Seller’s Stamp Duty Singapore 2026: Complete Guide to SSD Rates, Holding Periods & Exemptions

Quick Answer: Singapore SSD at a Glance

- What is SSD? Seller’s Stamp Duty is a tax charged by IRAS when you sell a residential property within 3 years of buying it.

- Current rates (properties purchased on/after 11 March 2017): Year 1 = 12%, Year 2 = 8%, Year 3 = 4%, after 3 years = Nil.

- Calculated on: the higher of the sale price or market value — you cannot avoid SSD by under-declaring the price.

- Who pays: the seller, not the buyer. SSD must be paid within 14 days of the sale contract date.

- Commercial and industrial property: separate SSD rates apply; commercial property currently has no SSD.

- Key exemptions: death of owner, divorce court order, en-bloc collective sale, HDB upgrading exercises, certain government acquisition.

- Industrial SSD: 15%/10%/5% for Years 1/2/3 (effective 11 March 2023 for industrial properties).

- Why it exists: introduced to curb short-term speculative “flipping” and protect housing market stability.

What Is Seller’s Stamp Duty (SSD)?

Seller’s Stamp Duty (SSD) is a stamp duty levied by the Inland Revenue Authority of Singapore (IRAS) on sellers who dispose of residential properties within a specified holding period after purchase. Unlike Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) — which the buyer pays on acquisition — SSD falls entirely on the seller. It is part of Singapore’s suite of property market stabilisation measures, designed to discourage speculative short-term trading that can inflate prices and reduce affordability for genuine owner-occupiers.

SSD applies to residential properties only: HDB flats, private condominiums, executive condominiums (ECs), terraced houses, semi-detached houses, and bungalows all fall within scope. Commercial shophouses, offices, industrial buildings, and strata retail units are treated separately under the industrial-property SSD framework introduced in 2011 and last updated in March 2023.

The Ministry of Finance (MOF) and IRAS jointly administer SSD policy. Rates and holding-period windows have been adjusted several times since SSD was first introduced on 20 February 2010, and understanding which era applies to a given transaction is critical — sellers who purchased property at different points in time face materially different SSD exposure.

Figure 1: Residential SSD rates 2026 — properties purchased on/after 11 March 2017. Source: IRAS.

SSD Rate History: How the Rules Have Evolved

Singapore’s SSD has been tightened and loosened in tandem with each property market cycle. Understanding the history is essential because the era in which a property was purchased determines the applicable rate schedule — these do not update retrospectively.

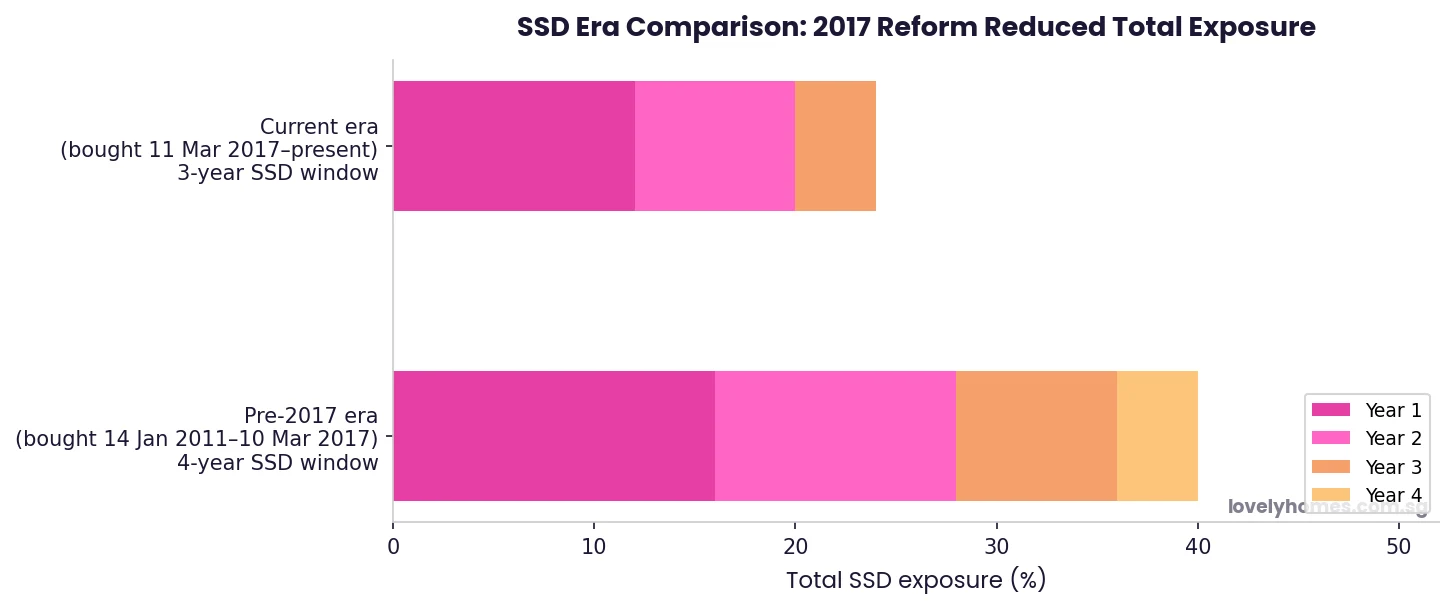

February 2010 — SSD introduced. A flat 1% SSD was applied on residential properties sold within one year of purchase. This was a modest initial measure aimed at checking the most acute short-term flipping.

August 2010 — First tightening. The holding period was extended to 3 years and rates were raised: Year 1 = 3%, Year 2 = 2%, Year 3 = 1%. The government wanted to extend the disincentive horizon.

January 2011 — Major escalation. Rates jumped sharply: Year 1 = 16%, Year 2 = 12%, Year 3 = 8%, Year 4 = 4% (holding period extended to 4 years). This era lasted until March 2017.

March 2017 — Current framework. The 4-year window was trimmed to 3 years and top rates were reduced: Year 1 = 12%, Year 2 = 8%, Year 3 = 4%. This partial easing recognised the market had cooled following the 2013–2015 cooling measures. Properties purchased on/after 11 March 2017 fall under this framework.

The April 2023 cooling measures — which raised ABSD substantially for second-property buyers and foreigners — did not change residential SSD rates. Industrial property SSD was separately restructured in March 2023 to align more closely with the residential framework.

Figure 2: SSD eras — the 2017 reform shortened the holding window from 4 to 3 years and reduced the cumulative rate burden. Source: IRAS, MOF.

Current SSD Rates in Detail (2026)

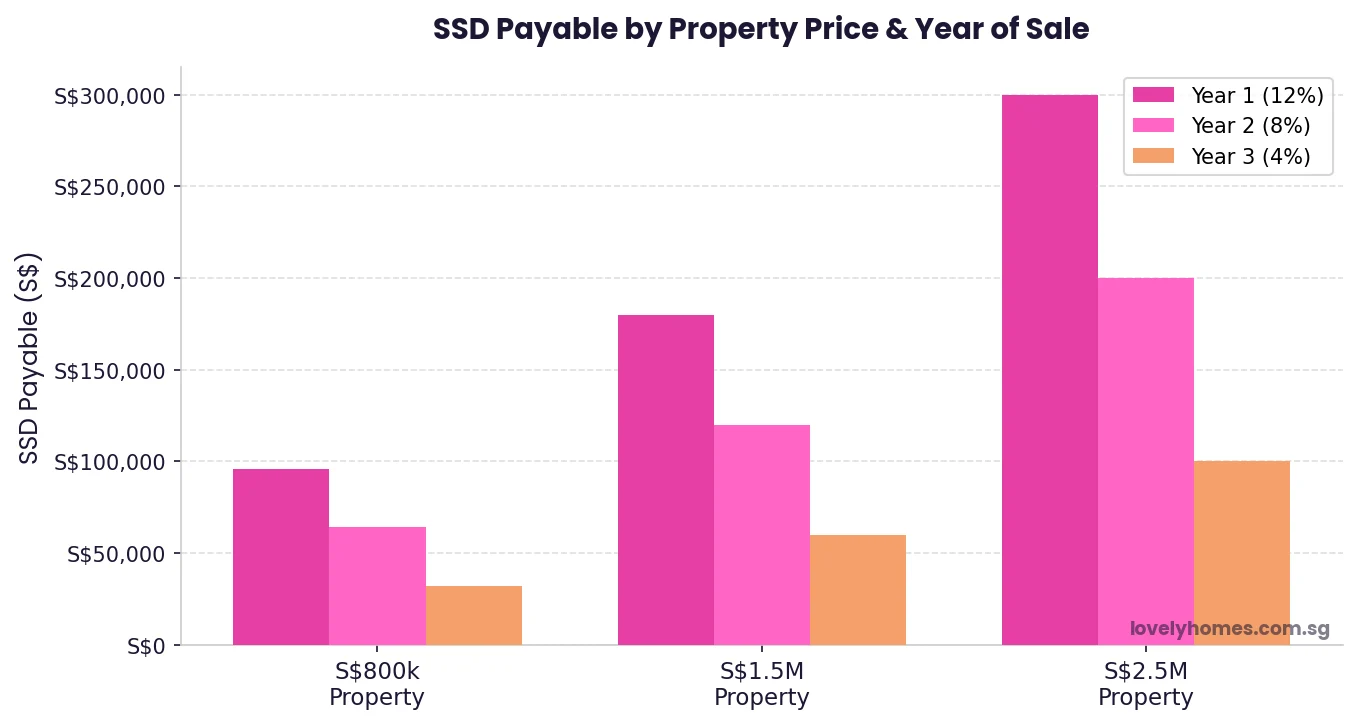

For any residential property purchased on or after 11 March 2017, the SSD rates are as follows:

| Year of Sale | Holding Period at Sale | SSD Rate | Example (S$1.2M property) |

|---|---|---|---|

| Year 1 | Sold within 12 months of purchase | 12% | S$144,000 |

| Year 2 | Sold in months 13–24 | 8% | S$96,000 |

| Year 3 | Sold in months 25–36 | 4% | S$48,000 |

| After Year 3 | Sold after 36 months | Nil | S$0 |

The SSD is calculated on whichever is higher — the agreed sale consideration or the property’s open market value as assessed by IRAS. This prevents artificial under-pricing of transactions between related parties.

The “year” is counted from the date of purchase (specifically, the date of the Sale and Purchase Agreement, or the date of the Option to Purchase if exercised). A property bought on 1 April 2024 sold on 31 March 2025 is in Year 1; sold on 2 April 2025, it enters Year 2. Getting the date calculation right — down to the day — materially affects the tax bill.

Payment of SSD is due within 14 days of the date of the contract to sell (or date of transfer if there is no formal contract). Late payment attracts penalties and interest charges from IRAS.

What Is SSD Calculated On?

SSD is assessed on the higher of: (a) the actual sale price agreed between buyer and seller, or (b) the open market value of the property as determined by IRAS at the time of sale. The practical effect is that artificially depressed selling prices do not reduce SSD liability — IRAS will use market value instead.

For most arm’s-length market transactions, the sale price is the market value, so there is no difference. However, where a property is sold between related parties (family members, or a company to a director), IRAS typically commissions its own valuation to verify. Sellers should obtain an independent valuation before transacting in such circumstances to avoid a surprise SSD reassessment.

In cases where the property is partially gifted (e.g., the seller receives S$500,000 for a property worth S$1M, with the remainder as a gift), IRAS treats the full market value of S$1M as the basis for SSD — the gift portion does not reduce the SSD calculation.

Figure 3: SSD payable in absolute S$ terms across three price points — the tax is substantial in Years 1 and 2 even at moderate property values. Source: IRAS, LovelyHomes calculations.

Key SSD Exemptions

Not every sale within the 3-year window triggers SSD. IRAS recognises a set of circumstances where requiring SSD would be inequitable. The main exemptions are:

| Exemption | Conditions | Who to Apply To |

|---|---|---|

| Death of owner | Property is transferred to the estate or beneficiaries following the owner’s death | IRAS (estate executor applies) |

| Divorce / separation order | Property is transferred pursuant to a court order in divorce or separation proceedings | IRAS with supporting court order |

| En-bloc / collective sale | Property sold as part of an en-bloc (collective sale) exercised under the Land Titles (Strata) Act | Automatically exempted by IRAS on production of the collective sale order |

| Compulsory acquisition | Land or property compulsorily acquired by the government under the Land Acquisition Act | IRAS notified by acquiring authority |

| HDB upgrading / SERS | HDB flat acquired by HDB under SERS (Selective En-bloc Redevelopment Scheme) or similar exercises | HDB administers; automatic |

| Certain matrimonial transfers | Transfer to or from a spouse during the course of marriage (not divorce) — partial relief only; specific conditions apply | IRAS advance ruling recommended |

Notably, financial hardship is not an automatic SSD exemption. If a seller must sell early due to retrenchment or mortgage default, SSD still applies unless one of the listed exemptions is met. Sellers in distress should consult a property lawyer to explore whether any exemption is available before proceeding with a sale.

Industrial Property SSD (2026)

A separate SSD framework covers industrial properties — factories, warehouses, light industrial space, and business parks. This framework was introduced in January 2013 and was significantly revised with effect from 11 March 2023, when the MOF extended the industrial SSD holding period to match the residential framework:

| Year of Sale | SSD Rate (Industrial) | Applicable To |

|---|---|---|

| Year 1 | 15% | Industrial properties purchased on/after 11 March 2023 |

| Year 2 | 10% | |

| Year 3 | 5% | |

| After Year 3 | Nil | All industrial property purchases |

Industrial SSD rates are notably higher than residential rates — the government treats speculative activity in industrial property with particular concern given its importance to business productivity. Commercial properties (offices, shophouses, retail units) currently attract no SSD in Singapore.

Worked Example: Calculating SSD Before You Sell

Case Study — Mr Tan’s D5 Condo

Background: Mr Tan (Singapore Citizen) purchased a 2-bedroom condo in the Buona Vista area for S$1,200,000 on 15 March 2024 (OTP date). His job changed and he needs to relocate; he accepts an offer of S$1,280,000 on 20 February 2026.

Holding period calculation:

- Purchase date: 15 March 2024

- Sale date: 20 February 2026

- Duration: 23 months 5 days → Year 2 (13–24 months)

SSD computation:

- Higher of sale price (S$1,280,000) vs market value — assume arm’s-length transaction so S$1,280,000 applies.

- Year 2 rate: 8%

- SSD payable: S$1,280,000 × 8% = S$102,400

- SSD due within 14 days of 20 February 2026: by 6 March 2026.

What if Mr Tan waits until after 15 March 2027 (i.e., holds for more than 3 years)?

- Assuming the property appreciates modestly to S$1,310,000 by March 2027.

- SSD: Nil. He saves S$102,400 in SSD, in exchange for holding 13 more months.

- Net gain from waiting: S$30,000 (appreciation) + S$102,400 (SSD saved) = S$132,400 — significant for a 13-month wait.

This illustrates why the 3-year SSD window is a powerful behavioural anchor: even a modest price gain can be outweighed by SSD in Year 2, making it economically rational to hold.

SSD vs ABSD: Understanding the Difference

SSD and ABSD are both stamp duties on residential property transactions, but they serve different purposes and fall on different parties:

| Feature | SSD | ABSD |

|---|---|---|

| Who pays | Seller | Buyer |

| Purpose | Curb short-term speculation / flipping | Cool demand; differentiate by residency status and property count |

| Time-dependency | Yes — decreases with holding period; zero after 3 years | No — flat rate on acquisition, regardless of how long buyer intends to hold |

| Maximum rate (residential, 2026) | 12% (Year 1) | Up to 60% (foreigners, any residential property) |

| Administered by | IRAS | IRAS |

| Applies to | Residential + industrial property | Residential property only (different rates for SCs, PRs, foreigners) |

A property transaction can involve both SSD (payable by the seller) and ABSD (payable by the buyer) simultaneously. For example, a seller disposing of a condo within Year 2 of ownership (SSD: 8%) sells to a foreigner (ABSD: 60%). The total stamp-duty burden across both parties at a S$1.5M price point: seller pays S$120,000 SSD; buyer pays S$900,000 ABSD. These are legally separate obligations borne by separate parties, though in practice the combined tax burden may influence the negotiated sale price.

What Does This Mean for Property Sellers in 2026?

With residential property prices having risen materially since 2020, and with SSD remaining at its post-2017 structure through 2026, there are several practical implications for sellers:

First, the 3-year holding period is a real constraint. Sellers who purchased a resale condo in mid-2024 at the market peak may find that selling in mid-2026 still attracts 8% SSD on a potentially lower sale price — a double adverse outcome. Patience past the 3-year mark is financially rational for most sellers who are not under financial duress.

Second, en-bloc candidates require careful SSD analysis. If a strata development proceeds to collective sale, individual unit owners may have purchased at different points in time. Those who bought within 3 years of the en-bloc completion are SSD-exempt under the collective sale exemption, but only if the sale is completed (not merely approved) within the relevant window.

Third, gifting property to family members does not avoid SSD. If a parent bought a condominium in 2024 and attempts to transfer it to an adult child in 2025 as a gift, IRAS will still assess SSD on the market value at the time of transfer. The gift exemption does not extend to SSD (unlike some other jurisdictions).

What Might Come Next for Singapore SSD?

The following section represents analytical commentary based on publicly available signals — it is not government guidance.

As at July 2026, there has been no announcement of changes to the residential SSD framework. The market remains broadly stable: URA’s Q2 2026 flash estimate shows the private residential price index rose just 0.5% quarter-on-quarter, decelerating from 0.9% in Q1 2026. This suggests the government sees no immediate need to further tighten the SSD framework to address speculative activity.

Were prices to accelerate sharply — driven by strong en-masse foreign demand or a sudden speculative upcycle — the government’s historical playbook (most recently demonstrated in April 2023) suggests it would first deploy ABSD increases or LTV tightening before revisiting SSD, which is a blunter instrument.

A possible policy evolution that industry observers have discussed is the introduction of a sliding-scale SSD that integrates with ABSD and BSD into a unified transaction-tax framework. As yet, this has not been mooted officially. The current three-lever approach (SSD + BSD + ABSD) remains the operative framework for the foreseeable future.

Frequently Asked Questions

Do I pay SSD on an HDB flat?

Yes. SSD applies to HDB flats in exactly the same way as private residential properties. If you sell your HDB flat within 3 years of the date of purchase (or the date of the Temporary Occupation Permit for new BTO flats), you are liable for SSD at 12%/8%/4% for Years 1/2/3 respectively. However, if HDB compulsorily acquires your flat under SERS or similar exercises, you are exempt. Note that HDB’s own Minimum Occupation Period (MOP) of 5 years means most HDB sellers are already beyond the SSD window before they are even eligible to sell on the open market — so SSD is rarely an issue in practice for standard HDB resale transactions.

I am selling a property bought in 2012 — which SSD rates apply?

Any property purchased between 14 January 2011 and 10 March 2017 is subject to the then-current framework: a 4-year holding period with rates of 16%/12%/8%/4% for Years 1/2/3/4 respectively. However, if you purchased in 2012 and are selling in 2026, you have well exceeded the 4-year window — SSD is Nil. Only sellers who purchased in the 2012–2022 period and sold promptly would have faced these older rates. As at 2026, all pre-2017 purchase dates are beyond their respective SSD windows.

Can I get SSD remission if I am retrenched and cannot afford the mortgage?

Financial hardship is not a legislated SSD exemption in Singapore. Unlike some other countries that allow compassionate remissions, IRAS currently provides no general hardship exemption for SSD. If you are facing forced sale due to retrenchment, medical emergency, or financial difficulty, you should consult a property lawyer to determine whether any of the specific exemptions (e.g., divorce, death) apply to your situation. You may also consider requesting a payment plan from IRAS, though SSD is not automatically deferred. Engaging a lawyer before signing any sale contract is strongly recommended if SSD will create a significant financial burden.

How is SSD paid — is it deducted from sale proceeds automatically?

SSD is not automatically deducted. It is the seller’s legal obligation to file and pay the SSD to IRAS within 14 days of the date of the contract of sale (typically the date on which the buyer exercises the Option to Purchase). The conveyancing lawyer acting for the seller will typically compute the SSD, prepare the stamping documents, and arrange payment from the sale proceeds at completion. The SSD amount is effectively deducted from the sale proceeds at the point of legal completion, coordinated by the seller’s solicitor. You should ensure your conveyancing lawyer calculates SSD correctly and builds it into the net proceeds computation before you commit to a sale price.

Does SSD apply to properties held under a company or trust?

Yes. SSD applies to corporate entities and trusts that hold residential property in the same way as it applies to individual sellers. A company or trust that purchased a residential property in 2024 and sells it in 2025 is liable for 12% SSD on the higher of sale consideration or market value. This is relevant for family investment holding companies and real estate investment structures. There is no corporate exemption from SSD; entities are treated on the same basis as individual owners for the purposes of the holding-period calculation.

What is the difference between the SSD “Year 1” calculation for a property bought on 1 April 2024?

Year 1 SSD applies when the property is sold within the first 12 calendar months from the date of purchase. For a property bought on 1 April 2024 (using the date of the signed Option to Purchase as the purchase date), Year 1 ends on 31 March 2025. A sale contract signed on 31 March 2025 falls in Year 1 (12% SSD); one signed on 1 April 2025 enters Year 2 (8% SSD). The difference of a single day can reduce SSD liability at S$1.5M from S$180,000 to S$120,000 — a saving of S$60,000. Sellers should confirm the exact purchase date and holding-period boundary with their conveyancing lawyer before signing the Option to Purchase for the sale.

Does SSD apply if I am selling to my own company?

Yes. Selling a property to a related company — including one you own or control — does not exempt the transaction from SSD. IRAS looks through related-party arrangements and will assess SSD on the open market value if the agreed consideration is below market. Where you sell a property to your company within 3 years of purchase, SSD applies at the full market value. This is a common trap in restructuring transactions: what looks like an internal reorganisation from a commercial perspective is still a taxable disposal for SSD purposes.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Buyer’s Stamp Duty Singapore 2026: BSD Rates, Calculation and Remissions

- Singapore Property Cooling Measures Timeline 2009–2026

- HDB CPF Housing Grant Guide 2026: EHG, Family Grant, PHG and Singles Grant

- Singapore Condo Sinking Fund & Maintenance Fee Guide 2026

- East Coast Neighbourhood Guide Singapore 2026: D15 Prices & TEL Impact

Disclaimer

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. SSD rates, exemptions, and administrative procedures are set by the Inland Revenue Authority of Singapore (IRAS) and the Ministry of Finance (MOF) and may change without prior notice. Readers should refer to the official IRAS website (www.iras.gov.sg) and the Stamp Duties Act for authoritative information. Before entering into any property transaction, you are strongly encouraged to seek independent advice from a licensed conveyancing solicitor and a qualified financial adviser.