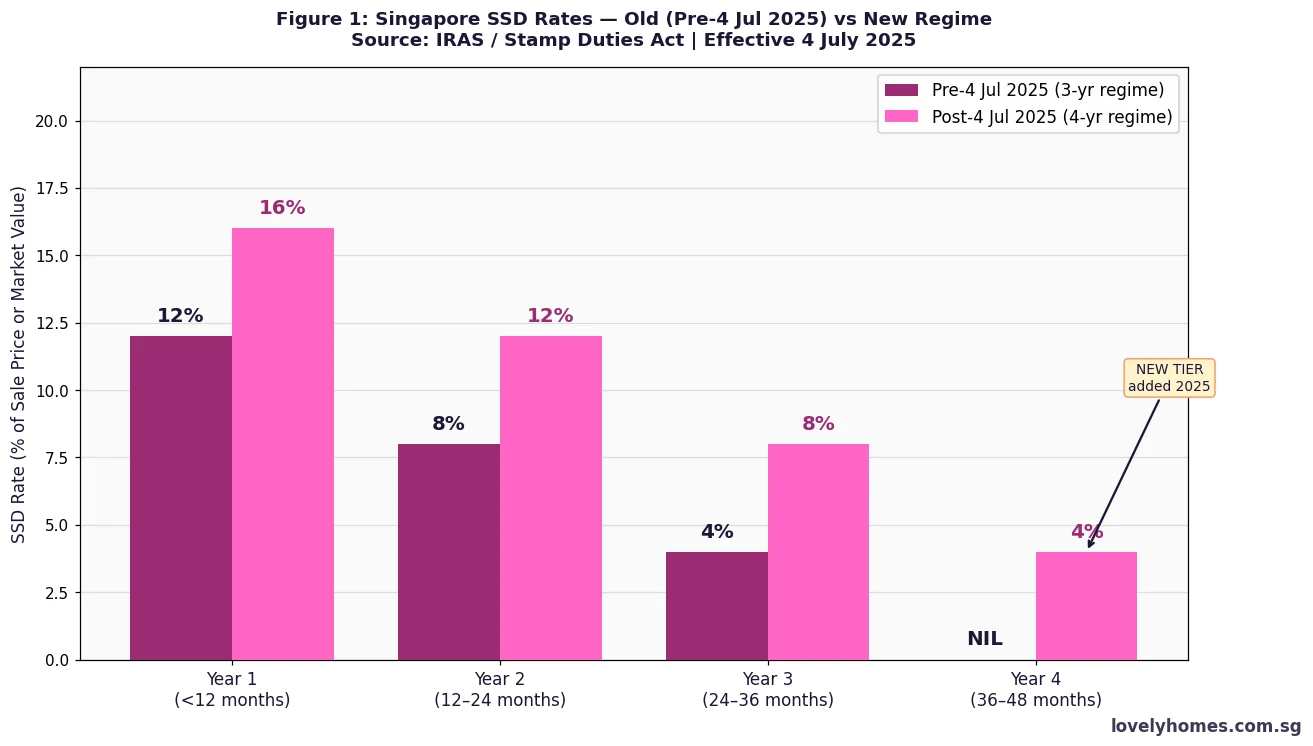

- New 2025 regime (effective 4 July 2025): 4-year holding period. Rates: Year 1 = 16%, Year 2 = 12%, Year 3 = 8%, Year 4 = 4%, after Year 4 = 0%.

- Old regime (11 March 2017 to 3 July 2025): 3-year holding period. Rates: Year 1 = 12%, Year 2 = 8%, Year 3 = 4%, after Year 3 = 0%.

- Applies to: All residential properties purchased on or after the respective effective dates — HDB flats, condominiums, landed homes, and ECs.

- Calculated on: The higher of the actual selling price or the market value at date of sale.

- Payment deadline: Within 14 days of signing the OTP acceptance or S&P agreement via the IRAS e-Stamping Portal.

- Key exemptions: Divorce, death of owner, en-bloc collective sale, compulsory Government acquisition, HDB disposal back to HDB.

- Industrial SSD (separate): 3-year regime — 15%/10%/5%/0%.

What is Seller’s Stamp Duty?

Seller’s Stamp Duty (SSD) is a tax levied by the Singapore Government on sellers who dispose of residential property within a prescribed holding period. The rationale is anti-speculation: by making it financially punishing to flip property shortly after purchase, the Government moderates short-term price volatility and encourages genuine owner-occupier demand. SSD was first introduced for residential property on 20 February 2010 in response to a rapid price run-up following the global financial crisis. It has been calibrated several times since, most recently on 4 July 2025 when the Government extended the holding period to four years and raised all rate tiers by four percentage points.

SSD is administered by the Inland Revenue Authority of Singapore (IRAS) under the Stamp Duties Act (Cap 312). It operates alongside the Additional Buyer’s Stamp Duty (ABSD) and Buyer’s Stamp Duty (BSD) as part of Singapore’s property market stabilisation toolkit. Where BSD and ABSD are levied on buyers, SSD is the only stamp duty that falls on the seller.

SSD Rates in 2026: The New 4-Year Regime

The 2025 tightening — announced on 3 July 2025 and effective for all residential properties purchased on or after 4 July 2025 — extended the SSD holding period from three to four years and raised each rate tier by four percentage points. The chart below makes the difference between the old and new regimes vivid:

Under the current regime, a seller who purchased a condominium on 1 August 2025 and sells it on 30 June 2026 — 10 months later — will pay SSD at 16% on the higher of the sale price or market value. On a S$1,500,000 sale, that is S$240,000 in SSD alone, on top of outstanding mortgage costs and agent commissions. The new rates make very short-duration property investments economically unviable in most scenarios.

For properties purchased between 11 March 2017 and 3 July 2025, the previous three-year regime applies: 12% (Year 1), 8% (Year 2), 4% (Year 3), 0% thereafter.

Which Properties Are Subject to SSD?

SSD applies to the following categories of residential property in Singapore:

- Private residential property: Condominiums, apartments, landed homes (terraces, semi-detached, bungalows, GCBs), strata landed units, and mixed-use units with a residential component.

- Executive Condominiums (ECs): Subject to SSD during the initial privatisation period for units resold on the open market within the holding period.

- HDB flats: SSD technically applies, but the 5-year Minimum Occupation Period (MOP) required before open-market resale means most HDB sales occur outside the 4-year SSD window anyway. See our HDB resale guide for details.

- Partial disposals and gifts: SSD applies to any disposal of a residential property interest — including gifts and transfers at below-market value — within the holding period. Computed on market value, not consideration paid.

SSD does not apply to commercial property or industrial property (the latter has its own separate SSD regime).

How SSD is Calculated

The computation is: SSD = applicable rate × max(selling price, market value).

IRAS uses the higher of two figures to prevent sellers from artificially deflating the declared sale price to reduce their SSD liability. If IRAS determines the declared price is below open-market value, it substitutes the market value — typically determined by a licensed valuation firm or IRAS’s own assessment — as the calculation base.

The holding period runs from the date of purchase (date of OTP or S&P, whichever is earlier) to the date of disposal (date the seller signs the acceptance of OTP or S&P agreement). If you bought on 1 March 2025 and sell on 2 March 2026, you have crossed into Year 2, and the Year 2 rate applies.

Figure 2 illustrates how costly an early sale can be under the new regime. A seller disposing of a S$1,800,000 property in Year 1 pays S$288,000 in SSD — more than the typical agent commission, legal fees, and BSD combined. The prudent investor’s minimum exit window is now four years and one day.

SSD Payment — Deadline and Process

SSD falls legally on the seller and is incorporated into the conveyancing process by the seller’s solicitor. Key steps:

- Date of disposal: The date you sign the acceptance of OTP or S&P agreement (whichever is earlier).

- 14-day deadline: SSD must be paid to IRAS within 14 days of the date of disposal. Late payment attracts a penalty of up to four times the unpaid duty.

- e-Stamping: Payment via the IRAS e-Stamping Portal. Your conveyancing lawyer handles this on your behalf.

- Funded from sale proceeds: SSD is deducted from the sale proceeds at completion — sellers do not need to fund it upfront.

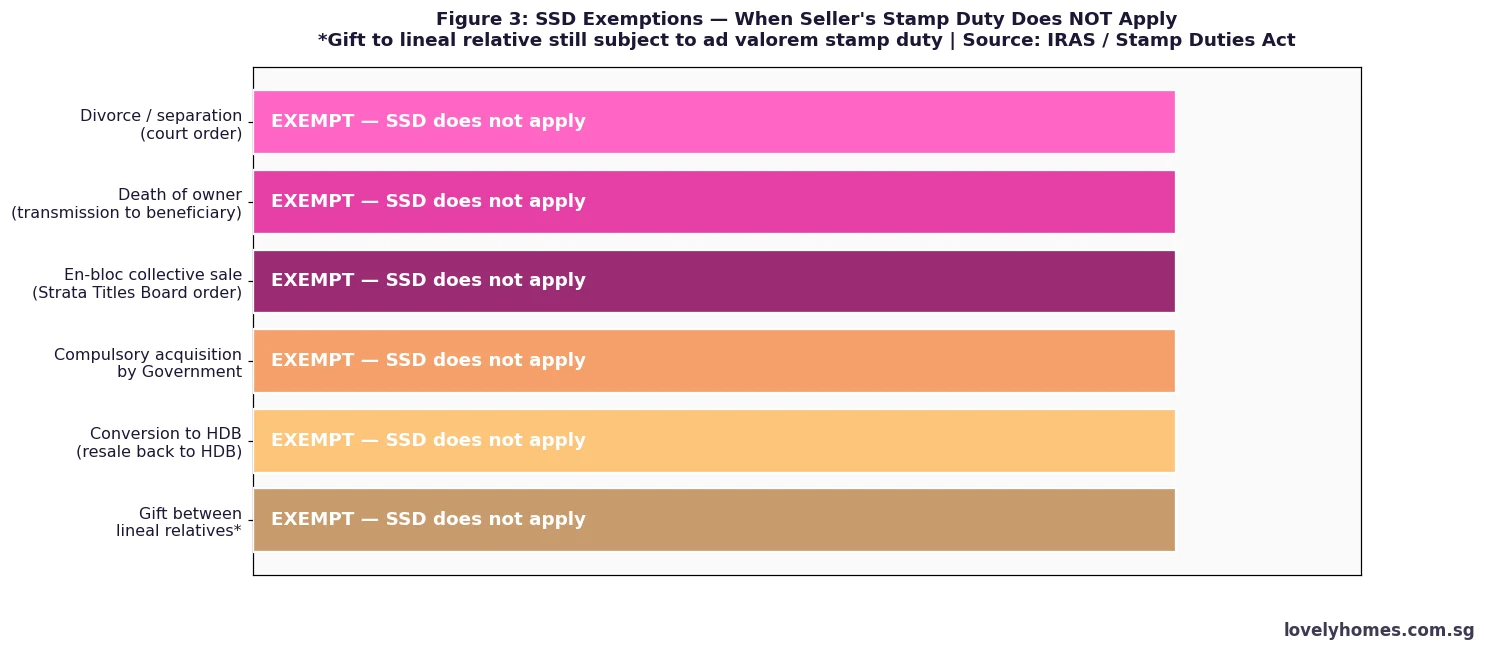

SSD Exemptions — When the Tax Does Not Apply

Not every disposal within the holding period triggers SSD. IRAS provides specific exemptions for involuntary or non-commercial transfers:

- Divorce or judicial separation: Transfer between spouses pursuant to a court order under the Women’s Charter or Matrimonial Proceedings Act — SSD waived. Voluntary spouse transfers without a court order are NOT exempt.

- Death of owner: Transmission of a deceased owner’s share to beneficiaries via intestacy or valid will is not treated as a disposal for SSD purposes.

- En-bloc collective sale: Where a Strata Titles Board (STB) or High Court order compels the collective sale, individual owners selling pursuant to that order are not subject to SSD. See our Singapore en-bloc guide.

- Compulsory acquisition: Where the Government acquires the property under the Land Acquisition Act (Cap 152), no SSD applies.

- HDB disposal back to HDB: Sale back to HDB (e.g., through voluntary early redemption schemes) is exempt.

- Gift to lineal relatives: A specific remission order may reduce SSD in qualifying circumstances, but ad valorem stamp duty on the transfer may still apply — consult a lawyer.

Industrial Property SSD — A Separate Regime

Industrial property — factories, warehouses, logistics facilities, and flatted factories — has its own SSD regime introduced on 12 January 2013. The holding period is three years with higher base rates:

| Holding Period (from purchase date) | Industrial SSD Rate |

|---|---|

| Up to 1 year | 15% |

| More than 1 year and up to 2 years | 10% |

| More than 2 years and up to 3 years | 5% |

| More than 3 years | Nil |

Industrial SSD rates effective 11 March 2017 | Source: IRAS

Summary Table: Residential SSD Regimes at a Glance

| Purchase Date | Year 1 | Year 2 | Year 3 | Year 4 | After Year 4 |

|---|---|---|---|---|---|

| On/after 4 July 2025 (current) | 16% | 12% | 8% | 4% | Nil |

| 11 March 2017 to 3 July 2025 | 12% | 8% | 4% | Nil | Nil |

| 14 January 2011 to 10 March 2017 | 16% | 12% | 8% | 4% | Nil |

| 20 February 2010 to 13 January 2011 | 3% | 2% | 1% | Nil | Nil |

Source: IRAS / Stamp Duties Act Cap 312 | Properties purchased before 20 February 2010 were not subject to SSD.

Worked Example: Mr Lee Sells His Condo 18 Months After Purchase

Mr Lee, a Singapore Citizen, purchases a resale condominium in Buona Vista for S$1,650,000 on 15 September 2025. His employment situation changes and he lists the property for sale in early 2027. He accepts an OTP at S$1,720,000 on 12 March 2027 — approximately 18 months after purchase.

Since the property was purchased after 4 July 2025, the new regime applies. The holding period from 15 September 2025 to 12 March 2027 is just over 18 months — meaning Mr Lee is in Year 2. The SSD rate for Year 2 is 12%.

IRAS compares the sale price (S$1,720,000) against the market value. An independent valuation confirms market value at S$1,700,000. The higher figure is the sale price of S$1,720,000.

- SSD base: S$1,720,000 (higher of sale price vs market value)

- SSD payable: 12% x S$1,720,000 = S$206,400

- Payment deadline: 14 days from 12 March 2027 = 26 March 2027

- Agent commission (approx. 1%): S$17,200

- Legal fees: S$2,500 to S$3,500

- Total selling costs: approximately S$226,100 to S$227,100

Had Mr Lee waited until 16 September 2029 — four years and one day after purchase — his SSD would be nil, saving him S$206,400. This is the clearest possible illustration of why the four-year holding period matters fundamentally to investment planning.

Why SSD Matters — What It Means for Property Investors

SSD is the Government’s most direct lever for curbing short-horizon speculation. Unlike ABSD — which targets buyers — SSD makes the exit itself expensive, creating a two-sided cost barrier that effectively locks investors in for at least four years under the current regime. For genuine owner-occupiers, this is largely irrelevant: they have no intention of selling quickly. For investors, the SSD calculus must be front-loaded into any acquisition model.

The July 2025 tightening came as the private residential price index rose 0.9% in Q1 2026 (following a 0.6% rise in Q4 2025, per URA Q1 2026 real estate statistics), signalling that investor appetite was returning. By extending the SSD window to four years and returning rates to the 2011-2017 levels (16%/12%/8%/4%), the Government effectively replicated the strictest historical SSD regime. For buy-to-let investors, the four-year minimum hold conveniently encompasses roughly two two-year lease cycles, allowing investors to cover carrying costs through rental income before an SSD-free exit.

What Might Come Next for SSD

This section reflects editorial analysis and is speculative in nature.

Having just restored the 2011-2017 rate structure in 2025, it would be unusual for the Government to tighten SSD further in 2026 absent a sharp market acceleration. The more likely near-term scenario is a data-driven review in mid-2027, 18 months after the July 2025 measures. If private residential prices cool to under 2% year-on-year growth, the framework will likely remain unchanged. A relaxation — possibly reverting to a three-year regime — would only be expected if the market corrects sharply due to external shocks such as a global recession or material rises in financing costs. Investors should plan on the four-year structure being the baseline through at least 2027.

Frequently Asked Questions

Does SSD apply if I bought my condo in 2023 and want to sell now in 2026?

Yes — under the old (pre-4 July 2025) three-year regime, since you purchased before 4 July 2025. If you bought in early 2023 and sell in mid-2026, you are within Year 3 of the three-year window, so the SSD rate is 4% on the higher of the selling price or market value. If you bought in mid-2023 and sell after mid-2026, you are past Year 3 and no SSD applies. The holding period is measured precisely from the date of your OTP or S&P agreement.

Can I avoid SSD by transferring the property to my spouse or child?

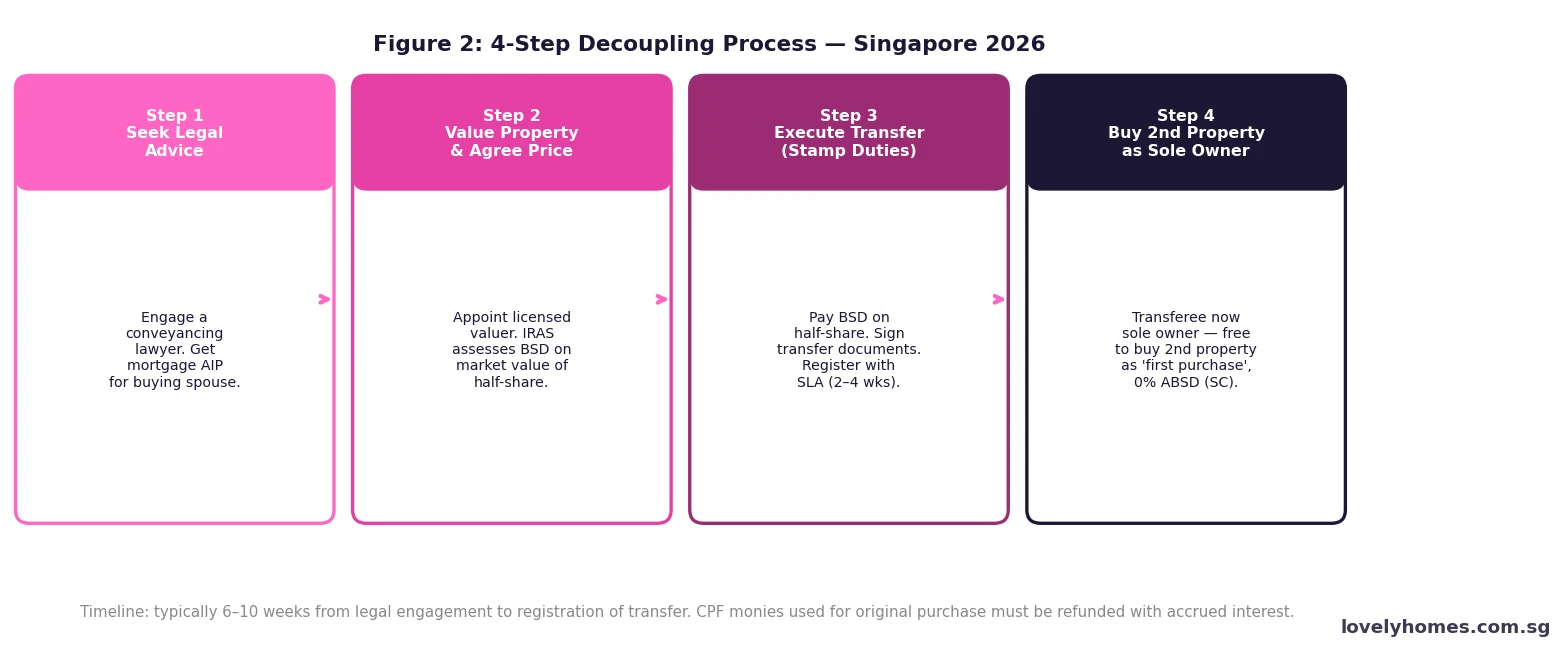

No. IRAS treats a transfer to a family member — even a spouse or child — as a disposal for SSD purposes. The SSD is computed on the market value of the property at the date of transfer, not the consideration paid. The only exempt family transfers are those made pursuant to a divorce court order, or specific lineal-relative remission scenarios under the Remission of Stamp Duties Order. If you are considering a transfer to a family member as part of a tax planning or decoupling strategy, consult a Singapore property lawyer first. See also our guide on property decoupling in Singapore.

My property is going en-bloc — will I pay SSD?

If the collective sale is effected by a Strata Titles Board (STB) order or High Court order, SSD is waived regardless of how long you have held your unit. However, if all owners agree to a private treaty collective sale without a STB or court order, the sale is treated as a voluntary disposal and SSD may apply. In practice, most collective sales proceed via the STB route, and the exemption applies. More detail at our Singapore en-bloc guide.

Does SSD apply if I sell my HDB flat?

Technically yes — SSD applies to HDB flat sales within the holding period. However, the HDB Minimum Occupation Period (MOP) of 5 years prohibits you from selling on the open market until 5 years from the date of collection of keys. Since the new SSD window is 4 years, by the time your MOP expires, you will typically be past the SSD window, and no SSD is payable. Plus and Prime flats have a 10-year MOP, making SSD entirely academic for them. The SSD overlap with HDB MOP is thus a theoretical rather than practical concern for the vast majority of flat owners.

Who pays SSD — the buyer or the seller?

SSD is legally the liability of the seller. Unlike BSD and ABSD which are buyer obligations, SSD is accounted for in the seller’s completion statement and deducted from sale proceeds at completion. Buyers are not responsible for paying it, though if SSD is unpaid IRAS has recovery powers that could cloud the title. Your conveyancing lawyer will confirm all stamp duties are paid before releasing title documents to the buyer’s lawyer.

I am relocating overseas — can I apply for an SSD waiver?

There is no general hardship or relocation waiver for SSD. The exemptions are limited to the specific statutory categories (divorce, death, en-bloc, compulsory acquisition, HDB disposal). A job relocation, financial hardship, or change in visa status does not qualify. If you are certain you will relocate within the holding period, it may be more cost-effective to rent out the property rather than sell it — provided you are eligible to do so. See our HDB rental landlord guide for how to do this compliantly.

How does SSD interact with ABSD remission for upgrading couples?

These are separate stamp duties and do not offset each other. ABSD remission for married SC couples allows the ABSD paid on a second property to be refunded if the first property is sold within 6 months of acquiring the second. SSD, if applicable on the first property being sold, is still payable — the ABSD remission does not waive or offset SSD. In the upgrading scenario, couples must factor in both: buyer pays BSD/ABSD on the new purchase, and seller pays SSD on the disposed property if within the SSD holding period. See our HDB upgrading guide for the full analysis.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty (BSD) Singapore 2026: Rates, Calculator and Worked Examples

- Singapore Property Decoupling Guide 2026: Save ABSD, Costs, Risks and Step-by-Step Process

- Singapore HDB Upgrading Guide 2026: Costs, ABSD, CPF and Step-by-Step Process

- Singapore En-Bloc Guide 2026: How Collective Sales Work, Timeline and What Owners Need to Know

- Singapore Property Investment Guide 2026: How to Buy, Rent and Build Wealth Through Property

- Singapore Property Cooling Measures: A Complete Timeline 2009 to 2026

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Stamp duty legislation and IRAS administrative practice can change at any time. Always verify current rates and exemptions directly with the IRAS website and consult a qualified Singapore conveyancing lawyer or tax adviser before making property decisions. Property values, interest rates, and government policy cited are based on information available as at 7 June 2026.