Singapore En Bloc Seller’s Guide 2026: Collective Sale Process, Proceeds and What Owners Need to Know

Quick Answer: What Is an En Bloc Sale in Singapore?

- An en bloc sale (collective sale) is where all owners of a strata-titled development — such as a private condo, HUDC estate, or cluster development — collectively sell the entire site to a developer or investor.

- Governed by the Land Titles (Strata) Act (LTSA), a collective sale requires the consent of owners holding at least 80% by share value and strata area for developments over 10 years old (90% for developments under 10 years old).

- Minority owners who refuse are bound by the decision if the Strata Titles Board (STB) or High Court approves the sale — they cannot block a properly executed collective sale.

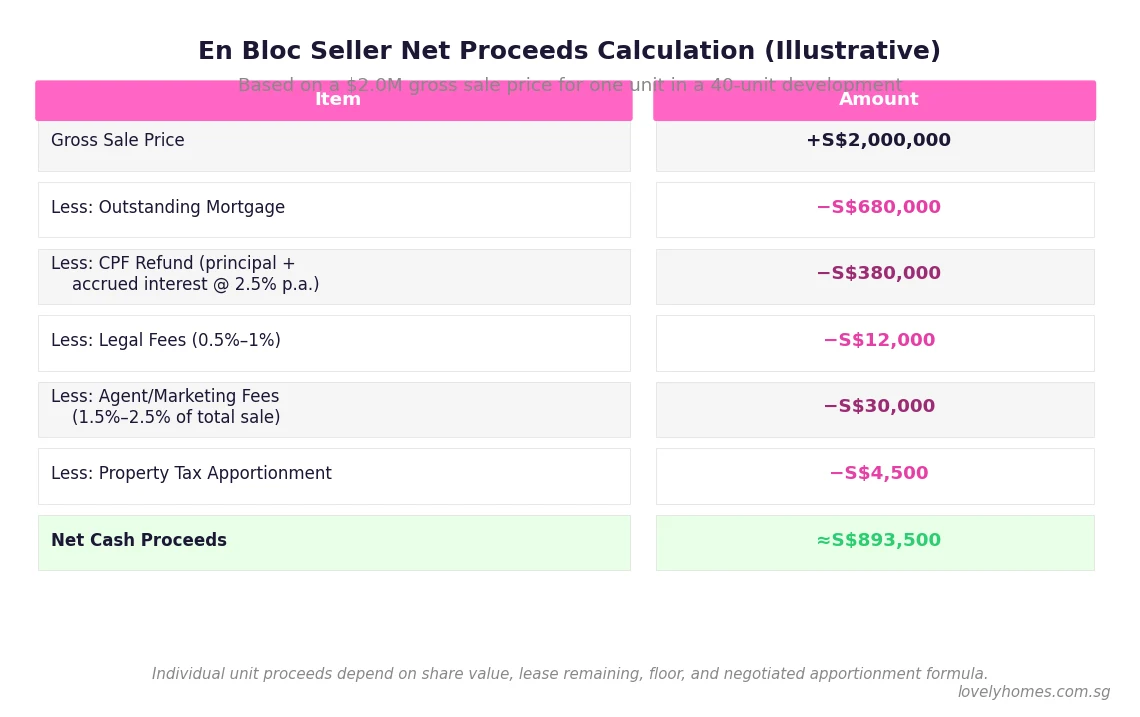

- Typical proceeds for a seller: the gross sale price for their unit, less their outstanding mortgage, CPF refund (principal + accrued interest at 2.5% p.a.), legal fees (~0.5–1%), and agent/marketing fees (~1.5–2.5% of total site price).

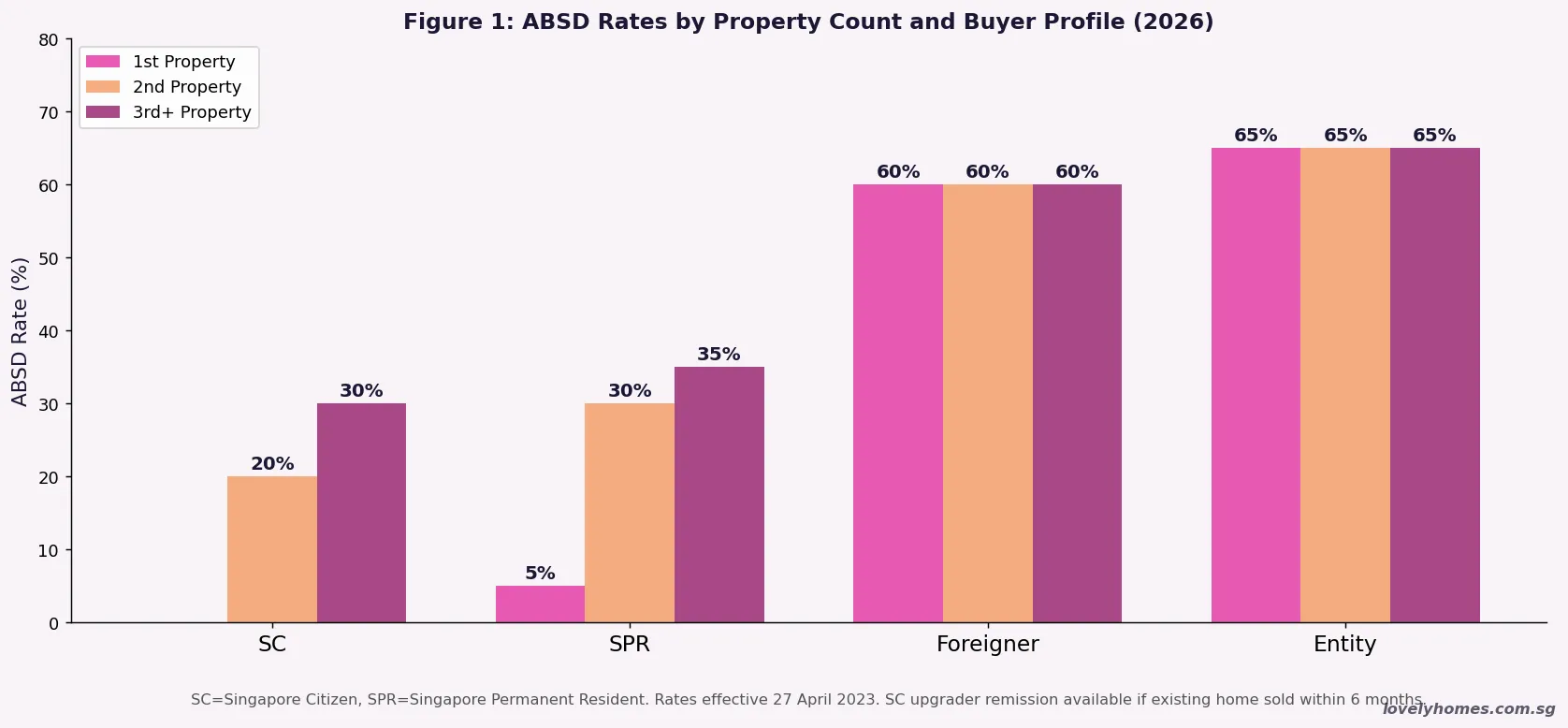

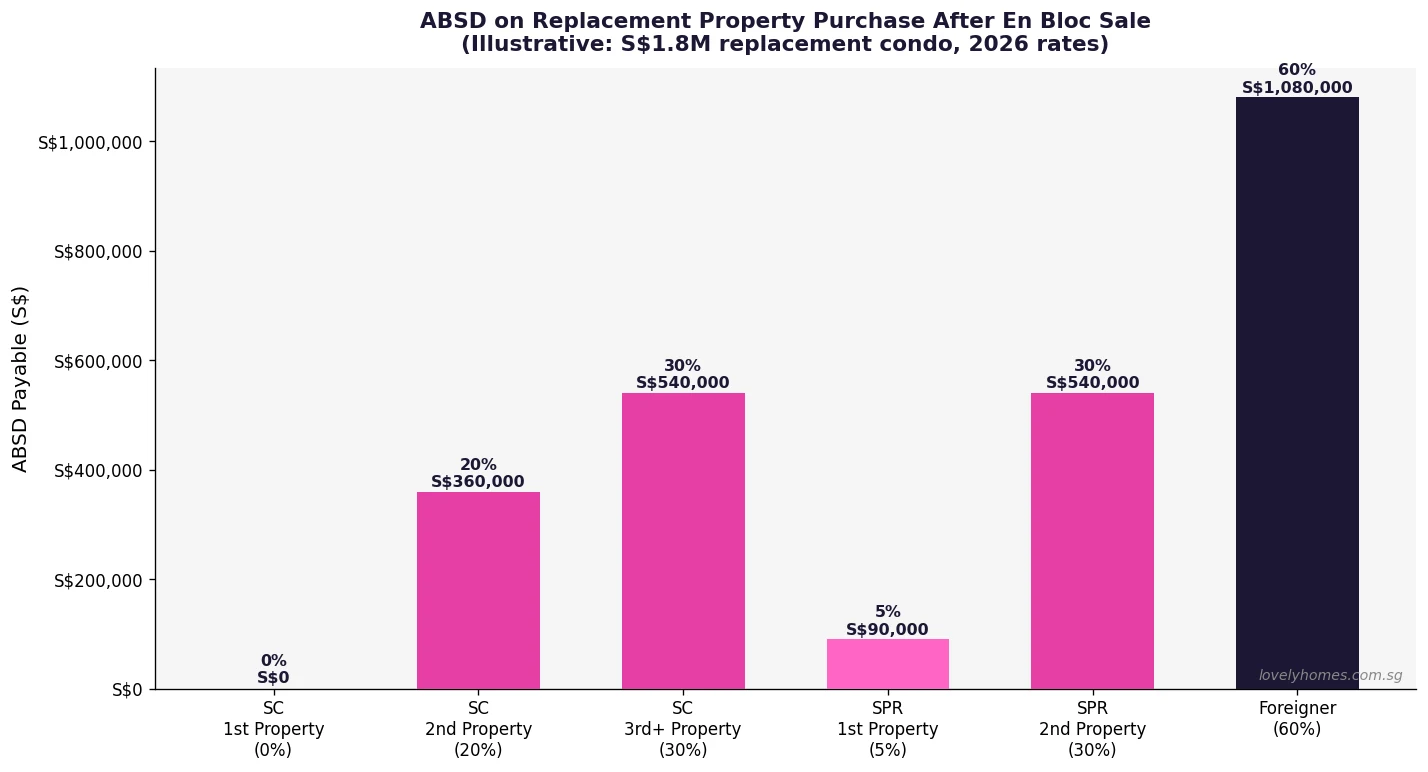

- The ABSD on any replacement property purchase depends on the owner’s profile — a SC first-time buyer pays 0%; a SC buying a second property pays 20%. Planning the next purchase is essential before accepting the en bloc offer.

- Typical timeline: 12–36 months from Collective Sale Committee (CSC) formation to completion. Some contentious sales take longer if STB or court proceedings are required.

- ABSD remission may be available for SC couples who sell their only property and buy a replacement within 6 months — plan this sequence carefully.

What Is a Collective Sale (En Bloc)?

A collective sale — commonly called an “en bloc” sale — is a transaction under which all unit owners in a strata development sell their units simultaneously to a single buyer, typically a property developer. The buyer acquires the entire site in one transaction, usually with the intention of redeveloping it.

En bloc sales are governed by Part VA of the Land Titles (Strata) Act (Cap. 158) (LTSA), administered by the Singapore Land Authority (SLA). The legislative framework sets out the consent thresholds, procedural requirements, the role of the Collective Sale Committee, and the mechanism for binding dissenting minority owners through the Strata Titles Board (STB) or the High Court.

For property owners, an en bloc sale is both an opportunity and a disruption. The opportunity: receiving a premium above individual unit market value, because developers pay for the land redevelopment potential — the “en bloc premium.” The disruption: forced relocation, the need to find replacement housing quickly, and a complex tax and financial planning exercise involving ABSD, CPF, and mortgage settlement.

The Consent Threshold: Who Decides?

The LTSA requires that an en bloc sale be supported by owners holding at least 80% of the share value and 80% of the total strata floor area — for developments that are at least 10 years old from the date of the Temporary Occupation Permit (TOP) or the Certificate of Statutory Completion (CSC). For newer developments (under 10 years from TOP/CSC), the threshold rises to 90% in both measures.

Once the threshold is crossed, the sale can proceed even without the agreement of the remaining minority — provided it meets all other statutory requirements. The STB or High Court may approve the sale over dissenting owners’ objections if it is satisfied that the sale is in good faith, the proceeds are distributed equitably, and the transaction price represents fair market value.

Share value in a condo development is allocated to each unit at the time of strata subdivision, typically proportional to the unit’s floor area. A larger unit with a higher share value has proportionally more voting weight in the en bloc consent process. Strata floor area is the individual unit size as defined in the approved strata plan.

| Requirement | ≥10-Year Development | <10-Year Development |

|---|---|---|

| Consent by share value | 80% | 90% |

| Consent by strata floor area | 80% | 90% |

| Minority bound? | Yes, if STB/court approves | Yes, if STB/court approves |

| STB Good Faith Test | Required | Required |

| Typical STB timeline | 2–4 months | 2–4 months |

How Proceeds Are Calculated and Distributed

The total sale price for the entire development is determined by the tender or private treaty negotiation process. Each unit’s share of the total proceeds is then calculated according to an apportionment formula agreed upon in the Collective Sale Agreement (CSA). The most common apportionment methods are: by share value, by strata floor area, or a combination of the two.

From each unit’s gross proceeds, the following deductions apply before the owner receives net cash:

The most significant deductions — and the ones most commonly misunderstood by owners — are the CPF refund and the agent/marketing fees. The CPF refund is not a fee paid to an external party; it is the owner’s own CPF money being returned to their Ordinary Account (plus compounding at 2.5% per annum). However, because it is returned to CPF — not paid as cash — owners who have drawn heavily on CPF for mortgage servicing may find that their net cash proceeds are lower than they expect.

Agent and marketing fees are typically charged as a percentage of the total site sale price — not just one unit’s share. For a 40-unit development sold for S$200M, a 1.5% commission totals S$3M, or S$75,000 per unit on average. This is negotiable and should be agreed upon before the agent is formally appointed by the CSC.

The Role of the Collective Sale Committee (CSC)

The Collective Sale Committee is elected at an Extraordinary General Meeting (EGM) of the Management Corporation Strata Title (MCST). The CSC is the body that initiates and manages the en bloc process on behalf of all consenting owners. Its key responsibilities include engaging a licensed marketing agent (or conducting a public tender directly), appointing a law firm to prepare the CSA and manage the STB application, commissioning an independent valuation of the site, and setting the reserve price below which the development will not be sold.

The CSC owes a duty of good faith to all owners — including dissenting ones. It must ensure that the sale is conducted transparently, that the reserve price is not set below the independent valuation, and that all owners receive equal access to information about the proposed terms.

Under the LTSA, CSC members cannot be a party to any contract that gives them a personal benefit from the sale that other owners do not share — they must remain impartial fiduciaries. Owners who believe the CSC has acted improperly can lodge objections with the STB.

ABSD on the Replacement Purchase: Planning Ahead

An en bloc sale forces owners to buy replacement housing. The ABSD implications of that replacement purchase are significant — and the planning must begin well before the en bloc sale is completed.

The key planning consideration is whether the owner will be a first-time buyer of their replacement property — i.e., will they own zero other properties at the time the replacement OTP is exercised. For most en bloc sellers, this depends on whether they have other private properties. If the en bloc unit is their only property, they will generally be a first-time buyer for ABSD purposes on the replacement purchase.

For Singapore Citizens who sell their only property and buy a replacement private residential property, the ABSD remission for SC couples may also be applicable: if they purchase the replacement property before selling their en bloc unit, they pay 20% ABSD upfront — but can apply to IRAS for a refund once they sell the en bloc property within 6 months of the replacement purchase. This sequence requires careful cash flow management, as the upfront ABSD may need to be funded while the en bloc proceeds are still in the completion pipeline.

Worked Example: The Ramasamy Family’s En Bloc Experience

Situation: Mr and Mrs Ramasamy are both Singapore Citizens. They own a 1,200 sq ft unit in a 48-unit Bishan condo originally purchased in 2010 for S$960,000. The development (TOP 2004, now 22 years old) has successfully obtained 83% consent for a collective sale at a total site price of S$420M. The Ramasamys’ unit’s gross share of proceeds is S$2,100,000 based on the apportionment formula.

Deductions from Gross Proceeds (S$2,100,000):

Outstanding mortgage balance: −S$320,000

CPF used (principal S$350,000 + accrued interest 2.5% p.a. for 16 years ≈ S$175,000): −S$525,000

Legal fees (~0.6%): −S$12,600

Marketing agent fees (their unit’s share at 1.5%): −S$31,500

Property tax apportionment and misc.: −S$5,200

Net Cash Proceeds: ≈ S$1,205,700

CPF OA top-up: S$525,000 (returned to their joint CPF OA accounts)

Replacement Property Planning:

The Ramasamys plan to purchase a S$1.9M freehold condo in District 20 as their replacement home. Since this will be their only property (the en bloc unit is sold), they are SC first-time buyers → ABSD: S$0.

BSD on S$1.9M: S$1,800 + S$3,600 + S$19,200 + S$4,000 (on last S$100K at 4%) = S$28,600 BSD

Downpayment (25%): S$475,000 — funded from net cash proceeds.

Bank loan: S$1,425,000 at 3.0% over 25 years → S$6,744/month.

Combined TDSR: S$6,744 ÷ S$15,000 (combined income) = 45.0% ✓

Net cash remaining after downpayment and costs: ≈ S$695,000

Key Timing Issue: The Ramasamys should confirm the en bloc completion date (typically 12 months after STB approval) before committing to a replacement OTP. If they need to purchase before completion, they may need bridging finance for the downpayment. Consult a mortgage adviser at least 6 months before the expected completion date.

What Minority Owners Can and Cannot Do

A minority owner (one who did not sign the CSA or who explicitly objects) has limited but meaningful protections under the LTSA. They may file an objection with the STB on the following grounds: (a) the sale price is not in good faith and does not reflect market value; (b) the proceeds distribution formula is inequitable; (c) the majority owners’ conduct has been improper; or (d) the sale will cause them a financial loss (i.e., their net proceeds after repaying their mortgage and CPF are negative).

The STB has the power to dismiss such objections if it finds that the sale meets the good-faith test and the distribution is equitable. Once the STB issues its approval order, all owners — including dissenters — are bound and must vacate and transfer title at completion. Refusal to do so may result in the court compelling the transfer.

Minority owners are entitled to receive the same gross proceeds per share as consenting owners. They cannot be offered a lower price for holding out — the CSA must apply the same formula to all units. The only difference is that dissenting owners bear their own legal costs for any STB objections they file.

Why En Bloc Matters: Singapore’s Urban Renewal Cycle

En bloc sales are a structural feature of Singapore’s built environment. Because 99-year leasehold land diminishes in value as the lease runs down, and because the island’s limited land area means underutilised sites are regularly returned to the urban system, collective sales serve as the primary mechanism for private-sector urban renewal. The Urban Redevelopment Authority (URA) monitors and facilitates this process through its Master Plan and development control rules that govern what can be built on a redeveloped site.

En bloc activity tends to be cyclical and correlated with developer land bank depletion and Government Land Sales (GLS) programme supply. When GLS supply is tight and developers need land, en bloc bids rise — driving the en bloc premium that makes collective sales attractive to owners. As of mid-2026, developer land bank levels are moderate, and the en bloc market remains selective — large, well-located developments with strong redevelopment potential continue to attract developer interest.

What Might Come Next

The LTSA en bloc framework has been revised several times — most recently in 2018, when procedural requirements were tightened to protect minority owners and ensure greater transparency in CSC governance. Regulators are unlikely to fundamentally alter the framework, which has proven effective at facilitating urban renewal while providing minority protections. However, incremental adjustments — such as minimum reserve price rules or stricter good-faith disclosure requirements — are possible in future Budget cycles.

For en bloc timing, owners in ageing developments (15–25 years from TOP) located in areas with active redevelopment potential — particularly in the Core Central Region and in major rejuvenation corridors designated in URA’s long-term plans — should monitor their development’s en bloc viability periodically. The window for maximum en bloc premium typically narrows as remaining lease runs below 60 years, at which point CPF and bank financing restrictions reduce the pool of eligible buyers for individual units, lowering their market value.

Frequently Asked Questions

Can I refuse to sell in an en bloc sale?

You can withhold your signature from the CSA — but you cannot ultimately block a sale that meets the LTSA consent threshold and passes the STB’s good-faith test. Once the STB issues its approval, all owners, including those who did not consent, are legally bound by the sale. The only recourse for a dissenting owner is to file an objection with the STB on specific grounds (e.g., financial loss, inequitable distribution, breach of good faith), and to appeal STB decisions to the High Court. Resistance beyond these legal channels will not prevent the sale from proceeding.

How is the reserve price determined?

The reserve price is the minimum price below which the CSC will not accept any offer. It is set by the CSC based on an independent valuation conducted by a licensed property valuer — the reserve price must not be set below this valuation, as doing so would fail the LTSA’s good-faith test. In practice, the reserve price is typically set at the independent valuation level or modestly above it, to reflect the en bloc premium that a developer would need to pay for the redevelopment potential. Once set, the reserve price is disclosed in the public tender documents and to all owners before the CSA signing exercise.

What happens to my HDB flat eligibility after an en bloc sale?

If you sold an en bloc private property and are now a “first-timer” (no current private property ownership), you may be eligible to purchase an HDB flat — provided you meet HDB’s income ceiling and citizenship eligibility criteria. However, if your household income exceeds S$14,000 per month (S$21,000 for extended families), you may not be eligible for a new BTO flat even as a displaced en bloc seller. The HDB Silver Housing Bonus and other schemes are available for elderly en bloc sellers downsizing. Consult HDB or a licensed real estate consultant before making assumptions about HDB eligibility.

Will my rental income from the en bloc unit continue until completion?

Yes, you retain the right to rent out your unit until the legal completion date — typically 12 months after STB approval for the transfer of legal title. However, any tenancy agreement must include a clause allowing early termination upon reasonable notice (usually 2 months) to accommodate the en bloc completion. Under the Residential Tenancies Act, tenants of en bloc units have specific rights regarding notice periods and relocation assistance. Ensure your tenancy agreement is reviewed by your solicitor in light of the en bloc proceedings.

What is the “good faith” test the STB applies?

The Strata Titles Board assesses whether the transaction price was arrived at in good faith, taking into account: (a) the sale price compared to the independent valuation; (b) the method of distributing sale proceeds among owners; (c) the relationship between the purchaser and any owner, or any agent; and (d) the latent defects of title affecting the development. If the STB finds that the transaction price was not arrived at in good faith — for example, if a CSC member had an undisclosed conflict of interest, or if the price was materially below valuation — it may refuse to approve the sale.

Can the developer delay completion and what recourse do I have?

Once the conditional SPA is executed, both parties are contractually bound to complete on the scheduled date, typically 12 months after the date of the Strata Titles Board Order. If the developer fails to complete, the CSA solicitors (acting on behalf of all owners) may pursue the developer for specific performance or damages under the SPA. Conversely, if owners cause delays by refusing to vacate, the purchaser may seek court orders compelling handover. Delays in en bloc completions, while uncommon, have occurred due to financing conditions in the SPA not being met — this should be flagged as a risk by your solicitor when reviewing the SPA terms.

What are the tax implications of receiving en bloc proceeds?

In Singapore, capital gains tax does not apply to individuals. The proceeds you receive from an en bloc sale — whether the gain is derived from an increase in property value or from the en bloc premium — are not subject to income tax for individual owners (as opposed to companies or developers, for whom different tax rules may apply). However, if IRAS determines that you are a “property trader” who regularly buys and sells properties for profit, the gains may be characterised as trading income and subject to income tax. For most homeowners with a single en bloc unit, this risk is low. Consult a tax professional if you are uncertain about your tax position.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore Private Property Buying Costs 2026: Complete All-In Cost Guide

- Singapore Joint Property Ownership Guide 2026: Joint Tenancy, Tenancy-in-Common, ABSD and CPF Rules

- Singapore Property Decoupling Guide 2026: How to Save ABSD by Transferring Ownership

- Singapore Private Property Resale Process 2026: Step-by-Step Guide from OTP to Keys

- Singapore CPF Accrued Interest for Property 2026: What You Owe Your CPF When You Sell

Disclaimer: The information in this article is provided for general educational purposes only. LTSA provisions, ABSD rates, CPF rules, and STB procedures cited are based on legislation and regulatory guidance current as at June 2026 and are subject to change. LovelyHomes does not provide legal, tax, or financial advice. Before making any decisions regarding an en bloc sale — whether as a consenting owner, dissenting owner, or CSC member — consult a licensed conveyancing solicitor, a tax specialist registered with IRAS, and a MAS-licensed financial adviser. Authoritative sources: SLA (sla.gov.sg), IRAS (iras.gov.sg), URA (ura.gov.sg), CPF Board (cpf.gov.sg), Singapore Statutes Online (sso.agc.gov.sg).