Singapore New Launch Condo Buying Guide 2026: Showflat, Balloting, Progressive Payments and Everything to Know Before You Buy

Quick Answer: Key Takeaways

- Buying a new launch condo in Singapore means purchasing directly from the developer before or shortly after the project receives Temporary Occupation Permit (TOP).

- You pay via the Progressive Payment Scheme (PPS): 5% booking fee at OTP, 15% on exercising the Sales & Purchase (S&P) Agreement, then staged payments tied to construction milestones.

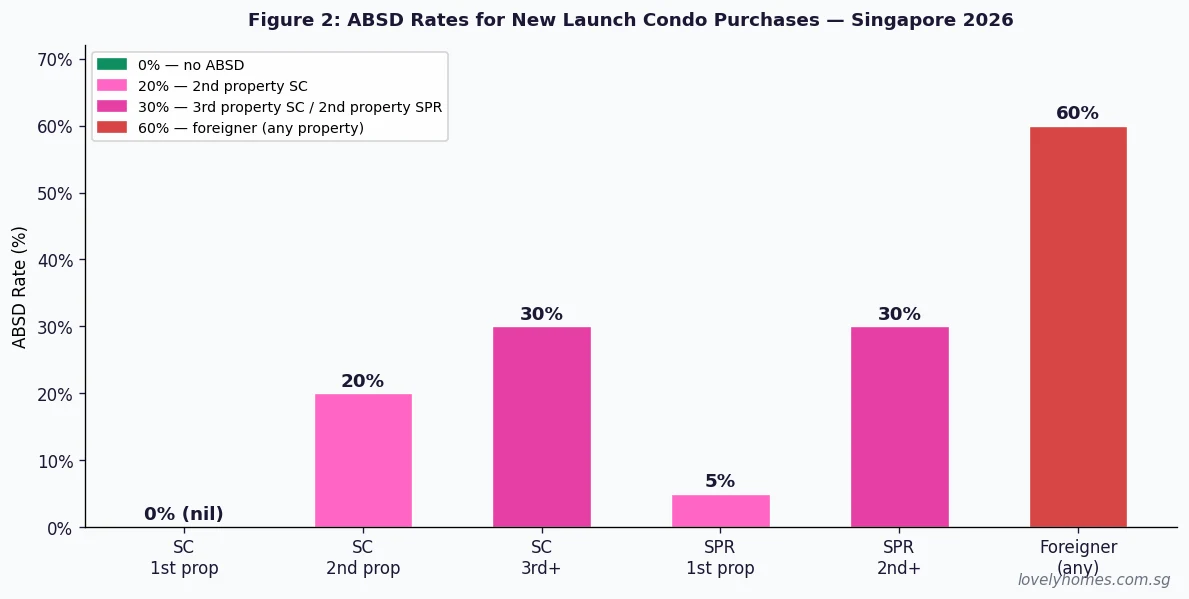

- ABSD applies upfront and is due within 2 weeks of the OTP exercise. For Singapore Citizens buying their second property: 20%. Foreigners: 60%. Plan for this before you commit.

- New launches carry a 5-year Seller’s Stamp Duty (SSD) lock-in — you cannot sell without a significant penalty within 5 years of purchase.

- Unlike resale, you receive the flat in its bare shell at TOP. Renovation costs (typically S$50,000–S$120,000 for a standard 2-bedroom) must be budgeted separately.

- The ballot system — especially for highly anticipated launches — means you may not get the unit or floor you want even after registering interest.

- New launch condos in Singapore have historically outperformed resale on price quantum appreciation from launch to TOP, but this is not guaranteed and varies by project and location.

What Is a New Launch Condo?

A new launch condo (or new launch private residential property) is a condominium development released for sale by the developer before or shortly after it receives TOP. In Singapore’s context, most new launches happen via a showflat sales exercise during the construction phase — you view show units and buy off-plan, before the actual building is complete. The developer holds a licence from the Urban Redevelopment Authority (URA) to sell, and the transaction is governed by the Housing Developers (Control and Licensing) Act.

New launches are distinct from resale condos (completed units bought on the secondary market) and from executive condominiums (ECs) (hybrid developments with HDB-like eligibility restrictions for the first five years). This guide focuses exclusively on private new launch condos.

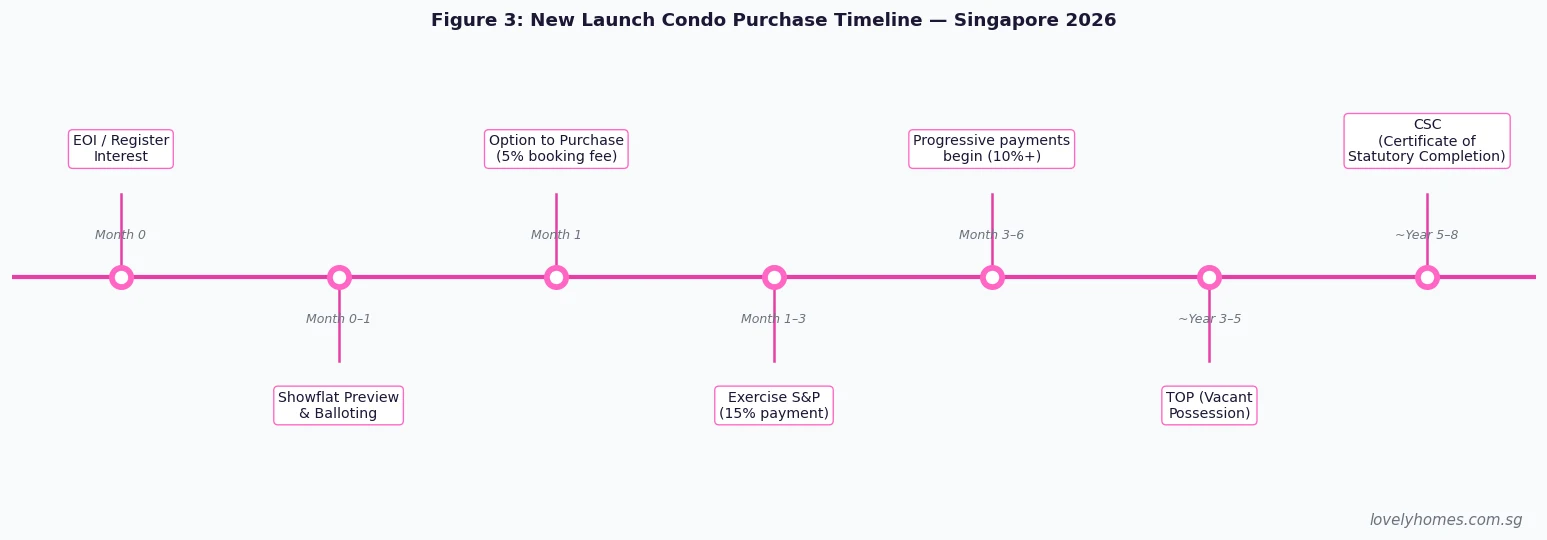

Step 1: Registering Interest and the Showflat Preview

Before a formal launch, developers typically invite potential buyers to register their interest (EOI). Registering is non-binding — it gives you priority access to a showflat preview before the public, and ensures you receive the developer’s price list and floor plan release in advance. At the preview, you view the show units (which may be furnished or bare-shell mock-ups) and indicate interest in specific units and stacks.

For highly subscribed projects, the developer may hold a ballot: if more buyers are interested in a particular unit type than units available, a computerised draw selects the order of purchase. Being balloted does not guarantee you receive your preferred unit — you may be offered an alternative or invited to return if units remain after the first round.

Under URA rules, developers must release at least 35% of available units in the first sale tranche. Price lists must be published at least 24 hours before the launch, and developers may not collect more than 5% as a booking fee (OTP fee) before exercising the Sale & Purchase Agreement.

Step 2: The Option to Purchase (OTP) and Booking Fee

When you decide to proceed, you sign an Option to Purchase (OTP) and pay the booking fee — typically 5% of the purchase price. In Singapore, developer OTPs for new launches have a standard form prescribed by the Controller of Housing. You then have a fixed period — typically 3 weeks — to exercise the OTP by signing the Sales & Purchase Agreement (S&P) and paying the next instalment.

The booking fee is non-refundable if you decide not to exercise. However, if you exercise the OTP and subsequently fail to complete (e.g., cannot obtain financing), the forfeiture is typically 25% of the purchase price — an extremely significant sum. This underscores why financing pre-approval matters before you sign any OTP.

Step 3: Stamp Duties — BSD and ABSD

Singapore imposes Buyer’s Stamp Duty (BSD) on all property purchases, calculated on the higher of the purchase price or market value:

- 1% on the first S$180,000

- 2% on the next S$180,000

- 3% on the next S$640,000

- 4% on the next S$500,000

- 5% on the next S$1,500,000

- 6% on any excess above S$3,000,000

For most new launch condos — commonly priced between S$1.5M and S$3M in 2026 — BSD is typically S$39,600 to S$69,600.

Additional Buyer’s Stamp Duty (ABSD) applies on top of BSD for buyers beyond their first property, PRs, and all foreigners:

Married couples where one spouse is an SC and the other is a PR buying their first property together are eligible for ABSD remission — the ABSD paid is refunded after holding the property for 5 years, provided they sell the other property (if any) within 6 months of TOP or purchase, and the purchased property remains their primary residence.

Step 4: Financing — LTV, TDSR and MSR (if applicable)

Private condo financing in Singapore is governed by the Total Debt Servicing Ratio (TDSR) framework: total monthly debt obligations (all loans) must not exceed 55% of gross monthly income. The Loan-to-Value (LTV) limit for private properties depends on your loan count:

| Loan Count | Max LTV (bank loan) | Min Cash Down | Min CPF/Cash Down |

|---|---|---|---|

| 1st housing loan | 75% | 5% cash | 20% cash/CPF |

| 2nd housing loan | 45% | 25% cash | 30% cash/CPF |

| 3rd and beyond | 35% | 25% cash | 40% cash/CPF |

Note: these are the LTV limits for standard bank loans. HDB loans are not available for private properties. There is no MSR cap for private condos — only TDSR applies.

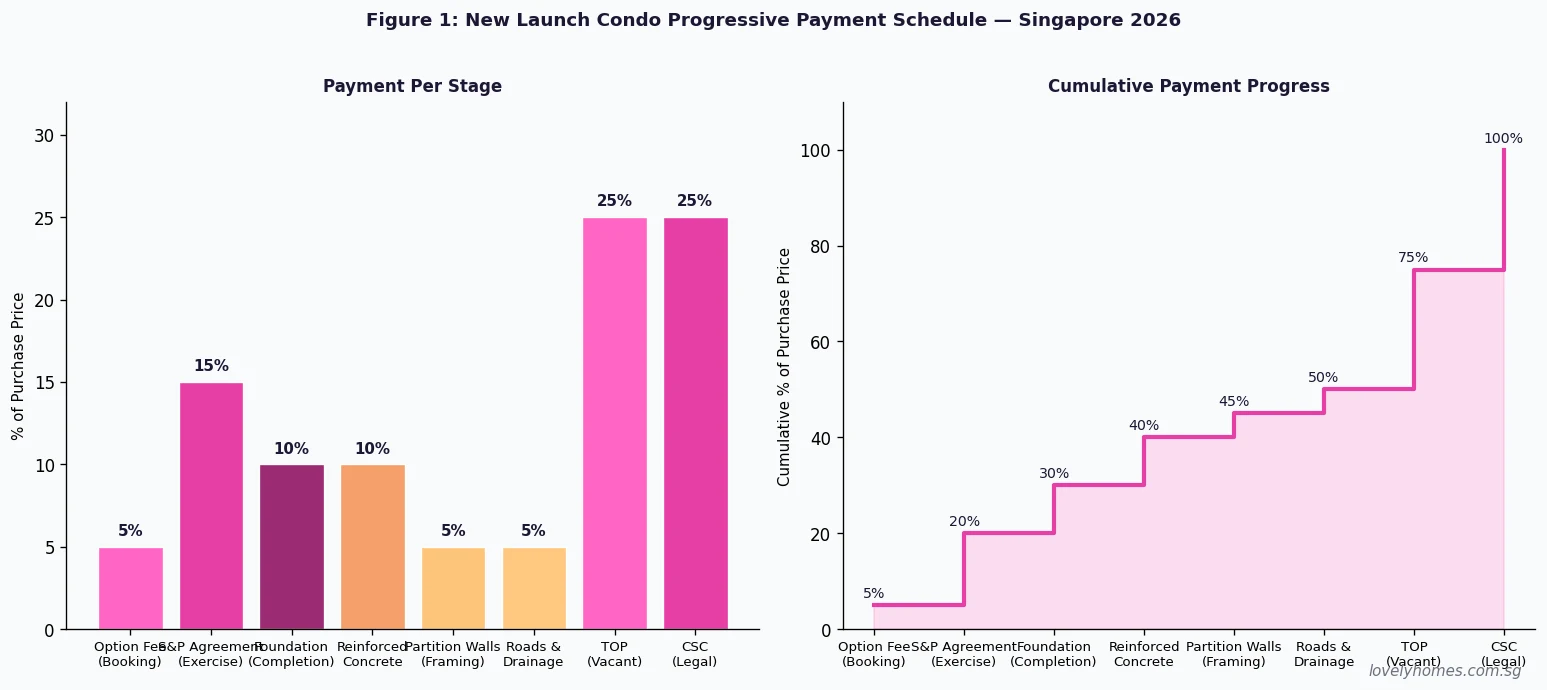

Step 5: The Progressive Payment Scheme (PPS)

Unlike resale purchases (where you pay the full price in one transaction), new launch condos use the Progressive Payment Scheme. You pay in stages as the building reaches construction milestones. Each payment is called a “progress payment” and corresponds to a defined stage of construction certified by an architect.

Each progress payment triggers a corresponding drawdown of your bank loan. This is why you need a bank’s Letter of Offer (LO) before or shortly after exercising the S&P — the bank needs to be ready to disburse as each stage is reached. You pay interest on the disbursed loan amount as construction progresses, typically at the bank’s prevailing rate (SORA-based in 2026).

Step 6: Deferred Payment Scheme (DPS) — Is It Still Available?

The Deferred Payment Scheme (DPS) allows buyers to defer up to 80% of the purchase price until TOP or CSC, rather than paying progressively. However, since 2007, the Monetary Authority of Singapore (MAS) has effectively restricted DPS on standard residential properties. Most developers no longer offer DPS as a standard option; where it appears, it is typically for high-end projects (luxury segment) under specific conditions. The PPS is the default for virtually all new launch condos launched from 2026 onwards.

Step 7: TOP, Possession and Renovation

When the building receives its Temporary Occupation Permit (TOP) from the Building and Construction Authority (BCA), you can take vacant possession of your unit. At this stage, you pay the remaining progress payments: typically 25% on TOP (vacant possession) and a final 5% on CSC (Certificate of Statutory Completion).

A new launch unit at TOP is delivered as a bare shell — bare concrete floors, unpainted walls, basic sanitary fittings (unless the developer has included a renovation package). You will need to engage contractors for flooring, painting, kitchen and bathroom fittings, carpentry, air-conditioning, and more. Budget conservatively: renovation for a 2-bedroom (around 700–850 sqft) typically ranges from S$50,000 to S$100,000 in Singapore’s 2026 market; for larger units, S$120,000 or more is common. Include this in your total acquisition cost model.

Seller’s Stamp Duty (SSD): The 5-Year Lock-In

Singapore’s SSD was introduced in 2011 to curb short-term speculation. For residential properties purchased on or after 11 March 2017, SSD applies if you sell within 3 years of purchase:

- Sold within 1st year: 12%

- Sold within 2nd year: 8%

- Sold within 3rd year: 4%

- Sold after 3rd year: 0%

SSD is calculated on the higher of the sale price or market value. For new launch condos, this effectively means you cannot profitably flip a unit until at least 3 years after OTP. Since most new launches take 3–5 years to reach TOP, many buyers hold well past the SSD window regardless.

New Launch vs Resale: Quick Comparison

| Factor | New Launch | Resale Condo |

|---|---|---|

| Payment structure | Progressive (PPS) | Full payment on completion |

| Condition at handover | Bare shell | Existing fittings |

| Waiting time | 3–5 years to TOP | Immediate |

| Price | Usually at or above market premium | Negotiated market price |

| HDB grant eligibility | Not applicable (private) | Not applicable (private) |

| CPF usage | Yes (Ordinary Account) | Yes |

| Renovation budget needed | Yes (significant) | Usually lower (existing fit-out) |

| ABSD | Same rates as resale | Same rates as new launch |

Worked Example: The Teo Family

Mr and Mrs Teo are Singapore Citizens, both aged 34. They own a 4-room HDB flat in Bishan (fully paid). They wish to buy a new launch 2-bedroom condo in Jurong East at S$1,600,000. This will be their second property.

BSD: 1%×S$180K + 2%×S$180K + 3%×S$640K + 4%×S$600K = S$1,800 + S$3,600 + S$19,200 + S$24,000 = S$48,600

ABSD: 20% on second property (SC) = S$320,000 — due within 2 weeks of OTP.

Booking fee (5%): S$80,000 cash.

S&P exercise (15%): S$240,000 (cash/CPF). Total upfront = S$320,000 cash + S$368,600 stamp duties.

Bank loan (75% LTV on first loan — but this is their 2nd property): LTV = 45%, so bank loan max = S$720,000. Total cash + CPF must cover S$880,000 (55%) — plus S$368,600 stamp duties already paid. Renovation budget: S$70,000.

Total funds required: approximately S$1,320,000 in cash and CPF before loan proceeds. The Teos should model whether their HDB flat sale proceeds (if they plan to sell) are sufficient, or whether they can service a bridging gap.

Common Pitfalls to Avoid

- Not stress-testing TDSR at higher SORA: SORA-based mortgage rates have fluctuated. Ensure you can service your loan even if rates rise 1–2 percentage points above today’s levels.

- Underestimating renovation costs: Get a proper quote before committing; budget overruns on renovation are extremely common in Singapore.

- Assuming your preferred unit is available: Popular stacks (high floor, pool-facing, corner units) are typically balloted first. Be prepared to accept alternatives.

- Overlooking maintenance fees: New launch condos with extensive facilities (pool, gym, concierge) can carry maintenance fees of S$400–S$800/mth or more for larger units.

- Not checking the developer’s track record: Review the developer’s past completions — quality, adherence to timeline, and handover defects. Singapore’s REDAS and the Controller of Housing maintain records of licensed developers.

Frequently Asked Questions

Can I use CPF to pay for a new launch condo?

Yes. You may use your CPF Ordinary Account (OA) balance to pay for the S&P downpayment and progressive payments (except the booking fee — the initial 5% OTP fee must be in cash). You can also use CPF OA for BSD and legal fees. However, you cannot use CPF for ABSD payments — ABSD must be paid in cash. CPF usage on private property is subject to the valuation limit and the withdrawal limit (typically capped at the assessed value of the property); once the OA balance used for the property reaches the assessed valuation, you must pay subsequent instalments from your bank loan or cash.

What happens if the developer delays TOP?

Developers in Singapore are legally required to obtain TOP by the Delivery Possession Date (DPD) stated in the S&P Agreement. If they fail to do so, they must pay Liquidated Damages (LD) to buyers — typically calculated at 8% per annum on the progressive payments already made, pro-rated for each day of delay. LD is automatically due; you do not need to take legal action to claim it. For extended delays (beyond 6 months), the Controller of Housing may also take action against the developer’s licence.

Can I back out after signing the S&P Agreement?

You can withdraw after exercising the S&P, but the consequences are severe. Under the standard Housing Developers (Show Units) Rules, the developer can forfeit up to 25% of the purchase price as liquidated damages. You also lose your 5% booking fee. In practice, most buyers do not withdraw after exercising — the financial penalty makes it uneconomical except in extreme circumstances (e.g., inability to obtain financing).

What is the difference between TOP and CSC?

TOP (Temporary Occupation Permit) is issued by BCA when the building meets minimum safety, fire safety, and occupancy standards. You can move in and begin renovation after TOP. CSC (Certificate of Statutory Completion) is issued when the development fully meets all planning and statutory requirements — typically 1–3 years after TOP. The final 5% payment is due on CSC. Legal completion (transfer of title) typically happens at or shortly after CSC. Until CSC, the developer retains the final 5% and your strata title has not yet been issued.

Do I need a lawyer for a new launch condo purchase?

Yes. All property transactions in Singapore require a licensed Singapore solicitor to act for you on conveyancing. For new launches, the developer typically has a panel of law firms; you may use one of these or appoint your own solicitor. Your solicitor will review the S&P Agreement, verify that the developer’s housing licence is valid, liaise with CPF Board (if you are using CPF), liaise with your bank (if you have a mortgage), and register the transfer of title at the Singapore Land Authority (SLA). Legal fees for a new launch typically range from S$2,500 to S$5,000 for standard condos.

Related Articles

- ABSD Singapore 2026: Complete Guide to Additional Buyer’s Stamp Duty

- Singapore HDB CPF Housing Grants Guide 2026: EHG, Family Grant and PHG

- Singapore First-Timer Home Buyer Complete Guide 2026

- CPF Property Usage Guide 2026: OA Withdrawal and Accrued Interest

- Singapore Executive Condo Guide 2026: EC Eligibility, Resale Levy and CPF Rules

- HDB BTO vs Resale Flat 2026: Complete Comparison Guide

Disclaimer

This article is for general information only and does not constitute financial, legal, or property advice. Stamp duty rates, LTV limits, TDSR rules, and grant schemes are subject to change by the Singapore government. Always verify current rules with the Inland Revenue Authority of Singapore (IRAS), Urban Redevelopment Authority (URA), and Monetary Authority of Singapore (MAS) before making any purchase decision. Consult a licensed conveyancing solicitor and a licensed financial adviser for advice specific to your circumstances.