Singapore HDB Downpayment Guide 2026: How Much Cash Do You Need?

Buying an HDB flat in Singapore involves one of the most consequential financial decisions most households will ever make — yet the mechanics of the downpayment are frequently misunderstood. How much cash do you actually need on completion day? How much can come from your CPF? Does it matter whether you take an HDB loan or a bank loan? The answers to these questions determine not just how much you need to have saved, but also how quickly you can buy and how you should be managing your CPF Ordinary Account in the months before applying.

This guide walks through the 2026 HDB downpayment rules in full — the minimum sums, the loan-to-value limits, the CPF rules, and the practical implications of choosing between an HDB concessionary loan and a bank mortgage. All figures reflect the rules administered by the Housing & Development Board (HDB) and the Monetary Authority of Singapore (MAS) as at July 2026.

Quick Answer — HDB Downpayment Singapore 2026

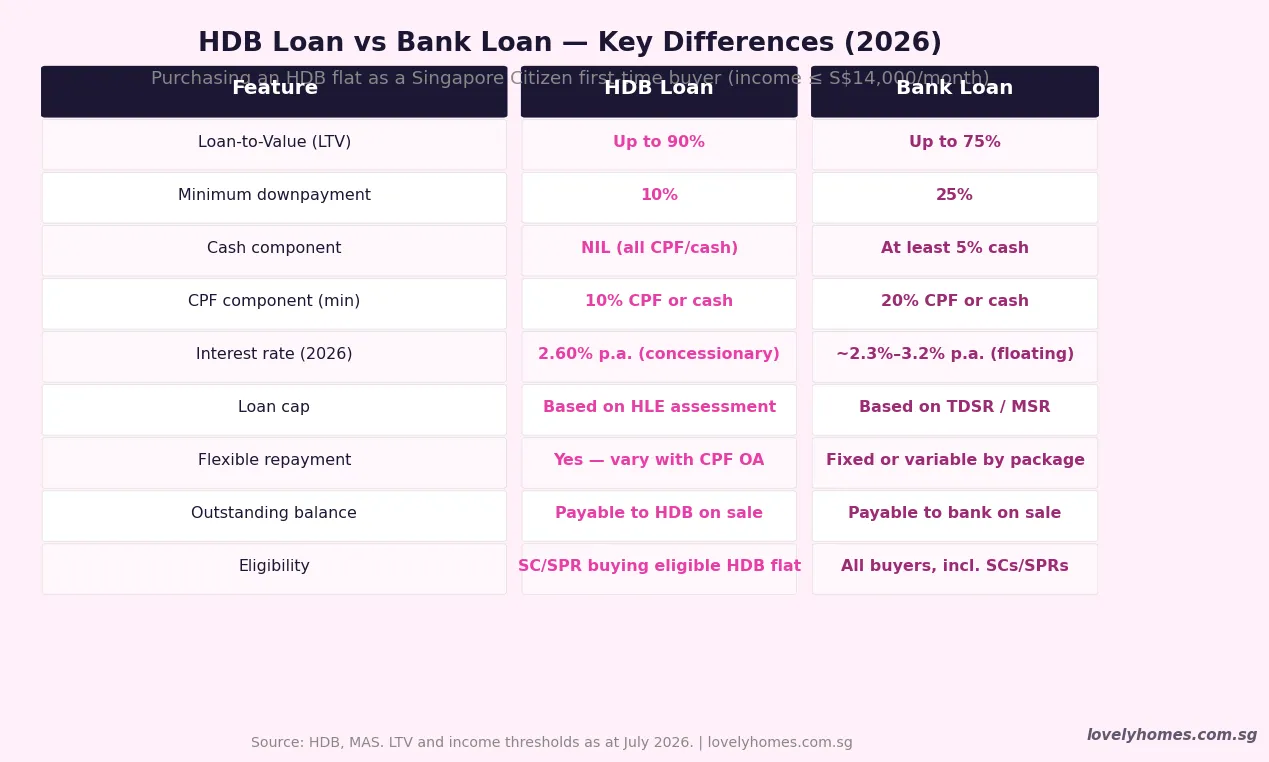

- With an HDB loan (LTV 90%): minimum downpayment is 10%, payable entirely from CPF OA or cash — no mandatory cash component.

- With a bank loan (LTV 75%): minimum downpayment is 25%, of which at least 5% must be in cash; the remaining 20% can come from CPF OA or cash.

- If you have an existing HDB loan or any other outstanding home loan, your LTV drops further — down to 45%–55% depending on the loan count.

- HDB loan interest is currently 2.60% per annum (0.10% above the CPF OA rate). Bank rates in 2026 range roughly 2.30%–3.20% depending on the package.

- CPF can be used to pay both the downpayment and the monthly instalments, subject to the CPF accrued interest rule on eventual sale.

- The HDB Flat Eligibility (HFE) letter replaces the former HDB Loan Eligibility (HLE) letter and the in-principle approval (IPA); you must obtain it before applying for any flat, BTO or resale.

- For resale flats, you must also obtain a valuation from a licensed appraiser; your CPF and loan quantum are pegged to the lower of price or valuation.

- The Minimum Occupation Period (MOP) for Standard flats is 5 years from keys; selling within MOP incurs claw-back of CPF-funded downpayment and grants.

Understanding Loan-to-Value (LTV) for HDB Flats

The Loan-to-Value ratio is the maximum proportion of a property’s purchase price (or valuation, whichever is lower) that a lender is permitted to finance through a loan. For HDB flats in Singapore, the LTV is governed by different rules depending on whether you borrow from HDB directly or from a commercial bank — and whether you have any existing outstanding home loans.

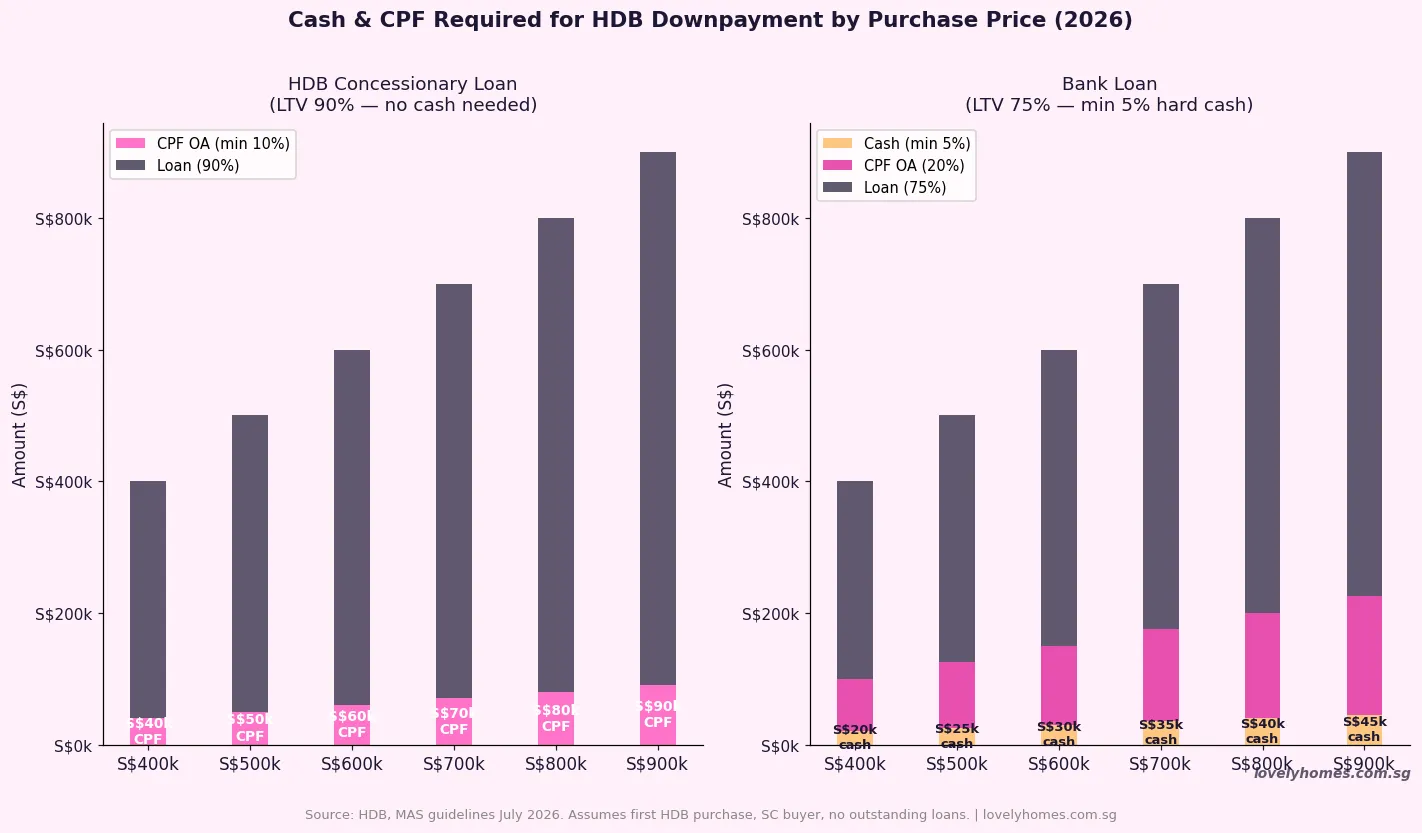

The HDB concessionary loan — available only to Singapore Citizens and, in some cases, PRs buying eligible HDB flats — offers a maximum LTV of 90%. This means you need to fund only 10% of the purchase price from your own resources. The bank loan, regulated by MAS, has a maximum LTV of 75% for a first housing loan. This means a 25% downpayment is required, with a hard cash floor of 5%.

Critically, these LTV limits apply to the lower of purchase price or valuation. If you are buying a resale HDB flat at S$650,000 but the HDB-appointed valuer values it at S$620,000, your loan will be calculated on S$620,000 — and the S$30,000 difference (called Cash Over Valuation, or COV) must be paid entirely in cash.

How Much Cash Do You Actually Need?

This is the question most first-time buyers ask first — and the answer depends entirely on your loan choice.

HDB Loan — Minimum Cash: S$0

If you qualify for and take an HDB concessionary loan, the 10% downpayment can come entirely from your CPF Ordinary Account (OA). There is no mandatory cash component. This is the key practical advantage of the HDB loan for buyers who may not have significant liquid savings but have been building CPF through employment.

However, “no mandatory cash” does not mean no cash at all. You will still need to pay BSD (Buyer’s Stamp Duty) — typically S$4,800–S$11,800 for a resale HDB flat priced below S$500,000 — and legal fees of around S$1,500–S$2,500. Both of these can be paid from CPF OA. If there is a Cash Over Valuation component, that must be paid in cash.

Bank Loan — Minimum Cash: 5% of Purchase Price

With a bank mortgage, MAS rules require that at least 5% of the purchase price be paid in cash — not CPF. For a S$600,000 flat, that is S$30,000 in cash. The remaining 20% of the downpayment (S$120,000) can come from CPF OA or cash. The cash floor exists because MAS wants borrowers to have genuine liquidity at stake, not just paper CPF balances.

In practice this means the bank loan path is only viable if you either have sufficient CPF OA savings to cover the 20% CPF component, or you have cash savings sufficient to cover more than the 5% minimum. Many first-time buyers who have not built up their CPF OA (for example, recent graduates or self-employed individuals with irregular CPF contributions) find the HDB loan more accessible for this reason.

CPF and the Downpayment — What You Need to Know

CPF Ordinary Account savings are the primary vehicle for funding an HDB flat downpayment in Singapore. As at July 2026, the CPF OA earns interest at 2.50% per annum (with an additional 1% on the first S$20,000 for members below 55). You can withdraw from your CPF OA to fund the downpayment on any eligible HDB property, subject to two key rules:

1. Valuation Limit: CPF can only be used up to the valuation of the property. If you paid COV above the valuation, that premium cannot be funded by CPF. It must come from cash.

2. Accrued Interest Obligation: All CPF used for property (including the downpayment) must be returned to your CPF account when you sell, together with accrued interest at 2.5% per annum compounded. This is sometimes called the “CPF accrued interest” and it can significantly reduce your net cash proceeds on eventual sale — particularly if you hold for many years. It is not a penalty, but it can feel like one if you have not accounted for it in your financial planning.

HDB Loan Eligibility — The HFE Letter

Since 9 May 2023, HDB replaced both the HDB Loan Eligibility (HLE) letter and the separate bank in-principle approval step with a single document: the HDB Flat Eligibility (HFE) letter. The HFE letter confirms three things simultaneously: (a) whether you are eligible to buy an HDB flat, (b) the CPF housing grants you qualify for, and (c) the HDB concessionary loan quantum you are eligible for.

You must have a valid HFE letter before applying for any BTO exercise or before submitting a resale application. The HFE letter is applied for through the HDB website using your Singpass. Assessment considers your household income, existing property holdings, outstanding loans, and citizenship status.

If you plan to take a bank loan instead, you will still need to obtain an HFE letter confirming your flat-buying eligibility, plus separately obtain an In-Principle Approval (IPA) from your chosen bank confirming the loan quantum they will offer. Most banks provide an IPA within two to three working days.

The Minimum Occupation Period and Your CPF

The Minimum Occupation Period (MOP) for Standard HDB flats — including the vast majority of BTO projects launched before 2024 — is five years from the date of physical possession of the keys. If you sell within the MOP, all CPF used for the purchase (downpayment, instalments) plus accrued interest must be refunded to your CPF OA, which can wipe out a significant portion of your sale proceeds. For Plus and Prime flats launched under the new classification framework, the MOP is 10 years.

This MOP interacts with your downpayment decision in a practical way: the more CPF you use for the downpayment, the higher your CPF accrued interest obligation grows with each passing year — meaning the longer you hold, the larger the CPF refund you owe. Some financially sophisticated buyers manage this by paying more cash upfront (even if not required to) in order to reduce their CPF drawdown and therefore their eventual CPF refund obligation.

Worked Example — 4-Room Resale Flat in Tampines, S$650,000

The Tan couple (both SCs) are buying a 4-room resale HDB flat in Tampines for S$650,000. HDB valuation: S$635,000. COV: S$15,000 (must be paid in cash). Combined income: S$7,800/month. They have S$130,000 in CPF OA combined and S$35,000 in savings.

Option A — HDB Concessionary Loan (LTV 90%)

Loan quantum: 90% × S$635,000 (valuation) = S$571,500

Downpayment (10%): S$63,500 — payable from CPF OA

COV (cash only): S$15,000

BSD on S$650,000: S$1,800 + S$3,600 + S$16,950 = S$12,750 (payable CPF or cash)

Legal fees: approximately S$2,000 (payable CPF)

Total cash needed on completion: S$15,000 (COV only, if BSD and legal paid from CPF)

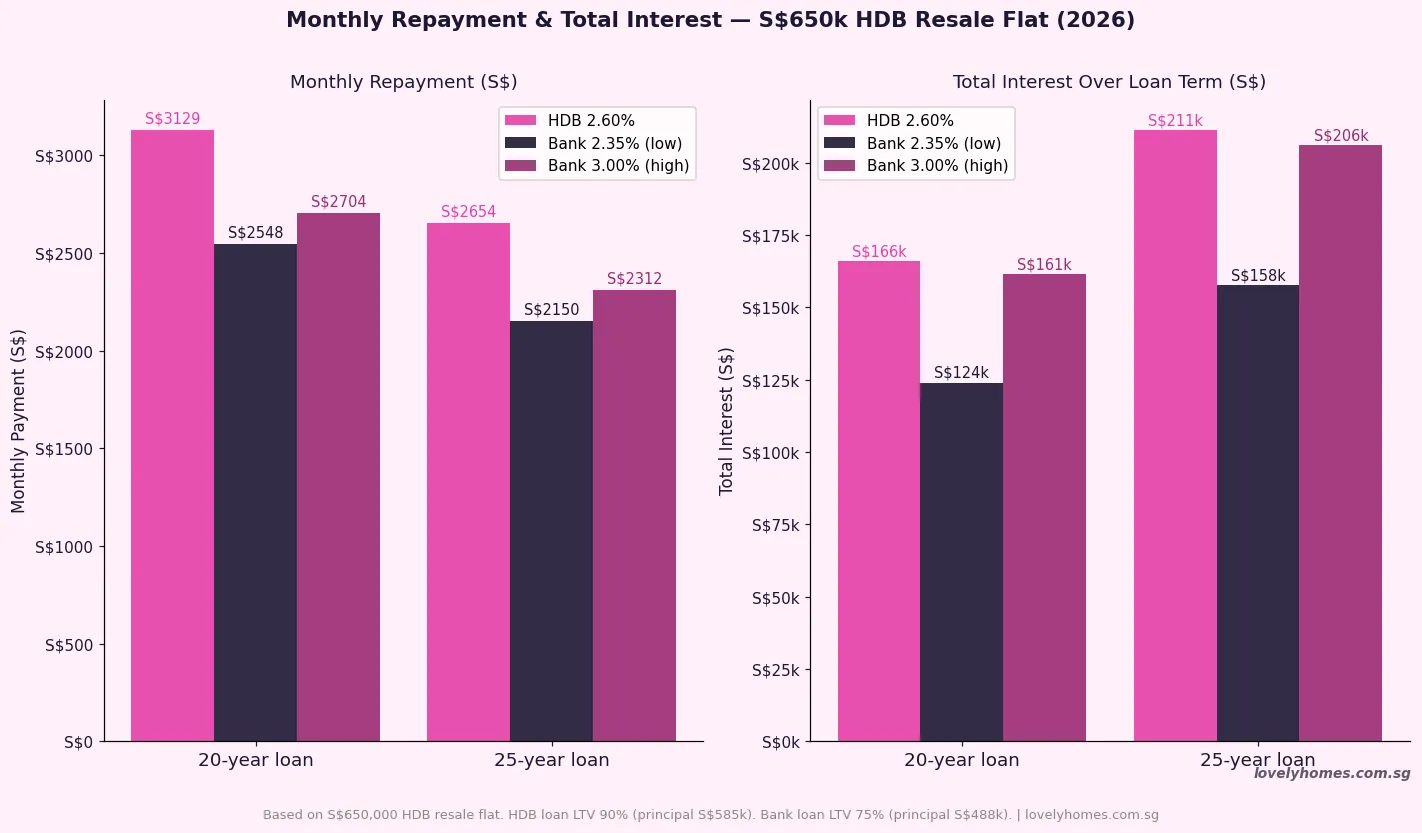

Monthly repayment at 2.60% over 25 years: approximately S$2,584

MSR check (30%): S$7,800 × 30% = S$2,340 — repayment S$2,584 exceeds MSR threshold, so loan tenor must be extended or CPF/cash prepayment considered, or loan quantum adjusted

Option B — Bank Loan (LTV 75%)

Loan quantum: 75% × S$635,000 = S$476,250

Downpayment (25%): S$158,750

Cash component (min 5% of S$650,000): S$32,500 cash

CPF component (balance): S$126,250 from CPF OA

COV: S$15,000 cash

BSD: S$12,750 (CPF or cash)

Total cash needed: S$32,500 + S$15,000 = S$47,500 minimum

Monthly repayment at 2.50% over 25 years: approximately S$2,138

MSR check: S$2,138 / S$7,800 = 27.4% — PASS (below 30%)

The Tan couple’s decision: Option A requires only S$15,000 cash but the monthly repayment slightly stresses the MSR limit. A 30-year loan tenor reduces the monthly payment to about S$2,280, which passes. Option B requires S$47,500 cash upfront — more than their savings buffer — but results in a lower monthly repayment. Given their CPF savings, Option B works if they are comfortable with a tighter cash position at completion. Most buyers in this situation choose Option A for its lower cash requirement.

HDB Loan or Bank Loan — What Matters for Your Decision

The choice between HDB and bank is not simply about interest rates. Several factors determine which is better for your specific situation. If you have limited cash savings and strong CPF, the HDB loan’s zero-cash-downpayment requirement is a decisive advantage. If you have substantial cash and want to reduce your total interest cost (and expect interest rates to remain low), the bank loan’s lower starting rate can be appealing — though the fixed-rate advantage over the HDB rate has narrowed significantly since 2022.

One important consideration in 2026 is that fixed-rate bank mortgage packages have come down from their 2023–2024 peaks, with the best promotional fixed-rate packages now available at around 2.20%–2.35% for the first two years. By contrast, the HDB loan rate of 2.60% has been stable and will remain at 0.10% above the CPF OA rate unless the Government changes the CPF OA rate — which it has not done since 2008. If you expect interest rates to fall further, floating-rate bank packages may outperform the HDB rate from 2027 onward. If you value certainty, the HDB rate’s long-term stability is valuable.

A third path — starting with an HDB loan, then refinancing to a bank loan after the MOP — is also possible. HDB permits borrowers to repay the HDB loan in full and switch to a bank loan at any time. There is no penalty for early repayment of the HDB concessionary loan, which gives buyers flexibility.

What Might Change — Downpayment Policy Outlook

The MAS Macroprudential Policy Review and HDB supply-demand management have been the primary levers for adjusting property accessibility rules. In 2022–2023, the Government adjusted LTV and MSR/TDSR parameters as part of the broader property cooling framework. As at July 2026, there is no official signal of any imminent change to the LTV, MSR, or downpayment rules for HDB flats. However, the upcoming release of the Full Q2 2026 HDB resale statistics (expected around 23 July 2026) will provide a clearer picture of whether the sequential price declines seen in Q1 and Q2 2026 prompt any policy review. A further softening of the resale market might create space for a modest easing of downpayment requirements — but this is speculative.

Summary — HDB Downpayment at a Glance, 2026

| Item | HDB Loan | Bank Loan |

|---|---|---|

| Max LTV | 90% | 75% |

| Minimum downpayment | 10% | 25% |

| Mandatory cash component | None | Min 5% |

| CPF OA usable | Yes — up to 10% | Yes — up to 20% |

| Interest rate (July 2026) | 2.60% p.a. | ~2.30%–3.20% p.a. |

| MSR cap (monthly repayment) | 30% of gross income | 30% of gross income |

| Eligibility letter required | HFE letter (via HDB) | HFE letter + bank IPA |

| Who can use | SC (some SPR) buying eligible HDB | All eligible buyers |

Frequently Asked Questions

Can I use my CPF Special Account (SA) for the HDB downpayment?

No. Only the CPF Ordinary Account (OA) can be used for property purchases, including the downpayment and monthly mortgage repayments. CPF Special Account (SA) and MediSave Account funds are not permitted for property payments. This is an important distinction — some buyers conflate their total CPF balance with what is available for property, but only the OA balance is accessible for this purpose.

What is Cash Over Valuation (COV) and how does it affect my downpayment?

COV is the amount you pay above the HDB-appointed valuation for a resale flat. For example, if you agree to pay S$680,000 for a flat valued at S$650,000, the COV is S$30,000. COV must always be paid entirely in cash — it cannot be funded by CPF or a bank loan. This is in addition to your regular downpayment and is one reason why buying a resale flat at a significant premium to valuation can demand more cash than buyers anticipate. In the current (mid-2026) market, COV has moderated from the peaks seen in 2022–2023, but still occurs frequently for popular mature-estate resale flats.

Does the MSR limit apply if my spouse is not employed?

Yes. The Mortgage Servicing Ratio (MSR) limit of 30% applies to the combined gross monthly income of all applicants on the HDB application. If your spouse is not employed, their income is counted as S$0, which means only your individual income is used to calculate the MSR threshold. This can significantly reduce the loan quantum you are eligible for, and may require you to extend the loan tenor to bring the monthly repayment within the 30% limit. Borrowers relying on a single income should calculate their maximum eligible loan quantum carefully before making an offer.

What happens if I switch from an HDB loan to a bank loan mid-mortgage?

You can refinance from an HDB concessionary loan to a bank loan at any time — HDB charges no early repayment penalty. However, once you switch to a bank loan, you cannot switch back to an HDB concessionary loan. This is a one-way door, so the decision deserves careful consideration. When refinancing, you will need to ensure the bank’s IPA covers the outstanding loan balance, and you should account for legal/administrative costs of refinancing (typically S$2,000–S$3,000 in conveyancing and valuation fees). Banks sometimes offer cashback promotions on refinancing that offset these costs.

Can CPF grants be used as part of the downpayment?

Yes. CPF housing grants (such as the Enhanced CPF Housing Grant, Family Grant, and Proximity Housing Grant for eligible resale flat buyers) are credited directly to your CPF OA and can be applied toward the downpayment and purchase price. This effectively reduces the CPF savings you need to have pre-existing in your account before the purchase. However, grants are credited only after the resale application is approved by HDB — they are not available to fund the initial Option exercise fee or the initial downpayment tranche. For BTO buyers, grants are applied at key collection. The maximum combined grant for an eligible first-timer SC couple buying a resale flat can reach S$190,000.

What if my CPF OA balance is not enough to cover the downpayment?

If your CPF OA balance falls short of the required downpayment, the shortfall must be made up in cash. For HDB loan buyers, the 10% downpayment can be a mix of CPF OA and cash — there is no restriction on using cash for this portion. For bank loan buyers, you must still ensure the 5% mandatory cash component is in cash, but any additional downpayment shortfall can also be funded by cash. If your combined CPF OA and cash are insufficient to cover the full downpayment, you may need to negotiate a lower purchase price, seek a higher grant, or delay your purchase until your CPF OA balance has grown sufficiently.

Related Articles

- Singapore HDB CPF Housing Grants Guide 2026: EHG, Family Grant, PHG

- Singapore HDB Minimum Occupation Period (MOP) 2026: Complete Guide

- Singapore HDB Ethnic Integration Policy (EIP) 2026

- Singapore Stamp Duty Calculator 2026: BSD and ABSD Explained

- Singapore Condo Buying Process 2026

- HDB BTO October 2026 Guide: All Projects and Prices

Disclaimer

This article is produced by LovelyHomes for general information purposes only and does not constitute financial, legal, or mortgage advice. HDB loan eligibility, CPF rules, LTV limits, and interest rates are subject to change by the Housing & Development Board, Monetary Authority of Singapore, and Central Provident Fund Board. Readers should verify all current rules and figures directly at hdb.gov.sg, cpf.gov.sg, and mas.gov.sg, and should obtain independent financial and mortgage advice before making any purchase decision.

Click anywhere to close